Rare Earth Elements Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

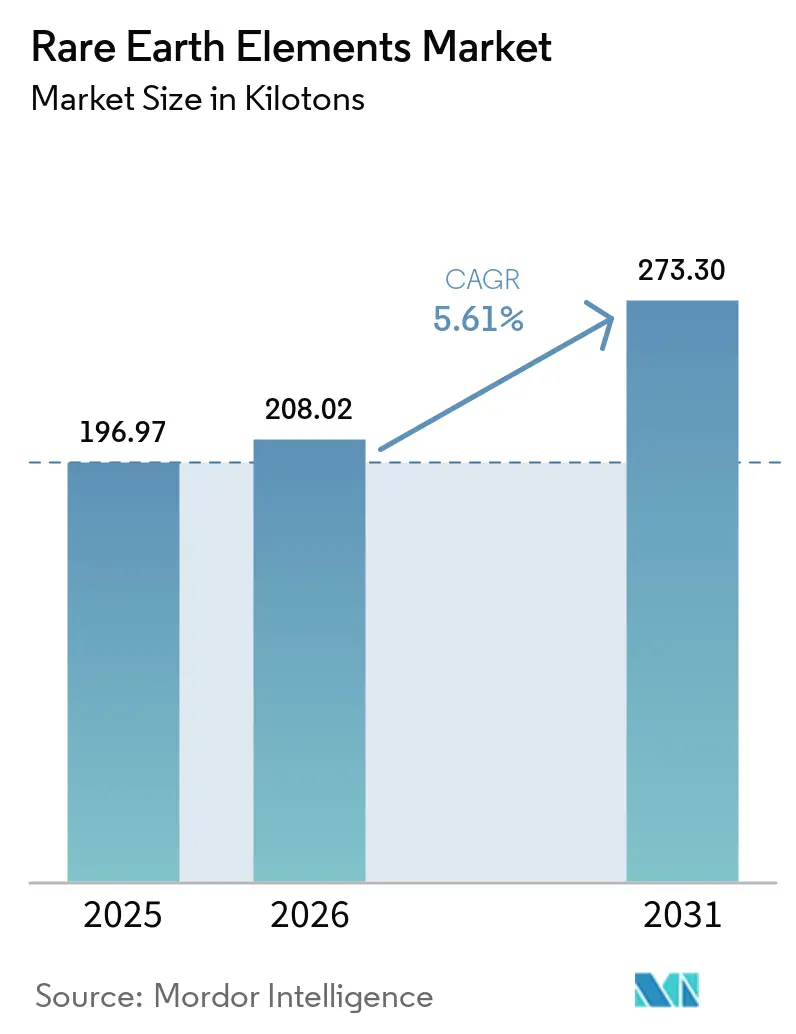

| Market Volume (2026) | 208.02 kilotons |

| Market Volume (2031) | 273.30 kilotons |

| Growth Rate (2026 - 2031) | 5.61% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rare Earth Elements Market Analysis by Mordor Intelligence

The Rare Earth Elements Market size is projected to be 196.97 kilotons in 2025, 208.02 kilotons in 2026, and reach 273.30 kilotons by 2031, growing at a CAGR of 5.61% from 2026 to 2031. Structural demand tied to electric-vehicle traction motors, offshore wind turbines, and grid-scale clean-energy infrastructure underpins this expansion, while lingering processing bottlenecks and policy-induced supply shocks temper the growth trajectory. Ongoing industrial automation roll-outs, additive-manufacturing adoption in aerospace, and tightening global emission standards provide additional demand pull, even as substitution research for dysprosium and terbium remains technically constrained. On the supply side, heavy reliance on China for both mining and separation amplifies price volatility, prompting strategic stockpiling and multi-year offtake agreements that stabilize short-term volumes but inflate procurement costs. Intensifying vertical integration among Western producers, alongside government incentives in the United States, Australia, and the European Union, signals a shift toward regionalized midstream capacity that will progressively reshape the Rare Earth Elements market through 2031.

Key Report Takeaways

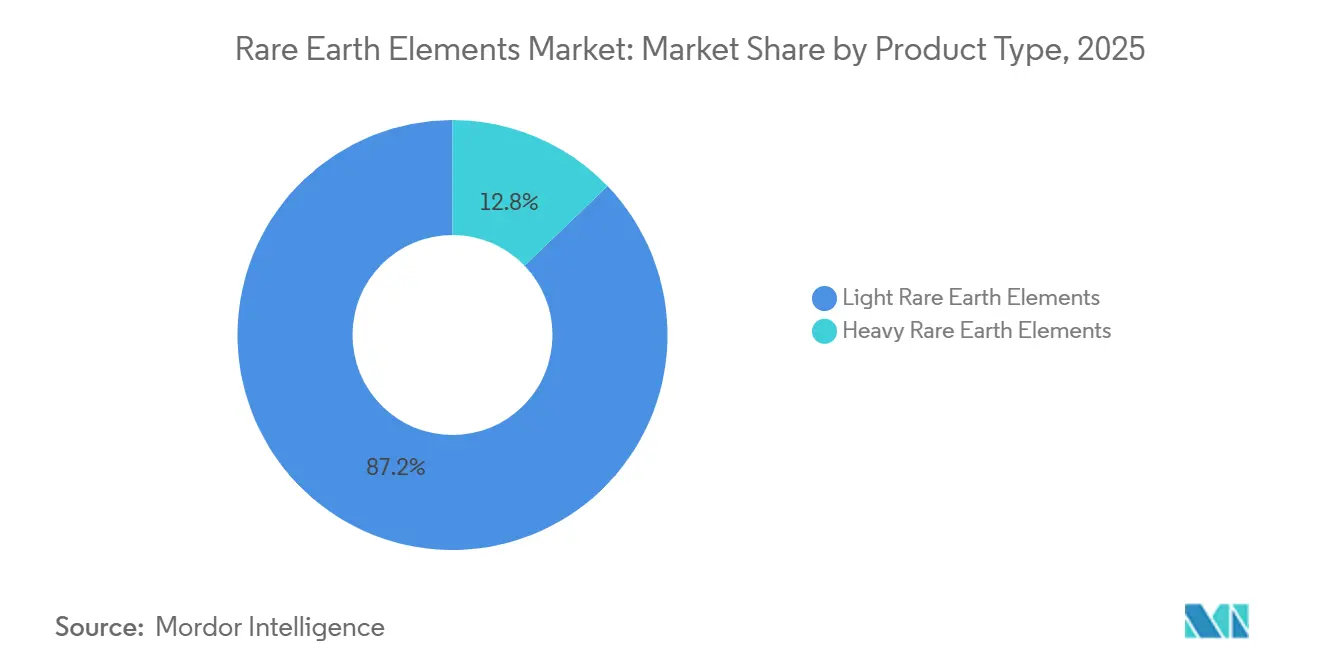

- By product type, light rare earths held 87.18% of the Rare Earth Elements market share in 2025 and are projected to expand at a 5.92% CAGR through 2031.

- By element, cerium led with 38.16% share of the Rare Earth Elements market size in 2025, while dysprosium is advancing at a 7.26% CAGR over the forecast.

- By application, magnets accounted for a 48.54% share of the Rare Earth Elements market size in 2025 and are growing at a 7.43% CAGR through 2031.

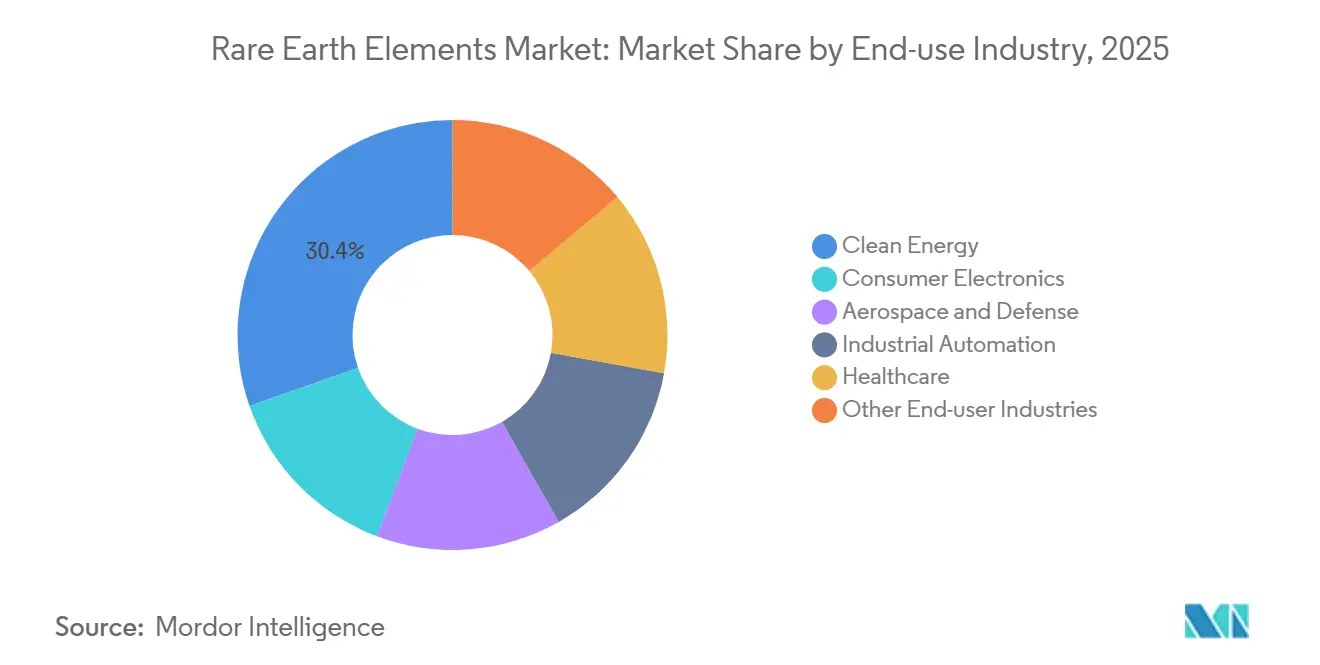

- By end-use industry, clean energy represented a 30.36% share of the Rare Earth Elements market size in 2025, while industrial automation records the strongest CAGR at 6.49% to 2031.

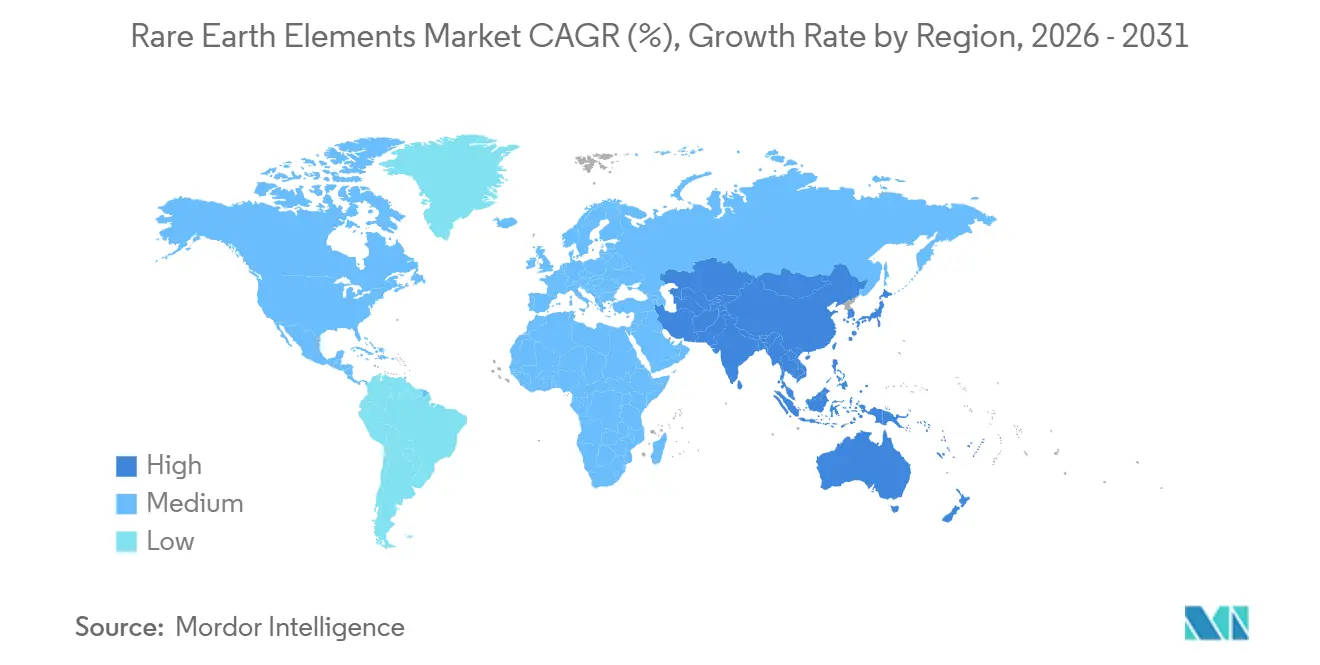

- By geography, Asia-Pacific dominated with 86.29% share of the Rare Earth Elements market size in 2025 and is forecast to progress at 5.97% CAGR during 2026–2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Rare Earth Elements Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renewable-Energy Turbine Magnet Requirement | +2.0% | Global, with concentration in China, Europe, North America | Medium to Long term (2–4+ years) |

| Dependency of 'Green Technology' on Rare Earth Elements | +1.3% | Global | Long term (≥4 years) |

| Growing Demand from Battery Applications | +0.5% | Asia-Pacific core, spillover to North America and Europe | Medium term (2–4 years) |

| Scandium-Aluminum Alloys Adoption in Aerospace Manufacturing | +0.2% | North America and Europe | Long term (≥4 years) |

| High Demand in Consumer Electronics | +0.5% | Asia-Pacific dominant, global demand | Short to Medium term (≤4 years) |

| Source: Mordor Intelligence | |||

Renewable-Energy Turbine Magnet Requirement

Neodymium-iron-boron magnets, favored by direct-drive wind turbines and battery-electric vehicles, offer unparalleled weight-to-power ratios compared to ferrite alternatives. Demand for magnet-grade rare earths is expected to grow significantly, predominantly driven by wind energy and mobility sectors. Each 3 MW offshore turbine incorporates neodymium-praseodymium and dysprosium, with global offshore installations experiencing substantial growth. The momentum in electric vehicles is undeniable, with shipments projected to increase significantly in the coming years. However, dysprosium supply poses a challenge, with a staggering majority sourced from China's ionic-clay deposits. Moreover, while efforts to find substitutes are ongoing, they've struggled to dip below a content threshold without jeopardizing thermal stability. This robust demand for magnets solidifies the position of the Rare Earth Elements market through 2031.

Dependency of Green Technology on Rare Earth Elements

Decarbonization policies are weaving rare earth elements into the fabric of the energy transition. From cerium oxide catalysts powering hydrogen fuel cells to yttrium phosphors illuminating solid-state lighting, these elements play a pivotal role. While the European Union's 'Fit for 55' initiative and the U.S. 'Inflation Reduction Act' champion domestic sourcing, they fall short in addressing the processing gap. Demand for lanthanum in nickel-metal-hydride batteries has eased. However, as emission norms tighten in emerging markets, demand for cerium oxide in automotive catalysts remains steady. This presents a strategic risk: the pace of clean-tech adoption might outstrip the growth of non-Chinese capacities, potentially leaving OEMs vulnerable to a concentrated supply chain.

Growing Demand from Battery Applications

Lanthanum-rich alloys remain the negative electrode in nickel-metal-hydride batteries that powered millions of hybrid vehicles in 2024[1]Toyota Motor Corporation, “Annual Report 2024,” global.toyota. Although lithium-ion dominates full-battery electrics, nickel-metal-hydride retains cost and safety advantages for mild hybrids and certain stationary systems. Research into lanthanum-doped solid-state electrolytes indicates a potential second-wave demand surge post-2028. Separately, neodymium and praseodymium are under investigation as cathode dopants to boost cycle life, reinforcing the Rare Earth Elements market’s increasing pivot from energy storage to high-performance motors.

Scandium-Aluminum Alloys in Aerospace Manufacturing

Adding scandium refines the grain structure of aluminum, allowing aerospace parts made with this additive to be significantly lighter than those made from traditional alloys. While Airbus and Boeing have approved the use of scandium in cabin brackets and engine-nacelle components, the high price of scandium limits its adoption to low-volume, high-value parts[2]Airbus, “Innovation in Aerospace Materials,” airbus.com. In 2024, global production remains limited, and for the aerospace sector to broaden its use of scandium, supply must expand. This expansion hinges on specific projects aimed at increasing availability.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chinese Policy-Induced Price Volatility | -1.2% | Global, most acute in Europe and North America | Short term (≤2 years) |

| Price Volatility Linked to Chinese Policy Shifts | -0.5% | Global | Short to Medium term (≤4 years) |

| Inconsistent Supply of Rare Earth Elements | -0.3% | Global, particularly non-Chinese supply chains | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Chinese Policy-Induced Price Volatility

In October 2025, Beijing expanded its export controls, introducing a content threshold. This new rule mandates that downstream producers certify the source of every rare earth atom in their finished goods. As a result, European importers witnessed a dramatic surge in dysprosium oxide prices, compelling turbine OEMs to scramble and renegotiate their supply contracts. While these controls faced a suspension until November 2026, the move set a precedent. It led to multi-year offtake deals being struck at premiums, underscoring the Rare Earth Elements market's heightened sensitivity to shifts in Chinese policy.

Inconsistent Supply of Rare Earth Elements

China dominates the global rare earths landscape, operating the majority of the world's facilities. As of early 2026, no Western plant has achieved commercial processing of heavy rare earths. Material from Mountain Pass continues its journey to China for final refining, a process that not only extends lead times but also subjects producers to tariffs. While Lynas' plant in Malaysia is missing heavy-earth circuits, Arafura's Nolans project in Australia won't hit its full output until 2027. Additionally, sporadic production from pilot operations, like Northern Minerals' Browns Range, adds to the planning uncertainty, hindering the near-term growth of the Rare Earth Elements market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Light Rare Earths Anchor Volume, Heavy Grades Command Premiums

Light rare earths captured 87.18% of volume in 2025 and are set to grow at a 5.92% CAGR through 2031. Cerium oxide, a key player in automotive catalysts, maintains a stable demand, bolstered by tightening Euro 7 and China VI standards. Lanthanum, essential for nickel-metal-hydride batteries, sees consistent consumption yearly. Meanwhile, neodymium-praseodymium production has exemplified the magnet-driven demand. Although heavy rare earths make up a smaller portion of the volume, they command premium prices. This is largely due to dysprosium, terbium, and yttrium's lack of scalable substitutes and their constrained supply. Dysprosium, the fastest-growing element, will track a 7.26% CAGR on the back of high-temperature magnet demand for EVs and offshore turbines.

China's dominance in supply heightens price sensitivity. Ionic-clay deposits in Jiangxi and Guangxi provinces produce a significant portion of the world's dysprosium, putting Western OEMs at risk of policy shocks. While Australian projects like Browns Range and Nolans offer a glimmer of diversification, they grapple with lengthy permitting and financing challenges. Consequently, producers capable of delivering separated heavy oxides retain significant pricing power, solidifying the premium structure in the Rare Earth Elements market.

By Element: Cerium Leads Volume, Dysprosium Captures Value

Cerium commanded 38.16% of the elemental share in 2025, driven by catalytic-converter and glass-polishing uses, and will remain volume leader through 2031. Forecasts indicate cerium will maintain its leadership position through 2031. Neodymium and praseodymium, together accounting for a significant portion of the market, play pivotal roles in the production of permanent magnets across China, Japan, and the U.S. Lanthanum finds its primary applications in fluid-cracking catalysts and nickel-metal-hydride batteries. Dysprosium, despite constituting a smaller share of the market, enjoys a high unit value and a 7.26% CAGR. This underscores dysprosium's critical importance in formulating high-temperature magnets, especially for electric vehicle traction motors and wind turbines. Terbium and yttrium, while occupying smaller market niches—terbium in green phosphors and yttrium in ceramics and LEDs—both grapple with similar supply constraints.

Scandium, with limited annual production, commands the highest price per kilogram in the market, a testament to its rarity and challenges in byproduct recovery. However, should recovery circuits in Canada and the U.S. become operational, scandium's applications could broaden from cabin brackets to encompass larger aerospace structural components, potentially expanding its presence in the Rare Earth Elements market.

By Application: Magnets Surge Past Catalysts as Primary Demand Vector

Magnets accounted for 48.54% of total volume in 2025 and are growing at a 7.43% CAGR, making them the engine of the Rare Earth Elements market through 2031. Industrial robotics adds momentum: each robot integrates servo motors, and global installations saw significant growth, with China leading in installations. Catalysts absorbed cerium in 2024 and stayed flat under rising hybrid penetration in emerging markets. Phosphors, glass-polishing, and metallurgy remain secondary, each with low single-digit growth, ceding share to the magnet segment as electrification accelerates.

By End-Use Industry: Clean Energy Dominates, Industrial Automation Accelerates

Clean energy held 30.36% of the 2025 volume and retains leadership as offshore wind and EV adoption surge. Industrial automation is the fastest-growing end use, advancing at a 6.49% CAGR, propelled by expanding collaborative-robot deployment across China, Germany, and the United States. Consumer-electronics demand is plateauing as smartphone shipments level off, though per-unit magnet content remains sticky. Aerospace and defense contribute a small demand but are immunized from cyclical swings by national-security designations in the United States and European Union, ensuring stable procurement of samarium-cobalt and dysprosium-rich magnets. Healthcare, metallurgy, and agriculture round out consumption with niche but steady volumes.

Geography Analysis

Asia-Pacific accounted for 86.29% of global volume in 2025 and will maintain dominance with a 5.97% CAGR to 2031. China produced oxides and commanded the majority of the separation capacity. This dominance allowed China to exert export-control leverage, causing European dysprosium prices to surge significantly post-October 2025. Australia is positioning itself as the leading non-Chinese supplier. Arafura's Nolans project aims to produce neodymium-praseodymium oxide by 2027. Concurrently, Iluka Resources is progressing with a refinery targeting mixed-carbonate output. To mitigate their reliance, Japan and South Korea have inked multi-year contracts with Lynas and MP Materials.

North America is making strides to localize its supply. Mountain Pass, having produced concentrate in 2024, halted exports to China in Q3 2025, redirecting its feed to a separation plant in California. A significant equity stake from the Department of Defense is backing a heavy-earth circuit, targeting output by mid-2026. Energy Fuels' White Mesa mill, traditionally focused on uranium, pivoted to process monazite. Meanwhile, Ucore is in the process of establishing a RapidSX plant in Alaska.

Despite its market presence in 2025, Europe remains heavily reliant on imports. This is in light of the Critical Raw Materials Act, which sets ambitious targets for extraction, processing, and recycling by 2030. While LKAB's Per Geijer deposit boasts significant oxide reserves, its development is a decade away. Pilot recycling initiatives from Cyclic Materials and Urban Mining Company seek to address the shortfall, yet the region lacks any commercial-scale separator. Both South America and the Middle East-Africa regions combined accounted for a minimal share of the total volume. However, Brazil and South Africa are eyeing potential capacities that could materialize post-2030.

Competitive Landscape

The Rare Earth Elements market is consolidated. Technology differentiation is surfacing: Ucore’s RapidSX molecular-recognition platform attains 99.9% purity in a single pass, trimming processing times from weeks to hours. Heavy-earth supply and recycling remain white-space opportunities. Firms that master heavy-earth separation and magnet-grade recycling stand to capture premium margins as Chinese export controls persist.

Rare Earth Elements Industry Leaders

China Rare Earth Group Resources Technology Co., Ltd.

Lynas Rare Earths Ltd

MP Materials

Iluka Resources Limited

Shenghe Resources Holding Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: MP Materials has initiated commercial production of neodymium-praseodymium (NdPr) metal and commenced trial production of automotive-grade, sintered neodymium-iron-boron (NdFeB) magnets at its Independence facility in Texas. This development represents a crucial milestone in reestablishing the U.S. rare earth magnet supply chain.

- January 2024: MP Materials secured a USD 58.5 million grant to propel the construction of the U.S.'s inaugural fully-integrated rare earth magnet manufacturing facility, located in Fort Worth, Texas. This funding comes under the Section 48C Advanced Energy Project tax credit initiative.

Global Rare Earth Elements Market Report Scope

Rare Earth elements are used in loudspeakers, telescope lenses, studio lighting, and computer hard drives to make them smaller and more efficient. They are used in screens and displays as they can produce different colors. Rare Earth elements usually have high electrical conductivity, naturally occur together in minerals. They are the strongest magnets available today.

The market is segmented by product type, element, application, end-use industry, and geography. By product type, the market is segmented into light rare earth elements and heavy rare earth elements. By element, the market is segmented into cerium, neodymium, lanthanum, dysprosium, terbium, yttrium, scandium, and other elements (e.g., promethium, samarium). By application, the market is segmented into catalysts, ceramics, phosphors, glass and polishing, metallurgy, magnets, and other applications (e.g., air cleaning). By end-use industry, the market is segmented into clean energy, consumer electronics, aerospace and defense, industrial automation, healthcare, and other industries (e.g., metallurgy, agriculture). The report also covers the market sizes and forecasts for the rare earth elements market in 17 countries across the major regions. For each segment, the market sizing and forecasts have been done based on volume (Ton).

| Light Rare Earth Elements |

| Heavy Rare Earth Elements |

| Cerium | Oxide |

| Sulfide | |

| Other Compounds | |

| Neodymium | Alloy |

| Lanthanum | Alloy |

| Oxide | |

| Other Compounds | |

| Dysprosium | |

| Terbium | |

| Yttrium | |

| Scandium | |

| Other Elements (Promethium, Samarium, etc.) |

| Catalysts |

| Ceramics |

| Phosphors |

| Glass and Polishing |

| Metallurgy |

| Magnets |

| Other Applications (Air Cleaning, etc.) |

| Clean Energy |

| Consumer Electronics |

| Aerospace and Defense |

| Industrial Automation |

| Healthcare |

| Other End-user Industries (Metallurgy, agriculture, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Nordics | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Product Type | Light Rare Earth Elements | |

| Heavy Rare Earth Elements | ||

| By Element | Cerium | Oxide |

| Sulfide | ||

| Other Compounds | ||

| Neodymium | Alloy | |

| Lanthanum | Alloy | |

| Oxide | ||

| Other Compounds | ||

| Dysprosium | ||

| Terbium | ||

| Yttrium | ||

| Scandium | ||

| Other Elements (Promethium, Samarium, etc.) | ||

| By Application | Catalysts | |

| Ceramics | ||

| Phosphors | ||

| Glass and Polishing | ||

| Metallurgy | ||

| Magnets | ||

| Other Applications (Air Cleaning, etc.) | ||

| By End-use Industry | Clean Energy | |

| Consumer Electronics | ||

| Aerospace and Defense | ||

| Industrial Automation | ||

| Healthcare | ||

| Other End-user Industries (Metallurgy, agriculture, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How large is the Rare Earth Elements market in 2026?

The Rare Earth Elements market size is 208.02 kilotons in 2026, with volume expected to reach 273.30 kilotons by 2031.

What is the forecast CAGR for rare earth demand through 2031?

Aggregate demand is projected to register a 5.61% CAGR between 2026 and 2031.

Which application segment is growing the fastest?

Permanent-magnet applications are expanding at a 7.43% CAGR, driven by electric vehicles, wind turbines, and industrial robotics.

Which element shows the highest growth rate?

Dysprosium leads elemental growth with a 7.26% CAGR, reflecting its irreplaceability in high-temperature magnets.

Page last updated on: