Qatar Taxi Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

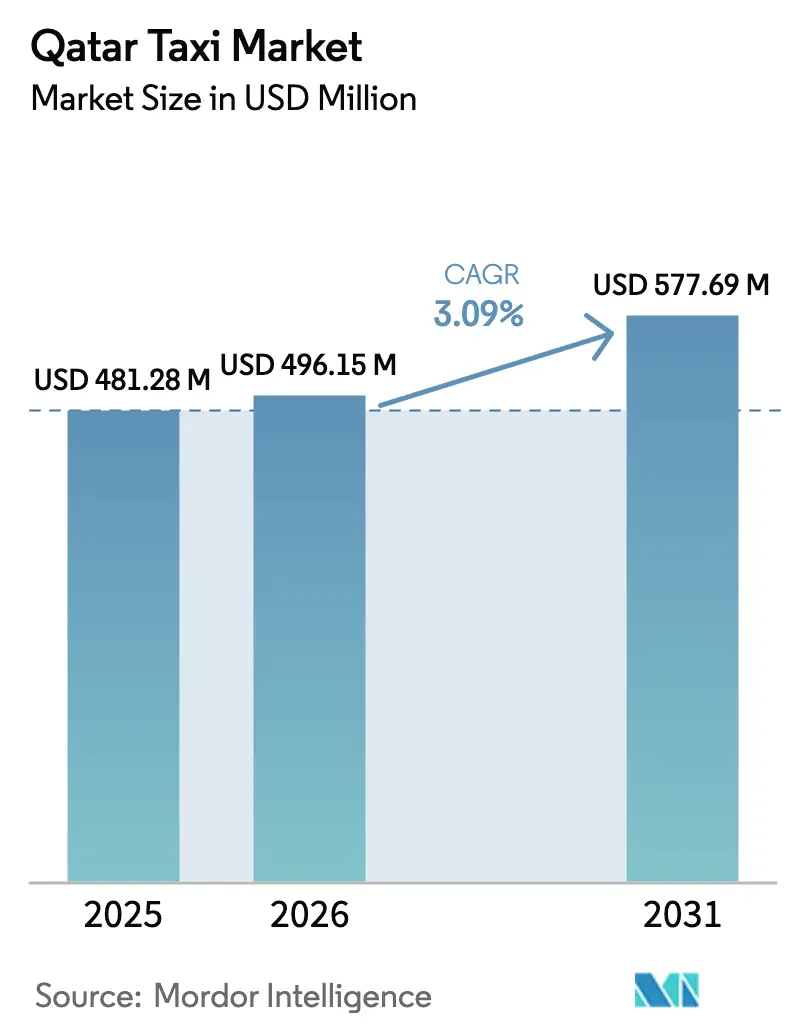

| Base Year Market Size (2025) | USD 481.28 Million |

| Market Size (2026) | USD 496.15 Million |

| Market Size (2031) | USD 577.69 Million |

| Growth Rate (2026 - 2031) | 3.09% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Taxi Market Analysis by Mordor Intelligence

The Qatar Taxi Market size is expected to increase from USD 481.28 million in 2025 to USD 496.15 million in 2026 and reach USD 577.69 million by 2031, growing at a CAGR of 3.09% over 2026-2031. Steady value growth conceals a structural pivot toward hybrid-electric fleets, autonomous robotaxis, and app-based dispatch, reshaping demand patterns, operating cost structures, and competitive dynamics in the Qatar taxi market. Mowasalat (Karwa) leads the transition, having converted 90% of its taxis to hybrid drivetrains and rolled out the country’s first level-4 autonomous service in December 2025, a dual move that offsets fuel-price volatility and responds to global utilization gaps between regulated taxis and ride-hailing vehicles.

Key Report Takeaways

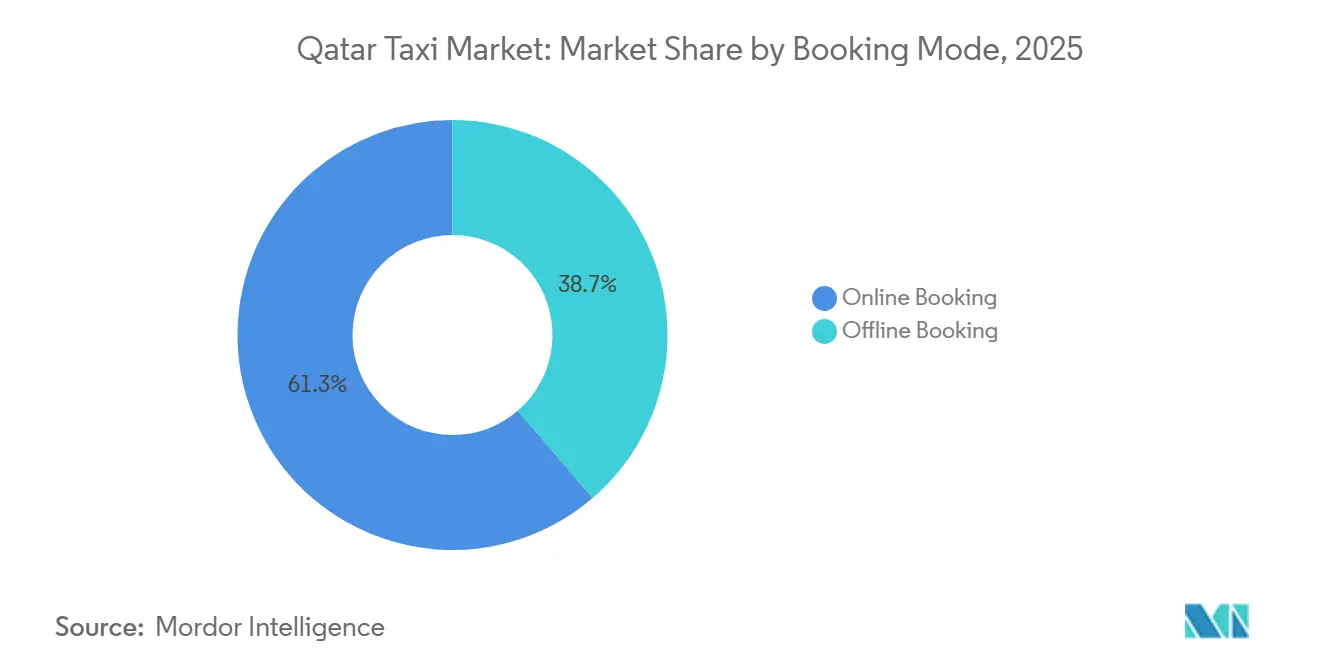

- By booking mode, online channels commanded 61.27% of the Qatar taxi market share in 2025, while offline channels are forecast to expand at only a 2.5% CAGR through 2031.

- By vehicle type, passenger cars accounted for 83.35% of revenue share in 2025 and are advancing at a 3.26% CAGR through 2031.

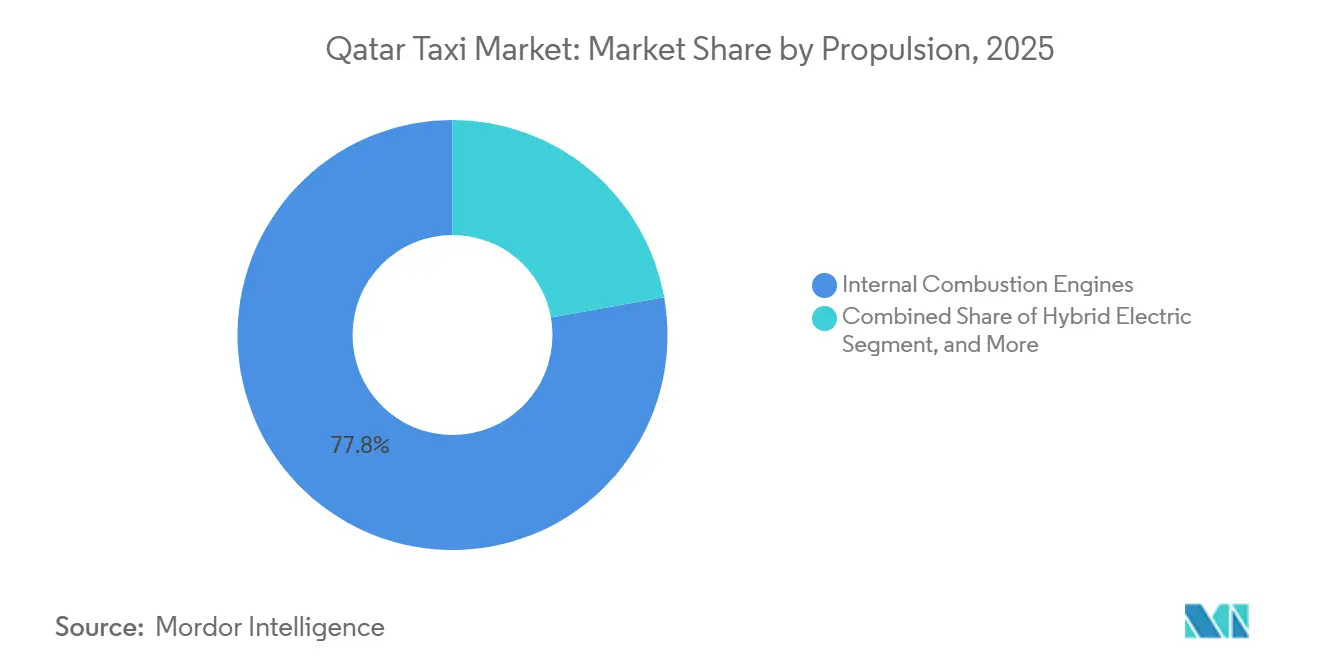

- By propulsion, ICE vehicles held 77.81% of the Qatar taxi market size in 2025, while BEVs are set to accelerate at a 3.15% CAGR over the same period.

- By passenger segment, airport-tourist rides led with 43.37% of Qatar taxi market share in 2025, and the same segment is projected to grow at a 3.21% CAGR to 2031.

- By geography, Doha accounted for 78.13% of the total value in 2025; Al Wakrah is the fastest-growing area, expected to post a 3.18% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Qatar Taxi Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tourism Rebound Under Vision 2030 | +0.7% | National, peak impact in Doha, West Bay, The Pearl, Al Wakrah | Long term (≥ 4 years) |

| Government-Backed Fleet Electrification Mandate | +0.6% | National, concentrated in Doha and Al Rayyan | Medium term (2-4 years) |

| Surge-Pricing Liberalisation | +0.5% | National, strongest in Doha and tourist zones | Short term (≤ 2 years) |

| Rapid Airport-Taxi Integration Via "Smart Taxi Rank" | +0.4% | Hamad International Airport, spillover to Doha metro hubs | Short term (≤ 2 years) |

| Qatar Rail First/Last-Mile Partnerships | +0.3% | Doha Metro corridors, Lusail, Education City | Medium term (2-4 years) |

| Pink-Taxi Licences For Female Riders | +0.1% | National, early gains in Doha and Al Rayyan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tourism Rebound Under Vision 2030

Visitors rebounded year-on-year in 2025, reviving high-margin airport, sightseeing, and leisure segments of the Qatar taxi market. Vision 2030’s goal of 6 million annual arrivals implies only modest growth in headcount. Still, taxi utilization scales faster because tourists make multiple same-day trips and are less price-sensitive than residents. Source markets led by Saudi Arabia, India, the UK, Germany, and the USA sustain a steady rider mix. At the same time, government investment in multilingual apps and contactless payments eases onboarding for first-time visitors.

Government-Backed Fleet Electrification Mandate

Karwa’s hybrid penetration reached 90%, enabling immediate fuel-cost savings and emissions cuts while sidestepping the charging-infrastructure gap that still limits BEV uptake [1]“Annual Report 2025,” Mowasalat, Karwa.qa . The Ministry of Transport intends to electrify 100% of public buses by 2030, creating shared supply chains that depress battery pack prices for taxi procurement. Commercial BEV total cost of ownership has reached parity with ICE at 0.8%, though summer heat reduces range by 23%, forcing fleets to either oversize batteries or rotate vehicles more frequently [2]“Gulf e-Mobility Outlook 2025,” PwC Middle East, pwc.com . A forthcoming insurance-inspection framework for EVs should lower underwriting risk premiums, encouraging smaller operators to follow Karwa’s lead.

Surge-Pricing Liberalization

Ministerial Decision 13 of 2024 licensed seven ride-hailing apps but stopped short of approving explicit surge multipliers, so platforms now adjust “service fees” on top of regulated base fares, achieving dynamic pricing via a loophole [3]“Land Transport Statistics 2026,” Ministry of Transport, mot.gov.qa . Karwa’s integration with Uber grants it identical flexibility, combining fixed-fare street hails with algorithmic app bookings. Enforcement sweeps in Q1 2025 penalized operators that attempted to impose off-meter surcharges, indicating that surge functionality will remain platform-mediated for the foreseeable future.

Rapid Airport-Taxi Integration Via “Smart Taxi Rank”

Exclusive curb-side rights and a QR 25 surcharge give Karwa privileged access to the 56% of visitors who enter Qatar through Hamad International Airport, a position soon to be enhanced by the TASMU smart-rank project that layers real-time tracking and multilingual fare displays on existing queues. Ride-hailing cars wait in external lots, adding 5-10 minutes and negating surge-pricing convenience, while Karwa’s May 2024 deal to appear in the Uber app merges fixed-metered tariffs with platform discovery, thus importing demand without surrendering price autonomy.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-Intensive EV Conversion Cost | -0.4% | National, concentrated among private operators | Medium term (2-4 years) |

| Driver-Quota Tightening | -0.3% | National, acute in Doha and Al Rayyan | Short term (≤ 2 years) |

| Higher Vehicle-Insurance Premiums | -0.2% | National, proportional to fleet age and vehicle value | Medium term (2-4 years) |

| Planned Congestion Surcharge | -0.2% | Doha central business district, West Bay, The Pearl | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive EV Conversion Cost

Private operators lack Karwa’s fleet-scale discounts and face higher TCO on retail BEV purchases. Qatar’s network has only 200 public fast chargers against a 2035 requirement of 4,800, compelling depot investments that stretch balance sheets.

Driver-Quota Tightening

Labor Law 12 embeds Qatarization thresholds that shrink the expatriate driver pool, and lift wage floors as employers scramble for compliant staff. Karwa’s state-owned status exempts it, widening a cost gulf with private franchisees. Enforcement crackdowns since Q1 2025 raise penalties for expired permits, intensifying supply pressure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Booking Mode: Online Dominance With Offline Resilience

Online services accounted for 61.27% of the Qatar taxi market in 2025, expanding at a 3.11% CAGR to 2031 on the back of app ubiquity, integrated digital wallets, and the Karwa-Uber tie-up. That partnership rebrands regulated taxis inside a global platform, effectively folding traditional supply into the on-demand economy while preserving airport exclusivity. Offline bookings still account for 38.73% among cash-oriented users, and in Doha’s dense districts, where customers value meter-regulated certainty. The Qatar taxi market size for offline channels remains material, despite slower growth, because airport street hails and corporate call-center orders ensure daily baseline utilization.

ITS dispatch upgrades are underway: a February 2026 TASMU accelerator cohort is co-piloting AI demand forecasting and dynamic routing within Karwa, expected to redirect slack capacity from low-yield hails toward higher-margin pre-booked trips once live. Yet regulatory sweeps continue to shield compliant operators; Ministerial Decision 13 obliges all platforms to hold twin licenses from Commerce & Industry and Transport ministries, creating administrative hurdles for any entrant seeking quick scale.

By Vehicle Type: Passenger Cars Anchor Growth, Vans Fill Gaps

Passenger cars accounted for 83.35% of revenue in 2025, growing at a 3.26% CAGR, driven by high trip frequency and superior fleet utilization. They form the backbone of the Qatar taxi market; their lighter curb weight translates into lower fuel spend and better alignment with Karwa’s hybrid strategy. Vans serve families, corporate shuttles, and wheelchair-accessible needs, averaging longer idle times and higher fuel burn. Insurance rates scale with vehicle value, so vans charge premiums to maintain margins. Accessibility directives unveiled at ICAO FALC 2025 require lift-equipped vans, pushing CAPEX higher for small fleets but creating a moat for operators able to comply.

Autonomous pilots focus on sedan platforms, underscoring capital concentration in the passenger-car pool. As battery prices decline through the domestic bus-assembly venture launched in December 2024, sedan BEV economics will become more favorable first, reinforcing segment leadership. Vans’ role should advance slightly in Al Wakrah, where family-oriented suburban growth lifts group-travel frequency.

By Propulsion: ICE Still Dominant, Hybrids Bridge to Full Electric

ICE units accounted for 77.81% of vehicles in 2025, yet their share erodes with each replacement cycle. Hybrids, already 90% inside Karwa’s fleet, quietly dominate incremental additions even though not separately reported in official share tallies. BEVs grow at a 3.15% CAGR but from a small base, constrained by infrastructure and thermal degradation.

The Qatar taxi market's hybrid share grows faster in absolute terms than BEV share through 2031, providing operators with an emissions-reduction pathway without range anxiety. The Ministry’s forthcoming EV inspection regime, expected in 2027, should compress insurance premiums and unlock bank financing, accelerating BEV purchases among private license holders.

By Passenger Segment: Airport-Tourist Remains Profit Engine

Airport-tourist rides captured a 43.37% share in 2025 and are projected to grow at a 3.21% CAGR, buoyed by high hotel occupancy and Vision 2030 visitor targets. The QR 25 airport flag-fall, combined with Karwa’s exclusivity, guarantees superior margins and shields this segment from ride-hail discounting.

Corporate travel, which accounts for nearly one-third of value, enjoys stable contractual volumes tied to the hydrocarbon and financial services clusters in West Bay and The Pearl, and benefits from limousine upsell opportunities. Residential commuting lags growth, cannibalized by Doha Metro’s three-line grid and subsidized Metrolink feeders. Nonetheless, commuter fares underpin weekday base load, enabling fleets to amortize fixed costs before peak tourist surges.

Geography Analysis

Doha contributed 78.13% of the 2025 turnover, owing to its concentration of employment, retail, and the nation’s only international airport. Karwa’s airport monopoly and the densest metro of hotels, malls, and event venues cement the capital’s lead in the Qatar taxi market. The Ministry’s January 2025 smart-parking initiative in West Bay and the Corniche cuts curb-search time, raising driver productivity. Yet operating costs are climbing: lane restrictions introduced in May 2024 prohibit taxis from using left lanes on multilane arterials, adding minutes to each trip, while stepped-up traffic-violation exit bans amplify compliance pressure.

Lusail’s mixed-use megaprojects, the Lusail Tram, and post-Cup stadium conversions drive corporate shuttle demand and special-event traffic. Qatar Rail’s integration APIs, mandated for all licensed platforms by 2027, will force fleets to synchronize real-time positions with tram and metro schedules, leveling digital capabilities across operators.

Al Wakrah and peripheral towns are clustered around a 3.18% CAGR. Coastal housing corridors and industrial free zones stimulate taxi journeys in areas with limited public transport links. The 125-project, QAR 1.2 billion road strategy earmarks multiple arterial widenings and park-and-ride sites southward, indirectly expanding addressable demand pools for app-based fleets seeking less-congested turf. By 2029, Q-Gates tolling—if finally enacted—could rebalance volumes by penalizing CBD ingress, accelerating suburban dispersion of taxi demand. Operators preparing optimized routing algorithms may secure congestion-exempt certificates or off-peak discounts, cushioning the surcharge hit.

Competitive Landscape

Mowasalat (Karwa) functions as a vertically integrated incumbent in the Qatar taxi market, owning dispatch, maintenance, and training academies, and securing rights to Hamad International Airport. Hybrid fleet penetration, electric robotaxi pilots, and an NVIDIA-powered Raheel IoT suite executed with Ooredoo in October 2025 give Karwa a technology stack that private operators struggle to match.

Seven ride-hailing licensees—Uber, Karwa Technologies, Q Drive, Badr, Aber, Zoom Ride, and Ryde—entered under the July 2024 regime. Uber re-entered through a distribution alliance after Careem’s 2023 withdrawal, balancing global brand appeal with local compliance. Utilization stats referenced by UITP show ride-hailing vehicles worldwide producing 9.8% more trips per car than traditional taxis, pushing Qatari fleets to digitize or risk declining seat-time yields. Small-scale disruptors cluster in gender-segregated services, accessibility vans, and AI dispatch; yet capital intensity and data-localization mandates impede the entry of hyperscale newcomers.

The Ministry’s early-2025 inspection blitz eliminated many unlicensed sedans, fortifying barriers to gray-market entrants. Strategy& values robo-mobility at USD 1 billion in Qatar by 2035, luring autonomous OEMs and software vendors into TASMU free zones where data sovereignty is assured. Karwa’s December 2025 robotaxi service sets the reference blueprint—level-4 vehicles, six cameras, four radars, and four lidars—and captures first-mover economics, compelling rivals either to partner or focus on underserved suburban niches where human drivers will remain relevant beyond 2031.

Qatar Taxi Industry Leaders

Mowasalat (Karwa)

Uber Technologies Inc.

DohaCabs

AL Million Group,

Fox Transport

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Qatar introduced the Digital Identity app, which enhances biometric verification across various services. This initiative aims to streamline processes, including transitions from the airport to taxis, ensuring a seamless, efficient experience for users.

- May 2024: In a move signaling a swift shift towards electrification, the Ministry of Transport announced that 70% of public buses have transitioned to electric power. This development highlights the government's commitment to reducing carbon emissions and promoting sustainable transportation. Additionally, it sets the stage for the accelerated electrification of taxis, further advancing the country's green mobility initiatives.

Qatar Taxi Market Report Scope

The scope of the report includes Booking Mode (Online Booking and Offline Booking), Vehicle Type (Passenger Cars and Vans), Propulsion (ICE, Hybrid Electric, and BEV), Passenger Segment (Airport/Tourist and More), and Geography.

| Online Booking (Ride-Sharing/Ride-Hailing) |

| Offline Booking (Taxi) |

| Passenger Cars |

| Vans |

| Internal Combustion Engine (ICE) |

| Hybrid Electric |

| Battery Electric Vehicle (BEV) |

| Airport / Tourist |

| Corporate / Business |

| Residential Commuter |

| Doha |

| Al Rayyan |

| Al Wakrah and Others |

| By Booking Mode | Online Booking (Ride-Sharing/Ride-Hailing) |

| Offline Booking (Taxi) | |

| By Vehicle Type | Passenger Cars |

| Vans | |

| By Propulsion | Internal Combustion Engine (ICE) |

| Hybrid Electric | |

| Battery Electric Vehicle (BEV) | |

| By Passenger Segment | Airport / Tourist |

| Corporate / Business | |

| Residential Commuter | |

| By City | Doha |

| Al Rayyan | |

| Al Wakrah and Others |

Key Questions Answered in the Report

How big is the Qatar taxi market in revenue terms by 2031?

The Qatar taxi market size is projected to reach USD 577.69 million by 2031, expanding at a 3.09% CAGR from 2026.

Which booking channel is growing faster, apps or street hails?

Online app-based bookings are growing quickly at a 2.5% CAGR, already holding 61.27% share in 2025.

What propulsion technology dominates taxi fleets today?

ICE vehicles still make up 77.81% of units, and BEVs are the fastest-growing at a 3.15% CAGR.

Why does airport demand matter so much for operators?

Airport-tourist trips capture 43.37% of revenue and command a QR 25 pickup fee, making them both volume and margin leaders.

How will autonomous taxis change the competitive landscape?

Karwa’s December 2025 level-4 robotaxi launch sets a new technology bar, and Strategy& expects autonomous mobility to unlock value by 2035.

Are labor regulations affecting driver supply?

Yes, Qatarization quotas effective April 2025 tighten expatriate hiring, raising wage costs especially for private ride-hailing fleets.

Page last updated on: