Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 12.62 Trillion |

| Market Size (2031) | USD 21.39 Trillion |

| Growth Rate (2026 - 2031) | 11.13% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Private Equity Market Analysis by Mordor Intelligence

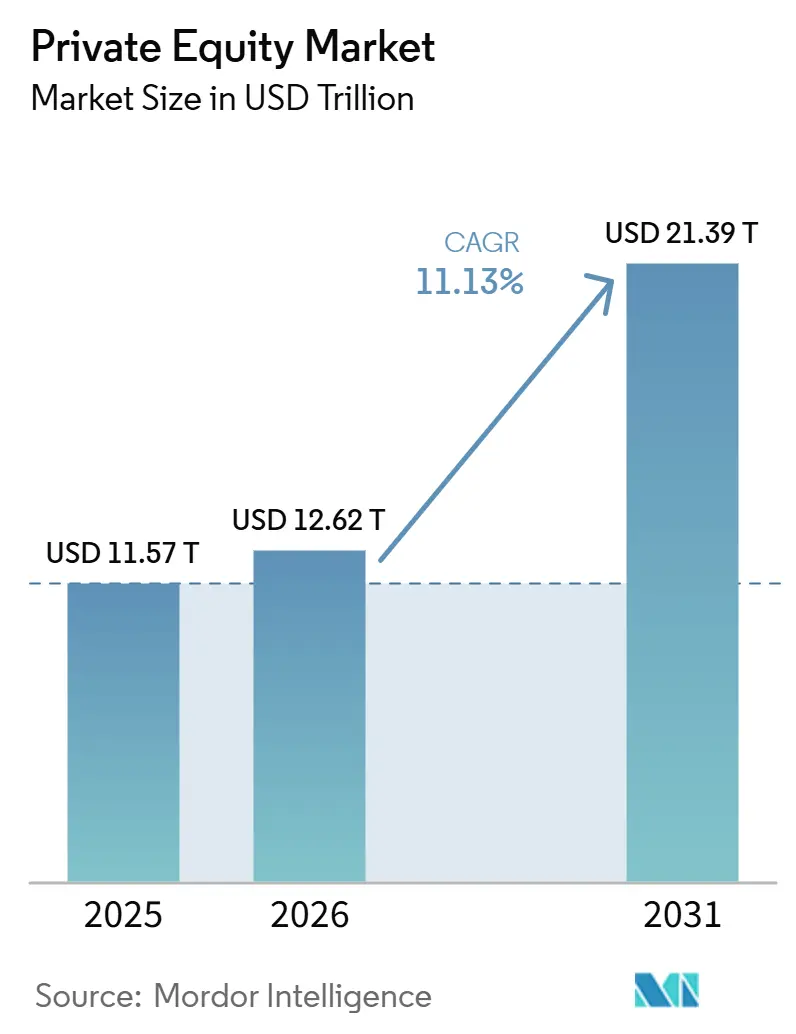

The Private Equity Market size is expected to grow from USD 11.57 trillion in 2025 to USD 12.62 trillion in 2026 and is forecast to reach USD 21.39 trillion by 2031 at 11.13% CAGR over 2026-2031.

Growth is driven by USD 1.2 trillion in dry powder for buyouts as of mid-2025, alternative liquidity solutions, and increased deployment in high-conviction sectors. After valuation compression and exit bottlenecks in 2022-2023, 2025 saw global deal value reach USD 1.5 trillion in the first three quarters, with full-year projections of USD 1.4-2.0 trillion. Median buyout entry multiples stabilized at 11.9x EV/EBITDA in 2024, reflecting competition for quality assets despite tighter financing conditions.

The secondaries market recorded USD 103 billion in transaction volumes in H1 2025, a 51% year-over-year increase, with full-year projections exceeding USD 210 billion. GP-led continuation vehicles accounted for 87% of GP-led volume and 16-19% of sponsor-backed exits in H1 2025. Distributions to LPs exceeded capital calls in H1 2024, but median DPI ratios for 2018-vintage funds remained at 0.6x versus the 0.8x norm. Retail investor access expanded through semi-liquid structures and evergreen funds, with aggregate NAV surpassing USD 400-427 billion in 2025, doubling from late-2023 levels, and private wealth contributing 18-22% of secondaries fundraising.

Key Report Takeaways

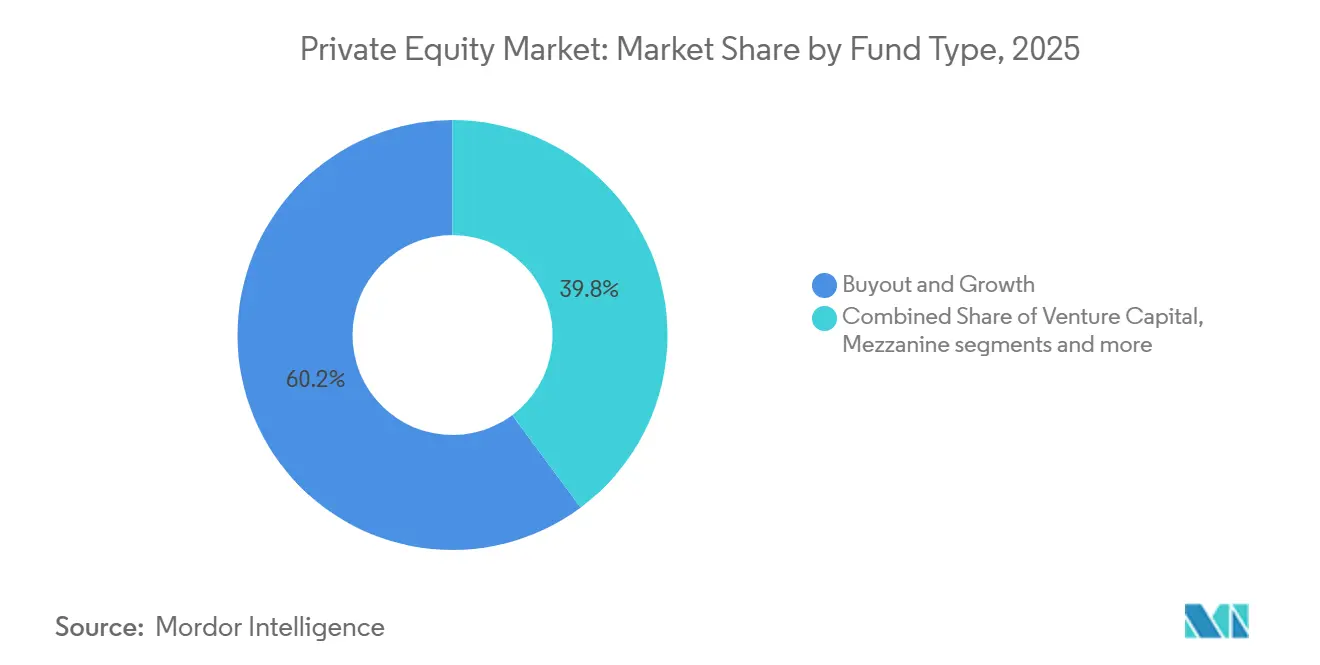

- By fund type, buyout strategies held a 60.17% share in 2025, while in the private equity market, secondaries & fund‑of‑funds are expected to grow at the fastest 10.08% CAGR through 2031.

- By sector, technology captured the largest 29.44% share in 2025, whereas in the private equity market, energy & power is projected to advance at a strong 11.46% CAGR through 2031.

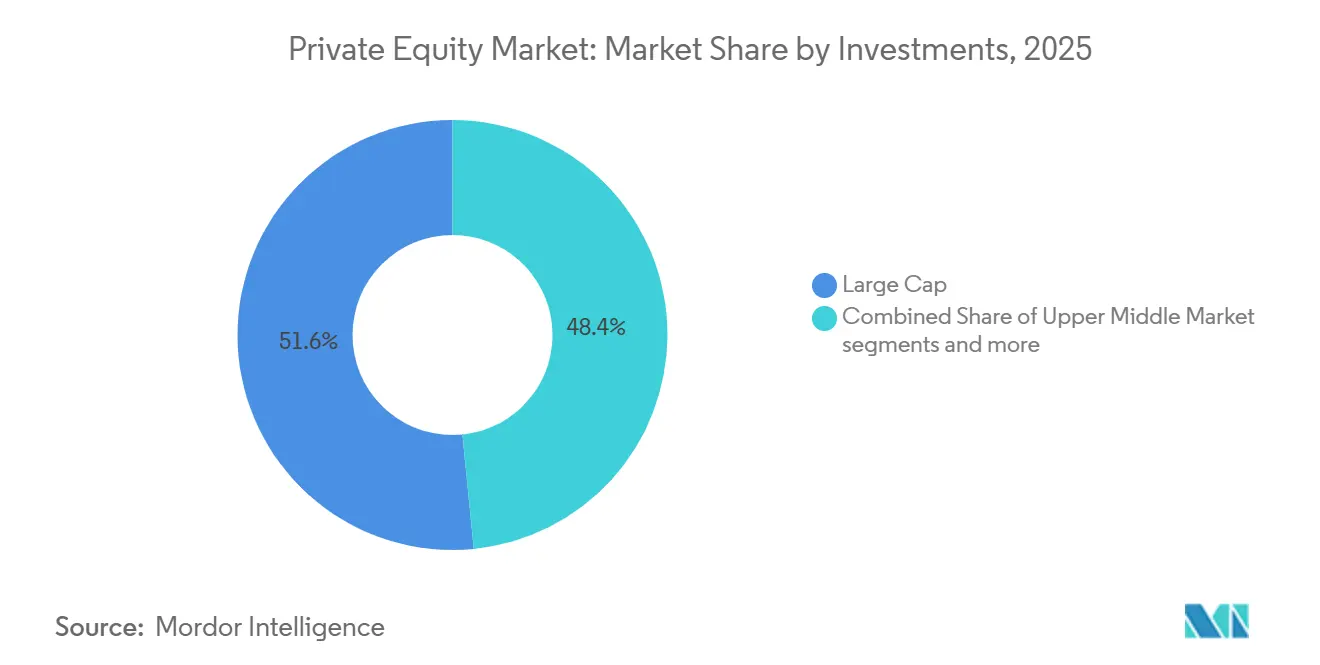

- By investment size, large‑cap transactions commanded a 51.58% share in 2025, and within the private equity market, the lower middle market is forecast to expand at the fastest 12.50% CAGR through 2031.

- By geography, North America led with a 56.23% share in 2025, while in the private equity market, Asia‑Pacific is anticipated to record the highest growth at a 9.61% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Private Equity Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Record dry-powder balances seeking deployment | +2.8% | Global, concentrated in North America & EU | Medium term (2-4 years) |

| Rising allocations to alternatives by pension & sovereign investors | +2.3% | Global, led by North America, increasing in APAC | Long term (≥ 4 years) |

| Digital transformation demand for operational value-creation expertise | +2.1% | Global core, spillover to MEA and Latin America | Medium term (2-4 years) |

| Liquidity unlocked through continuation & secondary funds | +1.8% | Global, with North America & Europe leading adoption | Short term (≤ 2 years) |

| Retail-investor access via semi-liquid / 401(k) structures | +1.5% | National (US-centric), with regulatory pilots in EU/UK | Long term (≥ 4 years) |

| Tokenisation of fund units enabling fractional ownership | +0.9% | National pilots (US, Singapore, EU), early-stage global spillover | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Record Dry-Powder Balances Seeking Deployment

Dry powder at buyout funds reached USD 1.2 trillion by mid-2025, which increases the pressure to deploy capital across the private equity market and supports deal activity as rates ease. In the United States, dry powder moved to USD 880 billion in September 2025, down from a December 2024 peak, which signals that deployment is picking up alongside improved market access. Dedicated secondaries dry powder reached USD 302 to USD 315 billion in Q3 2025, and when including alternative capital, the overhang multiple surpassed 2.0x, which supports GP-led pricing power and volume[1]Jefferies Secondary Team, “H1 2025 Global Secondary Market Review,” Jefferies, jefferies.com. Allocators are underweight private markets relative to targets and are gradually lifting private equity allocations, while the ratio of capital sought to funds closed moved to 3.1x in 2025. Sovereign wealth funds and pensions are joining large consortium deals to scale commitments, exemplified by the USD 55 billion Electronic Arts take-private. Rate cuts totaling 75 basis points through year-end 2025 lowered acquisition financing costs, which removed a visible hurdle to deployment and supported renewed momentum in the private equity market.

Rising Allocations to Alternatives by Pension & Sovereign Investors

Pension funds and sovereign wealth funds moved to increase or maintain private equity exposure in 2025 to enhance returns and diversify, which supports long-duration capital formation in the private equity market. The United Kingdom Mansion House Accord encouraged defined-contribution plans to allocate 5% to 10% to domestic private markets by 2030, which introduces policy support for incremental flows. Asian institutions also increased infrastructure allocations, with a majority of LPs in a 2025 survey indicating higher exposure to infrastructure continuation funds. Sovereign wealth funds from the Middle East participated in large-scale transactions and focused on AI, data centers, chips, and sports assets to pursue strategic diversification. Private wealth is growing in relevance, with an evergreen NAV above USD 400 billion in 2025 and private wealth accounting for 18% to 22% of secondaries fundraising. The broader environment remains supportive due to the need for return enhancement in a normalized rate regime, with the infrastructure’s recent return profile reinforcing diversification merits for large allocators[2]CBRE IM Research, “Infrastructure Quarterly: Q4 2025,” CBRE Investment Management, cbreim.com.

Digital Transformation Demand for Operational Value-Creation Expertise

As multiple expansion waned, managers shifted decisively to operating value creation, technology enablement, and AI adoption to drive EBITDA growth across the private equity market. Portfolio companies reported rapid adoption of AI tools in 2025, and executives increased AI-related software budgets to improve productivity and revenue capture[3]Blackstone CIO Office, “2026 Investment Perspectives,” Blackstone, blackstone.com. Mid-market PE funds also reported broad AI initiatives across portfolio holdings, indicating that digital capability has become a core differentiator in the private equity market. Operating improvements carry a measurable equity value premium at exit, which is motivating firms to invest in operating partners and specialized sector teams. The focus extends to healthcare IT, analytics, and workforce optimization, where deal value doubled in 2025 and where digital leverage correlates with competitive positioning. Longer holding periods also reinforce the need for continuous improvement that compounds value creation under more conservative leverage levels.

Liquidity Unlocked through Continuation & Secondary Funds

Continuation vehicles and GP-led secondaries delivered the fastest-growing liquidity channel in 2025, which supported distributions and reduced exit congestion across the private equity market. GP-led volume reached USD 47 billion in H1 2025 and is on track to exceed USD 100 billion for the year, with single-asset and multi-asset structures repricing assets that remain high-conviction holdings. Pricing trended above 90% of NAV for the majority of single-asset CVs, while LP-led portfolios also tightened discounts, which raised confidence for sellers. Dedicated secondaries dry powder reached USD 302 to USD 315 billion in Q3 2025, while traditional LPs and retail vehicles added incremental capacity, which increased the absorption of GP-led supply. Adoption broadened across regions, with more than half of APAC managers and about half of North American managers planning to increase GP-led activity in the next two years. Large managers forecast structural growth in secondaries volume toward USD 400 billion by 2030 as these tools become a standard part of the private equity market playbook.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher interest-rate driven financing costs | -1.8% | Global, most acute in North America & EU | Short term (≤ 2 years) |

| Bid-ask valuation gaps suppressing exits | -1.4% | Global core, spillover to all regions | Short term (≤ 2 years) |

| Stricter ESG & impact-reporting compliance burdens | -1.2% | Europe-led, expanding to North America & APAC institutional LPs | Medium term (2-4 years) |

| AIFMD II & equivalent data-transparency mandates | -1.0% | EU core, regulatory convergence anticipated in UK, APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher Interest-Rate Driven Financing Costs

Elevated borrowing costs through 2024 reduced leverage, narrowed debt service cushions, and compressed return potential for leveraged buyouts in the private equity market[4]NEPC Research Team, “Quarterly Private Markets Report: Q3 2025,” NEPC, nepc.com. Rates started to ease in late 2025, yet they remain above the 2010 to 2021 baseline, which sustains a higher hurdle for leveraged strategies relative to the last cycle. Interest coverage ratios for private credit borrowers fell from 3.2x in 2021 to near 1.5x in H1 2025, while a larger share of borrowers now sits at or below 1.5x, which is causing tighter lending structures and more conservative underwriting. The use of payment-in-kind features rose and surfaced in senior direct loans, which signals borrower stress and supports opportunistic and distressed strategies. Large-cap sponsors found relief in the syndicated loan market, where volumes jumped to a record USD 404 billion in Q3 2025, while smaller sponsors remained more dependent on direct lenders. Normalization is expected as easing continues, but the private equity market is recalibrated to a higher-for-longer rate regime that emphasizes operating value creation over pure financial engineering.

Bid-Ask Valuation Gaps Suppressing Exits

Exit activity improved in 2025, yet valuation disconnects persisted for 2021 to 2022 vintages, which slowed full realizations and dampened distributions in parts of the private equity market. Exit markups narrowed over the last three years, while many sales cleared near carrying values, which reduced the role of multiple expansion at exit. Limited partners favored full exits to continuation or dividend recapitalizations in several polls, and managers adjusted with more structured earnouts, seller notes, and contingent value rights to bridge pricing gaps. Backlog remains high with tens of thousands of portfolio companies queued for monetization, a third of which are held beyond six years, which supports the continued use of GP-led tools in 2026. As syndicated markets stabilized and rates steadied, valuation gaps began to narrow during 2025, which opened windows for IPOs and strategic sales. Exit value reached USD 832 billion by Q3 2025 with a public listing value of USD 198.7 billion, which was the strongest since 2020.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fund Type: Secondaries Emerge as Liquidity Catalyst Amid Exit Bottlenecks

Buyout strategies held a 60.17% share in 2025 as mega-LBOs and middle market activity rebounded, while the private equity market refocused on pricing discipline and tighter leverage levels. Median buyout entry multiples stabilized at 11.9x EV/EBITDA in 2024, which remained above pre-pandemic norms and reflected competition for high-quality platforms. Syndicated loan markets reopened to support large deals and public-to-private transactions, and direct lenders remained active, which together diversified financing sources across the private equity market. Fundraising trends favored managers with operating expertise, sector depth, and measured fund growth as LPs prioritized teams with consistent distribution profiles. The buyout playbook broadened into real assets, hybrid capital, and structured solutions to maintain deployment pace under normalized rates.

Secondaries and fund-of-funds represent the fastest-growing fund type at a 10.08% CAGR through 2031 as the asset class balances capital deployment with liquidity creation across the private equity industry. H1 2025 secondaries volume of USD 103 billion rose 51% year-over-year, and full-year projections exceeded USD 210 billion as GP-led transactions neared half of overall secondaries activity. Pricing tightened with most single-asset continuation vehicles clearing above 90% of NAV, while LP-led portfolios reached 94% of NAV on average, which reflected strong buyer demand. Dedicated dry powder continued to climb and was supplemented by traditional LPs and retail vehicles, which supported absorption of GP-led supply and portfolio rebalancing. Venture and growth equity exposure increased within LP-led secondaries as AI-driven exits improved liquidity conditions at the late stage.

By Sector: AI Infrastructure Propels Technology Leadership While Energy Surges

Technology captured 29.44% of sector activity in 2025, underpinned by USD 469 billion in global TMT PE investment and elevated valuations for high-quality software and AI assets across the private equity market. AI and machine learning funding of USD 160.8 to USD 193 billion through Q3 2025 accounted for a majority of venture deal value, which showed the scale of capital concentrating in AI relative to other growth themes. Hyperscalers increased 2026 capex plans after spending an estimated USD 415 billion in 2025, directing most of it to AI infrastructure spanning data centers, chips, power systems, and connectivity. Private equity invested heavily across the IT value chain since 2020, including data centers and semiconductors that enable AI workloads, to meet relentless compute and power demand. Software deal multiples eased from 2024 but stayed above pre-pandemic levels for high-growth, AI-enabled platforms, supported by persistent competition for mission-critical assets.

Energy and power is the fastest-growing sector at an 11.46% CAGR through 2031, driven by electrification, grid expansion, and AI-related power demands that are reshaping the private equity market. Global power investment approached USD 3.3 trillion in 2025, with most allocated to renewables, storage, and grid optimization, while battery energy storage spending expanded on cost declines and supportive procurement. Grid capital reached record levels in 2024, yet interconnection queues and materials inflation continue to challenge project timelines and raise the value of scale players. Data center electricity demand is projected to at least double by 2030, while leading cloud providers account for most clean energy contracting for these assets. Infrastructure fundraising accelerated in 2025 and skewed to renewables and data centers, which reflects investor conviction in real-asset platforms linked to AI workloads and grid modernization.

By Investments: Mega-Transactions Dominate Value While Lower Middle Market Offers Resilience

Large-cap deals over USD 1 billion held a 51.58% share in 2025 as public-to-privates returned and sponsor-to-sponsor sales scaled under improved financing access in the private equity market. Syndicated loan issuance hit a quarterly record in Q3 2025, and direct lenders contributed meaningful capacity, which together funded larger LBOs at conservative leverage. The USD 55 billion Electronic Arts take-private by a sponsor and sovereign consortium set a new high-water mark for LBOs and highlighted the role of co-investors in financing mega deals. Large platforms used structured financing and hybrid capital more actively to secure scale assets across technology and healthcare during 2025. Upper middle market valuation multiples expanded where assets had durable revenue, recurring models, or consolidation runways that justified premium pricing.

The lower middle market is the fastest-growing deal-size segment at a 12.50% CAGR through 2031, supported by entry multiples near 7.7x EV/EBITDA, lower leverage, and greater operational agility across the private equity industry. Service-oriented revenue models reduced exposure to trade and capital-market cycles, which helped sustain deal flow even when public markets were volatile. Financing costs weighed on smaller buyers in early 2025 and slowed closings, yet activity improved by late 2025 as rate expectations stabilized and lenders adjusted structures. Valuations rose for larger EBITDA brackets within the mid-market, which reinforced the premium for scale and resilience in the private equity market. Strategics remained active competitors with lower sensitivity to rates and greater collaboration capture, which influenced auction dynamics and outcome valuations.

Geography Analysis

North America held a 56.23% market share in 2025, supported by USD 880 billion in dry powder (as of September 2025, down from USD 1.3 trillion in December 2024). US PE deal value rose 8% year-over-year in H1 2025 to over USD 195 billion, while global buyout activity reached USD 911-1,500 billion, with North American sponsors driving mega-transactions. Broadly syndicated loan markets processed USD 404 billion in Q3 2025, and global leveraged finance issuance hit USD 1.3 trillion, up 45% year-over-year. TMT attracted USD 285.9 billion in PE investment through Q3 2025, healthcare reached USD 73.5 billion, and infrastructure/energy investments totaled USD 65.1 billion. Canada recorded 646 PE deals worth CAD 57 billion (USD 41.63 billion) in 2024, with 2025 activity at 488 deals for CAD 46 billion (USD 33.59 billion) by November.

Asia-Pacific is the fastest-growing region at a 9.61% CAGR through 2031, led by India’s 73% year-over-year deal value surge and Japan’s 155% increase. YTD Q3 2025 investment activity totaled USD 75 billion, with India and Japan contributing 60%. India’s growth is driven by SaaS platforms, healthcare, life sciences, and a favorable IPO market. Institutional allocations to infrastructure rose from 1.3% in 2020 to 2.2% by 2024. China’s sovereign fund seeks secondary buyers for USD 1 billion in PE investments, while South Korea and Middle Eastern funds expand regional investments. Exit activity reached USD 54 billion YTD Q3 2025, with India and Japan accounting for 60% of realized value.

Europe’s PE deal value reached €177 billion (USD 208.20 billion) in Q3 2025, a 25% rise over Q2, with megadeals exceeding €1 billion (USD 1.18 billion) accounting for 32% of total value. Public-to-private deal value rose 65% in 2024, with notable 2025 examples including Darktrace and Hargreaves Lansdown. Healthcare activity doubled to USD 59 billion, and the Verisure IPO raised €3.2 billion, the largest PE-backed IPO in European history. Regulatory changes, including AIFMD II and ELTIF 2.0, aim to enhance cross-border investments, while the UK’s Mansion House Accord targets 5-10% pension allocations to private markets by 2030.

South America and the Middle East & Africa show selective growth. Latin America has 39 unicorns and over 60 tech companies poised for liquidity events. Brazil leads in stablecoin adoption, while Nigeria’s fintech ecosystem matures with notable acquisitions. The Middle East attracts infrastructure and energy transition capital, with sovereign wealth funds co-investing globally and domestically.

Regulatory Landscape

The private equity market operates under tightening transparency, reporting, and investor-protection requirements across major jurisdictions, with regulators focusing on systemic-risk visibility and consistent disclosures. In the United States, the SEC and CFTC jointly proposed amendments to Form PF in April 2026 to streamline private fund reporting and reduce burdens, while SEC private-fund statistics highlighted the scale of the industry, with over USD 16 trillion in net assets reported as of Q2 2025.

In Europe, Directive (EU) 2024/927 (AIFMD II) reached its April 16, 2026 transposition deadline, introducing harmonized rules that affect alternative investment fund managers, including requirements for loan-originating AIFs, delegation clarity, liquidity management tools, and enhanced supervisory reporting. Alongside national implementations, international coordination continues through bodies such as IOSCO, reinforcing convergence around supervisory data, risk monitoring, and fund governance expectations that shape how global managers build compliance operating models.

Value Chain Analysis

The private equity value chain starts with capital formation from limited partners (pension funds, sovereign wealth funds, endowments, insurers, and increasingly private wealth) into closed-end funds and evergreen or semi-liquid structures. It then moves through sourcing, due diligence, and transaction execution supported by intermediaries such as investment banks, advisers, and legal and fund-administration providers (including SPV and domiciliation services). The investment phase centers on governance, portfolio oversight, and operating value creation (technology enablement, pricing, and productivity programs), with financing supplied by syndicated leveraged loan markets and direct lenders, and with risk management increasingly shaped by ESG and data transparency requirements.

The exit and distribution leg has become the most constrained link, changing how value is realized and recycled. Evidence of the bottleneck includes extended holding periods (6.4 years for US buyouts, cited in September 2025) and weaker distribution rates (9.6% in Q2 2025 versus the 2015-2019 historical average), which has elevated secondaries, GP-led continuation vehicles, and structured liquidity solutions as core channels alongside IPOs and strategic M&A. This shift also creates additional distribution pathways to private wealth investors, expanding the buyer base for secondary stakes and adding another outlet for liquidity when traditional exits clear at less favorable valuations.

Competitive Landscape

The private equity market is fragmented at the global level, yet competition intensified among scale managers as limited partners became more selective and capital remained concentrated in proven platforms. Large managers acquired peers more frequently in the last five years than in the prior period, which signaled consolidation around platforms with durable fundraising and operating capabilities. Performance persistence increased for top managers compared with prior vintages, while the gap between top and bottom quartiles widened, which elevated the premium on manager selection. Strategic buyers also competed actively for assets as they deployed balance sheets to pursue collaboration and longer integration horizons than most sponsors.

Operating value creation outperformed financial engineering as the primary source of returns, which increased emphasis on revenue acceleration, pricing, and AI-enabled productivity across the private equity market. Managers invested in operating partners and specialized talent for AI integration, pricing optimization, supply chain resilience, and data analytics to widen the operating delta at exit. Portfolio companies expanded AI use cases in 2025, and executives increased software budgets for AI compared with non-AI categories, which showed how digital adoption is now a baseline expectation for value creation. The private equity market saw active deployment across AI infrastructure and healthcare technology, where digital adoption maps to durable end demand and supports large-ticket deployment.

White-space opportunities included under-owned industrial assets, real-asset adjacencies to digital buildouts, and lower middle market platforms with disciplined operating plans and multiple exit pathways. Infrastructure tied to AI workloads, renewable power, and grids presented multi-year deployment potential, with the largest managers raising dedicated capital to scale into these areas. Continuation vehicles matured into a core toolkit for liquidity and for extending ownership of high-conviction assets as managers optimized the hold period to realize operating plans. The private equity market also drew incremental retail capital through evergreen structures, which added a more stable and countercyclical investor base alongside traditional institutions.

Private Equity Industry Leaders

Bain Capital

BC Partners

Blackstone

Brookfield Asset Management

Carlyle Group

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Liquidity solutions continue to open whitespace for product and platform innovation as managers respond to longer holding periods and lower distribution rates. Secondaries and GP-led continuation vehicles are increasingly used to deliver optionality to LPs and extend ownership of high-conviction assets. Market evidence includes the step-up in secondaries activity cited in the report context (USD 103 billion in H1 2025 transactions, with GP-led continuation vehicles accounting for a dominant share of GP-led volume), supporting dedicated secondaries strategies, portfolio financing, and differentiated structuring.

Operational value creation offers another actionable opportunity set, particularly around AI-enabled transformation rather than stand-alone tooling. Recent industry work emphasizes workflow redesign, stronger data foundations, and core systems modernization (ERP/CRM) and governance over 6 to 12 month cycles, with funds prioritizing revenue acceleration initiatives. At the same time, regulatory change is creating room for new manager operating models and product distribution: the UK HM Treasury and FCA consultation on a new three-tier UK AIFM regime (with NAV-based thresholds) points to a more proportionate rulebook, while US Department of Labor activity (EBSA proposed rulemaking dated March 31, 2026 on fiduciary duties for selecting designated investment alternatives) keeps retirement-channel access and product design under active scrutiny. This reinforces the need for compliant, transparent structures as retail participation expands.

Recent Industry Developments

- July 2026: Blackstone and Williams announced a USD 5.34 billion investment to form a power innovation joint venture. The investment is geared toward power infrastructure needs that have become central to data center and AI-related buildouts, aligning large-scale private capital with energy system expansion.

- June 2026: Broadcom, Apollo, and Blackstone established a strategic platform aimed at accelerating more than 20 gigawatts of global AI deployments. By linking a technology supplier with scaled private capital, the platform shows how sponsors are underwriting AI infrastructure as an investable, multi-asset buildout theme.

- December 2025: Blackstone and TPG completed their USD 18.3 billion take-private acquisition of Hologic. The transaction highlighted continued sponsor appetite for scaled healthcare and medtech platforms and indicated that large-cap buyouts continued to clear despite tighter financing conditions than the prior cycle.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the private equity market is sized as the value of capital managed and deployed by private equity funds globally, covering fund activity tied to acquiring equity stakes in companies that are not publicly listed, or that are taken private.

Scope exclusions: This sizing excludes private credit, standalone infrastructure funds, standalone real estate funds, and hedge fund strategies that do not center on private equity ownership.

Segmentation Overview

- By Fund Type

- Buyout & Growth

- Venture Capital

- Mezzanine & Distressed

- Secondaries & Fund of Funds

- By Sector

- Technology (Software)

- Healthcare

- Real Estate and Services

- Financial Services

- Industrials

- Consumer & Retail

- Energy & Power

- Media & Entertainment

- Telecom

- Others (Transportation, etc.)

- By Investments

- Large Cap

- Upper Middle Market

- Lower Middle Market

- Small & SMID

- By Geography

- North America

- Canada

- United States

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Asia-Pacific

- India

- China

- Japan

- Australia

- South Korea

- South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- Rest of Asia-Pacific

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- BENELUX (Belgium, Netherlands, and Luxembourg)

- NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- Rest of Europe

- Middle East And Africa

- United Arab of Emirates

- Saudi Arabia

- South Africa

- Nigeria

- Rest of Middle East And Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to build the first version of the model and to anchor it to repeatable public data series. We rely on sources such as central bank and financial regulator releases, IMF and World Bank macro series, OECD statistics, and public disclosures from industry associations that track fundraising, deal activity, and exits.

The desk phase also uses company filings, fund manager investor presentations, annual letters, and reputed financial press to interpret what is changing by strategy and by region. Where numbers need cross-checking, we reference paid subscriptions for company financials and intelligence, news and financials, and patent databases to validate sector exposure and the pace of new platform creation. The desk sources listed here are illustrative, and many other public materials were used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to test the desk assumptions with people who run funds, advise deals, or support fundraising and portfolio operations, and then to align the model to how capital is actually measured in practice. Since this is a global market, inputs are validated across APAC, EMEA, and the Americas so the same definition is applied consistently even when reporting currencies and fund structures differ.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 18% | APAC: 51% |

| Mid tier: 50% | Functional/Unit leaders: 23% | EMEA: 31% |

| Smaller Players: 22% | Managers: 59% | Americas: 18% |

Market-Sizing & Forecasting

The core model uses a top-down build where fund-level capital pools are reconstructed from reported assets under management, fundraising, dry powder, and deployment pace, and then converted to a single market value in USD for the year. To keep the totals practical, the output is cross-checked with selective bottom-up approximations, such as sampled fund counts by strategy, typical fee and carry structures, and implied capital deployment per deal size band, which are then used to adjust outliers.

Key inputs that shape the sizing include global fundraising volumes by vintage year, dry powder levels, deal value and deal count trends, exit value timing, and FX movement for major fundraising currencies. These variables matter because private equity market value can appear larger or smaller depending on whether capital is counted at commitment, at deployment, or at AUM valuation points. For forecasting, scenario analysis is used, with the base case guided by consensus expectations from primary respondents on rate cycles, IPO window reopening, and the speed of distributions, followed by sensitivity checks on deployment rates and valuation multiples. Where bottom-up signals are missing for smaller geographies, we apply proxy ratios from similar markets and re-test them during validation calls.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals, including fundraising totals, reported dry powder, deal value, and exit conditions, so any single data series does not steer the final number. Large variances trigger an anomaly review, where assumptions like FX timing, valuation mark schedules, and strategy mix are rechecked, and clarifying calls are scheduled when gaps remain.

Before sign-off, the model and narrative go through multiple analyst reviews that focus on logic consistency and year-on-year movement. The report is refreshed annually, and interim updates are made when material events shift deployment or valuations. Right before delivery, a fresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's Global Private Equity Market Estimate Compared With Other Published Estimates

Published figures for private equity often do not match because the word market is used for different things, and the reporting unit changes from one publisher to another. Some sources describe annual investment flow, others describe revenues tied to services, while a few use assets under management type measures.

The main gap comes from mixing investment flow with stock measures, where Mordor Intelligence counts global private equity as an AUM and capital pool view (including committed capital and dry powder) rather than only annual deal investment totals or fee revenues, which naturally creates a much larger value for the same year.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 19.96 T (2026) | |

| Trade Journal A | USD 2.10 T (2025) | Uses annual private equity investment value as the market proxy, which captures deployed deal flow in a year and does not include undeployed dry powder or the broader AUM stock. |

| Global Publisher B | USD 0.53 T (2025) | Defines the market as revenues from private equity related services and activities, and also includes adjacent fund types like infrastructure and real estate in its segment structure, which shifts scope and compresses the value versus an AUM-based view. |

The table shows that the spread is largely explained by what is being measured and when it is counted. When the definition is pinned to a clear capital pool logic, checked against fundraising and deployment signals, the result becomes easier to replicate and to track over time without hidden scope changes.

Key Questions Answered in the Report

What is the current size and growth outlook for the private equity market?

The private equity market size is estimated at USD 19.96 trillion in 2026 and is projected to reach USD 37.85 trillion by 2031 at a 13.65% CAGR.

Which fund types and sectors are leading and growing fastest in private equity?

Buyouts led with a 38.39% share in 2025, while secondaries and fund-of-funds are the fastest-growing at an 8.84% CAGR; technology held 32.87% share in 2025 and energy and power is the fastest-growing at an 11.38% CAGR.

What is driving deal activity and liquidity in private equity in 2026?

Elevated dry powder, reopened syndicated loan markets, and broad adoption of GP-led continuation vehicles and secondaries are driving deployment and unlocking exits, while retail evergreen vehicles add capital resilience.

Which regions offer the strongest momentum for private equity deployment?

North America held 51.87% share in 2025 with strong financing access, while Asia-Pacific is the fastest-growing at a 7.48% CAGR driven by India and Japan and rising infrastructure needs.

How are interest rates and financing conditions affecting private equity transactions?

Higher rates reduced leverage and pressured coverage, but 2025 easing and record syndicated loan volumes improved access for large-cap deals, which shifted value creation toward operating improvements.

What strategies are top managers using to differentiate performance?

Leading firms emphasize operating value creation, AI integration, sector specialization, and liquidity solutions through continuation vehicles and secondaries to enhance returns and distributions.

Page last updated on: