Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

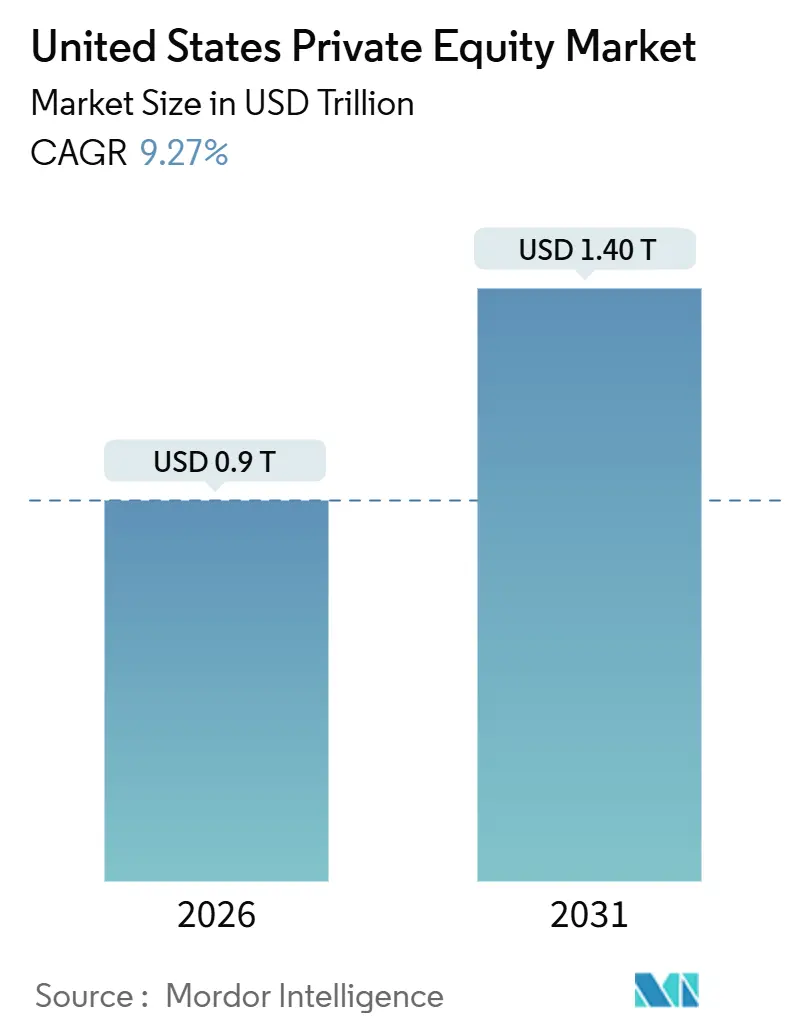

| Market Size (2026) | USD 0.9 Trillion |

| Market Size (2031) | USD 1.40 Trillion |

| Growth Rate (2026 - 2031) | 9.27% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Private Equity Market Analysis by Mordor Intelligence

The United States private equity market size is USD 900.16 billion in 2026 and is projected to reach USD 1,402.46 billion by 2031 at a 9.27% CAGR. This growth path reflects stronger deployment of dry powder, easier accredited-investor verification for Rule 506(c) offerings, and a wider pipeline of corporate carve-outs that align with operational value creation. Valuation discipline remains a core theme as sponsors compete with strategic acquirers and sovereign funds that bid aggressively for high-quality assets, which intensifies the need for operational transformation to offset thinner multiple arbitrage. The reacceleration reflects three structural shifts: first, dry-powder reserves now exceed USD 880 billion among US-based funds as of September 2025, creating deployment pressure that pushes sponsors toward mid-market platforms and add-on strategies. Liquidity management continues to evolve as continuation vehicles and secondaries provide interim distributions while preserving upside in core assets.

Key Report Takeaways

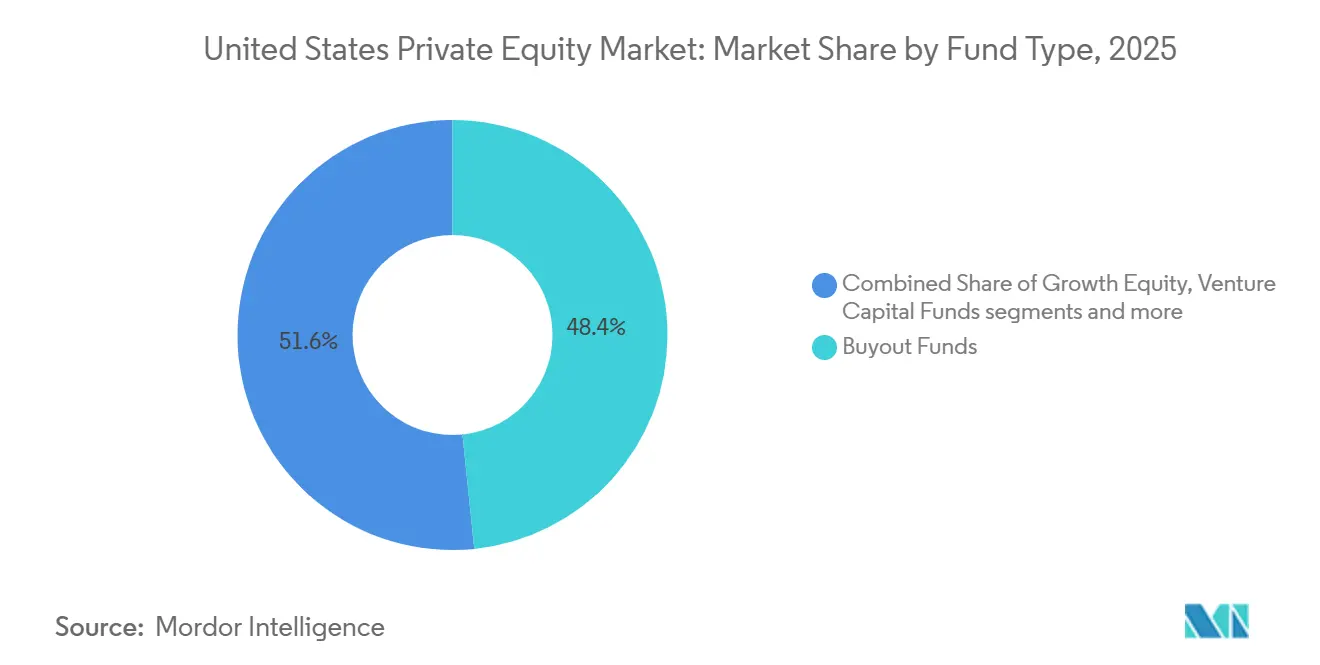

- By fund type, Buyout Funds led with 48.39% market share in 2025, while Venture Capital Funds are projected to expand at a 12.37% CAGR through 2031.

- By sector focus, Technology & Software commanded 33.24% share in 2025, while Healthcare & Life Sciences is forecasted to grow at a 14.39% CAGR to 2031.

- By deal size, Mid-Cap transactions held 42.34% share in 2025, while Small-Cap deals are projected to grow at an 8.39% CAGR through 2031.

- By investor type, Pension Funds accounted for a 36.83% share in 2025, while Family Offices & HNWIs are expected to grow at a 9.38% CAGR to 2031.

- By geography, the Northeast accounted for 41.64% of activity in 2025, while the West is projected to grow at a 12.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United States Private Equity Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Dry-Powder Levels from U.S. Institutional Allocations | +2.1% | Global, with core concentration in the Northeast (NY) and the West (CA) financial hubs | Medium term (2-4 years) |

| Digitization-Led Deal Flow in Software & Tech-Enabled Services | +2.8% | National, with early gains in Silicon Valley, Seattle, and Austin that will spill over to mid-market tech corridors | Short term (≤ 2 years) |

| Generational Succession in U.S. Mid-Market Businesses Creating Buyout Targets | +1.6% | Midwest manufacturing belt (IL, OH, MI), South (TX, GA), Northeast SME clusters | Long term (≥ 4 years) |

| SEC Marketing-Rule Relaxation Expanding Accredited-Investor Pool | +1.3% | National, with outsized benefit for evergreen fund managers targeting retirement plans | Medium term (2-4 years) |

| Energy-Transition Mandates Driving Infrastructure & Renewables PE Funds | +0.9% | West (CA solar and wind, CO grid modernization), South (TX battery storage), APAC spillover to MEA | Long term (≥ 4 years) |

| Corporate Carve-outs Accelerating as Conglomerates Refocus on Core | +0.5% | National, with notable activity in Midwest industrials, South energy assets, Northeast pharma and tech | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Dry-Powder Levels from U.S. Institutional Allocations

Global private equity dry powder reached USD 2.51 trillion by mid-June 2025, with United States-based funds holding roughly USD 880 billion, which sustains a strong deployment agenda across the United States private equity market. Allocators continued to raise target weights in late 2024 and 2025, and a meaningful portion of investors signaled intention to raise commitments through 2026 despite slower distributions, which prolongs the reinvestment cycle within the United States private equity market. Time pressure has grown as more mature assets sit in portfolios awaiting exit windows, so managers prioritize platform strategies and roll-ups where operating levers can shape returns independent of broad market timing within the United States private equity market. Institutions have concentrated commitments in USD 1 billion to USD 5 billion funds that can execute repeatable exits, which reinforces the middle-market’s appeal for proprietary sourcing and integration plays. This dynamic tilts activity toward founder succession, add-on programs, and disciplined bolt-ons, where execution steps can buffer elevated entry multiples and produce clearer value bridges in the United States private equity market.

Digitization-Led Deal Flow in Software & Tech-Enabled Services

Technology’s share of deployment climbed through 2024 and into 2025 as sponsors favored software models with high recurring revenue and predictable retention, which remains a core allocation driver in the United States private equity market. Software deal values rose in 2024 and early 2025, and median revenue multiples moved higher as buyers priced durable growth into platforms positioned for AI and cloud infrastructure needs across the United States private equity market. Generative AI absorbed a large share of venture capital in 2025, which reinforced sponsor appetite for carve-outs of tech-enabled divisions where stand-alone governance can accelerate product roadmaps. Thoma Bravo’s agreement to purchase Boeing’s Digital Aviation Solutions business in April 2025 highlighted the carve-out pipeline from legacy industrials into sponsor ownership inside the United States private equity market. Adoption of AI tools across the investment lifecycle has broadened, as firms automate sourcing, diligence, and portfolio monitoring workflows to expand capacity and improve decision quality in the United States private equity market [1]Thoma Bravo, “Portfolio Companies and Transactions,” Thoma Bravo, thomabravo.com.

SEC Marketing-Rule Relaxation Expanding Accredited-Investor Pool

In March 2025, the SEC staff issued a no-action letter simplifying accredited-investor verification for Rule 506(c) offerings by allowing issuers to rely on minimum investment amounts, which reduces friction for managers engaging a broader accredited base. Before this change, issuers often preferred Rule 506(b) to avoid the verification burden, which limited general solicitation and hampered outreach to new investor cohorts across the United States private equity market. Law firm commentary characterized the update as a catalyst for semi-liquid and evergreen fund structures that can serve mass-affluent pools while maintaining regulatory guardrails. Defined-contribution channels present a sizable opportunity, as product design and fiduciary frameworks evolve to allow private market sleeves within target-date strategies in the United States private equity market. Managers are responding by developing retail-aligned offerings with clearer liquidity, transparency, and fee structures that meet the expectations of the SEC and ERISA.[2]Reed Smith, “SEC Staff Simplifies Accredited Investor Verification for Rule 506 Offerings,” Reed Smith, reedsmith.com

Energy-Transition Mandates Driving Infrastructure & Renewables PE Funds

Global investment into energy-transition infrastructure accelerated through 2024 and 2025 as policy support and cost curves improved, which strengthened the infrastructure sleeve within the United States private equity market. Climate-focused fundraising grew even as broader PE fundraising softened, and sponsors targeted digital infrastructure, grid upgrades, and storage where demand visibility is rising alongside AI computing needs in the United States private equity market. The Inflation Reduction Act created tax incentives, financing support, and long-dated visibility that de-risk clean energy and related manufacturing projects, which aligns with pension and insurer demand for duration-matched returns. Institutional commitments, including large public pension allocations to transition strategies, illustrate how yield-plus-growth profiles fit liability-driven mandates in the United States private equity market. Most newly commissioned renewable projects in 2024 were already more cost-effective than the cheapest fossil alternatives, which reinforces sponsor conviction in stable operating cash flows and scalable platforms.[3]International Renewable Energy Agency, “Renewable Power Generation Costs,” IRENA, irena.org

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SEC Fee-Transparency Crackdown Raising Compliance Costs | -0.7% | National, with acute pressure on mid-sized managers lacking a dedicated compliance infrastructure | Medium term (2-4 years) |

| Sharp Rise in Interest Rates Inflating Leveraged Buyout Financing Costs | -1.2% | National, with greater sensitivity in mid-market deals reliant on syndicated debt | Short term (≤ 2 years) |

| Heightened Competition from SPACs & Strategics Compressing Entry Multiples | -0.8% | National, with bidding wars concentrated in Tech, Healthcare, and Consumer | Medium term (2-4 years) |

| Growing Political & ESG Scrutiny of PE Labor Practices | -0.3% | National, with enforcement concentrated in 19 anti-ESG states and litigation hot-spots | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

SEC Fee-Transparency Crackdown Raising Compliance Costs

SEC enforcement and examination priorities in 2025 sustained a focus on valuation, fees and expenses, custody, and marketing disclosures, which increased fixed overhead for mid-sized managers in the United States private equity market. Actions and penalties related to fee calculation and conflicts of interest required many advisers to invest in personnel, systems, and third-party valuation support. New and amended rules covering incident response, customer notification timelines, and AML program requirements that take effect in 2026 further raise the compliance bar in the United States private equity market. These obligations weigh more heavily on emerging managers that lack scale to amortize costs across larger asset bases, which can accelerate consolidation. Managers are responding with enhanced internal controls, audit readiness, and clearer client communications to reduce regulatory risk within the United States private equity market.[4]Sidley Austin, “2025 Fiscal Year in Review: SEC Enforcement Against Investment Advisers,” Sidley, sidley.com

Heightened Competition from SPACs & Strategics Compressing Entry Multiples

Buyout entry multiples moved higher in 2024 and 2025 as more sponsors and strategic buyers chased fewer scaled platforms, which increased pricing pressure across the United States private equity market. Strategics often paid a premium for assets with product or channel fit, forcing sponsors to justify bids with faster value-creation plans and structured consideration where needed. Creative tools such as earnouts and seller notes became more common to bridge valuation gaps, which added complexity to documentation and post-close governance in the United States private equity market. Elevated entry multiples and lower exit multiples compressed the room for multiple expansion, so operating improvements and margin expansion carried more of the return load. Niche sector specialists with proprietary sourcing and operating playbooks were better positioned to sidestep crowded auctions and protect underwriting discipline within the United States private equity market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fund Type: Venture Capital Races Ahead Despite Buyout Dominance

Buyout Funds commanded 48.39% of the United States private equity market share in 2025, reflecting sponsor preference for mature, cash-flow-generative platforms with reliable exit paths. Venture Capital Funds are projected to grow at a 12.37% CAGR through 2031, supported by the concentration of capital in AI and machine learning that captured a large portion of 2025 deal value in early-stage and growth rounds. Growth Equity Funds represented a notable share of deal flow by count in mid-2025, although large buyout add-ons skewed value toward control transactions across the United States private equity market. Mezzanine and preferred structures gained traction for bridging valuation gaps and managing downside in separation-heavy processes. Infrastructure and energy transition strategies attracted commitments consistent with long-duration needs and stable yield targets within the United States private equity market.

The United States private equity industry continues to diversify across fund types as allocators balance return targets against liquidity and risk preferences. Distressed and turnaround strategies remain a smaller slice but can expand if macro conditions tighten and over-levered assets need restructuring. Large, sector-focused managers with repeatable operating playbooks have broadened their capital menu to include structured equity and private credit, which widens their opportunity set in the United States private equity market. The performance wedge between top-quartile sector specialists and generalists emphasizes the benefit of scale and domain expertise. Managers who demonstrate disciplined underwriting, deep sourcing, and technology-enabled diligence continue to draw support in the United States private equity market.

By Sector Focus: Healthcare & Life Sciences Accelerate on AI-Enabled Diagnostics

Technology & Software captured a 33.24% share in 2025, driven by SaaS, cloud, and data platforms that align with mission-critical workflows in the United States private equity market. Healthcare & Life Sciences is forecasted to grow at a 14.39% CAGR through 2031 as AI-enabled diagnostics, specialty care, and medtech platforms draw sponsor interest. Medtech deal activity and exits picked up in 2025 versus 2024, creating scope for take-privates and carve-outs that can benefit from digital and AI-enabled operating upgrades. Energy, power, and utilities deal flow continued to tilt toward renewables, grid, and storage, reflecting policy support and project finance visibility in the United States private equity market.

The United States private equity industry also saw momentum across financial services and fintech, where payment processing, embedded finance, and wealth platforms attracted sponsor capital. Consumer and residential services platforms grew as managers used buy-and-build strategies to consolidate HVAC, plumbing, and specialty trades that exhibit recurring demand. Industrials and manufacturing benefited from supply chain realignment and domestic capacity additions, which supported roll-up playbooks that create procurement and operations efficiencies in the United States private equity market. Sponsors are allocating more operating resources to data, pricing analytics, and sales enablement within sector platforms to accelerate organic growth. Sector specialists maintain an edge in sourcing and integration, which supports premium underwriting assumptions in the United States private equity market.

By Deal Size: Small-Cap Buy-and-Build Strategies Gain Momentum

Mid-Cap transactions held 42.34% share in 2025 and represented the core of buyout activity by count and value in late 2024 and 2025. Small-Cap deals are projected to grow at an 8.39% CAGR through 2031 as succession-driven sales and regional manufacturing consolidation continue to supply targets for roll-ups in the United States private equity market. Large-cap and mega transactions saw a rebound in the number of USD 5 billion and above deals in 2024, which favored platforms with access to scaled capital and underwriting capacity. Entry multiples for mid-market deals stayed below large-cap levels, which preserved better odds for value creation through operating improvements. Sponsors with sector focus and disciplined integration playbooks achieved stronger relative outcomes in the United States private equity market.

Managers continue to use add-ons to capture regional density, standardize systems, and upgrade pricing strategies to widen margins in the United States private equity market. Deal teams also lean on private credit partners to balance speed and certainty where syndicated markets remain selective. Mega deals experienced slower exit cycles in mid-2025, which pushed some managers to extend hold periods or explore continuation vehicles to align horizons. Selectivity and execution discipline remain the differentiators across the deal-size spectrum in the United States private equity market.

By Investor Type: Family Offices Drive Co-Investment Surge

Pension Funds remained the largest capital supplier with a 36.83% share in 2025, which matches long-duration liabilities to fund life cycles in the United States private equity market. Family Offices & HNWIs are the fastest-growing investor cohort at a 9.38% CAGR through 2031 as co-investment interest and direct exposure increase. Direct deals account for a significant share of family office allocations, and many groups co-invest alongside sponsors to lower fees while accessing scale in the United States private equity market. Endowments and foundations continue to anchor diversified programs, given access to managers and the ability to tolerate illiquidity. Insurance companies and funds of funds maintain steady roles, and corporate LPs appear more frequently as strategic co-investors in the United States private equity market.

The United States private equity industry also sees rising product innovation for individual investors as managers develop semi-liquid vehicles designed for retirement channels. Regulatory interpretation and fiduciary safeguards guide how these products are structured, including transparency and liquidity frameworks. Interest in private markets from the mass-affluent base supports the design of evergreen and interval funds that fit within retirement plan guardrails in the United States private equity market. Distribution partnerships and digital platforms play a larger role in scaling these vehicles. As product structures evolve, fee models align to net asset value rather than committed capital for semi-liquid formats in the United States private equity market.

Geography Analysis

The Northeast accounted for 41.64% of the United States' private equity market share in 2025, anchored by the New York financial hub and the Boston biotech corridor that supports healthcare and software deal pipelines. The region benefits from deep advisory ecosystems and the proximity of leading limited partners, which tightens feedback loops between allocators and managers in the United States private equity market. Legal and accounting infrastructure in the corridor supports separation-heavy transactions and cross-border financings, which positions the region well for carve-outs and complex exits. Regulatory oversight from the SEC’s core offices informs adviser compliance priorities that are often adopted early by Northeast-based managers. The United States private equity market size in the Northeast reflects a concentration of high-value deals that rely on sector specialization and operating expertise.

The West is projected to grow at a 12.38% CAGR through 2031 as Silicon Valley software consolidation and Colorado’s clean energy investments advance. California anchors enterprise software, cloud infrastructure, and AI platforms, and the region’s venture density offers exit optionality through sponsor secondaries and continuation vehicles in the United States private equity market. Compliance considerations tied to climate disclosure rules in California and other states expand diligence requirements for West Coast targets. Arizona and Nevada are developing into data center hubs that serve AI workloads, and Utah’s software corridor supplies vertical-SaaS targets for platform roll-ups in the United States private equity market. These dynamics keep the West an attractive region for both buyout and growth equity sponsors.

The South and Midwest continue to capture inflows supported by corporate relocations, demographic growth, succession-driven founders, and energy transition projects. Texas remains a top destination for energy, technology, and healthcare investments, while Florida shows momentum in healthcare services and logistics in the United States private equity market. North Carolina and Georgia attract capital across fintech and financial services, and government contracting footprints in Virginia and Tennessee add depth to deal pipelines. The Midwest remains fertile for manufacturing and logistics roll-ups where entry multiples often sit below coastal levels and where integration can create value in the United States private equity market. Add-on density remains high in the lower middle market across these regions, which supports national scale strategies under experienced operators.

Competitive Landscape

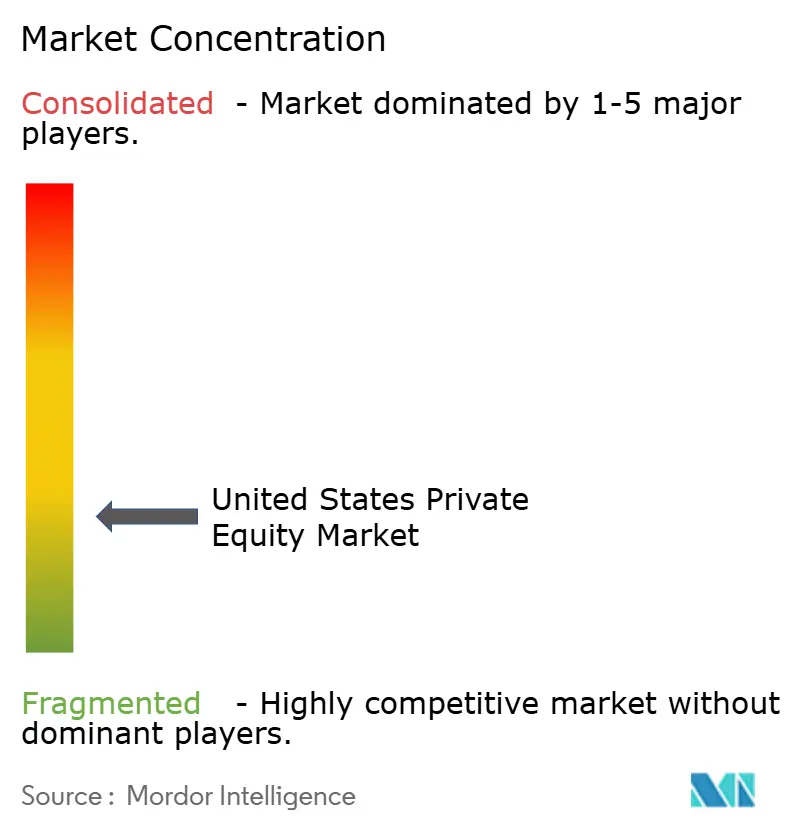

The United States private equity market is moderately concentrated at the top, with the ten largest managers collectively representing a sizable share of assets while leaving significant room for mid-market specialists. Competition has intensified as sovereign wealth funds and large strategics engage more actively in control transactions, which sustains elevated entry multiples and demands sharper operating theses inside the United States private equity market. Sponsors lean into digital toolkits to accelerate sourcing and diligence, and AI adoption in portfolio operations supports sales and service efficiency. For example, firms have deployed AI to reduce call times and lift retention in customer-facing platforms, which helps offset higher financing costs in the United States private equity market. Scale advantages continue to support fund-raising momentum for sector specialists that can demonstrate repeatable exits and disciplined capital rotation.

Managers are repositioning value creation from financial engineering to revenue and margin growth as exit multiples remain below entry levels in many sectors. Add-on acquisitions comprised a significant share of buyout activity in 2025, which aligns with platform strategies that build regional density and unify systems in the United States private equity market. Technology enablement across pricing, procurement, and integration planning has become a baseline expectation for operating teams. Firms have also accelerated secondaries and continuation vehicles to balance liquidity and long-hold theses, which reduces pressure to sell into soft windows in the United States private equity market. Manager selection matters more as performance dispersion widens between top-quartile and median funds.

Select platform examples illustrate the strategic playbook. Thoma Bravo’s carve-out of Boeing’s Digital Aviation Solutions in April 2025 demonstrated conviction in software platforms with mission-critical workflows and scale potential within the United States private equity market. Warburg Pincus continued to expand in financial services through targeted growth investments that leverage operating partnerships to accelerate product and distribution. Brookfield highlighted operating AI to improve customer service outcomes in residential infrastructure, illustrating how sponsors translate technology into measurable KPIs across holdings in the United States private equity market. These moves reflect a broader pivot toward operating intensity and sector depth that underpins competitive advantage.

United States Private Equity Industry Leaders

Thoma Bravo LP

Apollo Global Management, Inc.

Blackstone Inc.

Kohlberg Kravis Roberts & Co. L.P. (KKR)

The Carlyle Group Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Women’s health diagnostics firm Hologic, Inc. agreed to be acquired by affiliates of Blackstone and TPG in a transaction valued at up to USD 18.3 billion, with shareholders to receive a cash payout plus contingent value rights.

- September 2025: Electronic Arts announced a deal to be acquired by an investor consortium led by Saudi Arabia’s Public Investment Fund (PIF) alongside Silver Lake and Affinity Partners in a historic USD 55 billion all-cash transaction, making it one of the largest sponsor-led take-private deals ever.

- August 2025: Human-capital-management software provider Dayforce, Inc., entered into a definitive agreement to be acquired by Thoma Bravo for about USD 12.3 billion, valuing the company at a significant premium and taking it private.

- August 2025: Sycamore Partners finalized its takeover of retail pharmacy and healthcare giant Walgreens Boots Alliance, taking the company private and splitting its businesses into standalone operations under new ownership.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the United States private-equity market as all new capital commitments to professionally managed buyout, growth-equity, venture, secondaries, and infrastructure funds whose primary investment mandate targets U.S.-domiciled portfolio companies. Deal recycling, carried-interest proceeds, and passive minority stakes sold between financial sponsors are counted once, at the fund level, to avoid double counting.

Scope exclusion: angel rounds, crowdfunding platforms, and real-estate-only vehicles fall outside this report's perimeter.

Segmentation Overview

- By Fund Type

- Buyout Funds

- Growth Equity Funds

- Venture Capital Funds

- Mezzanine & Preferred Equity Funds

- Distressed/Turnaround Funds

- Infrastructure & Energy Transition Funds

- By Sector Focus

- Technology & Software

- Healthcare & Life Sciences

- Consumer & Retail

- Industrial & Manufacturing

- Financial Services & FinTech

- Energy, Power & Utilities

- By Deal Size

- Small-Cap (Less than $100 M EV)

- Mid-Cap ($100 M - $1 B EV)

- Large-Cap ($1 B - $5 B EV)

- Mega-Deals (Greater than $5 B EV)

- By Investor Type

- Pension Funds

- Insurance Companies

- Endowments & Foundations

- Funds of Funds

- Family Offices & HNWIs

- Corporate/Strategic LPs

- By Geography (United States)

- Northeast

- Midwest

- South

- West

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed general partners, placement agents, and institutional allocators across the Northeast, Midwest, South, and West. Discussions clarified dry-powder deployment rates, fee step-downs, and typical leverage levels, letting us fine-tune model inputs that raw filings rarely disclose.

Desk Research

We began with core U.S. monetary, pension, and capital-markets datasets issued by bodies such as the Federal Reserve, SEC, and NASRA, complemented by deal and fundraising tallies from trade groups like the American Investment Council and ILPA. Company filings, Form ADV brochures, and select academic journals supplied historical asset-class returns. Where coverage gaps emerged, subscription sources, including D&B Hoovers for manager financials and Dow Jones Factiva for transaction news, helped cross-check totals. This list is illustrative; many additional public documents fed our baseline.

The secondary stack then drew on customs statistics for cross-border capital flows and Questel's patent counts to link technology deal volume to innovation intensity, giving us proxies for sector appetite over time.

Market-Sizing & Forecasting

A top-down construct starts with total private-capital assets under management, subtracts non-U.S. mandates, and applies U.S. deployment ratios derived from Federal Reserve flow-of-funds data. Bottom-up checks, sampled fund counts multiplied by median closing size and mid-market buyout ASP multiplied by deal volume, validate the aggregate before adjustments. Key drivers include: (1) pension PE allocation targets, (2) median enterprise-value/EBITDA exit multiples, (3) leveraged-loan issuance, (4) technology patent growth, and (5) effective federal-funds rate shifts. A multivariate regression mapped these variables to historical commitment growth and then projected commitments through 2030; missing bottoms-up figures were bridged with averaged manager disclosures.

Data Validation & Update Cycle

Outputs face variance screens against independent indicators such as Preqin dry-powder totals and PitchBook deal counts. Senior reviewers re-audit anomalies, and clients receive an annual refresh, with interim updates if material events move the baseline.

Why Mordor's United States Private Equity Baseline Commands Reliability

Published estimates often diverge because firms pick different fund types, booking points, and currency conversions.

Key gap drivers stem from scope breadth, inclusion of unrealized NAV, and whether secondary transactions are double-counted before exit. Our model, refreshed yearly and grounded in verifiable regulator filings, avoids these traps and reports commitments at first-close cash value, giving decision-makers a stable reference.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 820 B (2025) | Mordor Intelligence | - |

| USD 475 B (2024) | Regional Consultancy A | Excludes infrastructure and venture funds, uses venture capital split reported separately |

| USD 464.6 B (2024) | Trade Journal B | Stops at final close commitments, omits dry-powder held for follow-ons |

| USD 3 279.5 B (2025) | Data Publisher C | Adds buyout unrealized NAV and credit strategies, leading to inflated total |

In sum, while other publishers swing wide due to either narrow or overly expansive scopes, Mordor's disciplined selection of fund universe, paired with cross-validated drivers, delivers a balanced, transparent benchmark that stakeholders can replicate and trust.

Key Questions Answered in the Report

What is the current size and growth outlook for the United States private equity market?

The United States private equity market size is USD 900.16 billion in 2026 and is projected to reach USD 1,402.46 billion by 2031 at a 9.27% CAGR.

Which fund types lead and which grow fastest in the United States private equity market?

Buyout Funds led with 48.39% share in 2025, while Venture Capital Funds are projected to grow fastest at a 12.37% CAGR through 2031.

Which sectors show the strongest momentum within the United States private equity market?

Technology & Software led with 33.24% share in 2025, while Healthcare & Life Sciences is projected to expand at a 14.39% CAGR to 2031.

How are financing conditions affecting deals in the United States private equity market?

All-in borrowing costs eased from 2023 peaks but often remain near 9% to 10% for upper mid-market credits, which raises equity checks and increases the focus on operating value creation.

Where is regional activity concentrated in the United States private equity market?

The Northeast accounted for 41.64% of activity in 2025, and the West is projected to grow at a 12.38% CAGR through 2031.

What strategies are sponsors using to address exit and liquidity timing in the United States private equity market?

Managers increasingly use add-ons for scale, continuation vehicles, and secondaries to provide interim distributions while preserving long-term upside.

Page last updated on: