Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

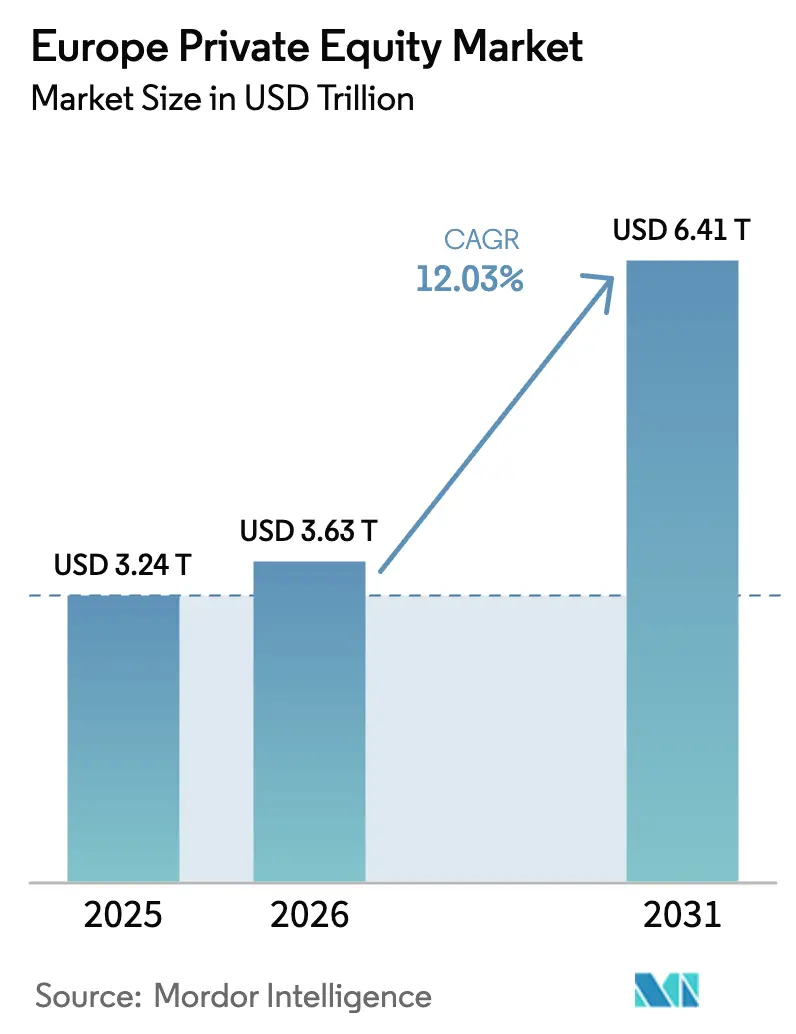

| Base Year Market Size (2025) | USD 3.24 Trillion |

| Market Size (2026) | USD 3.63 Trillion |

| Market Size (2031) | USD 6.41 Trillion |

| Growth Rate (2026 - 2031) | 12.03% CAGR |

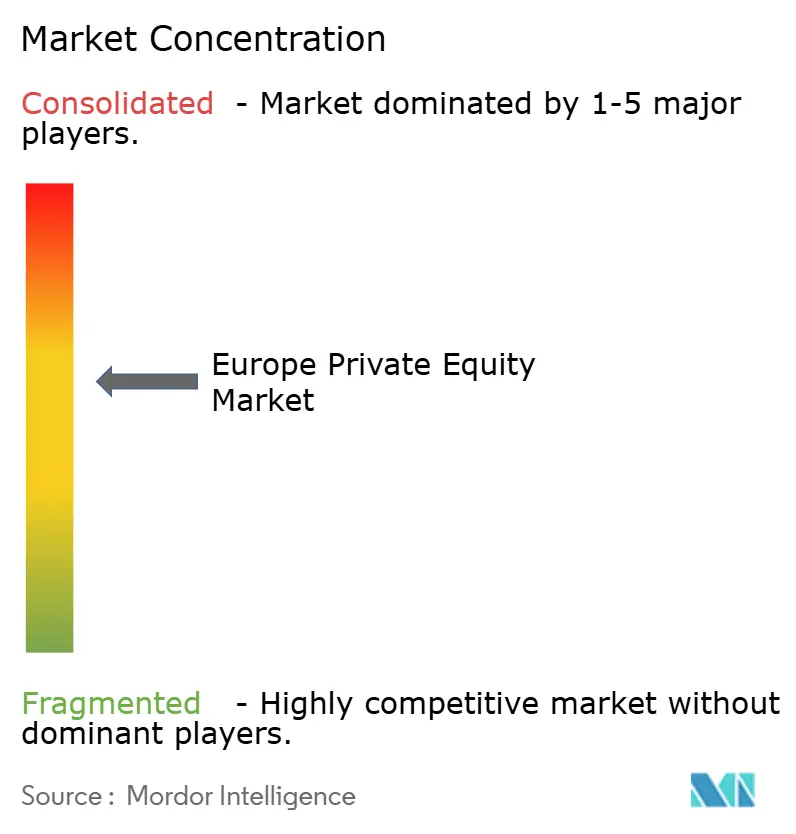

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Private Equity Market Analysis by Mordor Intelligence

Europe private equity market size in 2026 is estimated at USD 3.63 trillion, growing from 2025 value of USD 3.24 trillion with 2031 projections showing USD 6.41 trillion, growing at 12.03% CAGR over 2026-2031. A blend of strong dry-powder deployment pressure, regulatory moves toward sustainable finance, faster digital adoption after the pandemic, and innovative exit tools such as continuation vehicles underpins this expansion. Buyout managers still dominate deal flow, yet secondary and continuation strategies gain traction as institutional investors seek liquidity without exiting the asset class. Technology retains the largest industry allocation while healthcare accelerates fastest, both benefiting from macro themes of digitization and population ageing. At the same time, the United Kingdom keeps its lead in capital raised and deals closed, even as Spain posts the highest forward growth rate due to pro-investment reforms and solid GDP momentum. Competitive intensity rises as mega-managers consolidate assets, but mid-market specialists stay relevant by targeting fragmented European SME niches.

Key Report Takeaways

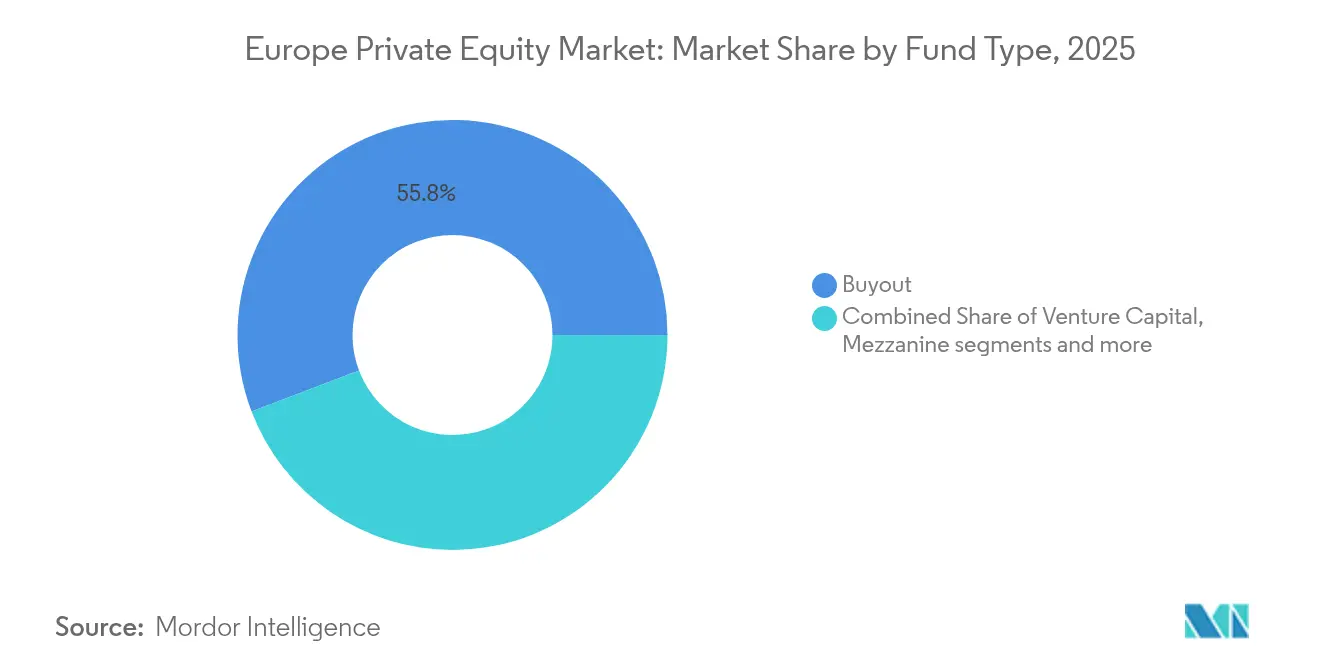

- By fund strategy, Buyout funds held 55.78% of the Europe private equity market share in 2025, whereas Secondaries & Fund-of-Funds record a 12.17% CAGR through 2031.

- By investment size, Upper Middle Market deals captured 43.02% of the Europe private equity market size in 2025, while Small & SMID transactions advanced at an 11.62% CAGR through 2031.

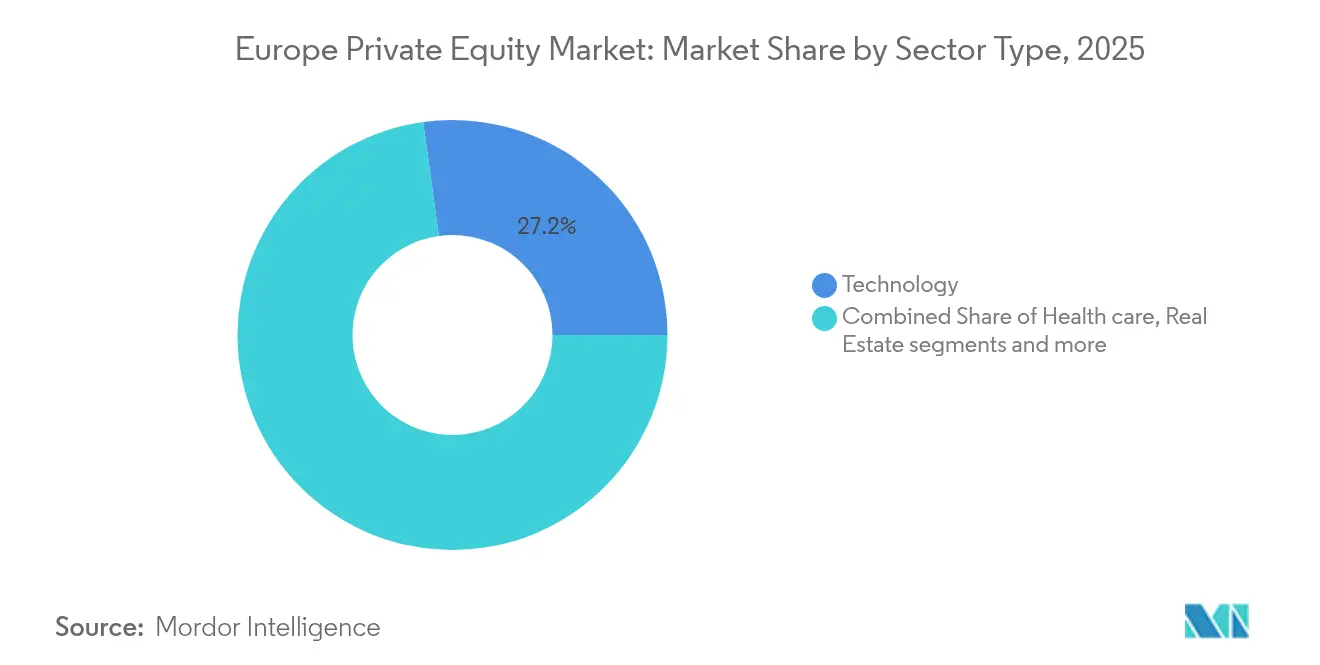

- By sector, Technology accounted for 27.18% of the Europe private equity market share in 2025; Healthcare expands fastest at a 14.22% CAGR to 2031.

- By country, the United Kingdom led with 25.06% revenue share in 2025, as Spain grows at a 10.37% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Private Equity Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent dry-powder overhang and LP pressure to deploy capital | +2.8% | Global – strongest in UK, Germany, France | Short term (≤ 2 years) |

| EU Green Deal incentives steering PE toward sustainability-linked assets | +1.9% | EU-wide – Nordic region, Germany | Medium term (2–4 years) |

| Digital-first business models scaling rapidly in post-COVID Europe | +2.1% | Pan-European – UK, France, Netherlands | Short term (≤ 2 years) |

| Secondary buyout wave driven by fund-to-fund trades | +1.6% | Major European financial hubs | Medium term (2–4 years) |

| Niche funds targeting succession in Mittelstand family businesses | +1.2% | Germany, Austria, Switzerland | Long term (≥ 4 years) |

| Surge in GP-led continuation vehicles unlocking trapped value | +2.0% | UK and Nordic markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent Dry-Powder Overhang and LP Pressure to Deploy Capital

European limited partners now hold unprecedented uncalled commitments, which fuel steady deal activity despite cyclical headwinds. Fundraising reached USD 118.8 billion in the first three quarters of 2024, almost matching the prior year total as pension plans and sovereign funds raised their allocation targets. Average holding periods stretch to 6.7 years, intensifying the need for larger tickets and off-market sourcing to absorb capital. Managers compete for scarce high-quality assets, often agreeing to higher entry multiples while concurrently designing ambitious operational-value plans to sustain returns. This behavior supports near-term growth in the Europe private equity market.

EU Green Deal Incentives Steering PE Toward Sustainability-Linked Assets

The Sustainable Finance Disclosure Regulation pushes Article 8 and 9 funds to nearly two-thirds of Europe’s fund launches. Private equity houses embed ESG targets directly into carried-interest hurdles, aligning teams with emissions-reduction or diversity metrics. The Corporate Sustainability Reporting Directive demands extensive disclosures, raising compliance costs for smaller managers yet rewarding early movers with access to larger pools of capital[1]Invest Europe, “Invest Europe Yearbook 2024,” investeurope.eu . Green-tilted deals in renewables, resource-efficient manufacturing, and circular business models regularly command premium exit valuations, pulling fresh capital into the Europe private equity market.

Digital-First Business Models Scaling Rapidly in Post-COVID Europe

Technology-enabled firms, from SaaS and AI to logistics platforms, maintain resilient topline growth, drawing EUR 24 billion of private equity capital in 2023 alone. Deep-tech investment grew to EUR 15 billion in 2024, while AI-enabled creative suite provider Freepik surpassed 800,000 subscribers. Private equity operators install data-analytics playbooks across portfolio companies to enhance pricing, procurement, and customer retention, creating repeatable value-creation levers. This digital imperative sustains deal flow and multiples within the Europe private equity market.

Secondary Buyout Wave Driven by Fund-to-Fund Trades

Exit windows through IPOs remain narrow, so fund-to-fund deals have risen to the leading exit route. Continuation funds now represent 13% of European exits, granting liquidity to existing LPs while allowing GPs to keep outperforming assets. Transaction structures favor negotiated partnerships rather than auctions, trimming friction costs and reducing bid-ask spreads. The phenomenon keeps assets circulating within the Europe private equity market ecosystem and moderates the impact of public-market volatility on distributions.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Valuation reset amid higher interest rates compressing exit multiples | -2.3% | Global leveraged deals | Short term (≤ 2 years) |

| Regulatory scrutiny on “national champions” deals delaying approvals | -1.1% | France, Germany, Italy | Medium term (2–4 years) |

| Fund-level ESG disclosure costs squeezing smaller GPs | -0.8% | EU-wide mid-market | Medium term (2–4 years) |

| Talent crunch in operational value-creation teams | -0.9% | London, Frankfurt, Paris | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Valuation Reset Amid Higher Interest Rates Compressing Exit Multiples

European Central Bank rate hikes raise discount rates and debt service costs, trimming equity valuations for levered businesses. Lower-growth industrial assets suffer the largest multiple compression, compelling sponsors to lean more on revenue and margin expansion rather than financial engineering[2]Neuberger Berman, “Rates and Valuations,” nb.com. Private debt funds step in to bridge financing gaps, but pricing still trails the record-low coupons of the pre-2022 cycle. This environment weighs on exit proceeds and temporarily tempers expansion momentum in the Europe private equity market.

Regulatory Scrutiny on “National Champions” Deals Delaying Approvals

Deal approvals now require deeper disclosures under the EU Foreign Subsidies Regulation[3]Debevoise & Plimpton, “EU Foreign Subsidies Regulation Insight,” debevoise.com . France, Germany, and Italy tighten screenings for critical-infrastructure and tech assets, extending closing timelines and occasionally forcing buyers to restructure transactions. While not halting activity, these interventions inject execution risk and add diligence costs, particularly for large-cap purchases. This headwind moderately offsets growth in the Europe private equity market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fund Type: Buyout Dominance Faces Secondary Market Disruption

Buyout funds controlled 55.78% of the Europe private equity market in 2025, attracting institutional investors that value strong governance rights and cash flow predictability. Yet, secondaries and fund-of-funds log a 12.17% CAGR to 2031, fueled by record LP demand for liquidity. Continuation funds now comprise 84% of GP-led secondary volume, a structure that extends hold periods without forgoing upside. Main Capital’s USD 603 million software vehicle and Corsair’s USD 600 million fintech continuation fund illustrate this shift. The Europe private equity market size for secondaries is therefore poised to widen materially.

Ongoing regulatory clarity under AIFMD II and the expansion of specialist secondary managers broaden the investor base. Pension boards allocate more to these strategies to smooth cash-flow profiles and dampen vintage-year risk, gradually nudging market share away from pure buyout pools. Even so, flagship buyout franchises retain scale advantages in sourcing and portfolio support, defending their lead in the Europe private equity market.

By Investments: Upper Middle Market Leadership Challenged by Small Cap Acceleration

Upper Middle Market tickets of EUR 100 million - EUR 500 million captured 43.02% of the Europe private equity market size in 2025, contributed by their balance of complexity and liquidity. Small & SMID deals, however, are expanding at an 11.62% CAGR, helped by average 10.2 times EBITDA entry multiples versus 13.3 times in the United States. Europe’s fragmented SME base, 99% of all businesses, offers roll-up potential at favorable valuations.

Sponsors establish dedicated origination teams to surface proprietary small-cap opportunities while leveraging operational playbooks to professionalize management processes quickly. ECB support for domestic credit markets sustains leverage availability for bolt-on acquisitions, reinforcing growth in this niche of the Europe private equity market.

By Sector: Technology Dominance Meets Healthcare Acceleration

Technology retained 27.18% of the Europe private equity market share in 2025, buoyed by software, AI, and digital solutions producing recurring revenue and high margins. Healthcare now posts the fastest advance at 14.22% CAGR as ageing demographics and efficiency reforms fuel demand for provider outsourcing and specialized pharmaceuticals. The Europe private equity market size captured by healthcare assets is projected to rise sharply as buyout groups pursue clinic networks, contract research organizations, and med-tech platforms.

Cross-sector convergence adds upside: sponsors deploy AI into clinical decision support and employ SaaS tools to streamline hospital workflows, thereby lifting exit multiples. Real estate, services, and industrials still draw interest, though growth trajectories lag the two headline sectors.

Geography Analysis

Europe’s private equity hubs remain concentrated, yet performance diverges across jurisdictions. The United Kingdom commands the largest pool of talent, advisors, and exit venues, supporting 25.06% of 2025 deal value. A stable legal regime and deep capital markets aid rapid fundraising and syndication. Germany’s share is anchored by industrial tech and succession-driven mid-market buyouts, exemplified by TPG’s USD 4.5 billion purchase of Aareon. France’s 2024 deal jump stems from reforms that boosted investment caps and overhauled labor laws, coupled with a vibrant TMT pipeline.

Spain’s momentum is striking. Private equity funds there delivered 11.2% net IRR in 2023, and sustainable Article 8/9 funds achieved 14.6%. Spain recorded 1,076 M&A deals worth USD 56.5 billion in 2024, including 264 sponsor transactions. Domestic houses such as Magnum and Portobello launched new vehicles exceeding EUR 2.5 billion, reinforcing fundraising depth. Italy adds diversification: USD 44.6 billion of 2023 deal value represented roughly 40% of its M&A market, with industrials climbing to 28% of activity. Southern Europe overall saw private equity deal value rise 31.4% to USD 93.8 billion even as volumes dipped, pointing to bigger average tickets. Cross-border expansion strategies intensify, with managers leveraging operational expertise across multiple countries to unlock margin gains. Nordic managers sustain global reputations despite smaller home markets, often leading pan-European consortiums. This mix of mature and emerging hotspots creates a balanced, opportunity-rich landscape for the Europe private equity market.

Competitive Landscape

Roughly 11,000 fund managers operate in Europe, yet the top 25 oversee 48% of managed enterprise value, confirming moderate concentration. CVC Capital Partners tops the list with USD 79.7 billion followed by KKR at USD 75.09 billion and EQT at USD 69.5 billion. Scale gives these groups priority access to marquee auctions, co-investment capacity, and technology budgets for data analytics and AI. American and British sponsors collectively manage USD 1.02 trillion, dwarfing German firms’ USD 49.8 billion despite Germany’s industrial heft.

Consolidation continues: publicly listed managers account for 84% of private equity M&A since 2012, buying specialist boutiques to deepen sector coverage. Sector focus sharpens competitive edges, Hg concentrates on TMT, Nordic Capital on healthcare and financial services, while continuation funds, defense assets, and energy transition platforms open fresh white spaces. Talent wars escalate for operating partners skilled in pricing, procurement, and digital transformation, contributing to rising cost structures.

Technology adoption marks the next frontier. Managers pilot AI engines to screen thousands of targets, accelerate diligence, and unlock portfolio efficiencies. ESG credentials also differentiate access to capital and premium valuations, driving investments in measurement systems and sustainability reporting. Overall, the Europe private equity market rewards diversified, tech-enabled, and operationally driven franchises while raising the bar for new entrants.

Europe Private Equity Industry Leaders

Permira partners

EQT

CVC Capital Partners

Apax Partners

Ardian

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Bain Capital and Cinven are reportedly exploring a potential sale of German drugmaker Stada, which could mark one of the region’s largest pharma exits in recent years.

- June 2025: Lone Star exits Novo Banco via a USD 7.4 billion sale to BPCE, one of the region’s largest financial-services deals.

- May 2025: Main Capital has successfully closed a EUR 520 million continuation fund aimed at supporting leading European software companies. This fund underscores the firm’s commitment to backing high-growth software champions across the region, enabling them to accelerate innovation and market expansion.

- May 2025: Corsair has completed a USD 600 million secondary fund focused on European fintech investments. This fund targets established fintech companies to support their growth and market presence.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Europe private equity market as the value of active capital that institutional and high-net-worth investors commit to buyout, growth, venture, mezzanine, secondaries, and fund-of-funds vehicles that deploy equity into privately held European companies or that delist public firms.

Scope exclusion: Infrastructure funds and pure private-credit vehicles are not part of this valuation.

Segmentation Overview

- By Fund Type

- Buyout & Growth

- Venture Capital

- Mezzanine & Distressed

- Secondaries & Fund of Funds

- By Sector

- Technology (Software)

- Healthcare

- Real Estate and Services

- Financial Services

- Industrials

- Consumer & Retail

- Energy & Power

- Media & Entertainment

- Telecom

- Others (Transportation, etc.)

- By Investments

- Large Cap

- Upper Middle Market

- Lower Middle Market

- Small & SMID

- By Country

- United Kingdom

- Germany

- France

- Sweden

- Italy

- Spain

- Netherlands

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Our analysts interviewed European general partners, placement agents, secondaries specialists, and corporate finance lawyers across the UK, DACH, Nordics, and Southern Europe. Conversations clarified carry structures, average holding periods, and fee drags, letting us refine cash-flow curves and stress-test return assumptions.

Desk Research

We began with public filings from the European Securities and Markets Authority, Invest Europe performance digests, and national bank flow-of-funds tables, then added deal counts and pricing benchmarks from PitchBook and Preqin. Trade bodies such as the British Private Equity & Venture Capital Association and Bundesverband Deutscher Kapitalbeteiligungsgesellschaften enriched country splits, while Eurostat macro series anchored currency and inflation adjustments.

Subscription tools from D&B Hoovers and Dow Jones Factiva provided manager AUM and fund-close news that helped reconcile dry-powder estimates. This list is illustrative; many additional open and paid sources informed cross-checks and narrative context.

Market-Sizing & Forecasting

A top-down and bottom-up blend underpins the model. We roll forward Invest Europe fundraising and net asset value data, layer in trade and IPO exit volumes, and validate totals with sampled manager roll-ups and deal-level average selling prices. Key variables include dry-powder rotation rates, leverage multiples, median EBITDA purchase prices, exit-route mix, and euro-sterling differentials. Forecasts employ multivariate regression that links these inputs to GDP growth, policy rates, and public-equity spreads, with scenario analysis used where gaps appear.

Data Validation & Update Cycle

Outputs pass automated variance checks against historical series, followed by peer review and a final sign-off. The model refreshes annually, with interim updates if material events, rate shocks, tax changes, or transformative fund closes shift baseline assumptions.

Why Our Europe Private Equity Baseline Commands Reliability

Published estimates often diverge because each provider chooses its own capital pools, vehicle types, and refresh timing. We disclose those choices upfront and revisit them each year, which keeps our base case steady yet responsive.

Key gap drivers include whether secondary continuation funds are counted, how unrealized gains are marked, and the speed at which foreign-currency investments are translated back to euros. More aggressive figures usually inflate valuations by incorporating infrastructure equity or by marking portfolios at the last funding round without discounting bid-ask spreads.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.24 trn | Mordor Intelligence | - |

| USD 1.50 trn | Regional Consultancy A | Excludes venture and growth funds; limited country coverage |

| USD 0.42 trn | Global Consultancy B | Counts only realized deal value, omits unrealized NAV |

| USD 0.15 trn | Industry Association C | Tracks fund-raising flows, not cumulative invested capital |

These comparisons show that our disciplined scope selection, variable transparency, and annual refresh give decision-makers a balanced, reproducible baseline they can trust.

Key Questions Answered in the Report

What is the current value of the Europe private equity market?

The Europe private equity market size stood at USD 3.63 trillion in 2026 and is forecast to reach USD 6.41 trillion by 2031.

Which country holds the largest share of European private equity activity

The United Kingdom leads with 25.06% of 2025 deal value, supported by deep capital markets and a well-established advisory ecosystem.

Which segment of European private equity is growing fastest?

Secondaries & Fund-of-Funds post the highest growth at a 12.17% CAGR through 2031, driven by investor demand for liquidity and continuation vehicles.

How are rising interest rates affecting private equity valuations in Europe?

Higher rates compress exit multiples, particularly for low-growth industrial assets, prompting sponsors to focus more on operational improvements.

Page last updated on: