Stereotactic Surgery Devices Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

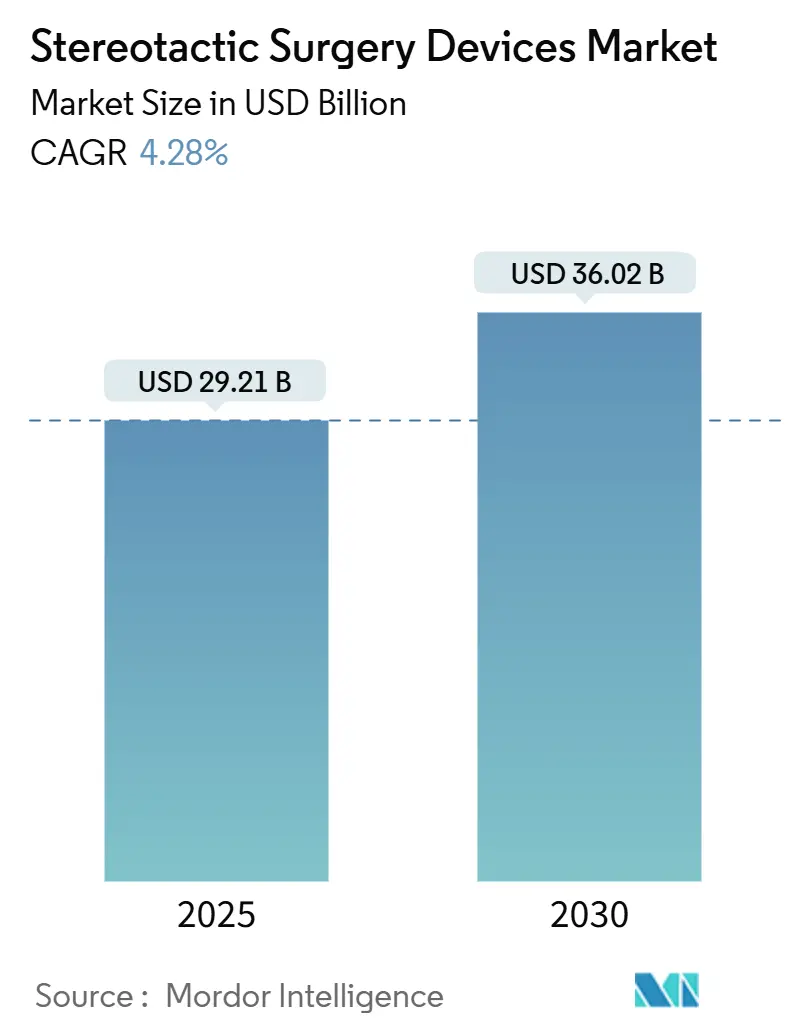

| Market Size (2025) | USD 29.21 Billion |

| Market Size (2030) | USD 36.02 Billion |

| Growth Rate (2025 - 2030) | 4.28% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Stereotactic Surgery Devices Market Analysis by Mordor Intelligence

The Stereotactic Surgery Devices Market size is estimated at USD 29.21 billion in 2025, and is expected to reach USD 36.02 billion by 2030, at a CAGR of 4.28% during the forecast period (2025-2030).

Sustained demand for image-guided radiosurgery, the convergence of artificial intelligence with robotic positioning, and pay-for-outcome reimbursement schemes are collectively steering this measured expansion. Hospitals are modernizing radiation suites to maintain high patient throughput, regional cancer centers are transitioning to outpatient stereotactic pods, and investors are backing the roll-out of compact linear accelerators (LINACs) that reduce the real estate burden on providers. At the same time, clinicians are broadening indications from brain metastases to functional disorders, thereby diversifying procedure volumes and anchoring recurring revenue streams. Competitive intensity is rising as incumbents layer adaptive imaging and real-time dose optimization onto existing platforms to defend share against AI-native challengers.

Key Report Takeaways

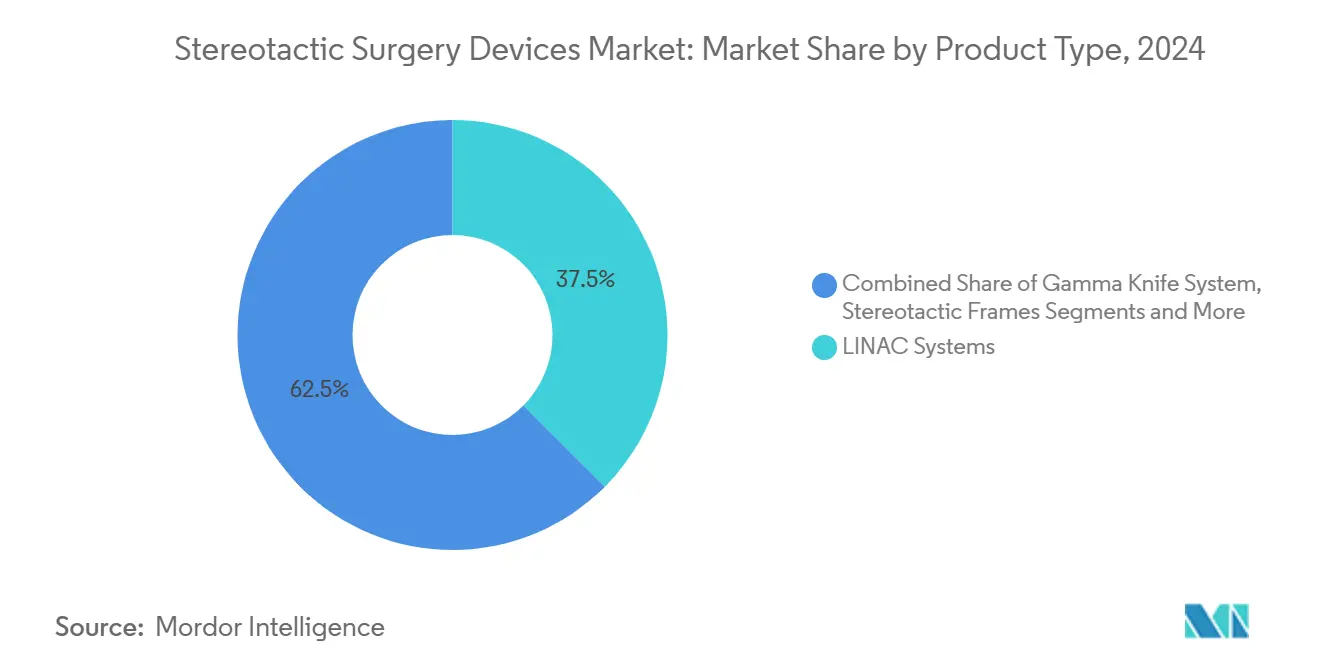

- By product type, LINAC systems led with 37.46% of the stereotactic surgery devices market share in 2024. CyberKnife and other robotic radiosurgery platforms are projected to expand at a 7.44% CAGR through 2030.

- By application, brain tumors accounted for a 44.69% share of the stereotactic surgery devices market size in 2024. Functional neurosurgery is advancing at an 8.37% CAGR during the forecast period.

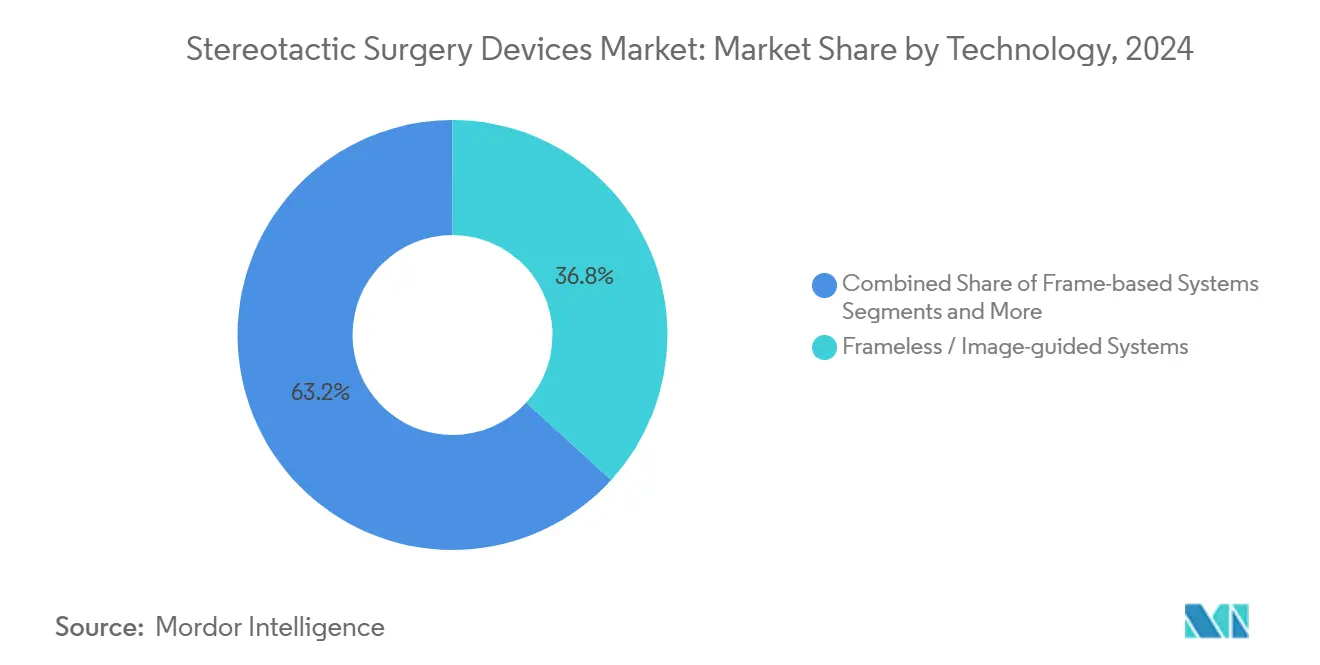

- By technology, frameless and image-guided systems commanded a 36.79% share in 2024. MRI-guided adaptive systems are expected to grow at a 7.88% CAGR to 2030.

- By end user, hospitals held a 71.42% share in 2024. Ambulatory surgery centers are poised to record a 6.48% CAGR through 2030.

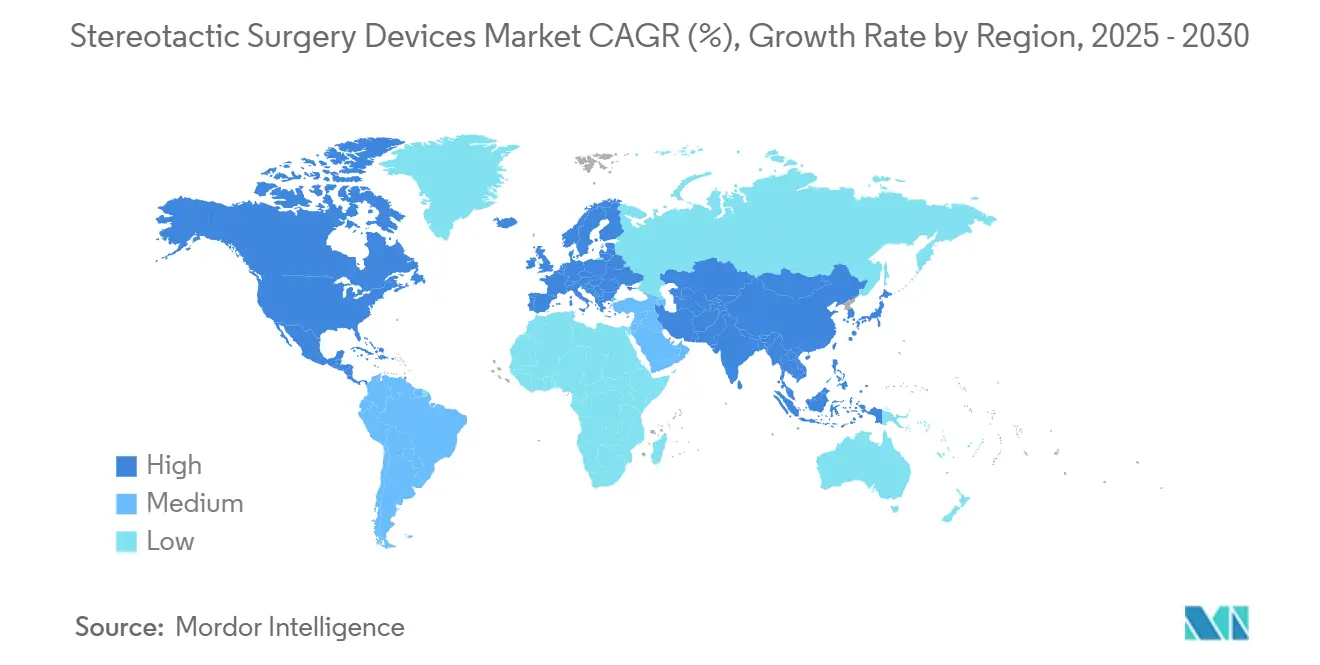

- By geography, North America maintained the most significant regional share at 39.86% in 2024. Asia-Pacific is forecast to register the fastest regional growth with a 6.04% CAGR to 2030.

Global Stereotactic Surgery Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence Of Intracranial Tumours & Functional Disorders | +0.8% | Global, with higher impact in aging populations of North America & Europe | Long term (≥ 4 years) |

| Shift Toward Minimally-Invasive Radiosurgery Over Craniotomy | +1.2% | Global, with accelerated adoption in Asia-Pacific | Medium term (2-4 years) |

| Image-Guided & MRI-LINAC Tech Breakthroughs | +0.9% | North America & Europe leading, Asia-Pacific following | Medium term (2-4 years) |

| Reimbursement Expansion To Essential Tremor & OCD | +0.6% | Primarily North America & Europe | Short term (≤ 2 years) |

| Roll-Out Of Compact LINAC Pods In Private Oncology Chains | +0.7% | Asia-Pacific core, spill-over to MEA | Medium term (2-4 years) |

| AI-Driven Adaptive Planning Cuts Treatment Time <15 Min | +0.5% | Global, with early adoption in developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Intracranial Tumors & Functional Disorders

Aging populations are creating a steady pipeline of patients requiring precision radiosurgery, while advancements in imaging are uncovering lesions at earlier stages.[1]A. Früh et al., “Robotic Stereotactic Radiosurgery for Intracranial Meningiomas in Elderly Patients,” Frontiers in Oncology, frontiersin.orgClinical studies report a 97.1% local control rate for stereotactic treatment of meningiomas in elderly cohorts, confirming its suitability for patients once considered inoperable. Movement disorders such as Parkinson’s disease and essential tremor are also shifting toward non-invasive stereotactic options that avoid hardware-based deep-brain stimulators. In emerging economies, the increasing availability of MRI scans is driving higher detection rates, thereby reinforcing a multi-regional demand curve. These overlaps between oncology and functional cases are compounding utilization and smoothing the revenue profile for providers.

Shift Toward Minimally Invasive Radiosurgery Over Craniotomy

Hospitals are rewriting surgical pathways as stereotactic procedures deliver comparable tumor control with shorter stays and fewer complications. Cost studies show notable savings in intensive-care days, while patients favor outpatient recovery over traditional craniotomy. The trend is especially visible in skull-base lesions, where open surgery carries high morbidity. As informed-consent discussions pivot to quality-of-life metrics, referral patterns are moving from neurosurgical theaters to radiation suites, cementing stereotactic protocols as first-line options.

Image-Guided & MRI-LINAC Tech Breakthroughs

Real-time magnetic resonance imaging, integrated with LINAC beams, allows for soft-tissue visualization during dose delivery.[2]O. M. Dona Lemus et al., “Adaptive Radiotherapy: Next-Generation Radiotherapy,” MDPI Cancers, mdpi.com Physicians can adapt plans on the fly, treating lesions near eloquent brain regions that were previously contraindicated. AI-assisted contouring now produces optimal plans in minutes, boosting daily throughput without sacrificing precision. Facilities investing in these next-generation systems achieve marketing differentiation while meeting payer expectations for evidence-based improvements in local control and reduction of toxicity.

Reimbursement Expansion to Essential Tremor & OCD

Payers in the United States and parts of Europe have widened coverage to include essential tremor, obsessive-compulsive disorder, and Parkinson’s symptoms treated with focused ultrasound and radiosurgery.[3]Jeff Hall, “FDA Expands Approval of MRI-Guided Ultrasound Treatment for Parkinson’s Disease,” Diagnostic Imaging, diagnosticimaging.comMedicare policy shifts typically ripple into commercial insurance, expanding addressable patient pools almost overnight. Cost-utility analyses demonstrate lower lifetime expenses compared to invasive alternatives, facilitating adoption among value-based purchasers. For providers, broader coverage reduces financial uncertainty and encourages the addition of functional schedules alongside traditional tumor lists.

CAPEX & Upkeep Costs of Radiosurgery Platforms

A Gamma Knife suite with MRI support can cost approximately USD 9.84 million upfront. At the same time, a CyberKnife room requires at least USD 3.2 million, plus additional build-out expenses—annual maintenance averages 3.13% of the purchase price for LINACs, straining operating budgets. Smaller hospitals struggle to reach break-even case volumes, delaying new installations in lower-income regions. Leasing and multi-institutional equipment sharing are emerging, yet financing hurdles persist.

Shortage of Trained Neuro-Radiosurgeons in LICs

The procedure’s complexity demands cross-disciplinary expertise that is scarce in low-income countries. Migration of specialists to high-income markets widens the gap, limiting the practical impact of donated or subsidized hardware. Remote planning hubs and visiting-expert programs offer interim relief, but hands-on skills remain the bottleneck.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: LINAC Systems Drive Market Leadership

LINAC platforms held a 37.46% share of the stereotactic surgery devices market in 2024, underscoring their versatility across various tumor sites and fractionation schemes. Hospitals value the dual-use design that supports both conventional radiotherapy and stereotactic boosts without additional capital expenditure. New AI-enabled versions, such as the Evo system showcased in 2024, promise sub-millimeter accuracy while trimming session times.

CyberKnife and other robotic units, projected to grow at 7.44% CAGR, lure centers seeking frameless convenience and intricate beam choreography. The Gamma Knife retains loyalty in pure cranial programs, whereas proton and heavy-ion systems secure niche slots in pediatric applications. As procurement cycles progress, many institutions adopt a hub-and-spoke model: a high-end robotic suite at the flagship site and compact LINAC satellites in feeder clinics, a strategy that broadens the footprint of the stereotactic surgery devices market without overshooting budgets.

By Application: Brain Tumors Dominate While Functional Cases Surge

Brain tumors represented 44.69% of the stereotactic surgery devices market size in 2024, reflecting decades of protocol refinement and robust outcome data. Multi-disciplinary tumor boards now combine stereotactic radiosurgery with systemic therapies to manage oligometastatic disease.

Functional neurosurgery, however, is the rising star with an 8.37% CAGR forecast. FDA clearance of MRI-guided focused ultrasound for Parkinson’s tremor expanded payer coverage, prompting more centers to add functional service lines. Radiosurgical ablation of epileptogenic foci and psychiatric circuits is entering trial pipelines, hinting at future demand spikes that could reshape the revenue mix across the stereotactic surgery devices market.

By Technology: Frameless Systems Lead the Innovation Wave

Frameless, image-guided modalities commanded a 36.79% share in 2024, proving that patient comfort and workflow efficiency can coexist with precision. Infra-red and X-ray fiducial tracking substitutes for invasive head frames, broadening candidate eligibility and improving satisfaction scores.

MRI-guided adaptive systems, expanding at a 7.88% CAGR, overlay soft-tissue clarity onto beam delivery, allowing clinicians to gate doses in real-time. Frame-based rigs are used for select cases of trigeminal neuralgia and AVM, where absolute immobilization is required. Meanwhile, robotic couches and six-axis collimators continue to push isocenter accuracy below 0.5 mm, driving an engineering race that sustains premium ASPs within the stereotactic surgery devices market.

By End User: Hospitals Maintain Dominance Despite Ambulatory Momentum

Hospitals controlled 71.42% of revenue in 2024, leveraging on-site imaging, anesthesia, and neuro-ICU back-up to handle high-complexity cases. Their procurement power attracts vendor-financed upgrades and bundled service contracts.

Ambulatory surgery centers (ASCs), projected to post a 6.48% CAGR, target low-acuity metastatic or functional cases that can be completed within the same-day windows. Compact pods lower shielding costs, making stereotactic capability feasible in suburban settings and fueling incremental growth of the stereotactic surgery devices market. Academic institutes keep pace by incubating AI-driven planning solutions, while pure-play cancer centers pivot to hybrid photon-proton partnerships that offer one-stop pathways to referring physicians.

Geography Analysis

North America retained a 39.86% share of the stereotactic surgery devices market in 2024, supported by deep reimbursement pools, early clinical adoption, and a dense network of multidisciplinary tumor boards. Robust clinical-trial ecosystems accelerate protocol updates and vendor-provider co-development contracts.

Europe presents a mature but steady landscape where cost-effectiveness audits shape procurement. National health systems emphasize the collection of longitudinal quality-of-life data, prompting providers to favor platforms with adaptive imaging that minimizes toxicity. China’s revised medical-device regulations have opened doors for multinational vendors willing to partner with domestic assemblers, a policy shift that could recalibrate supply chains.

The Asia-Pacific region is the growth nucleus, forecasted to grow at a 6.04% CAGR, as private capital sponsors oncology mega-chains equipped with compact LINAC rooms. The Middle East & Africa and South America are nascent but are building public-private alliances to circumvent capital hurdles. Collectively, demand is migrating toward regions where demographic tailwinds and infrastructure roll-outs align, diversifying the global stereotactic surgery devices market beyond its traditional Western core.

Competitive Landscape

The field remains moderately consolidated, with Elekta, Siemens Healthineers, and Accuray collectively anchoring a broad installation base and layering incremental software fees onto their hardware footprints. Each is investing in proprietary AI engines to keep planning ecosystems sticky.

Disruptors such as ZAP Surgical, which raised USD 78 million to fuse robotic articulation with gamma-like precision, are challenging incumbents on both cost and footprint. Start-ups benefit from modular designs that shorten construction timelines, a key advantage in emerging markets that are racing to add capacity.

Strategic moves include vendor-neutral treatment planning suites, cloud-based image archives, and service line franchising, where manufacturers manage uptime under outcome-linked contracts. The stereotactic surgery devices industry is therefore shifting from pure hardware sales to integrated, data-rich platforms that intertwine capital, software, and service revenues.

Stereotactic Surgery Devices Industry Leaders

-

Elekta AB

-

Siemens Healthineers

-

Accuray Incorporated

-

Brainlab AG

-

Monteris Medical Inc.

- *Disclaimer: Major Players sorted in no particular order

Global Stereotactic Surgery Devices Market Report Scope

| Linear Accelerator (LINAC) Systems |

| Gamma Knife Systems |

| CyberKnife & Robotic Radiosurgery Systems |

| Proton/Heavy-Ion Beam Systems |

| Stereotactic Frames |

| Frameless Navigation Systems |

| Brain Tumours |

| Arteriovenous Malformations (AVM) |

| Functional Neurosurgery (Parkinson’s, Epilepsy, Tremor) |

| Spine & Extracranial Metastases |

| Biopsy & Diagnostic Guidance |

| Frame-based Systems |

| Frameless / Image-guided Systems |

| Robotic Radiosurgery Platforms |

| MRI-guided Adaptive Systems |

| Hospitals |

| Ambulatory Surgery Centres |

| Cancer & Radiotherapy Centres |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Linear Accelerator (LINAC) Systems | |

| Gamma Knife Systems | ||

| CyberKnife & Robotic Radiosurgery Systems | ||

| Proton/Heavy-Ion Beam Systems | ||

| Stereotactic Frames | ||

| Frameless Navigation Systems | ||

| By Application | Brain Tumours | |

| Arteriovenous Malformations (AVM) | ||

| Functional Neurosurgery (Parkinson’s, Epilepsy, Tremor) | ||

| Spine & Extracranial Metastases | ||

| Biopsy & Diagnostic Guidance | ||

| By Technology | Frame-based Systems | |

| Frameless / Image-guided Systems | ||

| Robotic Radiosurgery Platforms | ||

| MRI-guided Adaptive Systems | ||

| By End User | Hospitals | |

| Ambulatory Surgery Centres | ||

| Cancer & Radiotherapy Centres | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the stereotactic surgery devices market?

The market is valued at USD 29.21 billion in 2025.

Which product category leads revenue?

LINAC systems lead, holding 37.46% share in 2024.

Which application segment is growing fastest?

Functional neurosurgery is forecast to expand at an 8.37% CAGR through 2030.

Why are frameless systems gaining popularity?

They improve patient comfort and reduce setup time without compromising accuracy.

Page last updated on: