Asphalt Modifiers Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

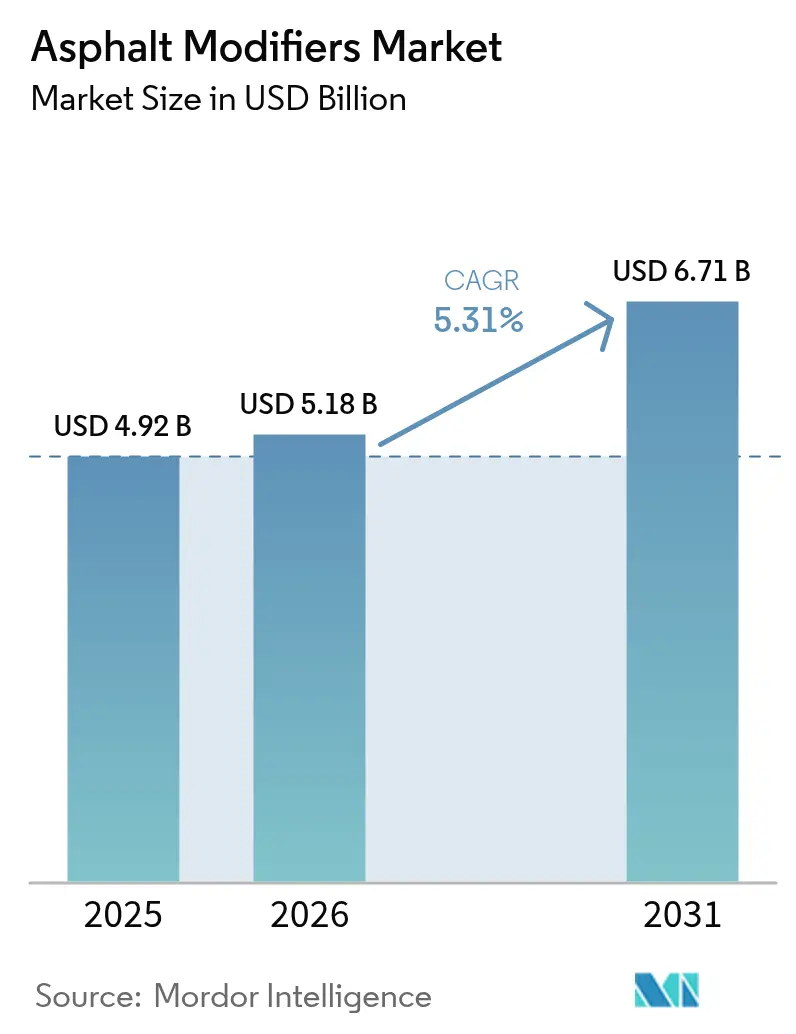

| Market Size (2026) | USD 5.18 Billion |

| Market Size (2031) | USD 6.71 Billion |

| Growth Rate (2026 - 2031) | 5.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asphalt Modifiers Market Analysis by Mordor Intelligence

The Asphalt Modifiers Market size is projected to expand from USD 4.92 billion in 2025 and USD 5.18 billion in 2026 to USD 6.71 billion by 2031, registering a CAGR of 5.31% between 2026 to 2031. Demand is propelled by performance-based binder mandates, mounting freight traffic that amplifies rutting risk, and circular-economy policies that reward the use of recycled plastics and tire rubber. Contractors seeking lower carbon footprints are shifting capital toward warm-mix technologies because they cut fuel consumption and asphalt-fume exposure, while agencies tighten specifications through Superpave, Balanced Mix Design, and EN 14023 revisions. Feedstock volatility for SBS (Styrene-Butadiene-Styrene) and SEBS (Styrene-Ethylene-Butylene-Styrene) continues to sway pricing, yet suppliers that integrate circular raw materials or bio-based rejuvenators are shielding margins. The confluence of regulatory push and infrastructure spending guarantees a steady pipeline of public-sector tenders that favor premium binders, sharpening the competitive contest around formulation know-how rather than scale alone.

Key Report Takeaways

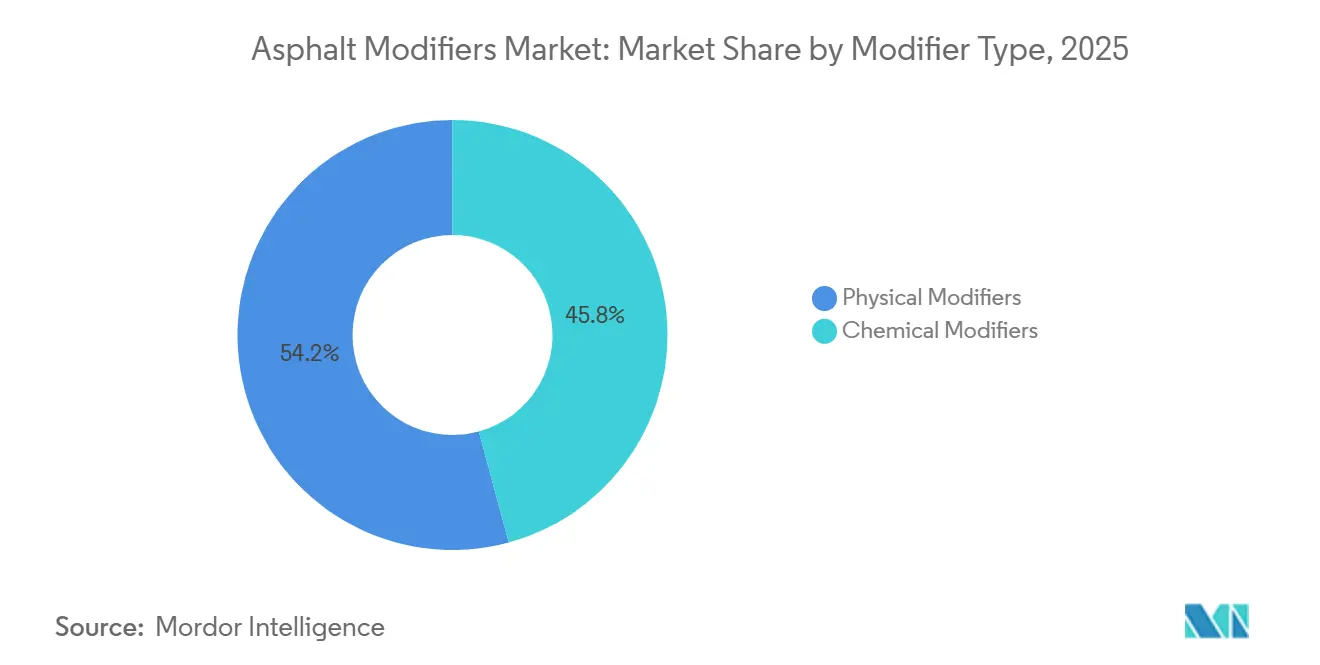

- By modifier type, physical modifiers held 54.22% of the Asphalt Modifiers market share in 2025, while chemical modifiers are forecast to expand at a 5.42% CAGR through 2031.

- By asphalt-mix technology, hot-mix asphalt commanded 70.78% share of the Asphalt Modifiers market size in 2025, while warm-mix asphalt is projected to grow at a 5.55% CAGR through 2031.

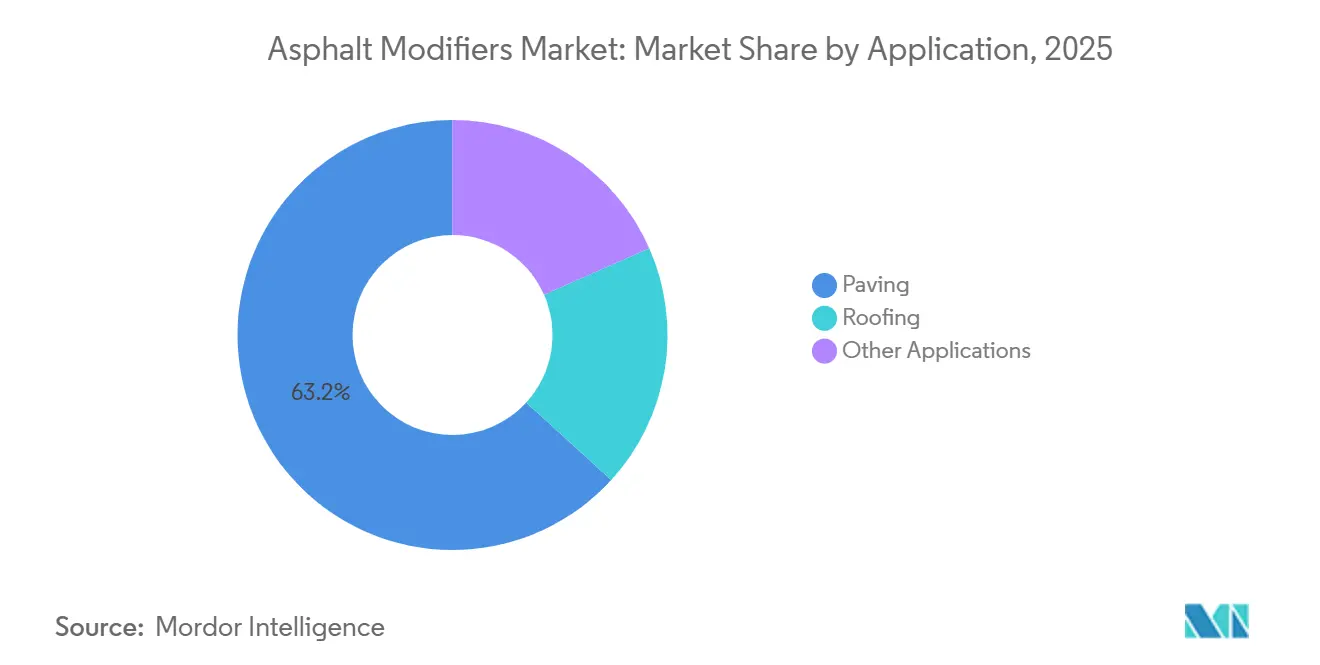

- By application, paving accounted for a 63.22% share of the Asphalt Modifiers market size in 2025 and is advancing at a 5.61% CAGR through 2031.

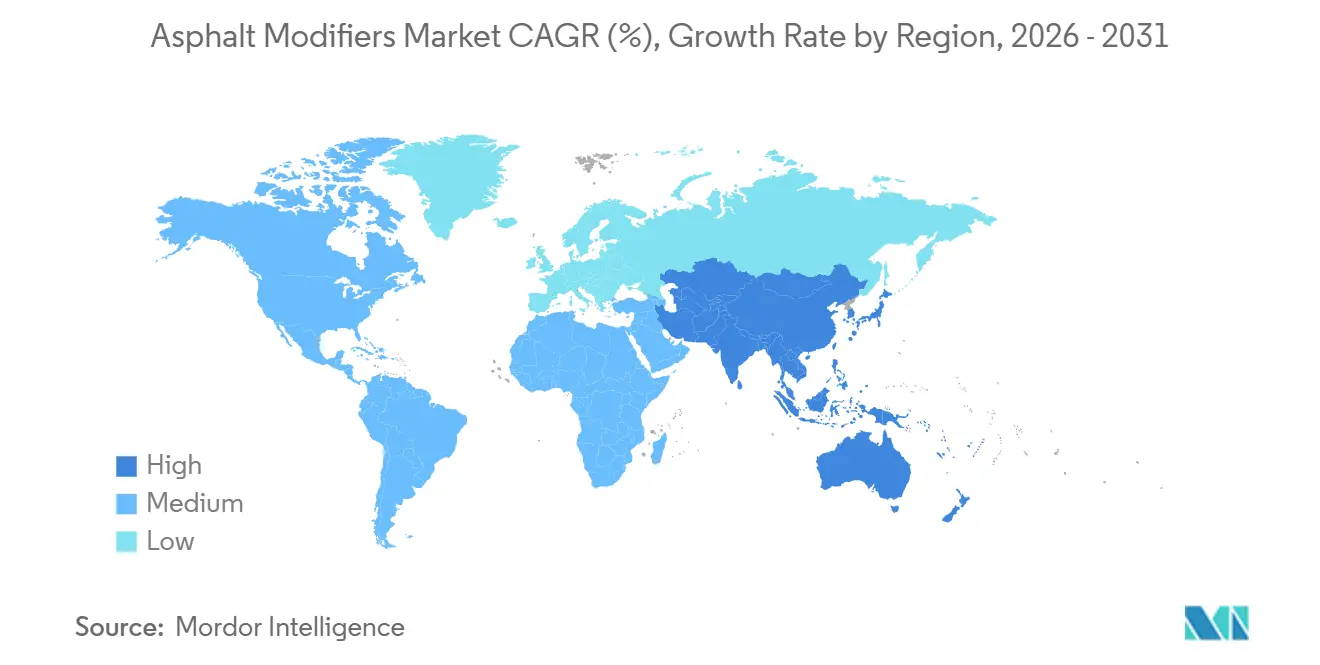

- By geography, Asia-Pacific led with 38.43% of the Asphalt Modifiers market share in 2025, while it is expected to grow at a 5.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Asphalt Modifiers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High traffic density and heavier axle loads | +1.2% | Global with peak intensity in APAC and North America | Medium term (2-4 years) |

| Mandated performance-based specifications | +1.0% | North America, Europe, Australia, emerging in ASEAN and the Middle East | Long term (≥ 4 years) |

| Net-zero carbon targets accelerating warm-mix | +0.9% | Europe, North America, select APAC cities | Medium term (2-4 years) |

| Surge in graphene and nano-reinforced R&D | +0.6% | Europe, Japan, South Korea, pilots in China and the United States | Long term (≥ 4 years) |

| Circular-economy push for waste-plastic asphalt | +0.8% | Global with strong policy tailwinds in EU, India, selected US states | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Traffic Density and Heavier Axle Loads

Freight tonnage per lane-kilometer has risen alongside e-commerce logistics, compelling highway agencies to enforce binders that resist rutting and fatigue cracking. China reported average expressway axle loads above 11 tons in 2024, a 15% increase over 2020, triggering mandatory polymer-modified overlays. India requires PG 70-10 binders on high-traffic corridors under Bharatmala Phase II. The United States Long-Term Pavement Performance data show polymer-modified sections posting 30-40% longer service life on truck routes, validating SBS, crumb-rubber, and Ethylene Vinyl Acetate (EVA) chemistries. Transitioning from recipe mixes to performance-graded contracts thus secures a baseline demand stream for modifier suppliers capable of field-proving durability under accelerated loading conditions.

Mandated Performance-Based Specifications (Superpave, BMD)

Superpave and Balanced Mix Design protocols oblige laboratories to verify rutting resistance, fatigue life, and low-temperature cracking before production approval. American Association of State Highway and Transportation Officials (AASHTO)’s 2024 M 320 update introduced intermediate-temperature grading to close loopholes that once favored marginal binders[1]American Association of State Highway and Transportation Officials, “M 320-24 Standard Specification,” transportation.org. Austroads AP-T351, published in 2024, imposes cracking and rutting indices on all federal-aid highways, spurring anti-stripping and rejuvenator uptake in Australia. Europe revised EN 14023 in 2025 to harmonize elastic recovery and softening-point criteria, enabling suppliers with pan-European footprints to streamline testing protocols. These frameworks disadvantage commodity bitumen and elevate suppliers that pair robust formulation libraries with on-site mix optimization.

Net-Zero Carbon Targets Accelerating Warm-Mix Adoption

Warm-mix technologies cut mixing temperatures by 20-40°C, slicing fuel use and CO₂ by up to 30%. Europe’s Fit for 55 embeds life-cycle carbon accounting into tender scoring. Germany now requires warm-mix on federally funded lots above 10,000 tons. In the United States, California’s Low Carbon Fuel Standard awards credits that neutralize the 2-5% additive premium, catalyzing contractor uptake. Honeywell reports double-digit growth for its zeolite and surfactant systems across both regions. Coupled with contractor safety gains from lower fume generation, warm-mix stands out as the asphalt modifiers market’s fastest-moving technology niche.

Surge in Graphene and Nano-Reinforced Binder R&D

Graphene oxide and carbon nanotubes deliver double-digit gains in rutting and cracking resistance at sub-0.5 wt% dosages. Iterchimica’s Gipave lifted rut resistance by 20% on Italy’s A4 motorway in 2024. NCAT (National Center for Asphalt Technology)’s five-year United States study confirmed graphene sections kept IRI (International Roughness Index) below 1.5 m/km after 2 million ESALs (equivalent single-axle loads) versus 2.1 m/km for SBS mixes. Japan funds a nanotube consortium aiming for commercialization in 2027. Despite a price premium of USD 50-150/kg, airports and toll-road operators are paying for the lifecycle savings, signaling a future pivot toward nano-reinforcement once dispersion and cost barriers fall.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health and fume-exposure concerns for crews | –0.7% | North America, EU | Short term (≤ 2 years) |

| Volatile pricing of SBS/SEBS and bio-feedstocks | –0.9% | Global, acute in import-dependent regions | Short term (≤ 2 years) |

| Municipal specification inertia | –0.5% | South America, Sub-Saharan Africa, parts of Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Health and Fume-Exposure Concerns for Paving Crews

The Occupational Safety and Health Administration (OSHA) limits asphalt-fume exposure to 5 mg/m³ TWA (time-weighted average), and NIOSH (National Institute for Occupational Safety and Health) recommends 0.5 mg/m³. The European Union (EU) classifies certain bitumen fractions as SVHCs (substances of very high concern) under REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals), forcing contractors to invest USD 15,000-50,000 per paver for extraction systems[2]Occupational Safety and Health Administration, “Asphalt Fume Exposure Limits,” osha.gov. A 2025 United States settlement awarded USD 12 million to workers with COPD (chronic obstructive pulmonary disease), spotlighting liability risks. Warm-mix lowers fumes by up to 50%, yet cost premiums and lax enforcement slow uptake in price-sensitive regions. The health imperative accelerates modifier demand where regulators wield strict penalties and carbon credits subsidize warm-mix additives.

Volatile Pricing of SBS/SEBS and Bio-Based Feedstocks

Butadiene and styrene volatility, Asian spot butadiene jumped 35% in 2024-2025, eroding margins for SBS-based modifiers. Kraton lifted SBS prices 10% in April 2025, squeezing contractors locked into fixed-price road bids. Bio-based oils face similar swings; soybean disruptions pushed Cargill’s Anova costs up 20% during 2024-2025. Small contractors without hedging tools revert to unmodified bitumen when polymer premiums exceed USD 150/ton, sacrificing long-term pavement quality. Integrated majors with captive monomer streams or synthetic biology pilots now hold a resilience edge.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modifier Type: Chemical Modifiers Gain on Durability Mandates

The physical modifiers held 54.22% of the Asphalt Modifiers market share in 2025, while the chemical modifiers are climbing at a 5.42% CAGR during the forecast period (2025-2031). Anti-stripping amines now appear in every moisture-susceptible tender across the United States. Southeast, while liquid warm-mix surfactants scale rapidly under EU carbon budgets. BASF’s B2Last promises a 15-20% life-extension without added binder, giving cash-strapped agencies a direct cost-out lever. Rejuvenators such as Cargill’s plant-oil line let contractors push recycled asphalt pavement (RAP) past 30% while meeting performance grade (PG) targets.

Nano-clay and graphene fetch premium pricing in airports where one night of runway closure outweighs additive cost. Physical modifiers remain the volume mainstay because SBS and crumb rubber underpin most highway overlays, yet their growth tapers as liquid systems simplify plant dosing and reduce stock-keeping units. Hybrid solutions, Kraton’s CirKular+ pairs SBS with recycled plastics, blur category lines, pointing toward a portfolio future where elasticity, adhesion, and carbon intensity are tuned simultaneously.

By Asphalt Mix Technology: Warm-Mix Outpaces Amid Carbon Accounting

Hot-mix retains absolute scale, with a market share of 70.78% in 2025, supported by legacy batch plants and regions without carbon pricing. Its share, however, slips as national ministries such as Germany’s BMDV (Federal Ministry for Digital and Transport (BMDV)) lock warm-mix into procurement over 10,000 tons. Warm-mix asphalt is projected to advance at a 5.55% CAGR during the forecast period (2026-2031), the fastest among all mix types. The asphalt modifiers market size for warm-mix additives is forecast to reach significant values by 2031 as Europe’s Fit for 55 and California’s Low Carbon Fuel Standard (LCFS) convert environmental savings into financial credits. Contractors report 15-30% burner-fuel cuts and cooler site temperatures that extend paving windows into colder months.

Cold and half-warm mixes stay niche, yet bio-emulsion breakthroughs could unlock low-traffic municipal lanes if demonstration projects prove durability. The specification overhaul within AASHTO M 320, now capturing intermediate fatigue, further boosts polymer demand within warm-mix formulations because lower mixing temperatures necessitate stiffer, more elastic binders to maintain rut resistance.

By Application: Paving Dominates Infrastructure-Led Volume

Paving absorbed 63.22% of global demand in 2025 and will log the fastest application growth at 5.61% CAGR through 2031, riding the USD 110 billion United States Infrastructure Act, China’s USD 140 billion expressway push, and India’s USD 7.8 billion Bharatmala Phase II. Heavy-axle corridors require PG 70-10 or better, effectively ensuring polymer inclusion. Airport runways, ports, and industrial yards generate outsized revenue via graphene or aramid fiber solutions that command double-digit price premiums.

Roofing, dependent on commercial real-estate cycles and facing TPO competition, lags with mid-single-digit growth. As municipalities lean on performance-grade tenders and life-cycle costing, paving remains the bellwether indicator for overall asphalt modifiers market expansion.

Geography Analysis

Asia-Pacific dominates with 38.43% of 2025 revenue and is on course for 5.92% CAGR to 2031, driven by China’s expressway overlays, India’s 50,000 lane-kilometer rollout, and ASEAN megaprojects like Indonesia’s Trans-Sumatra Highway. Regional polymer capacity in China and South Korea insulates supply chains, while Japan’s nanotube program positions the archipelago as a technology exporter.

In North America, the asphalt modifiers market size is buoyed by the Infrastructure Investment and Jobs Act, but mature road networks temper growth relative to the Asia Pacific. Carbon-credit incentives push warm-mix penetration in California and British Columbia.

Europe leverages Fit for 55, circular-plastics mandates, and a warm-mix requirement on German federal projects to nudge specifications toward low-carbon binders, yet fiscal austerity in parts of Southern Europe weighs on tender volumes.

The Middle East’s Vision 2030 corridors and NEOM’s extreme-temperature pavements necessitate SBS and devulcanized-rubber blends, while South America and Sub-Saharan Africa move sluggishly amid funding gaps and testing constraints, keeping modifier penetration below 15% outside premium toll roads.

Competitive Landscape

The Asphalt Modifiers market is moderately consolidated. Competitive stamina now depends on feedstock diversification, lab-to-field technical service, and partnerships with waste-management firms securing post-consumer plastic or tire streams. Integrated energy-to-polymer players like ExxonMobil wield cost shields yet must still adapt to nano-reinforcement and bio-routes to protect premium margins.

Asphalt Modifiers Industry Leaders

Dow

Arkema

BASF

Kraton Corporation

Shell plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Kraton implemented global price increases across SBS and SIS product lines to mitigate tariffs and raw-material inflation, directly affecting asphalt modifier's costs.

- September 2024: Shoalhaven City Council of Australia, commissioned a crumb-rubber plant supplying local road projects, strengthening the regional asphalt modifier supply chain.

Global Asphalt Modifiers Market Report Scope

Asphalt is manufactured from the distillation of crude oil during the process of petroleum refining. The major characteristics of asphalt include adhesion, waterproofing, and thermoplastic durability, among others.

The Asphalt Modifiers market is segmented by modifier type, asphalt mix technology, application, and geography. By modifier type, the market is segmented into physical modifiers (plastics (HDPE, SBS, EVA), rubber (crumb-rubber, devulcanized), fibers (cellulose, aramid, glass), and mineral fillers and extenders) and chemical modifiers (anti-stripping agents, warm-mix additives, rejuvenators and antioxidants, and others (nano-clay and graphene)). By asphalt mix technology, the market is segmented into hot-mix asphalt (HMA), warm-mix asphalt (WMA), and cold and half-warm mix. By application, the market is segmented into paving, roofing, and other applications. The report also covers the market size and forecasts for asphalt modifiers in 20 countries across major regions. For each segment, market sizing and forecasts have been done on the basis of value (USD).

| Physical Modifiers | Plastics (HDPE, SBS, EVA) |

| Rubber (crumb-rubber, devulcanized) | |

| Fibers (cellulose, aramid, glass) | |

| Mineral fillers and extenders | |

| Chemical Modifiers | Anti-stripping Agents |

| Warm-mix Additives | |

| Rejuvenators and Antioxidants | |

| Others (nano-clay, graphene) |

| Hot-Mix Asphalt (HMA) |

| Warm-Mix Asphalt (WMA) |

| Cold and Half-Warm Mix |

| Paving |

| Roofing |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN | |

| Australia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordic | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| Qatar | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Modifier Type | Physical Modifiers | Plastics (HDPE, SBS, EVA) |

| Rubber (crumb-rubber, devulcanized) | ||

| Fibers (cellulose, aramid, glass) | ||

| Mineral fillers and extenders | ||

| Chemical Modifiers | Anti-stripping Agents | |

| Warm-mix Additives | ||

| Rejuvenators and Antioxidants | ||

| Others (nano-clay, graphene) | ||

| By Asphalt Mix Technology | Hot-Mix Asphalt (HMA) | |

| Warm-Mix Asphalt (WMA) | ||

| Cold and Half-Warm Mix | ||

| By Application | Paving | |

| Roofing | ||

| Other Applications | ||

| Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Nordic | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| Qatar | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How big is the asphalt modifiers market in 2026?

It stands at USD 5.18 billion, on track for USD 6.71 billion by 2031 at 5.31% CAGR.

Which modifier type is growing fastest?

Chemical additives are rising at 5.42% CAGR, propelled by warm-mix surfactants and anti-stripping agents.

Why is warm-mix asphalt gaining share?

Lower fuel use, carbon-credit revenue, and reduced fume exposure make warm-mix economically and socially attractive.

Which region leads demand?

Asia-Pacific accounts for 38.43% of 2025 revenue and is advancing at 5.92% CAGR through 2031.

What is the main restraint on adoption in developing regions?

Municipal specification inertia and limited lab infrastructure slow performance-graded binder uptake.

Page last updated on: