Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

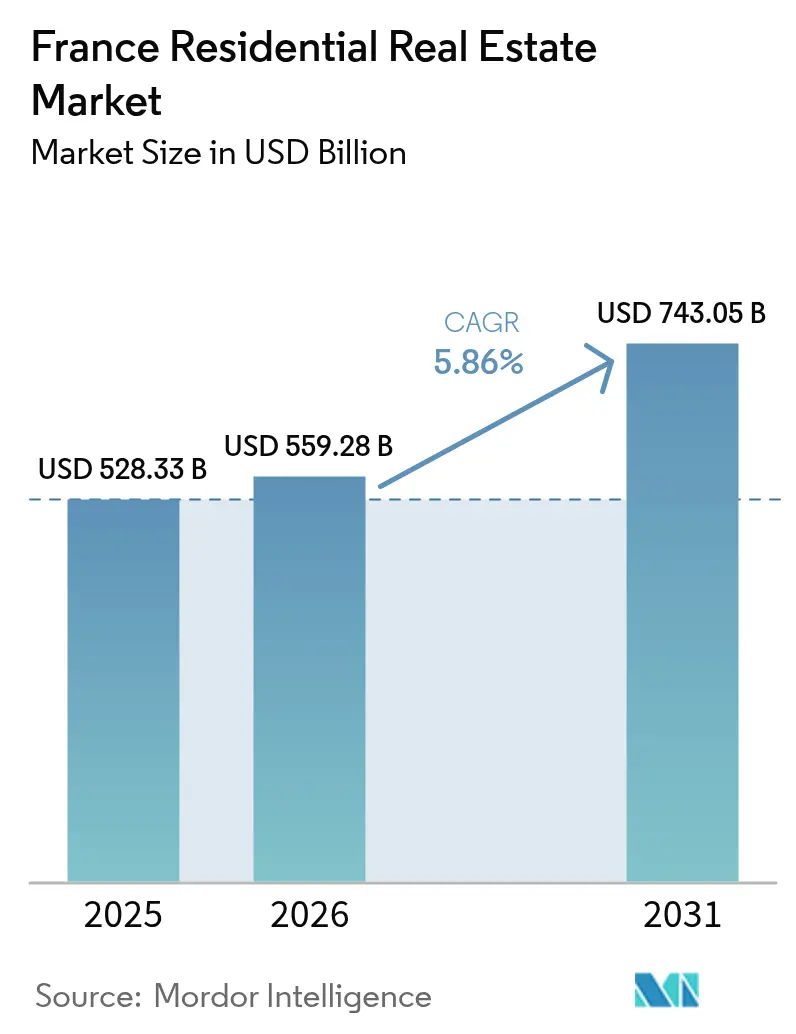

| Base Year Market Size (2025) | USD 528.33 Billion |

| Market Size (2026) | USD 559.28 Billion |

| Market Size (2031) | USD 743.05 Billion |

| Growth Rate (2026 - 2031) | 5.86% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Residential Real Estate Market Analysis by Mordor Intelligence

The France residential real estate market size is expected to grow from USD 528.33 billion in 2025 to USD 559.28 billion in 2026 and is forecast to reach USD 743.05 billion by 2031 at 5.86% CAGR over 2026-2031. This recovery follows the 35.6% collapse in transaction volumes that occurred between August 2021 and October 2024, underlining the market’s resilience as lending standards, mortgage costs, and demographic trends realign to new post-pandemic realities. Mortgage rates have eased from 4.21% in late 2023 to near 3.1% in 2025, and credit production is already 71% higher than the preceding year, signaling renewed purchasing power and liquidity. Structural housing shortages, regulatory energy-efficiency timelines, and remote-work migration to southern and western regions are adding durable tailwinds. At the same time, institutional capital is accelerating the rental-focused build-to-rent cycle, while energy regulations are accelerating upgrades in the existing stock, anchoring long-term value for compliant assets. Developers are pivoting toward recurring-income models and integrated investment services to shield margins from rising construction costs and policy-driven compliance outlays.

Key Report Takeaways

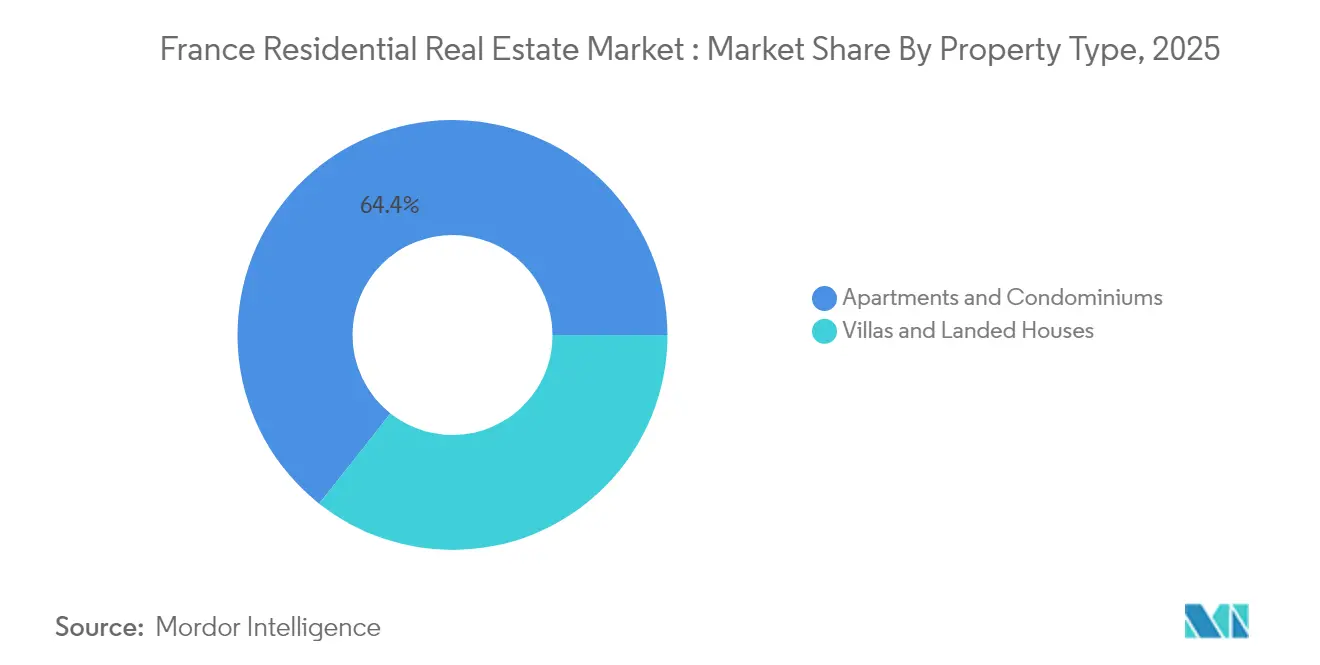

- By property type, apartments and condominiums led with 64.35% of France residential real estate market share in 2025, whereas villas and landed houses are projected to post the fastest 6.05% CAGR through 2031.

- By price band, the mid-market segment commanded 45.25% share of the France residential real estate market size in 2025; the affordable tier is projected to expand at a 5.98% CAGR from 2026 to 2031.

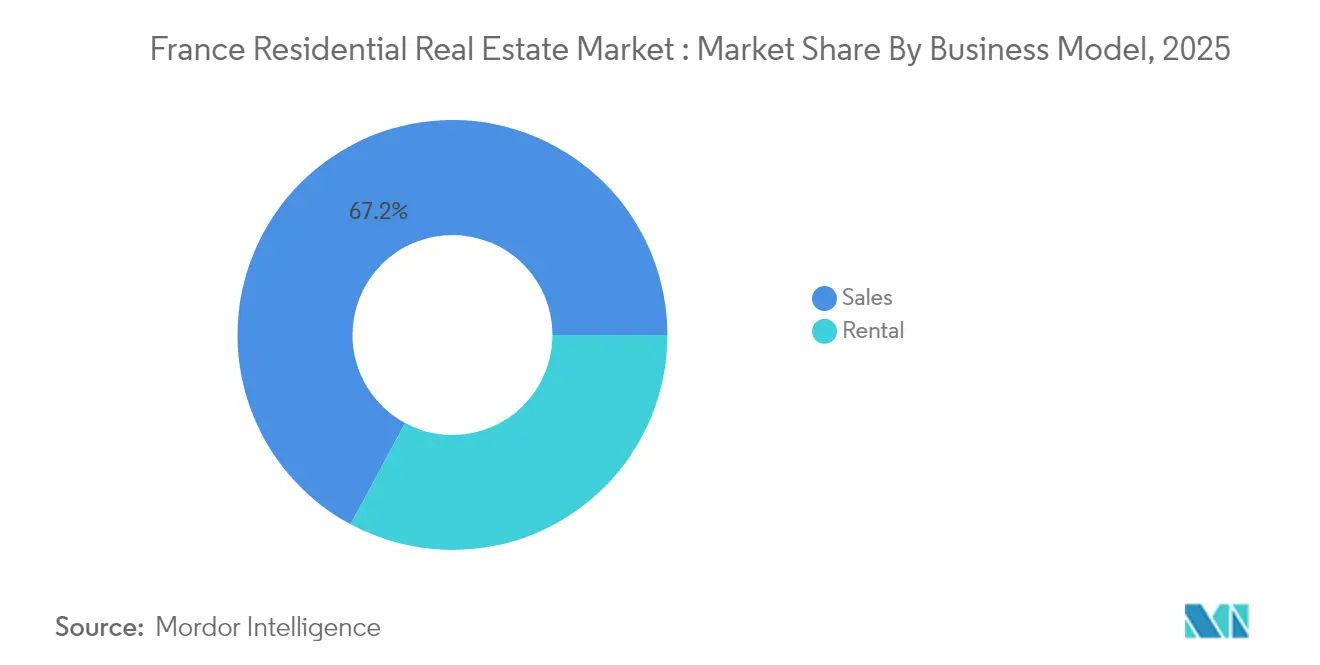

- By business model, the sales segment held 67.15% of France residential real estate market share in 2025, while rentals are forecast to rise at 6.15% CAGR through 2031.

- By mode of sale, the secondary segment accounted for 64.40% share of the France residential real estate market size in 2025, yet the primary segment is advancing at 6.08% CAGR to 2031.

- By region, Île-de-France remained the largest with a 27.60% share in 2025, whereas Occitanie is the fastest-growing at 6.20% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

France Residential Real Estate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Housing deficit & supply imbalance amid declining building permits | +1.2% | National; acute in Île-de-France, Lyon, Marseille | Long term (≥ 4 years) |

| Energy-efficiency regulations accelerating renovation & new-build demand | +0.9% | National; higher in older-stock regions | Long term (≥ 4 years) |

| First-time buyer incentives & PTZ+ extension fueling entry-level demand | +0.8% | Nationwide; stronger in Zones B and C | Medium term (2–4 years) |

| Build-to-rent institutional investment growth boosting rental supply | +0.7% | Major metros; expanding to secondary cities | Medium term (2–4 years) |

| Remote-work driven migration to suburban & rural areas | +0.6% | Occitanie, Nouvelle-Aquitaine, Centre-Val-de-Loire | Medium term (2–4 years) |

| Growing single-person households increasing demand for smaller units | +0.4% | Urban centers—Paris, Lyon, Toulouse | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Housing Deficit & Supply Imbalance Amid Declining Building Permits

New building permits fell 23.7% in 2023, deepening an estimated structural shortfall that underpins the France residential real estate market’s long-run price floor[1]Conseil Supérieur du Notariat, “Bilan Immobilier 2023,” Notaires de France, notaires.fr. The deficit is most severe where net in-migration persists, such as Île-de-France, which still adds roughly 50,000–60,000 residents per year despite accelerated outflows to southern regions. Costly materials and layered regulations slow new supply, so institutional investors target build-to-rent programs that lock in long leases and modern energy standards. Government ownership initiatives acknowledge the shortage’s role in stabilizing prices, rewarding developers that can maneuver within compliance constraints and swiftly deliver stock

First-Time Buyer Incentives & PTZ+ Extension Fueling Entry-Level Demand

France extended the zero-interest Prêt à Taux Zéro (PTZ+) to December 2027 and widened eligibility nationwide from April 2025, lifting entry-level purchase capacity[2]Service-Public France, “PTZ : conditions d’éligibilité 2025-2027,” Service-Public, service-public.fr. Lower mortgage costs around 3.1% in 2025 have coincided with PTZ+ uptake, and banks indicate longer 20-plus-year loan maturities that keep monthly burdens manageable. By mitigating equity gaps, the program funnels activity toward secondary cities previously outside high-tension zones, diversifying regional demand and re-energizing first-time buyer traffic.

Remote-Work Driven Migration to Suburban & Rural Areas

About 770,000 residents relocated from dense cities to rural communes in 2021, a 12% increase versus 2019, catalyzing fresh demand pockets and re-rating property values in Occitanie, Nouvelle-Aquitaine, and Centre-Val-de-Loire. With most movers citing permanent relocation plans, destination municipalities are fast-tracking infrastructure upgrades, creating circular benefits for local housing and services. High-income professionals retaining metropolitan salaries amplify purchasing power in recipient regions, amplifying the 6.36% CAGR forecast for Occitanie through 2030.

Energy-Efficiency Regulations Accelerating Renovation & New-Build Demand

The ban on G-rated rentals from 2025—and subsequent prohibitions on F-rated in 2028 and E-rated in 2034—creates a renovation market estimated at more than EUR 1,000/m², supported by MaPrimeRénov’ subsidies covering up to 90% of costs for qualifying households[3]Ministère de la Transition Écologique, “Entrée en vigueur du Diagnostic de Performance Énergétique 2025,” Ministère T.E., ecologie.gouv.fr. Efficient A/B-rated homes achieved price premiums of 1–2% during 2023, while F/G units lost up to 6% Notaires-de-France. Developers marketing compliant new builds enjoy preferential demand, and institutional investors deploy capital into energy-aligned portfolios that command higher rents and lower vacancy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising mortgage rates & tighter lending standards squeezing affordability | -1.10% | National; acute in Paris | Short term (≤ 2 years) |

| Stagnant real wage growth dampening purchasing power in core urban areas | -0.70% | Île-de-France, Provence-Alpes-Côte d’Azur | Medium term (2-4 years) |

| Ageing housing stock requiring high retrofit costs | -0.30% | National | Medium term (2-4 years) |

| Price volatility & market correction creating buyer uncertainty | -0.10% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Mortgage Rates & Tighter Lending Standards Squeezing Affordability

Although costs retreated from 4.2% peaks, the current 3.1% average still triples the record-low 1.05% rate of late 2021. Stricter prudential norms cap indebtedness, curbing access for mid-income borrowers, and outstanding housing loans slipped 0.65% y/y to EUR 1.424 trillion in July 2024 BNP-Paribas. Longer 253-month amortizations offset some pressure but highlight affordability strain in premium markets and defer ownership for younger households.

Stagnant Real Wage Growth Dampening Purchasing Power in Core Urban Areas

Real pay has lagged housing inflation, reducing the share of employees and workers in purchase transactions since 2019; top-tier managers now represent 52% of buyers Notaires-de-France. Paris prices above EUR 9,500/m² demand incomes well beyond regional medians, prompting sustained out-migration that eases local demand yet compresses liquidity across core urban segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Property Type: Apartments Anchor Volume While Villas Capture Growth Premium

Apartments captured 64.35% of France residential real estate market share in 2025, reflecting the dominance of higher-density living formats in metropolitan areas. Villas and landed houses account for a smaller base but are projected to expand at a 6.05% CAGR, benefiting from post-pandemic space preferences and remote-work flexibility. Energy mandates impose heavier per-unit retrofit costs on aging apartment blocks, whereas detached homes offer owners more control over upgrade timelines. Apartments nevertheless gain scale advantages in large urban regeneration projects such as Clichy-Batignolles, which is delivering 3,400 units including a 50% social-housing component. Rental-focused investors increasingly target suburban single-family assets to secure yield premiums above dense-core apartments, especially in Occitanie and Nouvelle-Aquitaine.

In the medium term, the France residential real estate market size of villa transactions is forecast to rise faster than apartment sales as household relocation to lower-density zones persists. Yet apartments will remain the backbone of urban portfolios, supported by inbound student and migrant populations, and by developer-led modernizations that lift energy labels to meet 2030 standards. Institutional buyers show growing appetite for mixed-use buildings that integrate residential floors atop commercial podiums, leveraging apartments’ steady cash flows to balance office-market volatility.

By Price Band: Mid-Market Dominance Faces Affordable-Tier Acceleration

Mid-market properties represented 45.25% of France residential real estate market size in 2025, providing the broadest match between buyer budgets and available stock. Affordable units, while smaller in value terms, are poised for 5.98% CAGR growth through 2031 as PTZ+ and MaPrimeRénov’ lower entry hurdles. Regional dispersion is visible: demand for affordable homes clusters in secondary towns offering below-median prices and quality-of-life advantages, whereas high-income purchasers still dominate Parisian prime and luxury segments.

Energy-efficiency rules also shape price-band dynamics. Owners in lower-priced brackets may struggle to finance mandatory upgrades, risking accelerated disposals that tighten supply and elevate residual values of renovated affordable stock. Meanwhile, developers supported by institutional mandates funnel capital toward intermediate housing priced for public-sector employees, addressing a structural gap highlighted by a EUR 200 million residential program from pension fund ERAFP.

By Business Model: Rental Growth Outpaces Sales as Institutional Capital Expands

Traditional home sales retained a 67.15% France residential real estate market share in 2025, but rentals are projected to outpace them at 6.15% CAGR, redefining the country’s tenure profile. Persistent affordability constraints, demographic trends toward later family formation, and professional mobility make flexible housing more attractive. Pension funds and insurers are ramping up build-to-rent projects with long-duration, inflation-linked cash flows, while large developers such as Bouygues Immobilier introduce PASS’INVEST packages that combine unit delivery, fit-out, and first-year property management to draw private investors.

As regulatory hurdles rise, institutional owners equipped with capital and compliance expertise will capture market share from fragmented private landlords. The France residential real estate market size allocated to purpose-built rental blocks is therefore set to rise, particularly in university cities and transit-oriented developments where tenant demand is consistent.

By Mode of Sale: Secondary Dominance Meets Primary-Sector Renaissance

Existing-home resales commanded 64.40% France residential real estate market share in 2025, entrenched in a mature housing stock. Yet the primary sector is forecast to grow at 6.08% CAGR on the back of stricter energy codes that favor new builds. Grand Paris Express rail extensions produce fresh land around new stations, catalyzing ground-up projects that offer immediate regulatory compliance and high-efficiency certifications.

Developers bundle sustainability features and turnkey warranties to justify price premiums, while buyers benefit from lower operating costs and PTZ+ incentives attached to new construction. Although the secondary market will remain dominant, rising retrofit expenses for older units could slowly chip away at its share as the primary pipeline scales.

Geography Analysis

Out of France’s 13 mainland regions, Île-de-France remains the most valuable residential market, responsible for 27.60% of total transaction volume in 2025 despite record net migration losses. The 21% rebound in Q1 2025 sales to 29,190 deals shows momentum returning, yet activity is still 10% under Q1 2023, reflecting affordability frictions and a higher-for-longer interest-rate backdrop. New metro lines under Grand Paris Express have repositioned peripheral communes such as Clichy-sous-Bois and Saint-Ouen as redevelopment hotspots, encouraging high-density projects that align with 2030 energy norms. Roughly one-third of Paris stock carries F or G energy labels, imposing urgent renovation needs but also creating upside for early movers who upgrade ahead of deadline.

Occitanie’s ascent illustrates the gravitational realignment of the France residential real estate market. The region welcomed 145,000 new inhabitants in 2016 alone, equal to 2.5% of its population; 59% of newcomers held at least a baccalauréat, confirming skilled-labor appeal. Toulouse commands Europe’s largest aerospace cluster, sustaining high-wage employment and spurring housing demand in both urban cores and peri-urban communes. Montpellier benefits from life-science hubs and a robust university ecosystem, drawing students and young professionals who underpin vibrant rental demand. Municipal investments in tramway extensions, bike lanes, and digital infrastructure enhance liveability, reinforcing the migration flywheel.

Provence-Alpes-Côte d’Azur aligns lifestyle pull with international capital inflows. Foreign purchasers rose 15% in 2024, and roughly one-quarter of trades involved second-home buyers, often from Northern Europe. Aix-en-Provence posted EUR 5,858/m² median prices, while sea-view villas in the Var or Alpes-Maritimes command EUR 2-4 million. With tourism generating steady short-let traffic, landlords achieve average gross yields near 4.5%. The regional council’s clean-energy roadmap, including stricter coastal building rules, is incentivizing eco-designed developments that already secure 10% rent premiums, anchoring long-term value for compliant assets.

Competitive Landscape

The France residential real estate market is moderately competitive, with competition shifting from the traditional build-and-sell model to platform models. These new models integrate development, asset management, and energy-compliance expertise. While the market share remains moderately fragmented, the looming energy mandates for 2025–2034 are driving a wave of consolidation. Major players, with their substantial balance sheets, are not only absorbing retrofit expenses but are also teaming up with institutional investors in pursuit of stable rental streams.

Bouygues Immobilier exemplifies strategic overhaul, launching PASS’INVEST to diversify income through rental management and tax-advantaged furnished-lease packages. The program reduces friction for retail investors, bundles accounting services, and secures furniture sourcing, thereby generating recurring fees beyond construction margins. ERAFP’s EUR 200 million allocation to residential mandates spotlights pension-fund appetite for intermediate housing, driving a wave of forward-funding agreements that guarantee developers off-take and align portfolios with social-impact metrics.

M&A momentum is likewise gaining pace. The agreed 13:1 share-swap merger of Inmobiliaria Colonial and Société Foncière Lyonnaise will create a pan-European platform focused on prime offices and high-end apartments, improving capital-market visibility and funding costs. Gecina, France’s largest listed residential owner, lifted recurrent net income per share 6.7% in 2024 by recycling non-core assets into energy-efficient flagship schemes expected to earn EUR 60-70 million annually by 2028 Gecina. Digital transformation supports competitive edges too: firms deploy PropTech tools for real-time energy monitoring, predictive maintenance, and remote leasing, trimming operating costs and boosting tenant satisfaction.

France Residential Real Estate Industry Leaders

Nexity

Bouygues Immobilier

Groupe Pichet

Icade

BNP Paribas Real Estate

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Bouygues Immobilier introduced PASS’INVEST, bundling furniture installation, accounting support, and first-year management to simplify rental investment for individual landlords

- April 2025: The government extended PTZ+ to end-2027 and opened eligibility to individual new homes nationwide.

- February 2025: Gecina recorded a 6.7% earnings rise for 2024, lifting per-share recurrent income to EUR 6.42 and announcing three pipeline projects worth EUR 60-70 million in future revenue.

- January 2025: France enforced its ban on renting G-rated homes and expanded MaPrimeRénov’ aid, while mandating energy audits for tourist rentals.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the residential real estate market in France as the annual value of completed new-build and existing dwellings, houses, villas, apartments, and condominiums traded for owner-occupation or long-term rental, expressed in constant 2024 USD. Transactions executed purely for short-stay hospitality, purpose-built student housing, and retirement facilities are excluded.

Scope Exclusion: Commercial, industrial, and mixed-use floor space that is primarily non-residential is kept outside the frame.

Segmentation Overview

- By Property Type

- Apartments & Condominiums

- Villas & Landed Houses

- By Price Band

- Affordable

- Mid-Market

- Luxury

- By Mode of Sale

- Primary (New-Build)

- Secondary (Existing Home Resale)

- By Business Model

- Sales

- Rental

- By Region

- Île-de-France

- Provence-Alpes-Côte d’Azur

- Auvergne-Rhône-Alpes

- Nouvelle-Aquitaine

- Rest of France

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview developers, brokers, mortgage executives, planning officials, and tenant associations across Ile-de-France, Auvergne-Rhone-Alpes, Occitanie, and Provence-Alpes-Cote d'Azur. These conversations test desk-derived assumptions on price sensitivity, buyer mixes, permit bottlenecks, and rental yields, enabling us to close information gaps before numbers are frozen.

Desk Research

We start with openly available macro and sector datasets, such as INSEE's household formation tables, Banque de France mortgage rate series, Eurostat building-permit filings, and the European Mortgage Federation's quarterly lending bulletins, to size demand pools and funding conditions. Construction ministry dashboards, notarial deed registries, and FNAIM's monthly price indices supply granular supply, pricing, and velocity clues. To validate company exposure and project pipelines, we tap D&B Hoovers and Dow Jones Factiva. A spectrum of press releases, investor decks, and parliamentary notes then helps clarify policy and tax levers. The sources quoted above are illustrative; many additional public and proprietary references inform the analysis.

Market-Sizing & Forecasting

A top-down construct aligns dwelling stock, turnover rates, and average sale values. Results are cross-checked through sampled developer roll-ups and channel probes, with a bottom-up touchpoint used once. Key variables in the model include mortgage affordability ratios, net household creation, building-permit issuance, average construction lead times, and policy incentives such as the extended Pret a Taux Zero. A multivariate regression with ARIMA error correction projects these drivers forward to 2030, while scenario analysis stress-tests shifts in rates or energy-efficiency rules. Where bottom-up evidence diverges, gaps are bridged by adjusting turnover assumptions within the bounds discussed with industry respondents.

Data Validation & Update Cycle

Before release, separate analysts audit formula chains, scrutinize outliers against INSEE, Banque de France, and cadastral feeds, and escalate anomalies for re-interview. The model refreshes annually; material shocks, such as rate jumps above 200 bps or policy changes on rental energy grades, trigger interim updates so clients receive a current baseline.

Why Mordor's France Residential Real Estate Baseline Commands Reliability

Published estimates rarely match because firms pick different scopes, price anchors, and refresh cadences. Some quote only owner-occupied sales, others fold in all mixed-use blocks, and many freeze exchange rates at data pull.

Key gap drivers include (i) inclusion or exclusion of rental turnover, (ii) treatment of provincial cities beyond the top ten, (iii) currency conversion timing, and (iv) frequency of primary-source validation.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 528.33 B (2025) | Mordor Intelligence | |

| USD 405.00 B (2024) | Global Consultancy A | Tracks only sale deeds in five metro areas, omits rental stock and secondary towns |

| USD 648.87 B (2024) | Data Platform B | Adds commercial units in mixed-use towers and applies static euro pricing without FX normalization |

The comparison shows that once scope breadth, rental turnover, and currency handling are harmonized, figures converge toward Mordor's disciplined, annually reviewed baseline, giving decision-makers a transparent and reproducible starting point.

Key Questions Answered in the Report

What is the current value of the France residential real estate market?

The market is valued at USD 559.28 billion in 2026 and is on track to reach USD 743.05 billion by 2031.

How fast is the France residential real estate market expected to grow?

A 5.86% compound annual growth rate is projected between 2026 and 2031.

Which region is growing the quickest?

Occitanie is forecast to post a 6.20% CAGR through 2031, outpacing all other regions.

Why is the rental segment expanding faster than home sales?

Institutional build-to-rent investment, affordability constraints, and shifting lifestyle preferences push the rental model toward a 6.15% CAGR, ahead of traditional sales growth.

Page last updated on: