Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

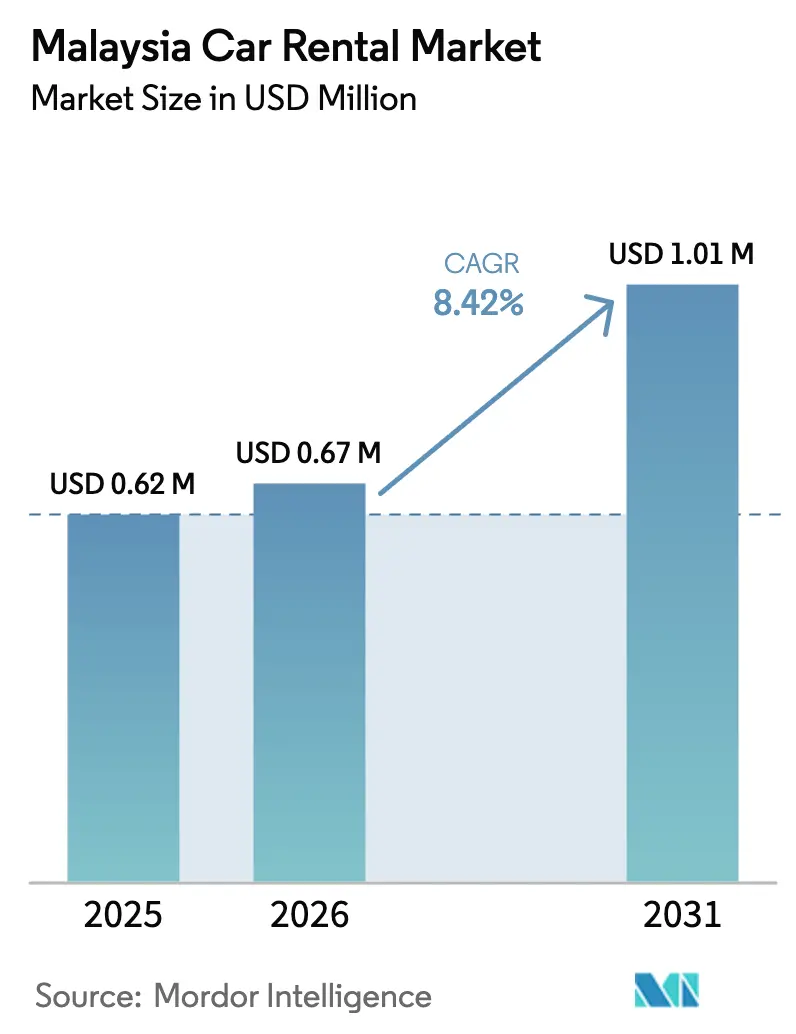

| Base Year Market Size (2025) | USD 0.62 Million |

| Market Size (2026) | USD 0.67 Million |

| Market Size (2031) | USD 1.01 Million |

| Growth Rate (2026 - 2031) | 8.42% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Malaysia Car Rental Market Analysis by Mordor Intelligence

The Malaysian car rental market size is expected to grow from USD 0.62 billion in 2025 to USD 0.67 billion in 2026 and is forecast to reach USD 1.01 billion by 2031 at 8.42% CAGR over 2026-2031. This expansion aligns with the post-pandemic rebound in international tourism, robust domestic demand, and the country’s positioning as a regional logistics and services hub. Inbound arrivals climbed to 38 million in 2024, eclipsing earlier government targets and feeding sustained demand for flexible mobility solutions. Operators are also benefiting from policy support for electric vehicles, improved digital road-tax compliance, and infrastructure upgrades across airports and highways. Competitive dynamics remain intense as global brands, local incumbents, and digital-native platforms race to deepen fleet capabilities, enhance customer experience, and hedge against volatile fuel costs.

Key Report Takeaways

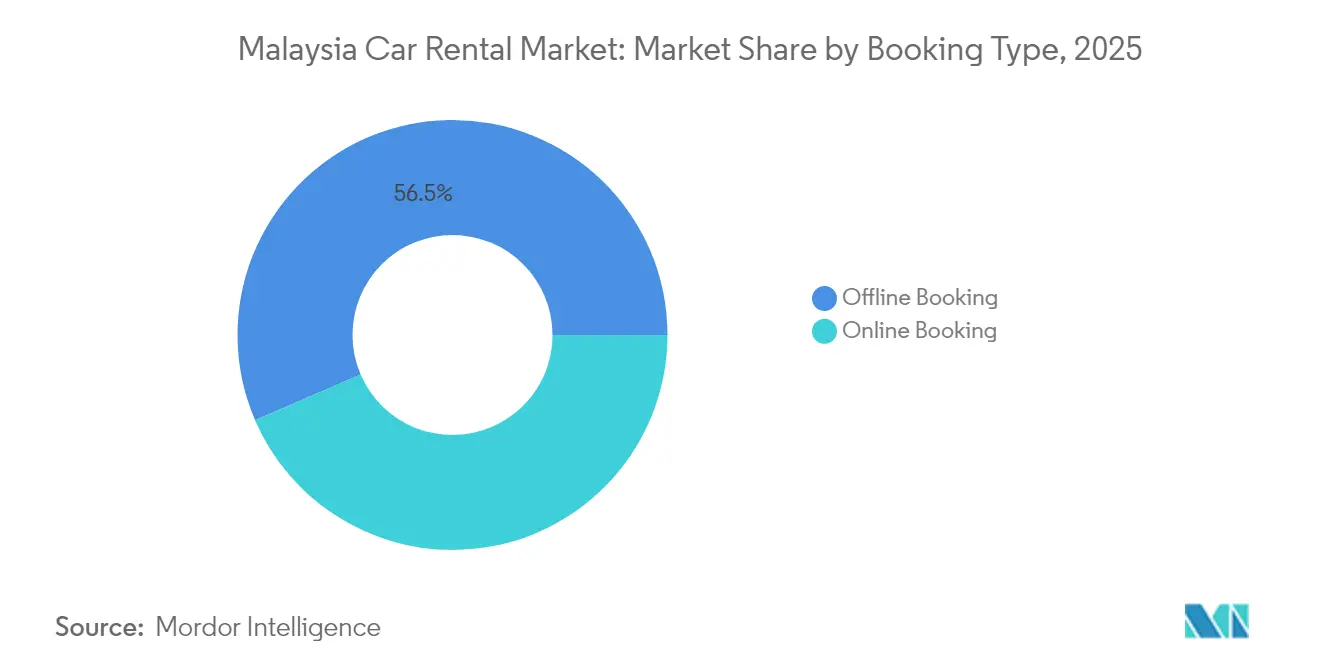

- By booking type, offline channels led with 56.48% of the Malaysian car rental market share in 2025, while the online segment is projected to post a 11.68% CAGR to 2031.

- By rental duration, short-term rentals captured a 69.62% of the Malaysian car rental market share in 2025, while long-term leasing is poised for a 9.31% CAGR through 2031.

- By vehicle type, economy/hatchbacks accounted for 42.75% of the Malaysian car rental market share in 2025; SUVs are projected to grow at an 11.12% CAGR.

- By rental channel, off-airport locations held a 63.52% of the Malaysian car rental market share in 2025, whereas on-airport outlets are set to expand at a 9.98% CAGR.

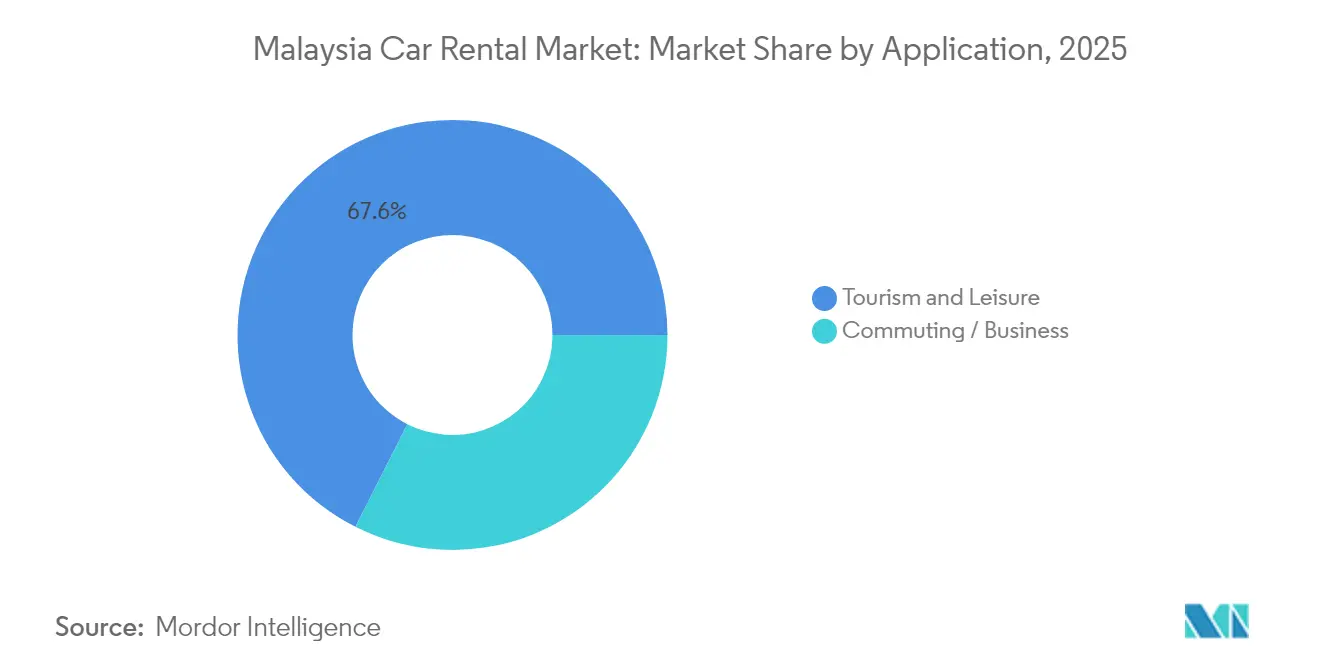

- By application, tourism and leisure represented 67.55% of the Malaysian car rental market share in 2025; business/commuting demand is advancing at an 10.78% CAGR.

- By customer type, individual users dominated with a 72.41% of the Malaysian car rental market share in 2025; corporate/fleet customers are heading for a 10.34% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Malaysia Car Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Inbound and Domestic Tourism | +2.1% | Kuala Lumpur, Penang, Langkawi | Medium term (2-4 years) |

| SUV Preference Boosts Fleet Mix | +1.8% | Nationwide urban and tourist areas | Medium term (2-4 years) |

| Shift to Online Booking Platforms | +1.3% | Major urban centers | Short term (≤ 2 years) |

| Corporate Gig-Mobility Demand | +1.1% | Kuala Lumpur and Selangor | Short term (≤ 2 years) |

| EV Incentives Catalyze Electric Fleets | +0.9% | Klang Valley, Penang, Johor Bahru | Long term (≥ 4 years) |

| Subscription Plans for Digital Nomads | +0.7% | Kuala Lumpur, Cyberjaya, Penang | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Inbound and Domestic Tourism Rebound

Malaysia welcomed 38 million visitors in 2024, a 31% jump over earlier targets and a clear signal of pent-up travel demand[1]“Tourist Arrivals & Receipts 2024,” Tourism Malaysia, tourism.gov.my. The government’s Visit Malaysia 2026 campaign now targets 35.6 million arrivals, underpinning a solid pipeline for mobility services. Passenger throughput across Malaysia Airports Holdings Berhad assets reached 77.8% of 2019 levels in 2023, with new routes from Shanghai and Phnom Penh restoring international connectivity. These trends reinforce the Malaysian car rental market as tourists extend stays into secondary cities where public transport density remains thin. Off-airport outlets that already command the majority of rental transactions stand to harvest additional volumes as travelers search for cost-efficient options outside terminals.

SUV Preference Boosting Higher-Margin Fleet Mix

SUVs' share in Malaysia’s new-car sales accounts for nearly one-third of total sales, reflecting consumer appetite for higher seating positions and multipurpose cargo space. Rental agencies benefit because SUVs yield 40 to 60% higher daily rates yet sustain strong utilization. Proton and Perodua plan several budget SUVs for 2025, including an electric crossover priced between RM50,000 and RM90,000 (USD 10,700–19,300), allowing operators to offer greener options without sacrificing the SUV flavor. Superior profit margins should keep this body style growing through 2030.

Accelerating Shift to Online-First Booking Platforms

Rapid smartphone penetration and nationwide 4G coverage have helped digital-native brands such as SOCAR and TREVO scale quickly, yet traditional agencies still secure the bulk of reservations. Offline channels illustrate how brick-and-mortar players migrate legacy clients onto proprietary apps and self-service kiosks. SOCAR’s 1,000-location network leverages real-time data streaming to right-size fleet allocation and pricing, demonstrating the operational upside of digital convergence. As Malaysia issues digital driving licenses and e-road-tax tags, identity verification and check-out times fall, widening the gap between tech-savvy operators and laggards.

Corporate Gig-Mobility Demand (Ride-Hailing Driver Leasing)

Ride-hailing incumbents such as Grab generated USD 673 million in Malaysia revenue during 2023, underscoring a vast pool of professional drivers that require leased vehicles [2]“Form 20-F 2024,” Grab Holdings, grab.com. Corporate delivery fleets and employee shuttle providers are also switching from outright purchase to usage-based contracts. Low subscription offers help to bundle maintenance, insurance, and telematics, yielding predictable cash flows for lessors.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying Ride-Hailing Competition | -1.8% | Kuala Lumpur and Penang | Medium term (2-4 years) |

| Persistent Fuel-Price Volatility | -1.4% | Nationwide, stronger on long-distance routes | Short term (≤ 2 years) |

| Rising Insurance Cost Burden | -0.9% | Nationwide | Medium term (2-4 years) |

| Urban Parking Inflates Operating Costs | -0.6% | Klang Valley, Penang, Johor Bahru | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Intensifying Competition from Ride-Hailing and E-Hailing

Grab’s ubiquity in urban corridors removes many friction points of self-drive rentals, such as parking and insurance. Price bundling with hotels and airlines lets platforms siphon spontaneous demand. Traditional agencies now focus on multi-day leisure trips, family tours, and specialty vehicles where ride-hailing is less cost-effective, yet the competitive overhang trims near-term pricing power.

Persistent Fuel-Price Volatility

Malaysia maintains a capped RON95 gasoline price at MYR 2.05 (~USD 0.48) per liter but plans to begin subsidy rationalization from mid-2025, following the June 2024 diesel subsidy rollback [3]“Fuel Subsidy Rationalisation Statement 2025,” Prime Minister’s Office of Malaysia, pmo.gov.my. Rental companies face margin pressure as pump prices float with global crude benchmarks. Operators with older fleets or long-distance itineraries feel a sharper squeeze, prompting a pivot toward hybrid and EV acquisitions.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Booking Type: Digital transformation reshapes legacy leadership

Offline channels controlled 56.48% of the Malaysian car rental market share in 2025 due to entrenched travel-agency relationships and walk-in hotel counters. Investments in mobile booking engines and contactless kiosks let these incumbents keep clients inside proprietary ecosystems while boosting upsell rates. The Malaysian car rental market size for online reservations is projected to expand at a 11.68% CAGR as operators integrate QR-code payments and real-time fleet tracking. Purely online portals face rising acquisition costs as search advertising grows crowded. Operators converge on omnichannel models, blending physical touchpoints with cloud-native inventory so customers can toggle seamlessly between app, call center, and counter.

Digital-first brands retain a data advantage because granular telematics feed dynamic-pricing engines that maximize yield per vehicle. Indoor-mapping APIs also shorten pick-up times at malls and airports, improving user satisfaction. Over the forecast horizon, online portals will deepen ties with airlines and travel-super-apps to widen funnel reach, yet mature growth curves suggest incremental share gains will be moderate. Offline operators that finish their digital overhaul could erode the perceived edge of pure-play platforms, especially among repeat domestic travelers.

By Rental Duration: Short-term strength meets long-term momentum

Short-term hires under 30 days generated 69.62% of the Malaysian car rental market share in 2025, leveraging the tourism upswing and spontaneous domestic weekend trips. Peak-season daily rates can climb 30% above shoulder months, giving agencies a revenue hedge. The Malaysian car rental market size for short-term contracts will grow in line with inbound traffic, though its CAGR trails the long-term segment. Corporations and expatriates now view leasing as an OPEX lever, pushing long-term and subscription models toward a 9.31% CAGR. These plans trim paperwork and bundle maintenance, making them attractive for HR departments managing rotating project teams.

Subscription customers show lower churn than day-to-day renters, yielding predictable fleet-utilization ratios that support financing agreements with banks. Long-term demand is also linked to the gig-mobility boom as ride-hailing drivers prefer hassle-free leases over vehicle ownership. Operators diversifying into 3-to-24-month contracts can smooth seasonality and shield against tourism shocks, anchoring a balanced portfolio across tenure buckets.

By Vehicle Type: Economy backbone with SUV margin accelerator

Economy/hatchbacks retained 42.75% of the Malaysian car rental market share in 2025, favored by budget travelers and domestic commuters seeking low fuel consumption. High resale values for Proton Saga and Perodua Axia models further protect fleet depreciation. However, the Malaysian car rental market share for SUVs is expanding rapidly as consumers opt for added comfort and cargo capacity. The SUV slice is climbing at an 11.12% CAGR due to affordable local nameplates and better highway infrastructure. Each SUV unit can yield more daily revenue, yet fill-rate discipline remains crucial because capital outlays are higher.

Sedans cater to corporate airport transfers where luggage and rear-seat space outweigh price, while MPVs serve extended families. Electric SUV launches for 2025 will let operators satisfy sustainability-minded visitors and hedge against fuel uncertainty. Agencies continuously rebalance purchase pipelines, steering 5-10 percentage points of fleet renewal toward SUV variants each year to protect margin lift.

By Rental Channel: Off-airport scale with airport speed

Off-airport counters located near city hotels, rail hubs, and residential neighborhoods delivered 63.52% of the Malaysian car rental market share in 2025. Lower concession fees and flexible lease terms at commercial buildings underpin competitive pricing pitched at domestic travelers. The Malaysian car rental market size derived from off-airport operations is expected to post steady mid-single-digit growth as local tourism and weekend getaways rise. Airport outlets are recovering quickly with a 9.98% CAGR as cross-border air seats are reinstated. Immediate access to arriving passengers lets operators command premium rates that offset higher royalty fees to airport landlords.

KLIA, Penang International, and Langkawi airports together host a significant number of rental brands, intensifying service-quality competition. Self-service lockers, digital key pick-ups, and facial-recognition check-outs are rolling out to shorten dwell time, crucial for high-value corporate travelers. A dual-channel footprint that streams vehicles between downtown and airport pools will be the optimal route to maximize utilization.

By Application: Leisure base with business expansion

Tourism and leisure still held 67.55% of the Malaysian car rental market share in 2025, anchored by sightseeing itineraries that cover Cameron Highlands, Melaka, and beach resorts. Operators calibrate pricing calendars around school vacations and religious holidays when vehicle shortages spark surge rates. Business and commuting use cases are forecast for an 10.78% CAGR as companies embrace flexible mobility allowances in place of fleet ownership. The Malaysian car rental market tied to corporate accounts is expanding faster than the leisure core.

Gig-platform drivers tap multi-month leases to eliminate upfront capital, and delivery firms like e-grocers contract van fleets during seasonal peaks. Multi-purpose solutions such as bundled fuel and toll packages add stickiness. Agencies that diversify into corporate sales pipelines reduce exposure to tourism swings and create upsell avenues for telematics and insurance add-ons.

By Customer Type: Individual dominance with corporate acceleration

Individuals constituted 72.41% of the Malaysian car rental market share in 2025, fueled by the return of international visitors and growth in domestic staycations. The Malaysian car rental market benefits from locals postponing car ownership due to rising living costs and urban congestion fees. Still, corporate clients are gaining share at a 10.34% CAGR, drawn by business-process outsourcing strategies that favor asset-light mobility contracts. Subscription bundles, telematics dashboards, and consolidated invoicing are particularly appealing to multinationals managing regional workforces.

For rental agencies, corporate accounts deliver twice the average revenue per user compared with ad-hoc leisure bookings. Negotiated volumes help secure favorable financing on fleet purchases, encouraging wider adoption of EVs where tax breaks further enhance cost competitiveness.

Geography Analysis

Klang Valley anchored a significant share of nationwide rental revenues in 2025, underpinned by KLIA’s role as the main aviation gateway and the region’s high concentration of expatriates and corporate headquarters. Penang contributed significant growth, buoyed by medical tourism and semiconductor supply-chain traffic that creates year-round bookings. Johor Bahru rental grows, as cross-border commuters from Singapore resumed daily travel after pandemic restrictions eased. The Malaysian car rental market size connected to these three corridors is forecast to expand at a high pace as highway upgrades and the Johor Bahru–Singapore Rapid Transit System elevate visitor flows.

Secondary tourism nodes such as Langkawi, Kota Kinabalu, and Kuching account for a notable share of rental services. These islands and East Malaysian cities have limited public transport coverage; hence, car hire remains the dominant mobility option for multi-stop excursions. Langkawi Airport achieved a high service-quality rating that lifts passenger confidence and supports premium rental tariffs. Emerging eco-tourism circuits in Sabah and Sarawak, combined with the government’s Borneo highway initiative, will gradually widen geographic diversification for operators.

Border regions with Thailand and inland highways through Perlis and Kedah log notable growth as self-drive overland tourism gains popularity among ASEAN residents. Cross-border entry-permit harmonization and upgrades to Bukit Kayu Hitam and Padang Besar checkpoints reduce administrative bottlenecks, making one-way international rentals viable. Operators looking to penetrate these corridors must navigate differing insurance regimes and vehicle-tracking requirements but stand to capture first-mover advantages.

Competitive Landscape

The competitive field is moderately fragmented. Global majors like Hertz, Avis, Europcar, and SIXT operate alongside regional players like SOCAR, GoCar, Mayflower, and Hawk. International brands leverage corporate contracts and standardized loyalty programs while local firms exploit deeper city-center networks and cultural affinity.

Technology remains the decisive battleground. SOCAR and GoCar rely on AI-powered dynamic-pricing engines to calibrate rates by micro-location and time slot. Peer-to-peer marketplace TREVO lists many privately-owned cars, expanding inventory without capex and giving owners supplemental income. Traditional agencies respond by adding subscription services, white-label EV fleets, and partnerships with hotel chains for bundled stay-and-drive packages.

Strategic moves since 2024 confirm a pivot to electrification and premium positioning. Sime Darby Rent-A-Car teamed with BMW distributor Auto Bavaria to pilot an all-EV rental fleet, capturing early-adopter tourists and corporate executives seeking sustainable options. Avis Malaysia opened a flagship outlet inside Kuala Lumpur’s Sheraton Imperial Hotel to tap into demand from upscale travelers and conference delegates. Over the forecast period, scale economics, insurance bargaining power, and data-science proficiency will likely trigger selective consolidation among mid-sized operators.

Malaysia Car Rental Industry Leaders

SOCAR Malaysia

Mayflower Car Rental Sdn. Bhd.

Hawk Rent A Car

The Hertz Corporation

GoCar Malaysia

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Bolt, a European ride-hailing platform, has officially debuted in Malaysia, kicking off operations in Kuala Lumpur. With competitive pricing, Bolt aims to rival established players, notably Grab.

- February 2024: Sime Darby Auto Bavaria partnered with Sime Darby Rent-A-Car (Hertz Malaysia) to introduce an electric-vehicle rental experience for Malaysian consumers.

Malaysia Car Rental Market Report Scope

Car rental and car lease companies are businesses that offer the service of renting vehicles for a specified period at a fixed price. These companies usually have multiple local offices in or near major cities and a website allowing customers to book cars online.

The Malaysian car rental market is segmented by booking type, rental duration, vehicle type, and application. By booking Type, the market is segmented into online booking and offline booking. By rental duration, the market is segmented into short-term and long-term. By vehicle type, the market is segmented into hatchback, sedan, sport utility vehicles, and multi-purpose vehicles. By application, the market is segmented into tourism and commuting. For each segment, the market sizing and forecast have been done based on the value (USD).

By Booking Type

| Online Booking |

| Offline Booking |

By Rental Duration

| Short-Term (Less than 30 days) |

| Long-Term/Leasing (≥30 days) |

By Vehicle Type

| Hatchback/Economy |

| Sedan |

| Sport-Utility Vehicles (SUV) |

| Multi-Purpose Vehicles (MPV) |

By Rental Channel

| On-Airport |

| Off-Airport |

By Application

| Tourism and Leisure |

| Commuting / Business |

By Customer Type

| Individual |

| Corporate / Fleet |

| By Booking Type | Online Booking |

| Offline Booking | |

| By Rental Duration | Short-Term (Less than 30 days) |

| Long-Term/Leasing (≥30 days) | |

| By Vehicle Type | Hatchback/Economy |

| Sedan | |

| Sport-Utility Vehicles (SUV) | |

| Multi-Purpose Vehicles (MPV) | |

| By Rental Channel | On-Airport |

| Off-Airport | |

| By Application | Tourism and Leisure |

| Commuting / Business | |

| By Customer Type | Individual |

| Corporate / Fleet |

Key Questions Answered in the Report

How large is the Malaysia car rental market in 2026?

The market is valued at USD 0.67 billion in 2026 and is projected to reach USD 1.01 billion by 2031.

What is driving growth in Malaysia’s car rental sector?

Surging inbound tourism, wider adoption of digital booking platforms, and consumer preference for SUVs are the primary growth catalysts.

Which customer segment is expanding fastest?

Corporate and fleet customers are forecast to grow at a 10.34% CAGR as businesses shift toward subscription-based mobility.

How significant are electric vehicles for rental fleets?

Government tax incentives and charging-infrastructure build-out are lowering entry barriers, prompting agencies to trial dedicated EV fleets from 2024 onward.

Page last updated on: