Respiratory Syncytial Virus (RSV) Diagnostic Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

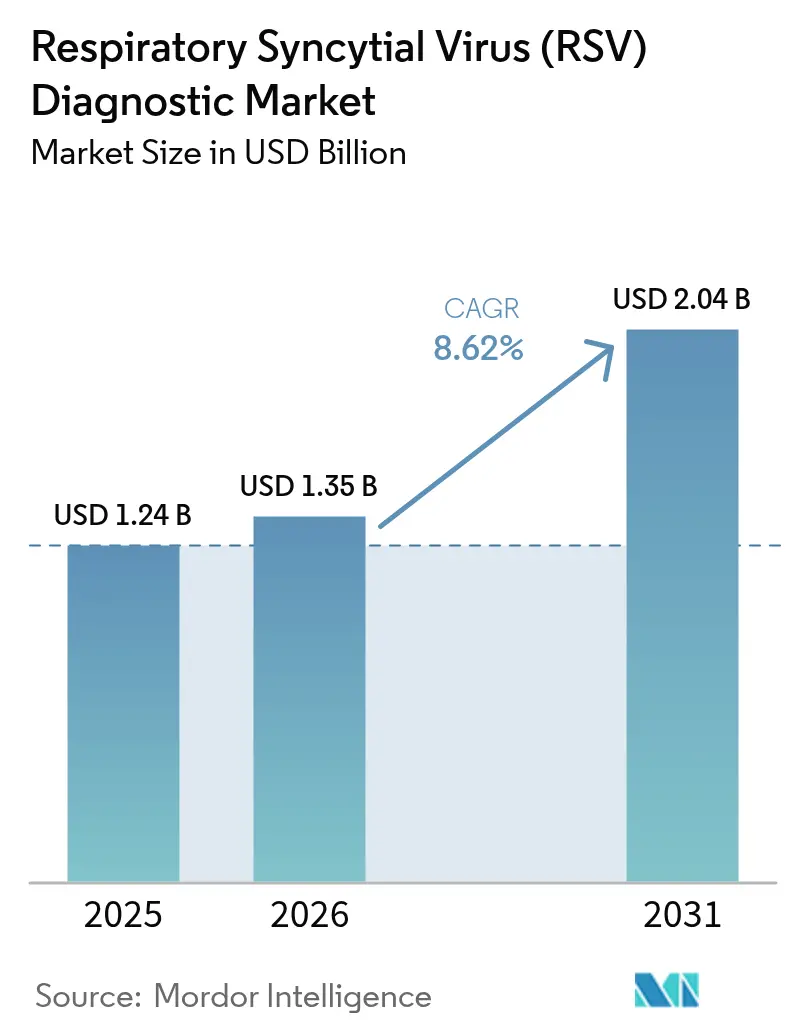

| Market Size (2026) | USD 1.35 Billion |

| Market Size (2031) | USD 2.04 Billion |

| Growth Rate (2026 - 2031) | 8.62% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Respiratory Syncytial Virus (RSV) Diagnostic Market Analysis by Mordor Intelligence

The Respiratory Syncytial Virus diagnostics market size is expected to grow from USD 1.24 billion in 2025 to USD 1.35 billion in 2026 and is forecast to reach USD 2.04 billion by 2031 at 8.62% CAGR over 2026-2031. This projected expansion reflects the rising adoption of molecular point-of-care platforms, stronger post-pandemic respiratory surveillance, and widening prenatal screening linked to newly approved maternal vaccines. Heightened R&D activity in RT-PCR and isothermal amplification is boosting test sensitivity, while rapid approvals of multiplex assays are shortening commercialisation cycles. Strategic bundling of RSV with influenza and SARS-CoV-2 in “respiratory panels” is lifting average selling prices and expanding use beyond paediatric wards into adult and geriatric settings. Asia-Pacific is set to outpace all other regions at an 11.75% CAGR as governments scale intensive-care capacity and reimburse outpatient testing, allowing the Respiratory Syncytial Virus diagnostics market to penetrate previously underserved rural districts. Competitive rivalry is intensifying around integrated sample-to-answer cartridges and AI-driven analytics that turn raw cycle threshold values into actionable treatment cues.

Key Report Takeaways

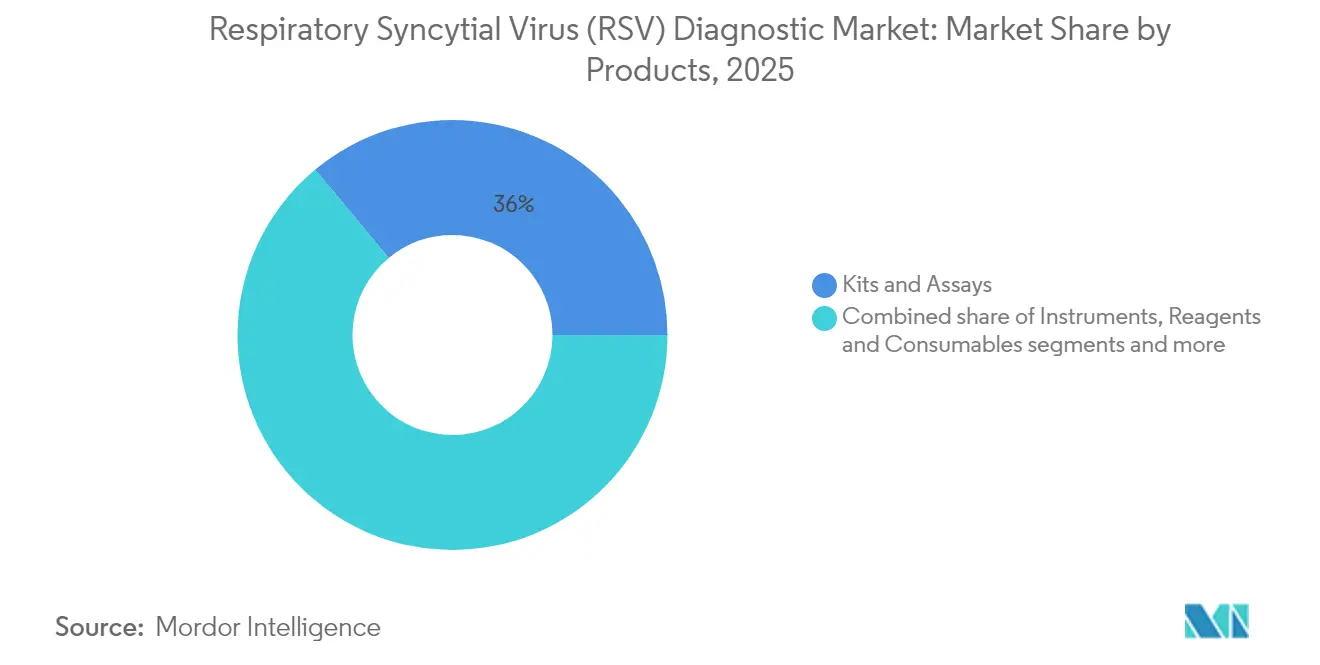

- By product category, kits & assays led with 36.02% of Respiratory Syncytial Virus diagnostics market share in 2025; software & analytics is projected to expand at a 9.87% CAGR through 2031.

- By method, rapid antigen detection accounted for a 27.05% share of the Respiratory Syncytial Virus diagnostics market size in 2025, while molecular diagnostics is advancing at a 10.22% CAGR to 2031.

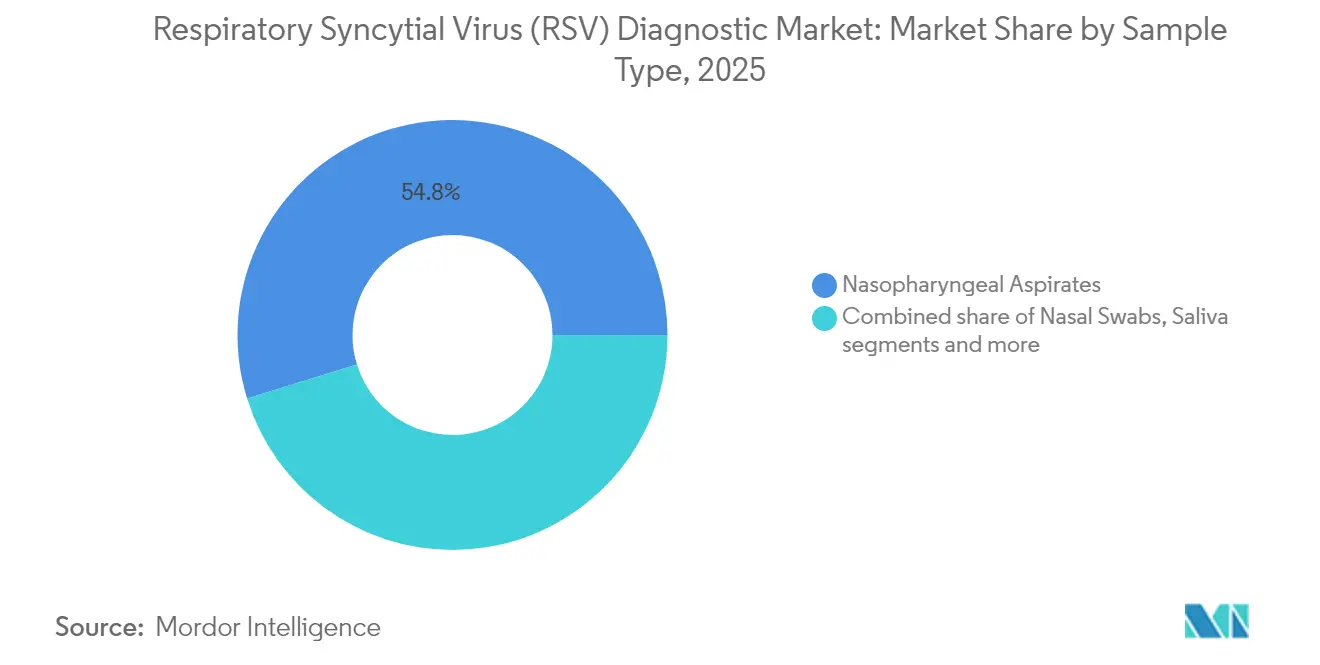

- By sample type, nasopharyngeal aspirates captured 54.78% of Respiratory Syncytial Virus diagnostics market size in 2025; saliva testing is forecast to grow at a 9.38% CAGR over the same horizon.

- By end user, hospitals & clinics held 42.71% of Respiratory Syncytial Virus diagnostics market share in 2025, whereas home-care tests are rising fastest at an 10.86% CAGR.

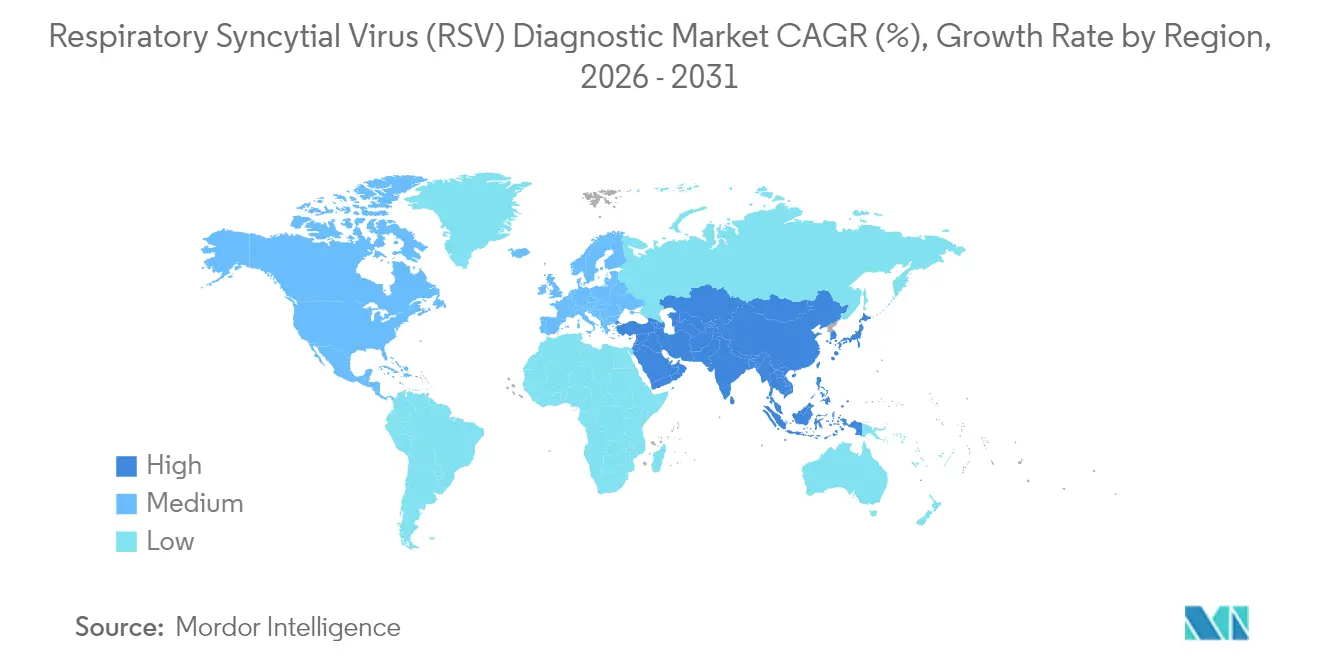

- By geography, North America dominated with 39.22% revenue share in 2025; Asia-Pacific shows the highest projected CAGR of 11.21% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Respiratory Syncytial Virus (RSV) Diagnostic Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timelin |

|---|---|---|---|

| Surging Adoption of Point-of-Care RSV Molecular Panels | ~+2.1% | North America, Europe, with spillover to urban centers in APAC | Short term (≤ 2 yrs) |

| Post-COVID 'Tripledemic' Seasons Driving Co-Testing in Urgent-Care Chains | ~+1.8% | Global, with highest impact in North America and Europe | Medium term (~ 3-4 yrs) |

| FDA Fast-Track Maternal RSV Vaccines Catalyzing Prenatal Screening Uptake | ~+1.5% | North America, with gradual expansion to Europe and developed APAC | Medium term (~ 3-4 yrs) |

| Increasing Approvals for Syncytial Virus Diagnostic Products | ~+2.3% | Global, led by North America and Europe | Short term (≤ 2 yrs) |

| Rising Burden of Syncytial Virus Infections | ~+1.4% | Global, with significant impact in pediatric populations across all regions | Long term (≥ 5 yrs) |

| Source: Mordor Intelligence | |||

Surging Adoption of Point-of-Care RSV Molecular Panels

- Field studies show that cartridge-based molecular systems deliver results in 0.2 – 3.8 hours versus up to 36 hours for batch PCR, trimming unnecessary antibiotic use and isolation bed days. Community clinics now embed these single-use panels into triage protocols, while large urgent-care chains adopt multiplex cartridges that identify RSV, influenza, and COVID-19 from one swab. Accelerated clinical decisions are raising physician confidence and fuelling repeat procurement, pushing the Respiratory Syncytial Virus diagnostics market deeper into primary-care channels.

Rising Burden of Syncytial Virus Infections

RSV accounts for up to 80 000 US child hospitalisations annually and triggers 100 000-150 000 admissions among adults aged 60+[1]Source: Centers for Disease Control and Prevention, “Weekly RSV-NET Reports,” cdc.gov . Globally, WHO attributes roughly 3.6 million paediatric hospitalisations and 100 000 deaths per year to RSV who.int. The sheer caseload is reinforcing payer support for early detection, sustaining long-run growth in the Respiratory Syncytial Virus diagnostics market.

FDA Fast-Track Maternal RSV Vaccines Catalysing Prenatal Screening Uptake

The licensing of maternal vaccines such as Pfizer’s Abrysvo is spurring obstetric clinics to add RSV screens to routine third-trimester panels. Surveillance data indicate a 43% drop in infant hospitalisations in birth cohorts whose mothers received vaccination plus monoclonal prophylaxis. Laboratories are therefore generating dual revenue streams: baseline prenatal screening and post-vaccination effectiveness audits. This synergy accelerates the Respiratory Syncytial Virus diagnostics market among women’s-health providers.

Increasing Approvals for Syncytial Virus Diagnostic Products

Regulators cleared over half-a-dozen RSV assays between 2024 and 2025, including Roche’s 20-minute cobas liat test and SEKISUI’s CLIA-waived OSOM strip . These approvals shorten procurement cycles for hospitals, catalyse distributor partnerships, and widen test menus inside existing analysers, placing further upward pressure on Respiratory Syncytial Virus diagnostics market volumes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High False-Negative Rates of First-Gen Lateral-Flow Antigen Tests | ~-1.2% | Global, with higher impact in resource-limited settings | Short term (≤ 2 yrs) |

| Stringent Regulations and Low Detection Limits of Immunoassays | ~-0.9% | North America and Europe primarily | Medium term (~ 3-4 yrs) |

| Source: Mordor Intelligence | |||

High False-Negative Rates of First-Generation Lateral-Flow Antigen Tests

Meta-analysis of paediatric studies shows that legacy antigen strips exhibit markedly lower sensitivity than RT-PCR, raising risk of missed cases and misguided cohorting . Hospitals in resource-constrained regions that still rely on these strips may delay treatment or isolation, dampening clinician trust and temporarily tempering demand in segments of the Respiratory Syncytial Virus diagnostics market.

Stringent Regulations and Low Detection Limits of Immunoassays

The FDA’s performance thresholds for respiratory tests require high analytical sensitivity that traditional immunoassays struggle to meet. Achieving sub-attomole detection often demands complex antibody engineering, prolonging design-verification timelines and elevating costs. Smaller manufacturers may defer entry, slowing product refresh cycles in parts of North America and Europe and nudging buyers towards larger incumbents within the Respiratory Syncytial Virus diagnostics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Kits & Assays Retain Primacy, Software Analytics Scales Up

Kits & assays generated the largest revenue in 2025 as clinicians continue to favour single-use cartridges and ELISA plates validated across age groups. Their 36.02% share translates into USD 0.45 billion of Respiratory Syncytial Virus diagnostics market size, supported by recurrent reagent sales. Software and analytics, although contributing a smaller absolute sum, is expected to post the quickest gains. Cloud dashboards that convert cycle-threshold curves into predictive severity scores are showing 0.811 AUC-ROC in early trials, bolstering purchasing interest among tele-health operators. Instruments remain essential for laboratories processing pooled respiratory panels, while reagents and consumables drive annuity-style cash flows for OEMs.

Growing emphasis on data-rich reporting grants software packages a central role in stewardship programmes tracking antimicrobial usage. Integrated AI modules are forecast to raise laboratory productivity by automating result validation, a trend that will reinforce double-digit growth for this niche. Consequently, the Respiratory Syncytial Virus diagnostics market is shifting from pure consumables toward hybrid hardware-software ecosystems that amplify clinical insight.

By Method: Rapid Antigen Testing Dominates, Molecular Diagnostics Ascend

Rapid antigen detection accounted for 27.05% of Respiratory Syncytial Virus diagnostics market share in 2025, owing to affordability and CLIA-waived status. These strips are widely stocked in paediatric units and nursing homes, underpinning broad geographic reach. Molecular diagnostics, however, is on a sharper 10.22% growth curve, leveraging CRISPR-based readouts and extraction-free protocols that cut sample prep time by 60%. The Respiratory Syncytial Virus diagnostics market size attributable to molecular formats is projected to surpass USD 0.86 billion by 2031 as price per panel narrows relative to antigen tests.

Advances in digital microfluidics and nanopore sequencing are pushing limits of detection below 10 copies/ml, capturing low-viral-load cases in immunocompromised adults. Chromatographic immunoassays hold a steady position in reference labs that prefer batch throughput, while emerging nanobubble platforms offer early-stage promise for decentralised testing. Collectively, these innovations are recalibrating the method mix and elevating overall assay accuracy in the Respiratory Syncytial Virus diagnostics market.

By Sample Type: Nasopharyngeal Aspirates Prevail, Saliva Surges

Nasopharyngeal aspirates delivered 54.78% of Respiratory Syncytial Virus diagnostics market size in 2025 because of their consistently high viral load and physician familiarity. Yet multi-specimen trials reveal that reliance on swabs alone underestimates adult RSV incidence by up to 112% . Saliva collection is hence emerging as a patient-friendly alternative, growing at 9.38% CAGR as self-collection kits gain FDA clearance. Saliva’s 61.4% sensitivity in some head-to-head studies surpasses that of nasopharyngeal swabs, bolstering its appeal for mass-screening drives.

Nasal swabs keep a solid second place due to user comfort, while whole-blood/serum assays stay confined to research or epidemiological sero-surveys. As home-care testing accelerates, saliva’s non-invasive nature is expected to chip away at aspirate dominance, broadening sampling options across the Respiratory Syncytial Virus diagnostics market.

By End User: Hospitals Anchor Demand, Home-Care Adoption Accelerates

Hospitals and clinics accounted for 42.71% of Respiratory Syncytial Virus diagnostics market share in 2025, reflecting acute care of severe paediatric and elderly cases. Observational data show 5% of adults diagnosed in outpatient settings are admitted within 28 days, reinforcing hospital demand. Diagnostic reference laboratories leverage higher-throughput instruments and bundled service contracts to serve regional providers.

Home-care platforms, buoyed by FDA frameworks for OTC respiratory tests, are expected to log an 10.86% CAGR to 2031. Pharmacies and online retailers now distribute self-administered molecular kits that upload results to tele-health portals within 30 minutes. This shift decentralises testing and supports chronic-disease patients unable to travel, expanding the Respiratory Syncytial Virus diagnostics market reach. Urgent-care and retail clinics fill out the remainder, using syndromic panels to triage high-footfall flu seasons.

Geography Analysis

North America generated 39.22% of revenues in 2025, driven by widespread insurance coverage and robust RSV surveillance networks that feed hospital dashboards in near real time. Early uptake of maternal vaccination and monoclonal prophylaxis is further expanding routine newborn screening. Amid these dynamics, the Respiratory Syncytial Virus diagnostics market benefits from established distributors and laboratory automation that accelerates test throughput during winter virus peaks.

Europe maintains a strong second position. National winter-respiratory frameworks mandate RSV testing alongside influenza, lifting baseline volumes across public hospitals. Germany, France, and the United Kingdom continue to procure multiplex PCR systems for integrated respiratory surveillance. Eastern European countries are adopting pooled-sample algorithms to mitigate reagent costs, gradually enlarging regional scope for the Respiratory Syncytial Virus diagnostics market.

Asia-Pacific posts the fastest expansion at 11.21% CAGR. China, Japan, and Australia are scaling neonatal intensive-care beds and embedding RSV panels into provincial reimbursement lists. India’s private laboratories are equipping tier-2 city hubs with cartridge PCR, narrowing rural access gaps. Government pandemic funds redirected toward respiratory preparedness are catalysing public–private partnerships in Indonesia, Malaysia, and the Philippines. Collectively, these investments underpin durable growth for the Respiratory Syncytial Virus diagnostics market across the region. Middle East & Africa and South America, though smaller in absolute size, are witnessing rising public-sector tenders for rapid antigen kits as part of broader acute-respiratory disease initiatives, paving long-term expansion pathways.

Competitive Landscape

Global leadership rests with Abbott, Roche, and Thermo Fisher, whose integrated portfolios span antigen strips, cartridge PCR, and cloud-based middleware. Their combined footprint places supply hubs within 48-hour shipping distance of most tertiary hospitals, ensuring resilient reagent supply during peak seasons. Roche’s cobas Respiratory flex test showcases TAGS technology that collapses 12 virus targets into a single 20-minute run, locking in instrument loyalty and deepening the Respiratory Syncytial Virus diagnostics market moat around multiplex innovation.

Second-tier challengers such as Seegene and QuantuMDx employ open-architecture systems that accept rival reagent brands, undercutting total cost of ownership for mid-sized community hospitals. CRISPR pioneers Sherlock Biosciences and Mammoth Biosciences are advancing room-temperature lyophilised reagents compatible with battery-powered readers, eyeing doorstep diagnostics for immunocompromised seniors. These entrants intensify competition on portability and turnaround speed, thereby broadening use cases within the Respiratory Syncytial Virus diagnostics market.

Strategic moves include co-marketing agreements between instrument makers and tele-health platforms to bundle test kits with virtual consultation packages. Midsized IVD firms are partnering with AI analytics start-ups to turn raw fluorescence traces into prognostic risk scores, seeking differentiation beyond assay accuracy. Across the board, intellectual-property filings for isothermal chemistries and nanopore readouts rose more than 20% year on year in 2024, signalling persistent innovation push across the Respiratory Syncytial Virus diagnostics market.

Respiratory Syncytial Virus (RSV) Diagnostic Industry Leaders

bioMerieux SA

Becton, Dickinson and Company

F. Hoffmann-La Roche Ltd

ThermoFisher Scientific Inc.

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: CMS mandated electronic RSV reporting from long-term-care facilities, boosting data-driven purchasing of rapid panels

- May 2025: SEKISUI Diagnostics launched the 15-minute CLIA-waived OSOM RSV test

Global Respiratory Syncytial Virus (RSV) Diagnostic Market Report Scope

Respiratory syncytial virus (RSV) is a virus that causes respiratory infections such as bronchiolitis and pneumonia. The symptoms of the disease usually include runny nose, sneezing, coughing, and fever.

The respiratory syncytial virus (RSV) diagnostic market is segmented by product (kits and reagents, instruments, and other products), method (molecular diagnostics, rapid antigen detection tests, immunoassays, flow cytometry, and chromatography), end-user (hospitals and clinics, clinical laboratories, and other end-users), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally.

The report offers the value (in USD) for the above-mentioned segments.

| Kits & Assays |

| Instruments |

| Reagents & Consumables |

| Software & Analytics |

| Molecular Diagnostics (RT-PCR, CRISPR, Isothermal NAAT) |

| Rapid Antigen Detection (Immunochromatographic/Lateral Flow) |

| Chromatographic Immunoassays (Enzyme-based) |

| Others |

| Nasal Swabs |

| Nasopharyngeal Aspirates |

| Saliva |

| Whole Blood/Serum |

| Hospitals & Clinics |

| Diagnostic Reference Laboratories |

| Home-Care |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Kits & Assays | |

| Instruments | ||

| Reagents & Consumables | ||

| Software & Analytics | ||

| By Method | Molecular Diagnostics (RT-PCR, CRISPR, Isothermal NAAT) | |

| Rapid Antigen Detection (Immunochromatographic/Lateral Flow) | ||

| Chromatographic Immunoassays (Enzyme-based) | ||

| Others | ||

| By Sample Type | Nasal Swabs | |

| Nasopharyngeal Aspirates | ||

| Saliva | ||

| Whole Blood/Serum | ||

| By End User | Hospitals & Clinics | |

| Diagnostic Reference Laboratories | ||

| Home-Care | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the Respiratory Syncytial Virus diagnostics market?

The market stands at USD 1.35 billion in 2026 and is projected to grow to USD 2.04 billion by 2031.

Which product category generates the highest revenue?

Kits & assays account for 36.02% of revenues, maintaining primacy across hospital and outpatient settings.

Why is Asia-Pacific the fastest-growing region?

Rising healthcare expenditure, expanded neonatal intensive-care capacity, and broader reimbursement for molecular tests are propelling an 11.21% CAGR in the region.

How are maternal vaccines influencing RSV diagnostics?

Prenatal RSV screening volumes are rising because obstetric practices monitor vaccine uptake and effectiveness, creating new testing demand.

What technologies are shaping next-generation RSV testing?

Isothermal NAAT, CRISPR-based detection, and AI-driven analytics are driving faster turnaround, higher sensitivity, and predictive decision support across care settings.

Page last updated on: