Probiotic Cosmetic Products Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

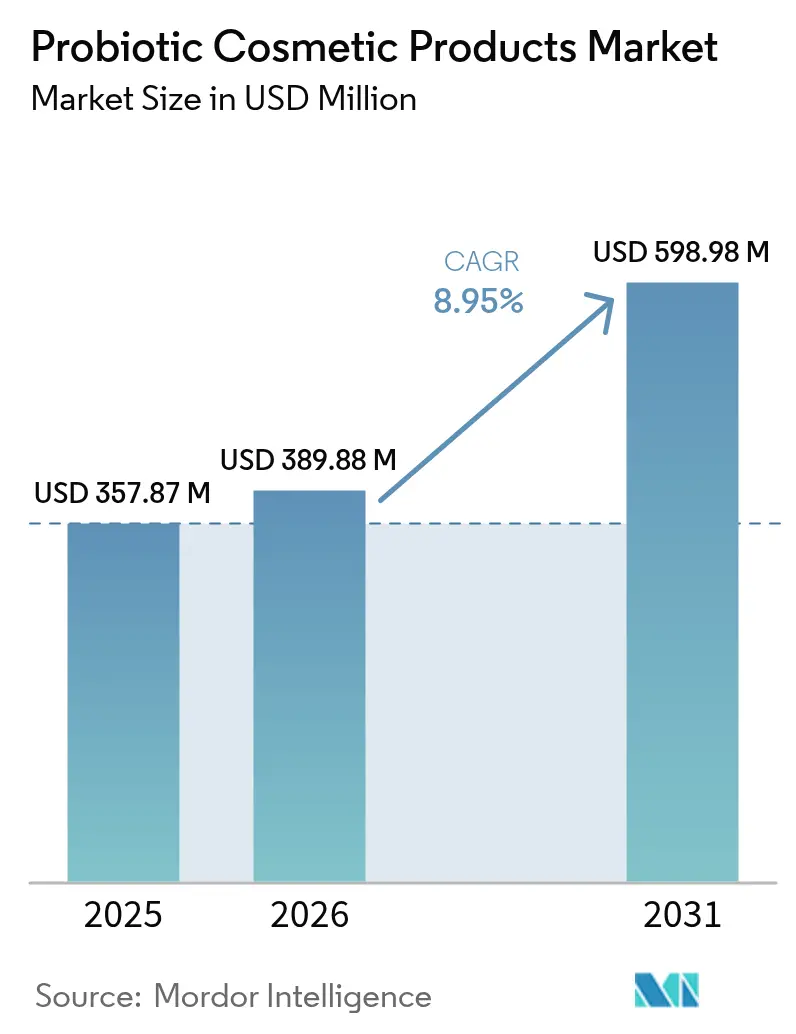

| Market Size (2026) | USD 389.88 Million |

| Market Size (2031) | USD 598.98 Million |

| Growth Rate (2026 - 2031) | 8.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Probiotic Cosmetic Products Market Analysis by Mordor Intelligence

The Probiotic Cosmetic Products Market size in 2026 is estimated at USD 389.88 million, growing from 2025 value of USD 357.87 million with 2031 projections showing USD 598.98 million, growing at 8.95% CAGR over 2026-2031. This growth trajectory reflects the convergence of scientific microbiome research with consumer demand for efficacious skincare solutions that address underlying skin health rather than merely cosmetic concerns. The market's expansion is fundamentally driven by the recognition that topical probiotics can restore skin barrier function and reduce inflammatory responses, positioning these products as therapeutic alternatives to conventional cosmetics. Market momentum stems from the ability of viable or lysed bacterial strains to reinforce barrier integrity, modulate inflammation, and deliver quantifiable dermatological benefits. Large beauty houses are embedding patented strains into hero stock‐keeping units, while venture-backed start-ups commercialize narrow applications such as scalp health. Digital commerce, social platforms, and dermatologist endorsements jointly accelerate product education, compressing the launch-to-adoption cycle. A balanced regulatory environment that treats probiotic cosmetics as low-risk leave-on formulations, provided safety dossiers are filed, further propels commercialization.

Key Report Takeaways

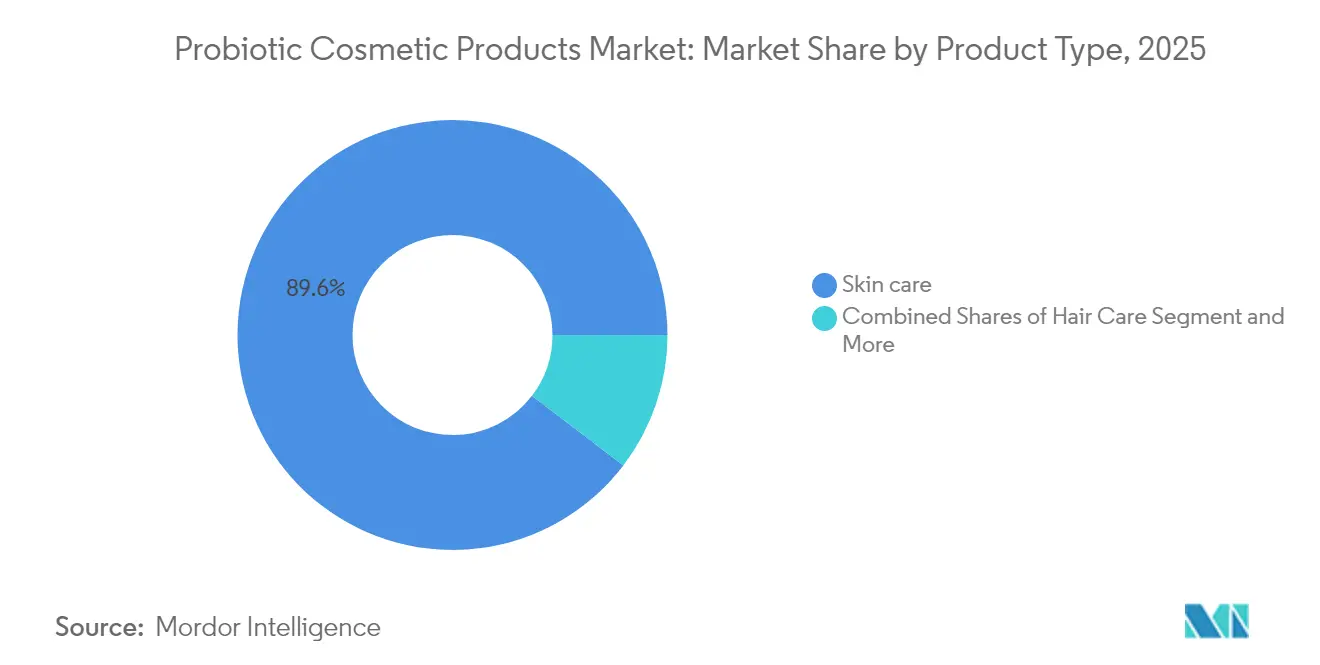

- By product type, skin care led with 89.62% revenue share in 2025; hair care is projected to expand at a 9.12% CAGR through 2031.

- By category, the conventional segment captured 81.55% of the probiotic cosmetic products market share in 2025, while organic products are advancing at a 10.58% CAGR to 2031.

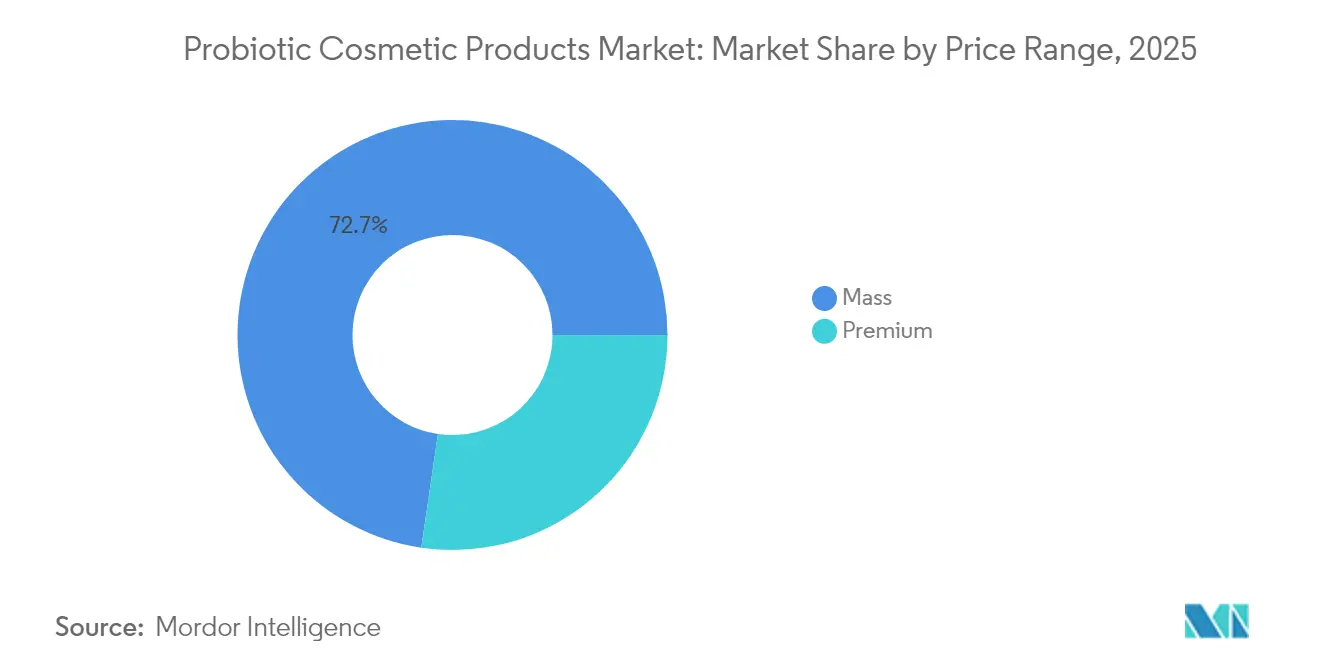

- By price range, mass offerings accounted for 72.68% of the probiotic cosmetic products market size in 2025 and premium lines are growing at a 10.45% CAGR to 2031.

- By distribution channel, health and beauty stores held 54.10% share in 2025; online retail is expanding at a 9.55% CAGR through 2031.

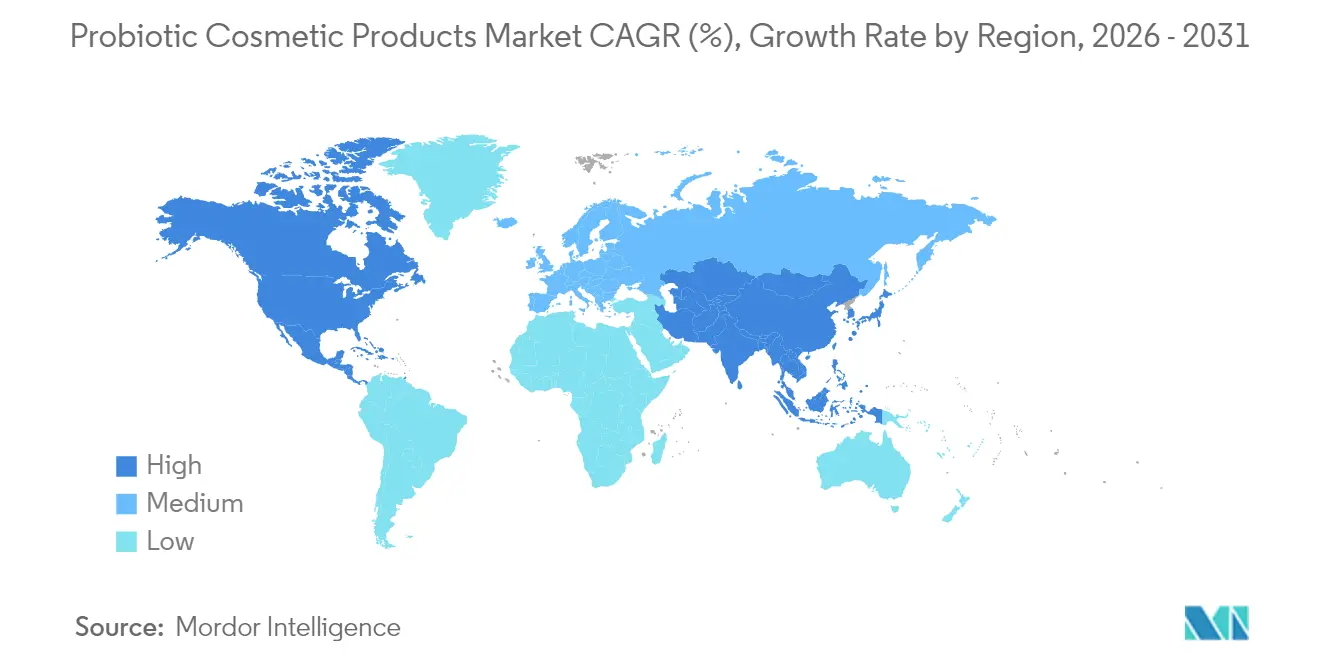

- By geography, North America commanded 36.62% share in 2025, whereas Asia-Pacific is forecast to record the fastest 9.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Probiotic Cosmetic Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Consumer Knowledge of Skin Microbiome | + 1.4% | Global, with early adoption in North America & European Union | Medium term (2-4 years) |

| Clean Beauty and Natural Formulation Demand | + 1.6% | Global, strongest in North America & Western Europe | Short term (≤ 2 years) |

| Trend Toward Multifunctional Products | + 1.1% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Prevalence of Sensitive Skin and Allergies | + 0.9% | Global, particularly urban markets | Long term (≥ 4 years) |

| Influence of Social Media, Influencers, and Celebrities | + 1.3% | Global, led by Gen Z and Millennial demographics | Short term (≤ 2 years) |

| Expansion of E-Commerce Platforms | + 1.4% | Global, accelerated in emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Consumer Knowledge of Skin Microbiome

Consumer understanding of skin microbiome science transforms purchasing decisions from ingredient-focused to mechanism-focused, creating demand for products that demonstrate measurable impact on microbial balance rather than superficial benefits. Clinical studies validating topical probiotic efficacy, including research showing comparable results to benzoyl peroxide for acne treatment, provide the scientific credibility that educated consumers increasingly demand. This knowledge shift enables brands to command premium pricing for formulations containing specific probiotic strains with documented clinical outcomes. The trend particularly accelerates in markets with established supplement cultures, where consumers readily translate gut health concepts to topical applications. Educational initiatives by dermatology associations and peer-reviewed publications in journals like Experimental Dermatology legitimize probiotic cosmetics as science-based interventions rather than wellness trends.

Clean Beauty and Natural Formulation Demand

The clean beauty movement evolves beyond ingredient exclusion toward active inclusion of beneficial microorganisms, positioning probiotics as the antithesis of harsh synthetic preservatives that disrupt skin ecology. Regulatory frameworks increasingly accommodate this shift, with FDA's Modernization of Cosmetics Regulation Act establishing clearer pathways for novel ingredients while maintaining safety standards[1]Source: U.S Food & Drug Administration, "Modernization of Cosmetics Regulation Act of 2022 (MoCRA)", fda.gov. Consumer willingness to pay premiums for clean formulations creates market opportunities for brands that can demonstrate both safety and efficacy through third-party testing and clinical validation. The trend particularly benefits smaller brands that can pivot quickly to meet evolving consumer preferences, often outmaneuvering established players constrained by legacy formulations and supply chains. This transformation in the beauty industry has led to increased investment in research and development of microbiome-friendly formulations, with laboratories worldwide conducting extensive studies on the skin's bacterial ecosystem. The integration of advanced biotechnology in cosmetic manufacturing has enabled the development of stable probiotic formulations that maintain their efficacy throughout the product lifecycle.

Trend Toward Multifunctional Products

Probiotic cosmetics inherently deliver multiple benefits through single formulations, addressing consumer demand for simplified routines while maximizing value per product. The microbiome approach enables brands to combine traditional cosmetic benefits with therapeutic outcomes, such as moisturizers that simultaneously strengthen barrier function and reduce inflammatory markers. This convergence particularly resonates in Asia-Pacific markets where consumers traditionally embrace holistic skincare philosophies and multi-step routines. Regulatory bodies like ISO are developing standards for multifunctional cosmetic claims, providing frameworks for brands to substantiate complex benefit profiles without overstating efficacy.

Prevalence of Sensitive Skin and Allergies

Rising incidence of sensitive skin conditions, attributed to environmental pollutants and lifestyle factors, creates sustained demand for gentle yet effective skincare solutions that probiotics uniquely provide. Clinical evidence demonstrates that topical probiotics can modulate inflammatory responses and strengthen skin barrier function, offering therapeutic benefits for conditions like eczema and rosacea without the side effects associated with pharmaceutical interventions. This medical positioning enables probiotic cosmetics to capture market share from both traditional skincare and dermatological treatments. Healthcare provider recommendations increasingly include probiotic skincare as adjunct therapy, legitimizing the category within medical communities and expanding market reach beyond beauty-conscious consumers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Market Presence of Counterfeit Products | -0.7% | Global, concentrated in emerging markets | Short term (≤ 2 years) |

| Strong Competition from Conventional and Synthetic Cosmetics | -1.1% | Global, particularly established markets | Medium term (2-4 years) |

| Regulatory Ambiguity and Lack of Standardization | -0.9% | Global, varying by jurisdiction | Long term (≥ 4 years) |

| High Product Pricing Constrains Market Growth | -0.8% | Price-sensitive markets, emerging economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Ambiguity and Lack of Standardization

The absence of standardized definitions for probiotic cosmetics creates market confusion and enables misleading claims that undermine consumer confidence in legitimate products. Regulatory frameworks vary significantly across jurisdictions, with some markets treating probiotic cosmetics as drugs requiring extensive clinical trials while others classify them as conventional cosmetics with minimal oversight. This inconsistency complicates international market entry strategies and increases compliance costs for manufacturers seeking global distribution. The lack of standardized testing protocols for probiotic viability and efficacy in topical applications further exacerbates quality control challenges, potentially leading to product failures that damage category credibility.

High Product Pricing Constrains Market Growth

Premium pricing strategies necessary to recover research and development costs for probiotic formulations limit market penetration in price-sensitive segments and emerging economies. Manufacturing complexities associated with maintaining probiotic viability through production, packaging, and shelf-life create cost structures that prevent mass-market pricing strategies. Consumer education requirements to justify premium pricing add marketing expenses that further inflate final product costs. This pricing constraint particularly impacts market expansion in developing regions where disposable income growth lags behind beauty product demand, creating opportunities for local manufacturers to develop cost-effective alternatives using indigenous probiotic strains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Skin Care Dominance Drives Market Foundation

Skin care commands 89.62% market share in 2025, reflecting consumer prioritization of facial health over other beauty applications and the concentration of clinical research validating topical probiotic benefits for dermatological conditions. Hair care emerges as the fastest-growing segment at 9.12% CAGR through 2031, driven by scientific evidence demonstrating probiotic efficacy for scalp health and hair growth stimulation. Color cosmetics and facial cosmetics represent emerging applications where brands experiment with probiotic integration to differentiate from conventional formulations, though adoption remains limited by formulation challenges and consumer unfamiliarity with the concept.

The dominance of skin care reflects the natural alignment between probiotic mechanisms and dermatological needs, particularly barrier function restoration and inflammatory response modulation. Systematic reviews published in peer-reviewed journals validate probiotic applications for conditions ranging from acne to anti-aging, providing the clinical foundation necessary for consumer acceptance and healthcare provider recommendations. Hair care growth accelerates as research demonstrates probiotic benefits for dandruff reduction and follicle health, expanding the addressable market beyond facial applications.

By Category: Conventional Products Maintain Share Despite Organic Acceleration

Conventional formulations retain 81.55% market share in 2025, demonstrating consumer acceptance of probiotic benefits regardless of broader formulation philosophy, while organic variants accelerate at 10.58% CAGR through 2031 as brands leverage clean beauty positioning. The conventional category's dominance reflects pragmatic consumer priorities that value probiotic efficacy over organic certification, particularly when clinical evidence supports specific strain benefits. Organic growth acceleration indicates emerging consumer segments willing to pay premiums for products that combine probiotic benefits with certified organic ingredients, creating opportunities for brands to capture both wellness-conscious and efficacy-focused consumers.

Regulatory frameworks increasingly accommodate both conventional and organic probiotic formulations, with certification bodies developing standards that recognize probiotic ingredients within organic cosmetic guidelines. This regulatory evolution enables brands to pursue dual positioning strategies that emphasize both probiotic science and organic credentials, potentially commanding higher price points while expanding market reach across consumer segments with different purchasing motivations.

By Price Range: Premium Growth Challenges Mass Market Dominance

Mass market products control 72.68% market share in 2025, reflecting broad consumer accessibility and established distribution channels, while premium segments expand at 10.45% CAGR through 2031 as brands justify higher prices through clinical validation and specialized formulations. The mass market's dominance demonstrates successful democratization of probiotic benefits through cost-effective manufacturing processes and simplified formulations that maintain efficacy while achieving accessible price points. Premium growth acceleration indicates consumer willingness to invest in advanced probiotic technologies, personalized formulations, and clinically-proven strain combinations that deliver measurable results.

Manufacturing innovations enable mass market brands to incorporate probiotic extracts and postbiotics that provide benefits without the complexity and cost of live cultures, making probiotic cosmetics accessible to price-conscious consumers. Premium brands differentiate through proprietary strain development, personalized microbiome testing, and clinical studies that justify higher price points while building consumer trust in probiotic efficacy. The development of stable formulations and enhanced shelf life has allowed manufacturers to expand their product portfolios across various cosmetic categories, from cleansers to serums. Additionally, advances in microencapsulation technology have improved the delivery systems of probiotic ingredients, ensuring their effectiveness when applied topically.

By Distribution Channel: Traditional Retail Faces Digital Disruption

Health and beauty stores maintain 54.10% market share in 2025, leveraging consumer trust and product education capabilities, while online retail channels accelerate at 9.55% CAGR through 2031 as direct-to-consumer brands bypass traditional gatekeepers. Traditional retail dominance reflects consumer preference for in-person consultation when purchasing unfamiliar product categories, particularly those requiring education about microbiome science and probiotic benefits. Online growth acceleration enables specialized brands to reach consumers directly while providing detailed educational content that traditional retail environments cannot accommodate.

Supermarkets and hypermarkets capture significant share through mass market positioning, while other distribution channels including pharmacies and dermatology clinics expand as probiotic cosmetics gain medical legitimacy. The evolution toward omnichannel strategies enables brands to leverage traditional retail for product discovery and online platforms for education and repurchase, optimizing customer acquisition costs while maintaining market reach across diverse consumer preferences. Specialty beauty retailers are increasingly incorporating dedicated probiotic skincare sections to meet growing consumer demand for these products. Direct-to-consumer channels are also experiencing rapid growth as brands invest in personalized shopping experiences and subscription-based models.

Geography Analysis

North America leads the global market with 36.62% share in 2025, benefiting from established consumer awareness of probiotic supplements that translates readily to topical applications and regulatory frameworks that accommodate cosmetic innovation. The region's dominance reflects early adoption of microbiome science in both healthcare and consumer products, creating educated consumer bases willing to invest in evidence-based skincare solutions. Established distribution networks and marketing infrastructure enable efficient market penetration for both domestic and international brands seeking to capitalize on consumer openness to novel cosmetic technologies. Healthcare provider acceptance of probiotic cosmetics as adjunct therapy further legitimizes the category and expands market reach beyond beauty-conscious consumers.

Asia-Pacific demonstrates the strongest growth momentum at 9.41% CAGR through 2031, driven by rising disposable incomes, cultural emphasis on preventive skincare, and regulatory evolution that facilitates market entry for innovative cosmetic formulations. China's streamlined cosmetic notification processes reduce barriers for international brands while domestic manufacturers leverage indigenous probiotic strains to develop cost-effective alternatives for price-sensitive consumers. The region's traditional medicine heritage creates cultural acceptance of beneficial microorganisms, accelerating consumer adoption of probiotic cosmetics compared to markets where the concept requires extensive education. South Korea's beauty innovation leadership and Japan's advanced manufacturing capabilities position Asia-Pacific as both a growth market and innovation hub for probiotic cosmetic development.

Europe maintains significant market presence through established organic and natural cosmetic markets that readily accommodate probiotic formulations, while regulatory frameworks under EU Cosmetic Regulation 1223/2009 provide clear pathways for novel ingredient approval . The region's emphasis on sustainability and environmental consciousness aligns with probiotic positioning as eco-friendly alternatives to synthetic preservatives and harsh chemicals. South America and Middle East & Africa represent emerging opportunities where growing middle classes and increasing beauty consciousness create demand for innovative skincare solutions, though market development requires education about probiotic benefits and adaptation to local regulatory requirements and consumer preferences.

Note: Segment shares of all Individual segments will be available upon report purchase

Competitive Landscape

The probiotic cosmetic products market exhibits moderate fragmentation, reflecting the coexistence of established beauty conglomerates and specialized microbiome startups that compete through different strategic approaches. Major players pursue acquisition-driven growth strategies to rapidly acquire probiotic expertise, exemplified by L'Oréal's February 2025 acquisition of Lactobio and Beiersdorf's majority stake in S-Biomedic, while smaller companies leverage scientific specialization and direct-to-consumer channels to capture market share.

Technology integration becomes a key differentiator as companies develop proprietary strain libraries, personalized microbiome testing platforms, and AI-driven formulation optimization systems that enable customized product recommendations based on individual skin microbiome profiles. White-space opportunities emerge in underserved segments including men's probiotic skincare, pediatric formulations, and therapeutic applications for specific dermatological conditions where clinical evidence supports probiotic intervention.

Emerging disruptors focus on precision diagnostics and personalized formulations, utilizing genomic analysis and machine learning to develop targeted probiotic treatments that address individual microbiome imbalances. Patent filings increasingly concentrate on delivery systems that maintain probiotic viability, novel strain combinations with synergistic effects, and formulation technologies that combine probiotics with complementary active ingredients, indicating strategic focus on technological differentiation rather than marketing-driven positioning.

Probiotic Cosmetic Products Industry Leaders

-

L'Oréal S.A.

-

Johnson & Johnson

-

Unilever

-

The Estée Lauder Companies Inc.

-

Procter & Gamble

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Following the partnership announcement with YUN NV, Bausch Health introduced the YUN ACN skincare line in Poland, which featured probiotic and prebiotic formulations designed for acne-prone skin. The product range included YUN ACN Repair Cream, Wash gel, and Micellar water, all of which supported the skin's natural microbiome without the drawbacks of traditional acne treatments.

- December 2023: L'Oréal announced the acquisition of Lactobio, a Copenhagen-based leader in probiotic and microbiome research. This acquisition enhanced L'Oréal's existing 20-year research into the microbiome, the community of microorganisms on the skin, and strengthened its position in this scientific field. The acquisition also aimed to leverage Lactobio's expertise and intellectual property to develop innovative cosmetic solutions involving live bacteria.

- September 2022: BioGaia and Skinome collaborated on the research and development of a product with live bacteria that could improve skin health in a natural way by supporting the skin microbiome. The first product, Skinome Probiotic Concentrate, became available to consumers since september of 2022. Skinome Probiotic Concentrate combined a strain of live Limosilactobacillus reuteri with a minimal number of skin identical ingredients, such as squalene which had the same structure and characteristics as human sebum to soften, improve elasticity and strengthen the skin barrier.

Global Probiotic Cosmetic Products Market Report Scope

Probiotic cosmetic products are beauty products that contain specific strains of probiotic microbes that are beneficial for skin health.

The probiotic cosmetic products market is segmented by product type, distribution channel, and geography. Based on product type, the market is segmented into skincare, haircare, and other product types. Based on the distribution channel, the market is segmented as specialty stores, supermarkets/hypermarkets, convenience stores, online retail, and other distribution channels. The scope includes a detailed analysis of regions including North America, Europe, Asia-Pacific, South America, and Middle East & Africa by geography.

For each segment, the market sizing and forecast have been done based on value (in USD million).

| Skin Care | Moisturizers and Creams |

| Cleansers and Toners | |

| Others | |

| Hair Care | Shampoos and Conditioners |

| Others | |

| Color Cosmetics | Facial Cosmetics |

| Others |

| Supermarkets/Hypermarkets |

| Health and Beauty Stores |

| Online Retail Stores |

| Other Distribution Channels |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| Rest of Middle East and Africa |

| By Product Type | Skin Care | Moisturizers and Creams |

| Cleansers and Toners | ||

| Others | ||

| Hair Care | Shampoos and Conditioners | |

| Others | ||

| Color Cosmetics | Facial Cosmetics | |

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Health and Beauty Stores | ||

| Online Retail Stores | ||

| Other Distribution Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How fast is revenue expected to grow for probiotic cosmetic products between 2026 and 2031?

Revenue is projected to expand at a 8.95% CAGR, taking the sector from USD 389.88 million in 2026 to USD 598.98 million by 2031.

Which product type currently captures most demand?

Skin care dominates, holding 89.62% revenue share in 2025, thanks to robust clinical evidence for barrier repair and anti-inflammatory effects.

What segment is forecast to post the fastest growth?

The hair-care sub-segment leads with a 9.12% projected CAGR through 2031 as probiotic actives gain traction for scalp health.

Which sales channel is expanding quickest?

Online retail is advancing at 9.55% CAGR because direct-to-consumer brands use educational content and personalized quizzes to drive conversion.

Page last updated on: