Asphalt Shingles Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 18.36 Billion |

| Market Size (2031) | USD 23.54 Billion |

| Growth Rate (2026 - 2031) | 5.10% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

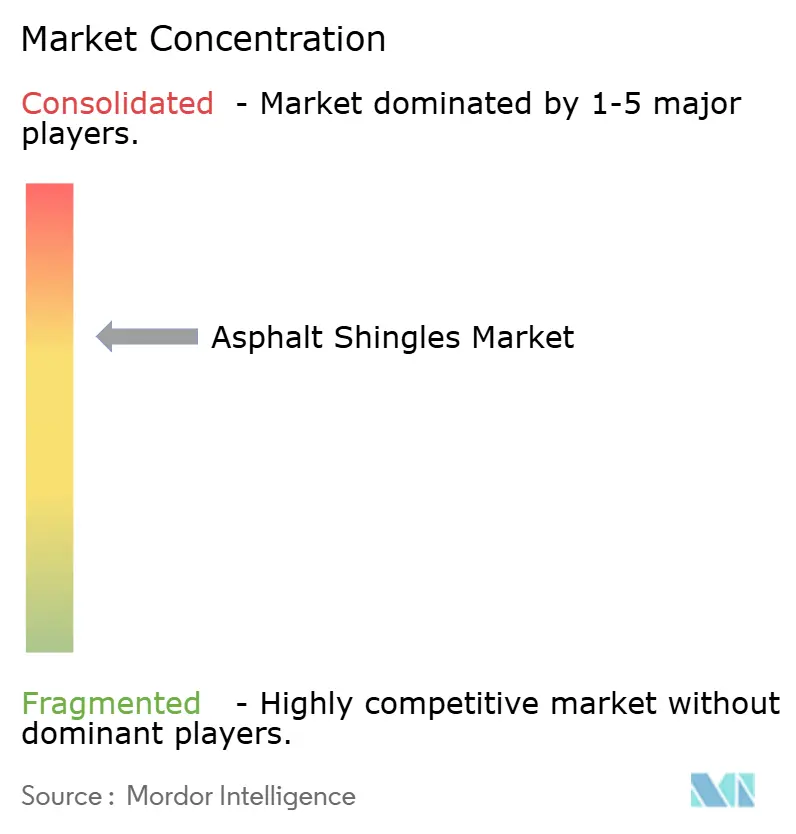

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asphalt Shingles Market Analysis by Mordor Intelligence

The Asphalt Shingles Market size is projected to expand from USD 17.51 billion in 2025 and USD 18.36 billion in 2026 to USD 23.54 billion by 2031, registering a CAGR of 5.10% between 2026 to 2031. The upswing rests on a replacement cycle that now turns in 19 years on average as storm activity intensifies, while polymer-modified laminates and cool-roof formulations lift per-square revenue faster than unit volume. Contractors are accelerating digital procurement, and e-commerce platforms that integrate real-time pricing and just-in-time delivery are compressing project timelines. Capacity additions in the southeastern United States and western Canada arrive ahead of forecast hurricane and hail seasons, supporting regional supply resilience. At the same time, circular-economy pilots that recover bitumen from tear-offs are beginning to temper landfill pressure and promote sustainability positioning across the Asphalt shingles market.

Key Report Takeaways

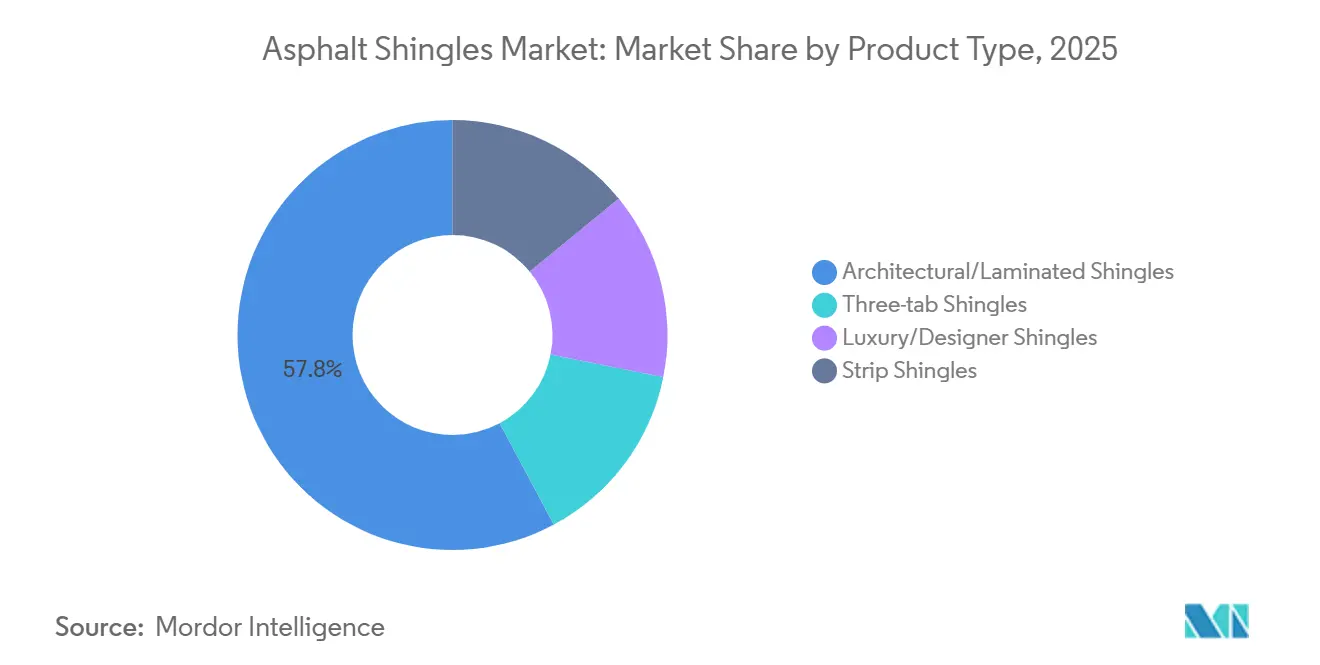

- By product type, architectural/laminated shingles held 57.80% of the Asphalt Shingles market share in 2025, while luxury/designer shingles are projected to record a 6.20% CAGR through 2031.

- By reinforcement material, fiberglass mat accounted for 78.50% share of the Asphalt Shingles market size in 2025, whereas organic mat shingles are poised to expand at a 6.12% CAGR to 2031.

- By distribution channel, roofing-supply distributors led with 43.30% share in 2025, while e-commerce/online channels are projected to grow at 6.31% CAGR to 2031.

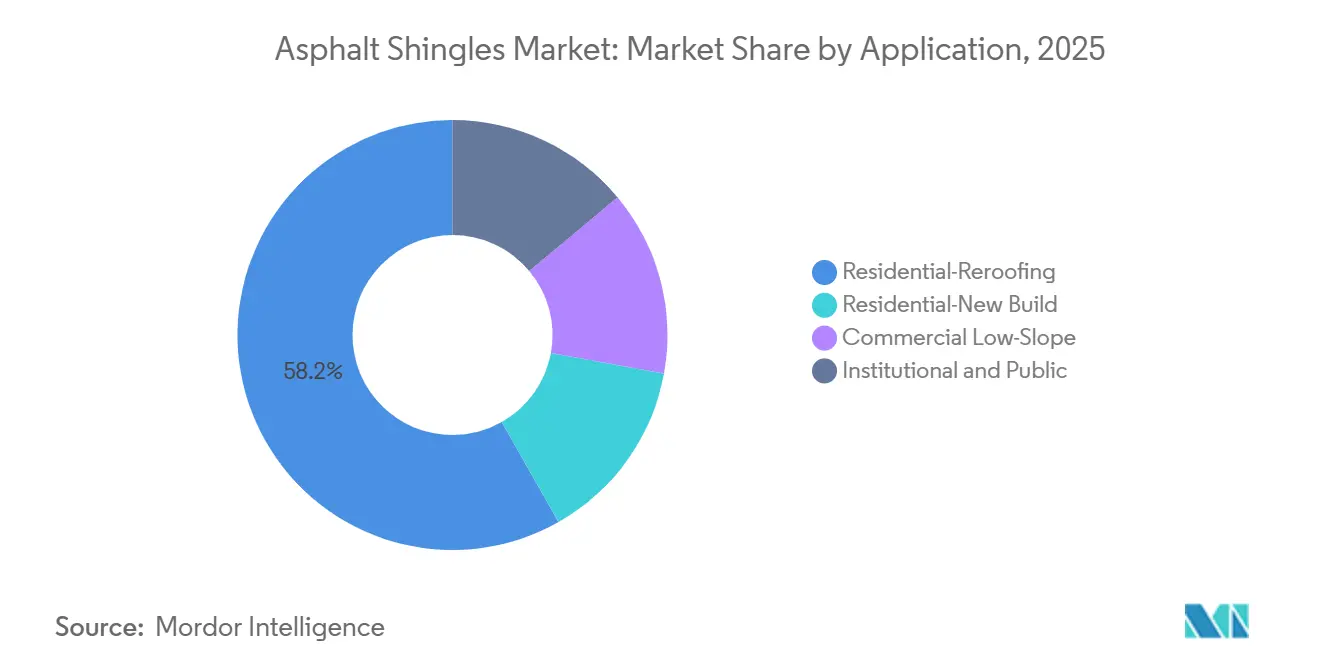

- By application, residential-reroofing captured 58.20% revenue share in 2025, and commercial low-slope is advancing at a 6.15% CAGR through 2031.

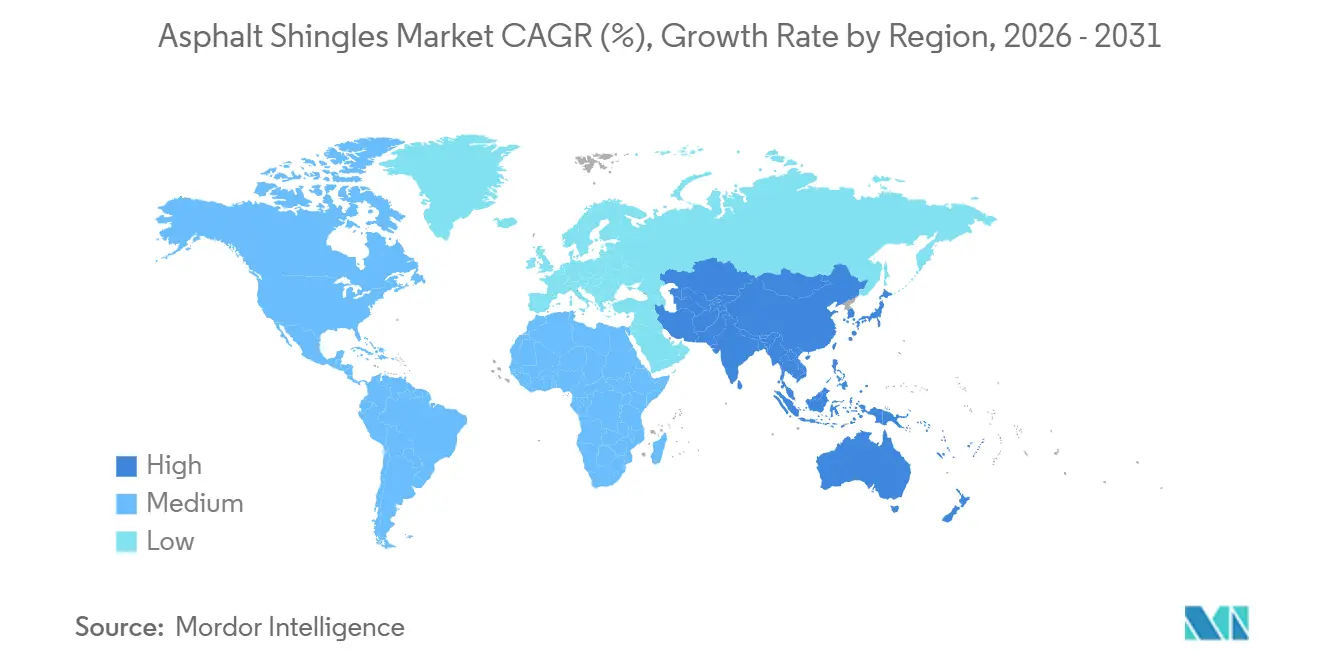

- By geography, North America commanded a 42.30% share in 2025, whereas the Asia-Pacific is forecast to post a 6.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Asphalt Shingles Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing residential construction and reroofing demand | +1.8% | North America, China, India | Medium term (2-4 years) |

| Cost-effective installation and life-cycle economics | +1.2% | Latin America, Southeast Asia, U.S. Midwest | Long term (≥ 4 years) |

| Architectural laminated shingles popularity | +0.9% | North America, Europe, Australia | Medium term (2-4 years) |

| Cool-roof and energy-code driven demand | +0.7% | California, Texas, Australia, Middle East | Short term (≤ 2 years) |

| Climate-resilient Class-4 polymer-modified laminates | +0.6% | Texas, Oklahoma, Japan, Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Residential Construction and Reroofing Demand

Replacement dominates the Asphalt shingles market, with reroofing representing 85% of roughly five million United States installations each year, and the mean service life sliding to 19 years because of more severe weather[1]National Roofing Contractors Association, “Market Survey 2025,” nrca.net. Storm damage matched leaks at 33% of reroof triggers in 2025, underscoring how climate volatility is pulling capital spending forward. Urbanization in India is adding greenfield demand; government housing programs and metro expansions have pushed the national roofing segment toward USD 11.7 billion by 2033. Labor scarcity is elevating wages, prompting 39% of North American contractors to adopt AI scheduling tools in 2026. These factors combine to keep reroof volumes high and sustain price discipline across the Asphalt Shingles market.

Cost-Effective Installation and Life-Cycle Economics

Asphalt shingles install for USD 3.50-5.50 per square foot versus USD 7-14 for metal panels, and a two-person crew can finish a 2,000-square-foot roof in as little as two days. Rapid installation tempers rising labor rates, which climbed 8-12% between 2024 and 2025. Buyers leveraging bulk orders of 100-plus tons secure 10-15% material savings, reinforcing the cost advantage. Although metal roofs last 40-70 years, the total outlay over 50 years for two asphalt replacements still runs below or near the metal premium, preserving value perception in the Asphalt Shingles market.

Architectural Laminated Shingles Popularity

Dimensional profiles that emulate wood shake or slate secured 57.8% of 2025 sales thanks to 110-130 mph wind ratings and 30-50 year warranties. Premiums run 20-40% above three-tab products yet unlock insurance discounts of up to 35% in hail belts. Solar-ready variants such as GAF Energy’s Timberline Solar ES 2, rated at 57 watts per shingle, illustrate how aesthetics, durability, and energy generation now converge inside one product family.

Cool-Roof and Energy-Code Driven Demand

California’s 2025 Title 24 update set minimum Solar Reflectance Index values that effectively mandate cool-roof asphalt shingles in six climate zones. Owens Corning, CertainTeed, and GAF offer shingles with SRI ratings between 20 and 29, lowering attic temperatures by 10-20°F and trimming cooling loads up to 15%[2]Cool Roof Rating Council, “Product Directory 2026,” coolroofs.org. Australia will enforce comparable ventilation and reflectance rules under its National Construction Code 2025, pushing specification trends in the broader Asphalt Shingles market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vulnerability to extreme weather and wind uplift | -0.5% | Florida, Gulf Coast, Japan, Philippines | Short term (≤ 2 years) |

| Bitumen-related environmental and disposal concerns | -0.4% | European Union, Canada, Australia | Medium term (2-4 years) |

| Growing appeal of metal and composite substitutes | -0.3% | North America premium, Europe sustainability segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vulnerability to Extreme Weather and Wind Uplift

Post-hurricane audits show 30-40% of asphalt shingle failures occur on roofs under 10 years old because of installation errors rather than material faults. Labor shortages raise the likelihood of missed nailing patterns and under-sealed tabs. States such as Florida now require 110 mph ratings in coastal zones, driving manufacturers to boost adhesive strength and fastener counts, which raises bill-of-materials costs by up to 10%.

Bitumen-Related Environmental and Disposal Concerns

Roughly 11 million tons of asphalt shingles enter United States landfills each year, and only 20% of jurisdictions permit diversion into recycled asphalt pavement streams. The European Union will mandate digital product passports in 2028, compelling embodied-carbon disclosure for roof coverings. Manufacturers are piloting recovery lines, and Northstar’s Calgary plant, operational in April 2026, now processes 80,000 tons annually, indicating early progress toward a circular Asphalt Shingles industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Laminated Profiles Dominate while Designer Niche Climbs

Architectural/laminated shingles contributed 57.8% to the overall Asphalt Shingles market share in 2025. Class-4 versions cost 10-15% more yet yield insurer savings that recover the premium within seven years. Luxury/Designer shingles are expected to grow at a CAGR of 6.2% during the forecast period (2026-2031) as upscale buyers in North America and Europe favor slate-look blends that offer 50-year guarantees. Three-tab shingles are fading outside price-sensitive regions but still meet budget constraints in parts of Latin America and Southeast Asia.

Upside potential centers on solar-ready laminates that merge energy generation with curb appeal. GAF Energy’s Timberline Solar ES 2 and CertainTeed’s Solstice Shingle illustrate how innovation steers demand toward higher-margin SKUs. As a result, the Asphalt shingles market size attributable to laminates is projected to widen through 2031 even if total square footage grows modestly.

By Reinforcement Material: Fiberglass Leads, Organic Finds Cold-Climate Foothold

Fiberglass mat dominated 78.5% of shipments in 2025, helped by its Class A fire rating and lower weight. Organic mat's market share is advancing at a 6.1% CAGR to 2031, where freeze-thaw cycles favor its bendability. Polymer-modified asphalt is shrinking the performance gap between the two substrates, yet capital inertia keeps most North American lines tuned for fiberglass.

Sustainability narratives are boosting organic mat’s appeal because cellulose fibers are renewable. Nevertheless, higher asphalt saturation offsets some carbon benefits. With neither substrate poised for wholesale displacement, the Asphalt shingles market is likely to stabilize near a 75-25 fiberglass-organic split over the forecast window.

By Distribution Channel: Consolidation Tightens Terms, Digital Ordering Gains Share

Roofing-supply distributors held 43.3% of 2025 revenue, but rapid mergers have placed half of the US branch capacity under only four owners, increasing their bargaining power with manufacturers. Direct-to-contractor programs remain strategic launch pads for innovative shingles.

E-commerce/online orders are climbing 6.31% per year to 2031 as platforms such as Roofr cut administrative tasks and shorten delivery windows. One-third of residential shingles at SRS Distribution were ordered digitally in 2025, proof that younger contractors are reshaping buying behavior within the Asphalt Shingles market.

By Application: Reroofing Commands, Commercial Low-Slope Accelerates

Residential reroofing generated 58.2% of 2025 demand as average service life contracts under harsher weather. Insurance incentives for Class-4 upgrades further swell replacement volume. New-build housing in Asia-Pacific adds incremental square footage, but growth remains moderate relative to reroofing.

Commercial low-slope roofing is pacing at a 6.15% CAGR through 2031 owing to a surge in logistics and warehouse projects. Modified bitumen systems outprice single-ply membranes, accelerating asphalt adoption on large flat roofs. Solar integration now appears on both residential and commercial specifications, linking the Asphalt shingles market to the wider energy retrofit wave.

Geography Analysis

North America supplied 42.3% of worldwide revenue in 2025, anchored by an 85% reroof mix in the United States. Class-4 impact-resistant shingles already hold roughly 18% share across Texas, Oklahoma, and Colorado, and southeastern capacity additions are timed to meet hurricane recovery peaks. Canadian demand skews toward organic mat in colder provinces, while Mexican growth aligns with industrial nearshoring that drives low-slope installations.

Asia-Pacific is the fastest-growing region at 6.24% CAGR to 2031. India's market share alone is on track to expand as urban migration fuels affordable housing. China’s residential slowdown is counterbalanced by warehouse construction for domestic e-commerce, and Japan’s typhoon exposure is lifting adoption of Class-4 polymer-modified laminates. Australia is incorporating embodied-carbon reporting into its building code, which could spur uptake of cool-roof and circular asphalt solutions beginning in 2026.

In Europe, upcoming environmental product declarations and digital passports under EU regulation will oblige material transparency from 2027, pressuring high-carbon inputs yet favoring makers with recycling pilots. Scandinavia and Germany may see modest gains tied to infrastructure spending, whereas fiscal constraints in France and the United Kingdom temper short-term volume. Emerging markets in South America, the Middle East, and North Africa contribute single-digit shares but present upside tied to urban infrastructure and climate-resilient roofing codes.

Competitive Landscape

The Asphalt Shingles market is moderately concentrated. Innovation pipelines prioritize polymer-modified impact resistance, solar integration, and recycling. GAF Energy’s Timberline Solar ES 2 brings on-roof generation into mainstream budgeting, and TAMKO introduced HailGuard shingles carrying an extended hail warranty in March 2026. Northstar Clean Technologies opened a Calgary line that reclaims bitumen from tear-offs, and Owens Corning is testing closed-loop shingle recycling with Redivius. These initiatives position incumbents for a sustainability-driven procurement landscape.

Asphalt Shingles Industry Leaders

GAF Materials Corporation

IKO Industries Ltd.

Owens Corning

TAMKO Building Products LLC

CertainTeed, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: TAMKO Building Products announced the launch of HailGuard-branded shingles, the industry’s first and only asphalt shingle with an Extended Hail Warranty.

- June 2025: Kingspan Group plc announced it is considering a foray into residential asphalt shingle production and bolstering its United States roofing investments by an additional USD 250 million.

Global Asphalt Shingles Market Report Scope

Asphalt shingles are a common and cost-effective roofing material, designed to protect homes from weather using a base of fiberglass or organic material coated with asphalt and mineral granules. Available as standard 3-tab or durable architectural (dimensional) styles, they are popular for their affordability and ease of installation.

The Asphalt Shingles market is segemnted is product type, reinforcement material, distribution channel, application, and geography. By product type, the market is segmented into three-tab shingles, architectural/laminated shingles, luxury/designer shingles, and strip shingles. By reinforcement material, the market is segmented into fiberglass mat and organic mat. By distribution channel, the market is segmented into roofing-supply distributors, direct-to-contractors, retail home-center stores, and e-commerce/online. By application, the market is segmented into residential-new build, residential-reroofing, commercial low-slope, and institutional and public. The report also covers the market size and forecasts for asphalt shingles in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Three-tab Shingles |

| Architectural/Laminated Shingles |

| Luxury/Designer Shingles |

| Strip Shingles |

| Fiberglass Mat |

| Organic Mat |

| Roofing-Supply Distributors |

| Direct-to-Contractors |

| Retail Home-Center Stores |

| E-commerce/Online |

| Residential-New Build |

| Residential-Reroofing |

| Commercial Low-Slope |

| Institutional and Public |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Turkey | |

| Rest of Middle-East and Africa |

| By Product Type | Three-tab Shingles | |

| Architectural/Laminated Shingles | ||

| Luxury/Designer Shingles | ||

| Strip Shingles | ||

| By Reinforcement Material | Fiberglass Mat | |

| Organic Mat | ||

| By Distribution Channel | Roofing-Supply Distributors | |

| Direct-to-Contractors | ||

| Retail Home-Center Stores | ||

| E-commerce/Online | ||

| By Application | Residential-New Build | |

| Residential-Reroofing | ||

| Commercial Low-Slope | ||

| Institutional and Public | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Turkey | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large will Asphalt shingles sales be by 2031?

The Asphalt shingles market size is projected to reach USD 23.54 billion by 2031, up from USD 18.36 billion in 2026.

Which product type leads current demand?

Architectural/laminated shingles held 57.8% share in 2025 and dominate specifications because of higher wind ratings and dimensional appeal.

What growth rate is expected for commercial low-slope applications?

Commercial low-slope roofing is forecast to expand at a 6.15% CAGR through 2031 as warehouse construction accelerates.

Where is regional growth strongest?

Asia-Pacific is the fastest-growing geography with a 6.24% CAGR through 2031, driven by Indian and Chinese urbanization.

Page last updated on: