MEMS Pressure Sensors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.82 Billion |

| Market Size (2031) | USD 3.74 Billion |

| Growth Rate (2026 - 2031) | 5.77% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

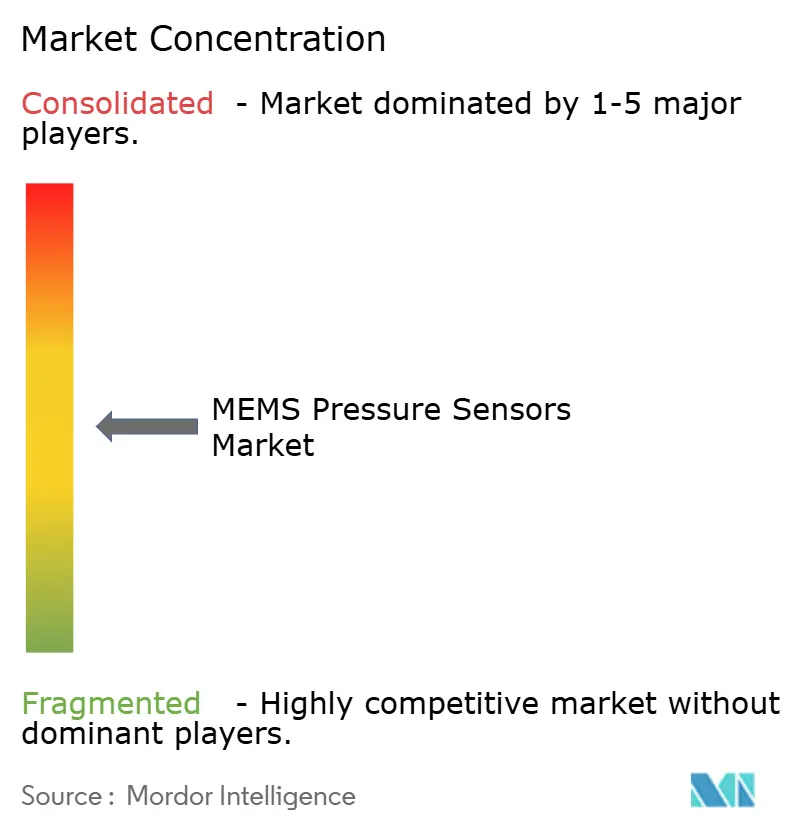

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

MEMS Pressure Sensors Market Analysis by Mordor Intelligence

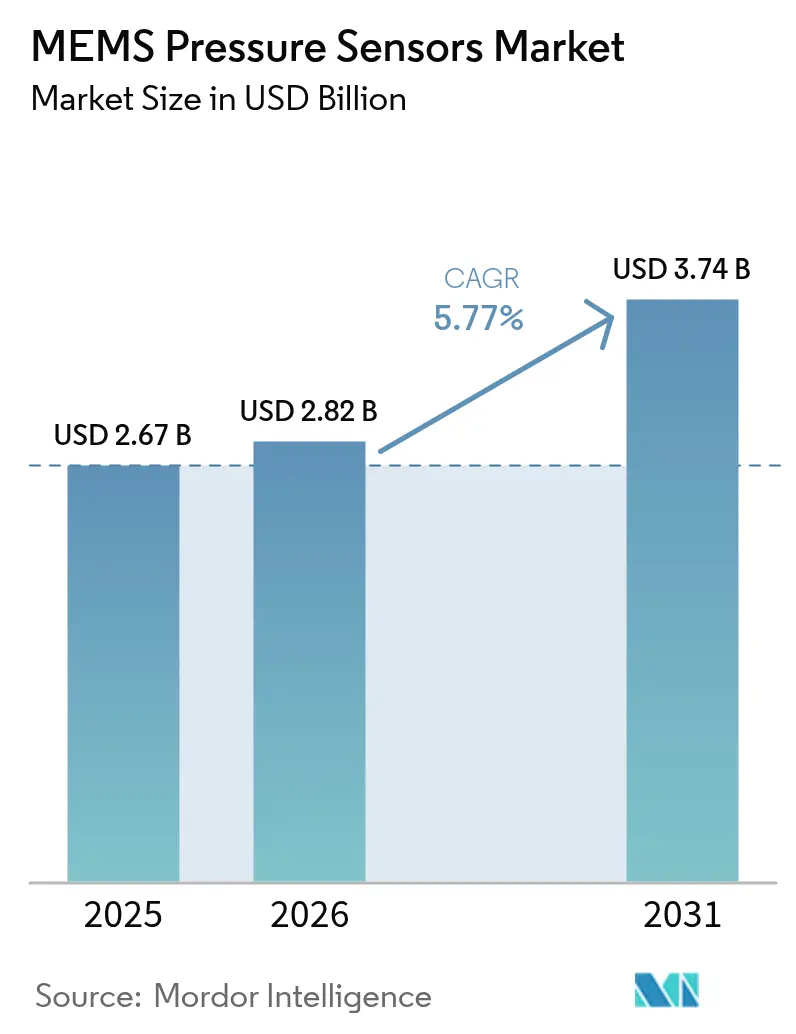

The MEMS pressure sensor market size is expected to grow from USD 2.67 billion in 2025 to USD 2.82 billion in 2026 and is forecast to reach USD 3.74 billion by 2031 at 5.77% CAGR over 2026-2031. Consistent adoption across automotive, medical, industrial, aerospace, and consumer electronics segments underpins demand, while investments in 300 mm wafer fabrication steadily lower production costs. Technical advances in parylene coatings, silicon-capacitive cell designs, and through-silicon-via architectures improve accuracy and long-term stability, sustaining replacement cycles. Regulatory programs, such as ISO 26262 for vehicle functional safety and FDA digital-health guidance, solidify design-win pipelines for suppliers who can quickly certify devices. Meanwhile, foundry-as-a-service business models help fabless start-ups prototype rapidly, broadening the supplier ecosystem and cushioning supply-chain shocks.

Key Report Takeaways

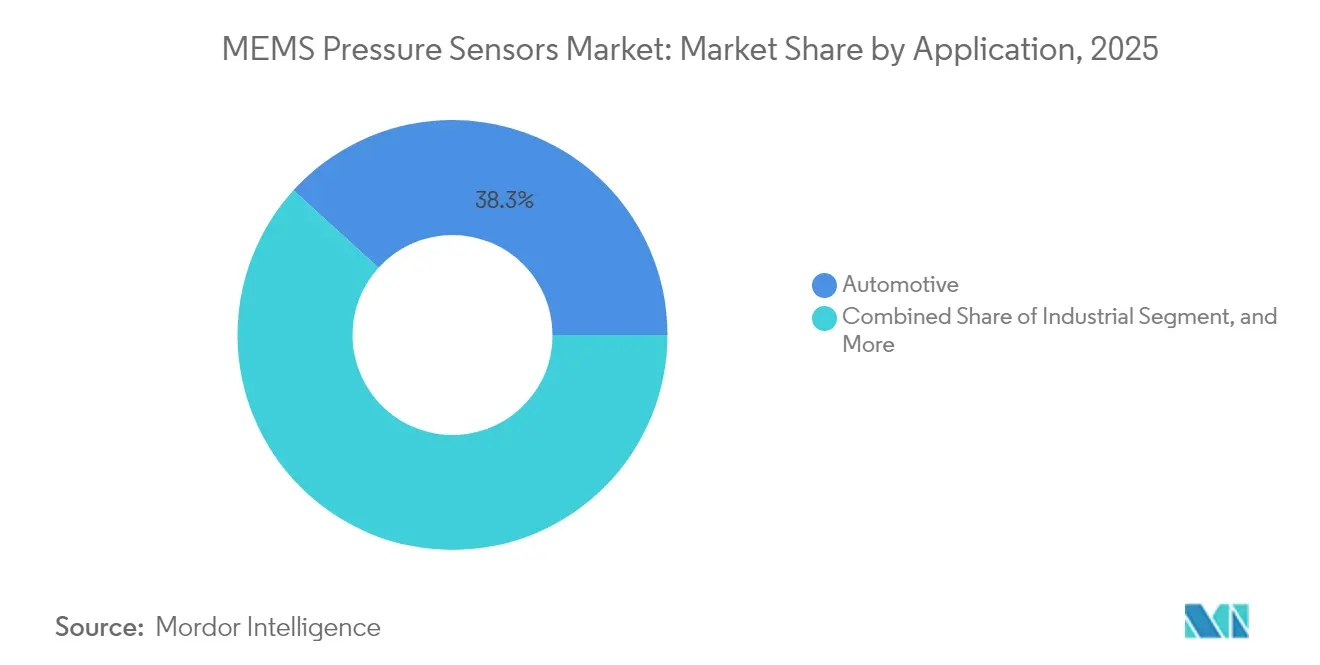

- By application, the automotive sector led with a 38.25% revenue share in 2025, while medical devices recorded the highest projected CAGR of 6.07% through 2031.

- By sensor type, silicon capacitive technology held a 52.96% market share of the MEMS pressure sensor market in 2025 and is projected to post a 7.57% CAGR through 2031.

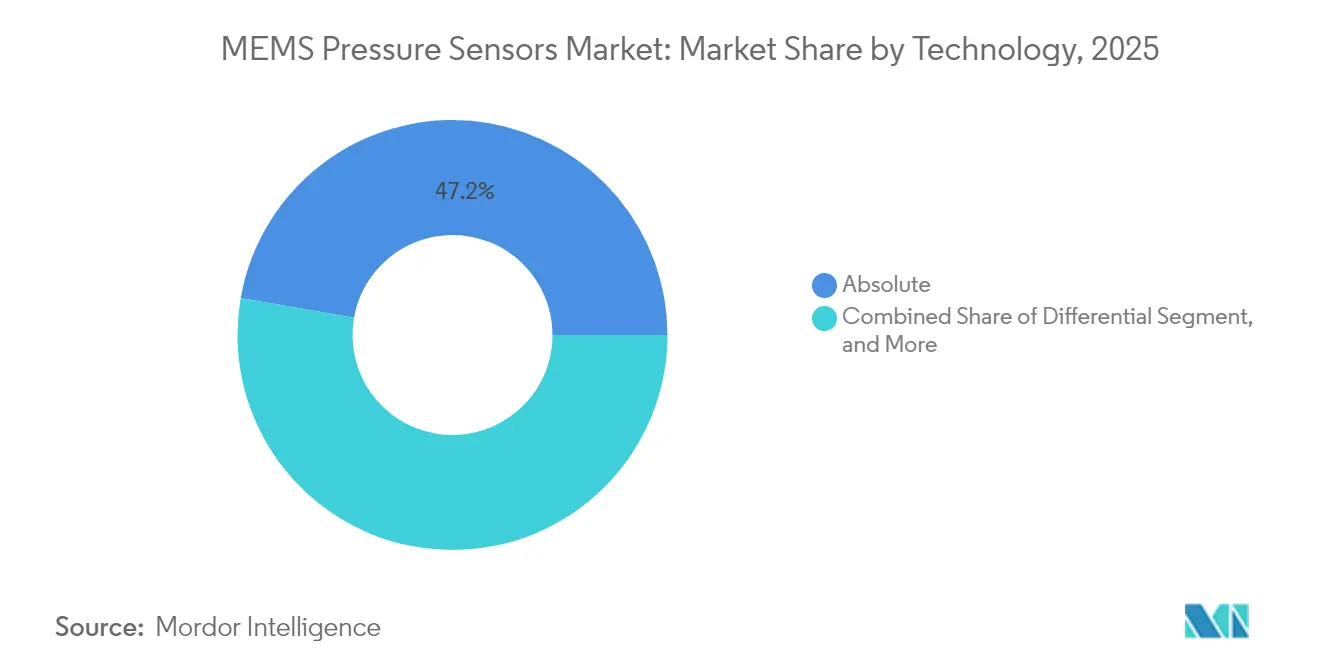

- By 2025, absolute pressure sensors captured 47.24% of the MEMS pressure sensor market size, whereas differential devices are projected to advance at a 7.18% CAGR through 2031.

- By pressure range, the 10 kPa-100 kPa band commanded 55.15% of the MEMS pressure sensor market size in 2025; sub-10 kPa devices are forecast to accelerate at a 7.34% CAGR by 2031.

- By geography, the Asia-Pacific region controlled 49.10% of the MEMS pressure sensor market in 2025 and is projected to maintain the fastest regional growth at a 6.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global MEMS Pressure Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Adoption of Advanced Driver Assistance Systems | +1.8% | North America and Europe first movers, global roll-out | Medium term (2-4 years) |

| Proliferation of IoT-Enabled Consumer Electronics | +1.5% | Asia-Pacific core, North America spill-over | Short term (≤2 years) |

| Rapid Industrial Automation and Industry 4.0 Rollout | +1.2% | Germany, China, Japan clusters | Medium term (2-4 years) |

| Rising Miniaturization in Medical Devices | +0.9% | North America and European Union, growing Asia-Pacific | Long term (≥4 years) |

| Emerging Demand for Drone-Based Atmospheric Sensing | +0.6% | North America and Europe, nascent Asia-Pacific | Long term (≥4 years) |

| MEMS Foundry-as-a-Service Accelerating Start-Up Innovation | +0.4% | Foundry hubs in Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of Advanced Driver Assistance Systems (ADAS)

MEMS pressure sensors now underpin brake-line monitoring, thermal loops in electric vehicle battery packs, and altitude-assisted navigation. Devices must withstand temperatures ranging from −40 °C to 150 °C and deliver a millisecond response, prompting automakers to specify ASIL-rated parts. Silicon-capacitive die architectures help vendors achieve <0.1% full-scale linearity and under-2 µA standby current, supporting multi-sensor arrays without draining vehicle 48 V networks.[1]“A Micro and Low-Cost Packaging Technology of High Accuracy Piezoresistive Pressure Sensors With Parylene Coating,” IEEE, ieee.org

Proliferation of IoT-Enabled Consumer Electronics

Smartphones, wearables, and smart-home gadgets embed barometric sensors measuring no larger than 2 mm² to derive floor-level positioning, indoor climate cues, and fitness metrics. Bosch Sensortec’s BMP581 consumes only 1.3 µA at 1 Hz while sustaining ±30 Pa accuracy, exemplifying the low-power benchmark consumers now expect.[2]Muhannad Ghanam et al., “MEMS Shielded Capacitive Pressure and Force Sensors With Excellent Thermal Stability,” Sensors, mdpi.com

Rapid Industrial Automation and Industry 4.0 Rollout

Factory digitization drives the integration of MEMS pressure sensors into pneumatic cylinders, robotics, and predictive-maintenance dashboards. Wireless LoRaWAN transducers extend coverage to legacy brownfield assets, allowing supervisors to flag leaks or drifts before downtime occurs. Fraunhofer research confirms that silicon-ceramic hybrids remain stable beyond 350 °C, unlocking potential for petrochemical and power-generation applications.[3]“Wafer-Level Self-Packaging Design and Fabrication of MEMS Capacitive Pressure Sensors,” Micromachines, mdpi.com

Rising Miniaturization in Medical Devices

Implantables and wearables rely on parylene-coated MEMS cells to meet the ISO 10993 biocompatibility standard. Parylene VT4 reduces urinary biofouling by 60%, making long-term bladder monitors feasible. Algorithms compensate for drift to ±1 mmHg across multi-year lifespans, supporting FDA-cleared digital biomarkers for chronic disease management.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complexity of Integrating Multiple Interface Standards | −0.8% | Fragmented European automotive supply chains | Short term (≤2 years) |

| Price Erosion Due to Intensifying Competition | −0.6% | Asia-Pacific cost leadership, global ripple | Medium term (2-4 years) |

| Supply Chain Risks in Advanced Wafer Bonding Materials | −0.4% | Semiconductor hubs worldwide | Short term (≤2 years) |

| Calibration Drift Under High Cycle Fatigue Conditions | −0.3% | High-reliability verticals worldwide | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Complexity of Integrating Multiple Interface Standards

Automakers face mixed I²C, SPI, SENT, and I³C buses within a single ECU, forcing the allocation of extra microcontroller resources and prolonging validation cycles by up to 12 months. Each protocol also demands separate cybersecurity and functional-safety documentation, straining engineering budgets and delaying platform launches.

Price Erosion Due to Intensifying Competition

Subsidized 300 mm fabs in East Asia drive wafer output higher and unit ASPs down. Large incumbents survive through volume scaling, but smaller fabless firms see their margins compress as list prices fall faster than cost reductions. Continuous innovation in process control and package miniaturization becomes essential to sustain profitability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Automotive Integration Anchors Near-Term Revenue

The MEMS pressure sensor market size for the automotive sector reached USD 1.02 billion in 2025, accounting for a 38.25% share, driven by TPMS, brake-line diagnostics, and EV thermal loops. OEMs now request sensors with self-test routines and over-the-air firmware capability, enhancing fleet maintenance analytics. The MEMS pressure sensor market share for medical devices remains smaller in 2025 but displays a 6.07% CAGR outlook, driven by continuous glucose monitors and implantable cardiovascular platforms that require sub-millimeter form factors.

Industrial automation utilizes LoRa-enabled pressure nodes to reduce maintenance costs by 30%, while aerospace programs require radiation-hardened units for launch vehicles. Consumer electronics are extending barometric sensing to augmented-reality headsets, targeting an elevation accuracy of ±0.5 m indoors.

By Type: Silicon Capacitive Cells Ascend

Silicon-capacitive elements accounted for 52.96% of 2025 revenue, with the MEMS pressure sensor market size for this type projected to expand at a 7.57% annual rate. Their superior linearity and drift of -40 °C to 125 °C, below 0.05%/°C, suit safety-critical ADAS and medical tools. Piezoresistive dies remain preferred for legacy analog ECUs due to their simple signal chains, but temperature-induced leakage limits their use in extreme environments.

The adoption of through-silicon-via interposers enables the 3D stacking of ASICs under the diaphragm, thereby shrinking the Z-height and boosting EMI immunity. Silicon-carbide piezoresistive prototypes now withstand temperatures exceeding 300 °C, paving the way for future deployment in gas turbines and down-hole drilling.

By Technology: Absolute Sensing Retains Leadership

Absolute devices accounted for 47.24% of the total value in 2025. Smartphones, altimeters, and vacuum systems benefit from sealed reference cavities that decouple readings from ambient air. Differential sensors rise fastest at 7.18% CAGR on HVAC, ventilator, and flow-meter demand. Gauge models cover brake-fluid monitors where atmospheric compensation suffices.

Wafer-level hermetic sealing tightens reference drift to <20 ppm/°C, extending calibration intervals and lowering the total cost of ownership for fleet operators. Software-defined sensors capable of toggling between absolute and gauge modes attract integrators seeking design reuse across platforms.

By Pressure Range: Mid-Band Dominates Volume, Low-End Leads Growth

The 10 kPa-100 kPa category accounted for 55.15% of the overall 2025 shipments, aligning with the barometric and TPMS sweet spots. Below-10 kPa sensors, although comprising just 13.00% of 2025 units, exhibit a 7.34% CAGR as semiconductor fabs and medical suction equipment demand high-vacuum accuracy. Above-100 kPa models serve hydraulics and aerospace bleed-air loops, commanding premium ASPs yet lower volume.

DRIE and silicon-on-insulator processes now enable the tailoring of diaphragm thickness down to 200 nm, yielding high-resolution sub-kPa sensors for drone meteorology that resolve 4 cm altitude steps.

Geography Analysis

Asia-Pacific commanded 49.10% of 2025 revenue and is on course to clock 6.56% CAGR through 2031. Strong smartphone assembly, expanding EV production, and government semiconductor incentives sustain momentum. China’s localization drive channels capital into domestic fabs, while Japan and South Korea refine front-end process know-how for advanced packaging.

North America ranks second; defense, aerospace, and medical regulations favor high-margin sensor designs. U.S. CHIPS Act grants underwrite new 300 mm MEMS lines, de-risking supply for critical sectors. Europe remains steady, thanks to Germany’s automotive core and stringent environmental regulations that drive sensor upgrades in industrial machinery. The Middle East and Africa register early traction in oil-rig and desalination plants that require harsh-environment sensors, whereas South America’s growth is tied to vehicle output in Brazil and Argentina. Region-specific safety and data-privacy mandates occasionally complicate the reuse of cross-border design, nudging vendors to localize their firmware stacks.

Regulatory Landscape

MEMS pressure sensors used in automotive and other safety-critical systems are shaped by functional-safety and reliability qualification regimes. ISO 26262 supports ASIL-oriented development and documentation in vehicle platforms, while the Automotive Electronics Council qualification framework (AEC-Q103-002 used alongside AEC-Q100 for active circuitry) is widely applied to MEMS pressure devices, adding time and cost to supplier onboarding and reinforcing barriers for new entrants.

Standards activity continues to broaden coverage across applications and regions. In China, GB/T 44531-2024 establishes classification, technical requirements, and test methods for automotive-grade MEMS pressure sensors, requiring global suppliers to manage dual-compliance strategies for multinational OEM programs. At the international level, IEC expanded guidance with IEC 60730-2-6:2025 for automatic electrical pressure sensing controls and IEC 62047-4:2026 for generic MEMS semiconductor device specifications, supporting more standardized qualification and test practices across consumer, industrial, and automotive use cases. In the United States, NHTSA safety rules under FMVSS No. 138 for TPMS continue to anchor baseline demand and compliance needs for tire-pressure-related sensing content in light vehicles.

Value Chain Analysis

The MEMS pressure sensor value chain spans silicon starting materials and specialty inputs (including wafer bonding consumables and coating chemistries such as parylene), front-end MEMS fabrication, ASIC integration, advanced packaging, calibration and test, and then module assembly and distribution into automotive, industrial, medical, aerospace, and consumer-electronics OEM channels. A structural pinch point remains packaging and test: wafer-level and zero-level packaging, hermetic sealing, and high-throughput calibration are cost intensive and yield sensitive, making OSAT and packaging know-how a key determinant of gross margin and delivery lead times.

Manufacturing and assembly footprints are globally distributed, with East Asia central to foundry, OSAT, and downstream module assembly, while higher-precision and regulated end-use requirements support specialized supply bases in regions known for medical-grade and ultra-high-accuracy sensor production. Competitive dynamics increasingly favor integrated players and tightly managed partner ecosystems that can deliver MEMS die, ASICs, and software-ready calibration as a single system, while foundry-as-a-service models broaden access for fabless challengers. Portfolio and capacity consolidation also reshapes chain control, illustrated by STMicroelectronics completing its USD 950 million acquisition of NXP Semiconductors' MEMS sensor business in January 2025, strengthening internal access to designs, process know-how, and customer programs that influence sourcing decisions across downstream tiers.

Competitive Landscape

The MEMS pressure sensor market features moderate concentration. Bosch Sensortec, STMicroelectronics, and TDK-InvenSense integrate design, front-end, packaging, and software, enabling cost synergies. STMicroelectronics bolstered its portfolio through a USD 950 million acquisition of NXP's MEMS business, securing sockets for the automotive and industrial sectors. Foundry-as-a-service leaders such as Silex Microsystems open 300 mm lines to fabless challengers, diversifying supply yet heightening price competition.

Strategic R&D themes include ultra-low-power ASICs, parylene-encapsulated diaphragms for aqueous media, and bundled machine-learning libraries that convert pressure waveforms into actionable diagnostics. Intellectual-property depth around wafer bonding and hermetic sealing remains a decisive barrier for new entrants.

Niche disruptors explore silicon-carbide die for 500 °C environments, while academic consortia investigate graphene diaphragms for sub-100 Pa resolution. Price erosion persists in commodity barometric parts, but aerospace and medical verticals sustain premium pricing through performance and certification hurdles.

MEMS Pressure Sensors Industry Leaders

-

Robert Bosch GmbH (Bosch Sensortec)

-

STMicroelectronics N.V.

-

Murata Manufacturing Co., Ltd.

-

Infineon Technologies AG

-

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regionalization of MEMS manufacturing capacity and conversion of legacy fabs into MEMS-capable lines is opening procurement whitespace for automotive, industrial, aerospace, and medical customers seeking shorter, more resilient supply chains. In July 2026, Silex Microsystems signed a definitive agreement to acquire an 8-inch fab in Mountain Top, Pennsylvania from onsemi for USD 40 million, with a stated total conversion capex estimate of about SEK 1.6 billion, signaling new US-based MEMS manufacturing options for pressure-sensor programs. In parallel, Rogue Valley Microdevices reported expanded capability in 2026 at Palm Bay, Florida, positioning itself as a US pure-play MEMS foundry with both 200 mm and 300 mm wafer manufacturing, supporting prototyping-to-volume pathways for pressure-sensor designers that previously relied more heavily on offshore capacity.

Another opportunity area centers on higher-value industrial and medical pressure sensing, where customers pay for stability, packaging robustness, and integrated processing rather than commodity die. In June 2026, Teledyne MEMS announced a USD 20 million expansion of its Edmonton facility to add wafer processing equipment and automation aimed at industrial and medical MEMS production, reflecting active investment in these higher-spec segments. On the product side, suppliers are pushing intelligence closer to the sensing element for factory and building automation. In 2026, STMicroelectronics highlighted industrial pressure sensors such as ILPS22QS and ILPS28QSW featuring embedded processing (including ISPU positioning) for condition monitoring and predictive maintenance, creating room for differentiated designs that reduce external MCU load and simplify subsystem certification and integration.

Recent Industry Developments

- July 2026: Silex Microsystems signed a definitive agreement to acquire an 8-inch semiconductor fab in Mountain Top, Pennsylvania from onsemi for USD 40 million to establish US MEMS manufacturing capacity. The move broadens regional sourcing options for MEMS pressure sensor supply chains and underlines the scale of investment required for fab conversion, with total capex for the transition referenced at around SEK 1.6 billion.

- September 2025: Silex Microsystems completed phase-one construction of its 300 mm MEMS fabrication expansion in Jarfaella, Sweden, as part of a USD 200 million investment program. Added 300 mm capacity supports higher output and lower per-unit costs for pressure sensor customers while reinforcing Europe as a meaningful node for advanced MEMS foundry services.

- January 2025: STMicroelectronics completed its USD 950 million acquisition of NXP Semiconductors' MEMS sensor business. Bringing additional MEMS sensor assets and customer relationships in-house strengthened STMicroelectronics' position across automotive and industrial sensing programs, including pressure-sensor-adjacent platforms that share process and packaging roadmaps.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market is defined as the revenue generated from MEMS-based pressure sensors that measure pressure in devices and equipment, and it is tracked in USD across end-use adoption and shipment demand across major regions.

Scope exclusions: The sizing excludes non-MEMS pressure sensors, and it also avoids counting downstream integration value such as control units, housings, and full modules beyond the sensor itself.

Segmentation Overview

-

By Application

- Medical

- Automotive

- Industrial

- Aerospace and Defense

- Consumer Electronics

-

By Type

- Silicon Piezoresistive

- Silicon Capacitive

-

By Technology

- Gauge

- Absolute

- Differential

-

By Pressure Range

- Below 10 kPa

- 10 kPa – 100 kPa

- Above 100 kPa

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Russia

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

-

Middle East and Africa

-

Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

-

Africa

- South Africa

- Egypt

- Rest of Africa

-

Middle East

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to build the starting structure of the model and to anchor assumptions that can be checked consistently year over year. We typically refer to public sources such as U.S. Census Bureau and USITC trade data, UN Comtrade, OECD industrial statistics, and macro series from the World Bank, which help explain how electronics output and cross-border flows are moving.

To keep the MEMS lens realistic, we also read electronics and semiconductor disclosures such as annual reports, investor presentations, and technical notes, and we scan standards and policy sources such as ISO documentation and FDA public guidance when it affects design and qualification timelines. Where needed, paid subscriptions for company financials and intelligence, patent databases, and shipment-level import and export records are used to cross-check revenue ranges, technology focus areas, and supply chain signals. The sources listed here are not exhaustive, and many other public references were reviewed for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to validate what the desk research cannot show clearly, especially pricing movement, mix shifts by application, and the timing of design wins converting into volume. We spoke with a spread of sensor ecosystem participants such as component makers, packaging partners, distributors, and engineering or procurement teams at end users, and inputs were balanced across APAC, EMEA, and the Americas to avoid a single-region view.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 13% | APAC: 47% |

| Mid tier: 48% | Functional/Unit leaders: 39% | EMEA: 34% |

| Smaller Players: 14% | Managers: 48% | Americas: 19% |

Market-Sizing & Forecasting

For sizing, the main build uses a top-down approach where electronics production, end-market unit volumes, and adoption rates are translated into a demand pool for MEMS pressure sensing, and then converted into value using blended pricing. Once that structure is in place, the totals are checked using selective bottom-up approximations such as sampled ASP times estimated shipment volumes for key use cases, plus a light supplier and channel roll-up to see if any region looks out of line.

A few practical inputs that matter in this market include vehicle production and key pressure-sensing fitment points, medical device shipment trends for monitoring and disposable use cases, industrial automation activity that pulls demand for stable sensing, consumer device unit cycles, and the mix between gauge, absolute, and differential sensors as it affects pricing. Packaging and qualification timelines are also monitored because they change when revenue shows up, not only whether a design exists.

Forecasting is run using multivariate regression, where the forward curve is tied to drivers like end-market unit outlooks, regional manufacturing trends, and expected ASP progression from interview consensus. When a bottom-up checkpoint is missing for a smaller geography or niche application, the gap is handled using proxy penetration rates and pricing bands taken from adjacent regions, then reviewed again during validation.

Data Validation & Update Cycle

Outputs are validated through a set of checks that compare the modeled value against independent signals such as end-market unit trends, trade flow direction, and reported capacity or investment cues from the supply chain. If a region or application moves too fast versus its drivers, the assumptions are revisited, and follow-up calls are triggered to re-check the adoption and pricing logic.

Before sign-off, the model goes through multi-step internal review where calculation logic, currency conversions, and year alignment are re-checked, followed by a final variance scan against prior refresh values. The report is refreshed annually, and interim updates are made when material events occur such as large end-market demand changes or meaningful shifts in manufacturing footprint. Right before delivery, a fresh review pass is completed so clients receive the latest updated view.

Mordor Intelligence's Mems Pressure Sensors Market Estimate Compared With Other Published Estimates

Published market sizes for MEMS pressure sensors can look different even when they appear to talk about the same product, because the scope lines and the time markers are not always matched. Differences also show up when firms rely on different demand signals, apply different price curves, or convert currencies using different timing.

The key gap drivers in this market are usually whether the estimate counts only discrete MEMS pressure sensors or also bundles modules and adjacent pressure technologies, how gauge versus absolute versus differential mix is treated, and whether automotive and consumer volumes are modeled with conservative or aggressive unit assumptions. On top of that, some figures are anchored to 2025, while others are stated for 2026, which can create a visible spread even before methodology differences are considered.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.82 B (2026) | |

| Industry Research Publisher A | USD 2.70 B (2025) | Uses a 2025 anchor year and a broader regional split approach, which can differ from a 2026-based view when unit demand and pricing shift year to year. |

| Industry Research Publisher B | USD 2.66 B (2025) | Anchors sizing to a 2024 base year with a 2025 estimate and may apply different gauge, absolute, and differential mix assumptions, which changes blended ASP and total value. |

The table shows a tight range centered around the mid-USD 2 B level, and the visible gap is largely year alignment rather than a single dramatic assumption. In Mordor Intelligence's model, discrete MEMS pressure sensor revenue is kept separate from downstream module value, and the 2026 size is tied back to adoption and pricing checks across the main application areas, which helps keep the estimate repeatable when the inputs are refreshed.

Key Questions Answered in the Report

How large is the MEMS pressure sensor market in 2026?

The MEMS pressure sensor market size reached USD 2.82 billion in 2026, reflecting broad uptake across vehicles, medical devices and IoT gadgets.

What is the growth outlook for MEMS pressure sensors to 2031?

Revenue is projected to rise to USD 3.74 billion by 2031, translating into a 5.77% CAGR as automotive electrification and medical wearables expand.

Which application area shows the fastest momentum?

Medical devices post the highest forecast CAGR at 6.07% thanks to continuous glucose monitors, implantables and digital therapeutics.

Why are silicon-capacitive sensors gaining share?

Capacitive designs offer better than 0.1% full-scale linearity and lower temperature drift, supporting stringent ADAS and implantable use-cases.

Which region leads global shipments?

Asia-Pacific accounts for 49.10% of 2025 revenue, supported by consumer electronics assembly hubs and expanding vehicle production.

How intense is price pressure in commodity segments?

Price erosion persists as East Asian 300 mm fabs scale output, compelling established players to differentiate through performance and software features.

Page last updated on: