Private Credit Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.96 Trillion |

| Market Size (2031) | USD 3.48 Trillion |

| Growth Rate (2026 - 2031) | 12.13% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Private Credit Market Analysis by Mordor Intelligence

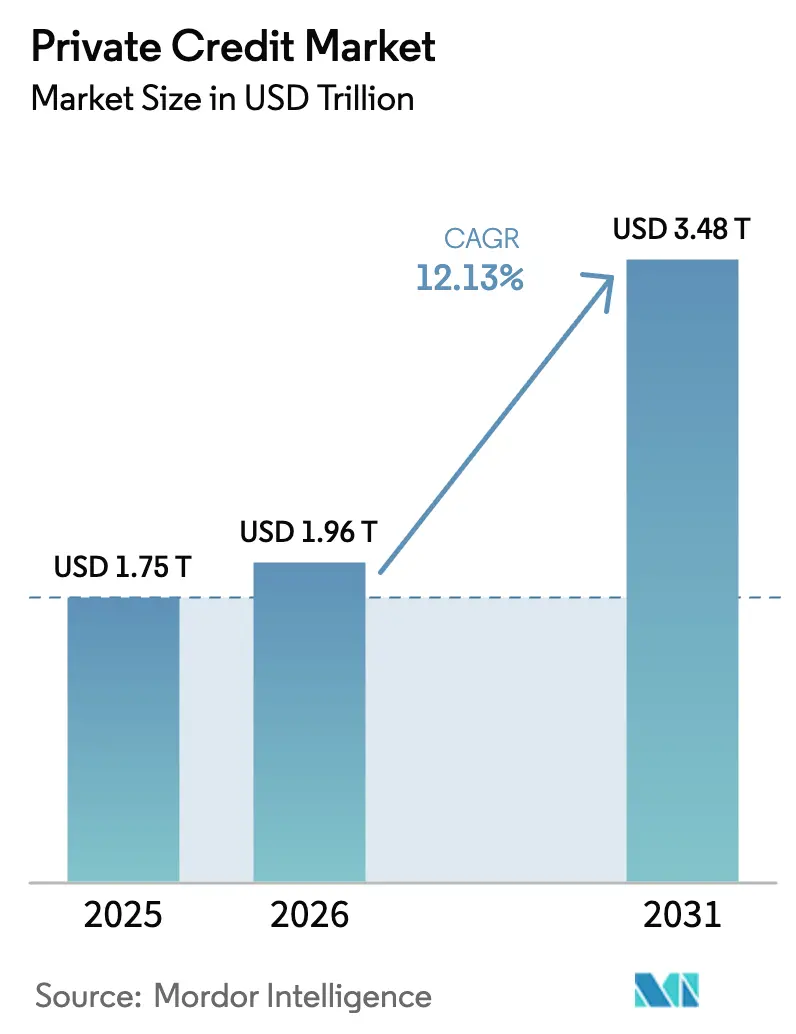

The Private Credit Market size is projected to expand from USD 1.75 trillion in 2025 and USD 1.96 trillion in 2026 to USD 3.48 trillion by 2031, registering a CAGR of 12.13% between 2026 to 2031.

The growth path reflects the shift from an alternative asset class to a mainstream financing channel that now supports a wide range of middle-market and large corporate borrowers. Competitive tension from banks has increased since late 2025, which is likely to moderate pricing and growth while not changing the long-term adoption trend. Structural bank capital constraints under finalized and pending Basel frameworks continue to steer select lending exposures toward nonbank channels, which supports ongoing origination for the private credit market. Platform scale and specialization are differentiators, as managers expand into asset-backed finance and risk transfer partnerships with banks to sustain deal flow and defend returns.

Key Report Takeaways

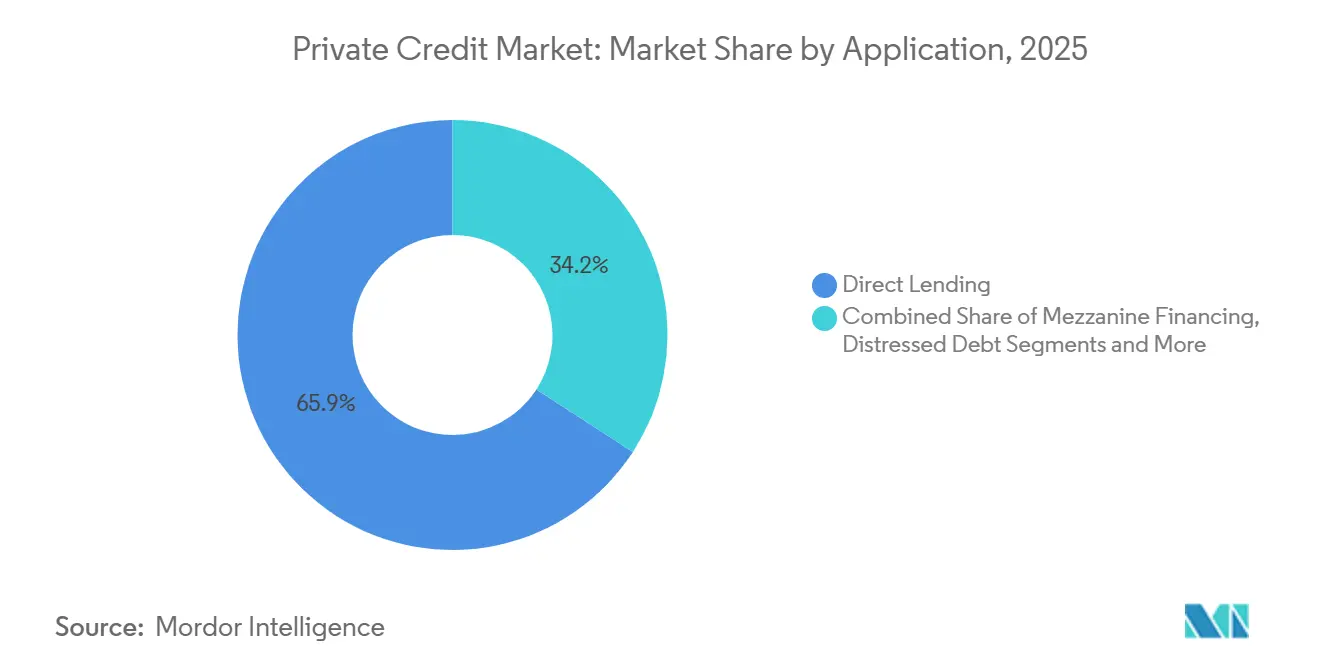

- By application, direct lending led with 65.85% revenue share of the private credit market in 2025, while specialty finance is forecast to expand at a 13.97% CAGR to 2031.

- By end user, small and medium enterprises accounted for a 65.25% share of the private credit market in 2025, and large corporations are projected to grow at an 11.20% CAGR through 2031.

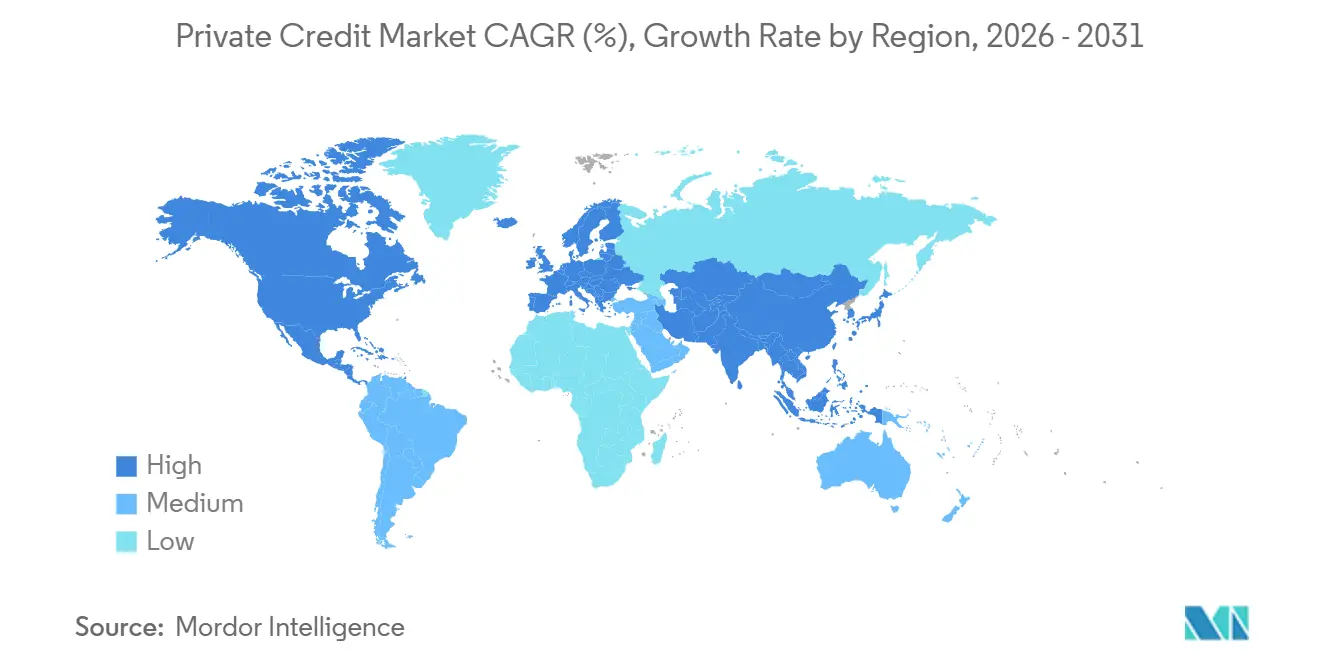

- By geography, North America held 60.12% of the private credit market in 2025, and the Asia Pacific is projected to advance at a 12.50% CAGR to 2031 on its current trajectory of expansion.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Private Credit Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bank retrenchment under Basel III Endgame raises bank capital costs, shifting corporate lending to private credit | +3.2% | Global, with near-term concentration in North America and acceleration in Europe from 2026 onward as Basel IV phases in | Short-term (≤ 2 years), intensifying through 2026-2027 implementation |

| Refinancing and maturity walls in leveraged finance and CRE create multi-year private credit deal flow | +2.8% | North America (primary), Europe (secondary), with CRE maturity concentration in US Sunbelt markets and European gateway cities | Medium term (2-4 years), peaking in 2026-2028 maturity cycle |

| Insurance capital accelerates allocations to private credit as Solvency II/NAIC clarifications improve capital efficiency | +2.1% | Global, with leading uptake in North America by life insurers and European insurers under the Solvency II framework | Medium term (2-4 years), institutionalizing by 2027-2028 |

| Bank risk-transfer deals (SRT/CRT) open a new flow of assets to private credit platforms | +1.7% | Europe (dominant, USD 550 bn+ annual SRT issuance), North America (accelerating, record US activity in 2024-2025) | Short to medium term (≤ 3 years), with regulatory tailwinds through 2027 |

| NAV financing and private credit secondaries expand liquidity and the addressable market | +1.9% | North America (mature), Europe (growth phase), with emerging activity in Asia-Pacific secondary markets | Medium to long term (2-5 years), institutionalizing as LP liquidity tools normalize |

| AI/data-center and energy transition capex require bespoke, large-ticket private financings | +2.4% | North America (AI infrastructure), Europe, and APAC (energy transition), with project-finance concentration in renewable-heavy regions | Long-term (≥ 4 years), with front-loaded AI capex in 2026-2027 and sustained energy-transition deployment through 2031 |

| Source: Mordor Intelligence | |||

Basel III Endgame and Bank Lending Retrenchment

United States and European regulatory reforms are recalibrating capital allocation at large banks, which is raising the relative capital intensity of select corporate, leveraged, and project finance exposures and reinforcing a shift in lending activity toward nonbank channels. European lenders are already acting under Basel 3.1 through greater use of significant risk transfer to optimize risk-weighted assets, evidenced by ABN AMRO’s inaugural USD 2.35 billion portfolio SRT that reduced risk-weighted assets by USD 1.88 billion[1]ABN AMRO Press Office, “ABN AMRO Announces Significant Risk Transfer Transaction with Blackstone,” GlobeNewswire, globenewswire.com. Banks are also using synthetic protection on the United States portfolios to manage concentration and reduce tail risk while retaining client relationships, as shown by Deutsche Pfandbriefbank’s SRT, where credit protection covered a mezzanine tranche of a performing United States loan book[2]Deutsche Pfandbriefbank Strikes $2 Billion SRT Deal with Oaktree,” Sahm Capital, sahmcapital.com. These actions create steady, diversified asset flow to private credit platforms that specialize in first loss and mezzanine tranches, which can meet banks’ capital relief goals and deliver attractive risk adjusted returns to investors. As implementation timelines continue in Europe and the United Kingdom, and as United States rulemaking advances, the private credit market retains a structural role as a complementary source of financing alongside banks.

Refinancing Wall Dynamics and Maturity-Driven Deal Flow

A multi year refinancing cycle across leveraged finance and commercial real estate is increasing demand for bespoke recapitalizations and senior plus capital structures that the private credit market can price and deliver with speed and certainty. Tighter bank underwriting and floating rate cost pressures elevate the need for hybrid solutions that blend senior secured debt, mezzanine layers, and preferred equity to bridge valuation gaps that arose from the low rate 2020 2021 issuance window. The result is a larger opportunity set in sectors that face maturity concentration, where private vehicles can tailor structures to asset quality, business plan, and sponsor profile rather than rely on standardized syndication. Managers with asset backed expertise and restructuring know how are positioned to underwrite DSCR sensitive properties and operating companies with variable cash flows, allowing prudent leverage and tighter covenants to protect downside. The private credit market is therefore not only a lender of last resort in these cycles but a primary liquidity source that can stabilize healthy borrowers and accelerate resolution for weaker credits.

Insurance Capital Allocation and Regulatory Clarity

Dedicated infrastructure and private credit vehicles are attracting life insurer allocations as floating rate income, structural protections, and lower mark-to-market volatility align with long-dated liabilities. Recent fund closes in infrastructure credit and energy transition finance indicate expanding pipelines for investment-grade equivalent structures that meet insurers’ capital efficiency and yield targets. As insurers standardize allocations to private credit sleeves, managers with robust origination, servicing, and reporting can offer longer tenors and features like cash sweeps and ratings-linked step-ups that fit regulatory and ALM constraints. These shifts help fund senior and senior plus lending to core sectors such as utilities, digital infrastructure, and contracted renewables, broadening the addressable base for the private credit market beyond sponsor-backed corporate loans. In turn, diversified insurer mandates can reduce cyclicality in fundraising and sustain deployment even as public markets reopen.

Bank Risk Transfer and SRT/CRT Market Expansion

Risk transfer is now a core channel linking bank balance sheets with private capital, where mezzanine and first loss tranches allow banks to release capital and continue client coverage. ABN AMRO’s first SRT with a private credit platform enabled capital relief on a large corporate portfolio, illustrating how European banks can de risk while maintaining origination and servicing. Deutsche Pfandbriefbank’s synthetic protection on a United States office loan book shows how SRTs can be tailored to specific asset classes and strategic pivots, including market exits. For investors, SRTs offer diversified exposure to seasoned portfolios with defined loss absorption roles and governance, which can produce mid to high single digit unlevered returns with meaningful downside buffers. As banks standardize these programs, private credit platforms with quantitative risk analytics and sector specialists can scale participation across corporate, CRE, and consumer pools.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Spread compression from reopened syndicated markets narrows the private credit illiquidity premium | -1.8% | North America (primary impact), with secondary compression in European large-cap segments as BSL markets re-engage | Short term (≤ 2 years), intensifying through 2026 if bank lending accelerates post-regulatory relief |

| Documentation erosion (loose maintenance covenants, LME risk) can increase loss severity | -1.3% | Global, with a concentration in North America, large-cap/upper mid-market deals, and European mega-transactions over USD 588.1 million | Medium term (2-4 years), materializing in default cycles as covenant protections prove inadequate |

| Valuation opacity and thin secondary liquidity elevate exit risk and NAV smoothing concerns | -0.9% | Global, with acute focus on semi-liquid retail vehicles in North America and evergreen structures capturing high-net-worth allocations | Short to medium term (≤ 3 years), crystallizing if redemption pressures force asset liquidations at discounts |

| Regulatory recalibration risk (Basel re-proposal, NAIC RBC tweaks) may soften bank pullback or raise insurer capital | -0.7% | North America (Basel Endgame revision uncertainty), Europe (ongoing Basel IV implementation monitoring) | Medium term (2-4 years), dependent on 2026-2027 regulatory finalization cycles |

| Source: Mordor Intelligence | |||

Spread Compression and BSL Market Competition

Reopened syndicated markets have tightened pricing and increased refinancing optionality for upper mid-market and large-cap borrowers, which compresses the illiquidity premium that supported recent private credit returns. As competition rises, deal terms trend toward borrower-friendly structures, with some transactions clearing at spreads that are closer to BSL levels[3]Spread Compression and BSL Market Competition . The impact is most visible in larger club deals where sponsors can syndicate risk across multiple lenders in either channel, pressuring private terms unless lenders enforce discipline on leverage, covenants, and documentation. Scale platforms with deep origination pipelines and sector breadth can be more selective, but mid-tier managers face deployment pressure that can erode risk-adjusted returns. In contrast, true middle market niches with smaller EBITDA still support firmer pricing and stronger creditor protections, which sustain differentiation for specialist lenders.

Documentation Erosion and LME Risk

Looser documentation in select segments reduces early warning visibility and can weaken bargaining positions during restructurings, which raises loss severity risk. Liability management exercises that subordinate non-participating lenders or move collateral can further depress recoveries if covenants and baskets are expansive. The effect is most acute in highly competitive, larger deals where speed and certainty command premiums and lenders accept weaker terms to win mandates[4]Global Legal Group Editorial Team, “Overview and Comparison of the Broadly Syndicated Loan and Private Credit Markets,” Global Legal Insights, globallegalinsights.com. In the lower mid-market, tighter financial maintenance covenants and bespoke reporting can moderate severity and enable earlier interventions that support creditor outcomes. Managers who maintain documentation discipline and align structures with cash flow durability can better navigate the next default cycle.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Specialty Finance Leads Growth Amid Direct Lending Maturity.

Direct lending accounted for 65.85% of the 2025 private credit market share, anchored by sponsor-backed buyouts and middle-market corporate financing, where untrenched and senior plus structures deliver certainty and speed. Sponsors have increasingly selected direct lenders as lead providers for leveraged transactions, which supports scale and consistency of deployment for large platforms with strong relationships. While competition is moderating forward growth in this segment, discipline around leverage, cash interest coverage, and governance keeps performance aligned with the profile of senior secured portfolios. In parallel, bank retrenchment in select corporate exposures and active risk transfer programs expand flow to nonbank channels, which supports steady origination even as public windows reopen. As a result, the private credit market continues to provide reliable sponsor finance, while pushing managers to differentiate on underwriting quality, sector focus, and portfolio construction.

Specialty finance is the fastest-growing application with a 13.97% CAGR to 2031, reflecting the rise of asset-backed finance, NAV lending, and credit secondaries as scaled, institutional strategies within the private credit market. Asset backed finance is gaining traction because collateral, structural features, and shorter durations can offset spread compression, while diversified loan pools help mitigate idiosyncratic risk. NAV lending has become a durable portfolio level tool, evidenced by record fund closes and balanced deployment across North America and Europe. Credit secondaries add another liquidity path for LPs and GPs and are now supported by multi billion dollar dedicated vehicles from leading platforms. Together, these strategies expand the private credit market size at the application level by adding diverse pools of risk that complement corporate direct lending and support smoother deployment across cycles.

By End User: SME Dominance Meets Large Corporate Growth

Small and medium enterprises held 65.25% share in 2025 as banks streamlined middle market balance sheets and private lenders filled the execution gap with bespoke structures, faster timelines, and consistent close rates. These borrowers value certainty, covenant frameworks matched to cash flow profiles, and relationship driven monitoring, which are features that scaled lenders can standardize without sacrificing diligence. The segment benefits from tighter maintenance terms than large cap deals, creating room for earlier interventions that can reduce loss severity and improve outcomes. Non sponsor finance has also grown in selective geographies where founder owned companies prefer non dilutive capital and service oriented partners. As banks re enter some mid market niches, the private credit industry still maintains a strong edge in speed, confidentiality, and capital structuring flexibility that SMEs require.

Large corporations are the fastest growing end user group at 11.20% CAGR to 2031, driven by AI data center buildouts, digital transformation, and select large cap LBOs where private credit clubs can match size and execution certainty. Public issuance has financed much of the near term capex, yet private facilities are integral to funding bespoke projects, securing specialized collateral, and aligning cash flows with long term contracts. Infrastructure, renewables, and digital assets sit at the center of this growth wave, given contracted offtake, real asset collateral, and supportive policy environments that reduce volatility. As a result, the private credit market size for large corporate borrowers is expanding through a mix of senior secured project debt, structured solutions, and club financings that complement public market capacity. Forward momentum depends on discipline around leverage, pricing, and documentation to preserve risk adjusted returns as competition increases.

Geography Analysis

North America held 60.12% of the private credit market in 2025, supported by the region’s deep sponsor ecosystem, institutional capital pools, and non traded vehicles that expanded access for a broader investor base. Fundraising slowed in late 2025 as borrowers tapped reopened public channels and banks re engaged on select leveraged financings, which contributed to tighter spreads in upper mid market deals. Even so, the private credit market continues to anchor sponsor backed transactions with execution speed and relationship depth, while serving as a liquidity backstop for maturities that require structured solutions. The private credit market share in North America remains supported by scaled platforms with cross cycle underwriting records and sector specialization.

Europe’s growth accelerated in 2025 as Basel 3.1 implementation raised capital costs for select bank exposures and directed balance sheets toward risk transfer, which expanded origination opportunities for large private lenders. Deployment and deal counts reached record levels in the region, reflecting both sponsor activity and growing demand from founder-owned businesses that value certainty and confidentiality. European banks’ use of SRT structures shows a durable path for banks and private lenders to collaborate on capital optimization, which expands the private credit market’s addressable pool across corporate and real estate assets. As regional regulations like CCD2 for consumer credit take effect, lenders are refining processes, disclosures, and oversight, which should improve transparency and investor confidence.

Asia Pacific is the fastest growing region with a projected 12.50% CAGR, supported by supply chain shifts, infrastructure buildouts, and regulatory evolution that enable more flexible nonbank lending. Dedicated Asia private credit funds have scaled, with managers targeting healthcare, education, logistics, real estate, and digital infrastructure across major markets with creditor friendly regimes. Real estate and infrastructure financing underpin much of the regional demand as local banks face balance sheet constraints and sponsors seek quick closes. On this path, the private credit market size in the Asia Pacific is set to rise as specialized managers expand origination and adapt structures to local legal frameworks while maintaining global risk standards.

Competitive Landscape

Scale remains a critical advantage in the private credit market as leading platforms leverage large balance sheets, broad sponsor coverage, and integrated asset based and corporate capabilities to win mandates. Golub Capital reported a record year of financing commitments and new capital raised in 2025 while expanding European capabilities and securitization activity, which strengthens origination and funding diversification. Quality-focused underwriting and senior secured orientation continue to differentiate performance and maintain low nonaccrual rates relative to broader leveraged credit proxies. At the same time, specialty finance strategies have gained share within platform mixes as managers expand asset-backed, NAV, and secondaries sleeves to defend yields and cycle-proof deployment.

Strategic partnerships with banks are another defining feature as SRT programs become repeatable and scalable, aligning bank RWA relief with investors’ return objectives. ABN AMRO’s corporate portfolio SRT with a private credit manager and Deutsche Pfandbriefbank’s synthetic protection on United States loans show how European banks are operationalizing capital optimization. These collaborations broaden private platforms’ access to diversified pools, increase data visibility, and enable portfolio construction that blends corporate and asset backed exposures. Firms that invest in analytics, servicing, and governance standards can secure recurring allocations in these programs and deepen bank relationships.

Product innovation and capital formation trends underscore the market’s institutionalization. Ares closed about USD 7.1 billion for its Credit Secondaries strategy in early 2026, citing demand for LP led sales and continuation vehicles backed by senior secured private credit portfolios. Evergreen and semi liquid formats are growing in select channels, while insurance mandates support longer tenor structures with ratings features. In this environment, disciplined managers emphasize documentation strength, governance rights, and asset selection to balance spread compression and maintain downside protection across cycles.

Private Credit Industry Leaders

Ares Management

Blackstone

Goldman Sachs Asset Management

HPS Investment Partners

Apollo Global Management

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Ares Management Corporation closed approximately USD 7.1 billion for its Credit Secondary strategy, including the final closing of its inaugural Ares Credit Secondary Fund (ACS) and affiliated vehicles, securing about USD 4 billion in LP equity commitments and exceeding its USD 2 billion target, targeting predominantly senior secured, private equity-backed, and floating rate private credit portfolios.

- February 2026: Power Sustainable Infrastructure Credit announced a final close in December 2025 with total capital aligned exceeding USD 1 billion across the fund and SMAs, targeting tailored financing solutions across energy, transport, digital, social, and recycling.

- January 2026: Golub Capital reported closing over USD 25 billion in financing commitments and raising USD 20.5 billion in new investment capital in 2025, expanding its European presence and ranking as the number one middle market CLO issuer.

- December 2025: ABN AMRO announced a significant risk transfer transaction with funds managed by Blackstone, providing first loss protection for a USD 2.35 billion portfolio of large corporate loans and expected to reduce risk weighted assets by USD 1.88 billion.

Global Private Credit Market Report Scope

Private credit involves non-bank lenders extending loans, primarily to small and medium-sized enterprises (SMEs) with non-investment grade status. This report provides a comprehensive analysis of the private credit market. It explores market dynamics, underscores emerging trends across various segments and regions, and offers insights into various product and application types. Furthermore, the report examines key players and the competitive landscape.

The Private Credit Market Report Segmented by Application (Direct Lending, Mezzanine Financing, Distressed Debt, and Specialty Finance), by End-User (Small and Medium Enterprises (SMEs) and Large Corporations), and by Geography (North America, South America, Europe, Asia-Pacific, and Middle East & Africa). The Report Offers Market Size and Forecasts for the Private Credit Market in Value (USD) for all the Above Segments.

| Direct Lending |

| Mezzanine Financing |

| Distressed Debt |

| Specialty Finance |

| Small and Medium Enterprises (SMEs) |

| Large Corporations |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX (Belgium, Netherlands, Luxembourg) | |

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Application | Direct Lending | |

| Mezzanine Financing | ||

| Distressed Debt | ||

| Specialty Finance | ||

| By End-User | Small and Medium Enterprises (SMEs) | |

| Large Corporations | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX (Belgium, Netherlands, Luxembourg) | ||

| NORDICS (Denmark, Finland, Iceland, Norway, Sweden) | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the private credit market size and projected growth to 2031?

The private credit market size is USD 1.75 trillion in 2025 and USD 1.96 trillion in 2026, with a forecast of USD 3.48 trillion by 2031 at a 12.13% CAGR for 2026 2031.

Which applications lead and which are growing fastest within private credit?

Direct lending led with 65.85% share in 2025, while specialty finance is the fastest growing application with a 13.97% CAGR through 2031.

How is regional growth distributed in private credit today?

North America held 60.12% of the market in 2025, and Asia Pacific is the fastest growing region with a projected 12.50% CAGR supported by infrastructure and supply chain shifts.

What factors are most supportive of private credit in 2026?

Structural bank capital rules, refinancing needs, insurance allocations, bank risk transfer deals, and capex for AI and energy transition are key drivers supporting origination and deployment in 2026.

What are the main headwinds for private credit in the near term?

Spread compression from reopened syndicated markets and weaker documentation in larger deals can pressure returns and raise loss severity risk in workouts.

Which end user groups drive demand in private credit?

SMEs held 65.25% share in 2025, and large corporations are growing fastest at 11.20% CAGR, driven by digital infrastructure and energy transition projects.

Page last updated on: