Market Overview

| Study Period | 2021 - 2031 |

|---|---|

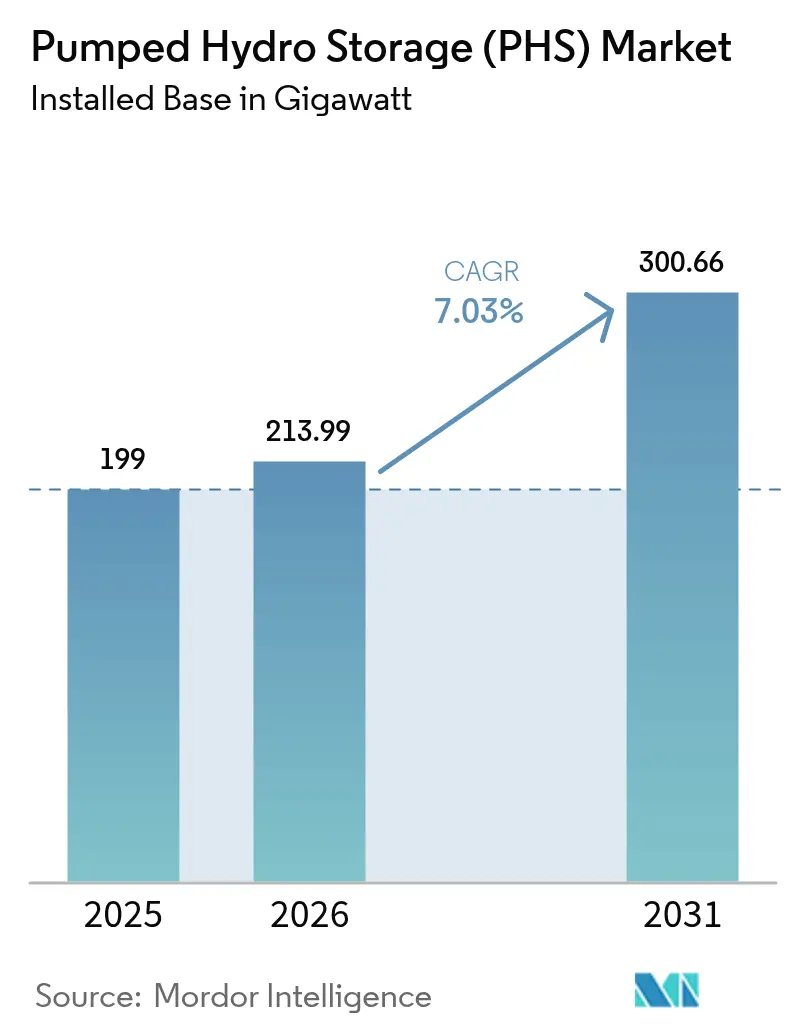

| Market Volume (2026) | 213.99 gigawatt |

| Market Volume (2031) | 300.66 gigawatt |

| Growth Rate (2026 - 2031) | 7.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pumped Hydro Storage (PHS) Market Analysis by Mordor Intelligence

The Pumped Hydro Storage Market size was valued at 199 gigawatt in 2025 and estimated to grow from 213.99 gigawatt in 2026 to reach 300.66 gigawatt by 2031, at a CAGR of 7.03% during the forecast period (2026-2031).

Rapid grid-scale renewable additions, supportive fiscal incentives, and modernization of aging hydro assets continue to anchor demand. Closed-loop technology’s smaller environmental footprint is accelerating project approvals, while joint-ownership structures reduce individual project risk amid capital-intensive balance sheets. Asia-Pacific remains the principal growth engine, buoyed by China’s 120 GW by 2030 target and India’s newly liberalized development guidelines. Developers are combining pumped storage facilities with floating solar and disused mine conversions, thereby widening the geographic scope of viable sites. Even so, lengthy environmental reviews and grid-tariff ambiguities temper near-term commissioning momentum.

Key Report Takeaways

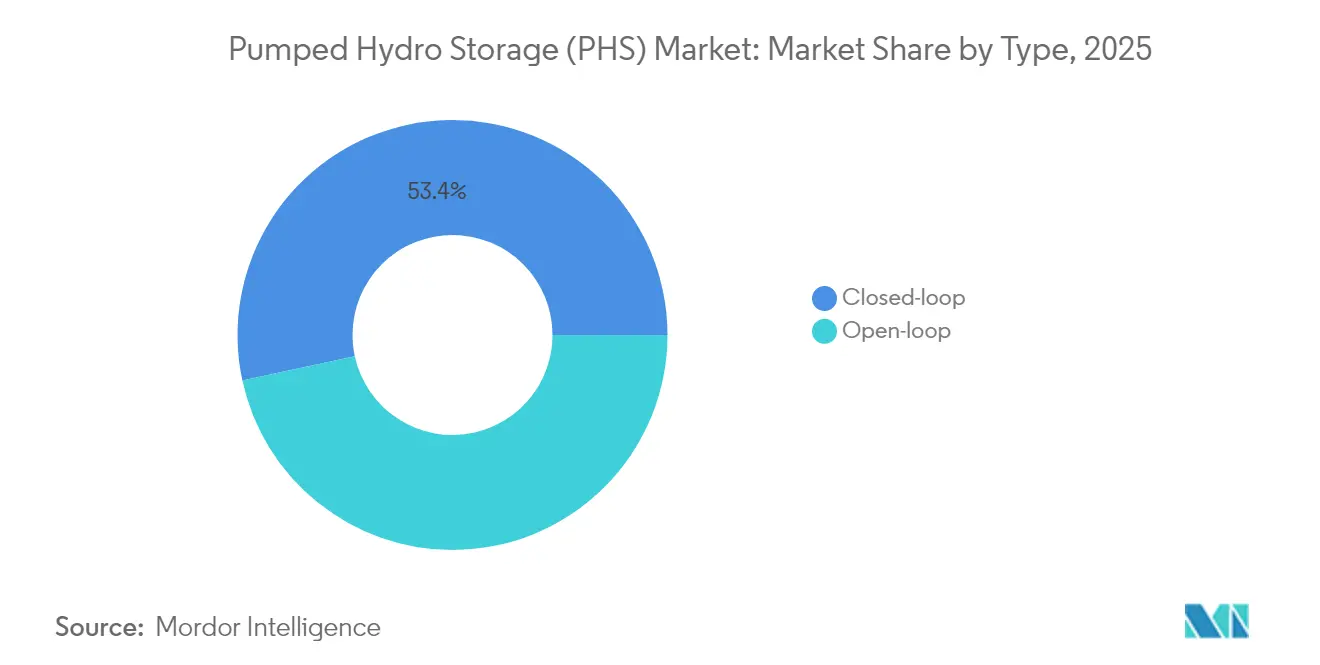

- By type, closed-loop systems held 53.40% of the pumped hydro storage market share in 2025 and are expanding at a 7.56% CAGR through 2031.

- By power rating, the 200-1,000 MW segment led with 45.20% of the pumped hydro storage market size in 2025, while projects below 200 MW are advancing at an 8.06% CAGR until 2031.

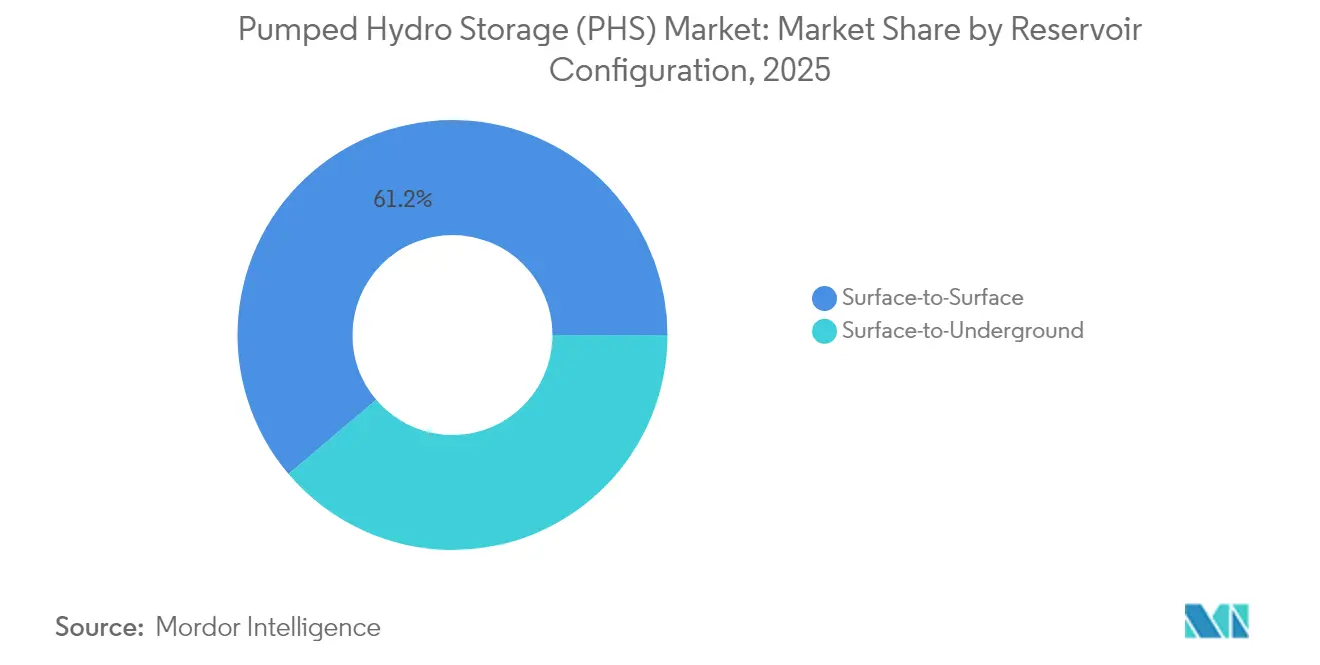

- By reservoir configuration, surface-to-surface plants retained 61.20% revenue share in 2025; surface-to-underground installations exhibit an 7.89% CAGR to 2031.

- By application, renewable-firming uses captured 50.30% share of the pumped hydro storage market size in 2025 and are forecast to post a 7.29% CAGR to 2031.

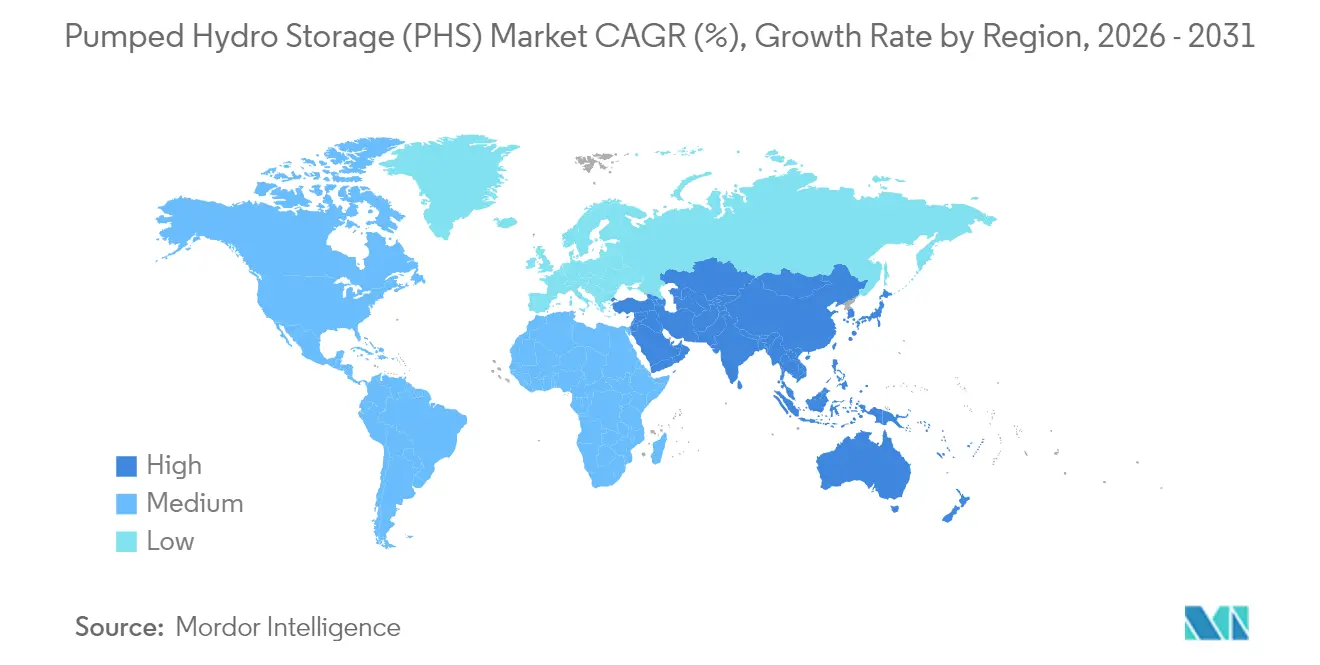

- By geography, Asia-Pacific controlled 48.40% revenue share in 2025 and is progressing at a 8.85% CAGR, powered by China’s and India’s pipelines.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pumped Hydro Storage (PHS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-scale renewable integration mandates | 2.10% | Global, with early gains in EU, China, California | Medium term (2-4 years) |

| Repowering of ageing hydro dams with reversible units | 1.80% | North America & EU, spill-over to APAC | Long term (≥ 4 years) |

| Long-duration storage incentives in Inflation Reduction Act (USA) | 1.50% | National, with concentration in Western states | Short term (≤ 2 years) |

| Fast-track licensing in EU for strategic energy-storage assets | 1.20% | EU core, extending to UK and Norway | Medium term (2-4 years) |

| Co-location with floating solar to raise round-the-clock CF | 0.90% | APAC core, emerging in Brazil and Mediterranean | Long term (≥ 4 years) |

| Use of disused mines & quarries for low-impact closed-loop projects | 0.70% | Global, with pilot projects in Australia, US, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Grid-scale renewable integration mandates drive deployment acceleration

Mandatory clean-energy targets are pushing utilities and state planners to expand the pumped hydro storage market, with China’s pledge for 120 GW by 2030 exemplifying the policy-led build-out. The “PSH-plus” model links renewable clusters with adjacent storage, trimming curtailment, and easing grid expansion costs. Europe mirrors this through its Projects of Common Interest list, which features 12 storage schemes that enjoy streamlined permitting.[1]European Commission, “Projects of Common Interest 2025,” ec.europa.euSpain’s EUR 700 million subsidy window further underlines national follow-through, providing clear revenue visibility that de-risks investor returns.

Repowering ageing hydro infrastructure unlocks latent capacity

Modernizing existing dams by adding reversible pump-turbines breathes new life into legacy assets without the land-use controversies of greenfield builds. The US Department of Energy’s USD 430 million initiative to upgrade the domestic fleet demonstrates the scale of latent gains. Ontario Power Generation’s USD 1 billion rehabilitation of eight stations adds 1,617 MW via higher-efficiency units, while Mexico’s nine-plant refurbishments will raise annual output by 1,754 GWh and extend operational lives by five decades.

Inflation Reduction Act incentives catalyze US market revival

A 30% investment tax credit, plus domestic-content bonuses, now applies to standalone storage, reshaping project economics and swelling a US pipeline of 39.5 GW, three projects already fully FERC-licensed. Federal backing for mine-land repurposing, such as the Lewis Ridge plant in Kentucky, underscores how policy can align environmental remediation with grid needs.[2]U.S. Department of Energy, “Clean Energy on Mine Land Program,” energy.gov

EU fast-track licensing streamlines strategic asset development

Recognizing the tight 2030 climate timetable, Brussels has instructed member states to condense approval cycles for priority storage projects, dovetailing with FERC’s expedited two-year window for US closed-loop filings. The UK’s cap-and-floor regime shields investors from volatile merchant returns by guaranteeing minimum cash flows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy environmental impact assessments | -1.90% | Global, most pronounced in developed markets | Medium term (2-4 years) |

| High upfront CAPEX vs. lithium-ion alternatives | -1.40% | Global, particularly affecting sub-1GW projects | Short term (≤ 2 years) |

| Scarcity of suitable dual-reservoir topographies in urban centres | -1.10% | Dense urban regions globally | Long term (≥ 4 years) |

| Grid tariff uncertainty for storage arbitrage revenues | -0.80% | Deregulated markets, primarily US and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lengthy environmental impact assessments constrain development timelines

Studies covering geology, biodiversity, and cultural heritage can take 5-10 years, adding cost overruns and permitting fatigue. Closed-loop schemes mitigate aquatic impacts, yet hydro-geological risks still demand case-specific reviews, as the Mineville filing in New York shows.[3]Pacific Northwest National Laboratory, “Pumped Storage Economic Analysis,” pnnl.gov

High upfront CAPEX versus lithium-ion alternatives

A 100 MW, 10-hour pumped plant runs USD 263/kWh versus batteries’ lower entry ticket for 2-4-hour services. Long asset lives soften lifecycle cost but leave developers searching for blended finance until paybacks materialize.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Closed-loop systems drive innovation

Closed-loop plants accounted for 53.40% of the pumped hydro storage market share in 2025 and are pacing at a 7.56% CAGR, largely because decoupling from rivers curtails aquatic disruption and speeds approvals. The Federal Energy Regulatory Commission now offers an accelerated two-year license solely for such projects, reinforcing their deployment advantage. Open-loop facilities retain a sizeable base but confront intensifying ecosystem scrutiny, especially where flow regulation or fish passage is contentious.

Closed-loop schemes also unlock new topographies, including disused mine pits and quarries, broadening the pumped hydro storage market’s geographic reach. Lifecycle analyses show lower sedimentation risk and simpler de-watering processes, helping operators maintain high round-trip efficiencies for decades. In parallel, suppliers are refining variable-speed pump-turbines that fit purpose-built reservoirs and allow rapid mode changes, crucial for renewables balancing.

By Power Rating: Mid-scale dominance with small-scale acceleration

Plants between 200 MW and 1,000 MW delivered 45.20% of the pumped hydro storage market size in 2025 because they harmonize capital outlay with grid uptake limits. Regional operators such as Adani Green’s 1,250 MW Uttar Pradesh project demonstrate how synchronized commissioning with transmission upgrades protects against congestion curtailment.

As distributed architectures emerge, installations below 200 MW record an 8.06% CAGR through 2031. Their lighter environmental footprint garners quicker local authority consent, and modular civil works lower schedule risk, fueling investor interest. Conversely, projects over 1,000 MW, while offering bulk inertia, confront longer lead times and heightened public scrutiny—witnessed by China’s 3.6 GW Fengning build that demanded substantial ecological offsets.

By Reservoir Configuration: Surface-to-surface prevalence with underground innovation

Surface-to-surface layouts maintained 61.20% of 2025 revenue as contractors leverage familiar dam and penstock techniques, shortening learning curves and ensuring predictable operations. Accelerated concrete placement methods and digital twin monitoring now further cut construction overruns.

Surface-to-underground schemes, though newer, are rising at an 7.89% CAGR. Repurposed mines such as Kentucky’s Lewis Ridge or New York’s Mineville tap existing shafts as lower reservoirs, trimming earth-moving needs and enabling urban or peri-urban locations where elevation differentials are scarce. Advanced rock-mechanics modeling underscores stability, helping win environmental approvals and broadening the pumped hydro storage market.

By Application: Renewable-firming dominance reflects grid evolution

Renewable-firming uses captured 50.30% share of the pumped hydro storage market size in 2025 and are advancing at a 7.29% CAGR. Curtailment episodes from wind and solar surpluses generate low-cost off-peak energy, ideal for pumping cycles. The Kidston project pairs a 250 MW plant with on-site PV, demonstrating firm, dispatchable output that traditional peakers struggle to match.

Ancillary services—frequency response, voltage support, spinning reserve—now fetch premium nodal prices, prompting plant refurbishments with variable-speed machines that can ramp from zero to full power within 30 seconds. Energy arbitrage remains viable for >8-hour spreads, though batteries dominate the 1-4-hour niche, prompting pumped operators to prioritize long-duration products that the grid lacks.

Geography Analysis

Asia-Pacific held 48.40% of the pumped hydro storage market in 2025 and is posting a 8.85% CAGR owing to China’s 50.94 GW installed base and an aggressive >300-plant pipeline. Beijing’s planning regime integrates storage with renewable bases, minimizing curtailment and shaving grid reinforcement costs, while India’s 103 GW technical potential remains largely untapped but is now primed for build-out after the release of supportive tariff guidelines.

Europe’s pumped hydro storage market enjoys policy heft via the EU’s €584 billion grid-modernization roadmap, which earmarks storage as a priority asset class. Institutional lenders like the European Investment Bank channel concessional loans—€108 million to Iberdrola in 2025—to refurbish and uprate Iberian plants, improving reservoir efficiency and adding peak capacity. Alpine nations continue to exploit natural elevation advantages, while the UK’s cap-and-floor mechanism has readied Glenmuckloch and Coire Glas for final investment decisions.

North America is rebounding under the Inflation Reduction Act, which gives the pumped hydro storage market direct parity with batteries under a 30% ITC. A 39.5 GW pipeline traverses Arizona, Oregon, and the Appalachians, with three schemes already through the FERC gate. Canada focuses on modernization; Ontario Power Generation’s USD 1 billion program illustrates how refurbishing ageing turbines can yield immediate incremental megawatts without new civil works.

Regulatory Landscape

Pumped hydro storage policy is increasingly treated as a strategic grid asset, with regulators and governments pairing permitting acceleration with revenue and grid-access measures. In the United States, the Inflation Reduction Act provides investment support for standalone storage, while FERC offers an accelerated two-year licensing path for closed-loop pumped storage projects, reinforcing the report’s emphasis on lower-impact configurations.

In Europe, policy work is centered on shortening approvals and reducing procedural friction for storage and related grid infrastructure, including streams tied to EU-level rules and practical tools for sub-national authorities (for example, the OECD’s October 2025 diagnostic toolkit for reducing regulatory barriers). The United Kingdom has moved forward with a cap-and-floor approach for long-duration electricity storage, with Ofgem designated as the regulator, while India has strengthened its enabling framework through Ministry of Power draft guidelines and a Central Electricity Authority roadmap targeting 100 GW of pumped storage by 2035-36. This is complemented by state-level implementation schemes (such as Madhya Pradesh) that formalize site allotment and procurement pathways.

Competitive Landscape

The pumped hydro storage market is moderately concentrated, dominated by legacy turbine manufacturers and EPC contractors delivering multi-decade reliability. Andritz alone has supplied over 550 units aggregating 40 GW, using proprietary variable-speed designs to secure recurring service contracts. GE Vernova and Voith likewise use lifecycle support agreements that embed them within operator O&M budgets for 30-50 years.

Risk mitigation shapes ownership. In the United States, 34% of installed pumped capacity sits under joint ventures, compared with just 2% for classical run-of-river plants. Spreading capital and permitting exposure enables utilities, independent power producers, and pension funds to co-finance USD 1 billion-plus projects. Emerging closed-loop developments often bundle environmental remediation, allowing miners to exit liabilities while equity partners receive long-dated cash flows.

Technological differentiation persists. Variable-speed machines allow rapid mode switching and turbine efficiencies above 85%, critical for frequency regulation markets. Submersible pump-turbines under R&D at Argonne National Laboratory promise lower excavation volumes, while geomechanical storage concepts seek to compress water in lined rock caverns, potentially slashing civil works costs. Suppliers court developers through digital twin performance analytics that flag efficiency drifts and optimize dispatch, embedding aftermarket revenue streams.

Pumped Hydro Storage (PHS) Industry Leaders

Enel SpA

China Three Gorges Corporation

Electricité de France (EDF)

Duke Energy Corporation

Iberdrola SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A large buildable pipeline and more explicit long-duration storage programs are widening the addressable market for pumped hydro storage, especially where grids are absorbing higher variable renewable shares and need multi-hour flexibility beyond the 1-4 hour battery niche. International Hydropower Association tracking shows global pumped storage capacity surpassing 200 GW in 2025, with 11.7 GW commissioned in 2025 and a 621 GW development pipeline (including 243 GW under construction), which underscores both the opportunity scale and the execution gap between announced and deliverable projects.

Near-term whitespace is visible in (i) hybrid configurations and control upgrades that monetize ancillary services without fully greenfield civil works and (ii) jurisdictions where policy directly reduces delivered-cost barriers. Enel’s BESS4HYDRO retrofit at the Dossi pumped hydro facility in Italy shows the direction toward pairing hydraulic storage with batteries to improve responsiveness and ancillary service value capture. Separately, India’s June 2025 order extending a 100% waiver of ISTS charges for pumped storage projects with construction work awarded by June 30, 2028 improves project bankability for inter-state dispatch. On the supply and capability side, China’s continued standardization and commissioning activity, including multi-unit stations brought online in 2026, supports an expanding market for variable-speed machines, high-head designs, and refurbishment-driven uprates, consistent with the report’s focus on modernization of aging hydro assets and closed-loop approvals.

Recent Industry Developments

- July 2026: Enel Green Power inaugurated the BESS4HYDRO project at the Dossi hydropower plant in Valbondione, Italy, integrating a 4 MW lithium-ion battery with the existing facility to enhance flexibility and grid services. The hybrid setup increases the range of ancillary services that can be delivered without relying solely on hydraulic cycling, and it points to a pathway for upgrading mature pumped storage assets through add-on power electronics and fast-response storage.

- February 2025: NTPC Limited and EDF India Private Limited signed a collaboration agreement to explore pumped storage and hydropower opportunities in India. The tie-up strengthens the development bench for large, capital-intensive projects by combining local market access and system planning capabilities with major-utility hydro expertise, aligning with India’s expanding policy focus on pumped storage build-out.

- December 2024: Enel announced plans to retrofit battery storage at the Dossi pumped hydro storage plant through the BESS4HYDRO initiative, structured as a 4 MW/8 MWh lithium-ion installation and backed by EU-level innovation support. Positioning a battery retrofit at an established pumped storage site highlights how operators can extract more grid value from existing reservoirs and turbines while limiting new environmental footprint.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the pumped hydro storage market covers pumped storage hydropower assets used to store electricity by moving water between two reservoirs and later generating power during discharge. The sizing focuses on installed capacity and expected capacity additions, tracked in gigawatts.

Scope exclusions: we exclude conventional run-of-river hydropower without a pumping cycle and battery-only storage systems that do not use pumped water reservoirs.

Segmentation Overview

- By Type

- Open-loop

- Closed-loop

- By Power Rating (MW)

- Below 200 MW

- 200 to 1,000 MW

- Above 1,000 MW

- By Reservoir Configuration

- Surface-to-Surface

- Surface-to-Underground

- By Application

- Renewable Firming

- Ancillary Grid Services

- Arbitrage & Peak Shaving

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia Pacific

- South America

- Argentina

- Rest of South America

- Middle East and Africa

- Iran

- Morocco

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with public capacity and generation datasets so the global pumped storage base can be rebuilt using consistent definitions. We rely on sources such as the International Hydropower Association, IEA electricity statistics, the US EIA, Eurostat, and national energy ministries and regulators that publish plant lists, capacity tables, and grid planning documents.

To cross-check what gets built and when, we also review developer and utility filings, annual reports, project announcements, and reputable press coverage on permitting and commissioning. A paid subscription focused on company financials and news helps us track ownership changes, project delays, and commissioning updates that can otherwise be missed. The sources listed here are illustrative, and additional public references were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to validate project timelines, typical ramp rates, and the practical difference between announced and finance-ready capacity. We speak with EPC and equipment-side teams, utilities and grid planners, project developers, and advisors across APAC, EMEA, and the Americas so assumptions can be checked against on-the-ground build reality.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 36% | CXOs: 13% | APAC: 47% |

| Mid tier: 46% | Functional/Unit leaders: 38% | EMEA: 31% |

| Smaller Players: 18% | Managers: 49% | Americas: 22% |

Market-Sizing & Forecasting

Our sizing is anchored in a top-down build from installed pumped storage capacity and the forward project pipeline. We reconstruct the pipeline using country and regional plant registers, plus grid and permitting disclosures. Once the demand pool is built, we stress-test totals using selective bottom-up approximations, such as sampled project MW roll-ups by geography, typical unit sizes by project type (open-loop vs. closed-loop), and channel checks on commissioning schedules.

A few practical inputs shape the model, including announced vs. under-construction MW, average construction and permitting lead times, retirement and refurbishment patterns for older plants, and grid flexibility needs linked to renewable capacity additions. Where project data is incomplete, we apply conservative timing rules and then revisit them during interviews, so gaps do not inflate near-term capacity. Forecasting uses scenario analysis supported by expert views on approval cadence and grid reliability spending, followed by an annualized ramp profile so the output matches how projects actually come online.

Data Validation & Update Cycle

Model outputs are checked against independent signals such as country-level capacity statements, commissioning news flow, and grid development plans. Outliers are flagged for analyst review before sign-off. If a large project is delayed, canceled, or re-permitted, we re-contact sources and update the timing logic so the forecast does not drift.

The report is refreshed annually, and interim updates are made when material events occur, such as policy changes affecting hydro permitting or major project sanction decisions. Before delivery, a final pass is completed to confirm that the latest plant additions and schedule changes are reflected in the numbers clients receive.

Mordor Intelligence's Pumped Hydro Storage Market Size Measured Against Other Published Estimates

Published estimates for pumped hydro storage often do not match because some studies measure installed capacity, while others publish USD value based on assumed equipment and construction costs. Differences also show up when one publisher counts early-stage announcements, and another counts only projects that are permitted or already under construction.

Commissioning timelines and the verified global installed base are the main evidence checks that keep Mordor Intelligence tied to a GW capacity view for 2026, which naturally will not align with USD-value estimates that bake in ASP and cost inflation assumptions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 213.99 B (2026) | |

| Global Consultancy A | USD 71.71 B (2025) | Reported as a value market in USD, so the total is sensitive to assumed EPC and equipment pricing, cost inflation, and currency timing, rather than only installed and pipeline capacity in GW. |

| Industry Publisher B | USD 43.67 B (2023) | Uses an earlier base year and a USD-value framing, which can include broader cost elements and different project inclusion rules, especially around announced capacity that is not yet construction-ready. |

The spread in the table is mainly explained by unit choice and boundary decisions, not by a disagreement that pumped storage is growing. By keeping the model traceable to project MW, timing, and validation checks, we can explain each step clearly and update it quickly when large projects shift schedules.

Key Questions Answered in the Report

What is the current pumped hydro storage market size?

The pumped hydro storage market size stands at 213.99 GW in 2026 and is forecast to reach 300.66 GW by 2031.

Which region leads the pumped hydro storage market?

Asia-Pacific leads with 48.40% revenue share in 2025 and an 8.85% CAGR outlook through 2031, driven mainly by China and India.

Why are closed-loop systems growing faster?

Closed-loop plants bypass rivers, easing environmental approvals and qualifying for expedited licensing that accelerates build times.

How does the Inflation Reduction Act affect US pumped storage?

A 30% investment tax credit now applies to standalone storage, helping develop a 39.5 GW project pipeline and improving financing terms.

What hurdle most delays pumped storage projects?

Multi-year environmental impact assessments, especially in densely regulated markets, often extend project lead times by up to a decade.

Are batteries replacing pumped hydro storage?

Lithium-ion dominates short-duration services, but pumped storage retains cost and lifespan advantages for applications exceeding 8-10 hours.

Page last updated on: