Pervious Concrete Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 5.46 Billion |

| Market Size (2031) | USD 7.45 Billion |

| Growth Rate (2026 - 2031) | 6.41% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

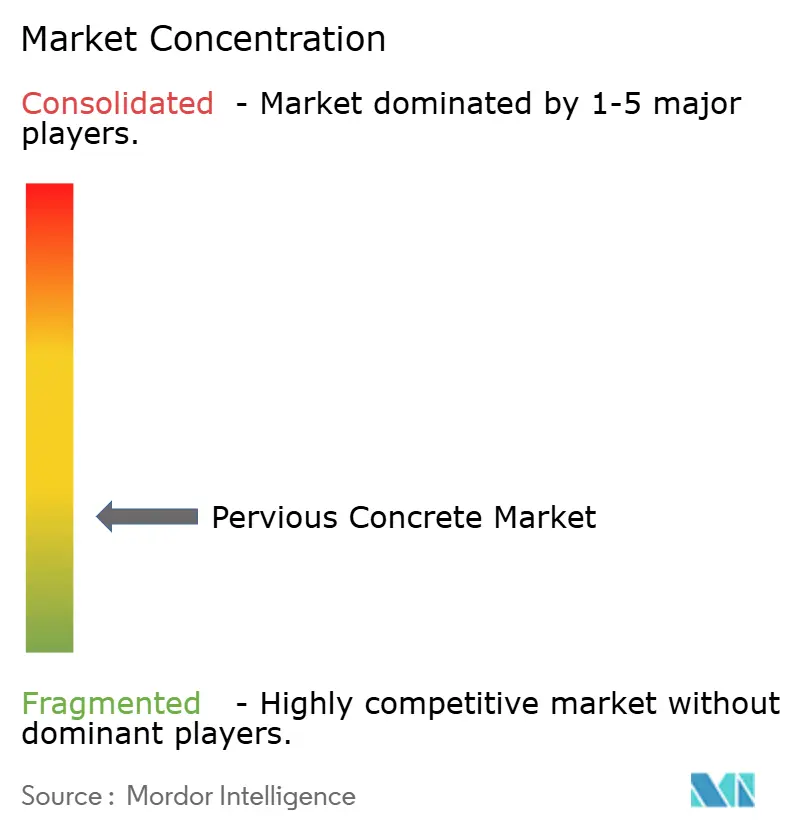

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pervious Concrete Market Analysis by Mordor Intelligence

The Pervious Concrete Market size is projected to expand from USD 5.16 billion in 2025 and USD 5.46 billion in 2026 to USD 7.45 billion by 2031, registering a CAGR of 6.41% between 2026 to 2031. Increasing occurrences of flash-flood events, mandatory low-impact development (LID) regulations, and corporate net-zero commitments are shifting stormwater budgets toward permeable pavements. In China, the sponge-city program is generating numerous municipal tenders specifically requiring pervious materials. Similarly, North American data center operators have reported surface temperature reductions of 3-5 °C, leading to decreased cooling demands. Adoption by end-users is further supported by property tax rebates and stormwater fee reductions, which shorten payback periods for residential projects. Concurrently, ready-mix suppliers are incorporating low-carbon cement and fiber additives to enhance the strength of pervious concrete without compromising infiltration capabilities, thereby expanding its applications beyond driveways and plazas.

Key Report Takeaways

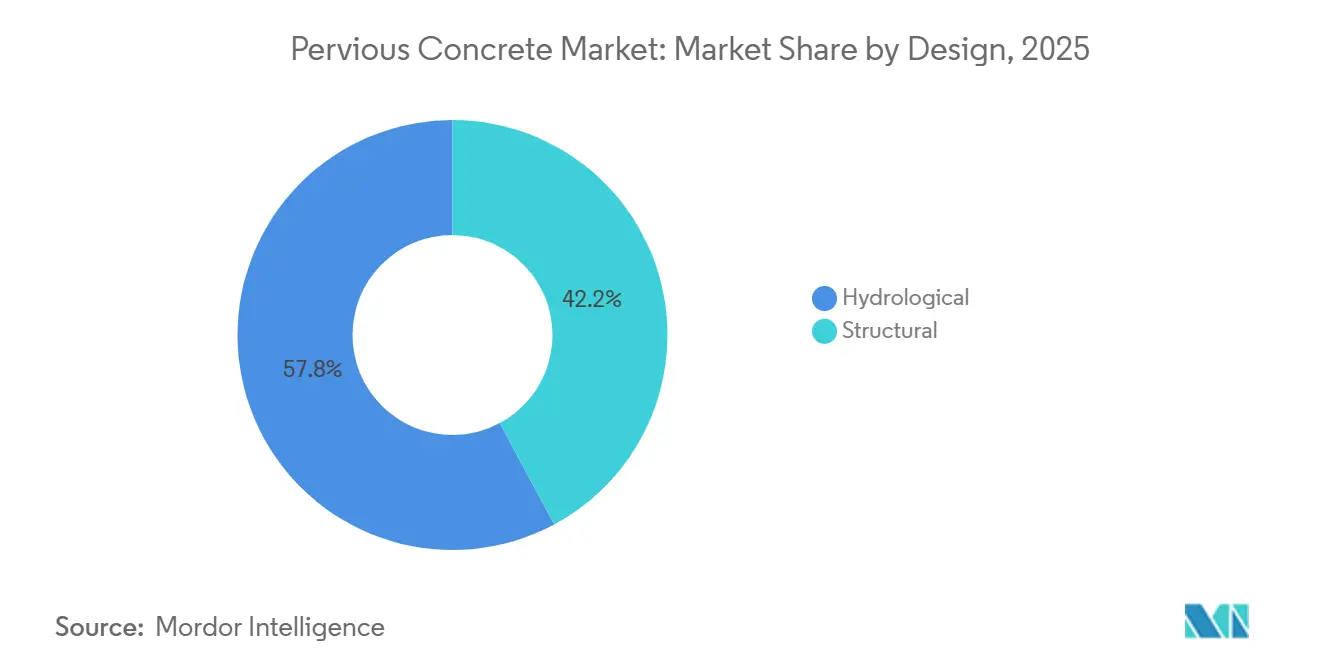

- By design, hydrological led with 57.84% of the pervious concrete market share in 2025, whereas structural design is projected to grow fastest at a 6.75% CAGR through 2031.

- By application, hardscape captured 71.41% of the pervious concrete market share in 2025 and is advancing at a 6.57% CAGR through 2031.

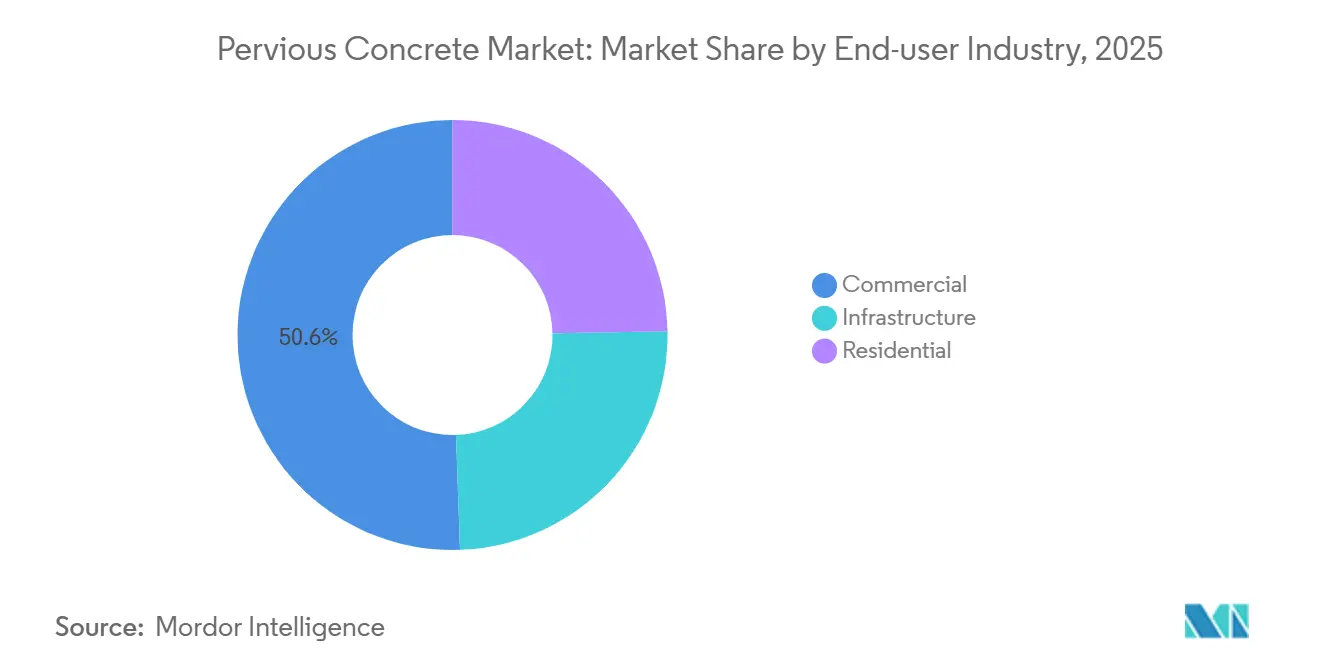

- By end-user industry, the commercial held 50.55% of the pervious concrete market share in 2025, while residential is forecast to expand at a 6.88% CAGR through 2031.

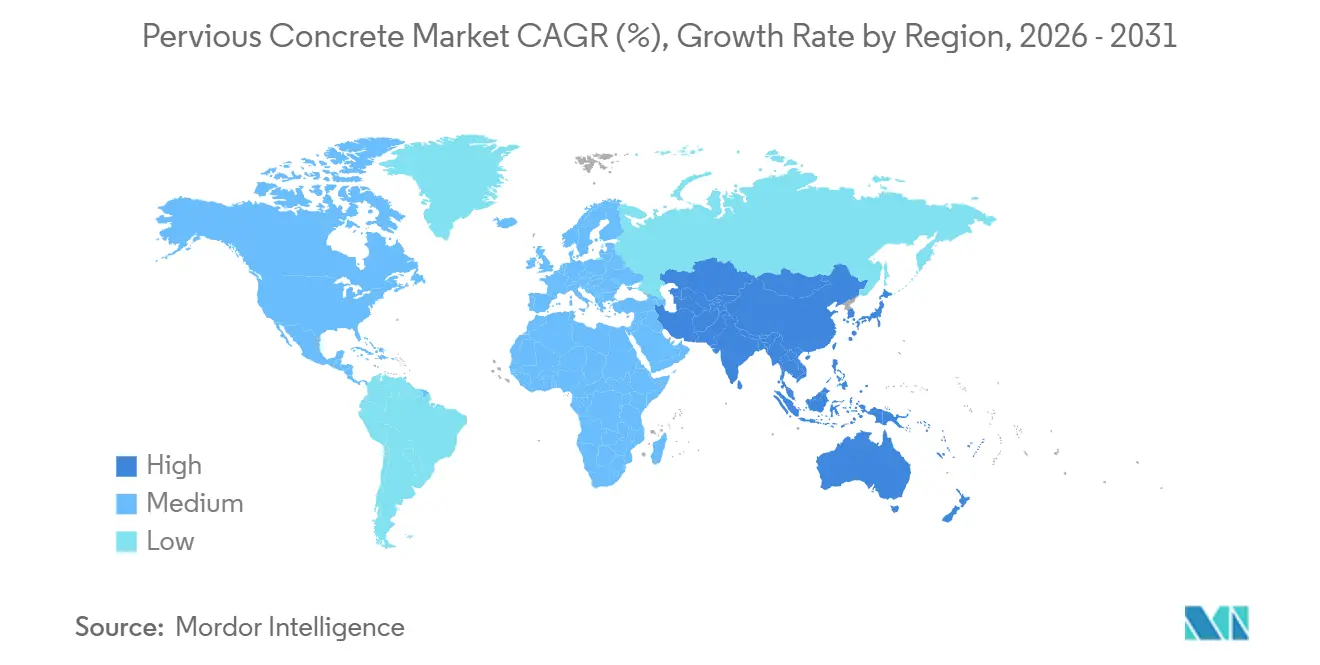

- By geography, Asia-Pacific captured 36.47% of the pervious concrete market share in 2025 and is projected to post the fastest regional CAGR of 6.95% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pervious Concrete Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing urban flash-flood incidents | +1.2% | Global, with acute pressure in APAC megacities and US Gulf Coast | Medium term (2-4 years) |

| Mandatory low-impact-development (LID) zoning codes | +1.5% | North America and EU, expanding to APAC tier-2 cities | Long term (≥ 4 years) |

| Tax incentives for porous pavements in North America | +0.8% | United States, Canada (Ontario municipalities) | Short term (≤ 2 years) |

| Rapid expansion of data-centre campuses | +0.9% | North America, Europe, emerging in India and Southeast Asia | Medium term (2-4 years) |

| Electrified last-mile warehouses favour cool pavements | +0.7% | North America, Europe, China coastal logistics hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Urban Flash-Flood Incidents

Municipalities are struggling with sewer overflows and climate-related cloudbursts that exceed the capacity of aging drainage systems. The U.S. Environmental Protection Agency recognizes pervious pavements as a best management practice under Phase II MS4 permits, requiring over 6,800 operators to implement infiltration surfaces. Cities such as Seattle and Wuhan have combined stormwater fee credits with sponge-city grants, redirecting procurement from asphalt overlays to permeable systems that also serve as groundwater-recharge infrastructure[1]Seattle Public Utilities, “Stormwater Code & Manual,” Seattle.gov. Furthermore, climate-adaptation bonds issued by coastal metropolitan areas are boosting bid volumes, particularly in regions where sea-level rise intensifies flood risks.

Mandatory Low-Impact-Development Zoning Codes

Local planning regulations now include Low-Impact Development (LID) thresholds in site approval processes, effectively making pervious concrete mandatory for projects in flood-prone areas. For example, Philadelphia requires all major developments to manage the first inch of rainfall on-site, while Los Angeles mandates bio-filtration or infiltration systems for parking lots larger than 5,000 ft², verified using ASTM C1701 infiltration standards. Similarly, China’s GB/T 51345-2018 standard enforces comparable requirements across more than 60 pilot sponge-cities. These regulatory frameworks establish a foundation that protects the pervious concrete market from typical construction cycle fluctuations.

Tax Incentives for Porous Pavements in North America

Tax incentives are narrowing the cost gap between permeable pavements and asphalt. For instance, municipalities in Ontario provide reimbursements of up to CAD 3,500 per household for permeable driveways, while Washington D.C.’s RiverSmart Homes program covers up to USD 4,800 of project costs. In Raleigh, stormwater utility fee reductions of 25% reduce residential payback periods to less than five years. As awareness of these rebates spreads among contractors, residential demand is growing at the fastest rate among all end-user categories.

Rapid Expansion of Data-Center Campuses

Hyperscale data-center operators benefit from the 3-5 °C surface-temperature reduction achieved by pervious pavements, which lowers cooling energy requirements in outdoor-air economizer modes. LEED v4.1 certification awards dual points for heat-island mitigation and permeable hardscapes, positioning pervious concrete as a cost-effective option for certification. India’s 1,700 MW data-center pipeline incorporates these specifications to qualify for green bonds, ensuring a stable demand channel that is less influenced by variations in retail construction activity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Need for certified contractors and specialised placement equipment | -0.6% | Global, acute in tier-2 and tier-3 cities lacking training infrastructure | Short term (≤ 2 years) |

| Limited structural load-bearing vs. conventional concrete | -0.5% | Global, constraining adoption in industrial and heavy-traffic applications | Long term (≥ 4 years) |

| Scarcity of open-graded aggregates in megacities | -0.4% | APAC megacities, Middle-East urban centers, select EU metros | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Need for Certified Contractors and Specialized Placement Equipment

Globally, fewer than 1,500 installers hold active NRMCA pervious-concrete credentials, causing delays, especially outside primary metropolitan areas. The additional cost of specialized equipment, such as vibratory rollers and mist-curing gear, ranges from USD 15,000-30,000 per crew, discouraging smaller contractors. Forensic evaluations reveal that 68% of early permeability failures result from improper compaction or curing, diminishing specifier confidence, and restricting short-term revenue growth.

Scarcity of Open-Graded Aggregates in Megacities

In Shanghai, suitable stone is transported from quarries over 150 km away, increasing costs by USD 8-12 per m³ and causing lead times of 4-6 weeks[2]Shanghai Municipal Commission of Housing and Urban-Rural Development, “Aggregate Supply Notice,” Shanghai.gov.cn. Dubai depends on imports from Oman and Iran, which raises costs by 40% and exposes projects to currency fluctuation risks. Recycled concrete aggregate partially addresses the shortage but can reduce permeability by up to 25%, limiting pavement durability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Design: Structural Design Gain Traction

Structural design is anticipated to grow at a CAGR of 6.75% through 2031, compared to hydrological design’s 57.84% share of the pervious concrete market in 2025. Fiber-reinforced mixes, which enhance compressive strength to approximately 4,000 psi, are expanding applications to include municipal bus bays and light-industrial truck courts. Premium admixture packages, which increase delivered costs by 15-20%, enable access to ESG-linked project financing by emphasizing carbon reduction and improved load capacity. Ready-mix producers are increasingly incorporating polypropylene microfibers and basalt macrofibers, supported by mix-design software that optimizes void ratios and uniformity.

Advancements in curing membranes and set retarders have enabled structural mixes to maintain infiltration rates above 250 mm/h, meeting ASTM C1701 standards. Hybrid overlays, which involve casting a 2-3 inch pervious topping over dense concrete bases, are gaining traction in retrofit projects by avoiding full-depth demolition. UltraTech’s ZeroCAL collaboration exemplifies innovation in this space, combining limestone-calcined-clay cement with fiber reinforcement to reduce embodied carbon by 40% while maintaining a compressive strength of 3,500 psi. This aligns structural variants with green-bond criteria.

By Application: Hardscape Dominance Reflects Regulatory Push

Hardscape applications accounted for 71.41% of the pervious concrete market size in 2025 and are expected to grow at a CAGR of 6.57% through 2031. Low Impact Development (LID) ordinances in cities such as Philadelphia, Los Angeles, and Shanghai prioritize permeable retrofits for parking lots and driveways, converting storm-water fees into high-return resurfacing projects. Hardscape applications also provide a straightforward path to achieving LEED heat-island credits due to the simplicity of documenting large contiguous surfaces.

Sub-segments like green roofs and erosion-control channels are gaining momentum, driven by European pilot projects that highlight pervious concrete’s acoustic benefits. Floors remain a niche application, primarily used in dairy barns and greenhouse walkways where improved drainage enhances hygiene. However, agricultural extension programs predict broader adoption as feedlot operators recognize the link between better hoof health and reduced veterinary costs, showcasing how non-storm-water benefits can diversify demand.

By End-user Industry: Residential Segment Accelerates

Commercial industry held 50.55% of the market demand in 2025, driven by retail centers and office campuses seeking LEED certification. However, the residential segment is anticipated to grow at a CAGR of 6.88% through 2031, supported by tax credits of up to CAD 3,500 in Ontario and USD 4,800 in Washington, D.C. Municipalities are increasingly pairing rebates with public contractor directories to ensure quality workmanship and expedite permit approvals.

Infrastructure projects, including transit plazas and municipal sidewalks, are leveraging green-bond capital allocated for climate resilience. For instance, New York City’s USD 10 billion bond program authorizes the use of permeable pavements in flood-prone areas, with procurement guidelines favoring NRMCA-certified crews. The combination of commercial stability, residential growth, and policy-driven infrastructure projects creates a balanced portfolio that supports long-term revenue growth in the pervious concrete market.

Geography Analysis

The Asia-Pacific region accounted for 36.47% of global revenue in 2025 and is expected to achieve the fastest regional growth, with a CAGR of 6.95% through 2031. China’s sponge-city initiative mandates that 80% of urban areas absorb 70% of rainfall by 2030, driving significant investments in permeable paving. For example, Wuhan allocated CNY 13 billion (USD 1.8 billion) to retrofit 38.5% of its built-up area, while Shanghai earmarked CNY 5.3 billion (USD 730 million) for similar projects. India’s Smart Cities Mission integrates pervious pavements with digital monitoring of infiltration performance, further expanding the regional project pipeline.

North America presents a mature but stable market outlook. Over 6,800 Phase II MS4 jurisdictions are required to quantify runoff reduction, and tax-incentivized retrofit programs continue to support residential demand. Infrastructure Canada’s co-funding initiatives bolster municipal budgets for green hardscape projects, while U.S. data-center and warehouse developers specify pervious concrete to meet LEED and ESG objectives, ensuring steady demand across commercial campuses.

In Europe, stringent water regulations and carbon accounting sustain market growth. Germany’s Federal Water Act mandates on-site storm-water management, the UK’s SuDS framework incorporates infiltration into major projects, and France’s RE2020 regulation caps lifecycle CO₂ emissions, favoring low-carbon pervious mixes. While high labor costs may limit revenue growth, stable policies ensure premium pricing and sustained margins. Emerging markets such as Brazil and Saudi Arabia are testing pilot projects that could lead to broader adoption as local supply chains develop.

Competitive Landscape

Global cement companies benefit from synergies by combining carbon-reduced clinker with permeable formulations. However, the top five players collectively accounted for only 35% of 2025 revenue, indicating high market fragmentation. Heidelberg Materials’ Brevik CCS plant captures 400,000 tons of CO₂ annually, supplying evoZero cement for pervious mixes and enabling sovereign funds to achieve Scope 3 emissions reductions. CRH’s USD 2.1 billion acquisition of Eco Material Technologies secures fly-ash and slag supplies, stabilizing costs amid declining coal-plant operations.

Companies such as Holcim, Cemex, and Sika differentiate their offerings through specialized admixture portfolios, including permeability enhancers, set retarders, and microfibers. Regionally, firms like Chaney Enterprises and Concreto Ecológico de México address labor shortages by offering contractor-certification programs that ensure placement quality. Digital mix-design tools, such as UltraTech’s ZeroCAL, streamline trial batches and improve job-site efficiency, providing a technological edge that is expected to grow over the forecast period.

Emerging opportunities are concentrated in data-center campuses and electrified logistics parks, which prioritize thermal performance and ESG compliance. Vendors offering integrated solutions, including design guidance, certification training, and embedded carbon accounting, are well-positioned to capitalize on the transition of pervious concrete from a niche material to a mainstream storm-water management asset.

Pervious Concrete Industry Leaders

Cemex S.A.B. de C.V.

CRH

Heidelberg Materials

Sika AG

HOLCIM

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: A study published in the International Journal of Pavement Engineering highlights the potential of lightweight pervious concrete in mitigating the urban heat island (UHI) effect through improved heat storage and release efficiency. The research analyzed the impact of variations in aggregate type, replacement ratios, and water-to-cement ratios on the concrete's mechanical and thermal performance.

- June 2024: New York City's Department of Environmental Protection (DEP) and Department of Design and Construction (DDC) commenced the installation of seven miles of pervious concrete pavement on Brooklyn roadways. The project, undertaken through a USD 32.6 million contract, was designed to enhance stormwater management.

Global Pervious Concrete Market Report Scope

Pervious concrete is made from cement, coarse aggregate, water, admixtures, and other cementitious materials, which are used to create a paste that forms a thick coating around aggregate particles. The lack of fine aggregates causes the pervious concrete to have a void structure, which allows liquids and air to be filtered and pass through the concrete into a sub-base or collection pond.

The pervious concrete market is segmented by design, application, end-user industry, and geography. By design, the market is segmented into hydrological and structural. By application, the market is segmented into hardscape, floors, and other applications. By end-user industry, the market is segmented into commercial, residential, and infrastructure. The report also covers the market size and forecast for the pervious concrete in 15 countries across major regions. For each segment, the market sizing and forecast have been done on the basis of value (USD).

| Hydrological |

| Structural |

| Hardscape |

| Floors |

| Other Applications |

| Commercial |

| Residential |

| Infrastructure |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Design | Hydrological | |

| Structural | ||

| By Application | Hardscape | |

| Floors | ||

| Other Applications | ||

| By End-user Industry | Commercial | |

| Residential | ||

| Infrastructure | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the pervious concrete market?

The pervious concrete market stands at USD 5.46 billion in 2026 and is expected to reach USD 7.45 billion by 2031.

Which region is expected to post the fastest demand growth by 2031?

Asia-Pacific is projected to expand at a 6.95% CAGR through 2031, the highest among all regions.

How does pervious concrete benefit hyperscale data-center campuses?

Field data show surface-temperature reductions of 3-5 °C versus asphalt, which lowers cooling loads and helps secure LEED Heat Island Reduction credits.

What structural innovations are widening the use of pervious concrete?

Fiber-reinforced mixes now reach compressive strengths near 4,000 psi, enabling light-industrial truck courts and municipal bus bays that once required conventional slabs.

Page last updated on: