Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

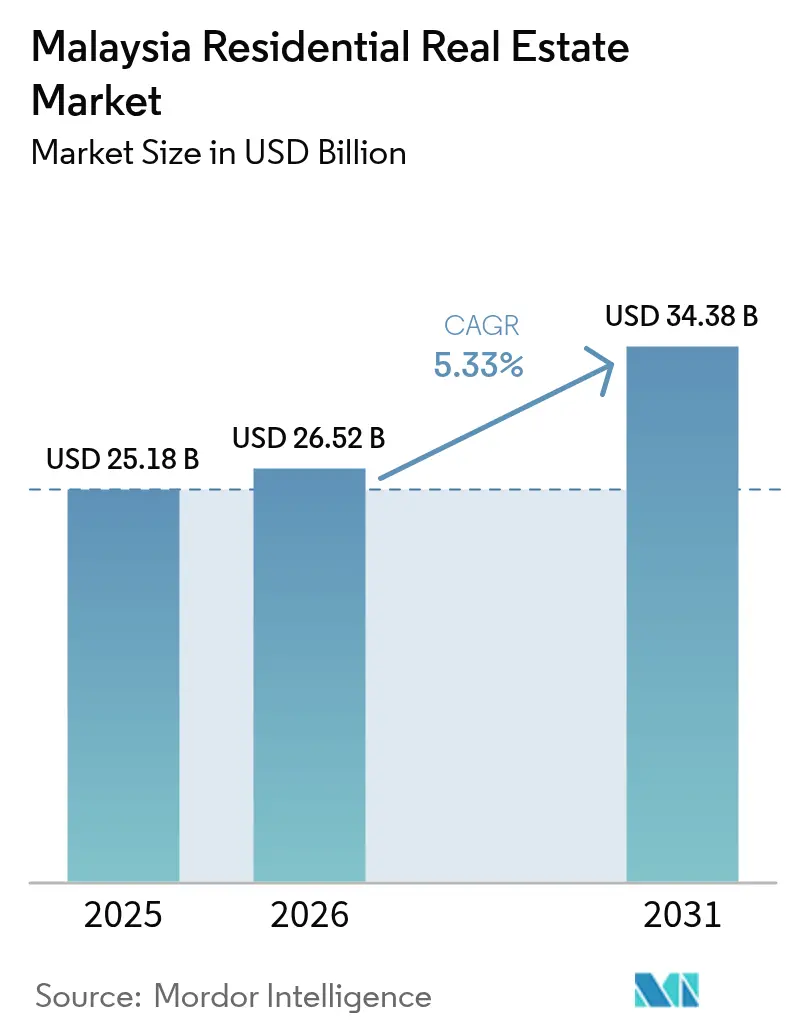

| Base Year Market Size (2025) | USD 25.18 Billion |

| Market Size (2026) | USD 26.52 Billion |

| Market Size (2031) | USD 34.38 Billion |

| Growth Rate (2026 - 2031) | 5.33% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Residential Real Estate Market Analysis by Mordor Intelligence

The Malaysia residential real estate market size is expected to grow from USD 25.18 billion in 2025 to USD 26.52 billion in 2026 and is forecast to reach USD 34.38 billion by 2031 at 5.33% CAGR over 2026-2031. Continuous MRT rollouts, the Johor Bahru–Singapore RTS Link, and a raft of budget-backed housing schemes are widening viable commuting zones and re-rating locations once deemed peripheral. A steady influx of international buyers, especially under the revised Malaysia My Second Home (MM2H) program adds depth to the demand pool even as local middle-class households gravitate to mid-income condominiums laden with lifestyle amenities. Meanwhile, construction-cost volatility and intermittent tweaks to foreign-ownership rules act as brakes, raising execution risk for developers and informing cautious portfolio strategies. Investor sentiment remains broadly constructive because the Malaysia residential real estate market continues to offer resilient yields amid moderating policy rates and a strengthening rental culture.

Key Report Takeaways

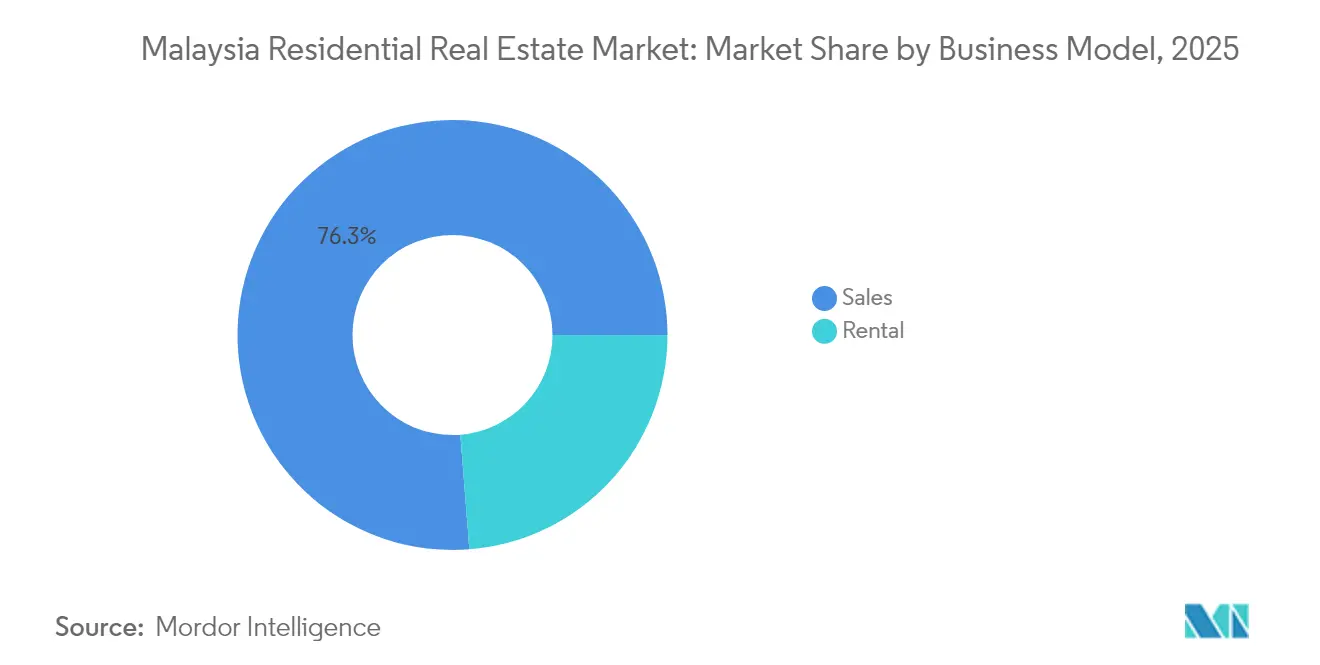

- By business model, ownership-driven sales dominated with a 76.25% revenue share in 2025; the rental segment is advancing at a 5.67% CAGR through 2031.

- By property type, apartments and condominiums held 70.55% of the Malaysia residential real estate market share in 2025, while villas and landed houses are projected to expand at a 6.23% CAGR through 2031.

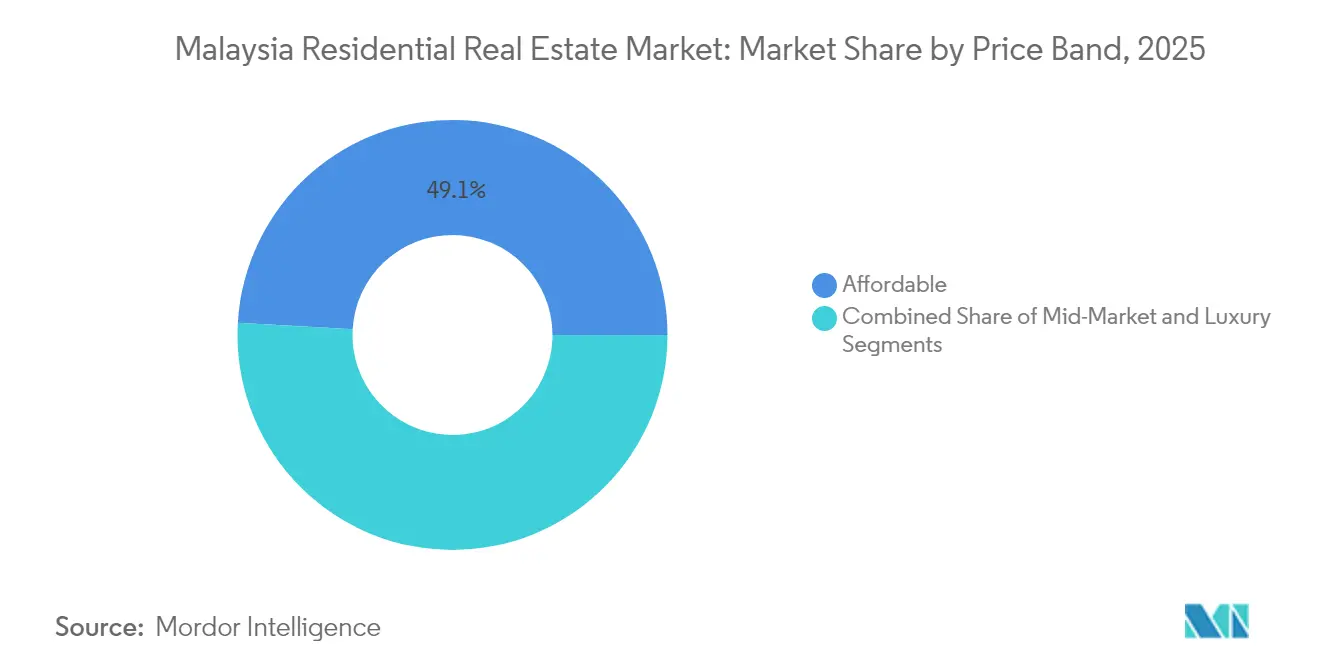

- By price band, affordable housing commanded 49.10% of the Malaysia residential real estate market size in 2025; the luxury tier is forecast to grow at a 6.44% CAGR to 2031.

- By mode of sale, the primary market accounted for 61.75% of the Malaysia residential real estate market size in 2025 and is progressing at a 6.18% CAGR until 2031.

- By key cities, Kuala Lumpur captured 48.60% of Malaysia residential real estate market share in 2025, while Johor Bahru leads growth at a 6.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization in Kuala Lumpur, Johor Bahru, and Penang | +1.2% | Kuala Lumpur, Johor Bahru, Penang | Medium term (2-4 years) |

| Growing middle class demanding mid-income condos and apartments | +1.1% | Greater KL, Penang | Medium term (2-4 years) |

| Infrastructure projects (MRT, highways, RTS) forging new corridors | +1.0% | Transit-oriented zones, Greater KL, Johor | Long term (≥ 4 years) |

| Government housing initiatives expanding first-time buyer access | +0.8% | National urban centers | Short term (≤ 2 years) |

| MM2H and related foreign-ownership policies | +0.7% | Premium areas of KL, Johor Bahru, Penang | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization in Key Cities

Urbanization is accelerating in Kuala Lumpur, Johor Bahru, and Penang, significantly influencing the residential real estate market. Migration to these cities is increasing demand, extending beyond central areas and fostering the development of dense, transit-oriented residential clusters. The operational MRT2 line has enhanced the appeal of suburban areas, attracting younger households seeking affordable housing with convenient rail access. In Johor Bahru, the upcoming RTS Link is transforming expectations for cross-border commutes, making southern neighborhoods more attractive to Singapore-based professionals. Penang's limited land availability is shifting development to fringe areas, where infrastructure upgrades are unlocking new opportunities for mixed-use projects. This self-reinforcing urbanization where new residents drive the need for additional rail, road, and amenities creates a positive cycle for the residential real estate market. Sustained population growth in these cities underpins a strong medium-term sales pipeline for developers.

Middle-Class Appetite for Condominium Living

Malaysia's expanding middle class increasingly values convenience, security, and shared amenities over larger floor areas. Premium mid-market projects like Gamuda Cove experienced full uptake upon launch, demonstrating the demand for integrated townships that combine retail spaces, green areas, and smart-home features. The redevelopment of industrial zones, such as Sentul, into lifestyle destinations further reflects the influence of this demographic. Developers are now integrating co-working lounges, daycare centers, and EV-charging bays into condominium designs to meet the expectations of these buyers. As middle-income households move up the housing ladder, the residential real estate market in Malaysia benefits from predictable upgrade cycles. Although economic slowdowns may heighten concerns about job security, the current labor market stability supports near-term growth[1]“Gamuda Cove Fully Booked at Launch,” The Edge Malaysia, theedgemalaysia.com.

Infrastructure Catalysts Redrawing Location Premiums

Malaysia's infrastructure advancements are reshaping urban landscapes and enhancing connectivity. The 51-kilometer MRT3 Circle Line will integrate with existing rail networks, reducing commute times and increasing land values along its alignment. In Johor Bahru, the USD 565.2 million mixed-use development at Bukit Chagar station highlights developer confidence in rail-focused urban planning. Similarly, highway extensions are bringing new suburbs within convenient driving distances of city centers, unlocking vast greenfield areas for affordable housing. Beyond improving mobility, these projects are spurring retail and office developments, creating self-sufficient districts. Consequently, Malaysia's residential real estate market is experiencing a sustained shift in demand toward infrastructure-supported corridors.

Government Housing Initiatives for First-Time Buyers

Malaysia's government is implementing targeted measures to address housing affordability challenges for first-time buyers. In a bid to bridge affordability gaps, policymakers are rolling out measures like credit guarantees, extended loan tenures, and significant budget allocations. Under Budget 2025, a USD 2.17 billion (converted from RM 10 billion) guarantee pool aims to assist 20,000 buyers. Additionally, tax relief on mortgage interest eases the financial burden post-purchase. The Housing Credit Guarantee Scheme has bolstered loan approval rates, showcasing the effectiveness of fiscal support. PR1MA’s ventures, some valued over USD 217 million, are strategically linking subsidized housing units with mass transit nodes, ensuring families remain close to their workplaces. While these initiatives are successfully lowering entry barriers and stimulating demand in Malaysia's residential real estate market, a significant challenge persists: aligning project locations with genuine market needs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban oversupply dragging absorption in select luxury pockets | -0.9% | Kuala Lumpur, Johor Bahru high-end zones | Short term (≤ 2 years) |

| Construction-cost inflation squeezing project economics | -0.8% | Nationwide | Short term (≤ 2 years) |

| Policy volatility on foreign ownership clouding sentiment | -0.6% | Prime districts favored by foreign buyers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Urban Oversupply in Luxury Segments

The Malaysian luxury housing market continues to grapple with oversupply challenges. By mid-2023, Malaysia's unsold housing stock reduced to 26,286 units. However, high-end neighborhoods still face imbalances as speculative developments exceed actual demand. Johor, with 4,717 unsold units, exemplifies regional concentration risks despite national improvements. Over half of the unsold inventory is priced below USD 108,700 (RM 500,000), reflecting a mismatch between property prices and local purchasing power. Developers have curtailed new launches and introduced rebates to expedite sales, yet high holding costs remain a concern. Without better alignment between property offerings and local affordability, certain segments of Malaysia's residential market may experience limited price growth.

Construction-Cost Volatility

Construction material costs have experienced significant volatility in recent years. Material prices fluctuated throughout 2023 and 2024, with predictions of a 4.5-5.5% rebound in 2025-2026 after a brief dip. These price swings, especially in steel and cement further intensified by rising energy costs are pushing developers to resort to hedging, redesigning projects, or even postponing them. Projects with capped end-prices, particularly in the affordable segment, are feeling the brunt of these fluctuations. As a result, Malaysia's residential real estate market is grappling with a tightening margin, potentially stalling supply, especially for its more price-sensitive housing segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: Rental Momentum in a Sales-Centric Landscape

Sales transactions comprised 76.25% of the Malaysia residential real estate market in 2025, reflecting the nation’s ingrained home-ownership culture. Yet the rental segment is accelerating at a 5.67% CAGR, underpinned by a mobile professional class that values flexibility, foreign tenants under MM2H, and graduates delaying first purchases in favor of liquidity. Tech-enabled platforms such as SPEEDHOME and BlueDuck are formalizing lease processes, improving transparency and boosting landlord confidence. Institutional investors are exploring build-to-rent portfolios near MRT stations, a nascent but scalable opportunity within the Malaysia residential real estate market. Tax incentives and assured yields could tilt more capital toward rental schemes if policymakers elect to formalize this asset class.

Continued fiscal support for mortgages, including the USD 2.17 billion guarantee pool, sustains sales volumes and keeps developers committed to ownership models. However, affordability stresses in central districts and shifting lifestyle preferences suggest rentals will keep gaining share through 2031. Developers are responding with dual-key condo layouts that cater to co-living trends, and some suburban townships now integrate purpose-built rental blocks alongside for-sale units. The parallel rise of co-working amenities within residential compounds further narrows the appeal gap between renting and owning.

By Property Type: High-Rise Dominance Faces Landed Revival

Apartments and condominiums led with a 70.55% slice of the Malaysia residential real estate market in 2025 thanks to land scarcity in prime corridors and demand for security and facilities. High-rise launches cluster around rail nodes where smaller unit sizes align with young professional budgets and investors chasing rental yields. Smart-home packages, clubhouse memberships, and rooftop community gardens are now standard inclusions, reinforcing the appeal of vertical living. Integrated mixed-use precincts such as Tun Razak Exchange illustrate how condo towers can anchor wider commercial ecosystems, reinforcing values.

Landed houses and villas, though smaller in aggregate, are pacing the field with a 6.23% CAGR as post-pandemic buyers chase extra space and private gardens. Suburban freehold land near new expressways allows developers to price terraced homes competitively while promising city-center access within manageable commute windows. Projects like Sime Darby Property’s Elmina and EcoWorld’s Eco Botanic harness wellness branding and extensive parklands to lure upgraders. The Malaysia residential real estate market benefits from this dual-track demand, allowing developers to diversify portfolios and hedge against cyclical shifts in buyer sentiment.

By Price Band: Affordability Anchors, Luxury Climbs

Affordable units dominated 49.10% of the Malaysia residential real estate market in 2025, buoyed by government guarantees and PR1MA stock targeted below USD 108,700. Loan-to-value ratios of up to 110% for qualified first-time buyers under the Step-Up Financing Scheme further buttress demand. Nevertheless, the luxury tier, priced above USD 217,000, is projected to outpace all bands at a 6.44% CAGR, fueled by foreign inflows and rising domestic wealth. Branded residences attached to five-star hospitality operators, such as the Ritz-Carlton Residences in Kuala Lumpur, command premiums through service conveniences and global brand equity.

Mid-market condominiums serve as a transition ladder for households moving from subsidized units toward aspirational addresses. Their positioning within the Malaysia residential real estate market is crucial, absorbing upgrading demand while preventing over-reliance on subsidy-driven segments. Developers focus on value engineering—modular construction, efficient shared facilities—to protect margins without compromising perceived quality.

By Mode of Sale: Primary Launches Sustain Momentum

Primary launches represented 61.75% of the Malaysia residential real estate market size in 2025 and continue to expand at a 6.18% CAGR, evidencing buyer preference for warranty-backed, modern layouts and flexible progress-payment schemes. Gamuda Land’s Palma Sands, a USD 99.1 million project in Gamuda Cove, achieved a full take-up for its opening 198 homes, validating demand for master-planned communities. Early-bird rebates, zero-entry fees, and bundled furnishings sharpen the appeal of new builds over secondary stock.

Secondary sales are still vital for market liquidity and price discovery, particularly in mature suburbs where land scarcity limits fresh supply. Yet aging building services and lower ESG credentials can deter younger buyers. Owners seeking capital recycling are thus motivated to refurbish existing units, injecting modern design cues and smart-home features to remain competitive. Transactional data suggest secondary-market discounts have narrowed, confirming a healthy coexistence of both channels within the Malaysia residential real estate market.

Geography Analysis

Kuala Lumpur's position as a key player in Malaysia's residential real estate market is supported by its diverse employment opportunities, extensive MRT network, and ongoing development of mixed-use precincts that transform underutilized land into high-density neighborhoods. Condominium towers near the upcoming Pantai Dalam and Mont Kiara Circle Line stations have recorded strong pre-sales, reflecting the continued appeal of proximity to rail transit. Additionally, government land releases along Sungai Besi are driving the development of new affordable housing projects, expanding the capital's market to cater to a broader range of income groups.

In Johor Bahru, residential development is increasingly concentrated in areas closer to the RTS terminus, as professionals from Singapore consider the trade-off between lower living costs and commuting convenience. Incentives tied to special economic zones are expected to create more employment opportunities around the Port of Tanjung Pelepas and the emerging technology hub in Forest City. This is fostering housing demand that extends beyond speculative investments. In Iskandar Puteri, average transaction values have shown consistent growth without signs of overheating, indicating a stable absorption rate in the southern segment of Malaysia's residential real estate market.

In Penang, the limited availability of land on the island has shifted new property launches to the Seberang Perai mainland and the Bayan Lepas Technology Corridor, where elevated bridge connections ensure reasonable commute times. The state's established expatriate communities and high-quality healthcare facilities make it an attractive destination for investors, resulting in rental yields that surpass those in Kuala Lumpur's comparable luxury segments. Meanwhile, Kuantan and Kota Kinabalu are benefiting from growth in the industrial and tourism sectors, respectively. This reflects a gradual regional diversification that reduces the concentration risks historically associated with Malaysia's residential real estate market.

Regulatory Landscape

Malaysia's residential real estate regulatory environment is being reshaped by the Ministry of Housing and Local Government (KPKT) under the MADANI Housing Reform agenda that began on January 1, 2026. The agenda includes proposals such as the Real Property Development Bill, electronic Sales and Purchase Agreement (eSPA), the Housing Integrated Management System (HIMS), housing data initiatives under TEDUH, and tighter oversight through Housing Development Account (HDA) audits. The Real Property Development Bill is positioned to replace the Housing Development (Control and Licensing) Act 1966 (Act 118), broadening coverage beyond traditional housing licensing and raising compliance expectations for developers across more project types.

Affordability and buyer access are also being tied to price and financing frameworks. The National Housing Policy 2026-2035 uses local income and demand data, including the 2024 Household Income and Basic Amenities Survey, to set affordable home price benchmarks using the median multiple method. In parallel, civil-servant demand is supported through LPPSA measures, including an increased maximum financing eligibility up to RM1 million (applicable through December 31, 2026), plus youth-focused financing features such as longer tenures, which widens the policy-enabled borrower pool for mass-market projects in major urban centers.

Value Chain Analysis

Malaysia's residential real estate value chain begins with land sourcing and planning approvals, followed by developer-led product design and financing, then procurement and construction through main contractors and specialist trades. Construction delivery is increasingly shaped by national digitalization agendas, including the Construction 4.0 Strategic Plan (2021-2025) and the National Construction Policy 2030, which promote Building Information Modelling (BIM) and common data environments in project coordination. CIDB quality benchmarks (QLASSIC/CIS 7) also set workmanship expectations during the build stage, pushing developers and contractors toward standardized execution, traceable documentation, and tighter site-to-office integration.

Downstream, distribution is supported by primary sales channels such as developer sales galleries, digital marketing, and agency networks, alongside mortgage intermediation. Rental processes are being formalized through tech-enabled leasing platforms that streamline tenant screening and contracts. The supply side has shown sensitivity to disruptions from material cost volatility, labor constraints, and regulatory changes, which feeds into more cautious launch and phasing decisions; for example, new residential launches in Peninsular Malaysia fell to 12,938 units in 1H 2025 from 17,404 units in 2H 2024. Government affordability programs and buyer incentives support absorption, while developers respond through value engineering, rebalancing unit mixes toward bankable price points, and tighter vendor management to protect margins and delivery schedules.

Competitive Landscape

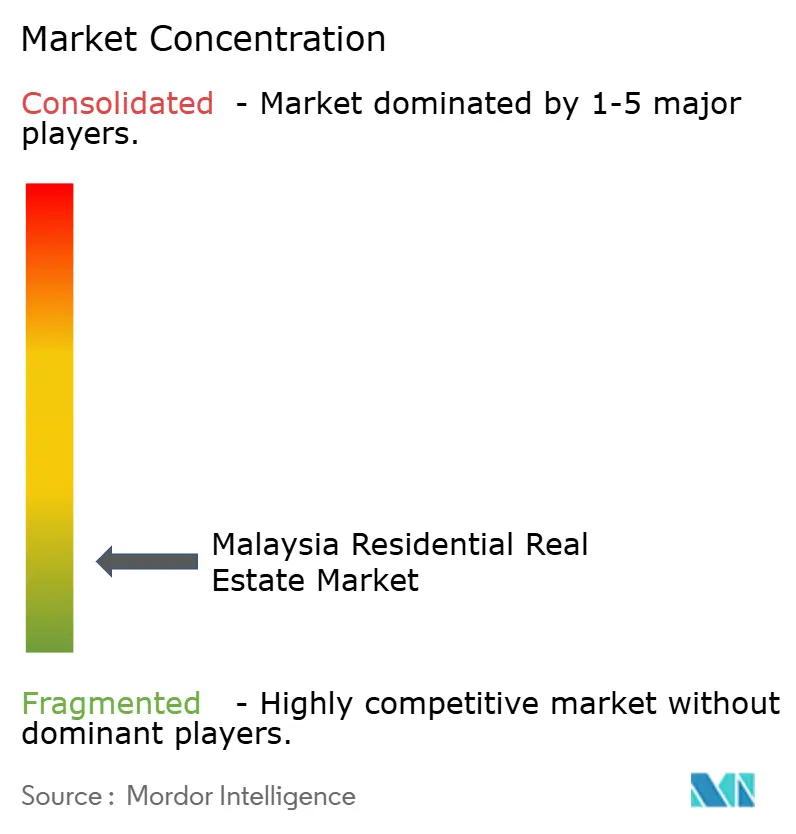

Malaysia’s residential real estate arena is moderately fragmented yet tilting toward consolidation as well-capitalized, government-linked companies absorb independent rivals. Government-linked companies with strong financial backing are increasingly acquiring independent competitors. For example, Permodalan Nasional Berhad (PNB) has made a USD 717.4 million bid to acquire a larger stake in S P Setia. This reflects a strategy to consolidate landbanks and distribute overhead costs across a wider revenue base. These approaches enhance the ability to execute large-scale township projects and improve access to funding, creating challenges for smaller players with weaker financial positions.

Additionally, diversified conglomerates are reducing their reliance on cyclical residential revenues by focusing on stable income streams. Sime Darby Property's partnership with Google to develop a hyperscale data center is expected to generate lease income for the next 20 years, providing a buffer against market fluctuations. Similarly, Sunway Group is utilizing its healthcare and education divisions to create a dedicated customer base for its on-site residential properties, establishing self-sustaining ecosystems that lower sales risks.

Developers are differentiating themselves by focusing on ESG credentials, obtaining green-building certifications, and implementing district-cooling solutions to reduce utility costs. As buyers increasingly prioritize energy efficiency, companies are adopting measures such as photovoltaic rooftops and rainwater harvesting systems. Moreover, digital sales platforms are gaining popularity, offering features like 360-degree VR tours, instant loan calculators, and blockchain-verified SPA documents, which streamline decision-making processes. In conclusion, success in the Malaysia residential real estate market will depend on combining strong financial resources with customer-focused innovation.

Malaysia Residential Real Estate Industry Leaders

S P Setia Berhad

Sime Darby Property Berhad

Sunway Property

Eco World Development Group Berhad

UEM Sunrise Berhad

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Policy-driven affordability calibration and tighter delivery governance are creating room for developers and solution providers that can connect product design, pricing, and execution to localized demand. Under the National Housing Policy 2026-2035, affordable housing price setting is anchored to local median household income and demand data using the median multiple method, which favors developers with granular, district-level market intelligence and the ability to tailor unit sizes and specifications to state and district affordability thresholds. KPKT's MADANI Housing Reform agenda, including HIMS and HDA audits, and the stated target of zero sick projects by 2030 also raise the value of audit-ready reporting, milestone monitoring, and end-to-end documentation for contractors, project-management firms, and proptech vendors.

On the product and geography side, transit-linked and infrastructure-adjacent residential nodes continue to attract mixed-use investment, supporting opportunities around MRT corridors and the Johor Bahru RTS station catchment. The Sunway Group and MRT Corp public-private partnership for the Bukit Chagar integrated development, a USD 565.2 million transit-linked district, provides a clear example of rail infrastructure being packaged with residential inventory, retail, and parking to widen viable commuting zones and deepen buyer pools. In Penang, new launches such as Mah Sing's M Amaya (833 units in Batu Maung, GDV RM516 million, launched in July 2026) show continued developer appetite in land-constrained, employment-linked corridors, reinforcing opportunities in mid-market vertical living and mixed-use formats where amenities and accessibility support take-up.

Recent Industry Developments

- July 2026: Malaysia's Ministry of Housing and Local Government outlined the National Housing Policy 2026-2035 approach to setting affordable home price benchmarks using local income and demand data, including median household income from the 2024 Household Income and Basic Amenities Survey. The shift strengthens location-specific planning and pushes developers to calibrate unit sizing and pricing to district-level affordability thresholds.

- October 2025: The government doubled the Housing Credit Guarantee Scheme under Budget 2026 to RM20 billion to support first-time homebuyers through credit guarantees. The increased guarantee pool reinforces demand-side financing access and improves absorption visibility for developers focused on affordable and mid-market stock.

- October 2024: Malaysia extended the Home Ownership Campaign 2.0 until the end of 2025, maintaining stamp duty exemptions for eligible first-time buyers and related tax relief measures tied to qualifying home purchases. The extension supported primary-market conversions by lowering up-front transaction costs and encouraging developers to align launch pricing with incentive thresholds.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as the total value of residential property activity in Malaysia that is tied to homes purchased or occupied for living, captured across new and existing stock and reflected through transaction and sales value measures.

Scope exclusions: This sizing excludes non-residential property activity such as offices, retail, industrial buildings, and pure land banking that is not linked to a residential unit sale.

Segmentation Overview

- By Business Model

- Sales

- Rental

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base on housing demand, supply additions, prices, and financing conditions before the model was built. We referred to public statistics and policy releases such as those from Malaysia government housing and planning bodies, the central bank, national statistics publications, and land or property registry style transaction summaries where available.

To pressure test trends, supporting reads were added from sources such as listed developer filings and investor presentations, bank and brokerage housing notes, reputable press coverage, and association pages covering homebuyers and the property industry. In addition, we used select paid subscriptions for company financials and intelligence, news and financials, and patents where relevant to validate corporate activity and major project timelines. These desk sources are not exhaustive, and many other public documents were also reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to convert the desk indicators into realistic shares, pricing logic, and on-the-ground assumptions for city demand and inventory movement. We spoke with a mix of developers, brokers, lenders, valuers, and professional advisors, and then validated key points with buyers-side and institutional viewpoints where possible.

Coverage was balanced across major urban centers and secondary cities, and discussions were used to close gaps on new launches versus resale mix, price band splits, and the practical impact of policy changes on absorption and funding.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 14% | |

| Mid tier: 57% | Functional/Unit leaders: 30% | |

| Smaller Players: 17% | Managers: 56% |

Market-Sizing & Forecasting

Sizing was built using a top-down approach where housing demand pools and transaction signals were reconstructed into value, and then filtered through city coverage and property-type splits to land at a national total. We then corroborated the totals using selective bottom-up approximations, such as sampled unit volumes by launch pipelines and resale activity, combined with observed price ranges and mix by price band.

Key inputs used in the model included residential transaction volumes, average transacted prices and price index movement, mortgage approvals and lending conditions, new launch and completion pipelines, and urban household formation signals. Because gaps can appear in city or type level splits, we used interview-led ranges and applied consistency checks so totals stayed aligned with known demand and supply movements.

For forecasting, scenario analysis was applied around interest rates, affordability, and inventory overhang (where it exists), and the base case was anchored to consensus expectations gathered from primary discussions. Assumptions were updated by city and by new versus resale share so growth does not get forced uniformly across Malaysia.

Data Validation & Update Cycle

Outputs were validated through repeated triangulation across independent indicators, including price direction, transaction momentum, credit conditions, and supply additions, and then checked for year-to-year jumps that do not match market reality. When variances appeared, the underlying drivers were revisited, and targeted re-contacts were triggered to confirm whether the shift was structural or temporary.

A multi-step analyst review was followed before sign-off, which included logic checks on segment totals and cross-checks against comparable housing metrics. Reports are refreshed annually, with interim updates added when material events occur, and a final pre-delivery review is done so clients receive the most current view.

Mordor Intelligence's Malaysia Residential Real Estate Market Size Compared With Other Published Estimates

Published market numbers for Malaysia residential real estate can look different even when the topic sounds the same, because the counted activity is not always identical and the base year timing can shift. Differences typically come from what is treated as residential value, how new builds versus resale are handled, and how prices are carried forward when the market is uneven across cities.

The table points to a spread that is strongly linked to scope and year alignment. Some estimates anchor the market to a 2024 starting point and then extend a straight growth path, while others include a wider set of residential-related value lines without fully separating sales from other housing services, which can move the total up or down.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 25.18 B (2025) | |

| Global Data Publisher A | USD 22.41 B (2024) | Uses an earlier base year and can understate the step-up from 2024 to 2025 if price recovery and transaction mix changes are not rebuilt by city and by new versus resale. |

| Industry Portal B | USD 29.84 B (2029) | Shows a forward year value that is not directly comparable to a base-year estimate, and the uplift can look larger if price growth is applied more uniformly across property types and locations. |

The comparison is easier to interpret once the year and the counted value lines are lined up. In Mordor Intelligence's model, residential value is tracked with explicit splits for primary (new-build) versus secondary (resale) activity and price band mix, which makes the totals more traceable when conditions vary across Malaysian cities.

Key Questions Answered in the Report

What is the current value of the Malaysia residential real estate market?

The Malaysia residential real estate market is valued at USD 26.52 billion in 2026.

How fast is the Malaysia residential real estate market expected to grow?

The market is projected to expand at a 5.33% CAGR, reaching USD 34.38 billion by 2031.

Which Malaysian city is forecast to grow the fastest for residential property?

Johor Bahru leads with a 6.79% CAGR, driven by the upcoming RTS Link to Singapore.

What policy measures support first-time home buyers in Malaysia?

Budget-backed loan guarantees, longer mortgage tenures, and tax relief under Budget 2025 lower entry barriers for new buyers.

Why are foreign investors interested in Malaysian housing?

The revamped MM2H program offers residency pathways alongside property purchase requirements, attracting capital from China, Singapore, and beyond.

Which property type is gaining popularity post-pandemic?

Landed houses and villas are rising at a 6.23% CAGR as buyers prioritize space and private outdoor areas.

Page last updated on: