Prophylactic HIV Drugs Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 34.75 Billion |

| Market Size (2031) | USD 42.23 Billion |

| Growth Rate (2026 - 2031) | 3.96% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

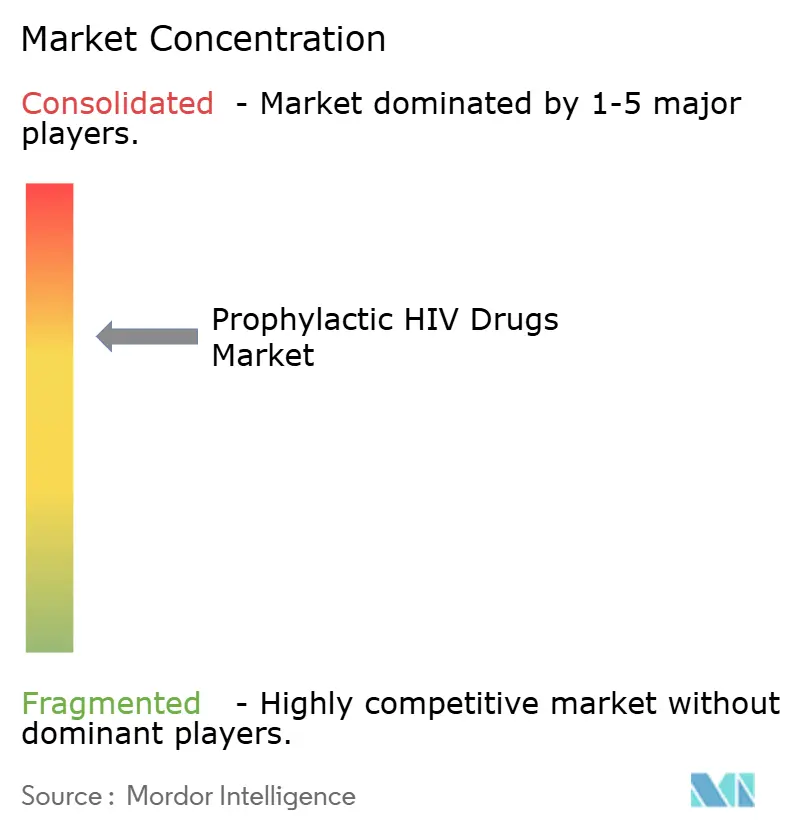

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Prophylactic HIV Drugs Market Analysis by Mordor Intelligence

The prophylactic HIV drugs market size was valued at USD 33.43 billion in 2025 and estimated to grow from USD 34.75 billion in 2026 to reach USD 42.23 billion by 2031, at a CAGR of 3.96% during the forecast period (2026-2031). Growing demand for long acting injectables, rising policy support, and widening digital distribution networks are reshaping the competitive field, while cost pressures tied to generic entry temper margins in mature economies. Innovation momentum remains high: FDA clearance of twice-yearly lenacapavir in June 2025 validates capsid inhibition as a breakthrough prevention class and anchors the fastest-growing dosage-form segment at 7.56% CAGR. North America preserves scale advantages through insurance reimbursement and clinical infrastructure, but Asia-Pacific posts the sharpest volume gains as governments embed PrEP into national AIDS plans and expand telehealth coverage. Across the prophylactic HIV drugs market, differentiation now hinges on dosing convenience, manufacturing partnerships, and value-based pricing models that reconcile R&D returns with equitable access.

Key Report Takeaways

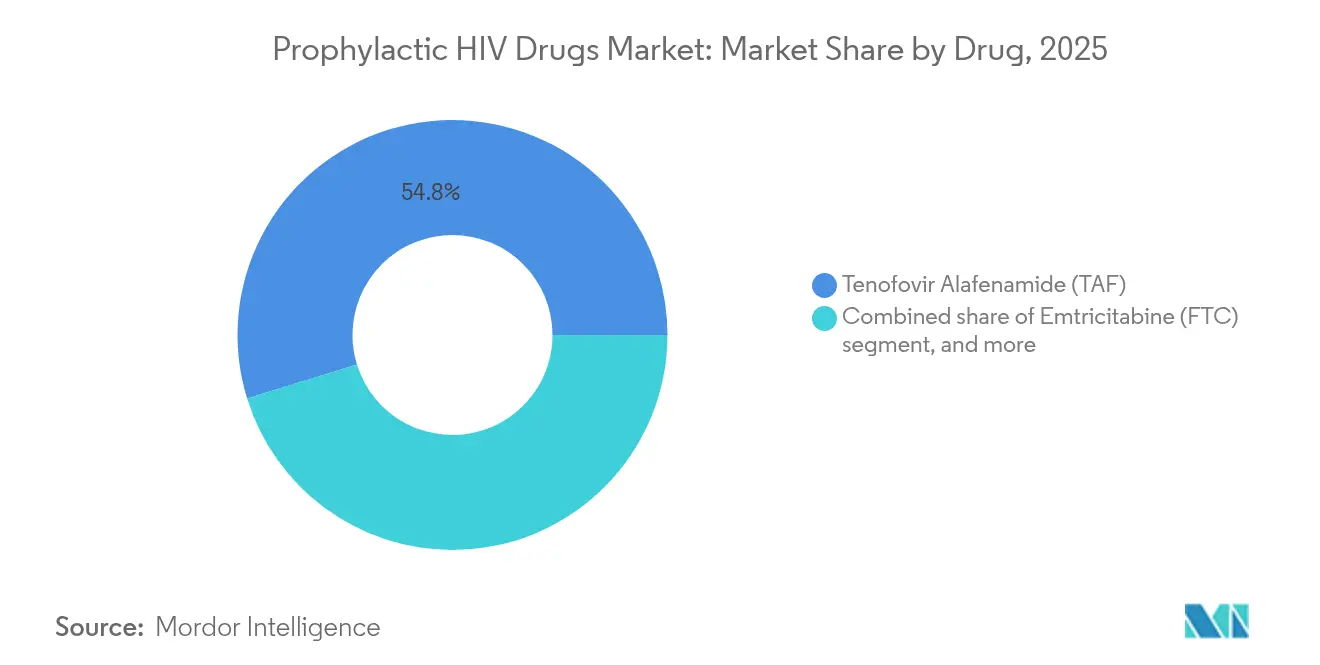

- By drug, Tenofovir Alafenamide led with 54.78% prophylactic HIV drugs market share in 2025, whereas lenacapavir is forecast to achieve the highest CAGR at 6.35% through 2031.

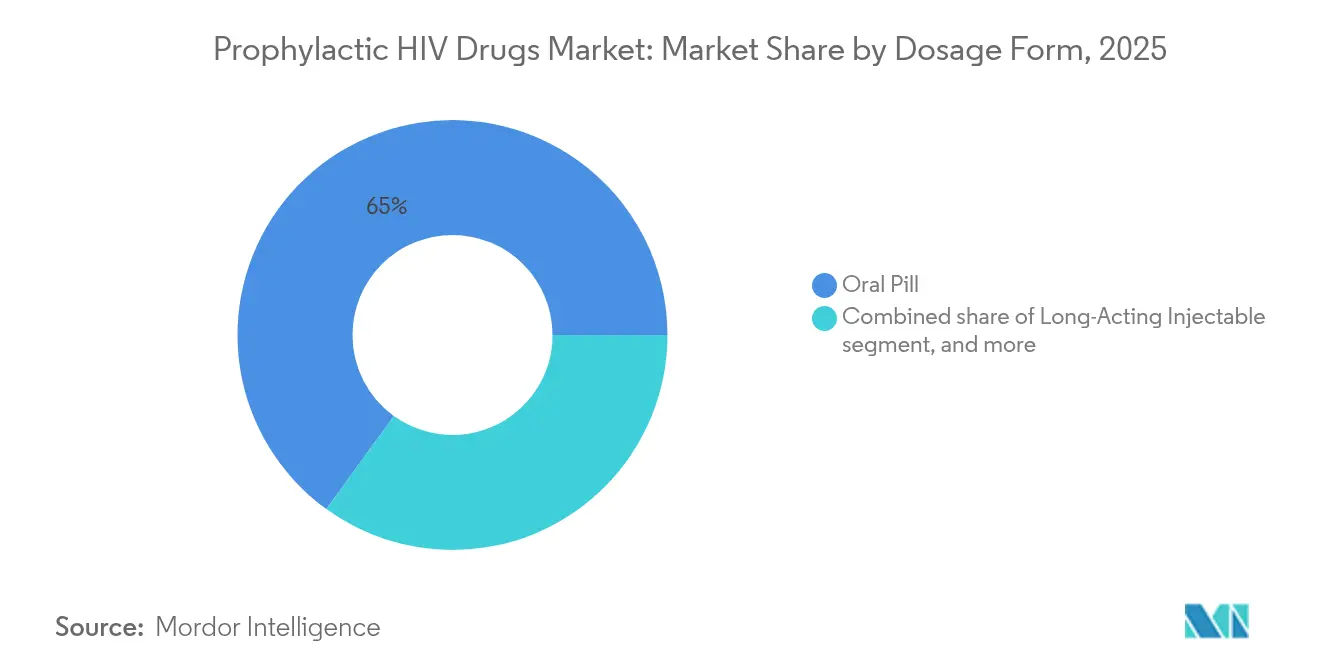

- By dosage form, oral tablets controlled 65.02% of the prophylactic HIV drugs market size in 2025, while long-acting injectables expand at a 7.31% CAGR between 2026 and 2031.

- By distribution channel, hospital pharmacies retained 55.21% revenue share in 2025; online pharmacies and tele-PrEP platforms record the fastest growth at 7.55% CAGR to 2031.

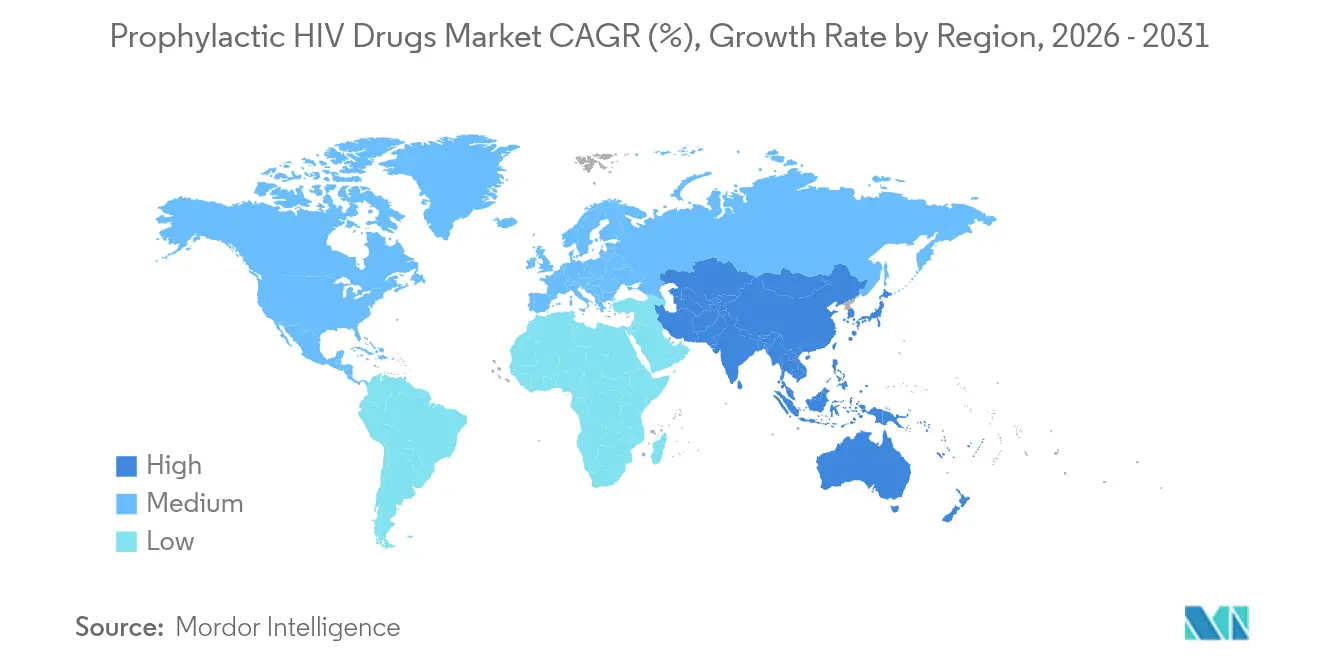

- By geography, North America held 41.02% of 2025 revenue and Asia-Pacific registers the highest projected CAGR at 5.28% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Prophylactic HIV Drugs Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global HIV incidence and prevalence | +1.2% | Sub-Saharan Africa, Asia-Pacific, Latin America | Long term (≥ 4 years) |

| Expanding government and donor funding for prevention programs | +0.8% | PEPFAR-supported regions; Global Fund priority countries | Medium term (2-4 years) |

| Increasing generic drug availability and affordability | +0.7% | Low- and middle-income countries; emerging markets | Medium term (2-4 years) |

| Ongoing innovation in antiretroviral drug-delivery technologies | +0.6% | North America and Europe (early adoption); global rollout as approvals widen | Short term (≤ 2 years) |

| Evolving digital health channels enabling remote PrEP access | +0.5% | North America, Europe, urban hubs in Asia-Pacific | Short term (≤ 2 years) |

| Integration of PrEP within sexual and reproductive health services | +0.4% | Europe and Latin America (accelerated implementation); global family-planning programs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global HIV Incidence and Prevalence

Roughly 1.3 million new HIV infections were reported worldwide in 2024, with adolescents and young adults accounting for a growing proportion of cases. The epidemiological urgency sustains baseline demand for prophylactic strategies and amplifies uptake of the prophylactic HIV drugs market across high-burden geographies. PURPOSE-1 and PURPOSE-2 trials documented 100% prevention efficacy for twice-yearly lenacapavir among cisgender women, eliminating adherence gaps that limited daily-pill effectiveness[1]Eric Sandstrom, “Lenacapavir Prevents HIV in PURPOSE Trials,” New England Journal of Medicine, nejm.org. Public-health agencies increasingly recommend capsid inhibitors for high-risk cohorts, signaling an evidence-driven shift in clinical guidelines. Rising drug-resistant HIV strains further heighten interest in mechanisms outside reverse transcriptase inhibition, reinforcing diversification within the prophylactic HIV drugs market. Collectively, disease-burden dynamics and resistance concerns underpin a structural growth floor for preventive pharmacotherapy.

Expanding Government and Donor Funding for Prevention Programs

Donor agencies are pivoting toward prevention as the fiscally prudent way to cut HIV incidence, with the Global Fund’s 2025 procurement of African-manufactured first-line regimens marking a watershed for regional supply chains[2]“Global Fund Invests in African Manufacturing,” Global Fund, globalfund.org. PEPFAR’s pledge to source 2 million locally produced treatments by 2030 illustrates how industrial-policy goals now overlap with public-health objectives. Such commitments enlarge the prophylactic HIV drugs market by guaranteeing predictable volumes and lowering last-mile costs. At the same time, program funding is tied to political cycles, injecting volatility into multiyear revenue forecasts. Manufacturers that master low-cost GMP production and navigate donor tender processes secure a durable competitive edge under the new access paradigm.

Increasing Generic Drug Availability and Affordability

Voluntary-licensing deals accelerate generic penetration while strategically sheltering premium margins in high-income markets. Gilead’s license for lenacapavir across 120 countries slashes cost of goods to USD 40-100 per patient per year versus the USD 42,250 branded price in the United States. As generic firms ramp volume, innovators face margin compression yet gain reputational benefits and extended lifecycle revenue through royalties. Middle-income nations left outside licensing envelopes, including Brazil and Mexico, intensify advocacy for broader access, signaling potential policy pressure that could reshape pricing corridors in the prophylactic HIV drugs market. The resulting price gradients reinforce tiered-market dynamics that reward efficient scale production and targeted portfolio management.

Ongoing Innovation in Antiretroviral Drug-Delivery Technologies

Pipeline assets such as Merck’s once-monthly oral MK-8527 and ViiV’s four-monthly N6LS antibody highlight a diverse wave of long-acting modalities moving through late-stage trials. Patient-preference studies show sustained willingness to switch from daily pills to injectable or monthly oral options, citing convenience and reduced stigma. Combination of extended-release pharmacology with digital adherence monitoring allows clinicians to tailor prophylaxis schedules, enhancing real-world effectiveness. Early adoption in North America and Europe drives premium pricing, while technology-transfer initiatives shorten lag-times before launch in emerging markets. Continuous innovation thus injects additional growth momentum into the prophylactic HIV drugs market and differentiates leaders via intellectual-property depth.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of novel long-acting formulations | -0.9% | Global; greatest effect in middle-income countries | Short term (≤ 2 years) |

| Persisting socioeconomic access disparities | -0.6% | Sub-Saharan Africa, Latin America, rural Asia-Pacific | Long term (≥ 4 years) |

| Regulatory and reimbursement uncertainties across markets | -0.5% | Emerging markets and countries with fragmented insurance systems | Medium term (2-4 years) |

| Stigma and misinformation limiting PrEP uptake | -0.4% | High-burden regions worldwide, particularly among marginalized populations | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Novel Long-Acting Formulations

Annual U.S. list pricing of USD 42,250 for lenacapavir stands a thousand-fold above estimated manufacturing costs, limiting payer acceptance despite clinical superiority. Insurers impose prior authorization and step therapy, delaying uptake of long-acting options in favor of cheaper generics. Middle-income markets caught between patent protection and absence of tiered pricing face the steepest affordability hurdles, curbing near-term penetration of the prophylactic HIV drugs market. To mitigate resistance, companies are exploring subscription-style agreements and value-based contracts, yet these models remain nascent and unevenly applied.

Persisting Socioeconomic Access Disparities in High-Burden Regions

Cold-chain requirements and skilled-provider administration constrain distribution of injectables in rural clinics, while stigma deters marginalized groups from engaging with public health systems[3]“Cold-Chain Barriers in Rural Clinics,” Science, science.org. Internet connectivity gaps hinder tele-PrEP rollout, dampening the digital-channel upside in low-resource settings. Such structural inequities create a floor beneath which technology alone cannot lift prophylaxis coverage, capping total-addressable share in the prophylactic HIV drugs market. Multisectoral interventions encompassing infrastructure, education, and legal reform are needed to resolve these systemic obstacles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug: Lenacapavir’s Capsid Inhibition Reshapes Competitive Hierarchy

Tenofovir Alafenamide controlled 54.78% of the prophylactic HIV drugs market share in 2025, reflecting its renal- and bone-sparing safety profile and wide familiarity among prescribers. However, lenacapavir unlocks a differentiated capsid-inhibition pathway that secures a 6.35% CAGR, displacing incumbents in high-adherence-risk populations and expanding the overall prophylactic HIV drugs market size by capturing patients previously unwilling or unable to manage daily pills. Emtricitabine remains a staple backbone in combination regimens, while cabotegravir long-acting sustains niche demand despite supply bottlenecks.

Competitive dynamics increasingly hinge on mechanism-of-action diversification to counter resistance evolution, positioning lenacapavir as the vanguard of next-generation prophylaxis within the prophylactic HIV drugs industry. As generic licensing unlocks volume in 120 countries, innovators must rely on lifecycle management and novel co-formulations to defend share in premium tiers.

By Dosage Form: Injectables Record Fastest Uptake

Oral tablets still accounted for 65.02% revenue in 2025, buoyed by entrenched procurement channels and lower unit costs. Yet injectables outpace all formats at 7.31% CAGR through 2031, helping enlarge the prophylactic HIV drugs market as twice-yearly dosing removes daily-adherence friction. Post-marketing studies show preference swings toward injectables among adolescents and cisgender women citing discretion and convenience.

Pipeline work on sub-dermal implants and microbicide rings signals a broader dosage-form diversification that supports personalized prevention. This heterogeneity shields the prophylactic HIV drugs market from single-technology shocks and distributes growth across varying patient needs and healthcare settings.

By Distribution Channel: Digital Platforms Scale Rapidly

Hospital pharmacies held 55.21% share in 2025 owing to mandatory baseline testing and monitoring requirements, anchoring traditional revenue streams for the prophylactic HIV drugs market. The pandemic-era telemedicine surge catalyzed online pharmacies and tele-PrEP services, which now expand at a 7.55% CAGR by offering remote prescribing, doorstep delivery, and app-based adherence reminders.

Retail pharmacies capture incremental volume because walk-in service lowers stigma, while community clinics leverage culturally tailored outreach to reach marginalized groups. Despite bandwidth gaps in some countries, digital platforms are projected to unlock significant incremental prophylactic HIV drugs market size by reducing travel time and provider shortages in underserved regions.

Geography Analysis

North America represented 41.02% of 2025 revenue for the prophylactic HIV drugs market, underpinned by broad insurance coverage, early regulatory approvals, and mature clinical trial ecosystems. United States payers increasingly adopt value-based reimbursement for long-acting injectables, while Canada’s single-payer system standardizes PrEP benefits nationally. Mexico leverages trade ties to accelerate technology transfer, enabling cross-border manufacturing partnerships that widen supply resilience.

Asia-Pacific posts the highest forecast CAGR at 5.28% and is projected to outpace global growth through 2031 as governments in Vietnam, Thailand, and India merge HIV prevention into universal-health-coverage agendas. Rapid smartphone penetration backs telehealth delivery, although rural cold-chain gaps still constrain injectable scale-up. Regulatory harmonization across ASEAN could streamline approval timelines, expanding the prophylactic HIV drugs market size in populous economies.

Europe shows mature yet uneven penetration; 38 of 52 countries had national PrEP guidelines by 2024, but recipient data reveal concentration among men who have sex with men at 98%, highlighting unmet needs in women and migrants. Germany’s insurance model has achieved 33% coverage of indicated users and targets 81% by 2030, illustrating how reimbursement stability lifts adoption. Divergent eligibility criteria across member states, however, continue to fragment the prophylactic HIV drugs market landscape within the region.

Competitive Landscape

The prophylactic HIV drugs market remains moderately consolidated: Gilead Sciences and ViiV Healthcare dominate innovation pipelines and maintain extensive manufacturing footprints. Gilead leverages integrated R&D and voluntary licensing to balance access with revenue preservation, while ViiV’s focused HIV franchise accelerates cycle times on long-acting formulations. Patent portfolios form formidable entry barriers, yet strategic licensing opens room for regional manufacturers like Emcure, Cipla, and Aurobindo to build share on cost-leadership in price-sensitive territories.

Competitive positioning now centers on dosing flexibility, cold-chain efficiency, and companion digital tools rather than molecular uniqueness alone. Multinationals forge contract-manufacturing deals to defray capital expenses and localize supply, exemplified by Emcure’s 2024 royalty-free license for lenacapavir covering 120 countries. Generic challengers pursue tender-driven volume in sub-Saharan Africa, but still rely on innovators for active-ingredient supply in early ramp-up phases.

Anticipated patent expiries post-2031 could spark steeper price erosion, prompting innovators to invest in next-wave assets like broadly neutralizing antibodies and ultra-long implants. Stakeholders that align portfolio depth with equitable-pricing frameworks are positioned to retain relevance as the prophylactic HIV drugs industry evolves toward value-based and access-driven paradigms.

Prophylactic HIV Drugs Industry Leaders

Merck & Co., Inc.

Cipla Inc

Bristol-Myers Squibb Company

Johnson & Johnson

Viatris Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Gilead Sciences presented Phase 3 data confirming twice-yearly lenacapavir efficacy across pregnant women and adolescents, bolstering global regulatory submissions.

- July 2025: Gilead and the Global Fund concluded discounted supply agreements to expand low-income country access to long-acting PrEP.

- June 2025: FDA approved lenacapavir (Yeztugo) as the first twice-yearly injectable PrEP modality in the United States.

- May 2025: European Centre for Disease Prevention and Control reported 159,819 PrEP users across Europe in 2023, with 38 countries publishing guidelines.

- April 2025: ViiV Healthcare’s EMBRACE study posted 96% viral suppression for four-monthly N6LS plus monthly cabotegravir.

- October 2024: Emcure Pharmaceuticals secured a royalty-free license from Gilead for lenacapavir across 120 countries.

Global Prophylactic HIV Drugs Market Report Scope

As per the scope of the report, human immunodeficiency virus (HIV) is a chronic and life-threatening disease. The disease can be transferred from one person to another through blood-to-blood or sexual contact. HIV prophylactic drugs are the medication that is given to prevent HIV disease before it even occurs.

The prophylactic HIV drugs market is segmented by drug, dosage form, and geography. By drug, the market is segmented into tenofovir, emtricitabine, and other drugs. The other drugs category includes cabotegravir, lenacapavir, and others. By dosage form, the market is segmented into oral and topical. By geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Tenofovir Disoproxil Fumarate (TDF) |

| Tenofovir Alafenamide (TAF) |

| Emtricitabine (FTC) |

| Cabotegravir Long-Acting (Apretude) |

| Lenacapavir (Yeztugo/Sunlenca) |

| Other Drugs |

| Oral Pill |

| Long-Acting Injectable |

| Sub-Dermal Implant (Pipeline) |

| Topical Microbicide (Gel/Film) |

| Vaginal Ring |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies & Tele-PrEP Platforms |

| Community-Based Clinics & NGOs |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug | Tenofovir Disoproxil Fumarate (TDF) | |

| Tenofovir Alafenamide (TAF) | ||

| Emtricitabine (FTC) | ||

| Cabotegravir Long-Acting (Apretude) | ||

| Lenacapavir (Yeztugo/Sunlenca) | ||

| Other Drugs | ||

| By Dosage Form | Oral Pill | |

| Long-Acting Injectable | ||

| Sub-Dermal Implant (Pipeline) | ||

| Topical Microbicide (Gel/Film) | ||

| Vaginal Ring | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies & Tele-PrEP Platforms | ||

| Community-Based Clinics & NGOs | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the prophylactic HIV drugs market?

The prophylactic HIV drugs market size is valued at USD 34.75 billion in 2026 and is forecast to reach USD 42.23 billion by 2031.

Which drug segment is expanding the fastest?

Lenacapavir leads growth with a 6.35% CAGR due to its twice-yearly injectable schedule and novel capsid-inhibition mechanism.

How quickly are long-acting injectables growing?

Long-acting injectable formulations post a 7.31% CAGR between 2026 and 2031, making them the fastest-growing dosage form.

Which region is projected to see the highest growth rate?

Asia-Pacific shows the highest regional CAGR at 5.28% thanks to government-led PrEP expansion and digital-health adoption.

What are the main barriers to wider PrEP adoption?

High pricing of novel long-acting products and systemic access disparities in rural and marginalized populations remain key obstacles.

How concentrated is the competitive landscape?

The market scores 7 on a 10-point concentration scale because the five largest suppliers hold about 70% of global revenue yet face rising generic competition.

Page last updated on: