Arbovirus Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

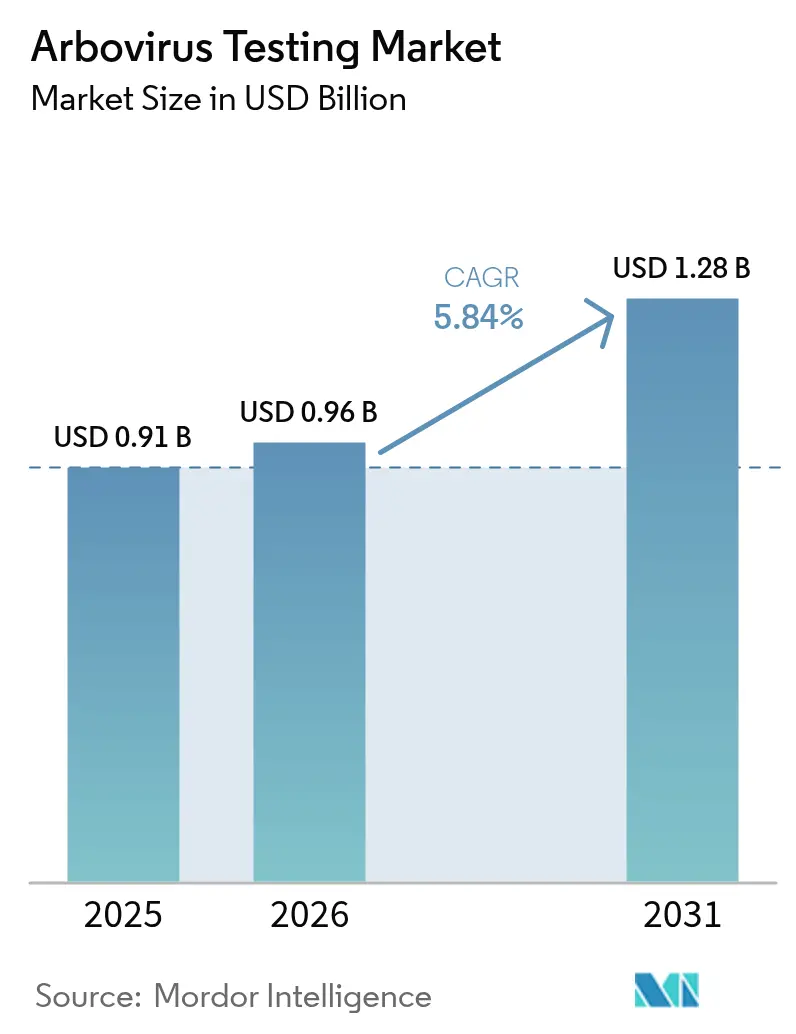

| Market Size (2026) | USD 0.96 Billion |

| Market Size (2031) | USD 1.28 Billion |

| Growth Rate (2026 - 2031) | 5.84% CAGR |

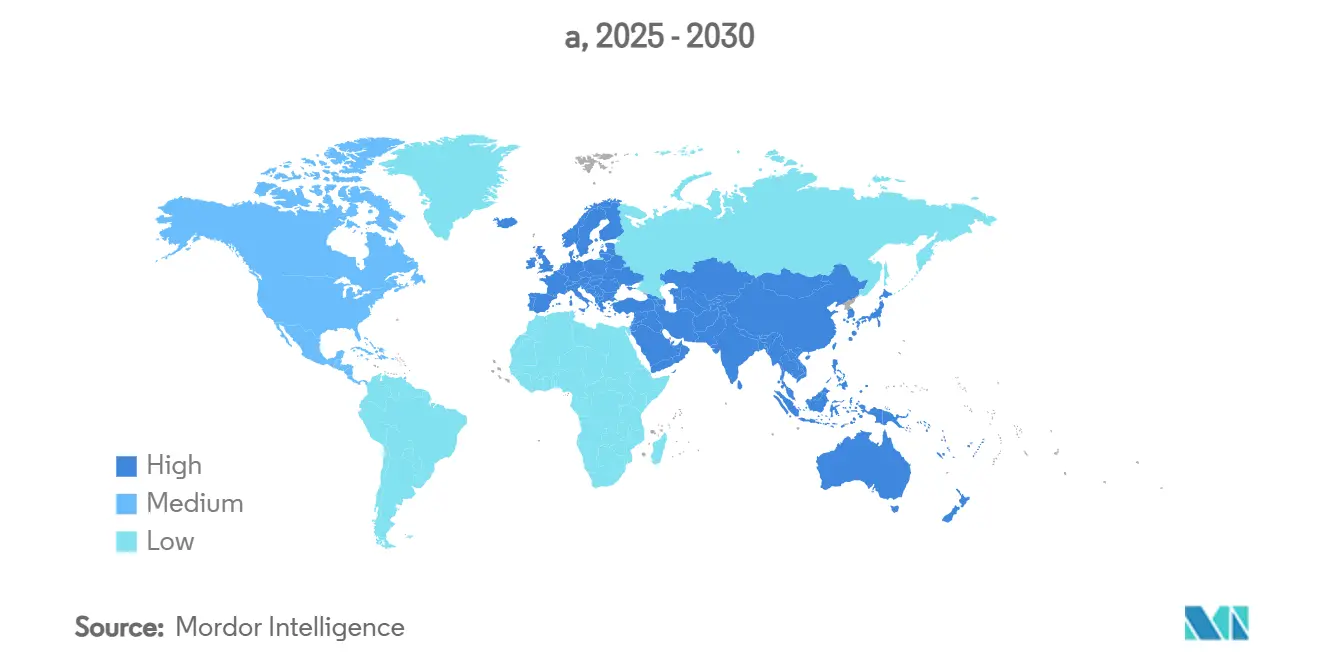

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

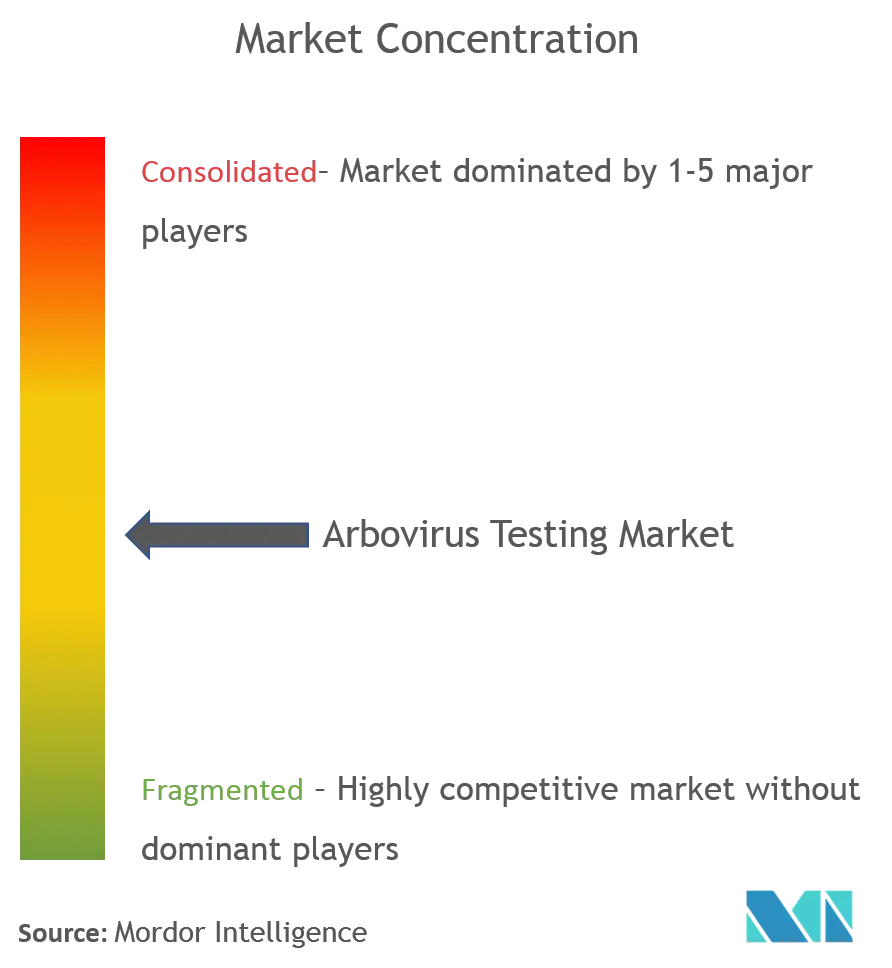

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Arbovirus Testing Market Analysis by Mordor Intelligence

The global arbovirus testing market size in 2026 is estimated at USD 0.96 billion, growing from 2025 value of USD 0.91 billion with 2031 projections showing USD 1.28 billion, growing at 5.84% CAGR over 2026-2031. Escalating dengue, Zika, and chikungunya outbreaks, in tandem with climate-driven vector expansion, are lifting demand for rapid, decentralised diagnostics across endemic and newly affected regions. Government budgets are shifting toward infectious-disease preparedness, catalysing procurement of next-generation ELISA, RT-PCR, and isothermal amplification platforms that shorten time-to-result in field conditions. Technological breakthroughs—CRISPR-assisted multiplex RT-PCR, AI-enhanced ELISA readouts, and extraction-free workflows—are improving accuracy while cutting consumable costs, making advanced molecular tools viable for low-resource settings. Competitive intensity centres on technology rather than price; platform synergies and integrated data solutions remain the core levers for share gains.

Key Report Takeaways

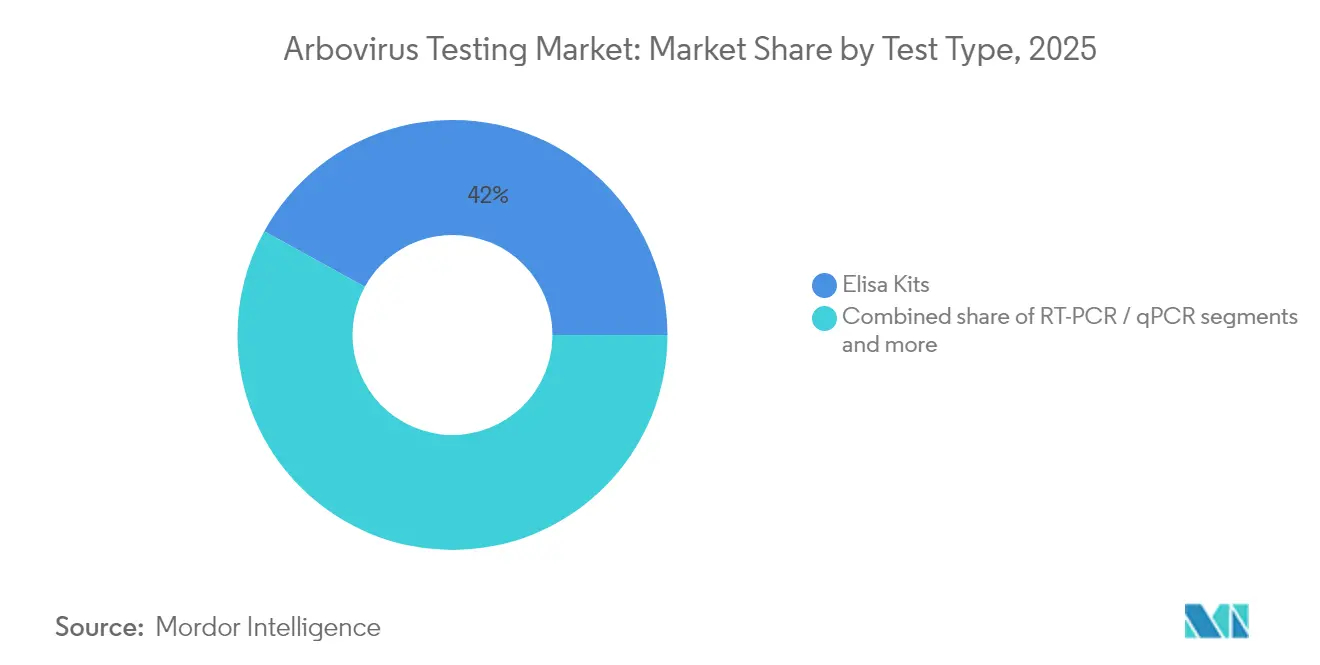

- By test type, ELISA kits captured 41.98% of the arbovirus testing market share in 2025; isothermal amplification platforms are projected to expand at a 6.03% CAGR through 2031.

- By end user, hospitals and clinics accounted for 38.15% of the arbovirus testing market size in 2025, while diagnostic laboratories are forecast to grow fastest at a 6.47% CAGR to 2031.

- By geography, North America commanded 35.85% revenue share of the arbovirus testing market size in 2025; Asia-Pacific is anticipated to log the highest 7.42% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Arbovirus Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating global outbreaks of dengue, Zika & chikungunya | +1.8% | Global, with highest impact in APAC and Latin America | Short term (≤ 2 years) |

| Technological advances in ELISA & RT-PCR platforms | +1.2% | Global, with early adoption in North America and Europe | Medium term (2-4 years) |

| Rapid-test adoption across LMIC primary-care settings | +1.0% | APAC, Africa, and Latin America | Medium term (2-4 years) |

| Government-funded vector-surveillance programs (genomics-enabled) | +0.8% | North America, Europe, and select APAC countries | Long term (≥ 4 years) |

| Multiplex isothermal amplification for field diagnostics | +0.6% | Global, with focus on endemic regions | Medium term (2-4 years) |

| Climate-linked procurement surges for outbreak preparedness kits | +0.4% | Global, with emphasis on tropical and subtropical regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Global Outbreaks of Dengue, Zika & Chikungunya

Record dengue notifications climbed to 13.7 million cases and 8,100 deaths across the Americas in 2024, a 260% leap over 2023 levels, pushing health-care systems toward molecular assays that enable serotype-specific management. Serological limitations during poly-virus circulation have prompted laboratories to upgrade to multiplex RT-PCR tools capable of distinguishing up to 32 arboviruses per run. Climate-related vector migration has driven local transmission in 15 previously unaffected countries, forcing non-endemic markets to stockpile diagnostic kits for front-line screening00298-9/fulltext). Novel reassortant Oropouche strains have also emerged, spurring demand for broad-spectrum detection panels. Economic modelling shows dengue now costs USD 4.1 billion annually, making early detection programs financially imperative.

Technological Advances in ELISA & RT-PCR Platforms

Next-generation ELISA readers use AI to cut indeterminate rates, lifting diagnostic accuracy to 99.6% for dengue serotype differentiation. Synthetic-biology-defined primers and CRISPR guard bands allow single-tube RT-PCR to concurrently detect 32 arboviruses without cross-reactivity penalties. Machine-learning analytics reduce false positives by 22% via amplification-curve pattern recognition. Extraction-free workflows shorten turnaround from four hours to under 65 minutes, a benefit proven during 2024 field pilots. Automation has freed skilled staff for confirmatory tasks, bolstering surge capacity during seasonal peaks.

Rapid-Test Adoption Across LMIC Primary-Care Settings

Isothermal platforms slashed deployment costs by 65% versus legacy PCR during 2024 roll-outs in 42 countries. LAMP-based devices posted 96.1% accuracy against reference labs, enabling same-day care in district clinics. FIND estimates a 4.2 million-test addressable demand at level-2 facilities, signalling a sizeable growth runway. Decentralised testing reduced health-system costs 52% by cutting patient transfers and preventing severe cases. mHealth connectivity now streams anonymised results to surveillance dashboards, strengthening outbreak intelligence while protecting privacy through encryption.

Government-Funded Vector-Surveillance Programs (Genomics-Enabled)

US GEIS scaled real-time sequencing to 28 countries in 2024, allowing rapid variant tracking and informing countermeasure allocation. Nanopore devices achieved unbiased strain typing from mosquito pools in under 3.5 hours, delivering near-instant epidemiological insight. Wastewater-based surveillance flags asymptomatic transmission earlier than clinical reporting, an essential capability given 85% of dengue infections are clinically silent. ECDC’s Enhanced Arbovirus Surveillance Network harmonised protocols across 27 EU states, unlocking joint tenders for high-throughput sequencers worth EUR 105 million in 2024. Economic models show every surveillance dollar avoids USD 24–28 in outbreak expenditure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cross-reactivity complicating regulatory approvals | -0.9% | Global, with highest impact in regions with multiple co-circulating flaviviruses | Medium term (2-4 years) |

| Stringent validation requirements & long approval cycles | -0.7% | Primarily North America and Europe | Long term (≥ 4 years) |

| Scarcity of pathogen-positive reference materials | -0.5% | Global, with particular impact on emerging market manufacturers | Medium term (2-4 years) |

| Post-COVID budget diversion away from arbovirus diagnostics | -0.4% | Global, with varying regional impact based on healthcare funding models | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cross-Reactivity Complicating Regulatory Approvals

Antigenic overlap among flaviviruses forces assay makers to validate against 18-virus panels, extending average approval timelines to 32 months in 2024. Multiplex assays risk performance compromise if any target shows cross-talk, prompting regulators to request geographically diverse clinical datasets that inflate trial budgets. PRNT remains the gold standard but is impractical for routine labs due to seven-day incubation, leaving a validation gap for rapid formats. Fifteen new arboviral variants identified in 2024 required additional verification cycles, resetting launch calendars. This barrier advantages large incumbents with deeper pockets and seasoned regulatory teams.

Post-COVID Budget Diversion Away from Arbovirus Diagnostics

Pandemic-era investments continue to prioritise respiratory surveillance, cutting vector-borne disease budgets by up to 40% in some LMICs during 202401234-5/fulltext). Capital previously earmarked for mosquito control and diagnostics was redirected to maintain SARS-CoV-2 PCR capacity, delaying arboviral kit procurement by eight to 12 months. International funding channels mirrored the shift; grants for dengue control fell 35% versus pre-COVID baseline. Skilled entomologists reassigned to COVID programmes have yet to return, leaving human-resource gaps in vector surveillance teams. The paradox is particularly acute in LMICs where rising case loads coincide with shrinking budgets, complicating national elimination strategies.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Isothermal Amplification Gains Momentum

ELISA maintained the largest foothold with 41.98% of arbovirus testing market share in 2025, underscoring its entrenched role in population-level screening. The segment continues to benefit from low per-test costs and simple instrumentation, yet growing demand for rapid, decentralised decisions is catalysing a shift toward isothermal technologies. Isothermal platforms are forecast to register a 6.03% CAGR and are already live in more than 650 Asia-Pacific primary centres, offering 70% cheaper operations than conventional PCR without sacrificing sensitivity.

Rapid antigen devices remain the smallest slice but have achieved 99.1% specificity for dengue NS1, improving early-phase case detection. Hybrid cartridge designs now merge immunoassay capture with isothermal amplification, blurring historical boundaries and threatening ELISA primacy. CRISPR-guided detection paired with recombinase polymerase amplification is moving through eight clinical trials and could reconfigure the arbovirus testing market once commercialised.

By End User: Diagnostic Laboratories Drive Innovation

Hospitals and clinics delivered 38.15% of 2025 revenue owing to immediate care pathways, but diagnostic laboratories are poised for 6.47% CAGR as outbreak volumes reward high-throughput hubs capable of processing surges exceeding 10,000 samples per day. Centralised labs achieved 99.2% proficiency in 2024 external quality assessments compared with 91.3% for decentralised sites, reflecting deeper assay expertise and robust QC systems.

Investment in AI-assisted analytics is automating result interpretation, trimming false positives by 28% and freeing scientists for confirmatory work. Multiplex demand exploded 189% in 2024 as clinicians sought one-run differential diagnoses where dengue, chikungunya, and Zika co-circulate. Research institutes, though smaller in spend, pipeline >185 experimental assays, ensuring a steady supply of cutting-edge formats that feed commercial portfolios.

Geography Analysis

North America retained a 35.85% revenue lead in 2025 thanks to CDC-backed lab-capacity grants and FDA guidance that shortens review cycles for emerging-pathogen assays. Aedes aegypti has established breeding in 18 US states, up from 15 in 2023, extending the diagnostic catchment and driving new municipal procurements. Canada and Mexico co-fund cross-border incident platforms under the USD 145 million North American Health Security Partnership, harmonising reagent demand across the bloc.

Asia-Pacific will post the steepest trajectory at 7.42% CAGR through 2031 as urbanisation and warming climates expand mosquito habitats. India’s National Vector-Borne Disease Control Programme dedicated USD 580 million to diagnostic infrastructure in 2024, while China advanced USD 4.1 billion in infectious-disease testing funds, 18% earmarked for arboviruses. ASEAN states invested USD 820 million to align with WHO IHR standards, and venture financing in regional med-tech exceeded USD 3.6 billion. Vector-competence studies warn that 14 more countries could sustain dengue transmission by 2030, underscoring the region’s diagnostic urgency.

Europe shows stable growth, propelled by travel medicine and autochthonous clusters in France, Italy, Spain, and Croatia. The EU’s Enhanced Arbovirus Surveillance Network pooled EUR 105 million for unified diagnostics in 2024, simplifying market entry for kit makers. Southern and Central regions now document established Aedes albopictus populations, widening routine-testing geography. EMA regulatory harmonisation continues to reduce multi-country approval costs, providing a predictable arena for innovation roll-outs.

Competitive Landscape

The arbovirus testing market is moderately concentrated: the top five providers—Abbott, Roche, Thermo Fisher Scientific, Cepheid, and bioMérieux—controlled roughly majority of global revenue in 2024. Platform integration remains the competitive fulcrum; bundled instruments, reagents, and analytics lock-in customers and discourage price wars. Abbott’s ID NOW Dengue Plus, cleared in December 2024, and Roche’s cobas Liat tri-plex assay, launched February 2025, underscore the pivot to near-patient molecular accuracy.

Technology differentiation drives M&A and venture flows toward isothermal and CRISPR assets. FDA reclassification of acute-febrile-illness devices in December 2024 created a fast lane for multiplex approvals, enticing start-ups with disruptive miniaturisation to challenge incumbents. White-space persists for battery-operated sequencers and reagents tailored to novel viruses such as Oropouche, Mayaro, and Jamestown Canyon, pathogens currently underserved by commercial menus.

Thermo Fisher’s USD 180 million reagent capacity expansion (November 2024) targets emerging-market roll-outs where distribution bottlenecks often cap revenue potential. Cepheid ramped Xpert system deployment for humanitarian response scenarios, demonstrating portability during climate-related disasters. BioMérieux’s VIDAS Dengue Trio integrates antigen and antibody panels into 30-minute formats, illustrating the hybridisation trend.

Arbovirus Testing Industry Leaders

Agilent Technologies, Inc.

Thermo Fisher Scientific

NovaTec Immundiagnostica GmbH

Euroimmun AG

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: FDA issued streamlined guidance for emerging-pathogen IVD approval, easing arbovirus test entry

- November 2023: FDA approved IXCHIQ, the first US chikungunya vaccine, creating new pre- and post-vaccination testing demand

Global Arbovirus Testing Market Report Scope

Arboviruses (Arthropod-borne viruses) are a unique, diverse, and fascinating group of viruses because they cycle between a wide variety of vertebrate hosts and arthropod species. Examples of the arboviral infectious diseases include Dengue, Chikungunya, St. Louis encephalitis, Yellow fever, California encephalitis, Eastern Equine Encephalitis, Powassan, West Nile, and Zika.

| ELISA / MAC-ELISA |

| RT-PCR / qPCR |

| Isothermal |

| Rapid Antigen |

| Others |

| Hospitals & Clinics |

| Diagnostic Laboratories |

| Research & Academic Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Test Type (Value) | ELISA / MAC-ELISA | |

| RT-PCR / qPCR | ||

| Isothermal | ||

| Rapid Antigen | ||

| Others | ||

| By End User (Value) | Hospitals & Clinics | |

| Diagnostic Laboratories | ||

| Research & Academic Institutes | ||

| By Geography (Value) | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the arbovirus testing market?

The arbovirus testing market size stood at USD 0.96 billion in 2026 and is projected to reach USD 1.28 billion by 2031.

Which region grows fastest in arbovirus diagnostics?

Asia-Pacific is forecast to post the highest 7.42% CAGR through 2031, propelled by large-scale government investments and expanding disease burden.

Which test type is gaining the most momentum?

Isothermal amplification platforms are projected to exhibit the quickest 6.03% CAGR because they deliver molecular-level sensitivity without complex cyclers.

Why are diagnostic laboratories outpacing hospitals in growth?

Laboratories offer high-throughput capacity, superior quality control, and AI-assisted analytics, driving a forecast 6.47% CAGR to 2031.

Page last updated on: