Rehabilitation Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

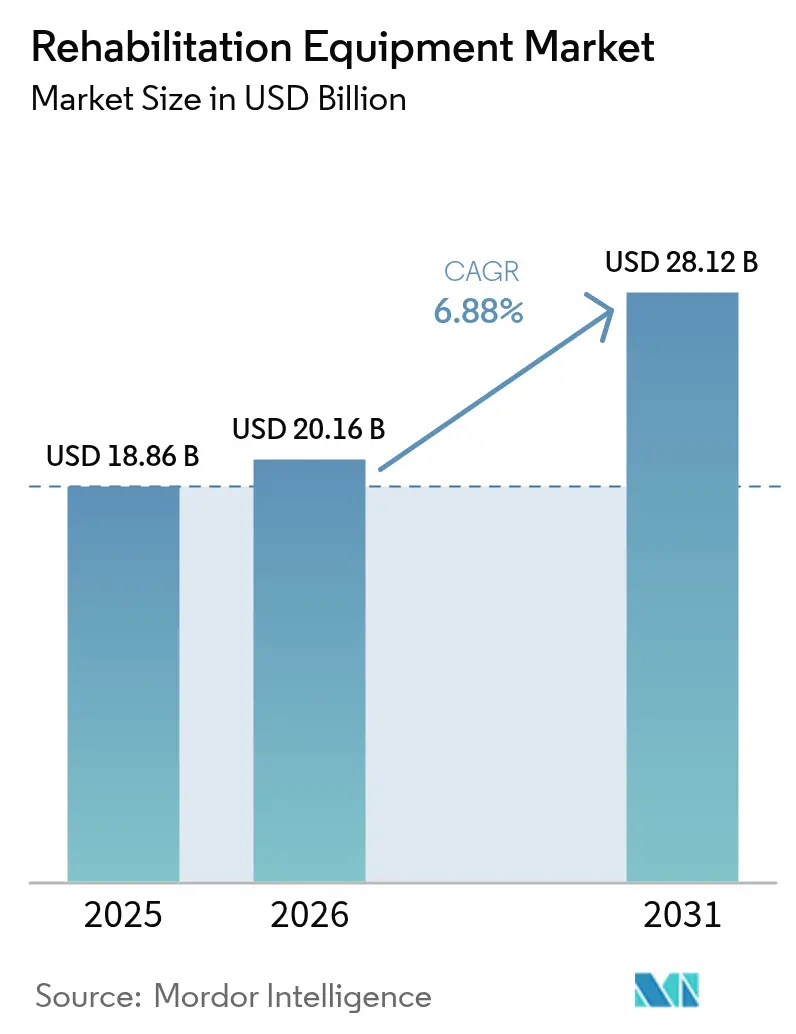

| Market Size (2026) | USD 20.16 Billion |

| Market Size (2031) | USD 28.12 Billion |

| Growth Rate (2026 - 2031) | 6.88% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rehabilitation Equipment Market Analysis by Mordor Intelligence

The rehabilitation equipment market size expanded to USD 18.86 billion in 2025, is estimated to reach USD 20.16 billion in 2026, and is projected to grow to USD 28.12 billion by 2031, registering a CAGR of 6.88% between 2026 and 2031. The growing prevalence of chronic diseases, rapid population aging, and payment reforms that reward improvements in functional outcomes are driving demand away from bulky, facility-bound devices toward connected, portable solutions. At the same time, ambulatory surgery centers, hospital-at-home programs, and remote monitoring codes are fragmenting the traditional care pathway, increasing the urgency for equipment that works across settings. Robotics, artificial intelligence, virtual reality, and sensor miniaturization are redefining product design priorities, tilting capital toward platforms that generate actionable data for clinicians and payers. Competitive boundaries are blurring as consumer electronics firms embed health sensors into mobility aids, while established durable medical equipment suppliers bolster digital capabilities through acquisitions and partnerships. Capital budgets remain tight, but leasing, pay-per-session, and reimbursement expansions for advanced devices are beginning to ease adoption hurdles in high-volume practices.

Key Report Takeaways

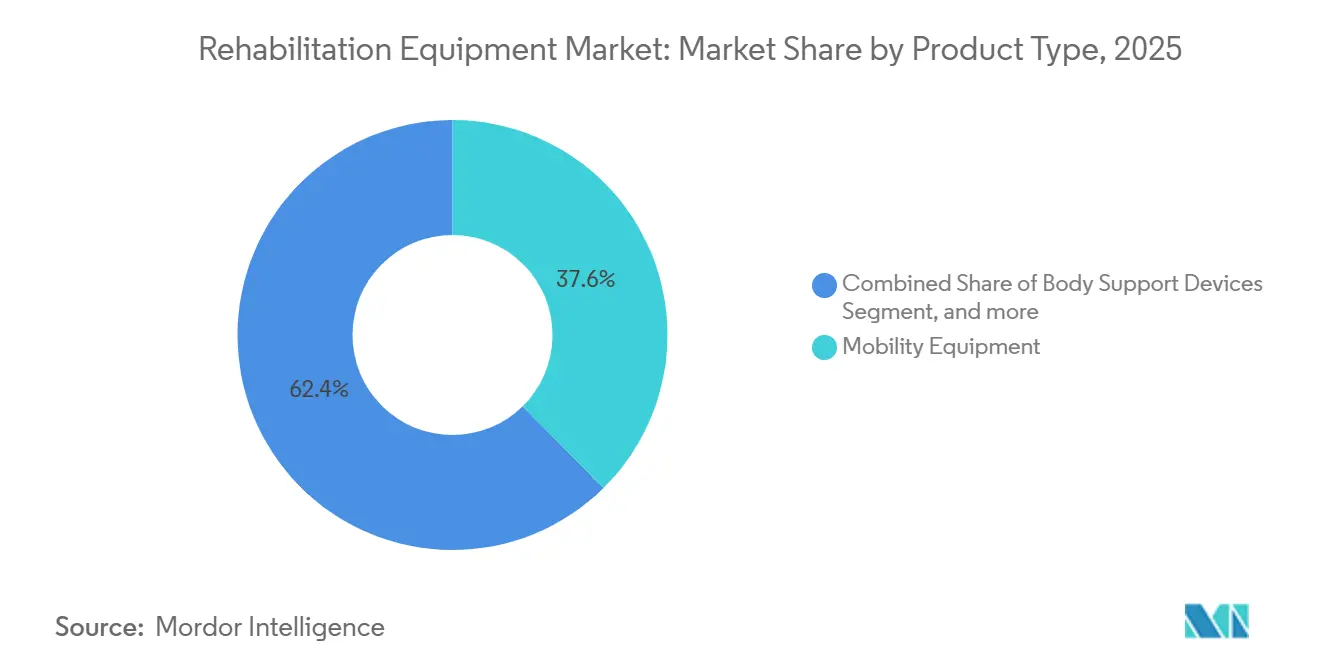

- By product type, mobility equipment led with 37.55% rehabilitation equipment market share in 2025, whereas robotic and smart systems are forecast to expand at a 12.85% CAGR through 2031.

- By application, physiotherapy accounted for 50.53% of the rehabilitation equipment market in 2025, while neuro-rehabilitation is projected to grow at a 10.75% CAGR through 2031.

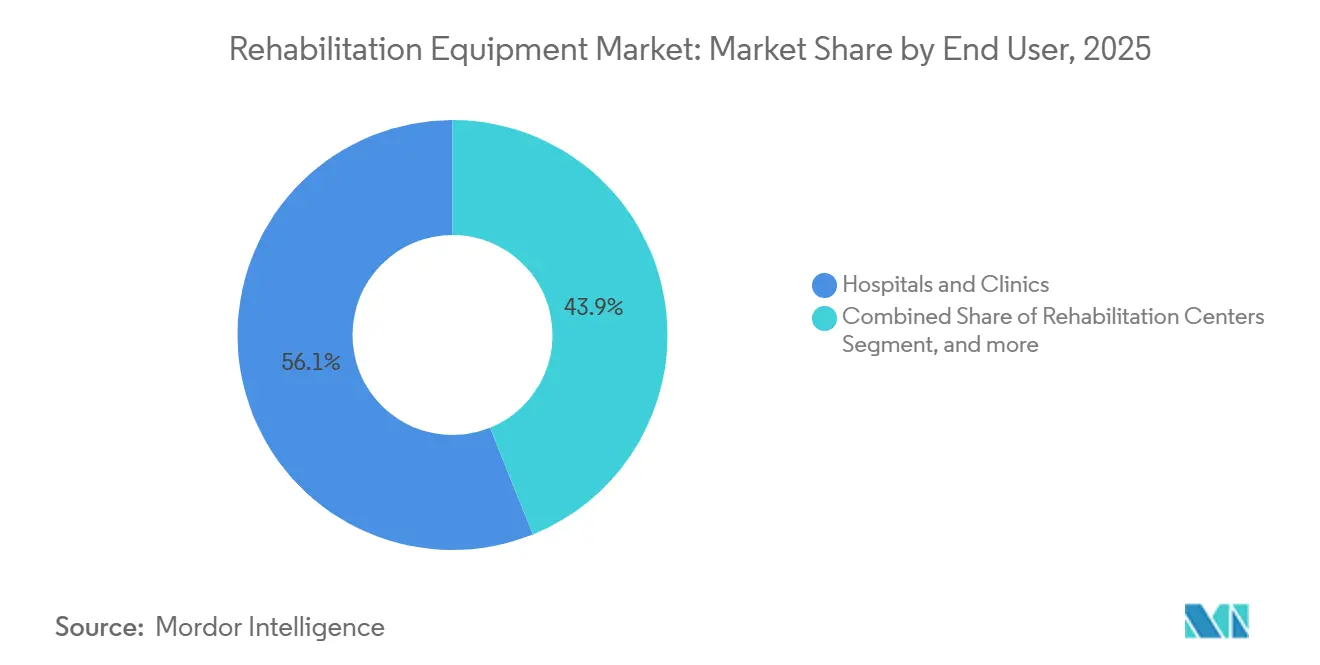

- By end user, hospitals held a 56.15% share of the rehabilitation equipment market in 2025, yet home-care settings recorded the highest projected CAGR of 11.82% during 2026-2031.

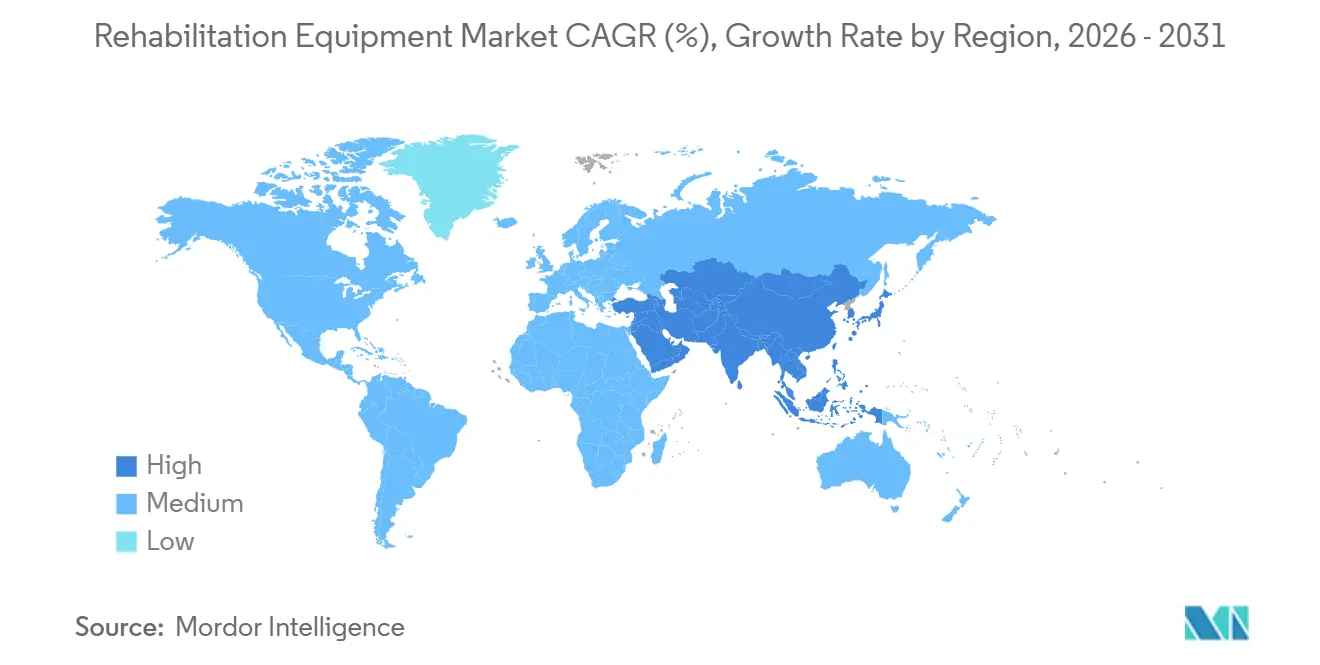

- By geography, North America commanded 42.52 of % rehabilitation equipment market share in 2025, although Asia-Pacific shows the fastest momentum with a 9.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rehabilitation Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth of Post-Acute and Chronic-Disease Rehabilitation Demand | +1.8% | Global, strongest in North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Rising Adoption of AI-Powered and Robotic Exoskeleton Devices | +2.1% | North America, European Union, Japan, South Korea, Australia | Long term (≥ 4 years) |

| Expansion of Home-Based Tele-Rehabilitation Ecosystems | +1.5% | North America, Western Europe, China, India | Short term (≤ 2 years) |

| Surge in Ambulatory Surgery Centers Driving Portable Device Uptake | +1.2% | United States, Canada, Germany, United Kingdom | Medium term (2-4 years) |

| Integration of VR And Gamified Therapy Boosting Adherence | +0.9% | United States, Japan, Germany, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of Post-Acute and Chronic-Disease Rehabilitation Demand

Hospitals are discharging patients sooner, shifting recovery workloads onto skilled nursing facilities, outpatient clinics, and homes. Stroke remains a pivotal public health concern, with roughly 795,000 annual events in the United States alone, each requiring months of intensive therapy[1]American Heart Association, “Stroke Facts,” heart.org. Orthopedic cases add volume, as hip and knee replacements climb among aging adults across developed markets. Diabetes, COPD, and heart failure add steady demand, since supervised exercise and education lower mortality by up to 30%[2]Journal of the American College of Cardiology, “Cardiac Rehabilitation and Mortality Reduction in Heart Failure,” jacc.org. Value-based payment models reward fewer readmissions, pushing providers to adopt equipment that accelerates mobility gains and measures progress. Together, these factors are driving the rehabilitation equipment market toward data-rich devices that demonstrate improved outcomes.

Rising Adoption of AI-Powered and Robotic Exoskeleton Devices

FDA clearances and emerging billing codes are shifting exoskeletons from research labs to clinics. Ekso NR received U.S. clearance in 2024, enabling data-guided gait therapy that improves weight-bearing symmetry[3]U.S. Food and Drug Administration, “510(k) Premarket Notification Database,” fda.gov. Lifeward reported a 40% increase in hospital uptake for ReStore after Medicare introduced a dedicated G-code reimbursing up to USD 150 per session[4]Lifeward, Inc., “Form 10-K 2024,” sec.gov. Japan widened nursing-care insurance in 2025 to subsidize exoskeleton rentals, reducing caregiver injuries. AI algorithms now adjust resistance in real time, extending therapy sessions while lowering therapist fatigue. As batteries shrink and component prices fall, small centers and even select home programs begin leasing units, widening the footprint of the rehabilitation equipment market.

Expansion of Home-Based Tele-Rehabilitation Ecosystems

Remote Patient Monitoring codes, expanded by CMS in 2024, allow connected devices to transmit range-of-motion, adherence, and pain data directly to therapists. A 2025 peer-reviewed study found that connected equipment users achieved 85% exercise adherence, compared with 60% for standard programs, and posted 15% higher functional gains. Medicare Advantage plans are scaling hospital-at-home benefits and bundling rehabilitation equipment into care packages to cut skilled nursing utilization. These trends boost demand for sensor-based bands, pedal exercisers, and lightweight walkers, solidifying the rehabilitation equipment market in living rooms and rural communities.

Surge in Ambulatory Surgery Centers Driving Portable Device Uptake

ASC procedure volume in the United States rose 8% in 2025, with joint replacements the fastest-growing category. Patients leave the same day and need devices within 24 hours, creating a premium on lightweight walkers, continuous passive motion machines, and battery-powered electrotherapy units. Germany’s statutory insurers now reimburse portable NMES devices immediately after orthopedic surgery, linking early muscle activation to lower disability claims. Rapid feedback loops between patients and suppliers shorten product iteration cycles, channeling more innovation into user-friendly form factors that strengthen the rehabilitation equipment market.

Restraints Impact Analysis*

| Restraint | (`) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront and Lifecycle Costs for Advanced Robotic Systems | -1.3% | Global, sharpest in emerging markets and small facilities | Medium term (2-4 years) |

| Fragmented Reimbursement for Home and Digital Therapies | -0.9% | United States, Europe, Latin America, Southeast Asia | Short term (≤ 2 years) |

| Limited Therapist Skill Sets for Multidisciplinary Tech Integration | -0.7% | Rural North America, Eastern Europe, developing Asia-Pacific | Medium term (2-4 years) |

| Low Awareness and Access in Rural and Low-Income Areas | -0.6% | Sub-Saharan Africa, South Asia, remote North America, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront and Lifecycle Costs for Advanced Robotic Systems

Acquisition prices of USD 75,000–150,000 plus 10–15% annual service fees challenge hospitals contending with thin operating margins. A 2024 American Hospital Association survey found that 62% of U.S. facilities delayed capital purchases amid higher interest expenses. Smaller centers rarely treat the 15–20 weekly patients required to break even within five years. Import duties and weak service networks further inflate costs in emerging markets. Leasing shifts expenditure to operating budgets but still demands utilization guarantees, moderating near-term growth in the rehabilitation equipment market.

Fragmented Reimbursement for Home and Digital Therapies

Only 38% of U.S. commercial plans covered app-based therapy or connected devices in 2025. Europe varies: Germany reimburses approved DiGA apps, whereas the United Kingdom restricts most devices to hospital discharge pathways. Navigating dozens of payer-specific codes slows launches and raises administrative overhead. Out-of-pocket costs deter adoption among lower-income patients, leaving portions of the rehabilitation equipment market untapped despite technological readiness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Robotic Systems Outpace Traditional Aids

Robotic and smart systems are set to expand at a 12.85% CAGR through 2031, nearly double the overall rehabilitation equipment market. Mobility equipment retained a 37.55% share in 2025, underscoring durable demand for manual and powered wheelchairs. Manual chairs remain volume leaders for short-term needs, while powered variants gain ground as insurers now fund advanced seating that prevents pressure sores. Daily living aids such as smart beds with weight sensors alert caregivers to unassisted exits, lowering fall risk and extending independent living. Exercise equipment is evolving into connected platforms that gamify motion and feed adherence metrics to therapists.

Robotic exoskeletons, gait trainers, and upper-limb robots are shifting momentum. A 2025 meta-analysis recorded 18% greater motor recovery in stroke patients receiving robotic-assisted therapy compared with matched conventional doses. With clinical evidence accumulating, payers are opening dedicated billing codes, positioning robotics to capture a growing share of the rehabilitation equipment market by 2031. Traditional suppliers are responding through joint ventures and acquisitions aimed at embedding AI modules into wheelchairs, lifts, and beds, signaling an era where software usability competes with mechanical durability.

By Application: Neuro-Rehabilitation Gains Momentum

Physiotherapy accounted for 50.53% of the rehabilitation equipment market in 2025, reflecting its broad scope across musculoskeletal injuries and chronic pain. Equipment ranges from resistance bands to isokinetic dynamometers and remains well reimbursed. Neuro-rehabilitation is climbing at a 10.75% CAGR, propelled by rising stroke survival rates and traumatic brain injury protocols that apply constraint-induced movement and brain-computer interfaces.

New brain-stimulation devices cleared by the FDA in 2025 expand therapist toolkits, while NIH earmarked USD 120 million for neuro-tech R&D that same year. The occupational therapy and geriatric rehabilitation segments are adding incremental growth through adaptive devices and fall-prevention systems designed for aging populations. Cardiopulmonary rehabilitation leverages treadmills and respiratory trainers to reduce readmissions, with 25% lower five-year mortality documented among program completers. Diversifying clinical evidence cements multi-disciplinary equipment portfolios, broadening the rehabilitation equipment market beyond core physiotherapy.

By End User: Home-Care Settings Accelerate

Hospitals and clinics commanded 56.15% of the rehabilitation equipment market share in 2025, buttressed by capital-intensive gear such as hydrotherapy pools and robotic gait trainers that deliver high throughput. Yet home-care settings are advancing at an 11.82% CAGR, energized by hospital-at-home waivers and direct-to-consumer e-commerce. Portable ultrasound, wearable gait sensors, and tablet-based exercise games now ship directly to living rooms, where therapists monitor compliance via cloud dashboards.

Ambulatory surgery centers strengthen this shift, discharging orthopedic patients on the same day and prescribing lightweight walkers and electrotherapy units that arrive before anesthesia wears off. Rehabilitation centers maintain relevance by bundling multi-disciplinary services under one roof, but their device choices increasingly mirror home-care priorities such as wireless connectivity and app-based coaching. Taken together, these trends disperse rehabilitation equipment market growth across settings, reducing reliance on any single channel.

Geography Analysis

North America preserved 42.52 of % rehabilitation equipment market share in 2025, led by the United States, where Medicare Advantage enrollment reached 31 million and bundled rehabilitation benefits encourage adoption of powered wheelchairs and connected exercise gear. Canada’s provincial formularies fund mobility aids, while its tele-rehabilitation pilots bridge therapist gaps in rural zones. A competitive mix of legacy suppliers and robotics start-ups operates through hospital GPO contracts, home-health agencies, and direct web sales.

Europe exhibits diverse reimbursement climates. Germany updated its Hilfsmittelverzeichnis in 2024 to include exoskeletons, enabling statutory coverage when evidence shows they outperform conventional therapy. The United Kingdom grapples with budget ceilings, favoring lower-cost connected exercise equipment for community rehab teams. France covers up to 100% of device costs depending on severity, stimulating demand for smart beds and adaptive bathrooms. Spain and Italy witness private centers offering VR therapies ahead of public adoption. The Medical Device Regulation’s stringent evaluation rules encourage consolidation, nudging small manufacturers toward partnerships.

Asia-Pacific leads in growth at a 9.12% CAGR. China’s plan to open 10,000 rehabilitation hospitals by 2030 subsidizes 50–70% of qualifying equipment purchases. Japan’s 2025 nursing-care reforms hike payments for robotic lifts to mitigate caregiver strain. India’s Production Linked Incentive scheme supports domestic manufacturing, though the market still favors imported mid-range devices. Australia and South Korea exploit high broadband penetration to deploy tele-rehabilitation, while Middle East, Africa, and South America progress steadily through medical tourism and private hospital expansion. Across regions, localized manufacturing incentives and digital-health investments will continue to diversify rehabilitation equipment market demand patterns.

Competitive Landscape

The rehabilitation equipment market remains moderately fragmented. Invacare, Permobil, and Sunrise Medical collectively hold a commanding position in manual and powered wheelchairs, bolstered by nationwide servicing and durable reputations. Arjo and Baxter leverage critical-care footprints to cross-sell patient lifts and smart beds under bundled contracts. Robotics specialists such as Ekso Bionics and Lifeward secured 2024-2025 FDA clearances, enabling them to target neuro-rehabilitation units willing to invest over USD 100,000 per system. Ekso’s 2025 patent for AI gait analysis that tweaks resistance based on electromyography signals highlights a pivot from hardware exclusivity to software defensibility.

Consumer electronics giants like Samsung and Xiaomi are putting pressure by embedding fall detection and vitals monitoring in walking aids and bathroom supports. ISO 13482 and IEC 60601-1 safety standards raise compliance costs, favoring firms with established regulatory teams. Strategic alliances multiply, pairing device makers with health IT vendors to feed rehabilitation data into electronic records, thereby locking in provider workflows. Looking ahead, suppliers lacking digital ecosystems risk share erosion as the rehabilitation equipment market rewards outcome-verified, data-driven platforms

Rehabilitation Equipment Industry Leaders

Medline Industries, Inc

Drive DeVilbiss Healthcare

Invacare Corporation

Permobil

Sunrise Medical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Ekso Bionics became the exclusive U.S. distributor of MediTouch’s BalanceTutor system, adding an evidence-backed balance trainer to its neuro-rehabilitation portfolio.

- December 2025: Sunrise Medical acquired Ergoflix, a German leader in premium foldable power wheelchairs, expanding its European direct-to-consumer reach.

Global Rehabilitation Equipment Market Report Scope

As per the report scope, rehabilitation equipment refers to a broad range of devices designed to assist individuals in recovering physical function, mobility, and strength following injury, illness, or surgery. It includes therapeutic tools, mobility aids, exercise and strength‑training systems, and daily‑living support devices. These products help improve patient independence, enhance functional outcomes, and support long‑term rehabilitation across clinical, home‑care, and community settings.

The rehabilitation equipment market is segmented by product type, application, end-user, and geography. By product type, the market is segmented into daily living aids (medical beds, bathroom and toilet assist devices, reading, writing and computer aids, and other daily living aids), mobility equipment (walking assist devices and wheelchairs and scooters), exercise equipment (upper body exercise equipment and lower body exercise equipment), body support devices (patient lifts and medical lifting slings), and robotic & smart rehabilitation systems. By application, the market is segmented into physiotherapy, occupational therapy, neuro-rehabilitation, cardiopulmonary rehabilitation, and geriatric rehabilitation. By end user, the market is segmented into hospitals, rehabilitation centers, home-care settings, and ambulatory surgical centers. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Daily Living Aids | Medical Beds |

| Bathroom & Toilet Assist Devices | |

| Reading, Writing & Computer Aids | |

| Other Daily Living Aids | |

| Mobility Equipment | Walking Assist Devices |

| Manual Wheelchairs | |

| Powered Wheelchairs & Mobility Scooters | |

| Exercise Equipment | Upper-body Exercise Equipment |

| Lower-body Exercise Equipment | |

| Body Support Devices | Patient Lifts |

| Medical Lifting Slings | |

| Robotic & Smart Rehabilitation Systems |

| Physiotherapy |

| Occupational Therapy |

| Neuro-rehabilitation |

| Cardiopulmonary Rehabilitation |

| Geriatric Rehabilitation |

| Hospitals |

| Rehabilitation Centers |

| Home-care Settings |

| Ambulatory Surgical Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Daily Living Aids | Medical Beds |

| Bathroom & Toilet Assist Devices | ||

| Reading, Writing & Computer Aids | ||

| Other Daily Living Aids | ||

| Mobility Equipment | Walking Assist Devices | |

| Manual Wheelchairs | ||

| Powered Wheelchairs & Mobility Scooters | ||

| Exercise Equipment | Upper-body Exercise Equipment | |

| Lower-body Exercise Equipment | ||

| Body Support Devices | Patient Lifts | |

| Medical Lifting Slings | ||

| Robotic & Smart Rehabilitation Systems | ||

| By Application | Physiotherapy | |

| Occupational Therapy | ||

| Neuro-rehabilitation | ||

| Cardiopulmonary Rehabilitation | ||

| Geriatric Rehabilitation | ||

| By End-User | Hospitals | |

| Rehabilitation Centers | ||

| Home-care Settings | ||

| Ambulatory Surgical Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How big will rehabilitation equipment spending be by 2031?

The rehabilitation equipment market size is forecast to reach USD 28.12 billion by 2031, growing at a 6.88% CAGR from 2026 through 2031.

Which product segment is growing the fastest?

Robotic and smart rehabilitation systems are projected to expand at a 12.85% CAGR, more than double the overall market pace to 2031.

What drives home-care demand for rehabilitation devices?

Hospital-at-home programs, Medicare Advantage benefits, and remote monitoring codes enable patients to receive therapy at home, lifting home-care equipment growth to an 11.82% CAGR.

Which region will add the most new revenue?

Asia-Pacific shows the strongest momentum, advancing at a 9.12% CAGR thanks to China's eldercare build-out, Japan's nursing-care reforms, and India's manufacturing incentives.

How much do robotic exoskeletons cost and who pays?

Units typically list between USD 75,000 and USD 150,000, with leasing options rising; coverage now exists through Medicare G-codes, Japan's nursing-care insurance, and select European funds.

Page last updated on: