Public Wi-Fi Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

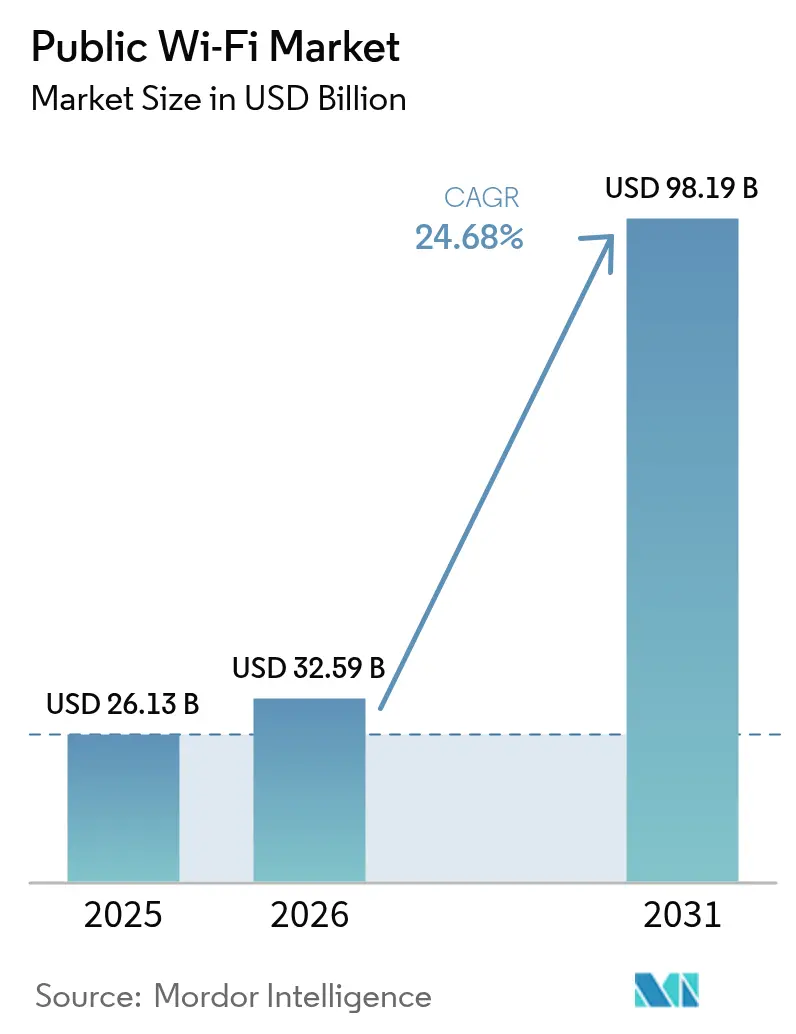

| Market Size (2026) | USD 32.59 Billion |

| Market Size (2031) | USD 98.19 Billion |

| Growth Rate (2026 - 2031) | 24.68% CAGR |

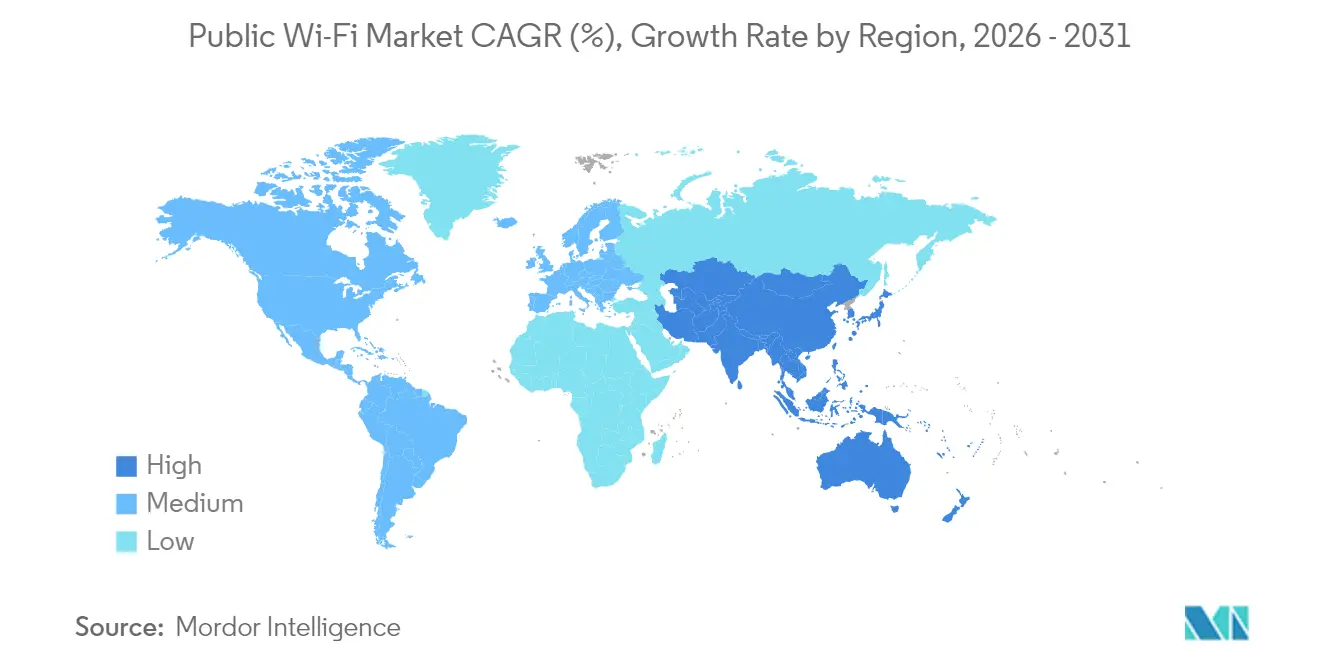

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Public Wi-Fi Market Analysis by Mordor Intelligence

Public Wi-Fi Market size in 2026 is estimated at USD 32.59 billion, growing from 2025 value of USD 26.13 billion with 2031 projections showing USD 98.19 billion, growing at 24.68% CAGR over 2026-2031. Accelerated smart-city funding, rapid adoption of Wi-Fi 6E and Wi-Fi 7, and AI-native cloud management platforms are reshaping the total cost of ownership, while open roaming standards expand monetization avenues in high-density venues. Hardware refresh cycles, subscription-based Wi-Fi-as-a-Service (WaaS), and edge analytics are combining to keep the public Wi-Fi market in double-digit growth territory. Government‐backed broadband programs and private-sector enterprise upgrades are aligning in a virtuous demand loop that encourages vendors to integrate AI automation directly into access points, controllers, and analytics layers. Energy-efficiency directives and 6 GHz spectrum licensing hurdles remain headwinds; yet, the ongoing CAPEX-to-OPEX migration is insulating network planners from large upfront investments and sustaining confidence in long-term deployment roadmaps.

Key Report Takeaways

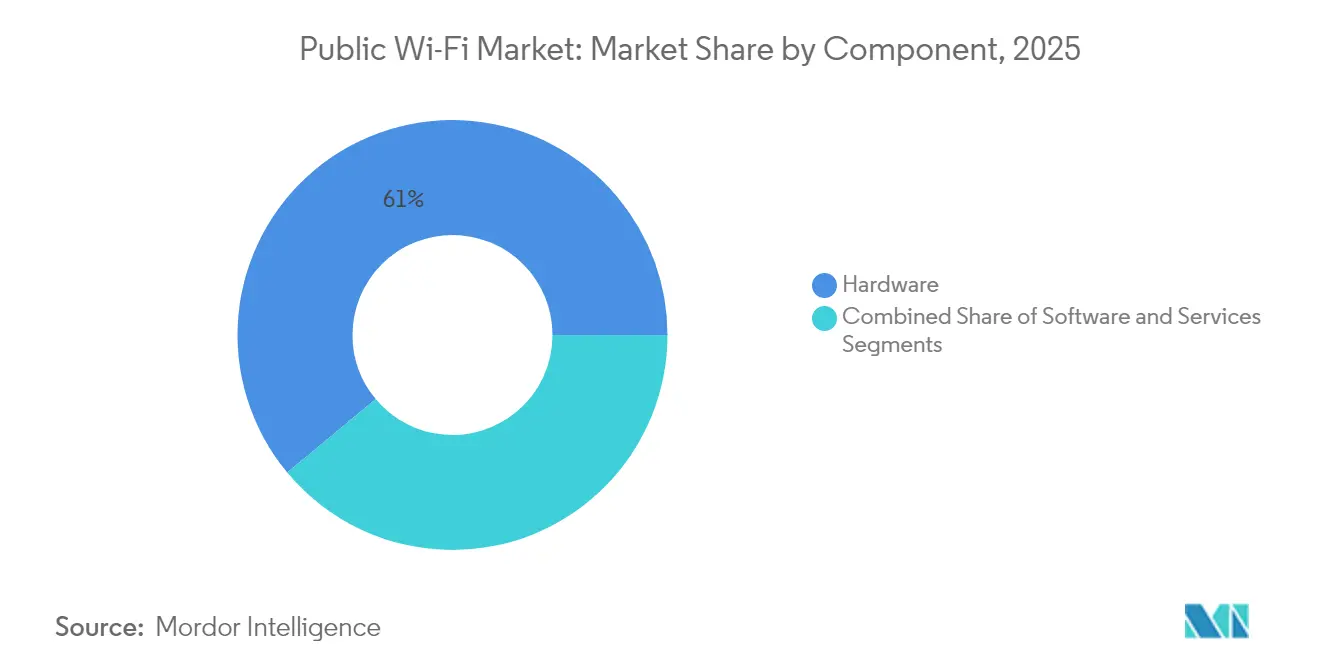

- By component, hardware led the 2025 revenue of the public Wi-Fi market, with 61.05%, while software is expected to advance at a 26.1% CAGR through 2031.

- By deployment model, cloud-managed platforms captured 60.10% share of the public Wi-Fi market in 2025; hybrid architectures are rising fastest at 26.3% CAGR.

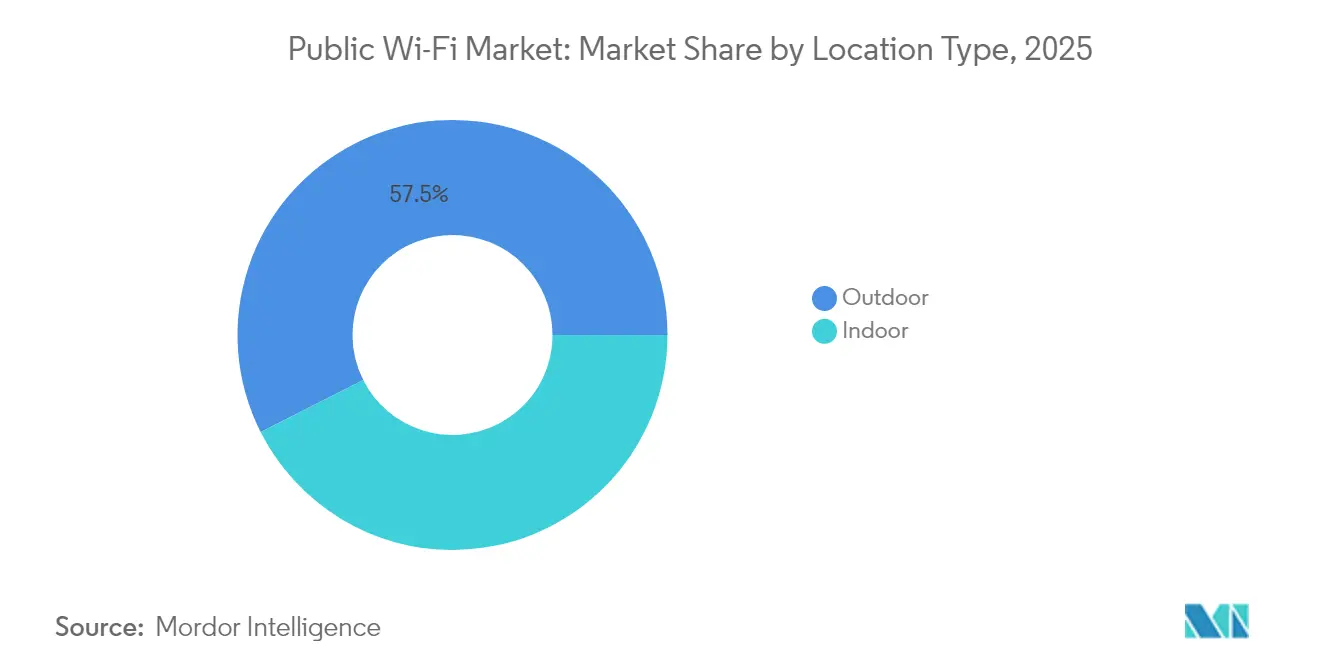

- By location type, outdoor installations accounted for 57.45% of the public Wi-Fi market's 2025 revenue and are expected to expand at a 25.6% CAGR, driven by smart-city projects.

- By end-user vertical, telecom and IT accounted for 28.30% of the 2025 public Wi-Fi market; transportation and logistics are expected to lead the field with a 27.2% CAGR to 2031.

- By geography, North America led the 2025 public Wi-Fi market with 37.90% of the revenue, while the Asia Pacific is expected to grow at a 26.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Public Wi-Fi Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart city-funded public Wi-Fi rollouts | +4.2% | Global (early gains in North America, China, India) | Medium term (2-4 years) |

| Exploding connected-device traffic driving network offload | +6.8% | Global | Short term (≤ 2 years) |

| Wi-Fi 6E-7 upgrades and AI automation boosting network ROI | +5.1% | North America and the EU with spill-over to Asia Pacific | Medium term (2-4 years) |

| Subscription-based Wi-Fi-as-a-Service trimming CAPEX | +3.9% | Global (early adoption in North America and Europe) | Long term (≥ 4 years) |

| OpenRoaming adoption unlocking seamless monetization | +2.7% | Developed markets | Long term (≥ 4 years) |

| Edge analytics-ads revenue streams via user telemetry | +2.4% | Asia Pacific core with spill-over to MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Smart City-Funded Public Wi-Fi Rollouts

National and municipal governments are underwriting large-scale Wi-Fi buildouts that guarantee multi-year demand for hardware and services. The USD 42.45 billion BEAD program is allocating awards of USD 1.355 billion to Louisiana and USD 416.6 million to Nevada, earmarking public Wi-Fi as the primary connectivity layer.[1]Sarah Bolton, “BEAD Program State Approvals 2024,” Broadband Now, broadbandnow.com Comparable commitments are emerging in the Philippines and Spain, ensuring a pipeline of enterprise-grade access points with energy-efficient designs that meet EU directives. RFP cycles of 3-5 years generate predictable revenues for vendors, while local content rules and power budget caps influence the development of SKU roadmaps. Collectively, these publicly funded projects enhance demand visibility and stabilize the public Wi-Fi market, counterbalancing the otherwise cyclical patterns of private-sector spending.

Exploding Connected-Device Traffic Driving Network Offload

Average enterprise sites now support 15-20 connected devices per employee, and public venues routinely top 1,000 simultaneous users per access point at peak.[2]Cisco Systems, “Catalyst 9176 Access Point,” cisco.com Offloading that traffic from congested cellular networks has become strategic rather than optional, positioning Wi-Fi 6E’s 6 GHz spectrum as an immediate capacity upgrade. Service-provider plans reveal 81% intend to enable OpenRoaming by 2025, recognizing that friction-free onboarding will be essential when offload revenues well. As Wi-Fi 7 chipsets mature, operators expect deterministic latency and wider channels to keep pace with real-time applications that otherwise hammer 5G macro networks.

Wi-Fi 6E-7 Upgrades and AI Automation Boosting Network ROI

Next-generation access points integrate AI engines that automate channel selection, power levels, and client steering, reducing manual intervention by up to 70%. Early adopters report 40-60% improvements in throughput-per-watt metrics, alleviating energy budget concerns while reducing help desk tickets. HPE Aruba’s Wi-Fi 7 730-series and Juniper’s AP47 family reinforce the trend by embedding machine learning and supplying actionable telemetry to cloud dashboards. The result is a virtuous cycle: elevated performance extends upgrade intervals and justifies premium ASPs, which in turn finance further AI research and development.

Subscription-Based Wi-Fi-as-a-Service Trimming CAPEX

WaaS shifts network spend from lumpy capital cycles to predictable OPEX streams that bundle hardware, software, and support. Cisco’s unified licensing and Aruba Central’s usage-based tiers are achieving 60-70% reductions in first-year cash outlay versus traditional models. SMBs value built-in lifecycle refresh and remote management included in monthly fees, while multi-site enterprises prefer rapid turn-up and common policy enforcement. The public Wi-Fi market is embracing the shift because hardware lifecycles align with contract terms, ensuring continuous innovation without requiring large, one-time budget approvals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent cyber-security and privacy vulnerabilities | -3.2% | Global | Short term (≤ 2 years) |

| 5G unlimited-data plans cannibalizing hotspot usage | -2.8% | North America and EU extending to Asia Pacific | Medium term (2-4 years) |

| Licensing costs for outdoor 6 GHz spectrum | -1.9% | Global with regulatory variation | Long term (≥ 4 years) |

| Energy-efficiency mandates limiting AP power budgets | -1.4% | EU and North America expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Cyber-Security and Privacy Vulnerabilities

Rising WPA3 exploits and stricter privacy mandates add layers of complexity to compliance. GDPR, HIPAA, and PCI-DSS frameworks require explicit consent, audit trails, and encryption across all authentication flows, compelling network operators to adopt zero-trust postures and implement frequent patching cycles.[3]European Union, “General Data Protection Regulation,” gdpr.eu Healthcare and finance remain cautious, delaying rollout timelines or segmenting guest traffic to isolate regulated data. Security overlays inflate TCO and cut into approval cycles, tempering the otherwise strong adoption momentum in the public Wi-Fi market.

5G Unlimited-Data Plans Cannibalizing Hotspot Usage

North American carriers now bundle 100 GB or more of mobile hotspot allowance into premium unlimited tiers, enticing casual users to stay on cellular networks. Where indoor 5G coverage or mmWave deployments meet throughput needs, public Wi-Fi session revenues decline, prompting venue owners to reevaluate their monetization models. The shift is uneven: video streaming, bulk downloads, and IoT backhaul still favor Wi-Fi economics, while retail browsing and social feeds are shifting to cellular. Venue operators must craft differentiated engagement layers, such as loyalty apps or location-based promotions, to defend footfall analytics revenue.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Foundation Supports Software Innovation

Hardware maintained a 61.05% share in 2025, driven by access-point refresh cycles that stabilize the public Wi-Fi market size for physical infrastructure. Access points alone accounted for the largest slice of revenue, and WLAN controller consolidation reflected the shift to cloud-based dashboards. Wi-Fi 7 rollouts, energy-efficiency mandates, and compliance renewals under Europe’s Radio Equipment Directive reinforce continuous demand for hardware and protect vendor margins. Indoor power constraints and outdoor weatherization continue to influence SKU variants, prompting vendors to incorporate adaptive power management into their ASIC designs.

Software is expanding at a 26.1% CAGR through 2031, fueled by AI-native cloud platforms that unify configuration, assurance, and monetization analytics. Consumption billing models scale with network growth, and the public Wi-Fi market share allocated to cloud management is therefore set to widen even as controllers decluster. Centralized dashboards simplify zero-touch provisioning for MSPs, enable advanced roaming analytics, and satisfy cross-vertical compliance logging requirements. Combined, hardware reliability and software intelligence form a mutually reinforcing value loop that sustains product differentiation for incumbents and dissuades price-only challengers.

By Deployment Model: Cloud Management Drives Hybrid Adoption

Cloud-managed architectures accounted for 60.10% of 2025 revenue, maintaining a significant market share in the public Wi-Fi market, where SaaS-delivered control planes dominate. Enterprises welcome centralized troubleshooting and AI-guided optimization that lifts uptime without site visits. Certification milestones, such as SOC 2 and ISO 27001, alleviate data-sovereignty concerns, enabling regulated industries to migrate guest SSID policies and non-PII analytics to public clouds while keeping sensitive workloads on-premises.

Hybrid adoption is growing at a 26.3% CAGR as organizations integrate local gateways under a global dashboard. This approach enables hospitals or banks to keep patient and transaction payloads local while benefiting from cloud-scale telemetry for guest portals and marketing analytics. On-premises dominance persists only in defense and ultra-low-latency automation, where air-gapped security or deterministic jitter takes precedence over cloud convenience. Together, these dynamics ensure deployment flexibility remains a core buying criterion across the public Wi-Fi market.

By Location Type: Outdoor Deployments Lead Infrastructure Modernization

Outdoor venues represented 57.45% of 2025 revenue, and their 25.6% CAGR cements their lead in the public Wi-Fi market. Smart-city corridors, airports, and transport hubs require ruggedized hardware with extended temperature and ingress ratings, as well as support for 6 GHz spectrum. Municipal tenders specify solar-ready mounting kits that meet energy-efficiency targets without requiring trenching for power, thereby simultaneously broadening the addressable acreage for access-point vendors.

Indoor growth remains anchored in retail, hospitality, and enterprise campuses where advanced location services and application quality of service extract deeper operational value from the same RF fabric. Integration with point-of-sale, staff communications, and shopper analytics drives incremental ASP for indoor gear, allowing vendors to package turnkey vertical solutions. The dual-track growth of indoor and outdoor environments keeps R&D diverse, spawning innovations in antenna and ASIC technologies that cross-pollinate both environments and reinforce the public Wi-Fi market share of vendors with comprehensive indoor-outdoor lineups.

By End-User Vertical: Transportation Growth Outpaces Traditional Leaders

Telecom and IT operators accounted for 28.30% of 2025 revenue, bolstering the public Wi-Fi market size by offloading mobile traffic and integrating Wi-Fi into customer experience campaigns. Retail followed, leveraging Wi-Fi analytics for omnichannel personalization. Government rollouts expand digital inclusion and civic services, while education upgrades loosen BYOD constraints via segmented SSIDs and identity-based policies.

Transportation and logistics are projected to post the fastest vertical CAGR of 27.2% from 2021 to 2031. Modernized airports, rail hubs, and fleet depots require uninterrupted handoff and high throughput for e-gates, e-manifests, and passenger engagement apps. Access points with integrated IoT radios handle baggage tracking and predictive maintenance sensors, cutting downtime and costs. As airline, transit, and logistics operators link Wi-Fi analytics to operational KPIs, spending migrates from pilot projects to multi-site production networks, enlarging the public Wi-Fi market share devoted to this vertical.

Geography Analysis

North America accounted for 37.90% of 2025 revenue, driven by BEAD allocations, enterprise migrations to Wi-Fi 6E, and early Wi-Fi 7 trials in stadiums and universities. U.S. cities are piloting open roaming to harmonize private and municipal networks, while Canada aims to close public Wi-Fi gaps in rural and Indigenous areas. Mexico’s maquiladora manufacturing corridors are adopting WaaS to overcome CAPEX hurdles, thereby generating incremental revenue for the regional public Wi-Fi market.

The Asia Pacific is expected to accelerate at a 26.2% CAGR through 2031. China bundles public Wi-Fi into nationwide smart-city blueprints, achieving economies of scale that push unit ASPs lower and spur adoption in tier-two cities. India’s Digital India Wi-Fi hotspots expand rural connectivity and stimulate e-commerce, reinforcing demand for cloud-managed dashboards that can operate on variable backhaul. Singapore, Malaysia, and Thailand modernize transport and tourism infrastructure, adopting Wi-Fi 7 to enable autonomous shuttles and augmented-reality visitor guides.

Europe sustains demand through privacy-centric innovation. Germany and the United Kingdom lead in enterprise cloud migration, France and Italy expand city-center tourist Wi-Fi, and Spain rolls municipal networks into smart-city sensor grids. Compliance with GDPR and the Energy Efficiency Directive drives exporter vendors to integrate data minimization and low-power hardware designs. Collectively, these initiatives are expected to preserve steady growth for the public Wi-Fi market despite macroeconomic headwinds.

Competitive Landscape

The competitive field remains moderately fragmented yet tilts toward vendors with broad hardware portfolios and AI-native cloud dashboards. Cisco extends its leadership with the Catalyst 9176/9178 access points, which embed machine learning engines and offer unified licensing, resulting in a 40% reduction in total cost of ownership. HPE Aruba leverages its acquisition of Athonet to converge private 5G and Wi-Fi under a single management fabric.[4]HPE, “HPE Completes Acquisition of Athonet,” hpe.com Juniper’s Mist AI and AP47 series apply AI-driven assurance to optimize user experience and reduce mean time to resolution.

Extreme Networks, TP-Link, Cambium, and Purple WiFi compete through niche strengths such as small-business cloud management, power-efficient outdoor gear, or privacy-preserving analytics. Regional players in China and India tailor solutions to local compliance and price points, challenging global incumbents in cost-sensitive tenders. Differentiation is increasingly based on end-to-end visibility, automated root-cause analysis, and open roaming support attributes that resonate across the public Wi-Fi market, regardless of geography or vertical.

Public Wi-Fi Industry Leaders

Cisco Systems Inc.

Hewlett Packard Enterprise Company

Huawei Technologies Co., Ltd.

CommScope Holding Company Inc.

Extreme Networks Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Cisco Systems announced the general availability of the Catalyst 9176 and 9178 Wi-Fi 7 access points, featuring AI-native optimization and unified licensing that reduces the total cost of ownership by 40%.

- September 2025: HPE completed its USD 155 million acquisition of Athonet, adding private 5G to its Wi-Fi portfolio.

- August 2025: Juniper Networks introduced the AP47 Wi-Fi 7 family featuring integrated IoT radios and cloud-native management.

- July 2025: The Wireless Broadband Alliance reported 81% of service providers plan to offer OpenRoaming by 2026.

- June 2025: Nokia and NTT Data agreed to deploy private 5G and Wi-Fi 6E networks across Japanese and Southeast Asian enterprises.

- May 2025: The U.S. FCC allocated 20 additional 6 GHz channels for Wi-Fi 6E outdoor use.

Global Public Wi-Fi Market Report Scope

Public Wi-Fi hotspots are created by deploying the necessary wireless hardware that enables internet connection to create a Wi-Fi network that connects devices, such as tablet, smartphone, and computer, among others. These hotspots are deployed across different outdoor locations like railway stations, hotels, airports, cafes, educational institutions, and other public places across regions. Most of the Public-hotspots deployed across regions are due to the government's push to expand internet coverage. Hence, most of the publicly available Wi-Fi hotspots are free. However, they enable different business models.

| Hardware | Access Points |

| WLAN Controllers | |

| Wireless Hotspot Gateways | |

| Software | |

| Services |

| Cloud Managed |

| On-Premises |

| Hybrid |

| Indoor |

| Outdoor |

| Telecom and IT |

| Retail and E-Commerce |

| Travel and Hospitality |

| Transportation and Logistics |

| Government and Public Sector |

| Education |

| Healthcare |

| Other End-User Verticals |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| South-East Asia | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Component | Hardware | Access Points |

| WLAN Controllers | ||

| Wireless Hotspot Gateways | ||

| Software | ||

| Services | ||

| By Deployment Model | Cloud Managed | |

| On-Premises | ||

| Hybrid | ||

| By Location Type | Indoor | |

| Outdoor | ||

| By End-User Vertical | Telecom and IT | |

| Retail and E-Commerce | ||

| Travel and Hospitality | ||

| Transportation and Logistics | ||

| Government and Public Sector | ||

| Education | ||

| Healthcare | ||

| Other End-User Verticals | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the public Wi-Fi market in 2026?

Shipments reached 1.32 billion units in 2026, and the figure is forecast to rise to 3.98 billion units by 2031.

What CAGR is forecast for the public Wi-Fi market to 2031?

The market is projected to grow at 24.68% CAGR through 2031.

Which component segment leads current shipments?

Hardware accounts for 61.05% of 2025 shipments, led by access-point refresh cycles.

Which deployment model is expanding fastest?

Hybrid cloud-managed architectures are advancing at 26.3% CAGR as enterprises balance security with flexibility.

Which vertical shows the highest growth momentum?

Transportation and logistics is pacing the field at 27.2% CAGR, driven by airport and fleet connectivity projects.

What regional market is growing fastest?

Asia Pacific is posting a 26.2% CAGR through 2031, propelled by smart-city initiatives in China, India, and Southeast Asia.

Page last updated on: