Preoperative Surgical Planning Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

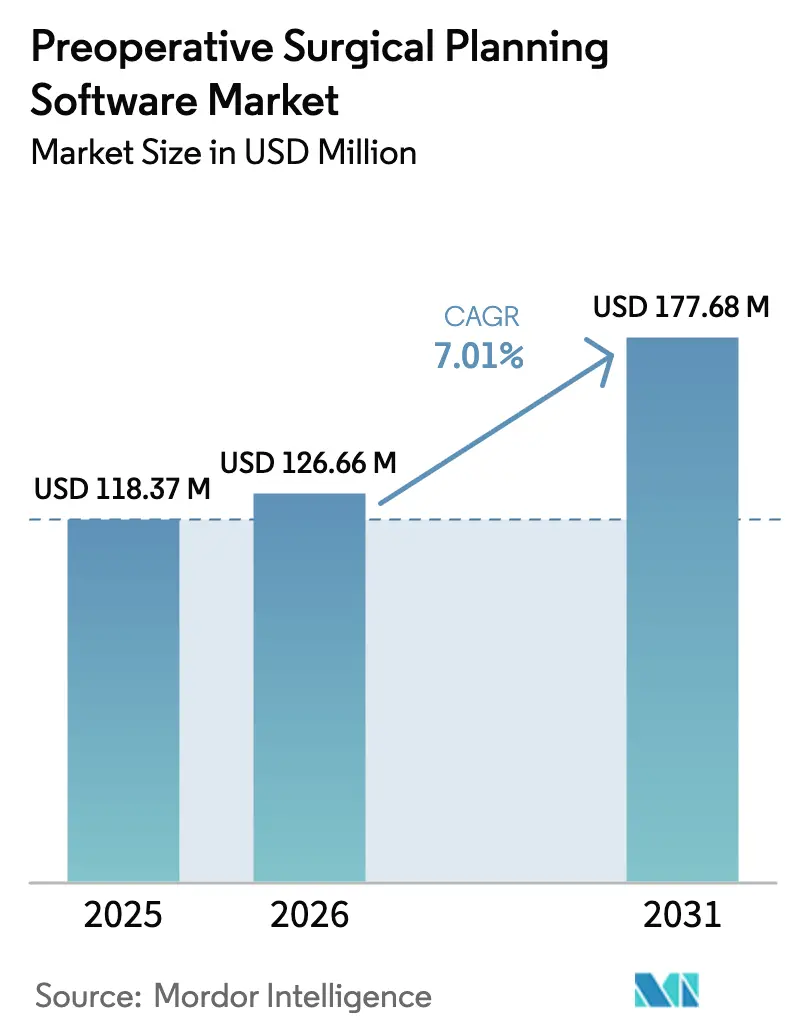

| Market Size (2026) | USD 126.66 Million |

| Market Size (2031) | USD 177.68 Million |

| Growth Rate (2026 - 2031) | 7.01% CAGR |

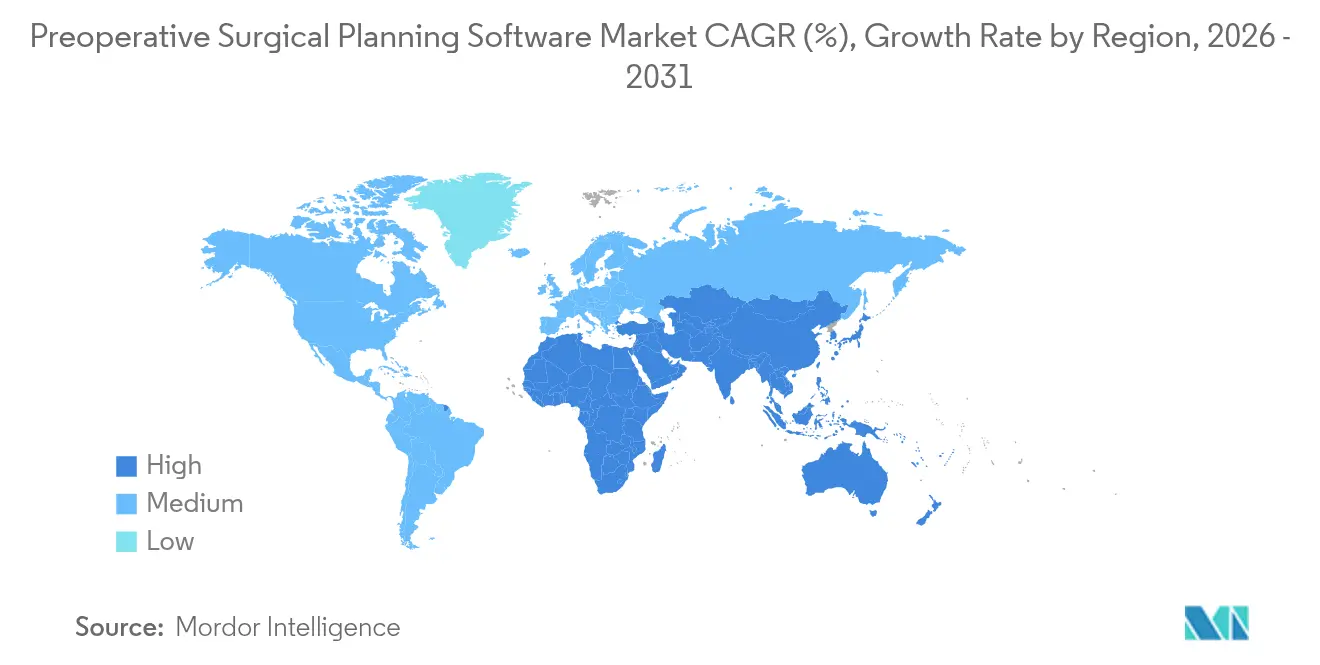

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Preoperative Surgical Planning Software Market Analysis by Mordor Intelligence

Preoperative Surgical Planning Software Market size market size in 2026 is estimated at USD 126.66 million, growing from 2025 value of USD 118.37 million with 2031 projections showing USD 177.68 million, growing at 7.01% CAGR over 2026-2031.

Across hospitals and outpatient centers, digital planning is increasingly viewed as core surgical infrastructure rather than an optional add-on, because AI-powered modeling shortens case preparation time, increases procedural accuracy, and lowers revision risk. Cloud-native platforms further accelerate adoption by allowing surgeons at different locations to collaborate on the same 3-D plan in real time while meeting stringent data-governance requirements. Vendor consolidation continues as large med-tech players acquire niche software innovators to broaden integrated “digital OR” portfolios and lock in multi-year enterprise contracts. Meanwhile, stronger FDA guidance on software as a medical device, paired with top-line savings from shorter lengths of stay, sustains a favorable reimbursement climate that rewards evidence-backed digital tools.

Key Report Takeaways

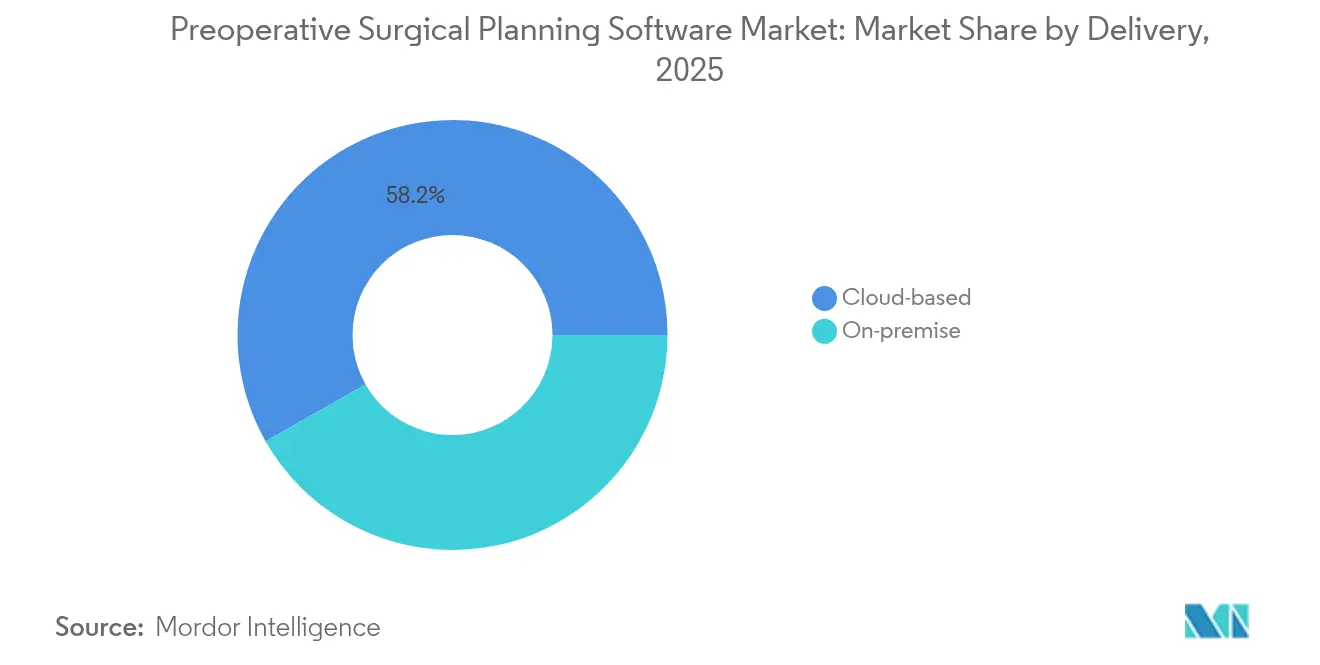

- By delivery, cloud solutions held 58.22% of preoperative surgical planning software market share in 2025, and this segment is projected to grow at a 10.31% CAGR through 2031.

- By application, orthopedics led with 46.10% revenue share in 2025, while oncology is expected to expand at a 12.92% CAGR to 2031.

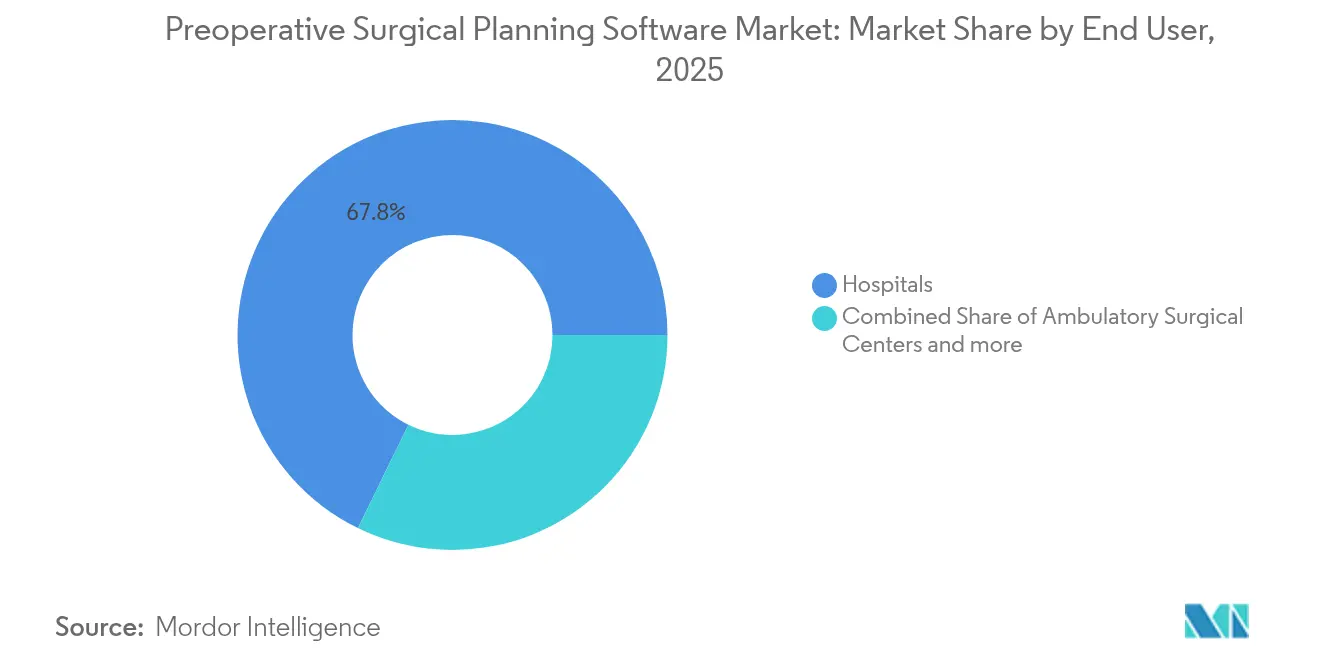

- By end user, hospitals accounted for 67.75% of the preoperative surgical planning software market size in 2025, whereas ambulatory surgical centers (ASCs) record the fastest CAGR at 7.72% through 2031.

- By geography, North America contributed 37.65% revenue share in 2025; Asia-Pacific is forecast to post the highest regional CAGR at 9.36% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Preoperative Surgical Planning Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Uptake of AI-Based 3-D Planning Tools | +1.8% | Global, with North America & Europe leading adoption | Medium term (2-4 years) |

| Growing Procedure Volumes for Complex Orthopedics & Spine | +1.5% | Global, concentrated in aging populations | Long term (≥ 4 years) |

| Cloud Deployment Enables Multi-Site Collaboration | +1.2% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Surgeon Shortage Fuels Demand for Decision-Support Software | +1.0% | Global, acute in developed markets | Medium term (2-4 years) |

| Emergence of Patient-Specific 3-D Printed Guides | +0.9% | North America & Europe, emerging in APAC | Medium term (2-4 years) |

| Hospital "Digital OR" Programs Bundling Planning + Navigation | +0.7% | North America & Europe primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Uptake of AI-Based 3-D Planning Tools

AI-driven platforms now convert multi-modal imaging into high-fidelity 3-D models within minutes, eliminating manual segmentation bottlenecks that historically consumed hours. Stryker’s FDA-cleared Spine Guidance 5 software with Copilot exemplifies this evolution by linking intelligent instruments with real-time feedback loops that refine trajectories mid-procedure.[1]Stryker Corp., “Spine Guidance 5 FDA Clearance,” stryker.com ClearPoint Neuro reports that its 2.2 release accelerates brain-structure identification and improves reproducibility in deep-brain stimulation cases.[2]ClearPoint Neuro, “ClearPoint 2.2 Release Notes,” clearpointneuro.com Early clinical studies show that AI-enabled risk stratification reduces unexpected complications by flagging high-risk anatomies before the first incision. These capabilities elevate planning software from passive viewer to active surgical co-pilot, allowing less-experienced surgeons to achieve outcomes that once required decades of expertise. Continuous model retraining on postoperative data then creates a virtuous cycle that further sharpens predictive accuracy over time.

Growing Procedure Volumes for Complex Orthopedics & Spine

Rising life expectancy, higher obesity rates, and improved diagnostics are driving double-digit growth in joint replacements and spinal fusions, pushing surgical caseloads beyond the capacity of traditional preoperative workflows. Zimmer Biomet’s USD 177 million acquisition of Monogram Technologies underscores the market’s strategic pivot toward software-driven precision arthroplasty, with AI guiding implant boundaries to protect soft tissue. Advanced planning tools allow surgeons to simulate osteotomies, assess implant fit, and optimize alignment angles on a virtual twin, decreasing the likelihood of costly revisions. Minimally invasive approaches heighten the need for accurate pre-planning because limited visual fields leave little margin for error once the procedure starts. As complexity rises, facilities that adopt robust digital planning platforms can safely schedule more cases per day without sacrificing quality, reinforcing a direct link between software adoption and throughput capacity.

Cloud Deployment Enables Multi-Site Collaboration

Enterprise health systems increasingly deploy cloud-native suites that centralize imaging, annotations, and plan iterations on a single secure tenant. Johnson & Johnson MedTech’s Polyphonic ecosystem integrates surgical video, telepresence, and planning modules, allowing subspecialists to co-author cases from different campuses in real time. Instant access to institutional best-practice libraries standardizes care pathways, reduces unwarranted variation, and accelerates credentialing for newly hired surgeons. Automatic version control ensures that everyone operates from the latest approved iteration, lowering the risk of intraoperative surprises. Cloud architecture also simplifies software-as-a-service pricing, shifting expenditures from irregular capital budgets to predictable operating lines that finance teams can forecast accurately. With cybersecurity frameworks such as zero-trust increasingly mandated by hospital boards, vendors that demonstrate end-to-end encryption and HIPAA-aligned audit trails gain a decisive edge in competitive tenders.

Surgeon Shortage Fuels Demand for Decision-Support Software

The World Health Organization forecasts a global shortfall of more than 1.2 million specialists by 2030, amplifying pressure on existing surgical staff to handle rising case volumes. AI-enabled decision tools mitigate this gap by recommending optimal incisions, implants, and approach angles derived from vast outcome datasets. Real-time analytics embedded in navigation consoles call attention to deviation from planned paths, giving early-career surgeons confidence to attempt complex cases in regional hospitals. Ambulatory centers leverage these systems to broaden service portfolios without recruiting additional full-time surgeons, improving local access to advanced procedures. As health systems compete for talent, bundled software that demonstrably reduces burnout and overnight call frequency often wins executive backing faster than hardware-only proposals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Subscription & Integration Costs | -0.8% | Global, acute in cost-sensitive markets | Short term (≤ 2 years) |

| Data-Security / HIPAA-Compliance Concerns | -0.6% | North America & EU primarily | Medium term (2-4 years) |

| Limited Reimbursement Pathways | -0.5% | Global, varying by healthcare system | Long term (≥ 4 years) |

| AI-Model Validation Gaps Slow Regulatory Approvals | -0.4% | Global, regulatory-dependent markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Subscription & Integration Costs

Subscription fees that run into six-figure annual totals, coupled with mandatory image-archive upgrades, place sophisticated planning platforms beyond the reach of many rural hospitals and startup ASCs. Integration teams must map picture-archiving interfaces, calibrate 3-D printers, and train scrub staff, adding indirect costs that often double the first-year budget. Smaller providers working on tight margins face difficulty justifying payback periods that extend beyond the usual 24-month capital allocation window. Although vendors now offer modular licenses or outcome-based pricing, CFOs remain wary of locking into long commitments while software regulations evolve. As a result, adoption in price-sensitive markets lags, limiting global volume growth during the near-term horizon.

Data-Security / HIPAA-Compliance Concerns

Cloud routing of high-resolution DICOM images introduces multiple attack surfaces, increasing organizational exposure to ransomware and breaches. U.S. regulators now expect software vendors to provide machine-readable software bills of materials (SBOMs) that document every third-party library, raising compliance costs and prolonging procurement cycles.[3]U.S. Department of Health and Human Services, “Healthcare Sector Cybersecurity Coordination,” hhs.gov European hospitals must also navigate cross-border data-transfer rules under the GDPR, which sometimes forces hybrid deployments with local edge servers. Internal IT teams often lack the bandwidth to audit encryption protocols, leading executives to postpone purchase decisions until security standards mature further. These delays translate into slower market penetration, especially among early-adopter health systems that set the tone for regional uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Delivery: Cloud Dominance Accelerates Multi-Site Workflows

Cloud-hosted suites comprised 58.22% of the preoperative surgical planning software market in 2025 and are forecast to grow at a 10.31% CAGR through 2031, highlighting the model’s scalability for geographically dispersed health networks. The preoperative surgical planning software market size attributable to cloud platforms is expected to exceed USD 103.5 million by 2031, underpinned by elastic computing that renders complex 3-D reconstructions without on-premise GPU clusters. New features roll out simultaneously for every customer, shortening innovation cycles and reducing service-desk load. Hospitals value this model for disaster-recovery resilience and the ability to shift compute-intensive workloads to off-peak hours, lowering local power consumption.

Conversely, on-premise deployments retain relevance where sovereign-data mandates or intermittent broadband require localized control. Defence hospitals and certain EU regions mandate that patient images stay within national borders, prompting hybrid architectures that replicate core datasets locally while syncing analytics to the cloud when bandwidth allows. Vendors that offer interoperable licensing across both environments ease migration paths as regulations evolve. Although growth in on-premise installations slows, cumulative installed base ensures continued service revenue and provides a gateway for eventual cloud transition once policy barriers recede.

By Application: Orthopedics Leads While Oncology Surges

Orthopedics commanded 46.10% of preoperative surgical planning software market share in 2025, reflecting the discipline’s long-standing use of digital templating for joint arthroplasty and trauma fixation. The orthopedic segment is projected to contribute over USD 81.1 million to the preoperative surgical planning software market size by 2031, supported by rising volumes of knee, hip, and shoulder procedures. Surgeons rely on virtual templating to select implant sizes, predict alignment angles, and simulate cut guides that later feed robot-assisted systems. As revision surgeries carry high reimbursement penalties, precise pre-planning is seen as an insurance policy against costly do-overs.

Oncology exhibits the fastest 12.92% CAGR, driven by the need to safeguard critical margins during tumor resections in neuro-oncology, ENT, and musculoskeletal oncology. AI-driven platforms such as TumorSight Viz create fused PET-MRI volumes that delineate malignancies in 3-D, enabling surgeons to choose tissue-sparing corridors with sub-millimeter fidelity. Patient-specific 3-D printed cutting blocks then translate those plans into the operating suite, reducing guesswork when lesions abut nerves or vasculature. As immunotherapy extends survival, more patients become surgical candidates, further stimulating demand for high-precision planning across cancer centers.

By End User: Hospitals Dominate Despite ASC Acceleration

Hospitals held 67.75% of total revenue in 2025 because tertiary centers perform the highest-complexity procedures and maintain IT budgets that accommodate enterprise licenses. Many academic facilities bundle preoperative planning into broader digital OR initiatives that also encompass intraoperative navigation, robotics, and postoperative analytics. Centralized procurement teams negotiate multi-site license pools, stretching dollar value while ensuring consistent user experiences across teaching and satellite campuses.

Nevertheless, ASCs represent the fastest-growing customer group at a 7.72% CAGR as payer policies favor cost-efficient settings for non-complex joints and spine interventions. The shift unlocks new addressable volume, and cloud delivery minimizes up-front capital outlays, aligning with ASC cash-flow models. Specialty orthopedic clinics occupy a strategically important niche by offering focused procedures such as sports-medicine reconstruction where outcome differentiation directly correlates with surgeon referral patterns. These clinics frequently opt for modular, case-based software pricing that matches fluctuating caseloads and avoids underutilized seats.

Geography Analysis

North America contributed 37.65% of 2025 revenue, supported by a robust FDA pathway that fast-tracks AI-enabled tools and by CMS policies that reimburse specific digital diagnostics, thereby encouraging adjacent surgical applications. Institutional review boards across leading U.S. hospitals embrace prospective studies, giving vendors a pipeline of peer-reviewed evidence that snowballs reimbursement credibility. Extensive hospital consolidation also allows group purchasing organizations to roll-out technology across dozens of sites in one contract, accelerating scale.

Europe remains the second-largest region with strong adoption in Germany, France, and the Nordics, where national health systems prioritize cost-effectiveness and long-term outcome data. GDPR compliance requirements compel vendors to demonstrate rigorous data-privacy tooling, which, once validated, acts as a moat against less-secure competitors. The continent’s early investment in point-of-care 3-D printing and its network of accredited additive-manufacturing labs position European providers at the forefront of patient-specific guide deployment.

Asia-Pacific posts the fastest regional CAGR at 9.36% through 2031 as China, Japan, India, and Southeast Asian nations upgrade hospital infrastructure and harmonize device regulations. Local ministries of health now run pilot programs that subsidize AI-driven orthopedic planning in provincial trauma centers, aiming to raise care parity with urban facilities. Domestic device makers increasingly integrate planning modules into joint implants to differentiate against multinationals, enlarging the competitive field. While reimbursement remains patchy across markets, high private-self-pay demand and rising medical-tourism volumes incentivize premium hospitals to adopt cutting-edge digital workflows ahead of formal policy shifts.

Competitive Landscape

The preoperative surgical planning software market is moderately fragmented, with the top five vendors estimated to control nearly significant market share in the global market. Stryker, Medtronic, Zimmer Biomet, Brainlab, and 3D Systems leverage installed bases of navigation consoles and robots to cross-sell subscription licenses, creating high switching costs. Recent deals, such as Zimmer Biomet’s Monogram acquisition, illustrate the strategic priority placed on proprietary AI engines that lock implants into closed software ecosystems. Brainlab’s planned Frankfurt IPO aims to raise EUR 200 million to fund cloud-first expansions and platform-agnostic integration, signalling investor confidence in pure-play software models.

Mid-tier challengers concentrate on oncology and cranio-maxillofacial niches where precision requirements present technical entry barriers. Start-ups tout native cloud architecture and collaborative workspaces to win contracts from hospital chains seeking vendor-neutral solutions. Large IT conglomerates are also entering through joint ventures with imaging OEMs, betting that their cybersecurity pedigree will reassure risk-averse hospital CIOs. To maintain lead, incumbents are opening developer portals that allow third-party AI modules to plug into their orchestration layers, transforming closed suites into curated app stores.

Preoperative Surgical Planning Software Industry Leaders

Brainlab AG

Stryker

Zimmer Biomet

Medtronic

Smith+Nephew

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Zimmer Biomet completed its USD 177 million acquisition of Monogram Technologies, enhancing its robotics portfolio with hands-free orthopedic surgery capabilities. The acquisition includes Monogram's mBôs system, which utilizes AI and CT scans for preoperative planning and establishes instrument boundaries to protect soft tissue during surgery.

- June 2025: Brainlab AG announced plans for an IPO on the Frankfurt Stock Exchange, aiming to raise up to EUR 200 million to accelerate digital transformation in healthcare. The company reported record revenues of EUR 239 million and a 22.4% EBITDA margin in the first half of FY 2024/25, with solutions used in approximately 4,000 healthcare institutions globally.

- April 2024: Materialise, a medical 3D printing and planning solutions provider, launched Mimics Enlight CMF, a 3D planning software that improves in-house planning for surgical applications. Mimics Enlight CMF offers automated planning and design tools that increase speed, ease of use, and precision for craniomaxillofacial surgical preparation.

- February 2024: Sira Medical, a healthcare technology company, received the US Food and Drug Administration 510(k) clearance for its augmented reality preoperative surgical planning application, which provides clinicians with advanced imaging to assist in making key patient management decisions.

Global Preoperative Surgical Planning Software Market Report Scope

As per the scope of the report, preoperative planning involves the meticulous preparation and evaluation of factors such as anatomical structure using specialized software to simulate the surgical process before the actual operation. The healthcare preoperative surgical planning market is segmented into delivery mode, application, end user, and geography. By delivery mode, the market is segmented into cloud-based and on-premise. By application, the market is segmented into orthopedics, neurology, cardiology, oncology, and other applications (dental and ophthalmic). By end user, the market is segmented into hospitals and surgical centers. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report offers values (USD) for the above segments.

| Cloud-based |

| On-premise |

| Orthopedics |

| Neurology |

| Cardiology |

| Oncology |

| Maxillofacial & Dental |

| Other Application |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Orthopedic Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Delivery | Cloud-based | |

| On-premise | ||

| By Application | Orthopedics | |

| Neurology | ||

| Cardiology | ||

| Oncology | ||

| Maxillofacial & Dental | ||

| Other Application | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Orthopedic Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the preoperative surgical planning software market?

The preoperative surgical planning software market size reached USD 126.66 million in 2026.

How fast is the preoperative surgical planning software market expected to grow?

The market is projected to register a 7.01% CAGR, reaching USD 177.68 million by 2031.

Which deployment model leads the market?

Cloud-based platforms hold the dominant 58.22% share and are advancing at a 10.31% CAGR thanks to multi-site collaboration benefits.

Why is oncology the fastest-growing application area?

Oncology’s 12.92% CAGR stems from the need for millimeter-level accuracy in tumor resections and the growing use of patient-specific 3-D printed guides.

Which region shows the highest growth potential?

Asia-Pacific is forecast to post a 9.36% CAGR through 2031 due to expanding hospital infrastructure and supportive regulatory harmonization.

What are the main barriers to wider adoption?

High subscription fees, integration complexity, and evolving data-security regulations remain the leading hurdles for resource-constrained providers.

Page last updated on: