Market Overview

| Study Period | 2019 - 2030 |

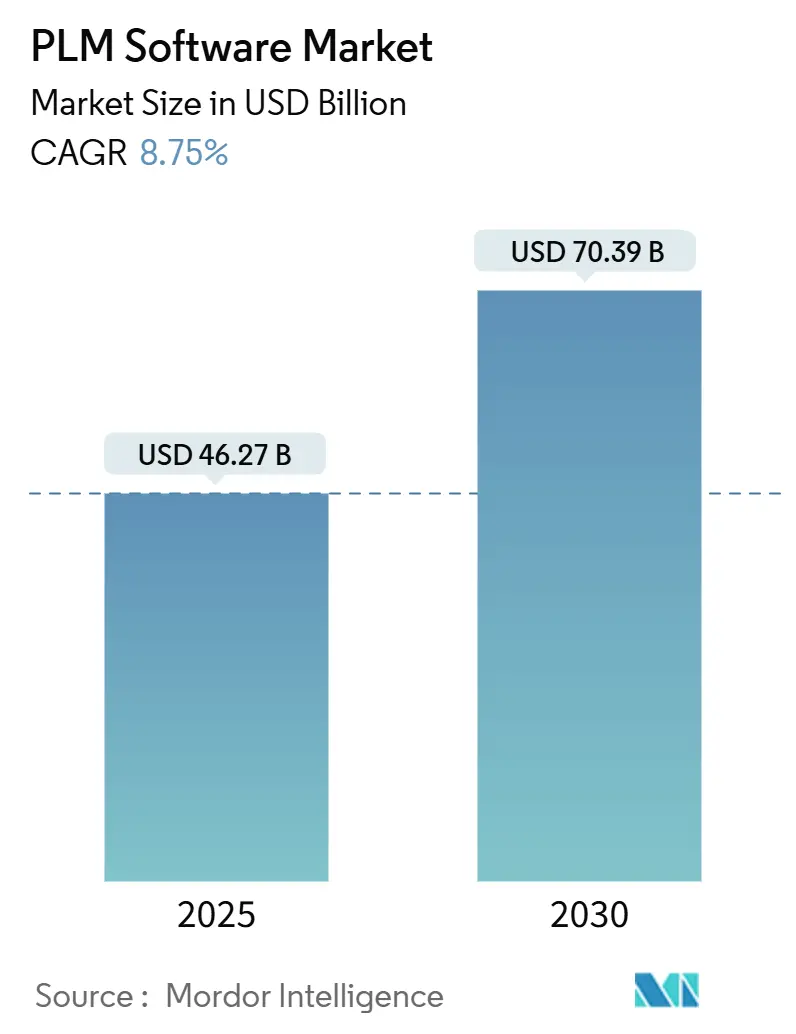

| Market Size (2025) | USD 46.27 Billion |

| Market Size (2030) | USD 70.39 Billion |

| Growth Rate (2025 - 2030) | 8.75% CAGR |

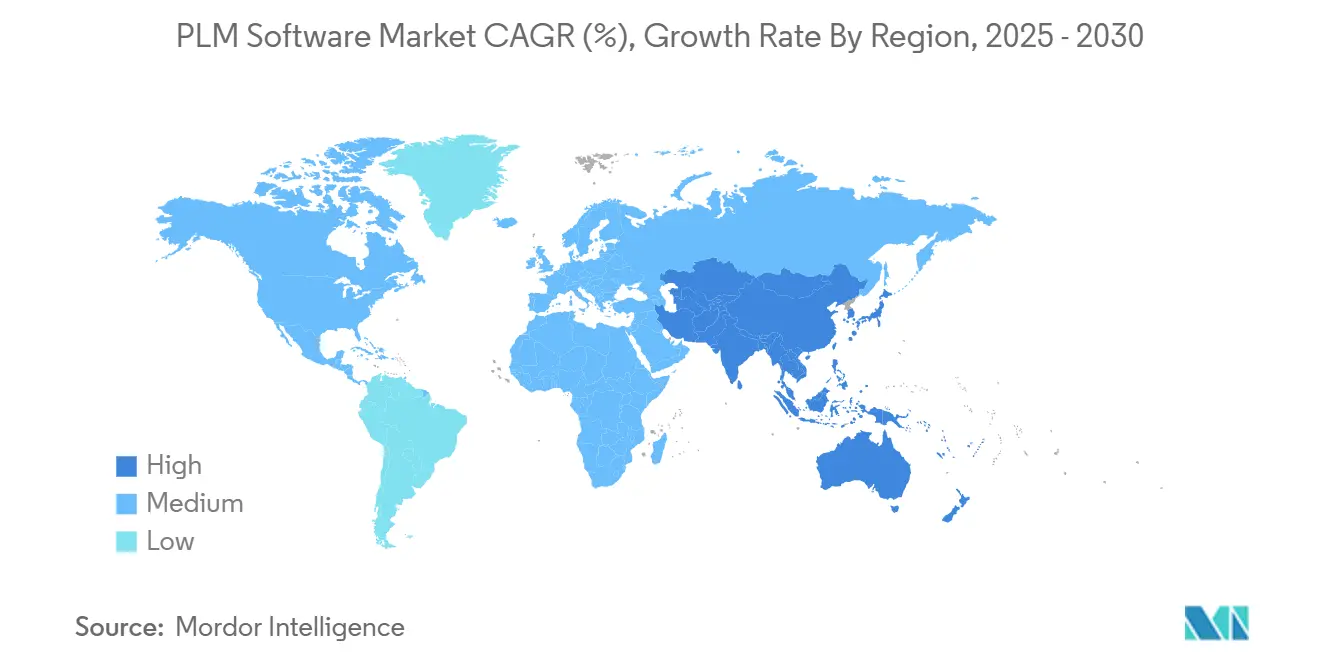

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

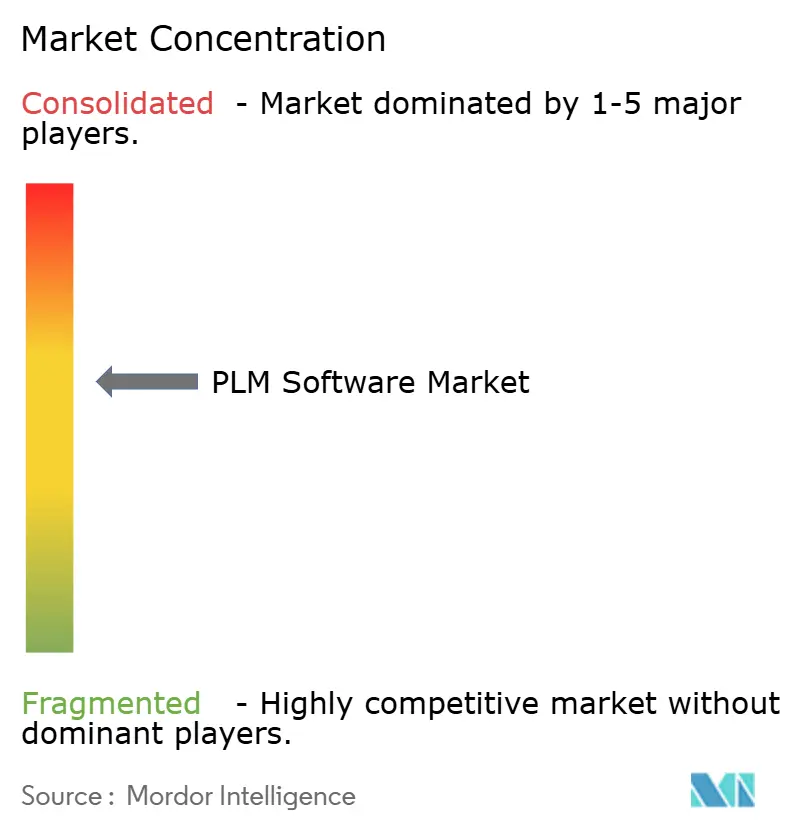

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

PLM Software Market Analysis by Mordor Intelligence

The PLM software market size stood at USD 46.27 billion in 2025 and is forecast to reach USD 70.39 billion by 2030, advancing at 8.8% CAGR Aras. Sustained migration from on-premise installations to cloud-native rollouts, the rapid infusion of generative-AI copilots into engineering environments, and rising regulatory demands for traceability collectively lift growth prospects. Vendors highlight that software-as-a-service (SaaS) PLM subscriptions expand collaboration across globally dispersed engineering teams while lowering operating expenses through automatic updates and elastic compute resources. Generative-AI assistants accelerate engineering change-order (ECO) cycles, freeing specialist capacity amid persistent skills shortages in automotive, aerospace, and electronics design. Meanwhile, end-to-end digital-thread projects that link design, simulation, manufacturing, service, and recycling data deliver a single source of truth that simplifies compliance with Europe’s Digital Product Passport and similar mandates worldwide. Competitive dynamics intensify as leading providers acquire adjacent simulation and data-science assets, signalling a race to deliver comprehensive industrial platforms built on secure, multi-tenant architectures.

Key Report Takeaways

- By deployment type, on-premise installations retained 68.2% of the PLM software market share in 2024, whereas cloud subscriptions are expanding at 10.5% CAGR to 2030.

- By solution type, collaborative PDM/cPDM commanded 56.1% revenue share in 2024; digital-manufacturing and MES/PLM integration is progressing fastest at 9.9% CAGR.

- By end-user industry, automotive and transportation led with 22.3% of the PLM software market size in 2024, while life sciences and medical devices is advancing at 9.2% CAGR to 2030.

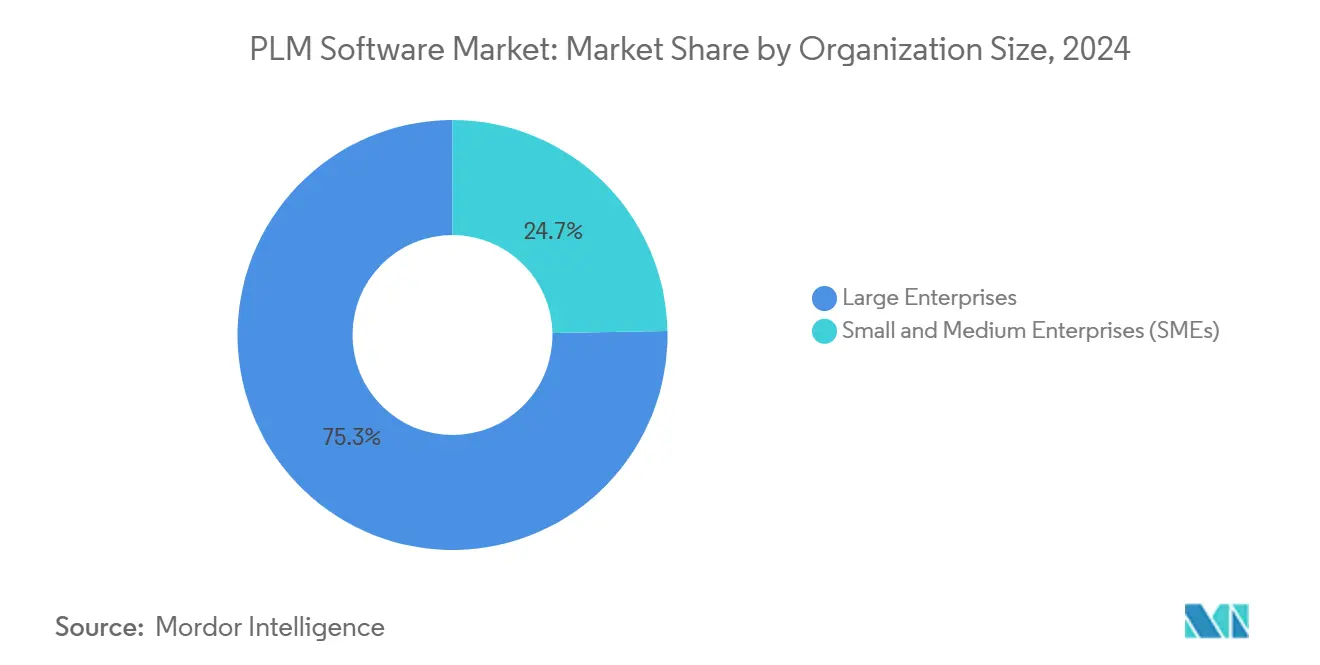

- By organisation size, large enterprises held 75.3% of the PLM software market size in 2024; the SME segment records a 10.3% CAGR through 2030.

- By geography, North America captured 36.4% revenue share in 2024; Asia-Pacific is set to post a 9.6% CAGR through 2030.

Global PLM Software Market Trends and Insights

Drivers Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability gaps between legacy CAD and modern PLM | –1.6% | Global; entrenched manufacturing regions | Long term (≥ 4 years) |

| Cyber-security and IP-leakage worries in multi-tenant SaaS | –1.1% | Global; defence and aerospace hotspots | Medium term (2-4 years) |

| Open-source digital-twin stacks cannibalising licences | –0.8% | Global; cost-sensitive SMB cohorts | Long term (≥ 4 years) |

Source: Mordor Intelligence

Cloud-first adoption among Tier-1 manufacturers

The PLM software market is pivoting from legacy on-premise environments to SaaS delivery as industrial leaders seek real-time collaboration across global design centres. Gartner notes that half of midsize and large manufacturers will standardise on SaaS PLM by 2026, while Aras reports more than 50% year-over-year growth in cloud subscriptions. Success stories such as Red Bull and H-TEC Systems reveal 35-50% cost savings after replacing locally hosted tools with Aras Innovator SaaS[1]Siemens AG, “Siemens to Acquire Altair Engineering for USD 10.6 Billion,” press.siemens.com. Automatic patching, built-in cyber-security, and instant access to AI-assisted analytics amplify the appeal, although data-sovereignty concerns temper adoption in markets such as Japan, where acceptance lingers at 60%. Even so, hybrid rollouts that retain sensitive workloads on site while using SaaS for collaboration act as a pragmatic bridge during migration.

Growing need for end-to-end digital thread

Enterprises now treat product data as a continuum spanning concept, design, simulation, manufacturing, service, and recycling. Lockheed Martin’s integration of Teamcenter with a next-generation MES demonstrates how aircraft builders gain full lifecycle visibility and cut unplanned rework. Airbus’s “Greenhouse” initiative ties more than 1,000 legacy systems into Aras Innovator, enabling rapid application prototyping while enforcing common data models. As sustainability audits rise, digital threads deliver granular carbon-footprint metrics, facilitating compliance with EU Eco-design rules and building resilient supply chains able to respond rapidly to disruption or recall events.

Regulatory push for product traceability and sustainability reporting

Europe’s Eco-design for Sustainable Products Regulation, effective July 2024, introduces Digital Product Passports that mandate lifecycle data disclosure between 2026 and 2030. PLM vendors respond by embedding material composition, recyclability, and energy-use fields directly into engineering workflows to minimise compliance overhead. Siemens Polarion supports FDA 21 CFR Part 11 and IEC 62304 for medical-device makers such as Sirona Dental Systems, which rely on automated validation to maintain audit readiness.

Generative-AI copilots trimming engineering change-order cycles

Unveiled at Hannover Messe 2024, Siemens Industrial Copilot integrates generative AI into the TIA Portal, accelerating PLC code generation and reducing manual documentation. Aras follows with an AI-Assisted Search that surfaces structured and unstructured product data via natural-language prompts[2]Aras Corp., “Aras Innovator SaaS Registers 50% YoY Growth,” aras.com. Early adopters cut ECO approval loops by double-digit percentages, freeing engineers to focus on innovation rather than administrative tasks. Food processors extend AI insights by ingesting social-media sentiment and point-of-sale data to refine formulations.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interoperability gaps between legacy CAD and modern PLM | –1.6% | Global; entrenched manufacturing regions | Long term (≥ 4 years) |

| Cyber-security and IP-leakage worries in multi-tenant SaaS | –1.1% | Global; defence and aerospace hotspots | Medium term (2-4 years) |

| Open-source digital-twin stacks cannibalising licences | –0.8% | Global; cost-sensitive SMB cohorts | Long term (≥ 4 years) |

Source: Mordor Intelligence

Persistent interoperability gaps between legacy CAD and modern PLM

Migrating 4,400 files from SOLIDWORKS to Teamcenter can still consume more than a month for skilled consultants, underscoring the disconnect between desktop CAD schemas and enterprise PLM databases. PTC’s Onshape migration-wizard powered by AWS attempts to automate data mapping, yet many firms run hybrid environments that inflate support costs and dilute the promised single source of truth.

Cyber-security and IP leakage concerns in multi-tenant SaaS

Aerospace primes view CAD models as national-security assets. Dassault Systèmes addresses risk via its 3DEXPERIENCE Trust Center with ISO 27001 and SOC 2 certifications[3]Dassault Systèmes, “Volkswagen Group Selects 3DEXPERIENCE,” 3ds.com. Aras Enterprise SaaS relies on Microsoft Azure for encryption-in-transit and at-rest, plus granular role-based access. Even so, buyer hesitation persists, prompting vendors to create sovereign-cloud editions that ring-fence sensitive data.

Segment Analysis

By Deployment Type: Cloud acceleration despite on-premise dominance

On-premise systems still house 68.2% of the PLM software market in 2024, reflecting sunk investments in data-centre hardware and bespoke integrations. Cloud subscriptions rise at 10.5% CAGR as pandemic-era remote-work imperatives uncover the collaboration limits of site-bound servers. Aras records >50% annual SaaS growth and cites surveys where 81% of industrial respondents expect SaaS to become the default delivery model. Modern rollouts favour hybrid design patterns that retain regulated data locally while exploiting cloud elasticity for analytics. This shift ensures the PLM software market size for cloud deployments is projected to eclipse USD 30 billion by 2030 at current growth rates. The DACH region features 91% SaaS acceptance, contrasting with 60% in Japan, where cultural emphasis on data sovereignty slows transition.

Second-generation SaaS architectures offer zero-downtime upgrades and built-in disaster recovery. Vendors layer AI services atop common data models, letting users tap natural-language search and automated code generation without installing patches. Security now equals or surpasses on-premise benchmarks thanks to hardware-root-of-trust modules and continual penetration testing. As a result, the PLM software market steadily reallocates budgets from capital expenditure on servers to operational expenditure on subscription bundles.

By Solution Type: Collaborative PDM leadership challenged by manufacturing integration

Collaborative PDM/cPDM tools capture 56.1% revenue share by managing drawings, specifications, and change records across multi-disciplinary teams. Yet the fastest-growing slot belongs to digital-manufacturing and MES-PLM integration, which expands 9.9% CAGR as plant managers seek real-time feedback loops between design intent and shop-floor execution. Lockheed Martin exemplifies gains after linking a next-generation MES to Teamcenter, shrinking rework via instant propagation of design updates[4]DXC Technology, “Lockheed Martin Chooses DXC for MES Modernization,” dxc.com. The PLM software market size for MES-linked offerings is on track to double by 2030, evidence that discrete boundaries between engineering and operations are disappearing.

Simulation, analysis, and ALM/SLM categories log steady demand, especially in software-defined products like EVs and connected medical devices. Siemens’ USD 10.6 billion Altair buyout unites multiphysics solvers with Teamcenter, creating an integrated environment where engineers iterate designs, run virtual tests, and push validated parameters directly to production. As Industry 4.0 accelerates, the PLM software market will likely elevate closed-loop workflows that merge design, production, and field-performance data into a continuous improvement cycle.

By Organisation Size: SME acceleration through micro-subscription models

Large enterprises captured 75.3% revenue in 2024, reflecting complex multinational programmes that require robust configuration management, advanced security, and integration with ERP, CRM, and MES hubs. Nevertheless, SMEs demonstrate a 10.3% CAGR as cloud delivery and simplified licensing flatten adoption barriers. Propelled by user-based subscriptions, SMEs can phase functionality, starting with BOM management before layering change control, quality, and supplier collaboration, without six-figure implementation fees. Consequently, the PLM software market share held by SMEs rises each year, fostering a more diverse customer base.

Case studies such as BRUNT Workwear—deploying Centric PLM to automate product launches—illustrate time-to-value measured in weeks rather than quarters. Vendors bundle e-learning portals and sandbox environments, letting lean engineering teams self-provision pilots. Should growth continue, the PLM software market size attributed to SMEs could exceed USD 10 billion by 2030, underscoring the democratising effect of SaaS economics.

By End-User Industry: Automotive leadership pressured by life-sciences growth

Automotive and transportation accounted for 22.3% of overall revenue in 2024, driven by electrification and autonomous-vehicle roadmaps demanding software-centric product architectures. Volkswagen Group’s adoption of Dassault’s 3DEXPERIENCE across Volkswagen, Audi, and Porsche aims to shorten vehicle-development cycles and synchronize cross-brand platforms. Yet life sciences and medical devices outpace all other verticals at 9.2% CAGR thanks to FDA 21 CFR Part 11 mandates and compressed clinical-trial timelines. Siemens’ Polarion supports automated design-history files and real-time traceability, with customers such as LifeWatch reducing regulatory-submission effort.

Electronics, aerospace, and industrial machinery sustain healthy adoption while retail and consumer-packaged goods embrace PLM to manage eco-labels and allergen data. As a result, the PLM software industry gains resilience from sectoral diversity. Should genomic-data integration and personalised-medicine pipelines mature, the life-sciences slice of the PLM software market could match automotive within the next decade.

Geography Analysis

North America captured 36.4% revenue in 2024, benefiting from deep aerospace and high-tech clusters that standardised early on digital-thread programmes. Generative-AI pilots proliferate in Silicon Valley, where start-ups co-innovate with PLM incumbents on context-aware assistants. Federal initiatives that stipulate model-based systems engineering in defence contracts further cement demand.

Asia-Pacific is the fastest-growing theatre with 9.6% CAGR as China’s industrial software sector more than doubled from 1,293 billion yuan in 2017 to beyond 3,000 billion yuan by 2024. Government drives such as “Made in China 2025” and India’s Production-Linked Incentive schemes spur factories to digitise. Hisense Group reports a 70% design-efficiency gain after rolling out a multi-site PLM backbone, trimming average cycle time from 60 days to 43.2 days. Consequently, Asia-Pacific’s slice of the PLM software market size is projected to surpass USD 20 billion by 2030 if present momentum persists.

Europe remains pivotal through regulatory leadership. The Eco-design Regulation forces manufacturers to embed sustainability attributes at design inception, reinforcing the need for lifecycle data management. Siemens’ partnership with BAE Systems under a five-year digital-innovation accord indicates ongoing modernisation within the UK defence complex. Meanwhile, sovereign-cloud imperatives in France and Germany steer procurement towards regional data centres certified under Gaia-X frameworks. Emerging economies in Latin America, the Middle East, and Africa are gradually entering the PLM software market, aided by public-cloud infrastructure that removes capex hurdles and local partners that deliver vertical templates.

Competitive Landscape

The PLM software market demonstrates moderate consolidation. Siemens leads inorganic expansion, acquiring Altair Engineering for USD 10.6 billion and Dotmatics for USD 5.1 billion to fuse simulation, data science, and life-sciences pipelines into its Xcelerator portfolio. Dassault Systèmes intensifies pressure through Centric Software’s EUR 220 million purchase of Contentserv, adding product-information-management (PIM) assets tailored for retail brands. PTC deepens public-cloud credentials via a multi-year alliance with AWS that bundles six-month Onshape trials and AI-powered design advisors.

Strategic partnerships complement mergers. Siemens and BAE Systems co-develop model-based engineering blueprints, while Lockheed Martin uses DXC-integrated MES to tighten digital threads. Disruptors such as OpenBOM and Trace One win deals by offering focused cloud apps that sidestep heavyweight rollouts, nudging incumbents to simplify pricing and UX. As AI features become table stakes, differentiation gravitates toward domain-specific compliance packs (e.g., life-sciences validation, automotive functional safety) and open APIs that anchor PLM inside broader digital-twin ecosystems.

PLM Software Industry Leaders

-

Siemens AG

-

SAP SE

-

Autodesk Inc.

-

Dassault Systems Deutschland GmbH

-

PTC Inc.

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- April 2025: Siemens closed the USD 5.1 billion acquisition of Dotmatics, adding AI-driven informatics aimed at drug-discovery workflows.

- March 2025: Centric Software agreed to buy Contentserv Group, expanding its PIM footprint to 1,600 global brands.

- March 2025: Aras launched AI-Assisted Search and an Intelligent Assistant for Innovator SaaS, built on Microsoft Azure OpenAI Service.

- February 2025: Volkswagen Group rolled out Dassault’s 3DEXPERIENCE platform across Volkswagen, Audi, and Porsche to shrink engineering cycles.

- February 2025: PTC and AWS unveiled a Strategic Collaboration Agreement covering Onshape cloud-native CAD and the new Onshape AI Advisor.

Global PLM Software Market Report Scope

PLM software refers to a solution that helps manage all the information and processes involved in the lifecycle of a product or service across global supply chains. This includes data related to items, parts, products, documents, requirements, engineering change orders, and quality workflows. The product lifecycle management (PLM) software market for the study defines revenues generated from adopting the different types of PLM software in various end-user industries, such as electronics, industrial equipment, automotive, aerospace, and defense. The analysis is mainly based on the market insights captured through various secondary research and the primaries. The market also covers the major factors impacting the growth of the PLM software market in terms of drivers and restraints.

The product lifecycle management (PLM) software market is segmented by deployment type (on-premise, cloud, and professional services), end-user industry (electronics, industrial equipment, high-tech, aerospace and defense, automotive, architecture, engineering, and construction [AEC]), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Deployment Type | On-Premise | |||

| Cloud | ||||

| By Solution Type | Collaborative PDM / cPDM | |||

| MCAD Integration PLM | ||||

| Simulation and Analysis | ||||

| Digital Manufacturing and MES-PLM | ||||

| ALM / SLM | ||||

| By Organisation Size | Large Enterprises | |||

| Small and Medium Enterprises (SMEs) | ||||

| By End-user Industry | Automotive and Transportation | |||

| Aerospace and Defence | ||||

| Electronics and High-Tech | ||||

| Industrial Machinery and Heavy Equipment | ||||

| Architecture, Engineering and Construction (AEC) | ||||

| Life Sciences and Medical Devices | ||||

| Consumer Packaged Goods / Retail | ||||

| Others | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Russia | ||||

| Rest of Europe | ||||

| Asia-Pacific | China | |||

| Japan | ||||

| India | ||||

| South Korea | ||||

| ASEAN | ||||

| Australia and New Zealand | ||||

| Rest of Asia-Pacific | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Middle East and Africa | Middle East | Saudi Arabia | ||

| UAE | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Rest of Africa | ||||

By Deployment Type

| On-Premise |

| Cloud |

By Solution Type

| Collaborative PDM / cPDM |

| MCAD Integration PLM |

| Simulation and Analysis |

| Digital Manufacturing and MES-PLM |

| ALM / SLM |

By Organisation Size

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

By End-user Industry

| Automotive and Transportation |

| Aerospace and Defence |

| Electronics and High-Tech |

| Industrial Machinery and Heavy Equipment |

| Architecture, Engineering and Construction (AEC) |

| Life Sciences and Medical Devices |

| Consumer Packaged Goods / Retail |

| Others |

By Geography

| North America | United States | ||

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| ASEAN | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How big is the PLM software market today?

The PLM software market generated USD 46.27 billion in revenue in 2025 and is projected to climb to USD 70.39 billion by 2030 at an 8.8% CAGR.

Which deployment model is growing fastest?

Cloud-native SaaS deployments are expanding at 10.5% CAGR as companies prioritise remote collaboration, automatic updates, and elastic scaling.

Which industry vertical is set to outpace others?

Life sciences and medical devices lead with a 9.2% CAGR as FDA and EU compliance deadlines push manufacturers toward traceable digital threads.

Why are SMEs adopting PLM now?

Micro-subscription pricing and cloud delivery remove upfront infrastructure costs, allowing SMEs to access enterprise-grade functionality on demand.

What role does AI play in modern PLM?

Generative-AI copilots integrated into design and change-order workflows cut manual documentation, accelerate code generation, and surface contextual insights.

Are security concerns slowing cloud PLM adoption?

Aerospace and defence firms remain cautious, but certifications such as ISO 27001, sovereign-cloud options, and end-to-end encryption mitigate most risks while preserving data isolation.