Qatar Used Car Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

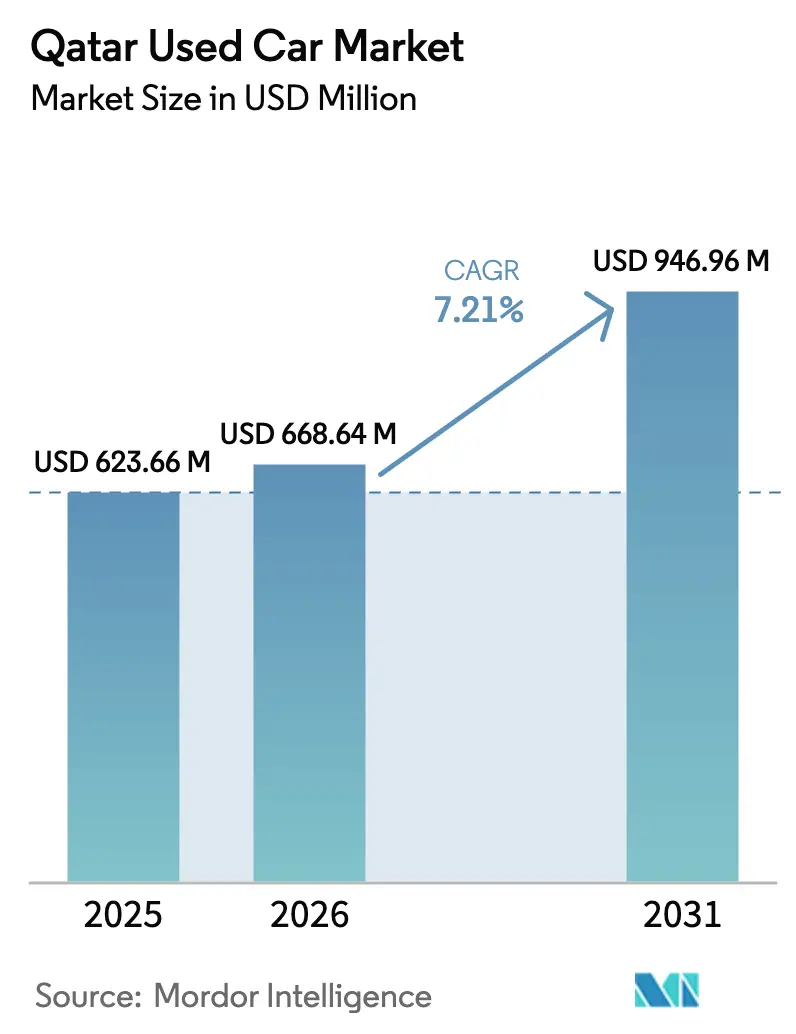

| Base Year Market Size (2025) | USD 623.66 Million |

| Market Size (2026) | USD 668.64 Million |

| Market Size (2031) | USD 946.96 Million |

| Growth Rate (2026 - 2031) | 7.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Used Car Market Analysis by Mordor Intelligence

Qatar used car market size in 2026 is estimated at USD 668.64 million, growing from 2025 value of USD 623.66 million with 2031 projections showing USD 946.96 million, growing at 7.21% CAGR over 2026-2031. This expansion unfolds against Qatar’s Third National Development Strategy, which promotes private-sector growth and sustainable mobility[1] International Monetary Fund, “Qatar Article IV Consultation—Staff Report,” imf.org. Digitized customs procedures introduced under the Integrated GCC Customs Tariff in January 2025 improve vehicle traceability, cutting clearance time and reinforcing buyer confidence[2]General Authority of Customs, “Integrated GCC Customs Tariff 2025,” customs.gov.qa. Currency stability—anchored by the Qatar Central Bank’s decades-old peg of QR 3.64 per USD - gives importers and financiers predictable cost structures. Meanwhile, steady 2% real GDP growth projected for 2025 underpins consumer spending power, while moderating 1% inflation preserves real wages. Digital platforms such as Q Motor shorten sales cycles, organized vendors capitalize on financing tie-ups, and a wave of low-mileage hybrids released from electrifying government fleets enlarges the pool of near-new inventory.

Key Report Takeaways

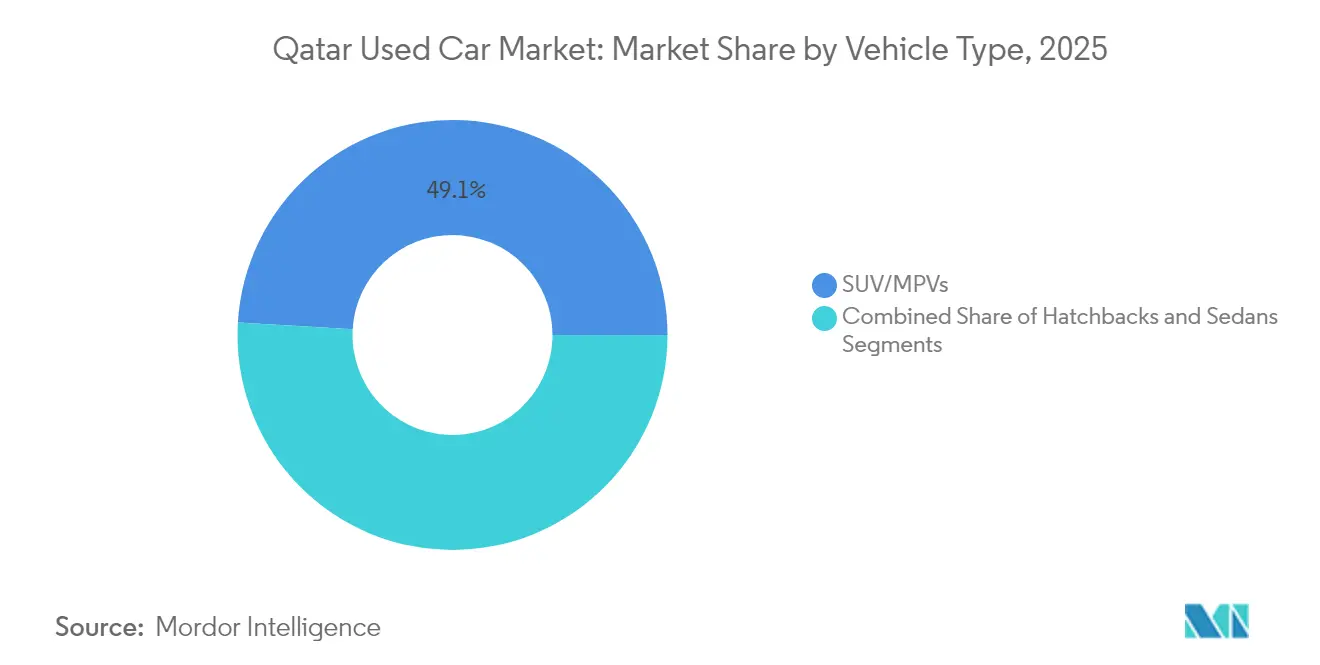

- By vehicle type, Sport Utility Vehicles dominated the Qatar used car market, holding a 49.08% share in 2025. SUVs are projected to grow at a robust 10.11% CAGR through 2031.

- By vendor type, the unorganized channel led the Qatar used car market with a 58.77% share in 2025. Meanwhile, the organized channel is expected to expand at an 8.41% CAGR, continuing through 2031.

- The petrol segment secured a 53.41% share of Qatar's used car market by fuel type in 2025. In contrast, battery electric vehicles are anticipated to surge, boasting a projected 14.52% CAGR over the forecast period.

- By sales channel, offline outlets held a 55.92% share of the Qatar used car market in 2025. However, online platforms are poised for significant growth, with a 13.35% CAGR expected from 2026 to 2031.

- By vehicle age, vehicles aged 3-5 made up 30.86% of the Qatar used car market in 2025. In contrast, vehicles aged 0-2 are forecasted to grow at a 9.18% CAGR through 2031.

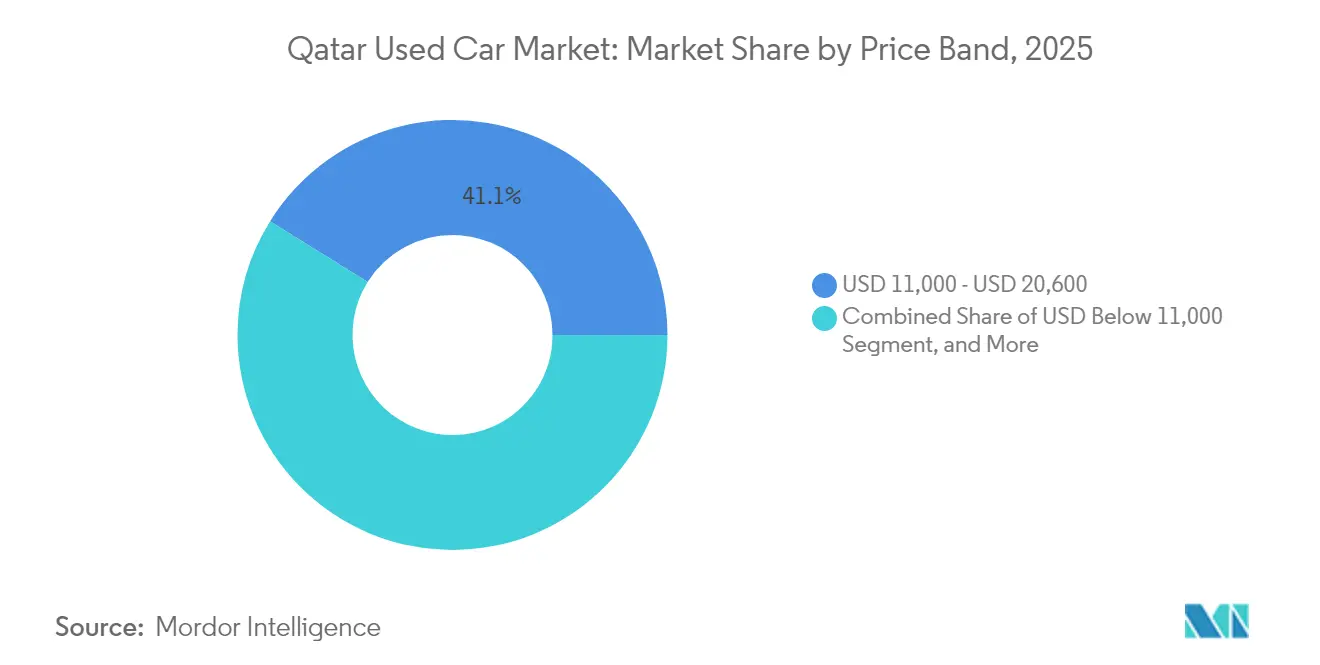

- By price band, vehicles between USD 11,000 and USD 20,600 dominated the Qatar used car market in 2025. Meanwhile, vehicles priced above USD 41,000 are projected to see an 8.28% CAGR increase.

- By city, Doha commanded a significant 78.62% share of the Qatar used car market in 2025, while Al Rayyan is set to experience the fastest growth, projected at a 6.60% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Expected changes in Qatar many a times form part of a broader pattern of global movement rather than an isolated trend. The report on worldwide used car market outlook by Mordor Intelligence brings these expectations together.

Qatar Used Car Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Retail Platforms | +1.8% | Doha and Al Rayyan | Short term (≤ 2 years) |

| Rising Expat Turnover | +1.5% | Nationwide, highest in Doha | Medium term (2–4 years) |

| Sharia-Compliant Financing Access | +1.2% | Urban centers nationwide | Medium term (2–4 years) |

| High Residual Value of Asian SUVs | +0.9% | Al Rayyan and suburban areas | Long term (≥ 4 years) |

| Government Inspection Centres | +0.8% | Major cities nationwide | Short term (≤ 2 years) |

| Taxi-Fleet Hybrid Influx | +0.6% | Doha metro area, expanding | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Digital-First Retail Platforms Accelerate Price Discovery and Inventory Turnover

Large classifieds such as Q Motor—drawing 500,000 monthly users—have moved the Qatar used car market toward transparent pricing and faster deal closure. Integrated inspection, warranty, and financing modules inside the app reduce friction for sellers and buyers alike. Improved data quality under the 12-digit customs codes introduced in 2025 lets platforms publish granular specs, supporting fair valuations and lowering dispute risk. With smartphone penetration topping 100% of residents, online reach now eclipses roadside dealer traffic, giving organized players scale economies that unorganized lots cannot match.

Growing Expatriate Population Shortens Ownership Cycles

Contract-based professionals often change cars every three to five years, recycling well-maintained stock into the Qatar used car market. The IMF expects real GDP to keep rising by 2% in 2025, sustaining job creation in non-hydrocarbon sectors and bringing new arrivals who favor late-model vehicles over older imports. A regulatory cap that bars imports older than five years compresses vehicle life cycles further, pushing demand toward younger inventory.

Wider Access to Sharia-compliant Used-car Financing

Banks such as Qatar Islamic Bank, whose ‘A’ rating was reaffirmed in July 2024, now bundle Murabaha contracts with dealer platforms, lowering down-payment hurdles for observant buyers. Competitive flat rates beginning near 3% and terms up to five years make organized vendors that can embed financing in the sale more attractive than cash-only roadside traders.

Japanese & Korean SUVs Retain Residual Value

Asian SUVs outperform rivals in Qatar’s hot climate regarding reliability, support higher resale prices, and encourage first-time buyers to pay a small premium upfront. A 5% uniform import duty plus a five-year age ceiling limits the supply of these models, further propping up prices. As government fleets phase in hybrids, gently-used Toyota and Kia SUVs filter into the secondary channel, enhancing stock depth without sacrificing margins[3]U.S. Department of Commerce, “Qatar—Automotive,” trade.gov.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chinese Brand Promotions Reduce Used-Car Appeal | -1.4% | National, with strongest impact in price-sensitive segments | Short term (≤ 2 years) |

| High Lending Rates Increase Ownership Costs | -1.1% | National, affecting middle-income segments disproportionately | Medium term (2-4 years) |

| Import Cap on 8+ Year Vehicles Limits Budget Supply | -0.8% | National, particularly affecting budget-conscious buyers | Long term (≥ 4 years) |

| Qataris Prefer First-Owner Vehicles | -0.6% | Concentrated in affluent areas of Doha and Al Rayyan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Aggressive Promotion of New Chinese Brands Narrows Used-car Price Gap

Cut-price launches bundled with lengthy warranties pull value-focused shoppers toward showroom-fresh vehicles. Chinese OEMs leverage the same 5% duty that applies to all imports yet undercut late-model used cars, squeezing dealer spreads. Their portfolio of small EVs also aligns with state green-mobility goals, further challenging conventional petrol offerings.

High Bank Lending Rates Inflate Total Cost of Ownership

Despite respectable banking liquidity, commercial lending costs remain elevated. Middle-income expatriates who finance purchases face higher monthly outlays, curbing demand in the Qatar used car market. Islamic lenders mitigate the pain, yet cannot completely offset tightening credit standards prompted by rising sector non-performing loans.[4] International Monetary Fund, “Qatar Article IV Consultation—Staff Report,” imf.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: SUVs Leads the Market and Demand Surges

SUVs commanded 49.08% of the Qatar used car market share in 2025, due to their maneuverability and lower running costs in dense Doha traffic. However, SUVs capture mindshare and are projected to expand at a 10.11% CAGR to 2031, buoyed by suburban migration into Al Rayyan and a cultural preference for higher-riding vehicles. This trend ensures the Qatar used car market size allocated to SUVs will outpace every other body style through the forecast window.

Compact sedans cater to families balancing affordability and cabin space, but their pie stabilizes rather than grows. Luxury SUVs maintain price resilience because of robust residual values, while micro-imports such as kei-class cars remain niche, hampered by limited service coverage.

By Vendor Type: Unorganized Dealers Extend their Lead

With a 58.77% grip on the Qatar used car market size in 2025, unorganized vendors exploit omnichannel tactics, and the organized channel is expected to grow with a CAGR of 8.41%. Digital storefronts steer traffic to air-conditioned showrooms where inspection reports and warranty add-ons close the sale. As quality-testing centers roll out nationwide, unorganized sellers lose a key point of differentiation-under-pricing-because buyers place a premium on certified condition.

Semi-organized independents, often single-location operators, ride the certification wave by affiliating with inspection labs, while roadside lots face higher compliance costs. Financing tie-ups further tilt the field: organized networks can approve loans in hours, a service street-corner dealers cannot replicate.

By Fuel Type: Electric Momentum Quickens

Petrol units still held a 53.41% of the Qatar used car market share in 2025, but electric cars headline growth at a 14.52% CAGR as public EV chargers proliferate. The Qatar used car industry feels the pull of policy targets that require all public transport to be eco-friendly by 2030, spurring private curiosity about EVs. Late-model hybrids released from taxi fleets give price-sensitive users an entrée into electrified powertrains.

Diesel drops in relevance, hurt by tighter emissions standards and higher maintenance bills. LPG/CNG remains confined to fleet buyers. As battery prices fall and charging spreads beyond the Pearl Island, pure EVs gain momentum yet remain a premium choice because of high upfront costs.

By Vehicle Age: Young Stock Dominates Turnovers

Vehicles aged 3-5 years delivered 30.86% of the Qatar used car market share in 2025, underscoring a preference for relatively new units with factory warranty remaining. 0-2-year models are forecast to post a 9.18% CAGR, lifted by expatriates’ short assignment cycles and constrained import rules that cap the supply of older cars. Cars 6-8 years old draw budget-conscious buyers, but looming proposals prohibiting imports above eight years could crimp availability. Over-eight-year units will likely become scarce, supporting price floors yet limiting volume potential in the Qatar used car market.

By Price Band: Middle Tier Anchors Demand

The USD 11,000-USD 20,600 range absorbed 41.12% of the Qatar used car market share in 2025, favored by mid-income households and younger professionals. Premium brackets above USD 41,000 captured affluent nationals eyeing luxury trims and are set for an 8.28% CAGR as wealth continues to pool in Doha’s high-end districts. Models under USD 11,000 face direct competition from zero-kilometer Chinese entry cars, whereas the USD 20,601-41,000 slice benefits from SUVs with enduring residual value. Financing approvals skew toward higher-ticket purchases where default risk is statistically lower.

By Sales Channel: Offline Dominates while Online Accelerates

Offline-only outlets captured the largest 55.92% Qatar used car market share in 2025, thanks to face-to-face negotiation, immediate handover, and established neighborhood service links. Dealer groups have upgraded these yards with climate-controlled showrooms and on-site inspection bays, keeping late-model SUVs and premium imports firmly priced as physical premises still anchor title transfer and registration.

Online-only marketplaces are projected to record the fastest 13.35% CAGR between 2026 and 2031, propelled by universal smartphone use, escrow payments, and AI-driven price benchmarking. Shoppers now browse on mobile, book test-drives at partner hubs, and complete paperwork digitally, creating an omnichannel loop that marries convenience with touch-and-feel assurance. Uniform inspection standards let digital sellers move vehicles nationwide with minimal reputation risk, so although offline retains the volume lead, future growth and margin expansion tilt toward platforms that master last-mile, paperwork-light delivery.

Geography Analysis

In 2025, Doha anchored 78.62% of the Qatari used car market. Its dense expat population, ubiquitous banking services, and rich dealer clusters foster high liquidity. Luxury demand also concentrates here: The Pearl Island logged 20 million vehicle entries in 2023. It now hosts the country’s fastest 180 kWh charger, cementing its role as the epicenter of premium EV adoption.

Al Rayyan, slated for a 6.60% CAGR, benefits from master-planned suburbs that combine affordable housing with new malls and schools. Families gravitate toward larger vehicles, pushing SUV turnover higher. As municipal roads connect seamlessly to Doha’s ring roads, cross-city test drives become practical, opening fresh catchment areas for dealers.

Emergent nodes such as Al Wakrah, Umm Salal, and Al Khor are from the long tail of the Qatar used car market. Population densities are lower, yet digital marketplaces neutralize distance by letting shoppers filter inventory nationwide. Regulatory consistency from centralized inspection protocols assures buyers that quality standards match Doha’s, even when the seller sits 80 km away.

Mordor Intelligence's coverage of the used car market extends across other regions including Africa, while country-specific intelligence is also available for Netherlands, Tanzania, South Africa, Portugal, Egypt, Ethiopia, Hong Kong, and Finland, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

The market structure is moderately fragmented, yet network effects are guiding consolidation. Digital leaders integrate AI-driven valuation, blockchain-secured service logs, and embedded credit scoring, helping them convert listings faster than traditional yards. Organized groups now bundle extended warranties underwritten by insurers, mitigating buyer anxiety over unforeseen repairs.

White spaces remain: dedicated electric-only remarketing, luxury consignment formats with concierge pick-up, and Sharia-first loan desks. Early movers exploiting these gaps can harvest a margin before the field crowds. Meanwhile, unorganized players pivot to niche sourcing—salvage auctions, classic imports, or low-spec commercial vans—to escape head-to-head bouts with platform giants.

Stable macro settings—anchored by the QR peg and predictable 5% import duty—encourage sustained capital investment in showrooms and reconditioning bays. Larger groups expand footprint into satellite cities, leveraging shared IT backbones to centralize inventory data while localizing customer touchpoints.

Qatar Used Car Industry Leaders

Qmotor

QatarSale

Qatar Living

Dubizzle

CarSemsar

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Qatar activated the Integrated GCC Customs Tariff with 12-digit vehicle codes, raising data accuracy and trimming border clearance times.

- November 2024: The Ministry of Commerce and Industry (MoCI) issued circular No. (4) for the year 2024 concerning car dealerships’ sale of vehicles on installments to customers.

- January 2024: United Development Company deployed seven public EV chargers, including a 180 kWh fast unit on The Pearl Island, laying the groundwork for broader EV uptake.

Qatar Used Car Market Report Scope

A used car/pre-owned vehicle, or a secondhand car, is a vehicle that previously had one or more retail owners. A certified pre-owned (CPO) vehicle, on the other hand, is a pre-owned vehicle that has been extensively inspected (pre-purchase inspection) and expertly reconditioned. The used car market consists of a wide range of companies involved in the purchasing and selling of pre-owned vehicles through online or offline sales channels.

The Qatar used car market is segmented by vehicle type, vendor type, fuel type, and sales channel. By vehicle type, the market is segmented into hatchbacks, sedans, and sports utility vehicles (SUVs)/multi-purpose vehicles (MPVs). By vendor type, the market is segmented into organized and unorganized. By fuel type, the market is segmented into petrol, diesel, electric, and other fuel types (liquefied petroleum gas, compressed natural gas, etc.). By sales channel, the market is segmented into online and offline.

The report offers market size and forecast value (USD) for all the above segments.

| Hatchbacks |

| Sedans |

| SUVs / MPVs |

| Organized (franchised dealers, OEM-backed platforms) |

| Semi-organized (inspection-certified independents) |

| Unorganized (roadside dealers, peer-to-peer) |

| Petrol |

| Diesel |

| Hybrid-electric |

| Battery-electric |

| LPG / CNG / Others |

| Online-only |

| Omni-channel (online-to-offline) |

| Offline-only |

| 0-2 years |

| 3-5 years |

| 6-8 years |

| Above 8 years |

| Below 11,000 |

| 11,000 - 20,600 |

| 20,601 - 41,000 |

| Above 41,000 |

| Doha |

| Al Rayyan |

| Al Wakrah |

| Others (Umm Salal, Al Khor, Al Shamal) |

| By Vehicle Type | Hatchbacks |

| Sedans | |

| SUVs / MPVs | |

| By Vendor Type | Organized (franchised dealers, OEM-backed platforms) |

| Semi-organized (inspection-certified independents) | |

| Unorganized (roadside dealers, peer-to-peer) | |

| By Fuel Type | Petrol |

| Diesel | |

| Hybrid-electric | |

| Battery-electric | |

| LPG / CNG / Others | |

| By Sales Channel | Online-only |

| Omni-channel (online-to-offline) | |

| Offline-only | |

| By Vehicle Age | 0-2 years |

| 3-5 years | |

| 6-8 years | |

| Above 8 years | |

| By Price Band (USD) | Below 11,000 |

| 11,000 - 20,600 | |

| 20,601 - 41,000 | |

| Above 41,000 | |

| By City | Doha |

| Al Rayyan | |

| Al Wakrah | |

| Others (Umm Salal, Al Khor, Al Shamal) |

Key Questions Answered in the Report

How big is the Qatar Used Car Market?

The Qatar Used Car Market size is expected to reach USD 668.64 million in 2026 and grow at a CAGR of 7.21% to reach USD 946.96 million by 2031.

What is the current size of the Qatar used car market?

The Qatar used car market size is USD 668.64 million in 2026 and is forecast to reach USD 946.96 million by 2031

Which vehicle type sells the most in Qatar’s used-car space?

SUVs lead with 49.08% share, and SUVs are the fastest climber at a 10.11% CAGR through 2031.

How fast are battery electric cars growing in the Qatar used car market?

Battery electric vehicles are expanding at a 14.52% CAGR, the quickest among all fuel types as charging points proliferate.

Why are organized dealers gaining ground over roadside sellers?

They pair digital listings with certified inspections, warranty bundles and instant Sharia-compliant financing, services that unorganized lots struggle to match.

How will new Chinese brands influence the used-car market?

Aggressive pricing and long warranties on new Chinese models narrow the cost gap with late-model used cars, pressuring dealer margins in entry-level segments.

Page last updated on: