Quantum Dots (QD) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 10.3 Billion |

| Market Size (2031) | USD 15.73 Billion |

| Growth Rate (2026 - 2031) | 8.86% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia |

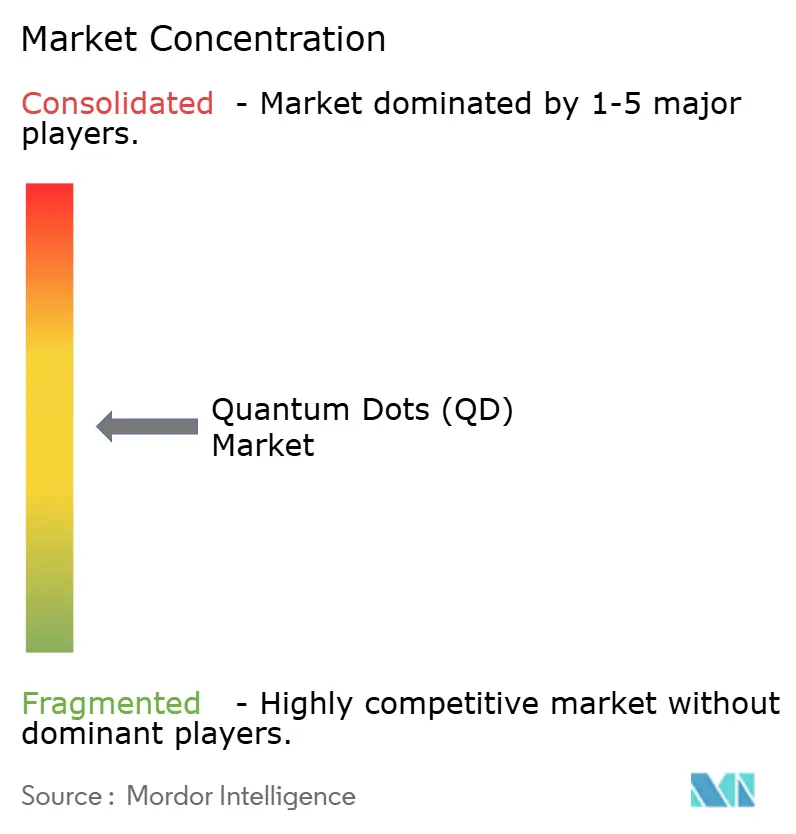

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Quantum Dots (QD) Market Analysis by Mordor Intelligence

The global quantum dots market size is expected to grow from USD 9.46 billion in 2025 to USD 10.3 billion in 2026 and is forecast to reach USD 15.73 billion by 2031 at 8.86% CAGR over 2026-2031. Commercial maturity is accelerating as the technology migrates from laboratory discovery to mass-produced components in ultra-high-definition displays, quantum‐secure communication nodes, and next-generation bio-imaging platforms. [1]Samsung Newsroom, “Real Quantum Dot Guide: Samsung's Innovations Redefine Picture Quality Standards,” news.samsung.com China’s rapid uptake of quantum-dot televisions, the emergence of cadmium-free chemistries that comply with EU RoHS limits, and sustained government funding in Asia and the Middle East are sustaining long-term demand. Manufacturing scale advantages in Asia-Pacific, combined with perovskite breakthroughs that lift efficiency and color purity, are lowering unit costs faster than legacy OLED alternatives, opening mainstream consumer price points. In parallel, quantum computing architectures based on semiconductor quantum dots, and five-fold sensitivity gains in cancer diagnostics, are expanding total addressable opportunities well beyond displays.

Key Report Takeaways

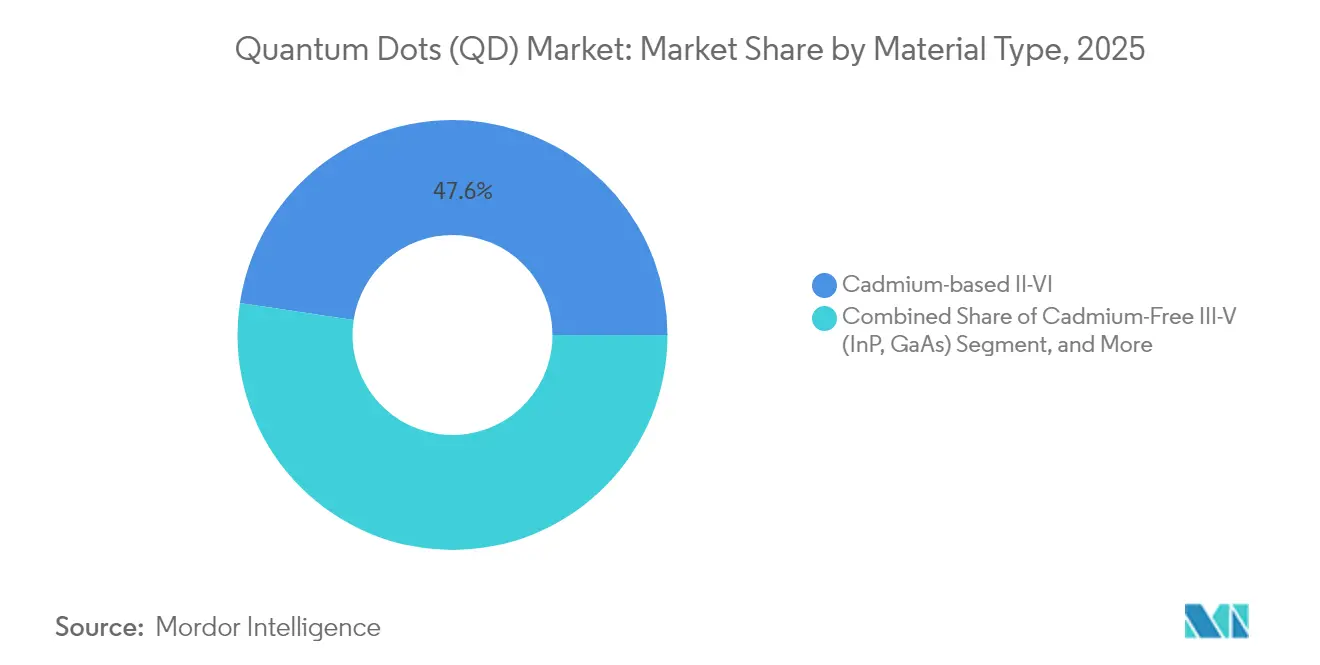

- By material type, cadmium-based II-VI compounds led with 47.62% of quantum dots market share in 2025, while perovskite quantum dots are projected to grow at an 11.28% CAGR through 2031.

- By device form factor, QD films dominated with 71.35% revenue share in 2025; on-chip quantum dots record the highest forecast CAGR at 12.15% to 2031.

- By application, display technologies held 65.48% share of the quantum dots market size in 2025, whereas quantum computing and security solutions advance at a 12.92% CAGR.

- By end-use industry, consumer electronics commanded 67.22% revenue in 2025, while healthcare and life sciences expand fastest at a 11.74% CAGR.

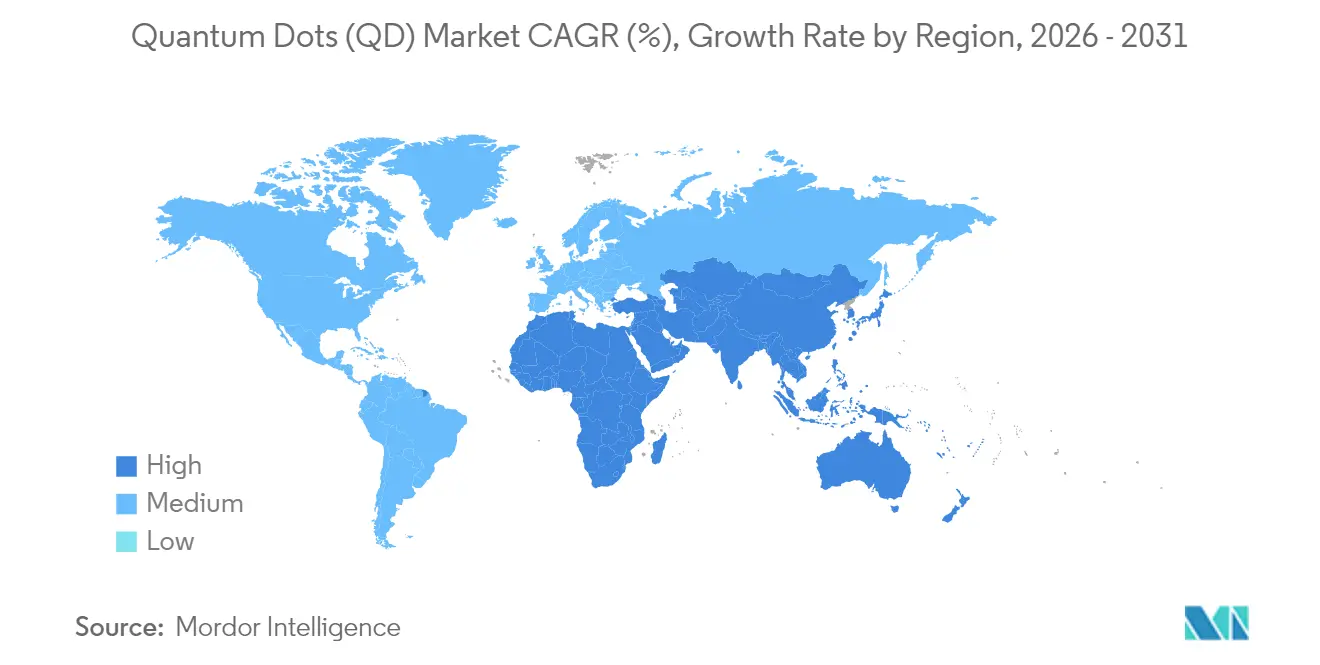

- By geography, Asia-Pacific accounted for 37.85% of 2025 revenue; the Middle East and Africa region is set to rise at a 10.18% CAGR, the quickest worldwide.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Quantum Dots (QD) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Quantum-dot adoption in ultra-high-definition TV panels | +2.80% | China; broader Asia-Pacific | Medium term (2–4 years) |

| Regulatory push for cadmium-free quantum dots in EU consumer electronics | +1.90% | Europe; spill-over to North America | Long term (≥ 4 years) |

| Rapid commercialization of perovskite quantum dots in display back-lighting | +2.10% | South Korea, China, Japan | Short term (≤ 2 years) |

| Surge in quantum-dot bio-imaging agents for healthcare | +1.40% | North America, EU, Asia-Pacific | Medium term (2–4 years) |

| Government-funded quantum-materials R&D programs in South Korea | +1.10% | South Korea; allied export markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Quantum-dot adoption in ultra-high-definition television panels, led by China

Domestic panel makers have installed high-capacity quantum-dot film lines that deliver more than 100% NTSC color gamut, while TCL’s QM6K series achieves 98%+ DCI-P3 coverage and 53% higher brightness through Super High Energy LED back-lights. BOE’s USD 9 billion Gen-8.6 AMOLED facility, coming online in 2026, reinforces cost leadership and secures supply for regional brands. The shift from RGB OLED to QD-OLED architectures simplifies manufacturing, enhancing yield and lowering capex per square meter for 4K and 8K screens.

Regulatory push for cadmium-free quantum dots in EU consumer electronics

The EU’s 0.01 wt% cadmium cap under RoHS is driving early movers toward copper-indium and indium-phosphide formulations.[2]European Chemicals Agency, “Restricted substances referred under Article 4 of RoHS,” echa.europa.eu UbiQD’s USD 20 million Series B round will scale cadmium-free production, while Applied Materials has proven lead-free devices matching cadmium performance in color conversion layers. Universities are commercializing aqueous synthesis routes that remove organic solvents and cut process emissions, creating cost and compliance advantages for adopters.

Rapid commercialization of perovskite quantum dots in display back-lighting

Surface-engineered perovskite quantum dots have sustained 12-hour continuous photon emission with no decay and reached 98% single-photon purity, clearing previous stability hurdles. Microfluidic synthesis delivers batch-to-batch uniformity and lowers reagent usage, pushing perovskite costs toward parity with traditional phosphors. Core-shell architectures and phospholipid coatings mitigate moisture sensitivity, enabling qualification for QD-EL and microLED back-lights in commercial prototypes seen at CES 2025.

Surge in quantum-dot bio-imaging agents in healthcare applications

Carbon quantum dots derived from pharmaceutical precursors enhance drug solubility and reduce systemic toxicity, while silicon quantum dots offer non-toxic ocular imaging at sub-16 µg/mL concentrations. Cancer-detection assays using zinc-to-silver exchange quantum dots register five-fold sensitivity improvements, and quantum-dot hydrogels achieve 43% photothermal conversion, inhibiting 83% of tumor growth in pre-clinical models. These breakthroughs position quantum dots for next-generation multiplexed diagnostics and targeted therapies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Bottlenecks for High-Purity Indium-Phosphide Precursors | -1.7% | Global, with acute impact on Asia-Pacific manufacturing | Medium term (2-4 years) |

| Performance Degradation of Perovskite QDs Under Moisture Exposure | -1.3% | Global, particularly humid climate regions | Short term (≤ 2 years) |

| Environmental-Compliance Costs of Cadmium Regulations in Europe | -0.9% | Europe, with regulatory spillover to North America | Long term (≥ 4 years) |

| Limited Mass-Manufacturing Infrastructure for QD Micro-LED Integration | -1.1% | Global, with concentration in Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-chain bottlenecks for high-purity indium-phosphide precursors

Indium demand from 6G infrastructure is projected to consume 4% of annual production, squeezing availability for indium-phosphide quantum dots and pushing prices higher. Soochow University’s ink-engineering route lowers photovoltaic costs to USD 0.06/Wp but relies on consistent indium purity, which remains scarce outside a handful of refiners. Microwave-assisted and ionic-liquid syntheses reduce hazardous reagents yet still require secure metal feedstocks, keeping supply risk elevated through at least 2028.

Performance degradation of perovskite quantum dots under moisture exposure

Ambient humidity promotes tin oxidation, methylammonium loss, and phase segregation in perovskite lattices, cutting device lifetimes. Protective PMMA coatings have extended operational integrity to 960 hours, and dynamic passivation with hindered urea bonds retains 94% efficiency after 1,500 hours at 85 °C, but mass-manufacturing lines must operate in low-dew-point environments to ensure repeatability. Climate-dependent degradation still limits adoption in hot, humid markets without robust encapsulation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Cadmium-free innovation accelerates despite legacy dominance

Cadmium-based II-VI compounds held 47.62% of 2025 revenues, anchoring the quantum dots market through well-established supply chains and high quantum yields. Regulatory exposure, however, compresses their outlook as EU and California policies converge on lighter-element chemistries. Perovskite variants, supported by 11.28% CAGR, move from lab novelty to production-ready emitters that match cadmium brightness and achieve room-temperature single-photon purity, broadening relevance for secure communications. Indium-phosphide platforms benefit from UbiQD’s scale-up funding and Applied Materials’ process optimization, yet precursor shortages temper near-term penetration. Silicon and carbon quantum dots are carving biomedical niches, showing negligible cytotoxicity at clinically relevant doses and enabling fluorescence-guided surgery. Historic data reveal cadmium alternatives growing 15–20% annually versus sub-5% for cadmium incumbents from 2020-2024, signaling a structural pivot in the quantum dots market.

Second-generation materials diversify end-use reach. Graphene quantum dots fused with silicon nanoshells achieve 71% aphid-population suppression, positioning nanomaterials for precision agriculture beyond displays. Perovskite glow layers are now printable at 140 PPI, easing integration into mid-sized monitors, while silicon dots deliver stable infrared photoluminescence critical for wearable biosensors. The quantum dots market size for cadmium-free segments is projected to rise at double-digit rates, reinforcing supplier pivots toward low-toxicity chemistries. Heightened corporate ESG targets, plus upcoming RoHS exemptions sunsets, cement the transition path.

By Device Form Factor: On-chip integration drives next-generation applications

QD films remain revenue mainstays with 71.35% share in 2025, favored by television OEMs seeking plug-and-play color converters that slip into existing LCD stacks. Yet on-chip quantum dots display the highest 12.15% CAGR as semiconductor fabs capture photonic emitters directly on foundry platforms. University of Cambridge’s 13,000-spin quantum register, achieving 69% fidelity at 130 µs coherence, underscores leapfrog potential for chip-scale quantum nodes. Core-shell nanopillars grown through microfluidic reactors now exhibit sub-5% size dispersion, crucial for coherent emission. Electrophoretic deposition on corrugated wafers yields crack-free near-infrared detectors, opening automotive LiDAR and medical endoscope markets. As line width reductions plateau, integrated photonics offers Moore-than-More scaling, with quantum dots supplying the single-photon sources missing from silicon photonics roadmaps.

Scaling pathways diverge. Inkjet printed QD-OLED panels already hit 31.5-inch diagonals at commercial yield, while electrohydrodynamic jetting produces micron-scale RGB pixels for microLED arrays. The quantum dots market size captured by on-chip formats is set to widen as performance gains in quantum computing justify higher ASPs. Investments in atomic-layer deposition and atomic-precision lithography will further align dot placement with transistor gateways, shrinking interconnect delays in quantum buses. Device OEMs are bundling intellectual property around packaging, thermal management, and lithographic alignment, creating new defensible moats.

By Application: Quantum computing emergence reshapes market dynamics

Display systems retained 65.48% of 2025 revenues, underpinned by Samsung’s shift to QD-OLED and mini-LED back-lighting that makes superior Rec. 2020 coverage affordable. However, quantum-secure communication links and register arrays record a 12.92% CAGR, propelled by IonQ’s USD 1.1 billion Oxford Ionics acquisition, which targets two-million-qubit hardware by 2030. Semiconductor-based quantum dots supply deterministic photon sources essential for error-corrected qubits and quantum key distribution. In bio-med, five-fold gains in oncology assay sensitivity reposition quantum dots as must-have contrast agents. Photovoltaic researchers at Los Alamos report 41% efficiency jumps using manganese-doped quantum dots, challenging perovskite tandem cells. Agriculture pilots that blend light-optimizing films with copper-indium dots improve greenhouse yields and cut pesticide loads, confirming multipronged upside.

Momentum is reinforced by diverse revenue pools. MicroLED fabs count on quantum dots for fine-pitch full-color conversion, offsetting slow yields in direct RGB chip processes. Security agencies fund quantum random-number generators for encrypted satellites, while oil & gas majors test quantum-dot tracers that map reservoir flow paths with single-ppm sensitivity. This broadening end-use scope cushions demand cyclicality in consumer displays and underlines the quantum dots market’s resilience.

By End-Use Industry: Healthcare disruption accelerates beyond consumer electronics

Consumer electronics held 67.22% of 2025 spend, but healthcare and life sciences clock the fastest 11.74% CAGR through breakthroughs in multiplexed imaging and targeted photothermal therapy. Carbon-based “quantum drugs” synthesized directly from APIs display enhanced bioavailability without added toxicity, while silicon dots visualize tear films in ophthalmology at nanogram doses. Hospitals deploy quantum-dot assays that isolate micro-RNA cancer markers at tenfold lower false-negative rates than ELISA. Defense users exploit quantum dots in quantum-secure radios and low-SWaP night-vision cameras. Energy firms integrate quantum-dot luminescent concentrators into building façades, harvesting diffuse sunlight to power IoT nodes. The quantum dots market has thus shifted from single-sector dependence to multi-industry diffusion, diluting price pressure risks typical of consumer cycles.

Regulation and sustainability reinforce diversification. EU ecodesign rules prioritize repairable TVs, nudging display OEMs to adopt quantum-dot films that withstand higher back-light temperatures and extend product lifetimes. Healthcare agencies favor cadmium-free probes, fast-tracking indium-phosphide and silicon dots into clinical trials. Agricultural quantum films secure green-house dispensations in sustainable-farming subsidies, aligning agritech with climate policy. Together these trends expand quantum dots market share for emerging verticals while stabilizing long-term demand.

Geography Analysis

Asia-Pacific maintains leadership with 37.85% of 2025 revenue due to vertically integrated panel makers and deliberate national R&D funding. Samsung Display’s USD 10.9 billion conversion to QD-OLED lines and South Korea’s KRW 491 billion quantum program cement the ecosystem, while China’s BOE invests USD 9 billion in Gen-8.6 capacity that anchors local supply chains. Japan complements manufacturing heft with process innovation, hosting seminars to solve toxicity and durability bottlenecks. The quantum dots market size in Asia remains underpinned by domestic demand for premium TVs and by export flows into North America and Europe.

North America follows with deep research assets at University of Cambridge (Cambridge-US collaborations), MIT Lincoln Laboratory, and Los Alamos National Laboratory driving quantum-secure links and high-efficiency photovoltaics. Venture capital traction is robust, proven by UbiQD’s USD 20 million raise and IonQ’s headline acquisitions. Strong IP protection and federal funding ensure commercialization pipelines, and US export-control scrutiny over cadmium compounds nudges suppliers toward indium-phosphide builds. Europe leverages regulatory influence: RoHS compliance sparks cadmium-free adoption, while University of Liège’s aqueous syntheses cut hazardous waste. Government green-deal funds deploy quantum-dot window films for energy-positive buildings.

The Middle East and Africa record the fastest 10.18% CAGR. UAE’s Norma Center, Qatar’s USD 10 million program, and Saudi R&D funds foster quantum-dot computing clusters, aiming to diversify oil economies. Import substitution policies encourage local assembly of QD-enhanced solar panels and medical devices. Latin America sees nascent demand in agrotechnology, where quantum-dot greenhouse sheets improve fruit yield in high-altitude farms, yet market penetration remains under 3%. Overall, geographic revenue dispersion reduces concentration risk: Asia’s share inches lower toward 35% by 2030 as Middle East and Africa capture investment flows and as Western regions on-shore critical materials processing.

Regulatory Landscape

The regulatory environment for quantum dots continues to be shaped by hazardous-substance rules for electronics and chemical-safety frameworks for nanomaterials. In the European Union, RoHS Directive (2011/65/EU) keeps cadmium limits central to material selection, and Commission Delegated Directive (EU) 2024/1416 (adopted March 13, 2024) tightened cadmium-containing quantum-dot pathways by ending the exemption for cadmium selenide in display lighting quantum dots (entry 39a) as of November 21, 2025.

Directive (EU) 2024/1416 also introduced a narrower, time-bound exemption for cadmium in downshifting quantum dots directly deposited on LED semiconductor chips for display and projection applications (entry 39b). The allowance is capped at 5 micrograms per square millimeter of LED chip surface, with a maximum of 1 milligram per device, and it expires on December 31, 2027. Separately, the European Chemicals Agency (ECHA) manages nanomaterial risk under REACH, including nanoforms of substances, which raises documentation, testing, and compliance requirements for quantum-dot chemistries and formulations supplied into Europe.

Value Chain Analysis

The quantum dots value chain begins with upstream feedstocks and high-purity precursors, including indium, phosphorus, selenium, and ligand systems, before moving into nanocrystal synthesis (core, core-shell, and perovskite variants) and purification steps that affect optical yield and stability. Midstream participants then formulate quantum dots into films, resins, inks, and color-conversion layers, which are qualified by display, lighting, photovoltaic, healthcare, and photonics OEMs using reliability testing (thermal, humidity, photobleaching) and device integration. Downstream, panel makers and device OEMs build QD-LCD and QD-OLED stacks, expand inkjet-printed emissive concepts, and commercialize quantum-dot products beyond display, including luminescent solar and agricultural films.

Recent supply-chain actions are also pointing to more semiconductor-grade structuring and diversification beyond displays. Quintessent and IQE established a dedicated epitaxial wafer supply chain in January 2025, with IQE supplying 6-inch GaAs-based quantum-dot wafers for QD laser and SOA devices aimed at AI optical interconnects. In July 2025, UbiQD and First Solar signed a multi-year exclusive supply agreement to integrate fluorescent quantum dot technology into thin-film bifacial PV modules, with an industrial scaling target of over 100 metric tons of quantum dots per year. This shift implies higher-volume requirements and more stringent qualification regimes, alongside persistent bottlenecks tied to concentrated sources for critical precursors and limited vendor bases for specialized equipment and high-purity processing, which in turn lengthen lead times and encourage vertical integration among major display and materials participants.

Competitive Landscape

Top Companies in Quantum Dots Market

Moderate concentration typifies the quantum dots market. Samsung, LG Display, and BOE exploit scale and captive fabs to supply television OEMs at competitive cost, yet specialized players such as Nanosys and UbiQD differentiate through patented cadmium-free chemistries. Applied Materials leverages process tooling expertise to deliver turnkey quantum-dot encapsulation lines, embedding itself across multiple customer roadmaps. IonQ’s USD 1.1 billion Oxford Ionics deal signals convergence between display heritage and quantum computing ambitions, while Quantinuum’s planned USD 10 billion IPO validates investor belief in non-display upside. [3] Laser Focus World, “Quantinuum eyes $10B IPO,” laserfocusworld.com

Strategic moves sharpen competitive contours. Samsung partners with the Institute for Basic Science to co-develop environmentally benign quantum‐dot interfaces, preserving lead times as RoHS deadlines loom. BOE’s Gen-8.6 plant includes vertically integrated perovskite pilot lines, hedging against future cadmium bans. UbiQD channels Series B proceeds into agricultural and solar films, opening revenue beyond electronics and reducing exposure to panel cycles. Intellectual-property friction is rising: over 4,300 quantum-dot patents were filed worldwide in 2024, and cross-licensing deals increasingly dictate supply permissions.

White-space opportunities attract newcomers. Start-ups bundle quantum-dot single-photon sources with photonic integrated circuits for telecom, while biotech firms license bright, narrow-band emitters for point-of-care diagnostics. Microfluidics vendors supply additively manufactured reactors that slash batch variation, winning contracts from healthcare and defense primes. As the quantum dots industry scales, downstream integrators (television brands, medical device OEMs, cloud service providers) shape demand signals, forcing upstream suppliers to diversify chemistries and geography. Pricing remains resilient because high-value performance gains outweigh material input inflation.

Quantum Dots (QD) Industry Leaders

Samsung Electronics Co., Ltd.

Nanosys Inc.

LG Display Co., Ltd.

BOE Technology Group Co., Ltd.

Nanoco Group PLC

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Tightening RoHS enforcement in Europe is creating clearer whitespace for cadmium-free and heavy-metal-free quantum dot materials that can meet high-temperature and high-flux demands in solid-state lighting and high-brightness displays. After the November 21, 2025 expiration of the broader RoHS display-lighting exemption, and with the narrower on-chip exemption limited to December 31, 2027, display and component supply chains need to qualify indium-phosphide, copper-indium, silicon, carbon, and other cadmium-free routes at production scale rather than relying on exemptions.

The commercial pull is also spreading beyond mainstream TV backlights into PV, optical interconnects, and print-based display manufacturing. In July 2025, UbiQD and First Solar moved quantum dots deeper into the PV value chain through a multi-year supply agreement for bifacial thin-film modules, tied to an industrial scale-up target above 100 metric tons per year. On the manufacturing side, the European Commission-funded QustomDot project reported in July 2026 on patented cadmium-free quantum dot inkjet inks and active engagement with display manufacturers for pilot projects, aligning with industry interest in inkjet printing for high-resolution architectures and new form factors. Taken together, these proof points support the opportunity for materials suppliers and integrators able to deliver stable, cadmium-free inks and films, along with the process controls needed for repeatable deposition and long-lifetime operation.

Recent Industry Developments

- May 2026: Samsung Display announced the development of a 4K 360Hz QD-OLED monitor panel, with mass production planned for the second half of 2026. The specification targets premium gaming and professional monitor segments where refresh-rate and color performance drive adoption, and it reinforces QD-OLED positioning against competing high-end display technologies.

- July 2025: UbiQD and First Solar entered a multi-year exclusive supply agreement to incorporate UbiQD fluorescent quantum dot technology into First Solar thin-film bifacial PV modules. The deal links quantum dots to a high-volume energy application and includes a scale-up ambition of more than 100 metric tons of quantum dots per year, signaling tighter supplier qualification and manufacturing readiness beyond display-centric demand.

- March 2024: The European Union adopted Commission Delegated Directive (EU) 2024/1416 amending RoHS exemptions for cadmium in quantum-dot applications, including setting the end date for the previous display-lighting exemption and defining a narrower on-chip exemption with explicit mass limits. The update increased compliance urgency for display and component suppliers selling into Europe and accelerated qualification programs for cadmium-free quantum dot chemistries.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the quantum dots market is defined as revenues generated from the commercial sale of quantum dot materials that are engineered and packaged for integration into end products across electronics, energy, and life-sciences use cases.

Scope exclusions: We exclude laboratory research reagents, one-off prototypes, and the value of finished devices like TVs, monitors, or solar panels that only embed quantum dots.

Segmentation Overview

- By Material Type

- Cadmium-based II-VI (CdSe, CdS, CdTe)

- Cadmium-Free III-V (InP, GaAs)

- Perovskite Quantum Dots

- Silicon Quantum Dots

- Graphene and Carbon Quantum Dots

- By Device Form Factor

- QD Films

- On-Chip Quantum Dots

- Core-Shell and In-Shell Architectures

- By Application

- Displays

- QD-LCD

- QD-OLED

- Micro-LED Integration

- Lighting

- General Illumination

- Specialty Lighting

- Solar Cells and Photovoltaics

- Medical Imaging and Diagnostics

- Drug Delivery and Theranostics

- Sensors and Instruments

- Quantum Computing and Security

- Agriculture and Food

- Others

- Displays

- By End-Use Industry

- Consumer Electronics

- Healthcare and Life Sciences

- Energy and Power

- Defense and Security

- Agriculture

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Nordics

- Rest of Europe

- South America

- Brazil

- Rest of South America

- Asia-Pacific

- China

- Japan

- India

- South-East Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Gulf Cooperation Council Countries

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary, map the value chain, and collect anchor indicators that can be checked each year. We leaned on public sources such as US DOE publications, the US International Trade Commission, OECD and World Bank macro indicators, and IEEE or similar peer-reviewed journals that discuss quantum dot performance and adoption.

On the commercialization side, we reviewed company filings, investor presentations, product announcements, and credible press coverage to understand where quantum dots are being integrated and how product formats are sold (for example, powders versus films or inks). Select paid subscriptions that cover company financials, patents, and shipment-level trade records were used only to fill gaps and keep assumptions consistent across regions. These examples are illustrative, and many additional public sources were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and surveys with material suppliers, component and film or ink formulators, display and lighting ecosystem participants, and downstream users in healthcare and sensing. We used inputs across APAC, EMEA, and the Americas to pressure-test adoption timelines, pricing movement, and what is counted as quantum dot material revenue versus embedded device value.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 13% | APAC: 38% |

| Mid tier: 43% | Functional/Unit leaders: 29% | EMEA: 37% |

| Smaller Players: 21% | Managers: 58% | Americas: 25% |

Market-Sizing & Forecasting

Sizing started with a top-down build where application demand pools were reconstructed from observable industry signals, and then translated into quantum dot material value. In practice, this meant mapping shipments for quantum dot enabled displays, pairing that with typical material loading or bill-of-material share, and then converting into value using application-specific price points.

To keep the model grounded, we used a small set of repeatable inputs such as display shipment trends for QD-enabled panels, penetration of QD film versus on-chip approaches, average selling price movement for quantum dot materials, cadmium-free substitution rates driven by compliance needs, and the pace of newer use cases like sensing and bioimaging. Selective bottom-up approximations were then used as a check, including supplier revenue roll-ups where available and sampled volume times ASP builds by product format, with gaps handled through conservative ranges that were rechecked in interviews.

For forecasting, we relied on scenario analysis supported by expert views on adoption curves and price erosion, since the market is influenced by technology transitions and regulatory choices. The final forecast was adjusted so that near-term growth reflects realistic qualification cycles, and later-year expansion is aligned with what downstream buyers are actually planning to scale.

Data Validation & Update Cycle

Validation is done through a series of cross-checks so one data point does not drive the full outcome. We compare the outputs against independent indicators like shipment growth, penetration assumptions, and price progression, and then review any large variances by region or application before sign-off.

If a major mismatch shows up, follow-up calls are triggered to revisit definitions and re-check the assumptions that caused the swing. Reports are refreshed annually, with interim updates when material events occur such as major capacity additions, regulatory shifts affecting cadmium use, or rapid pricing changes. Before delivery, an analyst does a fresh final pass so clients receive the most current view available.

Mordor Intelligence's Quantum Dots Market Market Size Compared Against Other Published Estimates

Published market sizes for quantum dots often vary because the counted revenue base is not always the same, and the application mix can be treated differently across studies. Differences also come from how quickly pricing is assumed to decline, and whether early-stage uses in healthcare, sensing, and solar are counted as commercial or still pre-scale.

By tracking shipment-led demand signals and refreshing the embedded-material rule each update, Mordor Intelligence keeps the total tied to quantum dot materials sold as powders, films, and inks, instead of counting the full selling price of finished displays or devices that only contain these materials.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 10.3 B (2026) | |

| Industry Publisher A | USD 12.53 B (2025) | Uses a different base year and often applies a broader revenue lens that can blend material revenues with downstream device value, and it can also assume faster adoption across consumer electronics. |

| Global Research Group B | USD 8.19 B (2024) | Anchors on an earlier year and may apply more conservative near-term commercialization weights for non-display applications, which tends to reduce the present-year total even if long-term growth is high. |

Taken together, the table shows that the largest swings are explained by what is counted as market revenue, the chosen base year, and the price and penetration paths assumed for display-led demand. Our checks stay repeatable by tying each application to observable shipment and adoption indicators, and then confirming that the implied pricing and volumes match what practitioners report in interviews.

Key Questions Answered in the Report

What is the current size of the quantum dots market?

The quantum dots market reached USD 10.3 billion in 2026 and is projected to climb to USD 15.73 billion by 2031.

Which material segment is growing fastest?

Perovskite quantum dots are expanding at an 11.28% CAGR through 2031, outpacing cadmium and indium-based alternatives.

Why are cadmium-free quantum dots gaining momentum?

EU RoHS restrictions limit cadmium to 0.01 wt%, pressuring manufacturers to shift toward copper-indium and indium-phosphide chemistries that satisfy environmental rules.

Which region shows the highest growth potential?

The Middle East and Africa region posts the fastest 10.18% CAGR, driven by national quantum R&D programs in the UAE, Qatar, and Saudi Arabia.

How are quantum dots impacting healthcare?

Advanced bio-imaging agents using carbon and silicon quantum dots deliver five-fold cancer-detection sensitivity and enable photothermal therapies with 83% tumor inhibition in pre-clinical tests.

What is driving on-chip quantum dot adoption?

Semiconductor integration offers deterministic single-photon sources crucial for scalable quantum computing networks, fueling a 12.15% CAGR in on-chip formats.

Page last updated on: