Cloud Radio Access Network Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

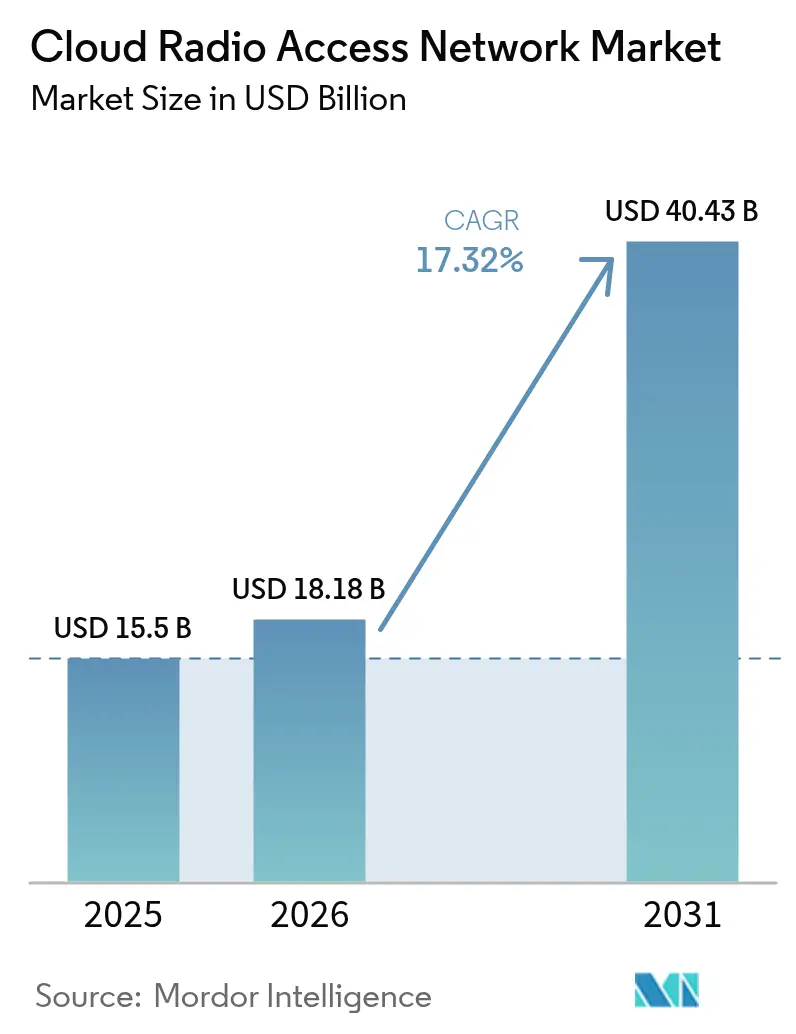

| Market Size (2026) | USD 18.18 Billion |

| Market Size (2031) | USD 40.43 Billion |

| Growth Rate (2026 - 2031) | 17.32% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cloud Radio Access Network Market Analysis by Mordor Intelligence

The Cloud Radio Access Network market size is expected to grow from USD 15.5 billion in 2025 to USD 18.18 billion in 2026 and is forecast to reach USD 40.43 billion by 2031 at 17.32% CAGR over 2026-2031.

Rapid 5G rollouts, the push for centralized baseband processing, and mounting pressure to trim network operating costs keep demand high. Operators are mapping out multi-layer coverage strategies in dense urban clusters, where pooling resources in the cloud has begun lifting cell-site throughput and spectrum utilization. Commercial proofs in the United States, Japan, and leading European capitals also indicate that AI-assisted scheduling can cut power draw across active radios, supporting sustainability targets alongside network modernization. Competition is intensifying as incumbent vendors defend their share against software-centric entrants, prompting a wave of partnerships that combine radio, compute, and silicon expertise to accelerate product road maps. While the cloud radio access network market benefits from supportive policy incentives, it still faces headwinds linked to spectrum release timetables and fronthaul bottlenecks that vary sharply by country.

Key Report Takeaways

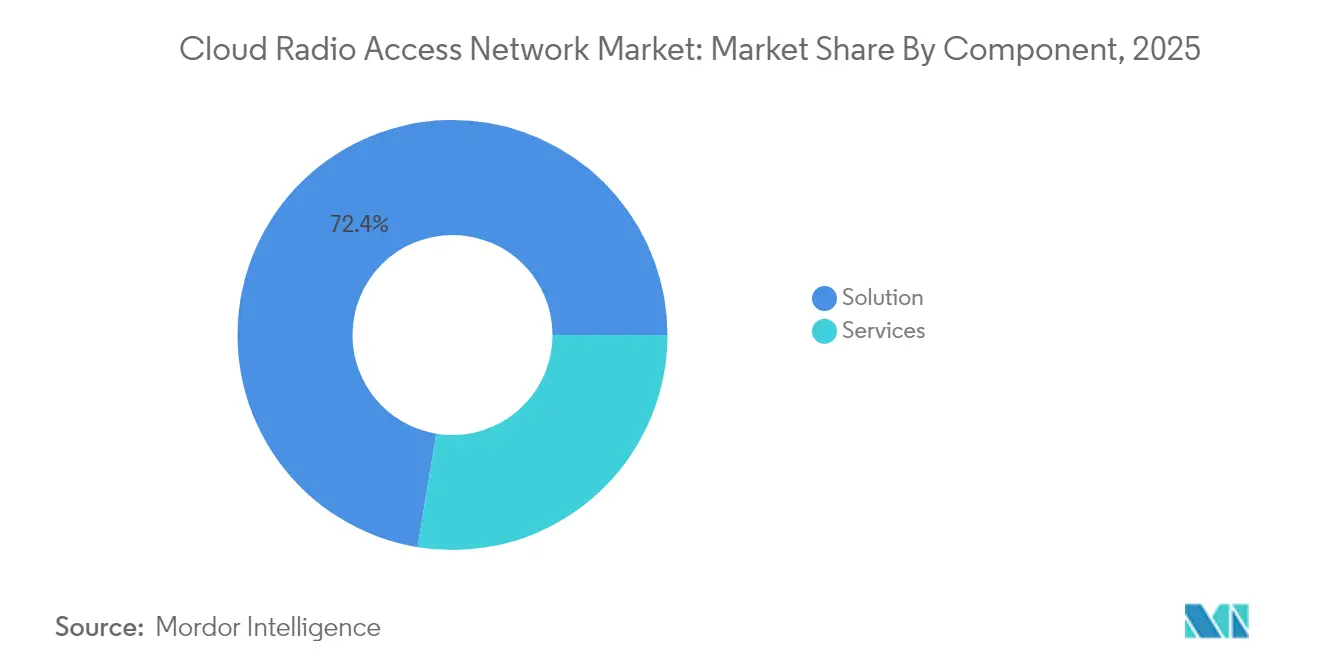

- By component, Solutions commanded 72.40% of the cloud radio access network market share in 2025, whereas Services are on track for the fastest 18.02% CAGR through 2031.

- By network type, 5G carried 61.80% revenue share in 2025; Open RAN is projected to expand at a 26.4% CAGR, topping segment growth.

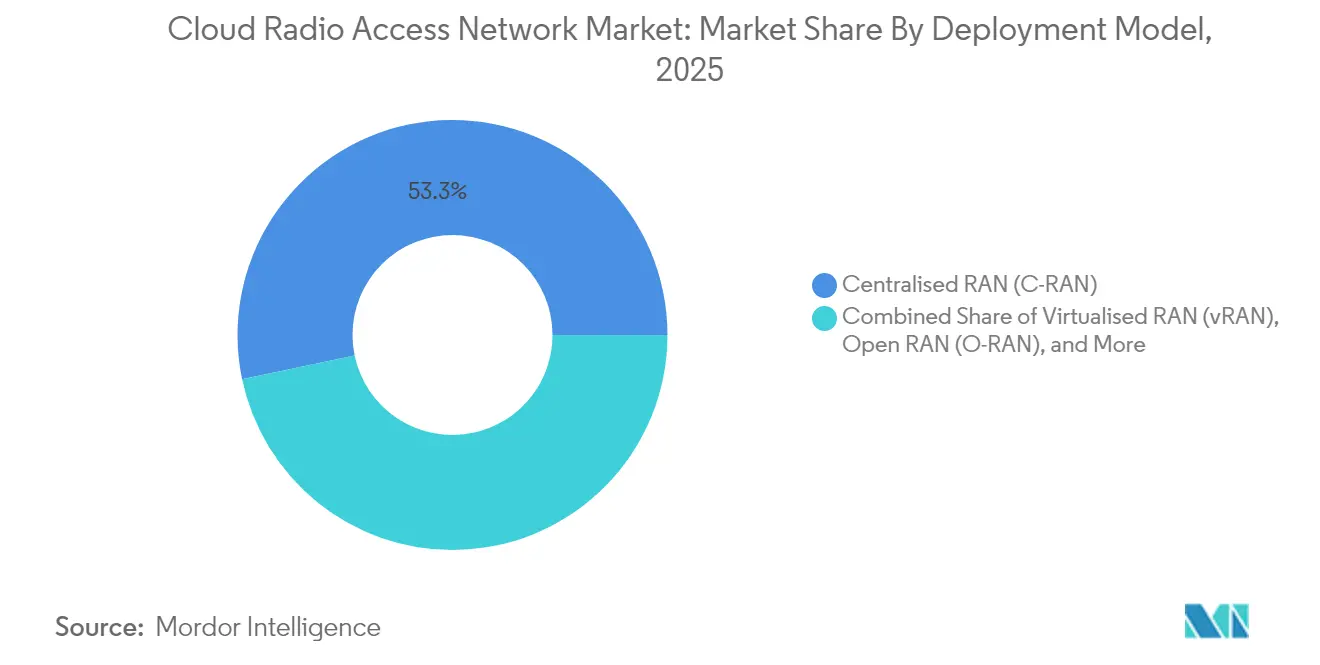

- By deployment model, Centralised RAN held 53.30% of the cloud radio access network market size in 2025, while Open RAN leads future growth at 26.4% CAGR.

- By end user, Mobile Network Operators accounted for 66.20% share in 2025, yet Enterprise networks are set to rise at a 18.93% CAGR.

- By geography, Asia Pacific captured 38.60% of the cloud radio access network market in 2025 and also shows the steepest 22.4% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cloud Radio Access Network Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G rollouts and densification | +5.20% | Global, highest in Asia Pacific and North America | Medium term (2-4 years) |

| CAPEX and OPEX savings from a centralized baseband | +3.80% | Global | Short term (≤ 2 years) |

| Surging mobile-data traffic | +4.10% | Global, acute in metropolitan hubs | Medium term (2-4 years) |

| Network virtualization and SDN adoption | +2.90% | North America, Europe, advanced Asia Pacific markets | Medium term (2-4 years) |

| AI-driven RAN optimization adoption (under-the-radar) | +2.3% | North America, Europe, China, Japan, South Korea | Long term (≥ 4 years) |

| Energy-efficiency regulations push cloud RAN (under-the-radar) | +1.8% | Europe, North America, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid 5G Rollouts and Densification Drive Architectural Change

Global operators are lighting up mid-band 5G layers and adding small cells to fill coverage gaps. In this environment, the cloud radio access network market delivers the centralized compute pools needed to manage thousands of radios without duplicating hardware. Field trials in Tokyo, Seoul, and New York show that dynamically shifting baseband workloads can raise utilisation by 30% and boost peak cell throughput by 25%. Commercial 5G standalone cores are now coordinating time-sensitive scheduling with virtual baseband functions, underscoring how cloud-native principles shorten feature release cycles. Large-scale deployments in China and the United States reveal that the same cloud site can host multiple radio generations, easing spectrum-refarming decisions and supporting progressive migration paths. These advantages spur continued investment, particularly where indoor coverage obligations require dense radio grids.

CAPEX and OPEX Savings Sustain the Business Case

The economic attraction of virtualized baseband pools is immediate: pooling reduces hardware duplication, trims real-estate expense, and simplifies upgrades. Vendor case studies from North America indicate that operators consolidating three legacy baseband types into a single cloud cluster recorded CAPEX cuts nearing one-third during year-one rollouts. OPEX declines follow as automation tools scale preventive maintenance and remote software updates. Energy bills fall when AI schedulers place lightly loaded radios in deep-sleep modes during off-peak periods, improving the network’s power-efficiency profile. These savings underpin aggressive 5G expansion plans, especially for carriers balancing dividend commitments with the need to enhance the quality of service. As consumption-based pricing models for public cloud gain traction, operators gain added flexibility to align spending with traffic peaks, reinforcing the appeal of cloud architecture.

Exponential Mobile-Data Growth Necessitates Architectural Innovation

Ericsson projects 6.3 billion 5G subscriptions by 2030, with 5G accounting for 80% of total mobile traffic[1]Ericsson, “Mobility Report Q4 2024,” ericsson.com. This volume strains traditionally distributed RAN layouts, where baseband resources sit idle during demand lulls yet max out during peak events. The cloud radio access network market responds by shifting processing to central locations, allowing resource pooling across dozens of cell sites. Operators in Singapore and Stockholm reported a 20-30% uplink throughput lift after activating coordinated interference-management features enabled by pooled compute. Centralization further simplifies multi-band carrier aggregation, supporting video streaming and emerging XR services that escalate bandwidth requirements. As mobile-first economies pivot toward immersive applications, cloud RAN stands out as a scalable answer to unpredictable traffic bursts.

Network Virtualization and SDN Adoption Reshape Strategies

Core networks already run on cloud-native stacks, making the radio layer the next logical step toward full end-to-end elasticity. The O-RAN ALLIANCE confirms that most tier-one operators now operate virtualized RAN pilot clusters or early commercial sites[2]O-RAN ALLIANCE, “Operator Survey 2025,” o-ran.org. Integrating RAN with broader SDN control frameworks lets engineering teams modify slicing policies in near real time, matching latency profiles to enterprise service-level agreements. Vendors have begun shipping containerized baseband functions deployable on generic servers, which harmonizes supply chains and lowers dependence on proprietary hardware. Early movers report that DevOps-style pipelines shorten software release lead times from quarters to weeks. Together, these factors support an ecosystem shift towards open interfaces, giving buyers greater bargaining power and stimulating healthy supplier competition across the cloud radio access network market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spectrum scarcity & regulatory limits | -2.70% | Global, with higher impact in developing markets | Medium term (2-4 years) |

| Limited fronthaul fibre & latency challenges | -3.10% | Emerging markets, rural areas in developed markets | Short term (≤ 2 years) |

| Security & privacy risks in centralised architecture (mainstream) | -2.4% | North America, Europe, enterprise segments globally | Medium term (2-4 years) |

| Uncertain ROI in emerging markets (under-the-radar) | -1.8% | Latin America, Africa, Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Spectrum Scarcity and Regulatory Limits Dent Momentum

Timely clearance and auction of mid-band spectrum remains a gating factor for nationwide 5G builds. The expiry of auction authority at the United States Federal Communications Commission in 2024 introduced uncertainty around future releases, slowing some carrier investment cycles[3]Federal Communications Commission, “2024 Communications Marketplace Report,” fcc.gov. Many emerging markets also grapple with opaque or politically driven allocation processes that delay turnkey deployment of 5G layers optimized for cloud RAN. Even where licenses are in place, guard-band conditions and power-level caps can restrict network layouts, forcing operators to rely on fragmented holdings that complicate radio planning. These realities moderate roll-out velocity and can postpone the point when pooling economics become compelling.

Limited Fronthaul Fibre and Latency Challenges Constrain Deployment

Centralizing the baseband demands high-capacity, low-latency fronthaul links. In rural North America and parts of Southeast Asia, insufficient fibre density compels operators to retain distributed baseband nodes, diluting pooling advantages. Cisco notes that packetized fronthaul architectures progress best where dark-fibre leases or utility rights-of-way lower trenching costs[4]Cisco Systems, “5G Transport Architecture,” cisco.com. Where fibre reach remains sparse, carriers deploy adaptive compression or higher functional splits that relax latency budgets, but those options reduce some spectral-efficiency gains. Closing the gap will depend on coordinated public-private investment and wholesale neutral-host models that make high-bandwidth links affordable beyond metro cores.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Unlock Value in Complex Deployments

The cloud radio access network market size derived from Solutions hit USD 11.22 billion in 2025, equal to 72.40% of segment revenue. Yet the Services market is expanding faster at an 18.02% CAGR as multi-vendor environments become the norm. Early greenfield installations chiefly required hardware and virtualized baseband licenses, but current brownfield upgrades demand integration, network optimization, and lifecycle support. Operators in Europe are signing multi-year managed-service contracts that bundle AI-driven performance analytics with DevOps enablement, letting internal teams prioritise new-service design. Consulting teams now guide spectrum-refarming, functional-split selection, and migration sequencing, roles critical for incumbent carriers balancing legacy 4G traffic and emerging private 5G use cases. Hardware providers respond by embedding open interfaces and reference automation workflows, blurring the line between product and professional service. In turn, this mix pushes the Services slice to account for a deeper share of the cloud radio access network market revenue pool as 2031 approaches.

A steady flow of innovation keeps the Solutions business vibrant. Silicon majors introduced integrated acceleration for beamforming and forward-error correction, lifting baseband capacity per rack unit by over 2× compared with 2023 blades. Radio suppliers complement these gains with lightweight Massive MIMO arrays tailored for rooftop and indoor settings. Such advancements compress the total cost of ownership while widening the addressable customer base, supporting consistent though moderate revenue growth on the Solutions side. The net result is a balanced landscape where software, silicon, and services each reinforce the transition to centrally orchestrated radio layers, widening adoption across incumbent and enterprise segments of the cloud radio access network market.

By Network Type: 5G Prevails as Open RAN Gains Ground

In 2025, the 5G tier commanded 61.80% of the overall cloud radio access network market revenue as carriers devoted capital to harness mid-band spectrum. Operators pivoted quickly to standalone architectures, which permit slicing and ultra-low-latency pipelines critical for Industry 4.0 workloads. Virtualized baseband pools make it feasible to run non-standalone 5G, LTE, and NR on common servers, letting carriers phase out 3G in favor of capacity upgrades. While 4G LTE still generates meaningful returns, its share declines each year as data-heavy consumer usage gravitates toward 5G bundles with subsidized devices.

Open RAN exhibits the fastest trajectory at a 26.4% CAGR through 2031, buoyed by high-profile commitments from North American and Asian tier-ones keen to diversify supply chains. The model’s open interfaces encourage best-of-breed combinations, but integration overhead remains considerable. Nevertheless, pilot results from live networks in Dallas and Seoul show that multi-vendor Massive MIMO stacks can reach spectral-efficiency parity with monolithic systems when orchestrated from a unified cloud platform. Regulatory support, such as grant programs from the United States government, offers added momentum. Collectively, these forces position Open RAN as a key disruptor, widening supplier diversity while intensifying competitive dynamics across the cloud radio access network market.

By Deployment Model: Centralised RAN Sets Baseline, Open RAN Accelerates

Centralised RAN retained 53.30% share of the cloud radio access network market size in 2025, reflecting its maturity and ease of integration with existing transport topologies. Many operators adopt staged migration: fibre-rich urban clusters shift first, followed by suburban cells as backhaul upgrades complete. Open RAN deployment, however, brings a fresh cost curve. AT&T’s multiyear programme aims to carry 70% of traffic over open-capable platforms by 2026, anticipating both capital and operating cost relief. Early calculations from carriers in Europe suggest equipment savings above 40% versus proprietary stacks when volume thresholds are met.

Virtualized RAN on commercial off-the-shelf servers runs in parallel, supporting brownfield adaptations where complete openness is not yet feasible. Hybrid cloud RAN appears where fibre or power limits require local processing, blending edge-cloud instances with metro hubs. Orange publicly supports such a flexible stance, citing the need to balance spectrum reform with legacy site contracts. The result is a deployment mosaic that varies by geography, with greenfield entrants like Rakuten Mobile embracing full Open RAN, and incumbents layering virtualisation atop existing macro grids. This pluralism creates sustained spending opportunities along the whole value chain inside the cloud radio access network market.

By End User: Enterprises Energize Demand Beyond Telcos

Mobile Network Operators generated 66.20% of the cloud radio access network market revenue in 2025, but private-wireless expansion lifts enterprise wallet-share quickly. Manufacturers, hospitals, and logistics hubs deploy on-premises 5G cores seated next to cloud RAN nodes to guarantee deterministic performance. These customers value indoor coverage, data sovereignty, and low-latency control loops that Wi-Fi cannot match. With vertical-specific applications emerging, solution providers add pre-integrated security gateways and network-slice templates, reducing setup time and easing IT integration.

Government and public-safety agencies pursue resilient campus coverage, often in partnership with neutral-host tower companies that pool capex across multiple tenant networks. TowerCos views cloud RAN as a lever to host multi-operator traffic without duplicating electronics, widening their services portfolio. This shared-infra model also accelerates rural coverage, a policy priority in many emerging economies. Collectively, these patterns lift the Enterprise CAGR to 18.93%, ensuring that non-telco clients become a central growth pillar for the cloud radio access network market while reinforcing innovation feedback loops into vendor road maps.

Geography Analysis

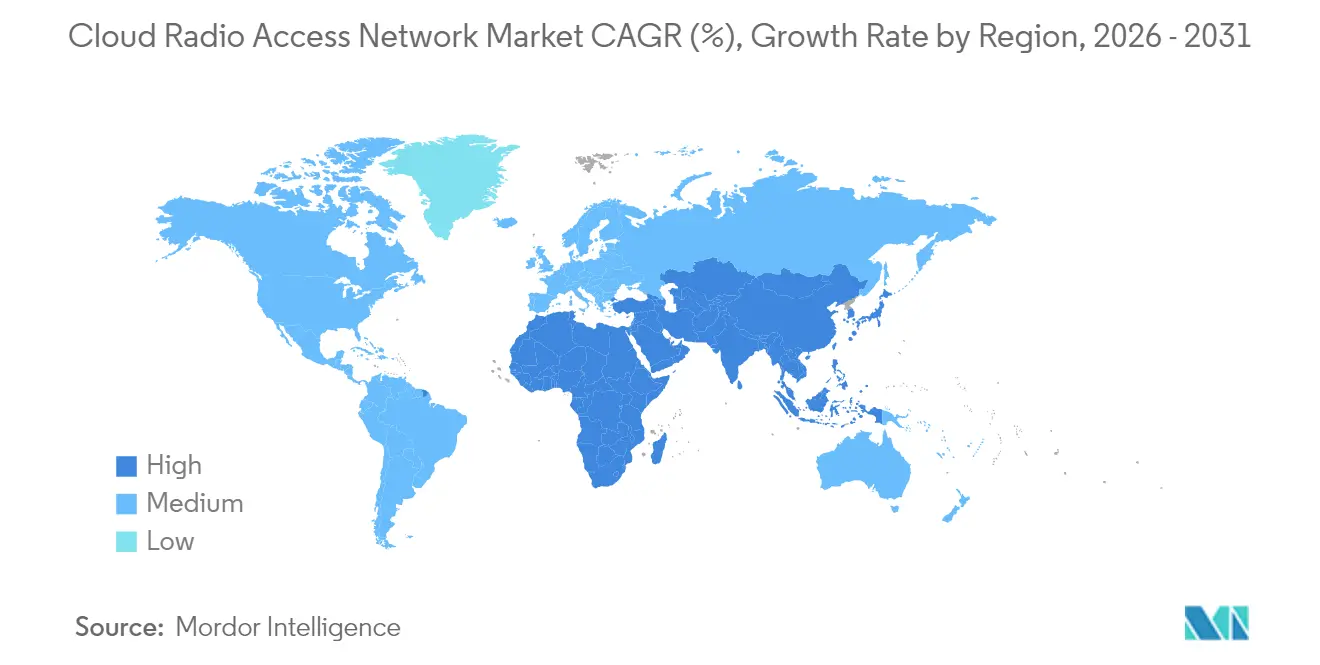

Asia Pacific dominates the cloud radio access network market with 38.60% revenue share in 2025 and leads in growth with a 22.4% CAGR. Aggressive 5G rollouts in China, Japan, and South Korea rely on high-density small-cell grids linked to large regional data centres. Operators in Shenzhen and Seoul already operate commercial open-interface clusters in core business districts, showcasing real-time spectrum pooling for video streaming during peak festivals. Governments provide supportive policy frameworks, such as spectrum fee rebates for virtualisation investments. Vendor ecosystems flourish around open testbeds, and joint ventures like the OREX initiative target export opportunities, cementing the region’s leadership.

North America ranks second in terms of revenue. United States carriers earmarked multibillion-dollar budgets to swap legacy hardware for open-capable radios by 2026. Federal grants under the CHIPS and Science Act co-fund silicon research that empowers AI-based scheduling engines, giving domestic supply chains greater resilience. Early deployments in Las Vegas and Seattle prove that GPU-accelerated cloud nodes can meet stringent millisecond-level latency targets for XR gaming and industrial automation. Canadian operator collaborations with Finnish and Korean vendors extend the regional innovation sphere, highlighting cross-border technology exchange that supports the wider cloud radio access network market.

Europe accelerates adoption through a blend of regulatory mandates and competitive necessity. Operators in the United Kingdom, Germany, and Spain rolled out the first commercial 5G Open RAN macro sites, supported by public test labs that certify interoperability among radios, basebands, and management systems. The European Union dedicates funding tranches to 5G and 6G network R&D, which bolsters an academic–industry pipeline for RAN software talent. Despite lagging standalone 5G coverage, incumbents pursue fast-track plans to cloudify their radio layers, citing lower total cost of ownership and faster service innovation as key motivators. Ongoing infrastructure programs upgrade fibre backbones through rural corridors, which will remove a historic bottleneck and further expand the cloud radio access network market footprint across the region.

Competitive Landscape

The cloud radio access network market shows moderate concentration, with the top five suppliers controlling a majority share outside China. Huawei secures leadership through scale deployments with domestic carriers, reinforcing its stronghold in emerging markets. Ericsson claims a roughly 37% share outside China, winning contracts with tier-one operators in North America and Europe that favour open-interface readiness. Nokia follows at close distance, leveraging broad service portfolios and recent optical-network acquisitions to integrate transport and radio solutions into cohesive packages.

Samsung rises as a strategic challenger by combining in-house silicon with Massive MIMO radios optimized for Open RAN. Its presence in the United States greenfield builds signals broader acceptance of diversifying supply chains. Software innovators Mavenir and Rakuten Symphony target disaggregation layers where value shifts towards orchestration and automation. They differentiate through cloud-native microservices and marketplace models that simplify the onboarding of third-party apps. Partnerships proliferate chipset vendors team with server OEMs, radio makers team with public cloud hyperscalers, and system integrators providing turnkey blueprints for enterprise verticals. AI sits at the heart of many new offers, where inference engines predict traffic loads and adjust power states. The result is a rich field of rivalry, cooperation, and co-opetition that propels ongoing advancement across the cloud radio access network market.

Cloud Radio Access Network Industry Leaders

Cisco System Inc.

Nokia Corporation

Huawei Technologies Co. Ltd.

Telefonaktiebolaget LM Ericsson

Intel Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Ericsson and Telstra unveiled the AIR 3284, the first 5G triple-band FDD Massive MIMO radio aimed at boosting downlink and uplink capacity for Telstra’s nationwide modernization.

- April 2025: Nokia and partners launched an initiative to accelerate AI-powered RAN, focusing on network efficiency gains and performance improvements.

- March 2025: SoftBank Corp. and Ericsson formed a strategic partnership to enhance cloud RAN capabilities and improve network efficiency.

- March 2025: O2 Telefónica activated its first commercial 5G standalone Cloud RAN site in Offenbach, Germany, using Ericsson technology.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the cloud radio access network (C-RAN) market as revenue from software, infrastructure, and managed services that relocate baseband processing to pooled, virtualized, or open cloud resources serving public or private mobile networks. The definition covers centralized, vRAN, and open-RAN variants across 3G, 4G/LTE, and 5G deployments.

Scope exclusion: pure telecom cloud core functions and legacy distributed RAN hardware are not counted.

Segmentation Overview

- By Component

- Solution

- Services

- Professional

- Managed

- By Network Type

- 5G

- 4G

- LTE

- 3G (EDGE)

- By Deployment Model

- Centralised RAN (C-RAN)

- Virtualised RAN (vRAN)

- Open RAN (O-RAN)

- Hybrid Cloud RAN

- By End User

- Mobile Network Operators

- Enterprises

- Government and Public-Safety

- Neutral Host/TowerCos

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- UAE

- Saudi Arabia

- Rest of the Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Detailed Research Methodology and Data Validation

Primary Research

Interviews with mobile operator CTO offices, cloud infrastructure architects, and RAN software suppliers across North America, Europe, and key Asia-Pacific hubs validate unit economics, fronthaul cost trends, and timing assumptions. Short surveys with neutral host tower firms help cross-check emerging indoor coverage demand.

Desk Research

Our analysts review public domain benchmarks such as 3GPP release notes, GSMA deployment trackers, ITU spectrum databases, and filings from national regulators (FCC, Ofcom, TRAI), which clarify spectrum, site, and fiber roll-out trends. Company 10-Ks, vendor road show decks, and operator CAPEX statements enrich pricing and adoption clues. Subscription-only resources, D&B Hoovers for financials and Dow Jones Factiva for deal flow, add numeric depth. Trade associations including the O-RAN Alliance supply technical adoption metrics. The sources listed illustrate the breadth consulted; many more inform data checks throughout the build.

Market-Sizing & Forecasting

A top-down addressable site pool is built from live macro and small cell counts and 5G densification road maps, then multiplied by region-specific virtualization penetration and average software plus service spend. Select bottom-up roll-ups of leading supplier revenues and channel checks adjust totals. Key inputs include: 5G subscriber additions, operator RAN CAPEX ratios, fronthaul fiber availability, average virtual BBUs per site, spectrum renewal schedules, and public cloud instance pricing. Multivariate regression ties market value to the first three variables, with scenario analysis for CAPEX swings. Gap cells where supplier splits are absent are bridged using primary insight-based mark-ups.

Data Validation & Update Cycle

Outputs pass tiered analyst review: variance scans versus historical spend, peer ratios, and price/volume sanity bands. Outliers trigger re-contacts. Models refresh annually, and major spectrum auctions or policy shifts prompt mid-cycle updates so clients receive the latest view.

Why Mordor's Cloud Radio Access Network Baseline Earns Decision-Makers' Confidence

Published figures often diverge because firms mix broader telecom cloud income, apply uniform hardware ASPs, or freeze exchange rates. Mordor's careful scope, live currency conversion, and annual refresh cadence anchor a balanced baseline.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 15.5 B (2025) | Mordor Intelligence | - |

| USD 25.6 B (2025) | Global Consultancy A | Bundles wider wireless infrastructure and assumes single global ASP |

| USD 14.4 B (2025) | Industry Journal B | Uses 2020 price curve unchanged and omits managed service revenue |

The comparison shows that totals inflate when non-RAN cloud segments are blended or deflate when service layers are ignored. By selecting only C-RAN specific spend and validating prices with operators, Mordor Intelligence delivers a transparent, reproducible baseline that strategy teams can trust.

Key Questions Answered in the Report

What is the current size of the cloud radio access network market in 2026?

The market stands at USD 18.18 billion in 2026.

What compound annual growth rate (CAGR) is projected for the cloud radio access network market through 2031?

Analysts forecast a 17.32% CAGR for 2026-2031.

Which region leads the cloud radio access network market, and how fast is it growing?

Asia Pacific holds 38.60% of 2025 revenue and is expanding at a 22.4% CAGR to 2031.

Which network type is expected to grow the fastest within cloud RAN deployments?

Open RAN shows the highest momentum with a 26.4% CAGR projected for 2026-2031.

How much cost relief can operators achieve by adopting cloud RAN architectures?

Independent studies indicate up to 49% first-year CAPEX savings and 31% cumulative OPEX savings over five years versus traditional distributed RAN.

What are the chief hurdles that could slow cloud RAN rollouts?

Spectrum scarcity, regulatory delays, limited fronthaul fiber, and strict latency requirements remain the primary obstacles.

Page last updated on: