Redispersible Polymer Powder Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

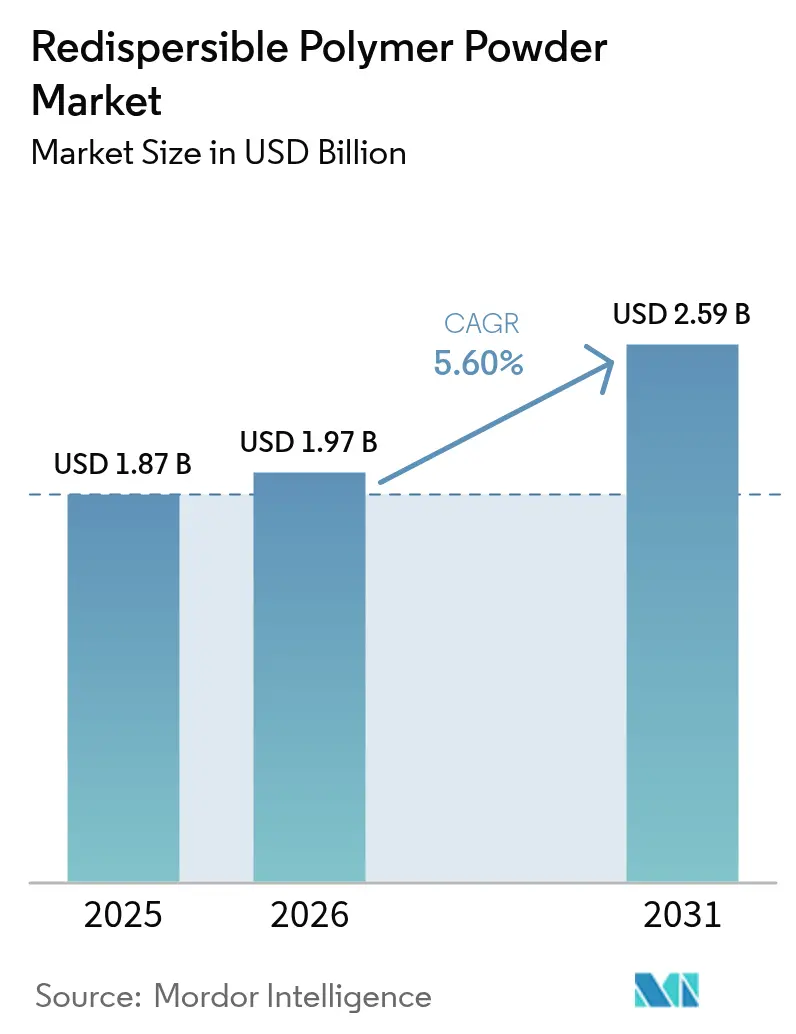

| Market Size (2026) | USD 1.97 Billion |

| Market Size (2031) | USD 2.59 Billion |

| Growth Rate (2026 - 2031) | 5.60% CAGR |

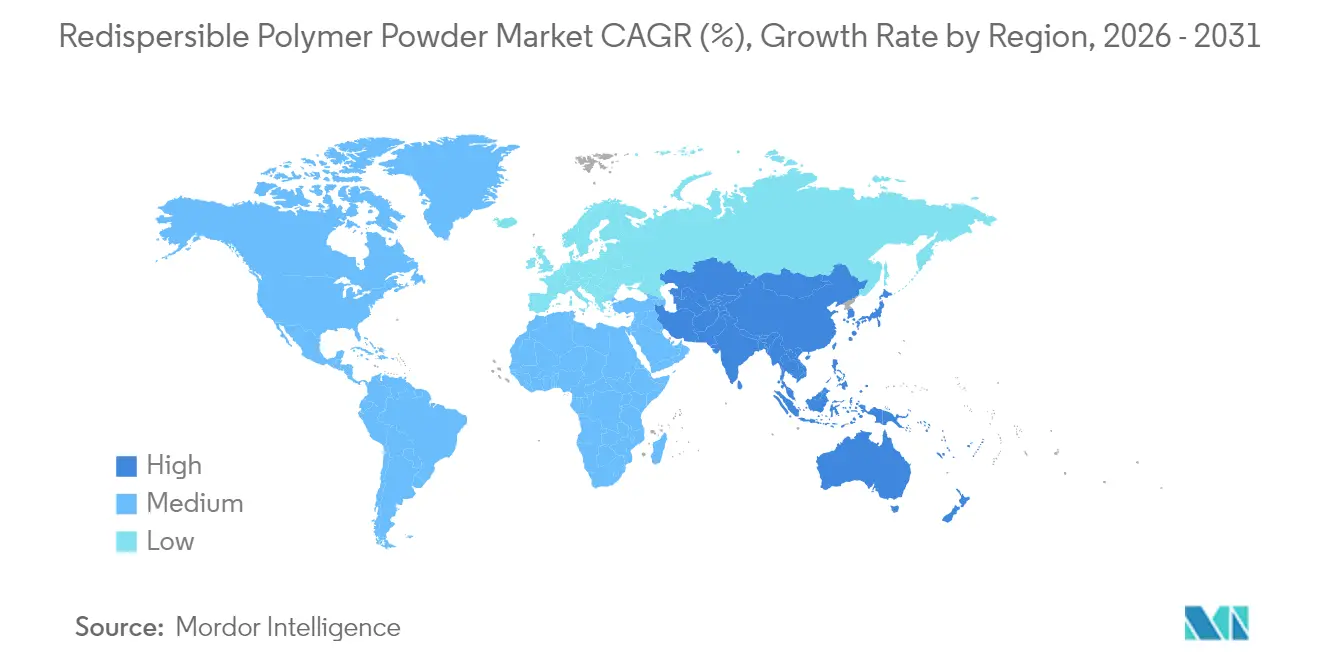

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Redispersible Polymer Powder Market Analysis by Mordor Intelligence

The Redispersible Polymer Powder Market size was valued at USD 1.87 billion in 2025 and estimated to grow from USD 1.97 billion in 2026 to reach USD 2.59 billion by 2031, at a CAGR of 5.60% during the forecast period (2026-2031). A steady preference for high-performance dry-mortar additives is raising demand as policymakers push for durable and energy-efficient buildings. Expanding infrastructure spending across emerging economies adds a strong volume base, while renovation programs in Europe and North America redirect product innovation toward low-VOC and bio-based grades. Volatile vinyl acetate monomer prices after 2024 compressed margins, yet vertical integration by leading producers helped to stabilize supply. Technology upgrades in spray-drying, along with polymer powders tailored for 3D-printed concrete, are widening the practical scope of the redispersible polymer powder market.

Key Report Takeaways

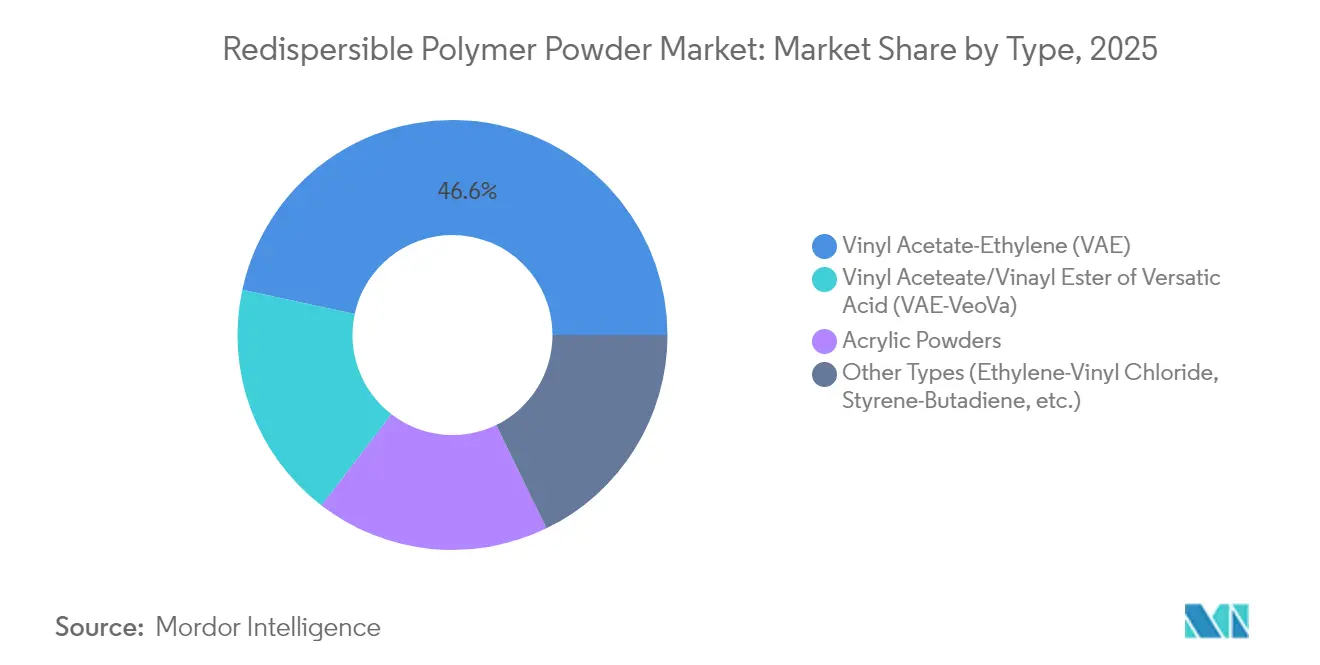

- By product type, Vinyl Acetate-Ethylene led with 46.62% of redispersible polymer powder market share in 2025 while Vinyl Acetate/Vinyl Ester of Versatic Acid is forecast to expand at a 6.08% CAGR through 2031.

- By application, tile adhesives accounted for 37.74% of the redispersible polymer powder market size in 2025; other applications, including External Thermal Insulation Composite Systems, are advancing at a 6.52% CAGR to 2031.

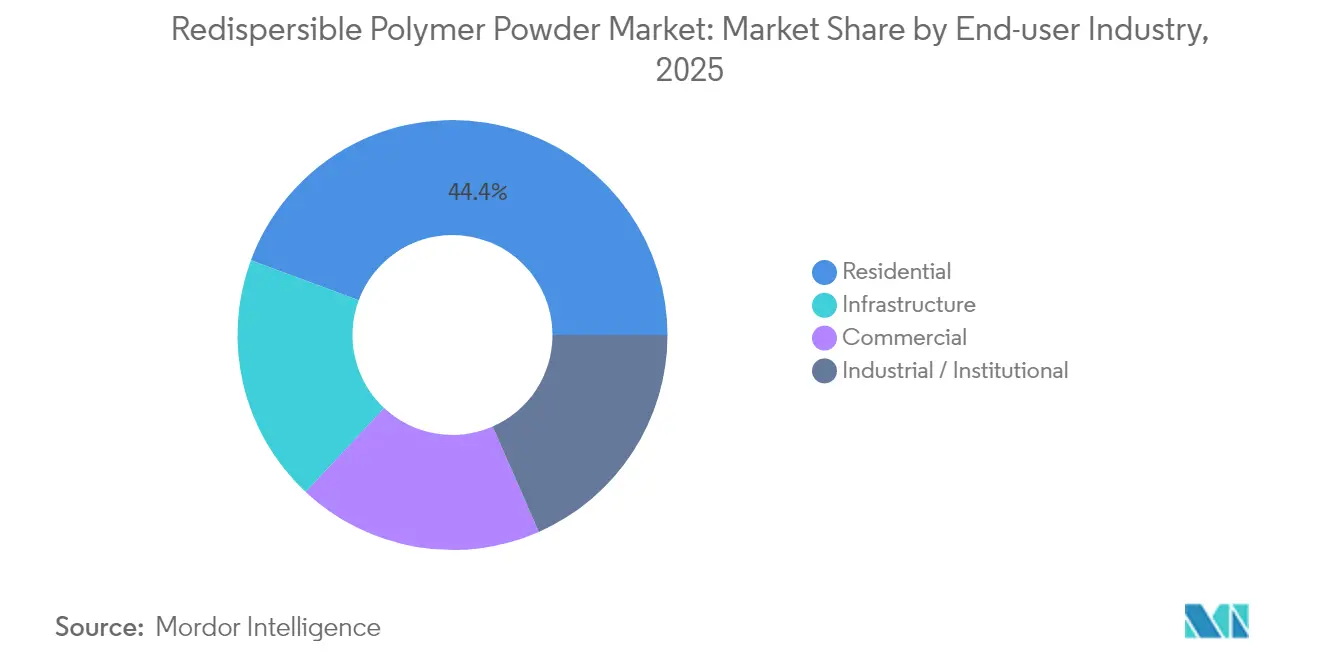

- By end-user industry, residential construction held 44.35% revenue in 2025 while infrastructure projects record the highest projected CAGR at 5.98% through 2031.

- By geography, Asia-Pacific commanded 45.55% of global demand in 2025 and is moving ahead at a 5.84% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Redispersible Polymer Powder Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Construction boom in emerging economies | +1.8% | Asia-Pacific core | Long term (≥ 4 years) |

| Rapid shift to ready-mix dry-mortar systems | +1.2% | Global | Medium term (2-4 years) |

| Renovation-led demand for high-performance tile adhesives | +0.9% | Europe and North America | Medium term (2-4 years) |

| Government energy-efficient building codes | +0.7% | North America and EU | Long term (≥ 4 years) |

| 3D-printed concrete adopting polymer binders | +0.4% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Construction Boom in Emerging Economies

Infrastructure expansion in Asia-Pacific underpins long-term growth as China’s carbon-neutrality roadmap and India’s housing drive collectively deliver more than 60% of regional consumption. BASF allocated USD 10 billion to its Zhanjiang Verbund site, ensuring renewable-powered production of construction polymers. India’s construction chemicals revenue touched INR 20,000 crore in 2025, and Master Builders Solutions set a turnover target of INR 500 crore by 2028. Saudi Arabia’s NEOM project earmarked SAR 1.3 billion for robotics-enabled building, which highlights a preference for specialty binders capable of supporting automated assembly. Such multi-year public programs guarantee visibility for the redispersible polymer powder market far beyond routine housing cycles.

Rapid Shift to Ready-Mix Dry-Mortar Systems

Factory-produced mortars cut job-site labor and minimize mixing inconsistencies, accelerating the worldwide transition from traditional batching to standardized formulations. Early adoption in Germany and France has proven the pathway for universal quality standards, and similar policy moves emerge in large U.S. metropolitan areas. Wacker introduced its VINNAPAS eco range to deliver bio-balanced VAE powders designed for automated silos and pumps. Ready-mix growth improves dosing accuracy, allowing contractors to meet stricter tile adhesive shear strength requirements. As skilled labor shortages worsen, automated dosing becomes a cost-avoidance strategy that further enlarges the redispersible polymer powder market.

Renovation-Led Demand for High-Performance Tile Adhesives

Energy-retrofit schemes across Europe stimulate premium tile adhesive sales as homeowners swap small tiles for large-format ceramic or stone. Scientific testing confirmed superior bond strength for ceramic finishes in north-facing facades, reinforcing the need for customized polymer-modified adhesives. North American remodelers echo this trend, and cellulose ether suppliers report an uptick in synergy requests for improved open time and slip resistance. The willingness to pay for reliable adhesion encourages manufacturers to launch higher-margin VAE-VeoVa blends. Renovation therefore lifts the redispersible polymer powder market beyond purely new-build demand.

Government Energy-Efficient Building Codes

The U.S. Department of Energy set aside USD 240 million in grants to help states update codes that cut operational energy use[1]U.S. Department of Energy, “DOE Announces $240 Million for Adoption of Energy-Efficient Building Codes,” iratracker.org. Federal buildings must phase out fossil fuels by 2030, giving procurement officers a mandate to select low-embodied-carbon construction chemicals. The General Services Administration added minimum recycled-content thresholds that create pull for bio-based polymer powders. Similar code upgrades in Canada and selective Asian economies indicate that compliance-driven material choice will keep pushing the redispersible polymer powder market toward eco-formulations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in vinyl-acetate monomer prices | -1.4% | Global | Short term (≤ 2 years) |

| Stricter VOC limits on protective colloids | -0.6% | North America and Europe | Long term (≥ 4 years) |

| Technical complexity in spray-drying | -0.8% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Vinyl-Acetate Monomer and Ethylene Prices

Feedstock spikes since 2024 forced BASF and Celanese to raise prices for several acetate derivatives. Celanese responded with a 1.3 million-ton acetic-acid unit in Texas and a 70 kt VAE debottleneck in Nanjing to capture scale economies. Larger groups with backward integration hedge risks, yet small firms lacking long-term contracts face margin compression, amplifying consolidation inside the redispersible polymer powder industry.

Stricter VOC Limits on Protective Colloids

The U.S. Environmental Protection Agency amended aerosol-coating standards in January 2025, signalling wider scrutiny of construction chemical emissions[2]Environmental Protection Agency, “VOC Emission Standards for Aerosol Coatings,” federalregister.gov. Michigan and Colorado tightened VOC caps for building materials, while South Coast AQMD Rule 1113 lowered permissible solvent content in concrete coatings. Manufacturers now pivot to bio-sourced colloids or powder-based stabilizers, which raise production costs and extend formulation cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: VAE Dominance Faces Premium Challenge

VAE controlled 46.62% of redispersible polymer powder market share in 2025 owing to its competitive cost and broad utility across tile adhesives, renders, and self-leveling compounds . Demand concentration allows economies of scale that underpin current price leadership. An uptick in premium construction jobs, however, is accelerating the adoption of VAE-VeoVa grades that grow at a 6.08% CAGR. Formulators prefer VAE-VeoVa for exterior insulation systems where alkaline resistance and flexibility are critical under climate stress. Acrylic powders sustain a niche in UV-exposed facades, whereas ethylene-vinyl-chloride blends serve industrial coatings that need chemical endurance.

Growth prospects hinge on producers’ capacity to maintain steady spray-drying consistency. Wacker’s renewable resource-based range targets carbon-footprint reductions without dampening shear strength. Celanese debuted Vinyl Acetate ECO-B with certified bio-content, catering to builders seeking verifiable sustainability claims. The redispersible polymer powder market thus shows dual momentum: volume security in VAE and margin growth in specialty subtypes.

By Application: Tile Adhesives Lead Infrastructure Surge

Tile adhesives captured 37.74% of redispersible polymer powder market size in 2025 due to booming renovation projects across the EU and escalating property upgrades in Chinese megacities. Larger format tiles need higher tensile adhesion and extended open time, driving polymer loadings up to 4% of total mortar weight. External Thermal Insulation Composite Systems rise at a 6.52% CAGR as regulators link façade insulation performance to heating emissions. Polymer powders that withstand freeze-thaw cycling gain priority in Nordic and Alpine regions.

Other emerging outlets such as self-leveling underlayment, concrete repair kits, and pumpable renders broaden the addressable base. Scientific findings on comparative adhesion underscore the preference for polymer-modified mortars on vulnerable facades. Grout and mortar additive segments stay resilient, underpinned by demand for colorfast and crack-resistant finishes in hospitality and retail refurbishments.

By End-user Industry: Residential Stability Meets Infrastructure Growth

Residential building generated 44.35% of global consumption in 2025 following sustained housing schemes in India and low-interest refinancing in the United States. Energy-retrofit subsidies in Germany further intensified demand for polymer-enhanced adhesives that improve indoor air quality and insulation. Infrastructure represents the fastest expansion at 5.98% CAGR as national programs finance climate-resilient highways, water systems, and mass-transit corridors. Contractors opt for high-flexibility grouts and repair mortars counted on to survive mechanical vibration and thermal shock in bridges and tunnels.

Commercial and industrial users form a stable mid-base, ordering bespoke polymer powders for flooring systems, clean-room finishes, and chemical containment slabs. Cross-segment opportunities arise when residential façade products retrofit government buildings that also need to meet net-zero mandates. Hence, end-user diversity fortifies the redispersible polymer powder market against downturns in any single construction vertical.

Geography Analysis

Asia-Pacific dominates the redispersible polymer powder market, recording 45.55% of global volume in 2025 and sustaining the fastest 5.84% CAGR. Government stimulus for rail, highway, and affordable housing projects amplifies baseline usage, while Chinese carbon-neutral targets encourage eco-certified polymer grades. Producers that localize capacity, as Sika did with twin plants in China and Indonesia, secure customs and freight benefits while ensuring supply reliability. The result is a structural tilt in global demand toward the region.

North America and Europe preserve share through stringent energy-performance regulations and large renovation stock. The U.S. DOE grant pool of USD 240 million elevates state adoption of advanced codes and steers builders toward polymer solutions that cut thermal bridging. EU directives on embodied-carbon reporting accelerate adoption of bio-based VAE-VeoVa powders. Mature distribution networks in both regions enable just-in-time delivery of customized grades, which explains robust margins even though absolute growth trails Asia-Pacific.

South America and Middle-East and Africa add a growth flank as megacities overhaul transport corridors and climate-proof coastal infrastructure. Saudi Arabia’s SAR 1.3 billion robotics-based NEOM agenda sets procurement protocols that favor high-durability binders. Brazil channels infrastructure stimulus toward sewer and road rehabilitation, spurring polymer demand in repair mortars. Local supply gaps invite joint ventures with global players that transfer technology while leveraging indigenous raw materials.

Competitive Landscape

The redispersible polymer powder market remains moderately concentrated. BASF, Wacker Chemie, and Dow leverage integrated feedstocks and worldwide technical centers to retain pricing power. BASF’s USD 10 billion Zhanjiang Verbund reinforces bulk capacity paired with renewable energy, while Wacker’s Nanjing upgrade added a reactor and spray dryer focused on VAE expansion. Dow channeled capital into Thailand’s propylene glycol line to secure upstream flexibility.

Celanese expanded its acetyl chain by scaling acetic-acid capacity in Texas and Nanjing to neutralize vinyl acetate volatility. Sustainability leadership surfaces through bio-based certifications and low-carbon supply chains—critical differentiators as public buyers tighten embodied-carbon specifications. Smaller regional firms confront rising compliance costs and technology demands—a dynamic that sparks mergers, such as JSC Pigment’s 2025 launch in Russia to insource domestic demand.

White-space competition now shifts to 3D-printing and automated masonry where bespoke polymer blends deliver shape stability. Early adopters collaborate with additive manufacturing start-ups, positioning incumbents for premium niches while reinforcing overall share in the redispersible polymer powder market.

Redispersible Polymer Powder Industry Leaders

Wacker Chemie AG

Celanese Corporation

BASF SE

Dow Inc.

Synthomer plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: JSC Pigment launches new production of redispersible polymer powders for dry construction mixtures. This project was implemented as part of the company's set of import substitution measures.

- May 2023: Wacker Chemie AG made a significant investment of around USD 100 million to enhance its production capabilities at its Nanjing facility in China. This investment featured the addition of a new reactor and spray dryer, tailored for vinyl-acetate-ethylene (VAE) redispersible polymer powders.

Global Redispersible Polymer Powder Market Report Scope

The Redispersible Polymer Powder Market report includes:

| Vinyl Acetate-Ethylene (VAE) |

| Vinyl Aceteate/Vinayl Ester of Versatic Acid (VAE-VeoVa) |

| Acrylic Powders |

| Other Types (Ethylene-Vinyl Chloride, Styrene-Butadiene, etc.) |

| Plasters and Renders |

| Tile Adhesives |

| Grouts |

| Mortar Additives |

| Other Applications (External Thermal Insulation Composite Systems (ETICS), etc.) |

| Residential |

| Commercial |

| Industrial / Institutional |

| Infrastructure |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Vinyl Acetate-Ethylene (VAE) | |

| Vinyl Aceteate/Vinayl Ester of Versatic Acid (VAE-VeoVa) | ||

| Acrylic Powders | ||

| Other Types (Ethylene-Vinyl Chloride, Styrene-Butadiene, etc.) | ||

| By Application | Plasters and Renders | |

| Tile Adhesives | ||

| Grouts | ||

| Mortar Additives | ||

| Other Applications (External Thermal Insulation Composite Systems (ETICS), etc.) | ||

| By End-user Industry | Residential | |

| Commercial | ||

| Industrial / Institutional | ||

| Infrastructure | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the redispersible polymer powder market?

The redispersible polymer powder market size stood at USD 1.97 billion in 2026 and is projected to reach USD 2.59 billion by 2031.

Which product type has the largest share?

Vinyl Acetate-Ethylene accounts for 46.62% of market share, making it the most widely used grade.

Why is Asia-Pacific growing faster than other regions?

Asia-Pacific benefits from large infrastructure programs in China and India, coupled with localized production investments that shorten supply chains and cut costs.

How do energy-efficient building codes influence demand?

Stricter codes oblige builders to use materials that enhance thermal performance and reduce embodied carbon, thereby increasing adoption of high-performance polymer powders formulated with bio-based or low-VOC components.

What is driving adoption of polymer powders in 3D-printed concrete?

Additive manufacturing relies on precise rheology and rapid film formation, properties delivered by tailored polymer powders that ensure shape stability and long-term durability.

Page last updated on: