Glaucoma Surgery Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

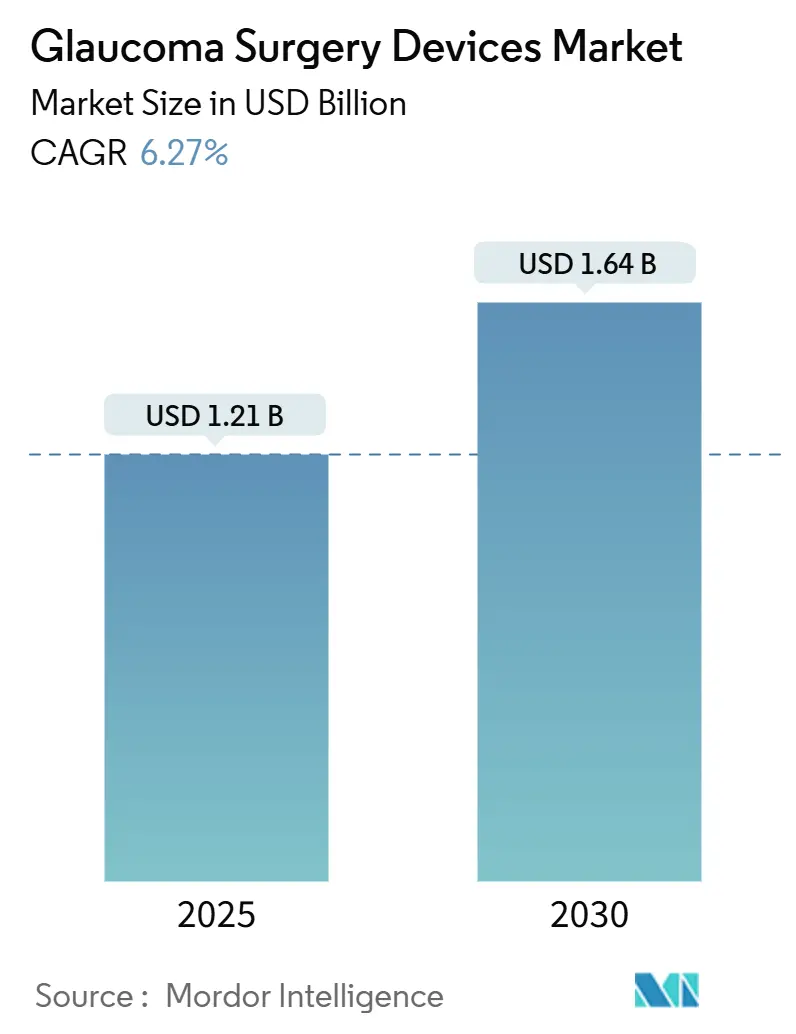

| Market Size (2025) | USD 1.21 Billion |

| Market Size (2030) | USD 1.64 Billion |

| Growth Rate (2025 - 2030) | 6.27% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

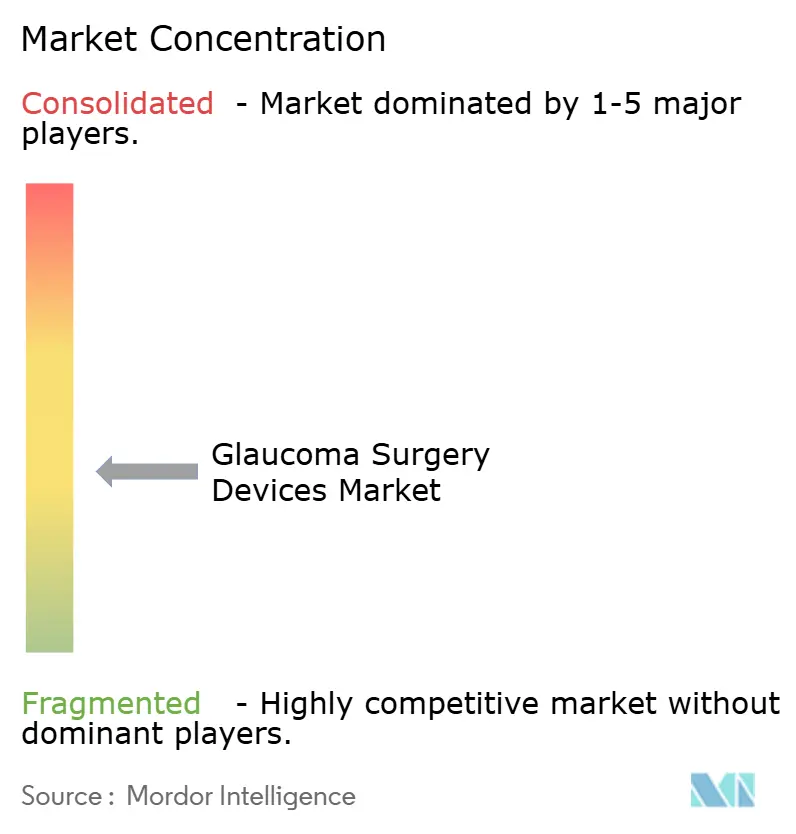

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Glaucoma Surgery Devices Market Analysis by Mordor Intelligence

The Glaucoma Surgery Devices Market size is estimated at USD 1.21 billion in 2025, and is expected to reach USD 1.64 billion by 2030, at a CAGR of 6.27% during the forecast period (2025-2030).

Momentum is driven by the rapid adoption of minimally invasive technologies, the growing pool of glaucoma patients, and increased access to surgery in many low- and middle-income economies. Technological advancements—especially automated laser systems and artificial intelligence-guided microsurgery—are increasing procedure volumes in ophthalmology clinics and ambulatory surgery centers. Globally, 4.22 million adults in the United States alone are living with glaucoma, with 1.49 million facing vision-threatening disease, underscoring the urgent need for modern surgical options. Surgeons increasingly favor devices that shorten operating time, decrease adverse events, and cut patients’ reliance on topical medication. Intense rivalry among innovators such as Alcon, Glaukos, and Sight Sciences is fueling product launches, patent litigation, and targeted regional expansions as each player vies for a larger share of the glaucoma surgery devices market.

Key Report Takeaways

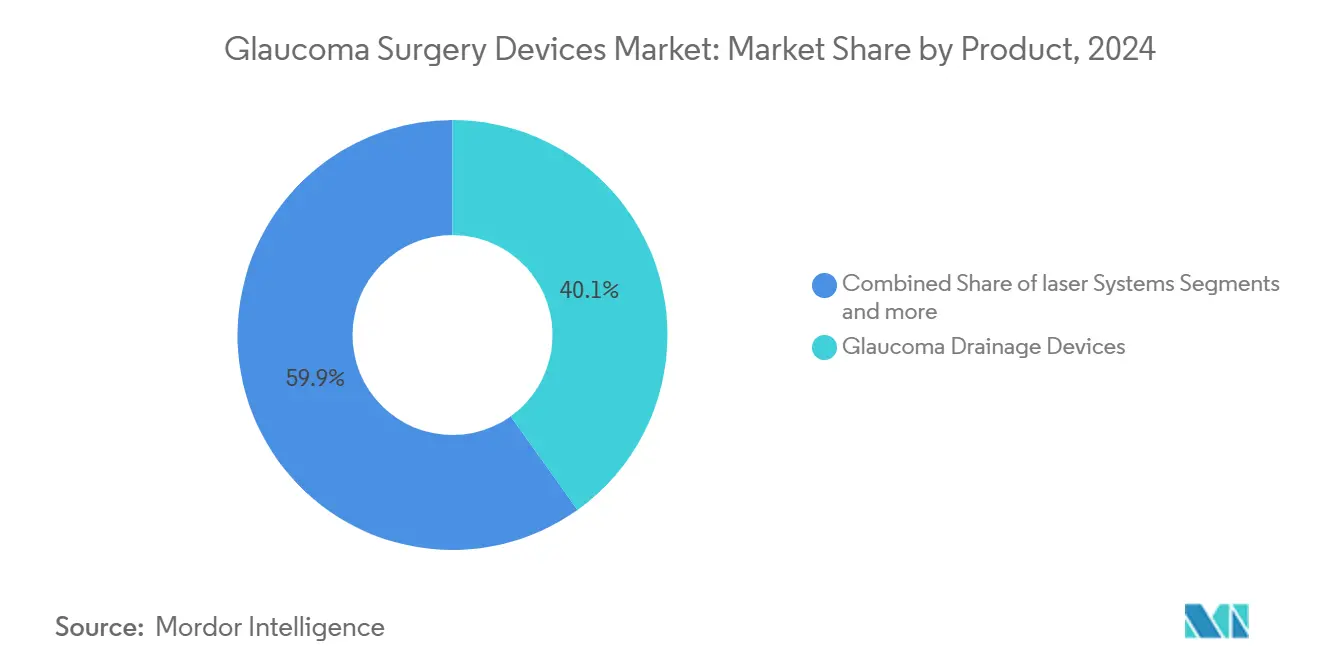

- By product type, glaucoma drainage devices contributed 40.12% of glaucoma surgery devices market share in 2024; laser systems are projected to advance at a 6.92% CAGR between 2025-2030.

- By surgery method, minimally invasive glaucoma surgery held 47.23% of the glaucoma surgery devices market share in 2024, while laser surgery is slated to post the fastest 6.89% CAGR through 2030.

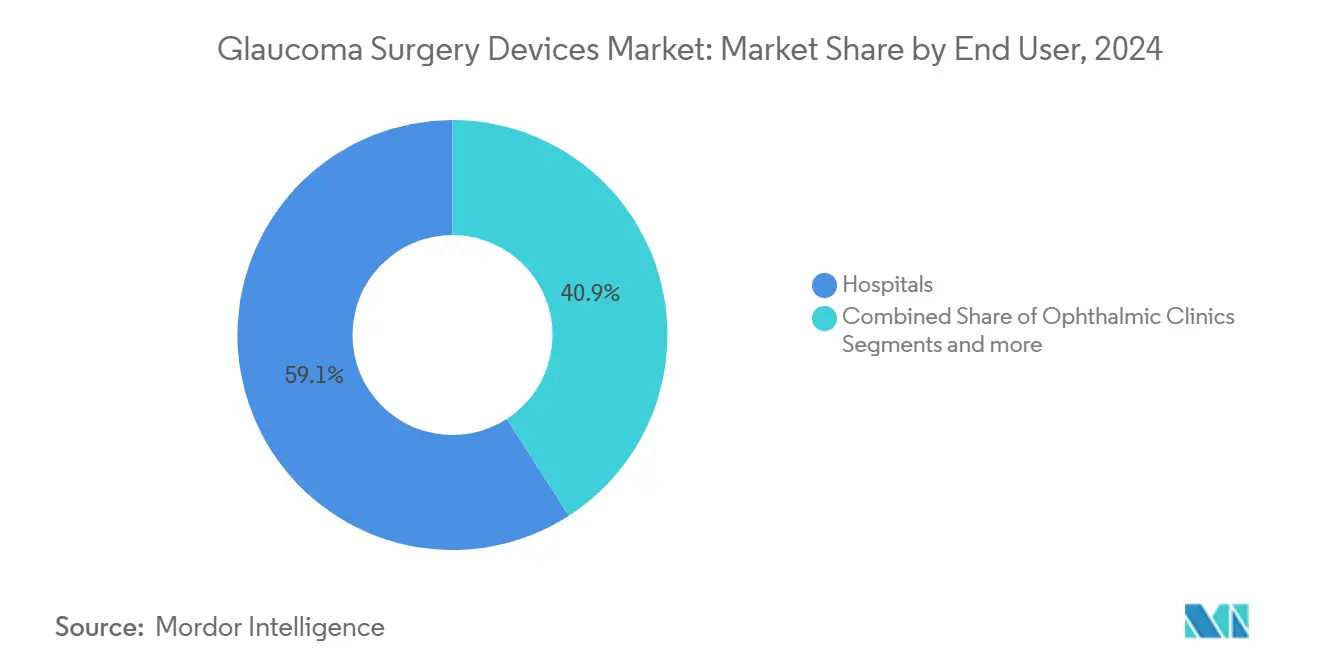

- By end user, hospitals controlled 59.12% of the glaucoma surgery devices market size in 2024, yet ophthalmic clinics are on track to register a 7.03% CAGR during the forecast window.

- By glaucoma type, primary glaucoma dominated with 80.14% share of the glaucoma surgery devices market size in 2024; secondary glaucoma is poised to expand at a 6.98% CAGR up to 2030.

- Geographically, North America led with 37.67% revenue share in 2024, whereas Asia-Pacific is the fastest-growing region at 7.14% CAGR toward 2030.

Global Glaucoma Surgery Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of glaucoma | +1.8% | Global; highest in Asia-Pacific | Long term (≥ 4 years) |

| Increasing geriatric population | +1.5% | Global; most pronounced in developed economies | Long term (≥ 4 years) |

| Growing adoption of surgical treatments | +1.2% | North America & EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Accelerated regulatory approvals for MIGS | +0.9% | North America & EU first, then global | Short term (≤ 2 years) |

| AI-assisted intra-operative imaging | +0.6% | High-income technology hubs | Medium term (2-4 years) |

| ASC reimbursement parity for MIGS | +0.7% | United States first, spreading internationally | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Glaucoma

New epidemiology indicates that 4.22 million U.S. adults carry a glaucoma diagnosis, equating to a 1.62% prevalence rate across adults aged 18 years or older[1]Steven Mansberger et al., “Prevalence of Glaucoma in the United States,” JAMA Ophthalmology, jamanetwork.com . In the United States, non-Hispanic Black adults show a 3.15% prevalence versus 1.42% among non-Hispanic White adults, pushing device makers to tailor outreach programs and design studies that reflect racially diverse disease patterns[2]University of Michigan Kellogg Eye Center, “Racial Disparities in Glaucoma,” umich.edu . The Asia-Pacific region shoulders almost 60% of global glaucoma cases, underscoring the urgency for affordable, high-volume surgical solutions. As the incidence climbs, procurement officials in public hospitals view MIGS as a cost-effective option to reduce lifetime medication costs and improve long-term vision retention. This epidemiological pressure is reshaping the glaucoma surgery devices market as suppliers prioritize higher-burden regions for direct distribution and local manufacturing.

Increasing Geriatric Population

Worldwide, populations aged 65 years and above are expanding faster than any other cohort, and glaucoma incidence rises sharply beyond age 60. Developed nations already have infrastructure that supports advanced micro-devices, yet rapidly aging middle-income countries now encounter similar disease loads without comparable specialist density. Health systems acknowledge that moving patients to earlier surgical care mitigates the cumulative burden of topical therapy and follow-up visits, leading to policy shifts that elevate cataract-combined MIGS procedures[3]Glaucoma Research Foundation, “Aging and Glaucoma,” glaucoma.org . In geriatric eyes, minimally invasive implants produce fewer inflammatory complications than trabeculectomy, allowing quicker visual rehabilitation. The demographic surge, therefore, sustains procedure demand even in markets where adoption appeared to be saturated.

Growing Adoption of Surgical Treatments

Clinical evidence has repositioned surgical intervention as a first- or second-line strategy. The LIGHT trial demonstrated that selective laser trabeculoplasty is superior to eye drops for newly diagnosed patients, prompting revisions to guidelines in Europe and North America. Medicare’s separate payment for standalone MIGS and laser procedures expanded surgeon willingness to intervene sooner, lifting case volumes in outpatient suites. Training curricula now embed MIGS into resident programs, lowering the technical barrier for widespread use. Automated devices, such as Alcon’s Voyager DSLT, shorten learning curves by replacing manual aiming with algorithmic targeting, thereby encouraging broader adoption in community ophthalmology centers. Collectively, these shifts translate into higher unit sales for state-of-the-art implants and lasers, underpinning steady growth in the glaucoma surgery devices market.

Accelerated Regulatory Approvals for Next-Gen MIGS

Regulators have signaled a receptive stance toward innovation. In February 2024, the FDA cleared Glaukos iStent Infinite, the first micro-stent approved for standalone implantation in refractory cases, marking a pivotal expansion beyond cataract-combined indications. Balance Ophthalmics secured De Novo classification for its pulse-modulated FSYX system only five months later, highlighting streamlined evaluation paths for novel mechanisms. Europe’s CE-mark timeline is narrowing as notified bodies prioritize ophthalmic devices, as evidenced by ViaLase’s femtosecond platform, which was certified in July 2024. Insurance authorities are aligning with regulators: U.S. Medicare contractors finalized local coverage for multiple MIGS codes in November 2024, reducing payer friction for surgeons. Faster approvals directly shorten commercial ramp-up cycles, lifting revenue forecasts across the glaucoma surgery devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of alternative therapies | -0.8% | Global; most pronounced in developed markets | Medium term (2-4 years) |

| High cost of advanced devices & procedures | -1.1% | Emerging markets; cost-sensitive segments | Long term (≥ 4 years) |

| Post-market safety recalls | -0.4% | Global; strict regulatory regions | Short term (≤ 2 years) |

| Shortage of MIGS-trained surgeons | -0.9% | Global; acute in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Availability of Alternative Therapies

Innovations in pharmaceutical delivery and non-incisional lasers are slowing the referral of early-stage patients into the operating room. Sustained-release implants, such as iDose TR, deliver three-year prostaglandin analog therapy without the need for an incision, and the LIGHT trial placed selective laser trabeculoplasty ahead of eye drops as the go-to initial therapy. Balance Ophthalmics’ FSYX platform achieved a 100% IOP response in pivotal data without breaching the eye wall, attracting clinicians wary of surgical risks. As these therapies lengthen the effective life of medical management, procedural growth could moderate unless surgical technologies continue to demonstrate superior long-term cost-effectiveness.

High Cost of Advanced Devices & Procedures

A complex MIGS kit may exceed USD 1,000 per eye, and capital equipment for automated lasers can surpass USD 200,000, excluding surgeon training costs. In low-resource markets, out-of-pocket payment deters uptake, even though the disease burden is high. Some hospitals adopt lower-priced drainage shunts like the Aurolab Aqueous Drainage Implant, yet global distribution remains spotty. Health insurers in emerging economies demand clearer proof of long-range savings before reimbursing premium implants, slowing broad diffusion of next-generation devices within the glaucoma surgery devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Device Innovation Drives Market Differentiation

Glaucoma drainage devices secured a 40.12% share of the glaucoma surgery devices market in 2024, benefiting from decades of clinical familiarity and improved design features such as the valveless Ahmed ClearPath and the low-profile Paul implant. Laser systems, however, are forecast to grow at 6.92% CAGR through 2030 and are increasingly positioned as standalone first-line procedures. Alcon’s Voyager DSLT automates energy delivery, producing 62% medication-free outcomes at 12 months and lowering chair time, a crucial metric for high-volume centers. Drug-delivery implants, AI-assisted targeting tools, and adjustable shunts are entering clinical trials, signifying an expanding competitive canvas that should widen the glaucoma surgery devices market size for suppliers offering multiproduct portfolios.

Surgeons continue to deploy traditional surgical instruments—forceps, scissors, and punches—because trabeculectomy remains mandatory for end-stage disease. Yet, even these tools are evolving; titanium tips reduce corneal haze and enable better visualization under high-definition microscope cameras, aligning with the broader theme of precision in the glaucoma surgery devices industry.

By Surgery Method: MIGS Dominance Accelerates Innovation Cycles

Minimally invasive glaucoma surgery held 47.23% of the glaucoma surgery devices market share in 2024. Patients favor its faster recovery and lower risk of hypotony. Laser surgery outpaces all other approaches, charting a 6.89% CAGR, led by selective laser trabeculoplasty and emerging femtosecond systems that promise non-incisional aqueous outflow enhancement. Schlemm’s canal-based devices, including the OMNI Surgical System from Sight Sciences, maintain durable IOP lowering at three-year follow-up, reinforcing clinician confidence.

Traditional filtration surgeries, such as trabeculectomy and tube shunts, remain critical for managing advanced or uncontrolled pressure cases. Suprachoroidal and subconjunctival implants are gathering evidence, positioning themselves as hybrid solutions between MIGS and traditional surgery. The interplay of these modalities ensures robust competition, sustaining device refresh cycles and protecting revenue diversity inside the glaucoma surgery devices market.

By End User: Ophthalmic Clinics Drive Market Expansion

Hospitals collectively managed 59.12% of glaucoma surgery procedures in 2024, but specialized ophthalmic clinics are emerging as growth leaders, clocking a 7.03% CAGR as they acquire MIGS-ready capital equipment. Clinics attract patients by offering shorter wait times, bundled cataract-plus-MIGS packages, and AI-enabled diagnostics that reduce the need for pre-operative consultations. The glaucoma surgery devices market size attached to clinics thus grows alongside their capacity upgrades.

Ambulatory surgery centers (ASCs) are the next frontier. Medicare parity has already sparked a wave of ASC certifications, and manufacturers now bundle instrument kits with in-service training, lowering the first-case barrier. Hospitals are responding by carving out dedicated glaucoma service lines to preserve referral streams in the glaucoma surgery devices industry.

Geography Analysis

North America generated 37.67% of global revenue in 2024, underpinned by comprehensive insurance coverage and a dense network of fellowship-trained surgeons. The United States remains the primary revenue engine, backed by Medicare’s separate payment pathway for standalone MIGS and ASC parity. Canada’s single-payer model reimburses implants based on provincial technology assessments, yielding moderate yet dependable adoption. Mexico’s private hospitals target medical tourists seeking combined cataract-MIGS procedures at competitive cash prices, adding incremental demand for cost-conscious devices.

Asia-Pacific delivers the fastest 7.14% CAGR, thanks to health-system modernization, rising disposable income, and a senior population boom. China’s tier-one hospitals now routinely stock second-generation MIGS, whereas tier-two facilities prefer lower-cost drainage tubes. India’s government insurance schemes are starting to reimburse basic stents, providing fertile ground for domestic OEMs that license Western IP. Japan and South Korea exhibit adoption curves akin to the United States, with clinics bundling AI-enabled diagnostics and micro-stents. Southeast Asian nations—Vietnam, Indonesia, and the Philippines—are training subspecialists through regional centers of excellence funded by industry grants, supporting future demand.

Europe exhibits steady mid-single-digit expansion as national health services introduce technology appraisal frameworks that reward procedures demonstrating long-term medication savings. Germany and the United Kingdom are early users of femtosecond laser trabeculotomy systems. France, Italy, and Spain invest in surgeon retraining programs that integrate MIGS into cataract fellowships. Eastern European markets, particularly Poland and Romania, are gradually opening to lower-priced implants as GDP per capita rises, broadening the addressable glaucoma surgery devices market.

Competitive Landscape

The competitive field is moderately fragmented, with the top five manufacturers accounting for approximately 55-60% of the revenue. Alcon expanded its glaucoma portfolio by acquiring Belkin Vision for USD 81 million in July 2024, gaining a direct laser platform that complements its Hydrus micro-stent. Alcon logged USD 5.5 billion in 2024 surgical sales, positioning it as the most significant single player. Sight Sciences won a USD 34 million patent verdict against Alcon’s Hydrus in April 2024, underscoring fierce IP battles central to the glaucoma surgery devices market. Glaukos reported record Q2 2024 sales of USD 95.7 million—up 19% year over year—buoyed by the uptake of iDose TR and iStent Infinite.

Strategic collaborations are blossoming. ForSight Robotics raised USD 125 million in Series B funding to refine an autonomous robotic system designed to mitigate the global shortage of MIGS-qualified surgeons.

Smaller entrants, such as ViaLase, are leveraging CE-mark approvals to gain early European footholds before tackling the U.S. market. Collectively, firms are converging on integrated ecosystems that wrap diagnostic AI, surgical hardware, and real-time analytics into a single value proposition to lock in customers and enlarge their slice of the glaucoma surgery devices market.

Glaucoma Surgery Devices Industry Leaders

Alcon Inc.

ASICO, LLC

Lumenis Be Ltd.

Glaukos Corporation

Topcon Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Alcon launched Voyager Direct Selective Laser Trabeculoplasty, the first fully automated glaucoma laser, achieving 62% medication-free outcomes at 12 months.

- January 2025: Sight Sciences released 36-month real-world data confirming sustained IOP control with the OMNI Surgical System.

- July 2024: ViaLase obtained CE-mark for a femtosecond laser that performs non-incisional trabeculotomy, reporting nearly 7 mmHg mean IOP reduction.

- July 2024: Alcon closed its USD 81 million acquisition of Belkin Vision, broadening its glaucoma laser portfolio.

Global Glaucoma Surgery Devices Market Report Scope

As per the scope of the report, glaucoma is a type of eye disease that can cause vision loss and blindness by damaging an optic nerve in the eye. Glaucoma surgery devices deal with the treatment of those diseases. The Glaucoma Surgery Devices Market is classified into three regions: North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Glaucoma Drainage Devices | Shunts |

| Valves | |

| Drainage Implant | |

| Stents | |

| Laser Systems | |

| Traditional Surgical Instruments | Punches |

| Probes | |

| Scissors & Forceps | |

| Others | |

| Other Products |

| Traditional Glaucoma Surgery | Trabeculectomy |

| Drainage Implant Surgery | |

| Minimally Invasive Glaucoma Surgery (MIGS) | Schlemm's Canal-based |

| Suprachoroidal based | |

| Sub-conjunctival | |

| Others | |

| Laser Surgery |

| Hospitals |

| Ophthalmic Clinics |

| Ambulatory Surgery Centers |

| Others |

| Primary Glaucoma | Open-angle Glaucoma |

| Normal-closure Glaucoma | |

| Angle-closure Glaucoma | |

| Others | |

| Secondary Glaucoma |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product | Glaucoma Drainage Devices | Shunts |

| Valves | ||

| Drainage Implant | ||

| Stents | ||

| Laser Systems | ||

| Traditional Surgical Instruments | Punches | |

| Probes | ||

| Scissors & Forceps | ||

| Others | ||

| Other Products | ||

| By Surgery Method | Traditional Glaucoma Surgery | Trabeculectomy |

| Drainage Implant Surgery | ||

| Minimally Invasive Glaucoma Surgery (MIGS) | Schlemm's Canal-based | |

| Suprachoroidal based | ||

| Sub-conjunctival | ||

| Others | ||

| Laser Surgery | ||

| By End User | Hospitals | |

| Ophthalmic Clinics | ||

| Ambulatory Surgery Centers | ||

| Others | ||

| By Glaucoma Type | Primary Glaucoma | Open-angle Glaucoma |

| Normal-closure Glaucoma | ||

| Angle-closure Glaucoma | ||

| Others | ||

| Secondary Glaucoma | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the glaucoma surgery devices market?

The glaucoma surgery devices market reached USD 1.21 billion in 2025 and is projected to climb to USD 1.64 billion by 2030 at a 6.27% CAGR.

Which region is expanding fastest in the glaucoma surgery devices market?

Asia-Pacific is growing at a 7.14% CAGR through 2030, propelled by infrastructure upgrades, aging demographics, and rising healthcare spending.

How dominant is minimally invasive glaucoma surgery?

Minimally invasive glaucoma surgery accounted for 47.23% of glaucoma surgery devices market share in 2024, offering strong safety and recovery advantages over traditional filtration surgery.

Why are laser systems gaining momentum?

Laser systems, especially automated selective laser trabeculoplasty, are forecast to grow 6.92% annually because they reduce operating time, minimize complications, and can serve as first-line therapy.

What drives hospitals and clinics to adopt new glaucoma devices?

Payers increasingly reimburse newer technologies, surgeons favor devices with lower learning curves, and AI-guided systems promise consistent outcomes, all fueling capital purchases by care facilities.

Which companies lead the glaucoma surgery devices industry?

Alcon, Glaukos, and Sight Sciences headline the competitive landscape, together capturing a significant portion of global revenue and advancing portfolios through acquisitions and new-product launches.

Page last updated on: