Real Time Location System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

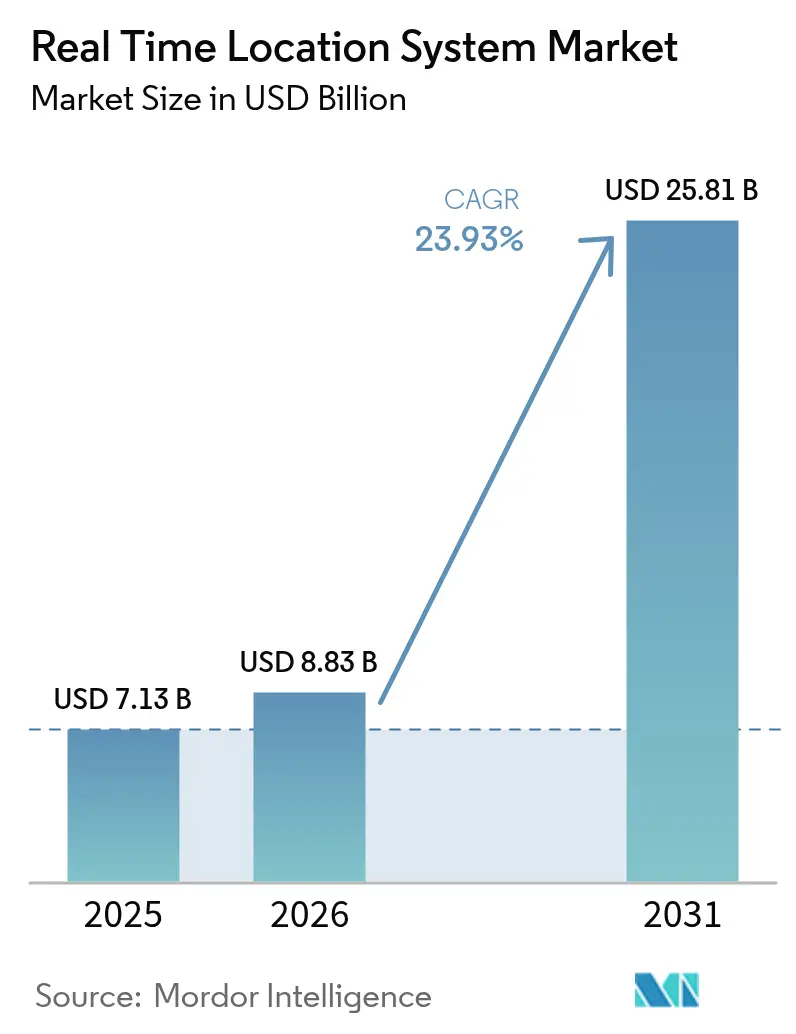

| Market Size (2026) | USD 8.83 Billion |

| Market Size (2031) | USD 25.81 Billion |

| Growth Rate (2026 - 2031) | 23.93% CAGR |

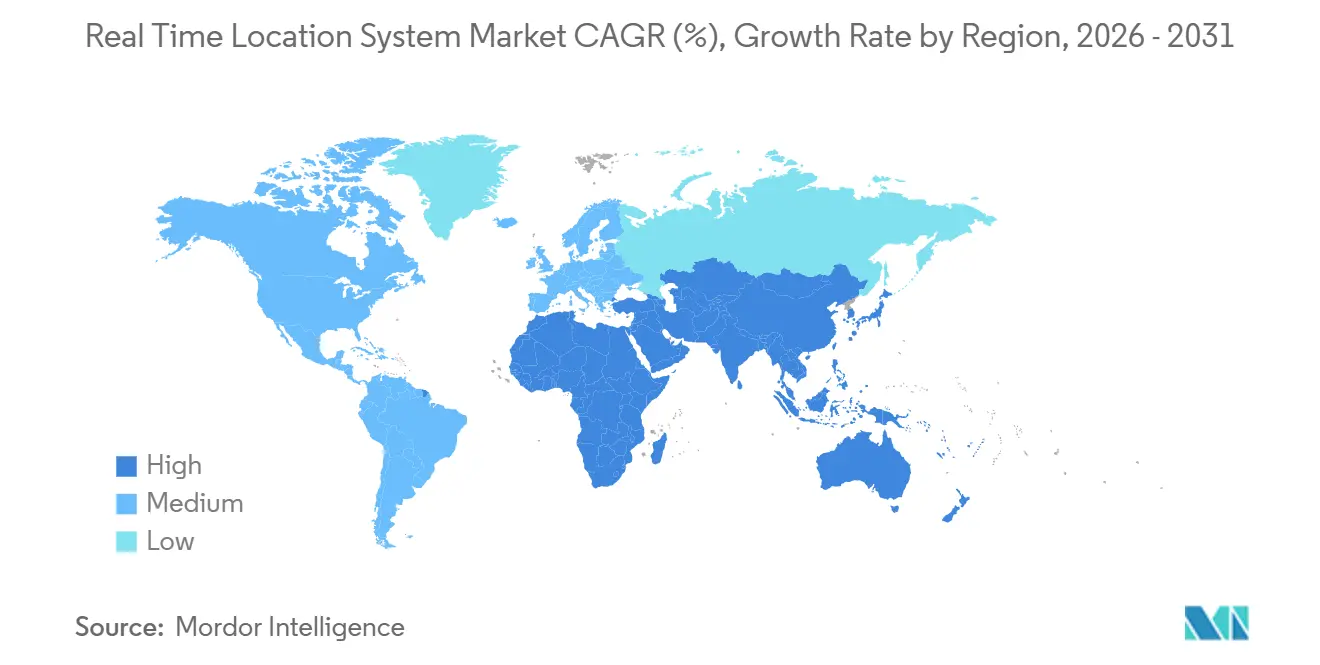

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Real Time Location System Market Analysis by Mordor Intelligence

The Real time location system market size is projected to expand from USD 7.13 billion in 2025 and USD 8.83 billion in 2026 to USD 25.81 billion by 2031, registering a CAGR of 23.93% between 2026 to 2031. Enterprises have moved past proof-of-concept trials and now treat precise indoor positioning as foundational infrastructure that underpins digital twins, autonomous mobile robots, and data-driven supply chains. Ultra-wideband hardware that supports the IEEE 802.15.4z amendment delivers sub-20 centimeter accuracy at less than EUR 45 (USD 50) per tag, making precision tracking viable for mid-tier manufacturers. Hospitals validate Bluetooth Low Energy deployments by tying hand-hygiene compliance to reimbursement metrics, a linkage reinforced by the Joint Commission’s 2024 update. Software layers that fuse location streams with enterprise applications are growing faster than hardware revenue, while white-space opportunities remain in agriculture and mining, where radio propagation or battery-life constraints remain unresolved. Competitive activity is intense because no single vendor controls even half of global revenue, leaving room for specialists to thrive beside diversified conglomerates.

Key Report Takeaways

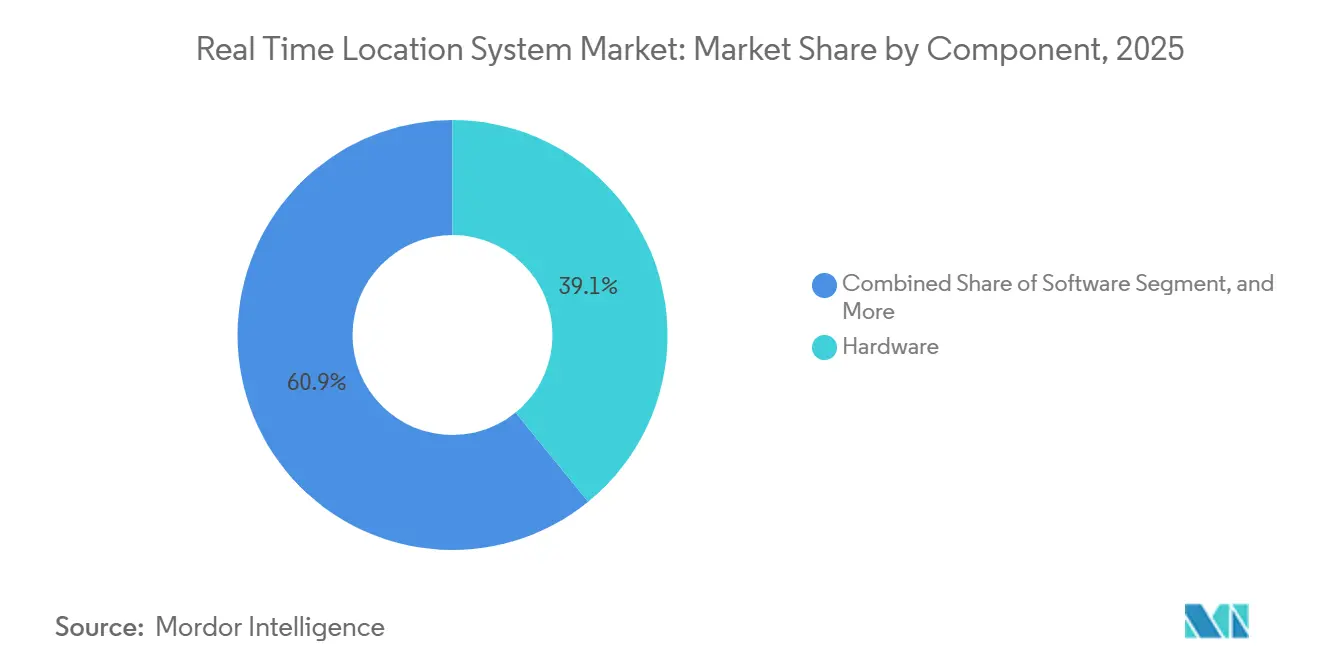

- By component, hardware led with 39.13% of Real time location system market share in 2025, while software is advancing at a 24.72% CAGR through 2031.

- By technology, RFID held 52.34% of the real time location system market in 2025, whereas ultra-wideband is forecast to expand at 25.43% through 2031.

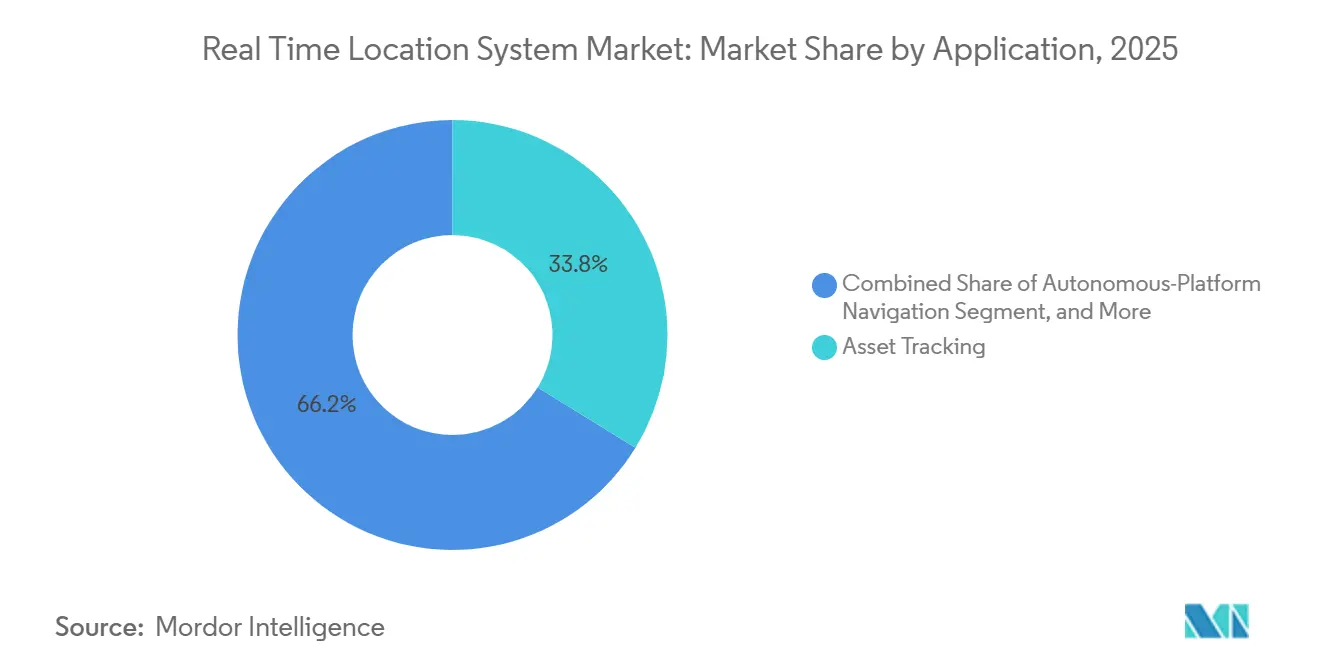

- By application, asset tracking accounted for 33.78% of the real time location system market size in 2025, and autonomous navigation is growing at a 26.36% CAGR through 2031.

- By end-user vertical, healthcare captured 28.73% real time location system market share in 2025, yet oil and gas is projected to grow at 26.21% through 2031.

- By geography, North America accounted for 39.17% of 2025 revenue, while Asia Pacific is growing at a 24.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Real Time Location System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Need for Cost Reduction and Process Optimisation | +4.2% | Global, with early traction in North America and Europe manufacturing hubs | Medium term (2-4 years) |

| Rapid Adoption in Healthcare and Patient-Safety Mandates | +5.1% | North America, Europe, Asia Pacific urban centers | Short term (≤ 2 years) |

| Advances in UWB Accuracy and Multi-Modal Tracking Platforms | +4.8% | Global, led by automotive and aerospace clusters in Germany, United States, Japan | Medium term (2-4 years) |

| Integration with Industry 4.0 Digital-Twin Initiatives | +3.9% | Europe, China, South Korea, with spill-over to ASEAN manufacturing corridors | Long term (≥ 4 years) |

| AI-Enabled Location Analytics for Hyper-Automation | +3.3% | North America, Europe, select Asia Pacific metros | Long term (≥ 4 years) |

| Edge-Native RTLS Chips Enabling Sub-Meter Precision Indoors | +2.6% | Global, concentrated in high-value verticals (healthcare, aerospace, defense) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Need for Cost Reduction and Process Optimization

Enterprises now deploy RTLS to eliminate idle motion, trim labor expense, and shrink inventory buffers. A European grocery chain that piloted battery-free Bluetooth tags cut temperature-related food spoilage by 90% and mis-shipments by 70%, saving EUR 2.3 million (USD 2.6 million) per distribution center.[1]Wiliot Ltd., “Battery-Free Bluetooth IoT Reduces Cold-Chain Losses,” wiliot.com Manufacturers report 15-25% shorter cycle times when supervisors rebalance work-in-process queues in real time instead of waiting for end-of-shift tallies. High-mix aerospace lines avoid production stalls worth USD 50 million when jigs go missing, and automotive plants achieve ten-minute just-in-sequence deliveries at line speeds above 60 jobs per hour. These savings matter most in regions where wages climb 8-12% yearly, such as Southeast Asia, making RTLS a hedge against headcount growth. The driver, therefore, has a material impact on the real time location system market.

Rapid Adoption in Healthcare and Patient-Safety Mandates

Hospitals embrace RTLS to meet infection-control benchmarks that affect reimbursement. The Joint Commission recognizes electronic hand-hygiene monitoring, catalyzing deployments by CenTrak and Stanley Healthcare that pair dispenser activations with staff badges. An Ohio facility cut bloodstream infections by 43% within 18 months, unlocking an extra USD 1.2 million in Medicare quality payments.[2]CenTrak Inc., “Hand Hygiene Compliance and HAI Reduction Case Study,” centrak.com Emergency departments using real-time bed dashboards reduced average length of stay by 22 minutes, improving CMS star ratings. Wander-management tags reduce elopement incidents by 65% in memory-care units, lowering liability premiums by up to 15%. Because patient safety aligns directly with revenue outcomes, healthcare spending on RTLS continues to grow at double digits even as overall hospital IT budgets flatten.

Advances in UWB Accuracy and Multi-Modal Platforms

Ultra-wideband benefited from the IEEE 802.15.4z security amendment and new European power limits, which increased indoor range by about 40%.[3]European Commission Radio Spectrum Policy Group, “Decision on UWB Power Limits 2024,” ec.europa.eu A single anchor now covers 1,200 square meters, slashing infrastructure costs. China harmonized spectrum rules in 2025, enabling vendors such as BlueIOT to ship more than 200,000 tags during the first half of the year. Multi-modal approaches overlay UWB for precision zones, Bluetooth for room-level presence, and Wi-Fi RTT for campus coverage, cutting total cost of ownership by up to 30%. Airports, factories, and fulfillment centers embrace this tiered design to balance accuracy, battery life, and capital outlay. Resulting performance gains are central to warehouse robots that need 10-centimeter guidance and to automotive tool tracking that demands zero mis-picks.

Integration with Industry 4.0 Digital Twins

Digital-twin platforms now ingest live RTLS coordinates to model production flows, predict downtime, and validate line reconfiguration before physical changes occur. Siemens’ MindSphere links asset positions to machine telemetry, enabling managers to test scenarios virtually, as demonstrated when a German supplier justified moving a welding cell 8 meters to save 340 meters of daily material travel. Pharmaceutical firms correlate dwell time with defect probability for FDA compliance, while building-management systems adjust HVAC zones based on real-time occupancy to cut utility bills by up to 18%. These outcomes reinforce RTLS as a core element of smart-factory roadmaps supported by public subsidies in Germany, China, and South Korea.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy Infrastructure Across End Users | -1.8% | North America and Europe, particularly in brownfield manufacturing and healthcare facilities | Short term (≤ 2 years) |

| Privacy and Cyber-Security Concerns | -2.4% | Europe (GDPR), North America (state privacy laws), with emerging scrutiny in Asia Pacific | Medium term (2-4 years) |

| High Up-Front Hardware and Calibration Costs | -2.1% | Global, most acute in price-sensitive markets (South America, Africa, Southeast Asia) | Short term (≤ 2 years) |

| RF Interference Risk in Dense IoT Environments | -1.6% | Global, concentrated in urban manufacturing zones and multi-tenant logistics hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Up-Front Hardware and Calibration Costs

Deploying anchors, tags, and gateways can exceed USD 150,000 for a 100,000-square-foot plant, a hurdle for mid-sized operators. Active UWB tags cost USD 25-45 each compared with USD 0.15 for passive RFID, restricting high-accuracy solutions to premium assets. Battery change cycles add recurring expense, and mis-calibrated anchors degrade accuracy from 15 centimeters to more than 1.2 meters, forcing costly re-surveys. Emerging markets also lack RF engineering talent, increasing risk of under-performing installations. Although vendors now offer self-calibrating algorithms, professional services remain essential for reliable outcomes.

Privacy and Cyber-Security Concerns

Location data is classified as personal information under GDPR, California’s CCPA, and China’s PIPL, obliging employers to secure consent, anonymize feeds, or keep processing on premises. Penetration tests found default passwords on 60% of surveyed RTLS anchors, permitting pivot attacks into wider IT networks. Clear-text Bluetooth advertisements can expose facility layouts. Healthcare operators face HIPAA penalties of up to USD 1.5 million per breach. Vendors respond with zero-trust frameworks and certificate authentication, yet those controls increase project costs by roughly 12% and extend deployment schedules by up to 6 weeks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Gains Momentum As Intelligence Layer

Software revenue is expanding at a 24.72% CAGR from 2026 to 2031, outpacing the real time location system market's trajectory as enterprises redirect budgets from anchors toward analytics that transform raw coordinates into operational decisions. Integration suites connect RTLS feeds to ERP, MES, and warehouse-management modules, generating alerts that reduce energy consumption or trigger inventory replenishment. Hardware still contributed 39.13% of 2025 revenue because tags and anchors remain indispensable, yet price competition from Chinese producers compresses margins. Services ranging from site surveys to managed support are capturing rising demand in oil and gas and regulated healthcare environments that require external validation documentation.

The software boom reflects a structural shift: location is no longer consumed via dedicated dashboards but is surfaced within the native interfaces of mission-critical applications. Honeywell packages RTLS-derived occupancy metrics in its Forge platform to reset HVAC setpoints and drive 12-18% energy savings. A similar embedment appears in warehouse suites that auto-replenish slow-moving stock when dwell-time thresholds are breached. Hardware commoditization will thus continue even as unit volumes climb, meaning value creation migrates toward algorithms and middleware that contextualize position data.

By Technology: Ultra-Wideband Challenges RFID Dominance

RFID retained 52.34% of the real time location system market share in 2025, thanks to passive item-level tagging in retail and active container tracking in logistics. Ultra-wideband, however, is set to grow at 25.43% through 2031, as automotive, aerospace, and warehouse automation require centimeter-level accuracy. Bluetooth Low Energy angle-of-arrival fills room-level needs in hospitals, hotels, and offices, exploiting existing smartphone ecosystems to lower entry barriers. Wi-Fi RTT leverages installed access points for zone presence, yet its 1-3 meter accuracy ceiling limits suitability for precision workflows. Infrared, ZigBee, and ultrasound retain niche roles where radio is restricted or underwater coverage is required.

FiRa Consortium interoperability profiles are accelerating UWB adoption by assuring that anchors from Sewio, Quuppa, and Ubisense communicate with tags from Qorvo, NXP, and STMicroelectronics, reducing lock-in risk. RFID vendors counter with readers such as Impinj’s M800 that extend range by 33% and introduce adaptive frequency hopping to coexist with dense IoT traffic. The technology landscape is therefore stratifying: UWB for accuracy-critical cells, BLE for cost-sensitive zones, RFID for high-volume inventory, and Wi-Fi for opportunistic coverage.

By Application: Autonomous Navigation Outpaces Asset Tracking

Asset tracking contributed 33.78% of revenue in 2025, yet autonomous mobile-robot navigation is growing at 26.36% as fulfillment centers deploy fleets that depend on sub-meter localization. Robots guided by UWB reduce picker headcount by 30% in a 500,000-square-foot warehouse, saving USD 2.1 million annually while boosting throughput 20%. Work-in-process, personnel safety, and patient monitoring each hold 8-12% slices, supporting specialized verticals. Environmental monitoring that pairs location with temperature or vibration sensors expands drug and perishable logistics, while proximity marketing trails due to high opt-out rates among shoppers.

The real time location system market for autonomous platforms will continue to expand as labor shortages and wage inflation make robotics more attractive in Japan, the United States, and key European hubs. Oil and gas platforms adopt intrinsic-safety UWB tags to enforce exclusion zones and cut evacuation drill times by 40%. Hospital badges trigger duress alerts, shrinking code-blue response time by 25%. These diverse benefits sustain double-digit growth across discrete application silos.

By End-User Vertical: Oil And Gas Climb on Safety Imperatives

Healthcare accounted for 28.73% of 2025 revenue but expects modest growth, as many hospital networks have completed initial rollouts. Oil and gas, however, is forecast to advance by 26.21% through 2031 as offshore operators deploy explosion-proof tags that meet ATEX and IECEx standards. Manufacturing leverages RTLS for digital twins and automated material handling, heightened by subsidies under Made in China 2025 and Germany’s Industrie 4.0. Retail banks are on the lookout for falling RFID tag prices, which have dipped from USD 0.12 in 2020 to USD 0.06 in 2025, crossing the mass-adoption threshold. Logistics, government, mining, agriculture, and hospitality round out smaller but specialized segments.

A Gulf of Mexico platform equipped 320 workers with UWB badges integrated into the control system, cutting near-miss incidents by 55% and reducing insurance premiums by 12% after demonstrating faster muster capability. Such a direct financial impact explains the steep trajectory in oil and gas. Manufacturing growth will hinge on multi-modal tracking that feeds predictive-maintenance algorithms and shortens changeover times in high-mix lines.

Geography Analysis

North America accounted for 39.17% of global revenue in 2025. The region now emphasizes software and analytics upgrades that layer on the RFID and Bluetooth hardware installed between 2018 and 2023. Hospitals embed room-level tracking into electronic health record workflows to meet infection control targets and secure Medicare incentives. Automotive and defense contractors invest in ultra-wideband guidance for mobile robots, yet annual spending growth has cooled to the high-teens because much of the anchor infrastructure is already deployed. Europe follows North America in absolute value but accelerates through Industrie 4.0 and Usine du Futur subsidies, even as GDPR-driven edge processing adds 10-15% to project budgets.

Asia Pacific is the fastest-growing territory, expanding at a 24.89% CAGR through 2031 on the strength of China’s CNY 150 billion (USD 21 billion) smart-factory stimulus that funds ultra-wideband rollouts across Guangdong, Jiangsu, and Zhejiang. India’s Smart Cities Mission, backed by INR 48,000 crore (USD 5.8 billion), equips municipal command centers with fleet and asset tracking, expanding the real-time location system market for public-sector buyers. Japanese logistics firms deploy UWB-guided robots to offset labor shortages, while South Korean shipyards embed tags into digital twins, shortening vessel assembly cycles by 8-12%. In the Middle East, oil and gas operators deploy intrinsically safe badges that cut evacuation drill times 40%, trimming insurance premiums and expediting permit renewals.

South America is early in the adoption curve, yet Brazilian miners and Argentine grain terminals have begun Bluetooth Low Energy pilots for yard logistics, signaling gradual diversification beyond high-income regions. African uptake centers on South African mining shafts and Egyptian logistics hubs, where radio-enabled mustering systems safeguard workers in confined spaces. Currency volatility and a scarcity of RF engineering talent constrain large-scale rollouts across both continents, leading operators to favor cloud-hosted proofs of concept over capex-heavy anchor grids. As subsidies and safety mandates spread, regional gaps tighten, supporting a balanced real time location system market-share trajectory that marries mature upgrade spending with greenfield deployments.

Competitive Landscape

The real-time location system market remains moderately fragmented, as the top five suppliers, Zebra Technologies, Impinj, Stanley Healthcare, Siemens Healthineers, and Honeywell, control just 35-40% of combined revenue. Zebra’s USD 1.3 billion purchase of Elo in 2025 broadened its retail suite with point-of-sale and rugged tablets that unify inventory visibility and checkout on a single device stack. Siemens embeds RTLS inside MindSphere to capture Industry 4.0 budgets, while Honeywell offers warehouse-management, energy-management, and safety modules that raise switching costs. Specialist firms thrive in niches: Quuppa powers sports-venue analytics, Ubisense dominates automotive body-shop tracking, and CenTrak leads acute-care hospitals.

Technological differentiation centers on multi-modal fusion engines, advanced location algorithms, and battery-free tags that harvest ambient RF energy. Standards-body participation provides early insight into interoperability updates, benefiting contributors to FiRa and IEEE working groups. Patent portfolios in UWB time-of-flight ranging confer defensible advantages to chipmakers such as Qorvo and NXP. Regulatory expertise has become another moat; vendors that navigate FDA 510(k) filings or IECEx safety tests win preference in risk-averse industries. Meanwhile, price pressure emerges from Chinese entrants offering UWB tags at 40% discounts, compelling incumbents to bundle software and services to protect margins.

White-space opportunities linger in agriculture, where sub-USD 10 livestock tags with multi-year batteries remain elusive, and in underground mining, where rock absorption limits radio range. Hybrid GPS-UWB products now target construction sites so equipment stays visible when moving between outdoor yards and enclosed structures. Battery-free Bluetooth tags from Wiliot illustrate an adjacent threat to active sensors in low-value item tracking. Overall, success hinges on delivering secure, interoperable, and analytics-ready platforms rather than simply shipping hardware.

Real Time Location System Industry Leaders

Zebra Technologies Corporation

Ubisense Limited

Securitas Healthcare LLC

TeleTracking Technologies Inc.

Savi Technology Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Siemens Healthineers updated its Atellica laboratory-automation suite to add RTLS specimen tracking that cut labeling errors by 40% in pilot installations.

- March 2025: CenTrak rolled out its third-generation Bluetooth Low Energy platform with sub-1 meter accuracy and a five-year battery, integrated directly with leading EHR systems.

- February 2025: Zebra Technologies closed its USD 1.3 billion purchase of Elo, combining RTLS with point-of-sale and mobile computing to build an integrated retail stack.

- January 2025: Sonitor Technologies merged with Tagnos, creating a combined portfolio that spans ultrasound and infrared RTLS across 3,000 healthcare sites.

Global Real Time Location System Market Report Scope

The Real Time Location System Market Report is Segmented by Component (Hardware, Software, Services, Integration and Consulting), Technology (RFID (Active and Passive), Wi-Fi, Bluetooth Low Energy (BLE), Ultra-Wideband (UWB), Infrared (IR), ZigBee, GPS/GNSS, Ultrasound), Application (Asset Tracking, Work-in-Process Tracking, Personnel Safety and Security, Patient / Resident Monitoring, Inventory and Supply-Chain Visibility, Environmental and Condition Monitoring, Hand-Hygiene Compliance, Contact Tracing, Theft and Loss Prevention, Proximity-Based Marketing, Vehicle and Fleet Management, Autonomous-Platform Navigation), End-User Vertical (Healthcare, Manufacturing, Retail, Transportation and Logistics, Government and Defense, Oil and Gas, Aerospace and Aviation, Mining, Agriculture and Livestock, Education, Hospitality and Entertainment), and Geography (North America, South America, Europe, Asia Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Services |

| Integration and Consulting |

| RFID (Active and Passive) |

| Wi-Fi |

| Bluetooth Low Energy (BLE) |

| Ultra-Wideband (UWB) |

| Infrared (IR) |

| ZigBee |

| GPS / GNSS |

| Ultrasound |

| Asset Tracking |

| Work-in-Process Tracking |

| Personnel Safety and Security |

| Patient / Resident Monitoring |

| Inventory and Supply-Chain Visibility |

| Environmental and Condition Monitoring |

| Hand-Hygiene Compliance |

| Contact Tracing |

| Theft and Loss Prevention |

| Proximity-Based Marketing |

| Vehicle and Fleet Management |

| Autonomous-Platform Navigation |

| Healthcare |

| Manufacturing |

| Retail |

| Transportation and Logistics |

| Government and Defense |

| Oil and Gas |

| Aerospace and Aviation |

| Mining |

| Agriculture and Livestock |

| Education |

| Hospitality and Entertainment |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Hardware | ||

| Software | |||

| Services | |||

| Integration and Consulting | |||

| By Technology | RFID (Active and Passive) | ||

| Wi-Fi | |||

| Bluetooth Low Energy (BLE) | |||

| Ultra-Wideband (UWB) | |||

| Infrared (IR) | |||

| ZigBee | |||

| GPS / GNSS | |||

| Ultrasound | |||

| By Application | Asset Tracking | ||

| Work-in-Process Tracking | |||

| Personnel Safety and Security | |||

| Patient / Resident Monitoring | |||

| Inventory and Supply-Chain Visibility | |||

| Environmental and Condition Monitoring | |||

| Hand-Hygiene Compliance | |||

| Contact Tracing | |||

| Theft and Loss Prevention | |||

| Proximity-Based Marketing | |||

| Vehicle and Fleet Management | |||

| Autonomous-Platform Navigation | |||

| By End-User Vertical | Healthcare | ||

| Manufacturing | |||

| Retail | |||

| Transportation and Logistics | |||

| Government and Defense | |||

| Oil and Gas | |||

| Aerospace and Aviation | |||

| Mining | |||

| Agriculture and Livestock | |||

| Education | |||

| Hospitality and Entertainment | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How fast will spending on software rise inside the Real time location system market?

Software revenue is projected to increase at a 24.72% CAGR between 2026 and 2031 as buyers shift from hardware acquisition to analytics and integration layers.

Which technology is gaining the most share from RFID?

Ultra-wideband is expected to grow at 25.43% through 2031, challenging RFID in automotive, aerospace, and robotic navigation that demand centimeter-level precision.

Why are hospitals investing heavily in precise location tracking?

Updated infection-control standards and financial incentives link hand-hygiene compliance to reimbursement, pushing hospitals to deploy RTLS for patient safety and operational efficiency.

What restrains adoption of RTLS in mid-sized factories?

Up-front capital can exceed USD 150,000 for a medium facility and calibration mistakes degrade accuracy, making returns uncertain without skilled integrators.

Which region will add the most new RTLS installations by 2031?

Asia Pacific leads with a projected 24.89% CAGR, buoyed by Chinese smart-factory subsidies and India’s Smart Cities Mission that funds municipal tracking projects.

How fragmented is vendor competition today?

The five largest suppliers hold about 38% of revenue, leaving meaningful share for specialized competitors in healthcare, sports analytics, and automotive applications.

Page last updated on: