Wi-Fi Range Extender Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

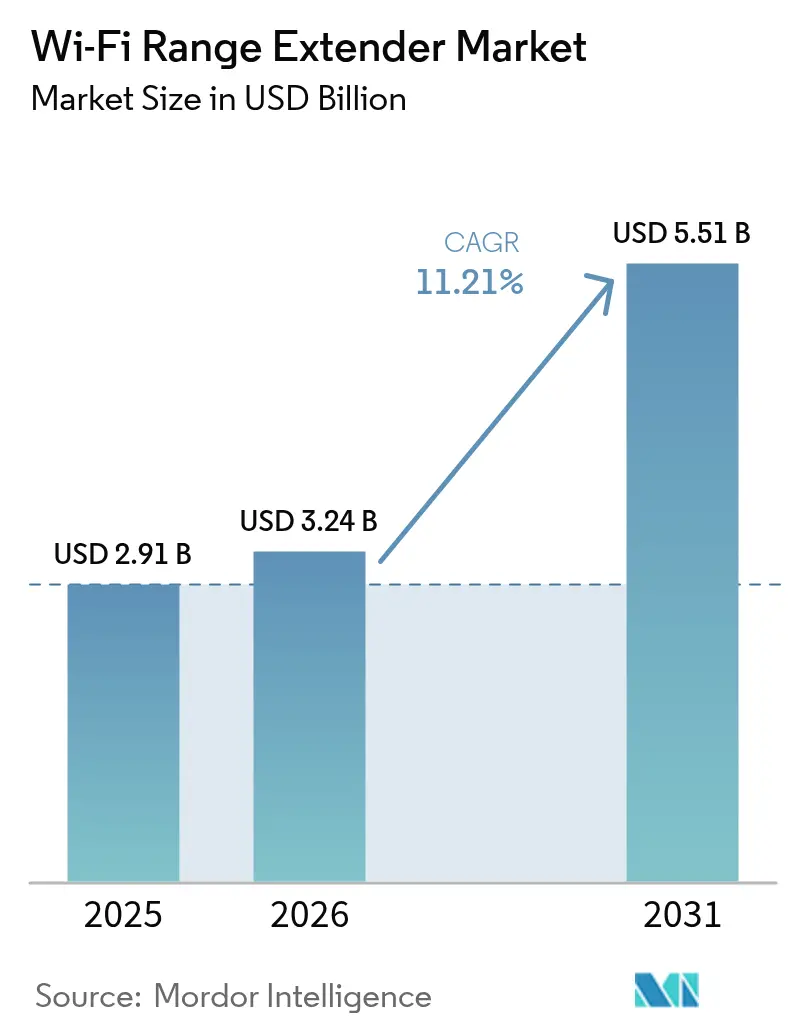

| Market Size (2026) | USD 3.24 Billion |

| Market Size (2031) | USD 5.51 Billion |

| Growth Rate (2026 - 2031) | 11.21% CAGR |

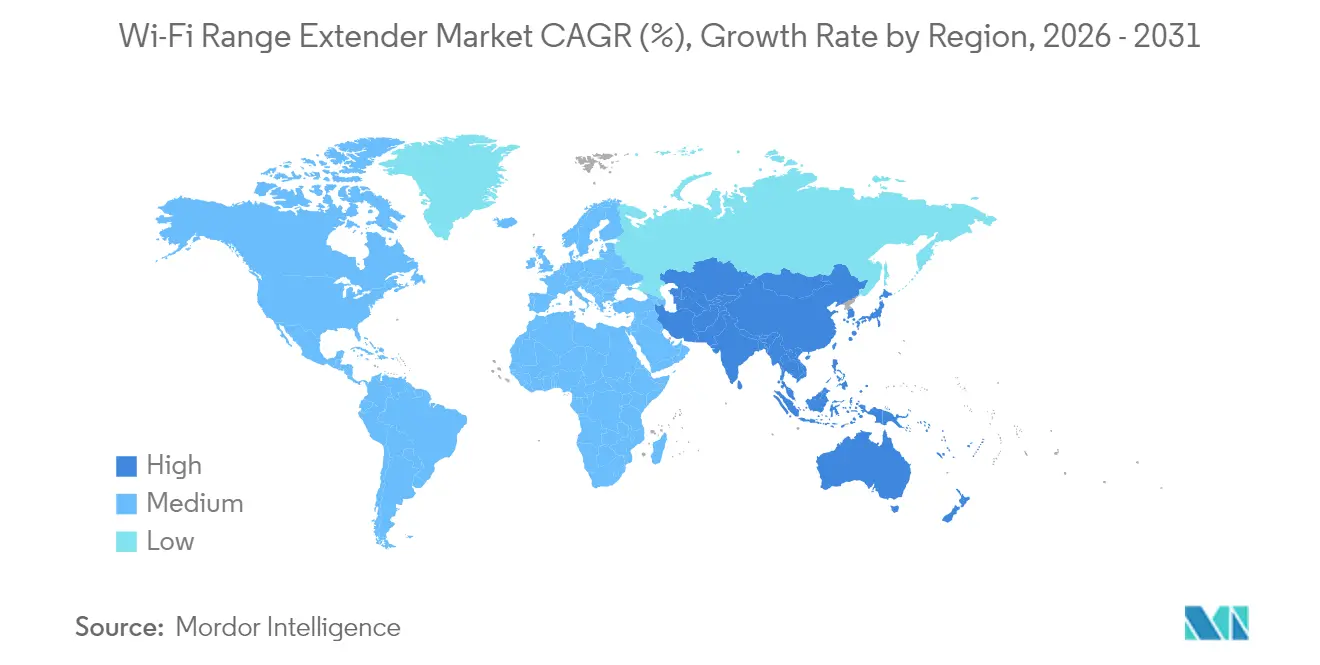

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

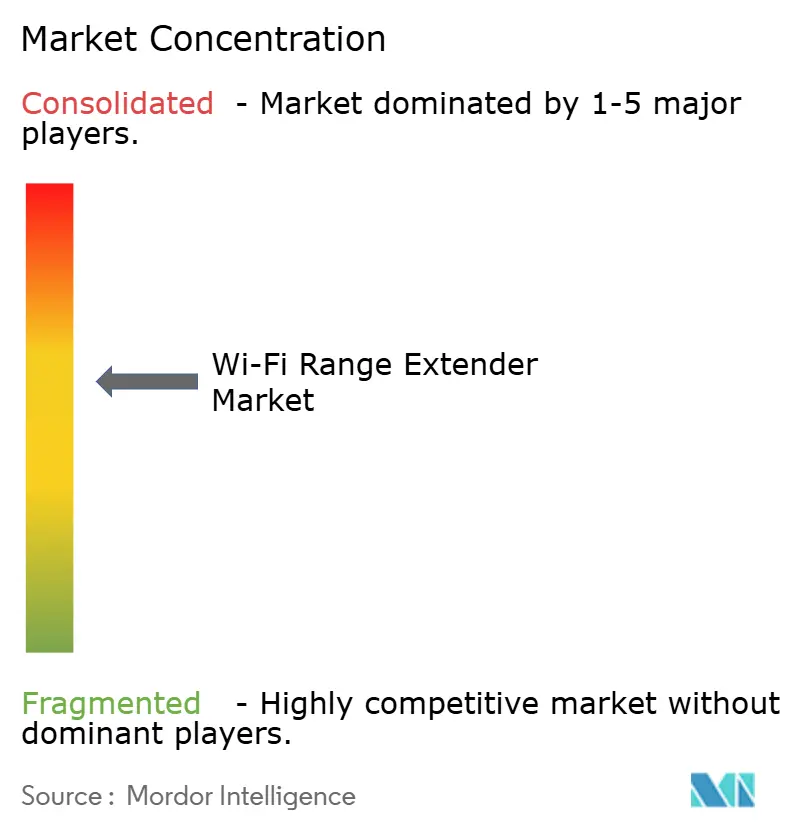

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Wi-Fi Range Extender Market Analysis by Mordor Intelligence

The Wi-Fi range extender market size was valued at USD 2.91 billion in 2025 and estimated to grow from USD 3.24 billion in 2026 to reach USD 5.51 billion by 2031, at a CAGR of 11.21% during the forecast period (2026-2031). Surging smart-home adoption, hybrid-work policies and expanding regulatory mandates are extending wireless coverage requirements well beyond the reach of standard routers. Product redesigns to satisfy the European Union’s 2025 cybersecurity and energy-efficiency rules are lifting development costs yet creating protective moats for compliant brands. Enterprises now regard uninterrupted Wi-Fi coverage as business-critical infrastructure, and the transition to Wi-Fi 7 is widening performance gaps that legacy devices cannot bridge. Simultaneously, mesh-networking solutions and antitrust investigations are reshaping competitive tactics in the Wi-Fi range extender market.

Key Report Takeaways

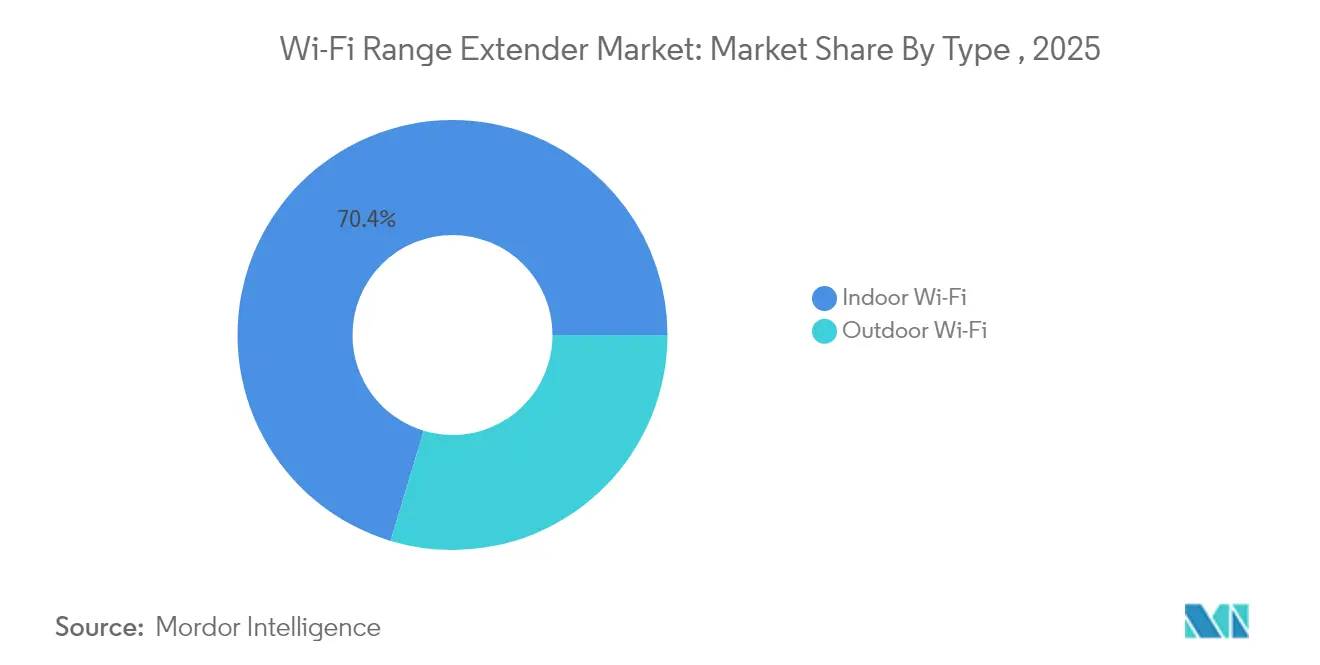

- By type, indoor installations held 70.35% of the Wi-Fi range extender market share in 2025, whereas outdoor projects are growing at a 12.94% CAGR through 2031.

- By product, extenders and repeaters commanded 53.25% of the Wi-Fi range extender market size in 2025, while access points are advancing at the fastest 16.12% CAGR.

- By technology standard, Wi-Fi 6/6E led with 47.35% share of the Wi-Fi range extender market size in 2025; Wi-Fi 5 equipment is still expanding 13.78% annually as cost-conscious buyers favor proven solutions.

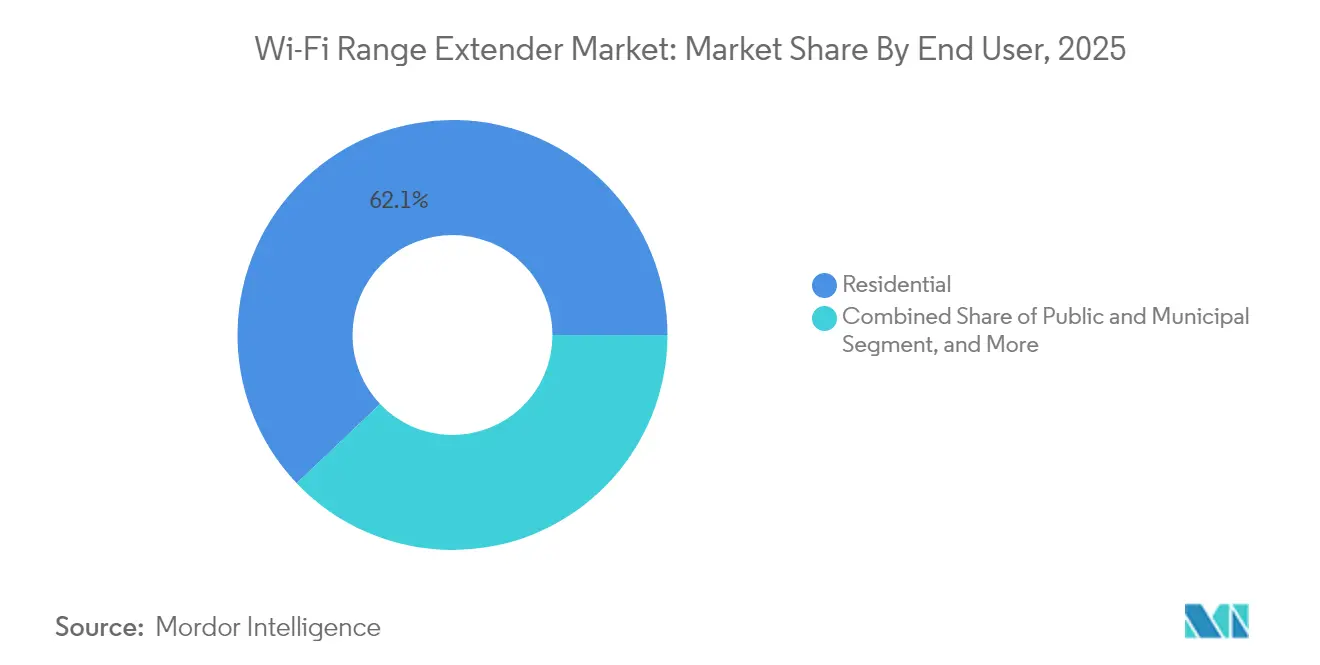

- By end user, residential applications generated 62.10% revenue in 2025, whereas public and municipal deployments exhibit a 15.32% CAGR owing to smart-city initiatives.

- By sales channel, online platforms captured 51.40% revenue in 2025 and are progressing at a 12.08% CAGR as buyers prioritize direct-to-consumer convenience.

- By geography, North America accounted for 39.45% of Wi-Fi range extender market share in 2025, while Asia Pacific is the fastest-growing region with a 13.32% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Wi-Fi Range Extender Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) Impact on CAGR Forecast (%) | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Smart-home device explosion | +2.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| BYOD and hybrid work models | +2.1% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Video-streaming quality race | +1.9% | Global, with North American lead | Short term (≤ 2 years) |

| Wi-Fi 7 upgrade cycle pull-through | +1.7% | Early adoption in North America and EU | Medium term (2-4 years) |

| Work-from-anywhere outdoor coverage | +1.4% | North America and EU, selective APAC | Medium term (2-4 years) |

| Mandatory in-building Wi-Fi codes | +0.8% | Primarily EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Smart-home Device Explosion

Annual shipments of 4.1 billion Wi-Fi devices in 2024 pushed the installed base to 21.1 billion and overloaded single-router footprints.[1]Wi-Fi Alliance, “Annual Wi-Fi Shipments Reach 4.1 Billion Units,” wi-fi.org Multi-story homes, thick walls and growing IoT ecosystems force households to add extenders for consistent automation and security performance. Corporate facilities mirror this density, requiring blanket coverage for sensor-driven building-management systems. As user experience degrades when latency spikes, both homeowners and enterprises allocate incremental budgets to coverage extension solutions.

BYOD and Hybrid Work Models

Hospitality chain Mitchells & Butlers installed 8,000 access points across 1,700 UK venues, underscoring how hybrid labor and guest expectations broaden Wi-Fi footprints.[2]Cisco Systems, “Mitchells & Butlers Modernizes UK Hospitality Wi-Fi,” cisco.co Finance and healthcare firms face regulatory imperatives for secure mobile access, driving demand for professionally managed extenders and access points in re-purposed or temporary spaces that lack structured cabling.

Video-streaming Quality Race

European field tests show Wi-Fi 7 median download rates of 565.80 Mbps—a 78% jump over Wi-Fi 6—and hotels upgrading to newer gear report fewer connectivity complaints. Consumer tolerance for buffering is fading as 4K/8K content and interactive gaming gain ground, compelling venues and employers to eliminate dead zones through targeted range extension.

Wi-Fi 7 Upgrade Cycle Pull-through

Taiwanese chipmakers cite Wi-Fi 7 demand as a 2025 revenue stabilizer, and NETGEAR attributes recent U.S. and EU share gains to its premium Wi-Fi 7 portfolio. Because Wi-Fi 7’s multi-link operation only shines when every hop is upgraded, firms must refresh both primary routers and secondary extenders, enlarging the total hardware bill of materials.

Restraints Impact Analysis*

| Restraint | (~) Impact on CAGR Forecast (%) | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mesh-Wi-Fi cannibalization | –1.8% | Global, strongest in North America | Short term (≤ 2 years) |

| Cyber-security and privacy fears | –1.2% | EU and North America | Medium term (2-4 years) |

| Energy-efficiency compliance costs | –0.9% | EU first, global later | Long term (≥ 4 years) |

| Antitrust scrutiny on leading vendors | –0.7% | North America focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mesh-Wi-Fi Cannibalisation

TP-Link’s new Wi-Fi 7 mesh kits “democratize” seamless roaming and real-time management, eroding the value proposition of single-node extenders.[3]TP-Link, “Wi-Fi 7 Mesh Product Launch,” tp-link.comEnterprises favor mesh for unified control while mass-market advertising stresses plug-and-play benefits, accelerating category blurring and price compression.

Cyber-security and Privacy Fears

High-profile flaws such as CVE-2023-52160 and CVE-2023-52161, documented in the MITRE database, demonstrate how attackers can bypass WPA2/3 protections. The EU’s EN 18031 security rules taking effect in August 2025 force vendors to certify hardened firmware, extending product-development cycles and increasing BoM costs.[4]MITRE, “CVE-2023-52160 and CVE-2023-52161,” cve.mitre.org

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Outdoor Deployments Drive Infrastructure Expansion

Outdoor deployments are growing at a 12.94% CAGR through 2031, reflecting municipal Wi-Fi and campus-wide coverage projects, yet indoor installs still account for 70.35% of the Wi-Fi range extender market size in 2025. Stadiums and transport hubs increasingly demand ruggedized extenders with directional antennas to manage dense crowds. The indoor segment’s scale continues to anchor revenue, but volume growth is plateauing as many homes already own at least one extender. Smart-home adoption in emerging markets provides residual tailwinds, and retrofit demand spikes when families add connected security or entertainment gadgets.

Municipal projects under the WiFi4EU banner and city safety networks across France and Denmark favor weather-sealed Wi-Fi 6 and Wi-Fi 7 units, broadening supplier opportunities. Vendors with environmental-hardening expertise therefore gain traction. In contrast, indoor refresh cycles hinge on cost-effective Wi-Fi 5 or Wi-Fi 6 upgrades, sustaining legacy chip demand.

By Product: Access Points Gain Enterprise Traction

Extenders and repeaters retained 53.25% revenue leadership in 2025, yet enterprise migrations toward controller-based architectures are pushing access points at a 16.12% CAGR. Businesses appreciate remote firmware orchestration and role-based access security embedded in AP-centric designs. Consumer channels, however, favor plug-and-play repeaters for quick fixes.

Retailer Conforama Switzerland adopted Aruba WLAN solutions to streamline omnichannel inventory checks, illustrating how centralized AP management reduces operational friction. Conversely, mid-priced repeaters remain preferred in apartments where tenants cannot install Ethernet backhaul. Hybrid portfolios that couple APs with mesh satellites help vendors address both camps, keeping the Wi-Fi range extender market diversified.

By Technology Standard: Wi-Fi 5 Resilience Surprises

Wi-Fi 6/6E devices commanded a 47.35% share in 2025, but Wi-Fi 5 shipments are still climbing 13.78% annually among cost-sensitive buyers, underlining how price trumps peak throughput in segments with limited broadband speeds. Supply chain delays for advanced chipsets spur some enterprises to leapfrog Wi-Fi 6E and plan direct Wi-Fi 7 roll-outs once gear is broadly available.

Europe leads early Wi-Fi 7 adoption, delivering 78% faster throughput than Wi-Fi 6 and enhancing multi-gigabit fiber differentiation. Vendors that manage SKU complexity across three generations can service both upgrade laggards and cutting-edge adopters, maintaining resilience across economic cycles.

By End User: Municipal Sector Emerges

Residential users contributed 62.10% revenue in 2025, but public and municipal projects are compounding at 15.32% as governments pursue digital-inclusion mandates. Ecuador’s Telconet deployed 1,700 Huawei Wi-Fi 6 access points for a nationwide “Wi-Fi for All” program, evidencing policy-led demand.

Large campuses and SMEs continue to add capacity to support hybrid work. Education boards, transit agencies and healthcare trusts increasingly bundle Wi-Fi obligations into tender documents, signaling sustained momentum for municipal orders over the next five years in the Wi-Fi range extender market.

By Sales Channel: Online Dominance Continues

E-commerce captured 51.40% revenue in 2025 and is scaling at 12.08% annually, propelled by transparent pricing and doorstep delivery. Small firms, once reliant on VARs, now self-install extenders ordered directly from brand stores or marketplaces. Subscription-based management add-ons from NETGEAR are generating USD 35 million recurring revenue and anchoring brand stickiness.

Brick-and-mortar retailers still resonate with buyers needing same-day replacement or tactile evaluation, particularly during holiday seasons. B2B integrators specialize in multi-site roll-outs with ongoing SLAs, retaining relevance for mission-critical enterprise deployments.

Geography Analysis

North America retained 39.45% revenue share in 2025, building on mature broadband penetration and early smart-home uptake. Growth is moderating as saturation sets in, yet hybrid-work adoption and extensive single-family housing sustain replacement cycles. Canada’s rural broadband subsidies and Mexico’s digital-inclusion grants continue to lift volume. U.S. regulatory scrutiny, exemplified by the TP-Link antitrust probe, may re-shape competitive dynamics but is unlikely to dent overall demand given ingrained dependence on wireless connectivity.

Asia Pacific is the fastest-growing region with a 13.32% CAGR through 2031. China’s near-universal fiber-to-the-home creates high expectations for in-unit Wi-Fi, yet structural barriers such as thick concrete walls constrain signal propagation, boosting extender sales. India’s Smart Cities Mission and rapid smartphone adoption propel municipal Wi-Fi projects, while Japan and South Korea spearhead Wi-Fi 7 enterprise pilots focused on factory automation and immersive media. The diversity of economic stages requires suppliers to offer both entry-level Wi-Fi 5 and flagship Wi-Fi 7 skus.

Europe blends advanced regulation with moderate volume growth. Energy-efficiency and cybersecurity rules raise compliance costs but erect entry barriers that benefit incumbents. France posts the world’s highest Wi-Fi 7 deployment density, translating fiber speed leadership into user-experience differentiation. Germany and the UK emphasize secure enterprise WLANs for Industry 4.0 and financial services, generating steady refresh cycles. EU subsidies such as WiFi4EU remain a cornerstone of rural and municipal roll-outs, ensuring durable public-sector demand.

Regulatory Landscape

Regulation for Wi-Fi range extenders is tied to radio approvals for unlicensed spectrum, with product design increasingly shaped by cybersecurity and energy-efficiency requirements. In North America, 6 GHz RLAN operation (5925 to 7125 MHz) is governed under FCC Part 15.407, supported by specific test guidance such as FCC KDB 987594, which affects how Wi-Fi 6E and Wi-Fi 7 extender SKUs are certified and labeled for sale. Europe uses ETSI-led harmonization for Wi-Fi 6E in the lower 6 GHz band (5945 to 6425 MHz), with ETSI EN 303 687 applied as a harmonized compliance standard for relevant devices.

India also shows how quickly national spectrum parameters can reshape addressable product configurations. In January 2026, the Department of Telecommunications, WPC issued G.S.R. 47(E), defining technical parameters and limits for equipment operating in 2.4 GHz, 5 GHz, and 6 GHz bands. At the same time, market access and channel decisions are influenced by security-linked restrictions, including the FCC Covered List for equipment and services considered national-security risks, which raises scrutiny of certain foreign-made consumer networking products and can change distributor and ISP procurement behavior.

Value Chain Analysis

The value chain covers chipset and RF front-end supply (Wi-Fi SoCs, memory, power management, and RF components such as filters), device design and firmware development, outsourced manufacturing/PCBA, certification (FCC/ETSI and country-specific approvals), and finally omnichannel distribution (e-commerce, retail, and B2B/ISP/integrator routes), with after-sale software and subscription services layered on top. For many consumer brands, contract manufacturing is a core model, while compliance testing for 6 GHz operation and additional security hardening add schedule risk and cost ahead of scaled shipments.

In 2025-2026, execution risk centers on component availability and compliance-driven change control. PCBA lead times for dual-certified Wi-Fi 7 and Matter boards in Southeast Asia reportedly extended to about 16 weeks as RF calibration capacity and certification queues tightened. Memory and substrate constraints also triggered operational workarounds, including AT&T seeking FCC waivers (May 2026) to support incremental hardware changes on certified router models. Limited concentration in specialized RF parts (such as BAW filters from a small set of suppliers), together with heightened restrictions on certain foreign-made networking equipment, can force redesigns and manufacturing shifts, and those ripple into extender availability and pricing.

Competitive Landscape

Market leadership is shared by a handful of global brands, yet category boundaries blur as mesh systems converge with traditional extenders. Scale players leverage economies in chipset procurement and cross-segment R&D, while challengers carve niches in ruggedized or ISP-bundled hardware. Software and subscription layers are becoming decisive differentiators, turning one-off device sales into multi-year service relationships.

Early Wi-Fi 7 certifications confer temporary pricing power; however, standardization spreads performance parity, refocusing competition on firmware security, energy-efficiency and channel partnerships. Regulatory probes add uncertainty: TP-Link’s investigation may spur distributors to diversify vendors, opening windows for ASUS, D-Link and regional specialists. Component shortages experienced in 2024 have accelerated vertical integration strategies as vendors move design and testing in-house to control timelines.

Mesh cannibalisation pressures extenders at the low end, yet hybrid systems that mix mesh nodes with standalone repeaters appeal to price-conscious buyers upgrading incrementally. Enterprise interest in cloud-managed access points—exemplified by Aruba and Cisco Meraki—shifts margins toward software subscriptions, compelling pure-hardware vendors to rethink roadmaps. Overall, the Wi-Fi range extender market is evolving into a broader managed-connectivity ecosystem rather than a discrete hardware niche.

Wi-Fi Range Extender Industry Leaders

D-Link Corporation

Linksys Group Inc.

TP-Link Technologies Co. Ltd

NETGEAR Inc.

Huawei Technologies Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Wi-Fi 7 provides a clear replacement and upgrade wedge for range extension, since the practical benefit of multi-link operation and wider channel capabilities depends on secondary nodes and extenders being upgraded alongside primary equipment. IEEE 802.11be was formally published in June 2025, and the Wi-Fi Alliance expanded Wi-Fi Certified 7 at CES 2026, including a program for devices restricted to 20 MHz channels. That broadens the set of certifiable endpoint types, creating room for premium extenders as well as smaller-footprint, lower-power range-extension nodes designed around constrained spectrum and channel profiles.

High-density venues and managed enterprise WLAN rollouts are also an immediate whitespace where extenders, access points, and hybrid mesh-plus-extender architectures are deployed together to remove dead zones without full recabling. Extreme Networks deployed a Wi-Fi 7 network at the University of Florida Ben Hill Griffin Stadium in May 2026 to support very high concurrent user density, and that reinforces demand for complementary coverage-extension hardware at the edge of seating bowls, concourses, and back-of-house areas. At the same time, mesh networking continues to compress the standalone extender proposition at the low end, shifting opportunity toward differentiated segments such as ruggedized outdoor units for municipal projects, cloud-managed add-ons, and compliance-ready SKUs tuned to region-specific 6 GHz allocations and security rules.

Recent Industry Developments

- June 2026: NETGEAR announced NETGEAR Align, an AV platform layer that consolidates infrastructure services, with an Align Controller (GB406) planned to ship in August 2026. The move expands NETGEAR's presence in managed connectivity workflows where stable, extended Wi-Fi coverage is deployed alongside switching and control software in venues and enterprise environments.

- May 2026: TP-Link India commenced local manufacturing of the Wi-Fi 7 Omada EAP770 enterprise access point in India after national 6 GHz parameters were clarified by the Department of Telecommunications, WPC earlier in 2026. Local output supports faster fulfillment for managed Wi-Fi deployments that often include access points plus range-extension nodes to cover retrofit sites and multi-building campuses.

- May 2025: The European Commission implemented revised energy-efficiency limits on standby power for routers and extenders, targeting EUR 530 million in annual consumer savings by 2030 and 1.4 million tonnes of CO2 reductions. The rule increases the premium on efficient power design and compliance testing, affecting product refresh timing and favoring vendors with compliant portfolios across multiple regional SKUs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenue from Wi-Fi range extenders used to improve wireless coverage by receiving a Wi-Fi signal and re-broadcasting it to reduce dead zones in indoor spaces and in selected outdoor settings.

Scope exclusions: standalone Wi-Fi routers, gateways, and mesh router systems are excluded when they are sold mainly as primary networking equipment rather than as range extension devices.

Segmentation Overview

- By Type

- Indoor Wi-Fi

- Outdoor Wi-Fi

- By Product

- Extenders and Repeaters

- Access Points

- Powerline/Wi-Fi Combo Units

- High-gain Antennas

- By Technology Standard

- Wi-Fi 5 (802.11ac)

- Wi-Fi 6 / 6E (802.11ax)

- Wi-Fi 7 (802.11be)

- By End User

- Residential

- Small and Medium Enterprises

- Large Enterprises and Campuses

- Public and Municipal

- By Sales Channel

- Online (e-commerce, D2C)

- Offline Retail

- B2B/Enterprise Integrators

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Asia Pacific

- China

- India

- Japan

- South Korea

- ASEAN

- Rest of Asia Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts with building a clean view of device shipments, installed base indicators, and household and enterprise connectivity trends that drive demand for range extension hardware. We typically refer to public sources such as the FCC equipment authorization database, IEEE 802.11 standards publications, the US Census and American Community Survey, ITU connectivity statistics, and OECD broadband indicators to anchor adoption and upgrade cycles.

To translate these signals into usable assumptions, we also review company annual reports, product specification sheets, and investor presentations to understand price bands, launch timing, and channel mix. Supporting context is taken from association and retailer category pages, plus credible press coverage on Wi-Fi 6, Wi-Fi 6E, and the early Wi-Fi 7 transition. Where needed, we use paid subscriptions for company financials and intelligence, patent lookups, and shipment-level import and export checks to confirm directional trends. The desk sources listed here are illustrative, and we use additional public references to fill gaps and validate findings.

Primary Interviews and Surveys

Primary interviews and surveys are used to pressure-test the desk assumptions around attach rates, replacement timing, average selling prices, and whether mesh nodes are bought mainly for extension versus full-home routing. We speak with channel participants, product and category managers, installers, and enterprise IT staff across key regions, so the final model reflects real purchase behavior and not only shipped units.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 20% | APAC: 40% |

| Mid tier: 42% | Functional/Unit leaders: 24% | EMEA: 34% |

| Smaller Players: 20% | Managers: 56% | Americas: 26% |

Market-Sizing & Forecasting

Sizing begins with a top-down build, where broadband households, connected device density per home, and Wi-Fi performance expectations are used to reconstruct the demand pool that typically leads to extender purchases. We then map those totals into likely unit demand by region, using indicators such as router upgrade cycles, penetration of multi-story housing, share of remote work setups, and the mix of single-band versus dual-band and tri-band installs.

To keep the model grounded, we cross-check results with selective bottom-up approximations, including sampled channel price points, public shipment trends, and a supplier and distributor roll-up for a limited set of representative geographies. We adjust the model when gaps appear. Pricing is handled carefully because promotions can shift realized ASPs, so we use an ASP band approach that is refreshed with channel checks and product launch tracking. Forecasting uses scenario analysis backed by expert consensus on upgrade timing for Wi-Fi 6E and early Wi-Fi 7, along with expected normalization in consumer electronics spending and small office refresh activity.

Data Validation & Update Cycle

Outputs are validated through multiple checks, including comparing implied units, ASPs, and growth rates against independent signals such as broadband additions, home networking category momentum, and trade flow direction where applicable. If a variance is unusually high in a country or year, assumptions are re-checked and, if needed, we re-contact respondents to clarify the driver before the numbers move forward.

A second analyst review is completed to ensure definitions are applied consistently and that regional totals reconcile to the global figure. Reports are refreshed annually, and interim updates are made when material events occur, such as major standard transitions or large channel disruptions. Before delivery, a final pass is done so clients receive the latest view based on the newest public releases and the most recent validation notes.

Mordor Intelligence's Wi Fi Range Extender Market Size Versus Other Published Estimates

Published market sizes for Wi-Fi range extenders often vary because the product boundary can be interpreted differently, and because pricing and upgrade cycles are not treated the same across models. Differences also come from the year selected as the anchor point, currency conversion timing, and whether forecast paths assume a steady upgrade wave or a more stepwise refresh.

The table shows a tight cluster in the 2025 starting point. In Mordor Intelligence's model, the value is tied to purpose-built range extender devices, including plug-in repeaters, desktop extenders, and mesh nodes marketed for extension, while excluding primary routers and gateways to reduce double counting. Some other estimates appear to include a wider home networking hardware bucket or apply a higher assumed ASP progression across Wi-Fi 6E and Wi-Fi 7 cycles, which can lift the base value and the forward curve.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.91 B (2025) | |

| Global Consultancy A | USD 2.92 B (2025) | Uses a broader type list that can blend outdoor extenders and mesh extender variants without consistently separating nodes bought mainly for extension versus full-home systems, which can change the counted revenue base. |

| Industry Publisher B | USD 3.80 B (2024) | Anchors on a 2024 base year and appears to apply a wider Wi-Fi extender definition with faster ASP uplift assumptions, which can inflate the starting value compared with a device-only scope. |

Looking across the three numbers, most of the spread can be explained by how mesh-related hardware is classified, how ASP changes are modeled through new standard transitions, and whether the base year is 2024 or 2025. By keeping the inputs tied to observable adoption signals and then re-checking them through interviews, the estimate remains traceable to clear demand drivers and can be repeated when new public data is released.

Key Questions Answered in the Report

What is the current size of the Wi-Fi range extender market?

The Wi-Fi range extender market size stands at USD 3.24 billion in 2026 and is projected to reach USD 5.51 billion by 2031.

Which segment is growing fastest?

Outdoor deployments are advancing at a 12.94% CAGR as municipalities and campuses extend coverage to open spaces.

How will Wi-Fi 7 affect demand?

Because Wi-Fi 7’s benefits only materialize when entire networks are upgraded, organizations will need new extenders and mesh nodes, fueling incremental hardware spending.

Why are mesh systems seen as a threat to extenders?

Mesh kits bundle multiple intelligent nodes that auto-optimize roaming, often replacing single-purpose extenders and pressuring prices.

What regulations most influence product design in 2025?

The EU’s Radio Equipment Directive cybersecurity clause and tougher standby energy limits compel manufacturers to redesign firmware and power architectures.

Who are the leading vendors?

TP-Link, NETGEAR and Huawei collectively capture 38% Wi-Fi range extender market share, while ASUS, D-Link and Linksys round out the competitive top tier.

Page last updated on: