Green Cement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 35.1 Billion |

| Market Size (2031) | USD 49.46 Billion |

| Growth Rate (2026 - 2031) | 7.10% CAGR |

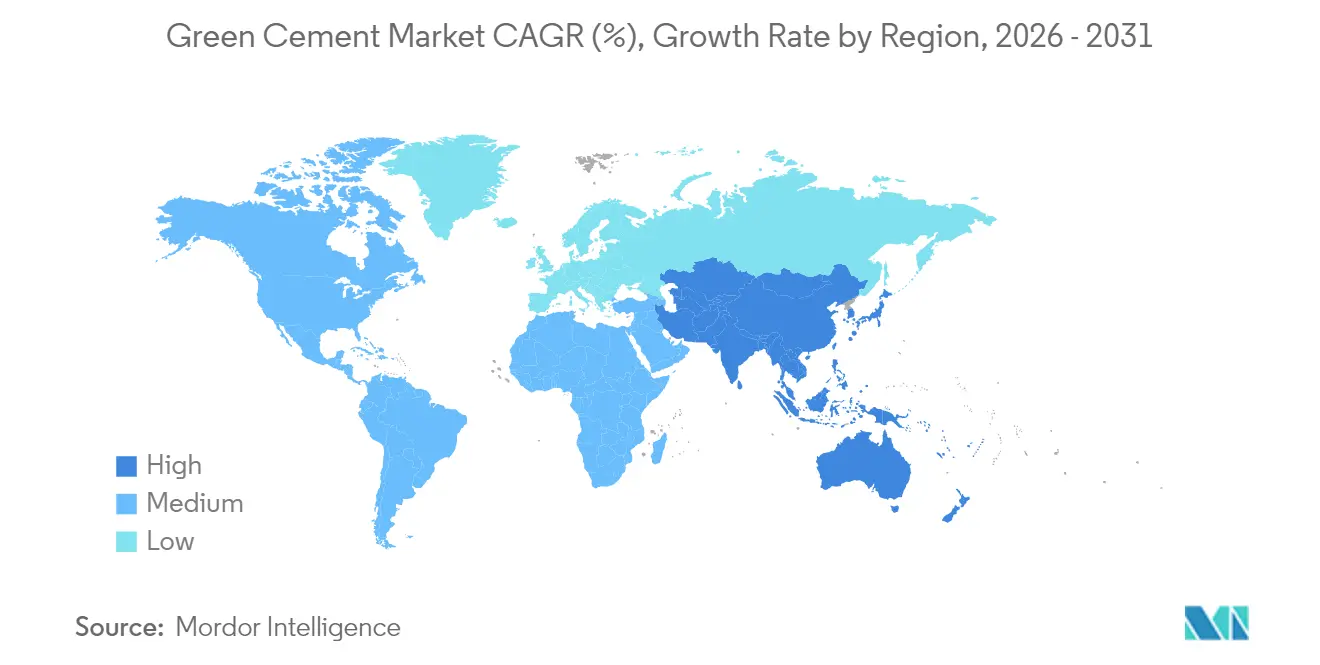

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

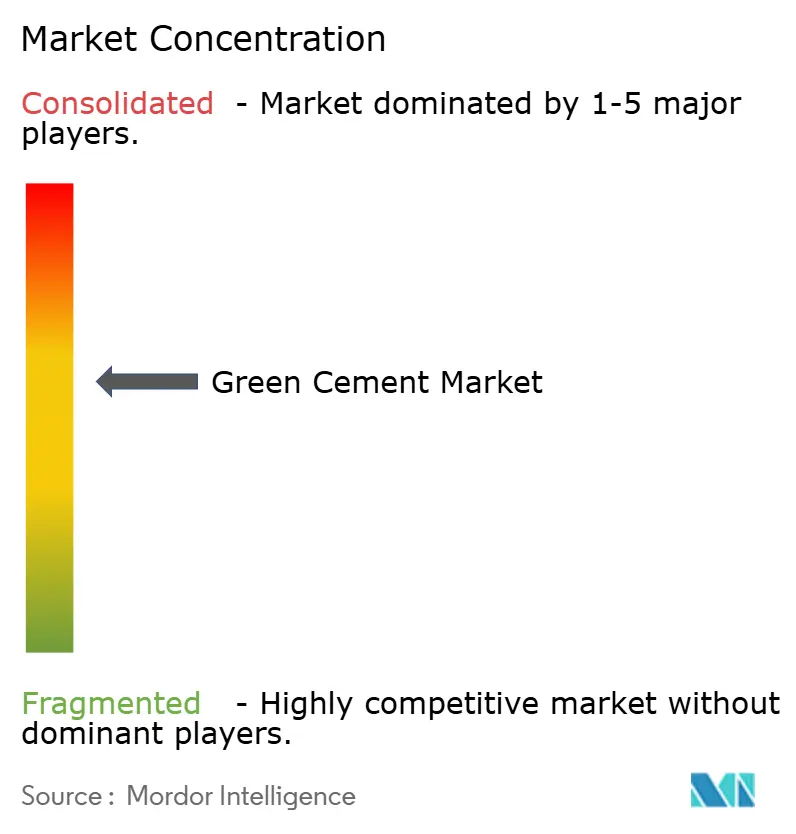

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Green Cement Market Analysis by Mordor Intelligence

The Green Cement market size is expected to grow from USD 32.77 billion in 2025 to USD 35.1 billion in 2026 and is forecast to reach USD 49.46 billion by 2031 at 7.1% CAGR over 2026-2031. Regulatory mandates, rising carbon prices, and procurement rules that favor low-carbon materials move the green cement market from niche status to mainstream selection in public and private projects. Fly-ash-based formulations command the largest revenue share, while infrastructure spending and ESG-linked financing accelerate uptake across non-residential works. Asia-Pacific provides the fastest growth, whereas North America retains volume leadership because of early policy adoption and mature supply chains. Competitive intensity stays moderate as incumbent cement majors scale green portfolios and specialized producers leverage secured feedstock contracts.

Key Report Takeaways

- By product type, fly-ash-based cement led with 43.55% of the green cement market share in 2025, and is projected to expand at a 7.62% CAGR through 2031.

- By construction sector, non-residential works accounted for 57.80% of the green cement market size in 2025 and are forecast to advance at an 8.15% CAGR to 2031.

- By geography, North America held 37.55% revenue share of the green cement market in 2025; Asia-Pacific is set to register the fastest regional CAGR at 7.94% during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Green Cement Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global decarbonisation mandates & ESG-centric building codes | +2.10% | Global, led by EU & North America | Medium term (2-4 years) |

| Rising carbon pricing & emissions-trading schemes | +1.80% | EU, California, select APAC markets | Long term (≥ 4 years) |

| APAC urbanisation surge requiring low-carbon materials | +1.50% | APAC core, spill-over to MEA | Short term (≤ 2 years) |

| Abundant SCM feedstocks (fly-ash, slag) lowering costs | +1.20% | Coal-heavy regions worldwide | Medium term (2-4 years) |

| Commercialisation of hydrogen-fuelled kilns | +0.90% | EU, select North American plants | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global Decarbonization Mandates & ESG-Centric Building Codes

Mandatory low-carbon procurement policies drive immediate demand shifts from ordinary Portland cement to verified green formulations. California targets a 40% emissions cut for its cement sector by 2035 and net-zero by 2045, anchoring similar actions in other U.S. states[1]California Air Resources Board, “Cement Sector Net-Zero Strategy,” arb.ca.gov . The EU’s revised Construction Products Regulation obliges digital passports and CO₂ disclosure for concrete from 2024, pushing producers already equipped with life-cycle documentation to the front of tender lists. France, Denmark, Ireland, and New York State have each introduced progressive emissions ceilings or Buy Clean rules that make compliant materials the default choice rather than a premium option. As jurisdictions replicate pioneering statutes, the green cement market gains a policy-driven growth floor that traditional producers can meet only by retrofitting kilns or partnering with specialized suppliers.

Rising Carbon Pricing & Emissions-Trading Schemes

Carbon costs alter clinker economics by turning CO₂ into a direct expense. The EU Emission Trading System gradually withholds free allowances, prompting cement manufacturers to accelerate low-carbon substitutions or risk margin compression. China’s national trading platform now covers cement, expanding cost pressure to the world’s largest producer. As more regions price carbon, supplementary cementitious materials gain relative competitiveness, and the green cement market benefits from a structural cost advantage over legacy products.

APAC Urbanization Surge Requiring Low-Carbon Materials

India’s accelerating infrastructure buildout contrasts with China’s moderated real-estate cycle, yet both markets enforce stricter environmental rules that raise demand for low-carbon binders. Regional utilities, transport authorities, and private developers incorporate sustainability clauses that specify green cement in designs for metro lines, data centers, and renewable-energy foundations. With APAC electricity generation having risen 16.5-fold between 1971 and 2018, the construction sector remains under pressure to decarbonize quickly—even as concrete volumes grow[2]Asian Development Bank, “Asia’s Infrastructure Growth and Emissions,” adb.org .

Abundant SCM Feedstocks Lowering Costs

Fly ash continues to dominate as a supplementary cementitious material, representing nearly 90% of global pozzolan use and helping green cement achieve price parity in many regions. Harvested ash from legacy ponds—now 10% of recycled volumes in the United States—extends supply life even as coal closures mount. Concurrently, steel-slag supply faces uncertainty due to electric arc furnace adoption, directing producers to sign long-term contracts or acquire processing assets, as seen in Heidelberg Materials’ purchase of The SEFA Group.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Performance scepticism among builders & contractors | -1.40% | Global, acute in emerging markets | Short term (≤ 2 years) |

| Fragmented standards in emerging markets | -0.80% | APAC, MEA, Latin America | Medium term (2-4 years) |

| Shrinking slag supply as steel shifts to EAF/DRI | -1.10% | Steel-producing regions worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Performance Scepticism Among Builders & Contractors

Some contractors resist specification changes, citing extended curing, cold-weather set delays, and inconsistent regional availability of supplementary materials. Standards bodies work to replace prescriptive mix limits with performance-based guidelines, yet knowledge gaps persist, especially in small and mid-size firms. Demonstration projects and targeted training remain essential for mainstream adoption.

Fragmented Standards in Emerging Markets

Divergent definitions of “green cement” across national codes complicate compliance for multinationals and inflate testing costs. Regulators in Asia, the Middle East, and Latin America advance at uneven paces, which slows cross-border project execution and supply consolidation. Technical assistance programs and regional alignment initiatives aim to unify standards over the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fly-Ash Dominance Faces Supply Constraints

Fly-ash-based formulations kept a 43.55% green cement market share in 2025, underscoring their status as the default low-carbon substitute where coal-combustion residues remain abundant. Producers leverage mature logistics and well-documented performance to serve large infrastructure contracts and government tenders. However, declining coal generation narrows future feedstock pools, prompting companies to harvest legacy ash ponds or shift toward limestone-calcined clay blends. LC3 technology, able to trim emissions by up to 40%, gains visibility as laboratories validate mechanical parity with ordinary Portland cement. Silica-fume-based variants occupy high-specification niches, delivering impermeable concrete suited to marine and chemical containment structures. Slag-based alternatives struggle with impending supply shifts but retain relevance near integrated steelworks. Novel binder chemistries, including geopolymer concretes, progress through pilot projects that could diversify the green cement market if scale economics improve.

Growing diversification reduces over-reliance on any single supplementary stream and insulates producers from raw-material shocks. With harvested ash constituting 10% of recycled U.S. fly ash, supply security improves, yet processing costs rise. Strategic agreements between cement makers and utility coal-ash reclamation entities therefore feature prominently in recent deal flow. Slag-grinding partnerships and clay-calcination joint ventures become equally critical as companies balance technical feasibility, emissions objectives, and raw-material economics.

By Construction Sector: Infrastructure Drives Non-Residential Leadership

Non-residential projects held 57.80% of 2025 revenues and will advance at an 8.15% CAGR through 2031, reflecting policy-backed spending on transport corridors, grid upgrades, and public buildings that now specify verified low-carbon mixes. Procurement documents increasingly mandate third-party environmental product declarations, giving compliant producers a clear channel to recurring work. Commercial real-estate developers also integrate green cement into core-and-shell scopes to secure sustainability certifications that attract institutional investors.

Residential uptake grows more gradually. Although mortgage-rate declines in 2025 could lift housing starts, cost-sensitive builders remain cautious about adopting unfamiliar binders without scheduling assurances. Trials in Egypt show potential 44.5% CO₂ savings in non-structural blocks using modified green formulations. As building codes tighten and consumer awareness rises, the segment should close adoption gaps, yet near-term growth continues to lean on large civil works where public procurement dictates material choices.

Geography Analysis

North America retained 37.55% of 2025 revenues, anchored by federal and state Buy Clean rules, early carbon-capture pilots, and high contractor familiarity with blended cements. Heidelberg Materials’ Mitchell CCS project alone targets geological storage for more than 50 million t of CO₂ over 30 years, signaling infrastructure that can underpin long-run volume commitments. Supply availability differs by region: Midwest states leverage proximity to coal-ash basins, while coastal areas import slag or calcined clay to meet specifications.

Asia-Pacific registers the fastest 7.94% CAGR to 2031, fueled by India’s multi-year infrastructure pipeline and progressively stricter codes across Southeast Asia. China’s consolidation efforts prompt large groups to upgrade plants with low-carbon lines to retain permits amid property-sector headwinds. Two-thirds of global high-speed rail networks reside in the region, requiring concrete that satisfies tightening emissions caps and boon the green cement market as projects replenish track and station stock.

Europe blends robust climate policy with mature industrial capabilities. Ireland’s 2024 mandate for low-carbon cement in all state projects and Denmark’s 2025 emissions ceiling of 7.1 kg CO₂e/m²/year set influential benchmarks. Carbon pricing ensures that the green cement market size expands despite construction-volume volatility, as CO₂ costs tilt bid evaluations toward low-clinker mixes. The Middle East and Africa witness emerging demand, especially in Gulf economies planning hydrogen hubs and large-scale public works, yet fragmented standards and limited on-site expertise slow penetration until harmonized guidelines mature.

Mordor Intelligence provides coverage of the green cement market across other key regional markets, including Middle East, Africa, Europe, Asia, and North America, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The green cement market exhibits moderately consolidated concentration. Holcim, Heidelberg Materials, and Cemex exploit integrated logistics and brand recognition while retrofitting kilns for alternative fuels and carbon capture. CarbonCure pursue differentiated chemistries that circumvent clinker altogether, targeting early adopters seeking greater emissions cuts than blended cements offer.

M&A activity concentrates on feedstock control and technology access. Heidelberg Materials’ takeover of fly-ash recycler The SEFA Group secures consistent pozzolan supply along the U.S. Eastern Seaboard. Cemex’s minority stakes in KC8 Capture Technologies and HiiROC provide in-house pilots for solid-carbon capture and hydrogen production. Vertical integration into ash harvesting, clay calcination, and renewable-power procurement strengthens margin resilience as carbon costs rise.

Strategic collaboration emerges through the Global Cement and Concrete Association’s Green Cement Technology Tracker, which now monitors calcined-clay kiln roll-outs to facilitate knowledge sharing. Producers co-invest in R&D to de-risk novel binders and jointly lobby for performance-based codes. The resulting ecosystem encourages portfolio differentiation while maintaining baseline interoperability for global contractors—an environment in which the green cement market can scale without compromising structural performance requirements.

Green Cement Industry Leaders

Cemex S.A.B DE C.V.

Heidelberg Materials

Holcim

UltraTech Cement Ltd.

Votorantim Cimentos

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Hoffmann Green has announced that it has received a major certification for its H-UKR 0% clinker cement in the United States, which is also recognized in Saudi Arabia. As clinker-free cement is categorized as a type of green cement, this certification is anticipated to enhance the company's position in the green cement market.

- December 2023: Hoffmann Green Cement Technologies has extended its 2021 partnership with the Centre Scientifique et Technique du Bâtiment for three more years. This extension ensures faster assessments of its technologies, including the innovative clay-based solutions. This move is set to accelerate the growth of the green cement market.

Global Green Cement Market Report Scope

Green cement is an environmentally friendly cement that is manufactured using a carbon-negative technique. Most of the raw materials needed to make green cement are waste from industrial work. The primary components used in the production of green cement are blast furnace slag and fly ash. It offers higher strength, longevity, crack resistance, and low chloride permeability.

The green cement market is segmented by product type, construction sector, and geography. Based on product type, the market is segmented into fly ash-based, slag-based, limestone-based, silica fume-based, and other product types. Based on the construction sector, the market is segmented into residential and non-residential sectors. The report also covers the market size and forecasts for the green cement market in 15 countries across major regions.

For each segment, market sizing and forecasts have been done based on revenue (USD million).

| Fly-Ash-Based |

| Slag-Based |

| Limestone-Based |

| Silica-Fume-Based |

| Other Product Types |

| Residential |

| Non-Residential |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Product Type | Fly-Ash-Based | |

| Slag-Based | ||

| Limestone-Based | ||

| Silica-Fume-Based | ||

| Other Product Types | ||

| By Construction Sector | Residential | |

| Non-Residential | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the green cement market?

The green cement market size stands at USD 35.1 billion in 2026 and is projected to grow to USD 49.46 billion by 2031.

Which product type leads the market?

Fly-ash-based formulations lead with 43.55% revenue share, supported by established supply chains and proven performance.

Which region shows the fastest growth?

Asia-Pacific records the highest forecast CAGR at 7.94%, driven by large infrastructure pipelines and tightening environmental codes.

How do carbon prices influence green cement adoption?

Rising carbon prices directly increase the cost of clinker-intensive cement, making low-carbon alternatives cost-competitive and accelerating substitution.

What are the main challenges facing the green cement industry?

Supply constraints for supplementary materials, performance skepticism among contractors, and fragmented standards in emerging markets remain key hurdles.

Which companies are the major players in this market?

Holcim, Heidelberg Materials, Cemex S.A.B DE C.V., UltraTech Cement Ltd., and Votorantim Cimentos are the major players in the green cement market.

Page last updated on: