Market Overview

| Study Period | 2021 - 2031 |

|---|---|

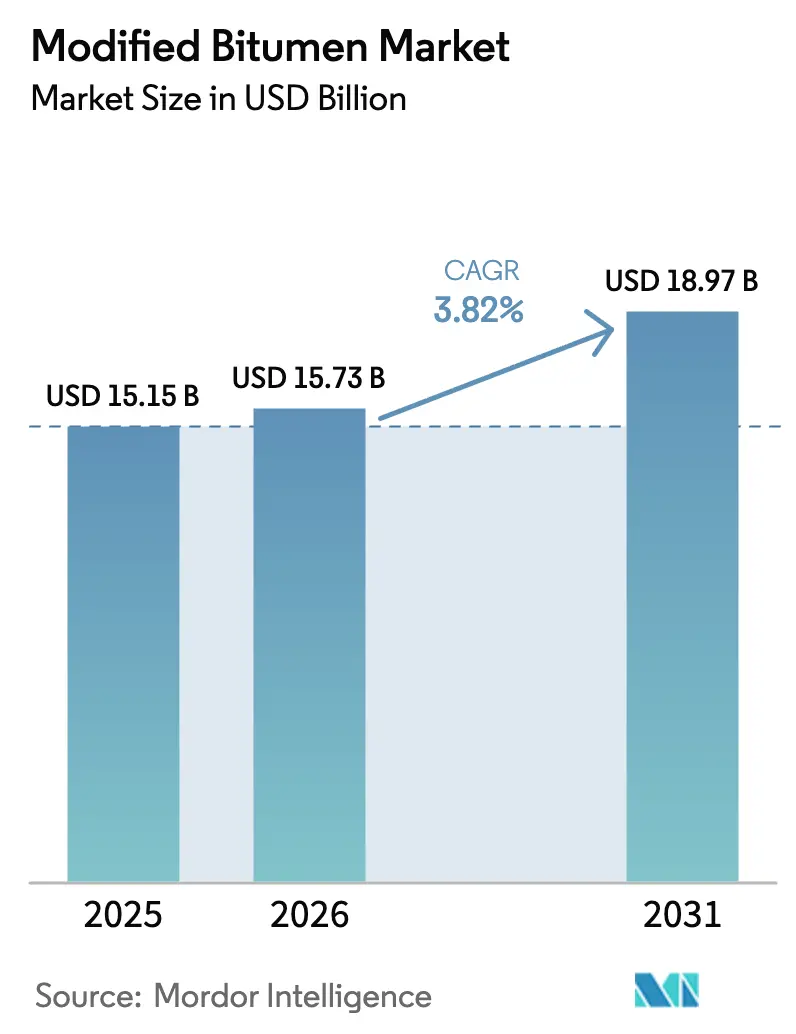

| Market Size (2026) | USD 15.73 Billion |

| Market Size (2031) | USD 18.97 Billion |

| Growth Rate (2026 - 2031) | 3.82% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Modified Bitumen Market Analysis by Mordor Intelligence

The Modified Bitumen Market size is projected to be USD 15.15 billion in 2025, USD 15.73 billion in 2026, and reach USD 18.97 billion by 2031, growing at a CAGR of 3.82% from 2026 to 2031. Sustained road-building incentives in the United States, India, and Europe are anchoring demand for polymer-enhanced binders, while rising performance specifications in China and Australia accelerate substitution away from commodity asphalt. Middle East megaprojects and Africa’s corridor upgrades are creating white-space opportunities for APP-based heat-reflective membranes, whereas North American and European roofing markets shift toward self-adhered systems to reduce labor-site fires and address installer shortages. Volatile crude-oil prices, tightening VOC and PAH caps, and divergent feedstock trends for SBS and APP continue to compress blender margins, favoring vertically integrated oil majors and specialty-polymer suppliers. Overall, suppliers with diversified modifier portfolios, bio-based research and development pipelines, and proximity to stimulus-funded projects are best positioned to capture steady yet measured growth.

Key Report Takeaways

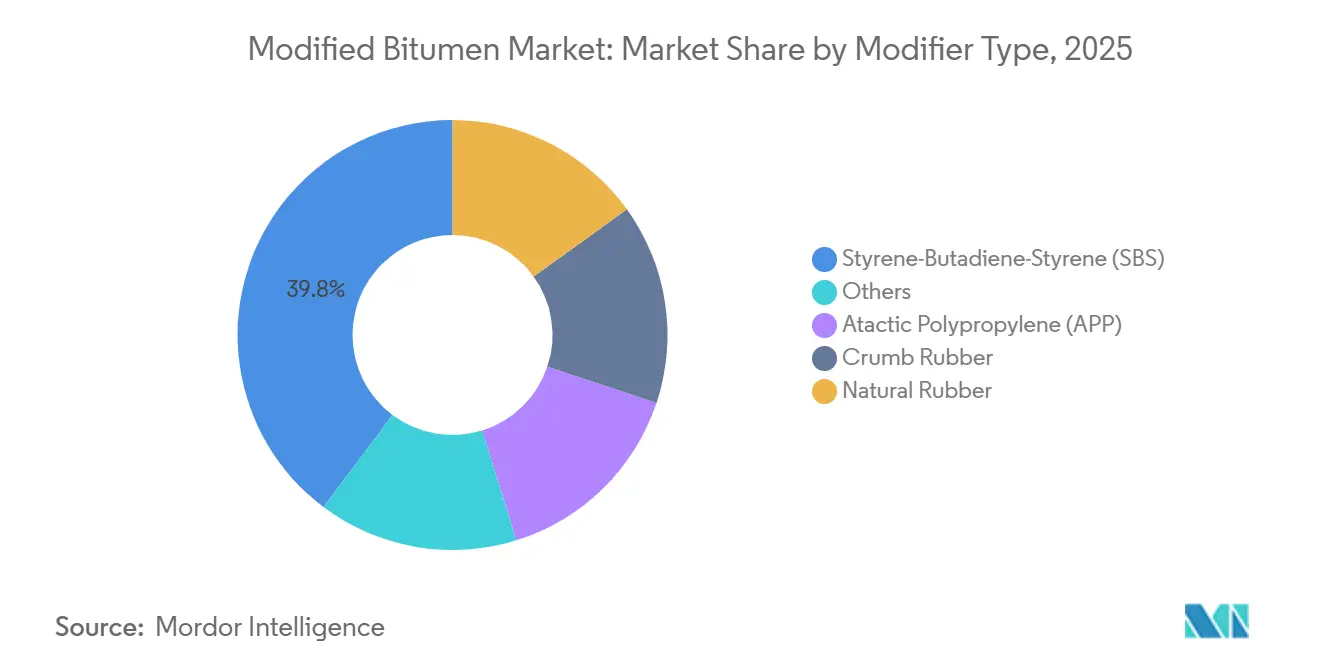

- By modifier type, styrene-butadiene-styrene (SBS) held 39.75% of the modified bitumen market share in 2025, while atactic polypropylene (APP) is forecast to grow at a 4.29% CAGR through 2031.

- By application method, hot asphalt commanded 45.74% of the modified bitumen market size in 2025 and is projected to expand at a 4.01% CAGR between 2026 and 2031.

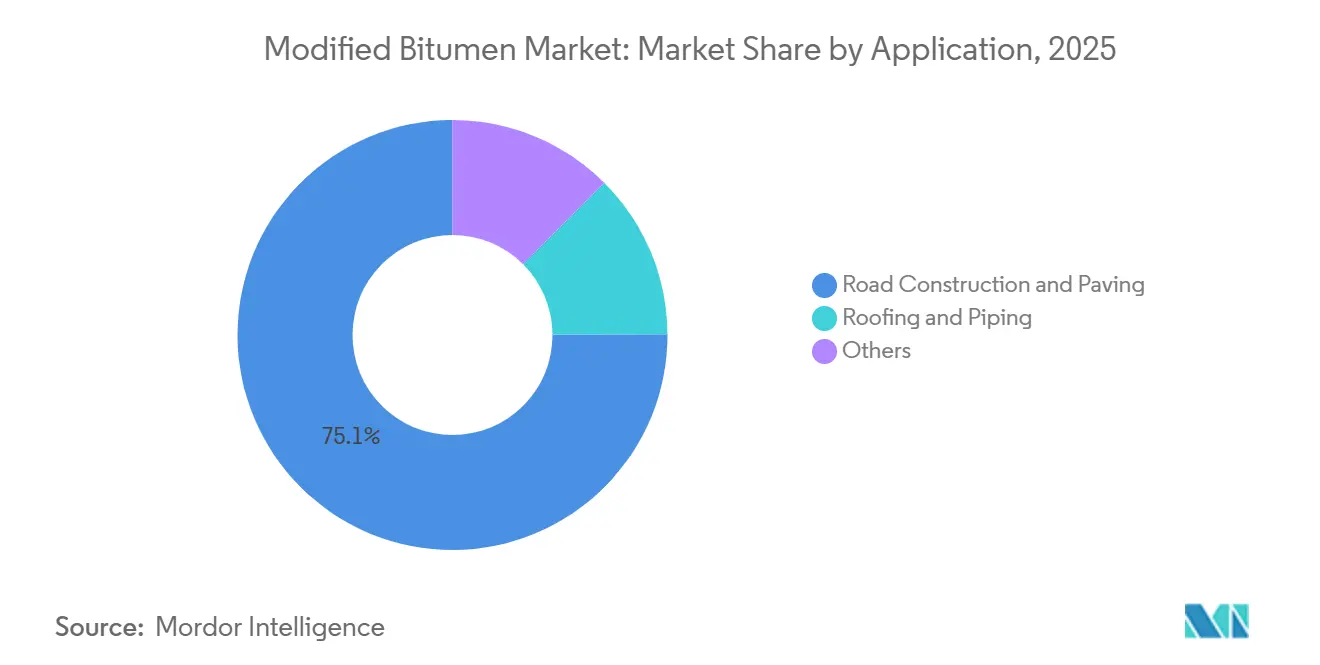

- By application, road construction accounted for 75.05% of the modified bitumen market size in 2025 and is advancing at a 3.96% CAGR through 2031.

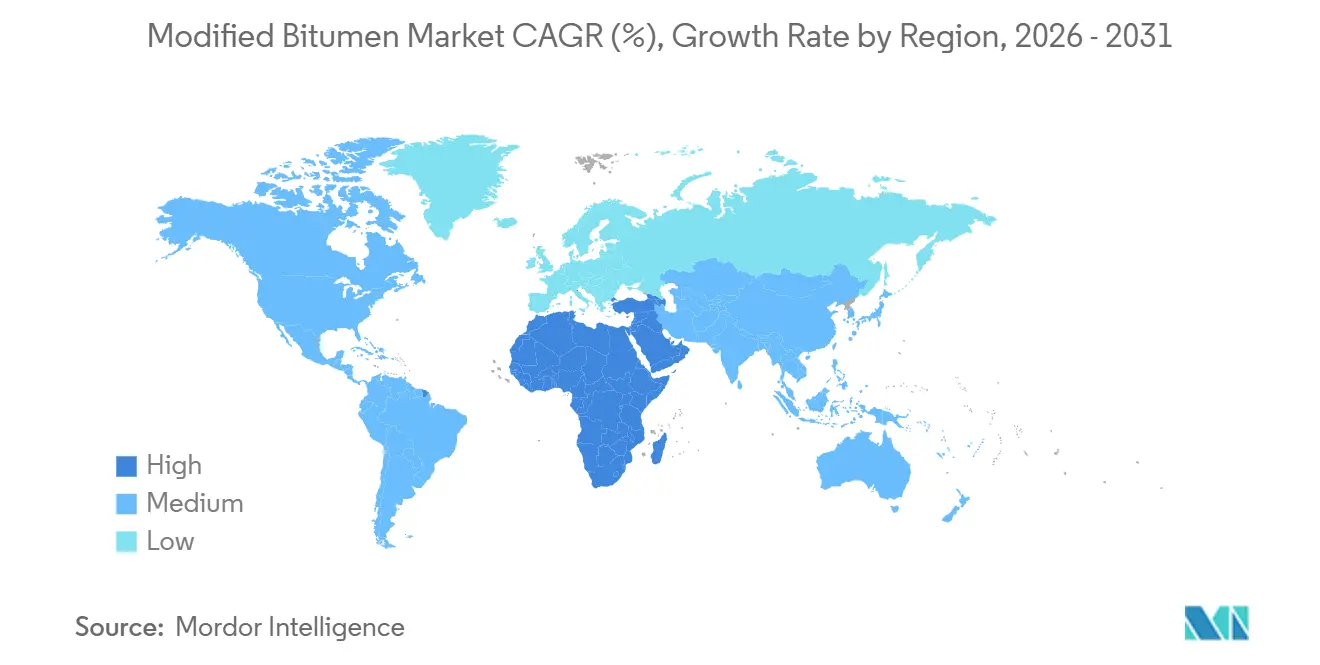

- By geography, Asia-Pacific led with 44.36% of 2025 revenue, while the Middle East and Africa region is set to record the fastest 5.98% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Modified Bitumen Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Road-building stimulus in the US IIJA, EU CEF-2, and India PM-Gatishakti | +1.2% | North America, Europe, Asia-Pacific (India core) | Medium term (2–4 years) |

| Tightening asphalt-performance specs in China's JTGF40-2021 and Austroads hybrid-PMB standards | +0.8% | Asia-Pacific (China, Australia, ASEAN spill-over) | Short term (≤ 2 years) |

| Shift to self-adhered and cold-applied membranes cutting labor-site fires | +0.6% | North America, Europe | Medium term (2–4 years) |

| Recycled-rubber (crumb-rubber-PMB) quotas in EU Green Deal roads | +0.5% | Europe, with early adoption in Netherlands, France, Spain | Long term (≥ 4 years) |

| Bio-polymer (lignin, algae) modified binders hitting commercial scale | +0.4% | Global, pilot deployments in Scandinavia, California | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Road-Building Stimulus in the US IIJA, EU CEF-2, and India PM-Gatishakti

Multi-year lettings, fueled by substantial funding allocations, are driving up the consumption of polymer-modified asphalt. The US Infrastructure Investment and Jobs Act has earmarked significant funds for highways. While a large portion of this amount is obligated, only a fraction has been spent as of September 2025, hinting at a purchasing peak in the coming years. In India, the PM-Gatishakti corridors and the PMGSY-IV rural-road initiative are set to cover extensive kilometers, utilizing waste plastic and cold-mix technologies. This move is set to accelerate the adoption of SBS, especially in emerging states. Meanwhile, Europe’s CEF-2 program has tied a significant portion of its budget to climate objectives, pushing projects towards using recycled rubber and bio-polymer binders[1]European Commission, “Connecting Europe Facility-2 Transport Programme,” ec.europa.eu. Suppliers boasting regional blending terminals, sourcing both SBS and APP, and maintaining pre-approved product lists are reaping the benefits as agencies shorten bid timelines. The cumulative result is a notable surge in volumes, albeit unevenly distributed across regions, bolstering the modified bitumen market for the foreseeable future.

Tightening Asphalt-Performance Specs in China JTGF40-2021 and Austroads Hybrid-PMB Standards

China's JTGF40-2021 has set new rutting-resistance thresholds for expressways with high daily traffic, effectively mandating the use of SBS-rich mixes[2]Ministry of Transport China, “JTGF40-2021 Technical Specifications for Highway Asphalt Pavements,” mot.gov.cn. Enforcement began in 2024 in Guangdong and Zhejiang, leading to an increase in SBS demand. Austroads' guidelines for hybrid binders advocate a blend of SBS and crumb rubber, achieving a balance between high-temperature stability and low-temperature flexibility. This approach allows a reduction in polymer dosage while still meeting fatigue criteria. These evolving standards not only shorten payback periods for polymer-blending plants but also narrow competition to pre-qualified suppliers. Furthermore, they expedite the diffusion of technology to ASEAN nations that are adopting codes from Australasia. Contractors who neglect to upgrade their formulations face the risk of warranty voids and project delays. This scenario underscores the growing entrenchment of polymer-modified asphalt specifications within the modified bitumen market.

Shift to Self-Adhered and Cold-Applied Membranes Cutting Labor-Site Fires

In the United States, open-flame torch applications spark numerous roofing fires each year. This surge in incidents is pushing liability premiums upward and shrinking the pool of certified installers. Self-adhered membranes, favored under tightening fire codes in states like California and New York, as well as in Germany, not only slash installation time but also eliminate potential ignition sources. In 2025, industry giants GAF, Firestone, and SOPREMA introduced cold-applied liquid membranes that cure at ambient temperatures, extending their usability in chillier climates. As certified torch installers command high wages in major metropolitan areas, the resultant installer shortage is steering specifications towards self-adhered systems, even with their premium material costs. This labor-driven pivot is amplifying the demand for APP and hybrid membranes, fortifying the modified bitumen market against its usual road-centric fluctuations.

Recycled-Rubber Quotas in EU Green Deal Roads

By 2027, the EU's Circular Economy Action Plan mandates that EU-funded asphalt incorporate post-consumer tire rubber. This move creates a dedicated market for crumb-rubber-modified binders. In pilot projects across the Netherlands, France, and Spain, tire waste was successfully diverted per ton of asphalt, all while adhering to EN 12697 fatigue standards. Large blenders, equipped with in-house grinding capabilities, benefit from economies of scale. However, it's worth noting that this additional processing increases the asphalt cost. Suppliers are now patenting pre-treatment chemistries to counteract low-temperature brittleness. They foresee these innovations gaining traction, especially as the Green Deal procurement transitions from pilot phases to mainstream projects. Looking ahead, the quotas for recycled rubber are poised to provide a consistent boost to the modified bitumen market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude oil price volatility squeezing modifier economics | -0.7% | Global | Short term (≤ 2 years) |

| Skilled torch applicator shortages in North America and Europe | -0.4% | North America, Europe | Medium term (2–4 years) |

| VOC and PAH caps on hot asphalt in California, Germany, Korea | -0.3% | North America (California), Europe (Germany), Asia-Pacific (South Korea) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Oil Price Volatility Squeezing Modifier Economics

In 2025, Brent crude prices remained steady. However, in Asia, SBS spot prices surged due to tight butadiene supplies, leading to a reduction in blender margins. OPEC+ production curbs have kept forward prices elevated. In response to rising feedstock costs, polymer manufacturers are signaling price increases. Notably, government road contracts in India and Southeast Asia seldom incorporate price-escalation clauses, compelling blenders to shoulder the financial spread. While integrated oil majors with their own polymer assets remain shielded from these fluctuations, independent blenders are feeling the squeeze, facing pressures that could lead to consolidation and a diminished supplier diversity in the modified bitumen market.

Skilled Torch-Applicator Shortages in North America and Europe

The share of the United States roofing workers aged 55 and older has increased, while apprenticeship enrollments have declined, creating a noticeable labor gap. Germany is witnessing similar aging trends, leading to higher hourly wages for certified torch applicators. This labor shortage not only delays project timelines but also drives up costs for installed membranes. As a result, building owners are increasingly opting for self-adhered or cold-applied systems. Unless new installation methods gain widespread acceptance, the ongoing workforce attrition is likely to hinder growth in the modified bitumen market's roofing applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modifier Type: SBS Dominance Meets APP’s Heat-Reflective Surge

SBS accounted for 39.75% of the modified bitumen market share in 2025 on the strength of its low-temperature flexibility, especially for Canadian and northern European highways where thermal cracking dictates maintenance cycles. As road agencies in China, the United States, and Europe begin to incorporate SBS performance into their design manuals, the market size for SBS-linked modified bitumen is projected to grow steadily through 2031. APP, by contrast, is forecast to grow at a 4.29% CAGR, propelled by Middle Eastern and North African roofing mandates that require high solar-reflectance membranes under ambient temperatures exceeding 70 °C.

Demand for modified bitumen adjusts according to regional climates and regulatory codes. For instance, while SBS is favored in cold-climate resurfacing initiatives—such as Japan's expressway rehabilitation—APP is the go-to choice for hot, arid regions, especially for warehouse roofs equipped with photovoltaic arrays. Hybrid blends of crumb-rubber and SBS meet the EU's recycled-content standards but remain a niche segment due to challenges in quality control. Meanwhile, early-stage bio-polymer modifiers, currently categorized under "Others," are on the brink of expansion, especially if carbon pricing helps narrow their cost disparity. Suppliers adept at balancing their capacities between SBS and APP can navigate regional fluctuations and tap into the changing dynamics of the modified bitumen market.

By Application Method: Hot Asphalt Holds Specification Ground

Hot asphalt secured 45.74% of revenue in 2025 and will keep a 4.01% CAGR, buoyed by entrenched highway specifications that favor high-temperature polymer dispersion and dense aggregate packing. Hot asphalt plants in the United States are reaping the rewards of a highway rehabilitation budget, while in China, a plant-upgrade program is making waves. These developments are driving the growth of the modified bitumen market.

Cold asphalt technologies are scaling in India’s rural-road builds, cutting curing time to 6 hours and enabling traffic resumption the same day. Torch-applied roofing remains standard in emerging markets, but installer shortages in North America and Europe are shifting share toward self-adhered membranes. Over the forecast horizon, hot asphalt retains primacy for high-traffic roadways, while cold and self-adhered methods capture incremental growth in maintenance, rural, and roofing niches, diversifying the application-method composition of the modified bitumen market.

By Application: Road Construction’s Infrastructure Tailwinds

Road construction and paving represented 75.05% of 2025 revenue, underpinned by deferred maintenance backlogs in the United States and multi-lane expressway rollouts in India and China. This segment of the modified bitumen market size is forecast to register a 3.96% CAGR through 2031 as the U.S. IIJA outlays peak and China’s western provinces tackle connectivity gaps.

Roofing and piping are driven by data-center and warehouse builds that favor modified-bitumen membranes compatible with rooftop solar installations. While road volumes dwarf roofing tonnage, membranes offer higher gross margins and steadier demand, allowing producers to balance portfolio risk. “Other” uses, such as bridge-deck waterproofing and airport runways, supply niche but stable volume streams, further broadening the demand base of the modified bitumen market.

Geography Analysis

Asia-Pacific generated 44.36% of 2025 revenue, driven by China's addition of expressways and India's expansion of highways. Yet, as eastern provinces of China approach network saturation, growth has moderated. Concurrently, India grapples with land-acquisition delays, extending its tender-to-award cycles. Japan, investing heavily annually, emphasizes SBS polymers for expressway overlays, aiming to mitigate fatigue on its aging pavements. Meanwhile, ASEAN's demand surges, buoyed by ADB-financed industrial corridor projects, though challenges like currency risks and political shifts loom large.

The Middle East and Africa region is poised for the fastest 5.98% CAGR. Major investments in transport pipelines, roads for new administrative capitals, and freeway rehabilitation spur this growth. Additionally, the GCC's building codes mandate SRI-compliant APP membranes, while South Africa pushes for recycled-rubber, both bolstering volume prospects. However, the region grapples with funding volatility tied to oil prices and overarching security concerns.

North America and Europe are set to grow at a more tempered pace. As these mature networks pivot from expansion to maintenance, challenges arise. The U.S. National Bridge Inventory flags numerous structures in need of deck membranes. Yet, with IIJA allocations set to wane post-2026 and gas-tax revenues dipping due to rising EV adoption, the future looks uncertain. Across the Atlantic, Europe's CEF-2 dedicates a limited portion of its budget to highways, confining growth to essential resurfacing and urban retrofits. South America, though small and cyclical, sees a glimmer of hope: Brazil's toll concessions for 2024-2025 spark demand, yet macroeconomic instability casts a shadow on the outlook.

Regulatory Landscape

Modified bitumen is shaped by construction-product marketing rules alongside test and specification standards that define performance for roofing and paving applications. In the European Economic Area, Regulation (EU) 2024/3110, the Construction Products Regulation 2024, entered into force in January 2025 and became applicable on January 8, 2026, establishing the framework for placing construction products on the market and shifting requirements from the prior CPR regime. Existing harmonized specifications continue to apply until they are withdrawn or replaced under the new system.

Chemical and environmental compliance also affects formulations and manufacturing practices. REACH compliance via ECHA frames substance registration and restrictions relevant to additives and extender oils, while the US Environmental Protection Agency regulates wastewater discharges from paving and roofing materials manufacturing under the Paving and Roofing Materials Effluent Guidelines (40 CFR Part 443). In North America, ASTM International standards such as ASTM D5147 (sampling and testing of modified bituminous sheet material) and product specifications used for modified bitumen membranes set baseline performance metrics that owners, contractors, and procurement bodies reference.

Value Chain Analysis

The value chain begins with refinery-derived base bitumen supply and specialty modifier feedstocks, notably SBS and APP, together with fillers and performance additives such as anti-stripping agents, UV stabilizers, and carbon black. Modified bitumen is produced by blenders and membrane manufacturers using controlled heating and high-shear mixing to disperse polymers into base bitumen, typically with automated batching and PLC-controlled systems to keep viscosity and dispersion within specification.

Downstream, distribution is split between bulk deliveries to asphalt plants and terminals for road works, and converted rolls, sheets, and liquids supplied through roofing distributors and contractor networks. Product qualification is closely tied to standards and test methods, including ASTM D6164/D6164M for SBS-modified bituminous sheet materials and related ASTM/CSA frameworks for self-adhered systems. This drives demand for in-house or third-party testing capability and pre-approved product listings. Industry associations such as the Association of Modified Asphalt Producers and the Asphalt Roofing Manufacturers Association coordinate technical and policy inputs that influence specification adoption and contractor education, supporting pull-through at both installer and agency levels.

Competitive Landscape

The modified bitumen market studied is fragmented. Integrated oil majors leverage refinery adjacency to control base-bitumen feedstock and offer just-in-time delivery in Houston, Rotterdam, Singapore, and Mumbai. Roofing fabricators integrate membrane production with installation services, offsetting labor inflation yet constraining geographic agility. Emerging bio-polymer entrants are patenting lignin and algae-based modifiers that cut carbon footprints, targeting infrastructure owners with net-zero mandates. Digital logistics platforms in India and Southeast Asia aggregate small-contractor demand, reducing Days Sales Outstanding and clipping transaction fees while improving blender cash flow. Competitive positioning will increasingly hinge on technology adoption, carbon-intensity credentials, and the ability to serve decentralized project pipelines.

Modified Bitumen Industry Leaders

Shell plc

TotalEnergies

COLAS

Gazprom Neft PJSC

Exxon Mobil Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Road-agency procurement is increasingly anchored in verified performance frameworks. In China, JTGF40-2021 enforcement in Guangdong and Zhejiang raises expectations around polymer dispersion control and rutting resistance, while Austroads promotes hybrid-PMB approaches to balance performance with installability.

On the roofing side, installer safety and labor availability are steering demand toward self-adhered and cold-applied modified-bitumen systems, reinforcing APP and hybrid membranes that reduce open-flame installation risk. Sustainability-led formulations also remain a concrete opportunity area, with EU policy direction toward recycled-rubber content in roads, tied to the Circular Economy Action Plan and EN 12697 performance references in pilots. In parallel, research focused on higher reclaimed asphalt pavement enablement, including July 2026 research in Scientific Reports on modified binders supporting higher RAP incorporation, supports product development and service offerings around recycled-content recipes, testing, and supply assurance.

Recent Industry Developments

- June 2026: Bharat Petroleum Corporation Limited (BPCL) announced an agreement to acquire a 40% equity stake in Tiki Tar and Shell India Private Limited (TTSIPL), following approval from the Department of Investment and Public Asset Management (DIPAM). The deal expands BPCL's footprint in value-added bitumen, including polymer modified bitumen, crumb rubber modified bitumen, and emulsions, strengthening its ability to serve specification-driven road programs through an established manufacturing and distribution platform.

- November 2025: IndianOil Total Private Limited (a joint venture of Indian Oil Corporation Ltd. and TotalEnergies Marketing Services) inaugurated a greenfield bitumen-derivatives plant near Chennai (Gummidipoondi) to produce polymer modified bitumen, crumb rubber modified bitumen, and bitumen emulsions. Localized production near a major infrastructure corridor improves lead times and supply reliability for India's road-building pipeline.

- March 2024: Colas secured a long-term agreement to operate four new bitumen storage tanks at an expanded terminal in Durban, South Africa, operated by FFS Refiners. Additional terminal handling and storage supports more consistent supply into the Southern Africa market and improves logistics flexibility for modified and specialty bitumen grades serving road and waterproofing demand.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the modified bitumen market is counted as the value of bitumen that is improved using modifiers (such as polymers or rubber) and then sold for use in paving, roofing, piping, and related waterproofing needs across regions.

Scope exclusions: It does not count standard unmodified paving-grade bitumen, and it also excludes adjacent materials like roofing membranes that do not use modified bitumen as the main binder.

Segmentation Overview

- By Modifier Type

- Styrene-Butadiene-Styrene (SBS)

- Atactic Polypropylene (APP)

- Crumb Rubber

- Natural Rubber

- Others

- By Application Method

- Hot Asphalt

- Cold Asphalt

- Torch-Applied

- By Application

- Road Construction and Paving

- Roofing and Piping

- Others

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle-East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle-East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the fact base and anchor the model inputs to real, observable signals. We leaned on public infrastructure and construction indicators, such as road length additions and spending releases from national transport ministries and statistics agencies, and materials context from organizations such as the International Energy Agency and the World Bank.

To translate demand into a market value, we also referenced public customs and trade statistics for asphaltic products, technical standards and safety notes published by agencies such as ASTM and similar national bodies, and peer-reviewed papers that discuss modifier performance in asphalt and roofing. Company annual reports, investor presentations, and reputable press were reviewed for capacity expansion plans, price commentary, and regional exposure, and paid subscription sources for company financials and patent databases helped validate who is active and where product development is concentrated. The sources listed here are illustrative, and many other public and subscription references were checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was run to pressure-test the desk assumptions and close practical gaps that are hard to read from public data alone, such as where modified bitumen is specified versus substituted in real projects. We spoke with a mix of producers, modifier suppliers, distributors, contractors, and procurement or technical teams across the main consuming regions, so the model reflects how demand is actually formed and priced in paving and roofing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 34% | CXOs: 21% | APAC: 45% |

| Mid tier: 45% | Functional/Unit leaders: 29% | EMEA: 37% |

| Smaller Players: 21% | Managers: 50% | Americas: 18% |

Market-Sizing & Forecasting

Market sizing starts from a top-down build where country-level paving and roofing activity is reconstructed using public construction output, road spending pipelines, and trade signals for asphaltic materials, then converted to modified bitumen demand using adoption rates for performance grades and polymer or rubber modification. The totals are cross-checked against selective bottom-up approximations, such as sampled price per ton by region multiplied by estimated volumes in paving and roofing, followed by supplier and channel checks to see if the implied sales are consistent.

Key inputs that move the model include road construction and resurfacing intensity, roofing re-cover rates for low-slope buildings, modifier penetration in asphalt mixes, binder content assumptions for typical asphalt layers, and regional price spreads tied to crude-linked feedstock movements. Forecasts were produced using scenario analysis, where infrastructure budgets, construction starts, and expected specification tightening were varied, then aligned to what interviewees describe as the most likely adoption path. When bottom-up information is incomplete for smaller markets, gaps are handled through proxy ratios from similar countries and then adjusted for local trade dependency and project mix.

Data Validation & Update Cycle

Outputs are validated through multiple cross-checks so that no single data stream drives the final answer. We compare the implied modified bitumen volumes and values against independent signals like road funding releases, construction output trends, and trade movements, then flag outliers for a second pass review.

Before sign-off, assumptions are rechecked across regions and time series so sudden jumps can be explained by an observed factor such as a price spike, a regulation change, or a capacity shift. The report is refreshed annually, and interim updates are made when material events occur, followed by a final pre-delivery review so clients receive the most current view.

Mordor Intelligence's Modified Bitumen Market Size Versus Other Published Estimates

Published market sizes for modified bitumen often differ because the underlying boundaries are not always the same, even when the topic name looks identical. Differences usually come from what is counted as modified bitumen, which applications are included, the base year chosen, and how prices are converted and trended over time.

The table shows a wide spread in the 2024 to 2026 values, and in Mordor Intelligence's model the market is sized around modified bitumen used across road construction, roofing and piping, and other uses, with value tied to region-level pricing and application-driven demand rather than counting broader bitumen, membranes, or downstream installed system revenues. Some published figures appear to include a wider set of asphalt products or use aggressive price progression assumptions, which can lift the headline number even if physical demand does not move at the same pace.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 15.73 B (2026) | |

| Global Consultancy A | USD 42.76 B (2024) | The estimate likely uses a broader market boundary that can blend modified bitumen with wider asphalt and waterproofing revenues, and it applies higher growth and price ramps across regions, which inflates the value versus a binder-focused definition. |

| Industry Publisher B | USD 24.56 B (2024) | This figure appears to treat building construction demand more broadly, which can pull in roofing system value and related construction materials, and it also uses a different base-year setup that changes the starting point for scaling forward. |

Overall, the comparison mainly points to scope choices and pricing logic as the drivers of the gap, more than any single demand metric. By keeping inputs tied to project activity, modifier penetration, and region-level price checks, the final number stays traceable to clear steps that can be repeated when new construction and cost data is released.

Key Questions Answered in the Report

What is the projected value of the modified bitumen market in 2031?

The market is forecast to reach USD 18.97 billion by 2031 from USD 15.73 billion in 2026, registering a 3.82% CAGR.

Which modifier type is expected to grow fastest through 2031?

APP is projected to record a 4.29% CAGR, benefiting from heat-reflective roofing demand in the Middle East and North Africa.

Why is SBS dominant in cold-climate pavements?

SBS delivers superior low-temperature flexibility and fatigue resistance, meeting strict rut-resistance standards in China, Canada, and northern Europe.

How do labor shortages affect roofing applications?

Scarcity of certified torch applicators in North America and Europe pushes building owners toward self-adhered membranes, which require less specialized labor.

What regions will deliver the highest growth rates?

The Middle East and Africa region is expected to post a 5.98% CAGR, buoyed by Saudi Arabia’s Vision 2030 and Egypt’s New Administrative Capital projects.

How are environmental regulations influencing product innovation?

Tightening VOC and PAH caps alongside carbon-pricing schemes are driving investment in warm-mix additives, recycled-rubber blends, and emerging bio-polymer modifiers.

Page last updated on: