Remote & Digital NDT Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

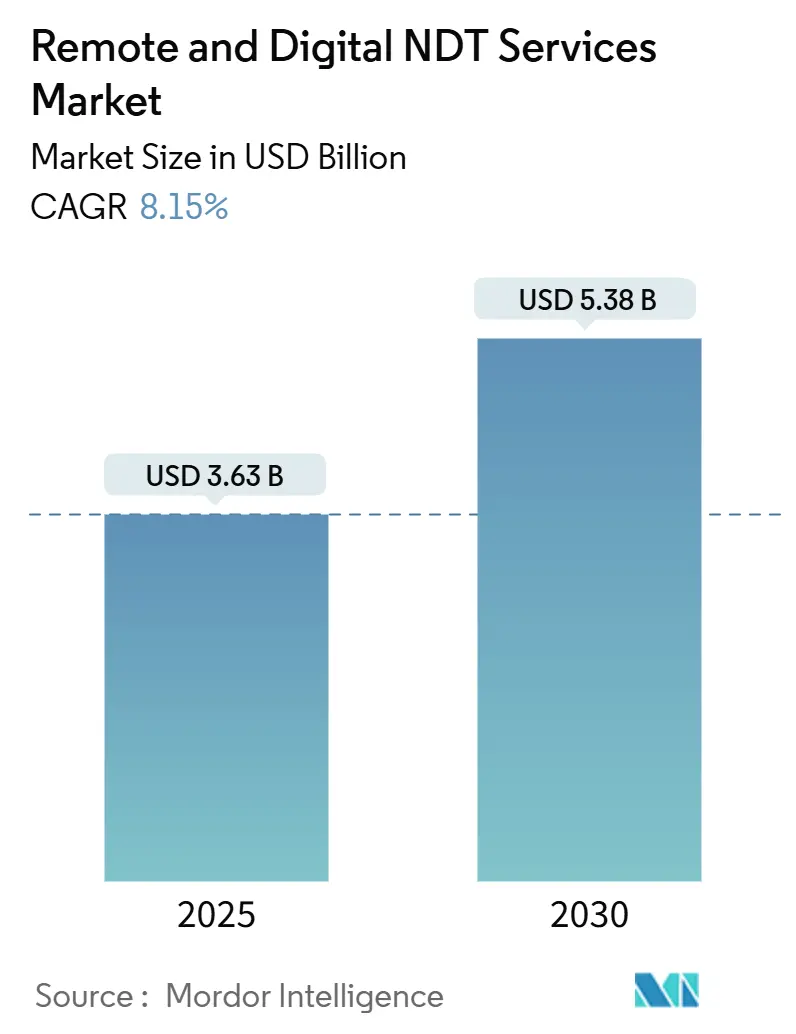

| Market Size (2025) | USD 3.63 Billion |

| Market Size (2030) | USD 5.38 Billion |

| Growth Rate (2025 - 2030) | 8.15% CAGR |

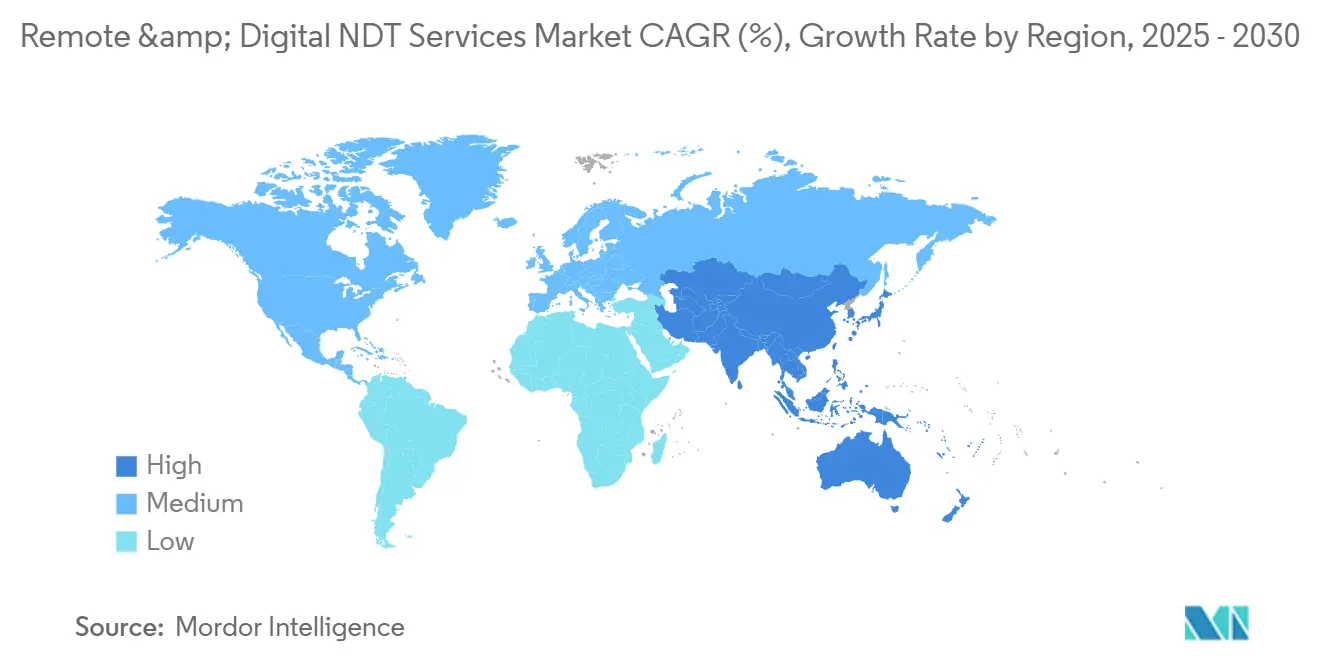

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Remote & Digital NDT Services Market Analysis by Mordor Intelligence

The remote and digital NDT services market size is estimated to be USD 3.63 billion in 2025 and is projected to reach USD 5.38 billion by 2030, growing at an 8.15% CAGR. The growing reliance on predictive maintenance, steady 5G rollouts at industrial sites, and expanding use of artificial intelligence in anomaly detection are steadily reshaping inspection budgets and staffing models. Operators are extending the life of aging oil, gas, and power assets far beyond their original design life because continuous streaming inspections eliminate costly shutdowns. High-resolution drones and autonomous crawlers now collect ultrasonic, visual, and radiographic data in confined or hazardous spaces, turning downtime savings into measurable earnings improvements. Large service vendors are integrating cloud analytics, edge gateways, and digital twin software into traditional field programs, strengthening long-term contracts and service-level guarantees.

Key Report Takeaways

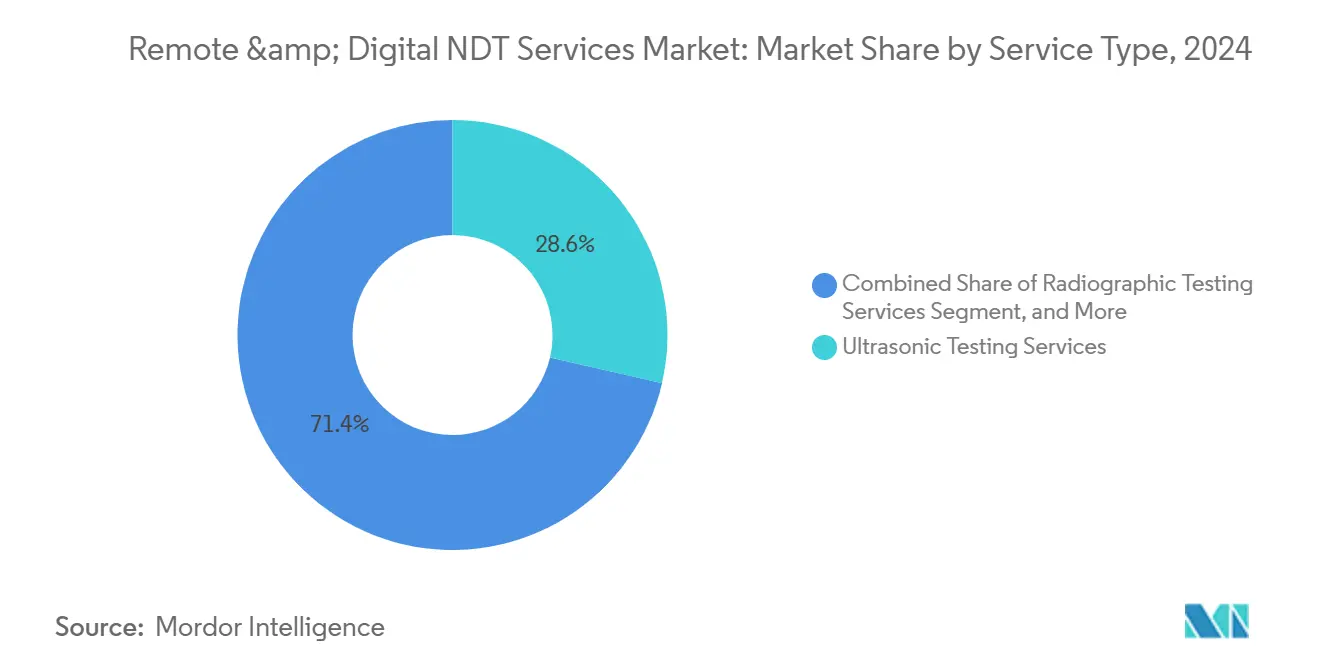

- By service type, ultrasonic testing led with 28.6% of the remote and digital NDT services market share in 2024, while remote visual inspection is expected to advance at a 12.2% CAGR through 2030.

- By service delivery mode, remote streaming and monitoring captured 34.5% of the revenue in 2024, whereas digital twin-based inspection is forecast to post the highest 14.2% CAGR over the 2025-2030 period.

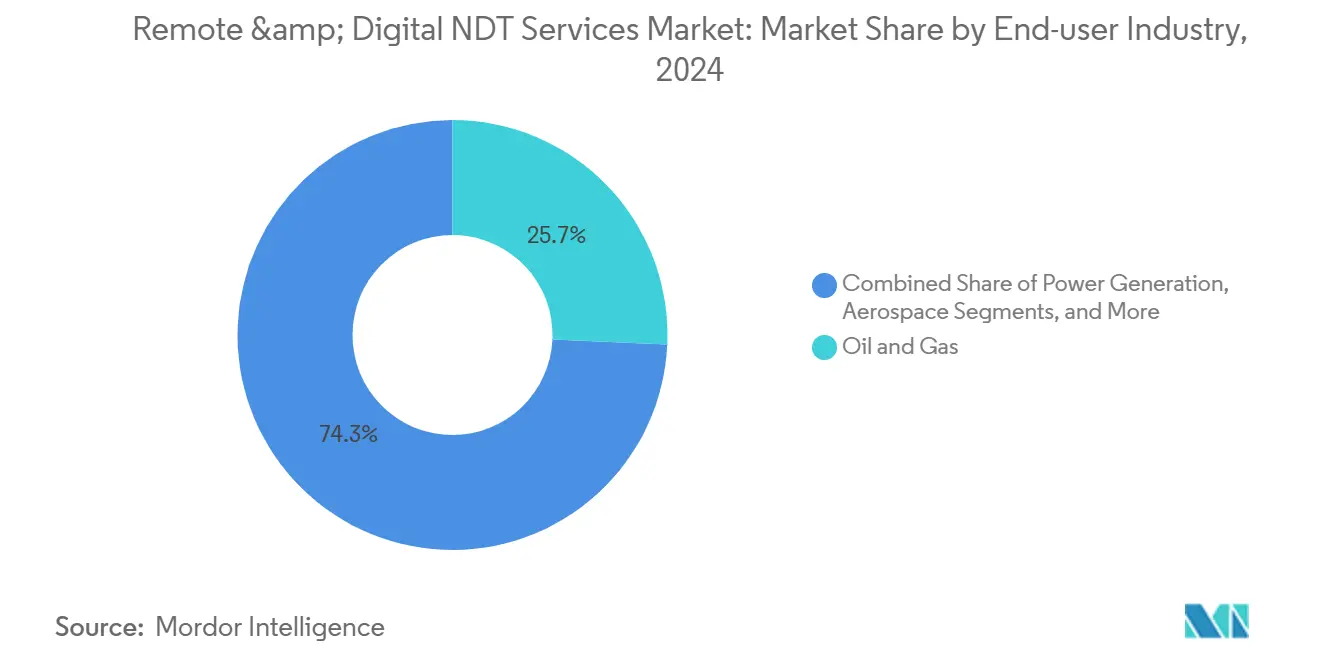

- By end-user industry, the oil and gas sector accounted for 25.7% of the remote and digital NDT services market size in 2024, and the automotive sector is set to expand at a 11.4% CAGR through 2030.

- By geography, North America accounted for 36.8% of the remote and digital NDT services market size in 2024, and the Asia-Pacific region is expected to expand at a 10.3% CAGR through 2030.

Global Remote & Digital NDT Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging industrial asset base requires continuous integrity assessment | +2.1% | Global, with a concentration in North America and Europe | Long term (≥ 4 years) |

| Rapid adoption of digital twins enabling remote inspections | +1.8% | North America and Asia-Pacific core, spillover to Europe | Medium term (2-4 years) |

| Cost pressure drives shift from shutdown-based to live-streamed inspections | +1.4% | Global, particularly the oil and gas sectors | Short term (≤ 2 years) |

| Stricter safety regulations on inaccessible assets (e.g., offshore platforms) | +1.2% | North America, Europe, and the Middle East | Medium term (2-4 years) |

| Availability of high-bandwidth 5G/edge connectivity at industrial sites | +0.9% | Asia-Pacific and North America early deployment | Medium term (2-4 years) |

| Decarbonization push accelerates asset life-extension projects using NDT | +0.8% | Europe and North America regulatory focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aging Industrial Asset Base Requires Continuous Integrity Assessment

Industrial equipment installed during the 1970-1990 expansion period now operates beyond its original design envelope. The American Society of Civil Engineers notes that more than 60% of critical North American industrial assets exceed their intended service life, intensifying the demand for high-frequency inspection data.[1]American Society of Civil Engineers, “Infrastructure Report Card – Industrial Assets,” asce.org Remote and digital NDT services enable operators to embed corrosion monitoring, thickness trending, and strain tracking directly into supervisory control systems, thereby reducing the risk of unplanned downtime. In power generation and refining, an unplanned outage can cost tens of thousands of U.S. dollars per hour, so even small reliability gains quickly offset inspection fees. Continuous remote data also satisfies API 580 and API 581 risk-based inspection programs, which now accept real-time inputs to validate the fitness-for-service of assets. The driver remains most pronounced where the replacement of large-diameter pressure vessels exceeds USD 100 million per plant, motivating owners to maximize the utility from their installed infrastructure.

Rapid Adoption of Digital Twins Enabling Remote Inspections

Digital twin platforms connect live sensor feeds with finite-element and material degradation models to forecast remaining asset life. Microsoft reports that seven out of ten industrial companies began pilot digital twins in 2024, with ultrasonic and visual NDT data forming a critical layer of telemetry.[2]Microsoft Corporation, “Industrial Digital Twin Adoption Study,” microsoft.com Virtual replicas reduce the frequency of manual inspections, cutting direct inspection costs by up to 40% while enhancing detection sensitivity and accuracy. Offshore platforms gain particular value because combined topside and subsea surveys can be simulated continuously without personnel transfer. Continuous twin-driven optimization of inspection intervals redistributes maintenance resources toward emerging anomalies, yielding fewer scaffolding hours and lower rope-access risk. Regulatory acceptance is on the rise: the United Kingdom's Health and Safety Executive now permits twin-augmented inspection evidence for specified duty-holder safety cases, signaling broader institutional trust in the approach.

Cost Pressure Shifts Inspections From Shutdown-Based to Live Streaming

Commodity price volatility forces operators to protect production uptime, so live-streamed inspections increasingly replace turnaround-centric methodologies. Remote ultrasonic crawlers and visual drones can acquire thickness, corrosion mapping, and crack growth data while pipelines, furnaces, and flare stacks remain fully operational. Avoiding a single mid-campaign shutdown in a petrochemical unit can prevent multi-million-dollar revenue loss, making the payback period for streaming hardware notably brief. Edge analytics boxes process waveforms on-site, then forward only compressed metadata to the cloud, reducing bandwidth costs and latency. This model also optimizes the use of skilled labor, as a single Level III analyst can oversee multiple geographically dispersed assets from a control room, thereby improving staff utilization and response times. The economic argument resonates most strongly where continuous-process units drive margin sensitivity, such as ammonia, ethylene, and base-metal smelters.

Stricter Safety Rules on Inaccessible Assets

Updated Occupational Safety and Health Administration confined-space rules increase the administrative burden and direct cost of manned entry, prompting asset owners to consider remotely operated crawlers, drones, and manipulators.[3]Occupational Safety and Health Administration, “Confined Space Rule Update,” osha.gov The International Maritime Organization likewise tightened inspection frequency for offshore installations, requiring more frequent evidence of structural integrity in splash-zone welds and conductor guides. Remote and digital NDT services mitigate fall, radiation, and drowning risks by eliminating physical exposure, thereby reducing workers’ compensation premiums. Insurance carriers have begun to offer discounts on policies when operators verify reduced human entry hours through authenticated inspection logs. Standard bodies, such as API 510 and ASME Section XI, now explicitly recognize remote ultrasonic and visual data under defined validation procedures, which accelerates compliance adoption at nuclear and petrochemical sites.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of certified NDT personnel skilled in data analytics | -1.3% | Global, particularly acute in North America and Europe | Medium term (2-4 years) |

| Cybersecurity concerns around the transmission of sensitive inspection data | -0.9% | Global, with a heightened focus on critical infrastructure sectors | Short term (≤ 2 years) |

| High upfront investment in sensor and robotic deployment infrastructure | -0.7% | Emerging markets and smaller operators | Short term (≤ 2 years) |

| Fragmented standards for data formats impede cross-platform interoperability | -0.5% | Global standardization challenge | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Certified NDT Personnel Skilled in Data Analytics

Remote workflows require technicians who can interpret phased-array waveforms, validate machine learning classifications, and manage cloud dashboards. The American Society for Nondestructive Testing identified a 35% shortfall in level II and level III personnel in 2024. Traditional classroom models require 18-24 months to reach dual competence in conventional flaw detection and advanced analytics, outpacing many service firms’ hiring cycles. Larger providers address the gap through internal academies, simulation-based e-learning, and augmented-reality job aids, yet smaller firms struggle to fund comparable curricula. Without sufficient skilled analysts, market growth can stall as contract backlogs lengthen and response times slip, especially during refinery turnarounds and power plant outages. Industry associations are lobbying for accelerated apprenticeships and remote proctoring of certification exams to widen the talent pipeline.

Cybersecurity Concerns Around Inspection Data Transmission

High-resolution radiographic files and corrosion maps are fed directly into integrity-management databases, which, if compromised, could expose plant vulnerabilities. The Cybersecurity and Infrastructure Security Agency issued strengthened industrial-control security guidance in 2024, urging asset owners to implement zero-trust network architecture and multi-factor authentication for inspection-data flows.[4]Cybersecurity and Infrastructure Security Agency, “ICS Security Guidelines,” cisa.gov Encryption, segmented networks, and strict key-management policies add incremental cost and complexity, particularly for smaller operators with limited information-technology staff. Insurers now require independent penetration tests before underwriting remote inspection systems, and some owners delay adoption until vendor cybersecurity credentials achieve ISO 27001 equivalence. While technology suppliers introduce built-in hardware roots of trust and secure-boot firmware, uncertainty around evolving threat vectors tempers the pace of roll-outs, especially in defense, nuclear, and water-utility assets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Ultrasonic Testing Underpins Digital Transformation

Ultrasonic techniques generated USD 1.04 billion in 2024, accounting for 28.6% of the remote and digital NDT services market share, as phased-array instruments can detect internal flaws with micron-scale resolution across steel, composite, and weld geometries. Digital coupling of phased-array probes with robotic crawlers lets inspectors map wall loss on live pipelines, boilers, and storage spheres at rates exceeding 2 m² per minute. The ability to stream raw A-scan data into cloud dashboards enables automated trending and thickness-loss forecasting that complies with risk-based inspection workflows. Remote visual inspection is expected to expand at a faster rate than any other service type, advancing at a 12.2% CAGR through 2030, as image-analysis algorithms classify pitting, cracking, and coating damage in real-time. Drones equipped with 4K cameras and stabilized gimbals can complete large-area surveys in a fraction of the person-hours previously required for rope access, scaffolding, or helicopter sorties. Radiographic testing retains niche importance for weld root defects in critical pressure circuits, while acoustic emission provides around-the-clock leak detection for pressure vessels. Electromagnetic methods, including eddy-current arrays and magnetic flux leakage, are utilized in aerospace and thin-wall heat-exchanger tubes, where non-contact operation is required. Hybrid multi-method platforms now integrate ultrasonic, electromagnetic, and visual modules on a single crawler, widening data correlation quality and minimizing deployment downtime.

Digital workflows enhance reporting efficiency: once crawlers complete a weld scan, auto-generated defect tables populate enterprise asset management systems within minutes, thereby shortening corrective action cycles. Proprietary time-of-flight diffraction algorithms further refine flaw sizing accuracy, meeting the stringent acceptance criteria of ASME Section VIII, Division 2. The expansion of oil and gas subsea inspection work scopes favors ultrasonic over radiographic methods due to radiation safety hurdles offshore. Simultaneously, power-plant operators adopt large-area corrosion mapping as thermal cycles and water chemistry variations accelerate wall thinning in heat-recovery steam generators. Sector diversification, from renewables to shipbuilding, underpins this segment’s revenue stability when hydrocarbon project pipelines fluctuate. Overall, ultrasonic workflows will continue to anchor vendor training, R and D spending, and edge analytics roadmap priorities over the forecast horizon.

By Service Delivery Mode: Digital Twins Gain Ground

Remote streaming and monitoring remained dominant, accounting for 34.5% of 2024 turnover, as it leverages existing supervisory control networks, requires minimal hardware retrofits, and delivers rapid uptime savings. Acoustic, strain, temperature, and guided-wave sensors feed high-frequency data to edge nodes, where on-board analytics flag anomalies and forward key metrics to cloud dashboards. Plant teams can then schedule targeted field verifications rather than blanket line-by-line checks, freeing scarce technicians for high-value tasks. Digital twin inspection, although smaller in absolute terms, is expected to post the fastest 14.2% CAGR through 2030, driven by simulation tools that reconcile historical ultrasonic runs with current load histories and material fatigue models. Asset owners derive particular benefit from chemical reactors, offshore jackets, and wind-turbine blades, where load paths are complex and failure modes are subtle.

Drone-based NDT advances rapidly as the Federal Aviation Administration expanded beyond-visual-line-of-sight permits for industrial campuses in 2024. New micro-ultrasonic transducers now mount under drone airframes, enabling thickness readings on flare stacks without shutdown. Robotic crawler systems address pipelines, risers, and long-distance scans of storage tank shells; autonomy software maps optimal routes, minimizes operator joystick time, and automatically returns to charge when battery levels dip below a threshold. Mixed-fleet inspection management suites coordinate the work of drones, crawlers, and tethered RVI robots in a unified scheduling engine. Operators evaluate delivery-mode choice against inspection window length, site access limits, and data-granularity needs, often blending modes in a single turnaround. Vendors that offer open application programming interfaces achieve higher platform stickiness because they enable digital teams to link inspection outputs to enterprise resource planning and maintenance management layers, thereby closing the loop between fault detection and work-order issuance.

By End-user Industry: Oil and Gas Remains Core

Oil and gas contributed 25.7% to the 2024 remote and digital NDT services market size, driven by the need for constant wall-thickness surveillance of pipeline mileage, offshore riser exposure, and midstream tankage to meet regulatory compliance requirements. Within exploration and production, unmanned subsea intervention reduces diver exposure and vessel day rates, making remote technologies readily fundable. Refiners also budget for crawlable phased-array mapping of crude distillation towers and catalytic crackers to mitigate hydrogen-induced cracking. Power generation represents the next largest slice because both conventional and renewable fleets depend on continuous inspection to prevent forced outages. Nuclear operators apply ultrasonic, eddy-current, and radiographic techniques under rigorous procedural controls, while utility-scale wind farm managers deploy drones and acoustic emission sensors to spot blade delamination.

The automotive industry is expected to expand at the fastest rate, with a 11.4% CAGR, driven by electric-vehicle battery inspection, laser ultrasonics for spot-weld quality assurance, and the validation of complex cast-aluminum chassis geometry. Aerospace and defense industries demand precision flaw detection in carbon-fiber composites and additive-manufactured metal components, driving the adoption of high-frequency phased arrays. Manufacturing and heavy engineering industries turn to digital NDT to validate the structural integrity of cranes, presses, and rolling mill components, while chemical and petrochemical operators focus on corrosion mapping in high-temperature, sour environments. The marine and shipbuilding segment integrates drone RVI inside double-hull tanks, reducing dry-dock days. Electronics and semiconductor plants use non-contact eddy-current coherence to check wafer and reticle carriers. Mining, medical devices, and other niche sectors provide incremental growth by requiring tailored inspection solutions for often remote or regulated environments, widening the vendor addressable market scope.

Geography Analysis

North America commanded 36.8% of 2024 revenue as stringent Department of Transportation pipeline rules, Nuclear Regulatory Commission guidance, and a mature energy infrastructure base foster early uptake of digital inspection. U.S. shale operators connect phased-array crawlers to cloud dashboards that integrate with SCADA, while Canadian oil sands producers deploy remote drones to measure tank-wall thickness in extreme cold. Regional service providers collaborate with leading universities to refine machine-learning defect libraries, accelerating the commercialization of new algorithms. Federal and state grants subsidize 5G deployment at industrial parks, lowering connectivity barriers for continuous streaming models.

The Asia-Pacific region is expected to register a 10.3% CAGR through 2030, outpacing all other regions. China’s Belt and Road infrastructure build-out—spanning refineries, pipelines, and high-speed rail—requires asset integrity solutions that scale geographically and support multilingual reporting. India’s production-linked incentive manufacturing program prompts automotive, electronics, and chemical plants to embed in-line inspection during start-up, bypassing legacy shutdown-heavy maintenance cultures. Japan and South Korea emphasize digital NDT in nuclear safety and semiconductor fabs, respectively, both of which tolerate near-zero downtime. Regional policy packages tied to Industry 4.0 adoption offer fiscal incentives for inspection automation, enabling local service firms to offset the high capital costs of advanced crawlers and drones.

Europe is experiencing steady growth driven by decarbonization imperatives and the rapid construction of offshore wind farms. The European Commission’s Green Deal calls for the life extension of existing industrial assets to minimize embodied carbon, making continuous remote inspection an attractive compliance tool. Germany applies phased-array corrosion mapping in hydrogen-ready gas pipelines, while the United Kingdom deploys robotic RVI on North Sea platforms to manage late-life assets. Nordic nations focus on hydropower penstock thickness trending, integrating acoustic emission sensors that transmit through rock tunnels. Southern European petrochemical hubs, although smaller, outsource inspection tasks to multinational vendors who integrate cloud analytics into their existing enterprise systems.

Competitive Landscape

The sector remains moderately fragmented. Traditional inspection houses, such as MISTRAS Group, Applus Services, and Bureau Veritas, have upgraded their portfolios with cloud analytics and edge connectivity, helping customers unify legacy ultrasonic and real-time streaming data. Technology-first players, such as Eddyfi Technologies, Waygate Technologies, and Oceaneering International, differentiate themselves through proprietary probes, robotics, and artificial intelligence stacks that automate the classification of flaws. Mid-tier specialists offer domain depth in niches such as composite airframes or subsea risers, often partnering with digital-platform vendors to deliver hybrid service bundles.

Strategic alliances drive innovation velocity. Bureau Veritas integrates Microsoft Azure machine-learning services into its AIMS3D platform, offering predictive models that flag abnormal corrosion rates in chemical reactors within minutes of data upload. Waygate leverages its Inspection Works ecosystem to combine 3D data from computed tomography, phased array, and visual modalities in a single dashboard, shortening report cycles from days to hours. MISTRAS Group invests in robotic fleet acquisitions that expand its reach in offshore renewables, complementing its legacy expertise in acoustic emissions.

Patent activity underscores competitive intensity. The United States Patent and Trademark Office logged a 40% year-on-year rise in remote crawler designs and sensor fusion algorithms in 2024. Vendors vie for intellectual property that enhances the probability of detection metrics under POD trials mandated by regulators. Pricing competition remains balanced; larger firms win multi-year, integrated contracts, while smaller entrants secure spot projects that demand uncommon probe geometries or rapid mobilization. Customers weigh vendor choice against cybersecurity posture, solution openness, and ability to deliver certified personnel amid persistent labor shortages.

Remote & Digital NDT Services Industry Leaders

Applus Services SA

MISTRAS Group Inc.

TEAM Inc.

Bureau Veritas SA

TUV Rheinland AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: MISTRAS Group announced a USD 45 million acquisition of a European robotic inspection specialist to expand automated NDT capabilities for offshore wind farms.

- August 2025: Waygate Technologies launched an integrated digital twin platform that merges real-time NDT data with predictive analytics to cut inspection costs by up to 35%.

- July 2025: Eddyfi Technologies secured a USD 25 million contract to deploy remote ultrasonic inspection across 500 kilometers of pipeline.

- June 2025: Bureau Veritas partnered with Microsoft Azure to deliver cloud-based NDT analytics using artificial intelligence.

Global Remote & Digital NDT Services Market Report Scope

| Remote Visual Inspection (RVI) Services |

| Ultrasonic Testing Services |

| Radiographic Testing Services |

| Acoustic Emission Monitoring Services |

| Electromagnetic Testing Services |

| Other Digital NDT Services |

| Remote Streaming and Monitoring |

| Digital Twin-based Inspection |

| Drone-based NDT |

| Robotic Crawler NDT |

| Oil and Gas |

| Power Generation |

| Aerospace |

| Defense |

| Automotive and Transportation |

| Manufacturing and Heavy Engineering |

| Construction and Infrastructure |

| Chemical and Petrochemical |

| Marine and Ship Building |

| Electronics and semiconductor |

| Mining |

| Medical Devices |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| South-East Asia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Service Type | Remote Visual Inspection (RVI) Services | |

| Ultrasonic Testing Services | ||

| Radiographic Testing Services | ||

| Acoustic Emission Monitoring Services | ||

| Electromagnetic Testing Services | ||

| Other Digital NDT Services | ||

| By Service Delivery Mode | Remote Streaming and Monitoring | |

| Digital Twin-based Inspection | ||

| Drone-based NDT | ||

| Robotic Crawler NDT | ||

| By End-user Industry | Oil and Gas | |

| Power Generation | ||

| Aerospace | ||

| Defense | ||

| Automotive and Transportation | ||

| Manufacturing and Heavy Engineering | ||

| Construction and Infrastructure | ||

| Chemical and Petrochemical | ||

| Marine and Ship Building | ||

| Electronics and semiconductor | ||

| Mining | ||

| Medical Devices | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the remote and digital NDT services market?

The market is valued at USD 3.63 billion in 2025, with a forecasted growth to USD 5.38 billion by 2030.

Which service type holds the largest share?

Ultrasonic testing services lead with 28.6% of 2024 revenue due to versatility across metals and composites.

Which delivery mode is expanding the fastest?

Digital twin-based inspection is projected to grow at a 14.2% CAGR between 2025 and 2030 as simulation tools gain traction.

Why is Asia-Pacific the fastest-growing region?

Rapid industrialization, government Industry 4.0 incentives, and large infrastructure programs combine to drive a 10.3% CAGR in the region.

How are safety regulations influencing adoption?

Updated OSHA confined-space rules and stricter offshore standards encourage remote inspections to minimize human exposure while maintaining compliance.

What skills gap challenges the sector?

A 35% shortage of Level II and Level III NDT personnel skilled in data analytics hinders project deployment and fuels wage inflation.

Page last updated on: