Preeclampsia Diagnostics Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

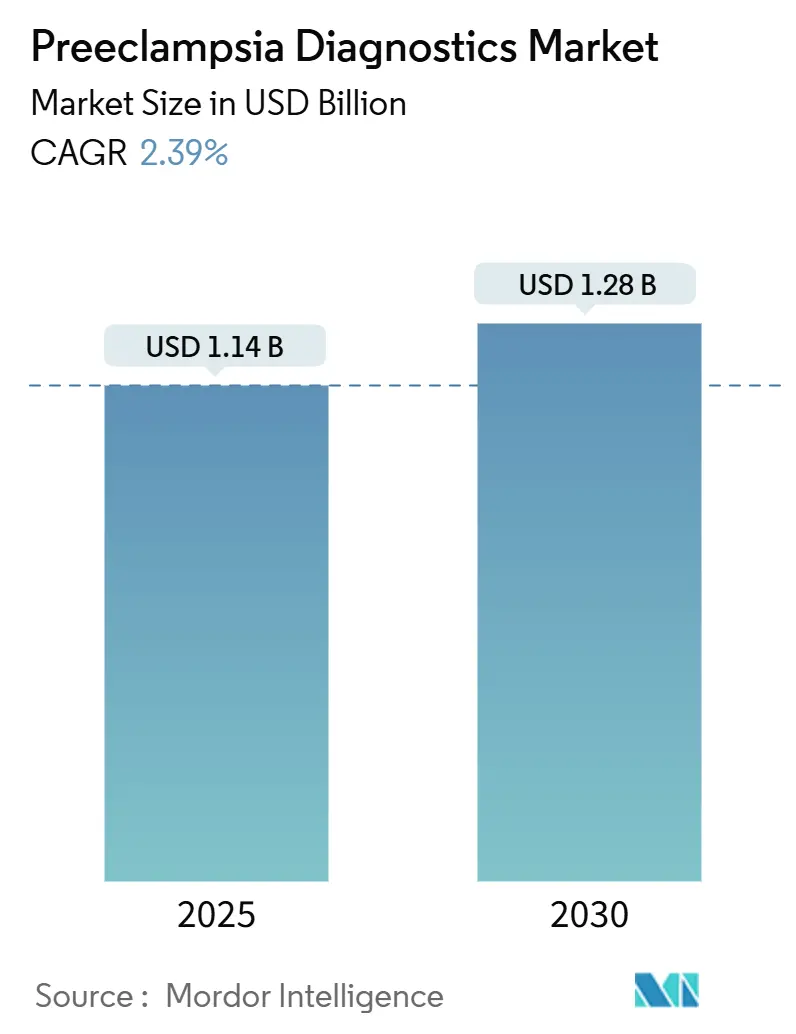

| Market Size (2025) | USD 1.14 Billion |

| Market Size (2030) | USD 1.28 Billion |

| Growth Rate (2025 - 2030) | 2.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Preeclampsia Diagnostics Market Analysis by Mordor Intelligence

The preeclampsia diagnostics market size is expected to reach USD 1.14 billion by 2025. It is forecast to reach USD 1.28 billion by 2030, reflecting a 2.39% CAGR driven by the shift from symptom-based assessments toward validated biomarker platforms. The move to precision testing means adoption grows steadily, rather than surging, as reimbursement rules and regulatory reviews unfold in measured stages. Blood assays that quantify sFlt-1 and PlGF continue to inform clinical practice because they align with existing laboratory workflows and procedures. At the same time, AI-supported genetic panels expand the addressable pool of pregnancies that can be screened at the first prenatal visit. North America retains its leadership position thanks to early FDA clearances, but the Asia-Pacific region is the fastest riser as maternal age increases and public programs fund routine screening. Competitive intensity remains moderate, with multinationals using scale advantages to defend share even as venture-backed start-ups introduce machine-learning algorithms that deepen risk stratification.

Key Report Takeaways

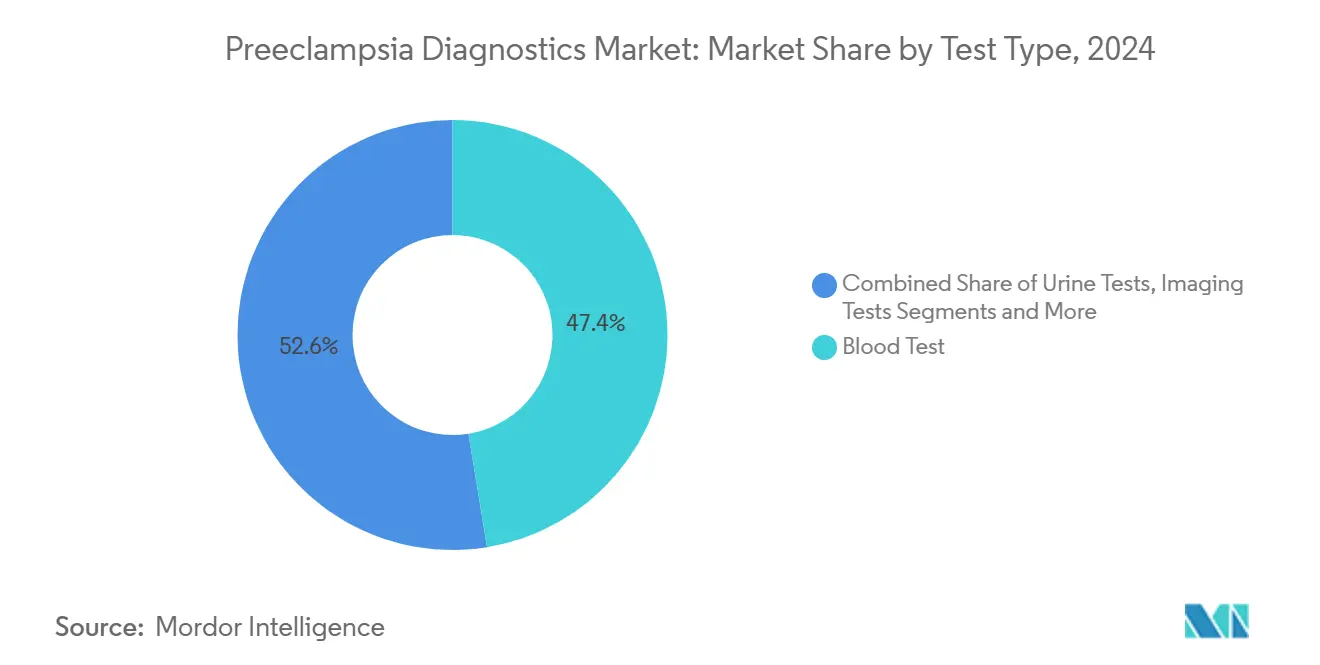

- By test type, blood tests led with 47.44% of the preeclampsia diagnostics market share in 2024; genetic and multiplex assays are advancing at a 5.89% CAGR through 2030.

- By product, kits and reagents captured 49.28% of the preeclampsia diagnostics market size in 2024, while instruments represent the fastest-growing category at a 4.44% CAGR.

- By end user, hospitals held 46.57% revenue share in 2024, whereas home healthcare and tele-prenatal settings are expanding at a 6.32% CAGR.

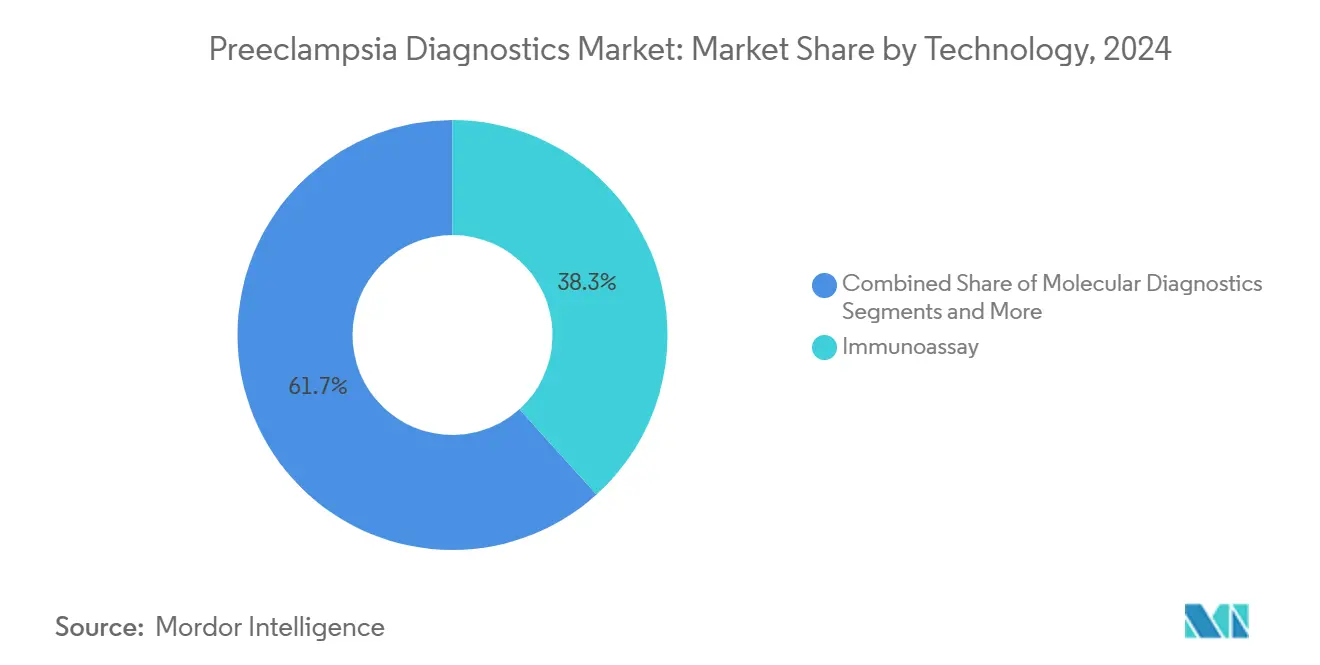

- By 2024, immunoassays contributed a 38.31% share of the preeclampsia diagnostics market size, and AI-driven analytics are projected to record the highest CAGR of 5.98% from 2024 to 2030.

- By mode of testing, laboratory-based methods accounted for a 66.37% share in 2024; point-of-care platforms are growing at a 5.61% CAGR over the same horizon.

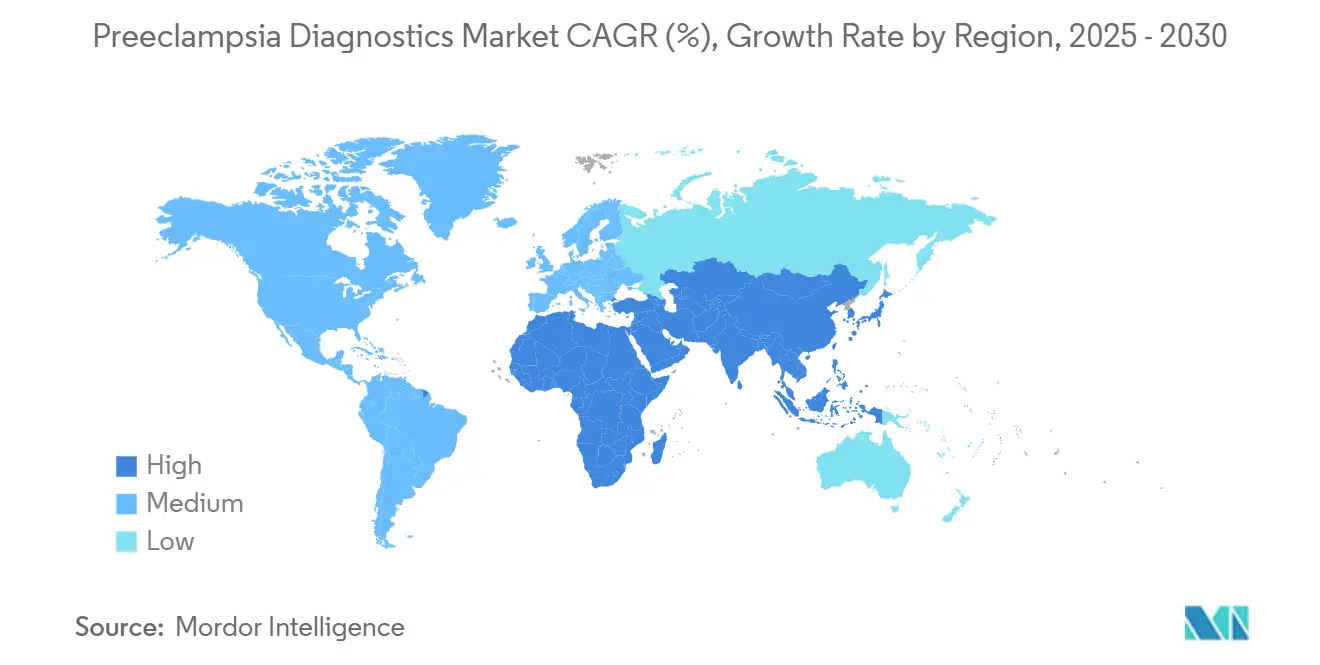

- By geography, North America led the preeclampsia diagnostics market with a 36.57% share in 2024, while the Asia-Pacific region is expected to post a 4.24% CAGR through 2030.

Global Preeclampsia Diagnostics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of hypertensive disorders in pregnancy | +0.8% | North America, Europe, global spill-over | Medium term (2-4 years) |

| Expansion of maternal-health screening programs and guidelines | +0.6% | OECD markets, global scale-up | Long term (≥ 4 years) |

| Rapid adoption of biomarker-based blood assays | +0.5% | North America, Europe, emerging Asia-Pacific | Short term (≤ 2 years) |

| Regulatory approvals and reimbursement expansion | +0.4% | United States, Germany, United Kingdom | Medium term (2-4 years) |

| AI and machine-learning risk-prediction tools | +0.3% | North America, Europe, selective Asia-Pacific | Long term (≥ 4 years) |

| WHO-backed low-cost point-of-care tests in LMICs | +0.2% | Sub-Saharan Africa, Southeast Asia, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Hypertensive Disorders in Pregnancy

Advanced maternal age and higher obesity rates have doubled U.S. preeclampsia incidence over the past decade, affecting roughly 1 in 12 pregnancies.[1]Catherine M. Bradford, “Mirvie Announces Results From New Simple Blood Test To Predict Preeclampsia Risk,” Preeclampsia Foundation, preeclampsia.org Women older than 35 now form the fastest-growing risk cohort, prompting payers to reassess the cost–benefit of widespread early screening. RNA-profile algorithms already detect 91% of preterm cases among this demographic, turning diagnostics from a niche obstetric option into a mainstream service. As similar epidemiologic trends surface in Europe and parts of Asia, the preeclampsia diagnostics market responds with scalable, population-level testing pathways.

Expansion of Maternal-Health Screening Programs & Guidelines

Guideline updates released by the American College of Obstetricians and Gynecologists in June 2024, together with WHO endorsements for point-of-care sFlt-1/PlGF testing, embed biomarker screening in standard prenatal care.[2]Jacqueline Sayers, “A Life-Saving Test for Preeclampsia,” University of Oxford, ox.ac.ukNational pay-for-performance policies, such as the U.K. MedTech Funding Mandate that backs the Oxford test, create guaranteed volumes and stable reimbursement, thereby lowering adoption risk for providers. These directives minimize practice variation, enabling vendors to forecast reagent demand and scale manufacturing with confidence.

Rapid Adoption of Biomarker-Based Blood Assays

FDA 510(k) clearance for Roche’s Elecsys sFlt-1/PlGF test in February 2025, alongside Thermo Fisher’s prior approval, confirms regulatory confidence in biomarker superiority over symptom scoring.[3]Foundation for the National Institutes of Health, “The Foundation for the National Institutes of Health Launches First Public-Private Partnership for Early Detection of Preeclampsia”, fnih.org Large laboratory chains, such as Labcorp, incorporate the assay into first-trimester panels and report a 90% sensitivity, which accelerates physician adoption. Publication of repeat-testing data from the PARROT-2 trial further reassures clinicians by demonstrating consistent performance across gestational weeks, thereby strengthening demand for consumables in core markets.

Regulatory Approvals & Reimbursement Expansion in OECD Markets

Clearances in the United States, Germany, and the United Kingdom shorten the pathway from innovation to bedside implementation. Reimbursement codes secured in 2024 align payer incentives with preventive care objectives, moving biomarker tests from discretionary use to routine prenatal orders. These policies directly add 0.4 percentage points to the global CAGR estimate as monetization certainty encourages hospital procurement committees to formalize testing protocols.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High test cost and limited access in resource-poor settings | -0.4% | Sub-Saharan Africa, Southeast Asia, rural pockets globally | Medium term (2-4 years) |

| Lack of single definitive biomarker resulting in diagnostic uncertainty | -0.3% | Global, with pronounced impact in moderate-risk cohorts | Short term (≤ 2 years) |

| Data-privacy and liability issues linked to AI diagnostics | -0.2% | European Union, North America | Long term (≥ 4 years) |

| Fragile supply chains for monoclonal-antibody reagents | -0.2% | Global, especially during logistics shocks | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Test Cost & Limited Access in Resource-Poor Settings

Current sFlt-1/PlGF assays cost USD 100–200 in wealthy countries, a sum equal to several weeks of household income in low-income regions. Refrigerated transport for antibody kits further increases landed costs, limiting penetration despite elevated maternal mortality rates. Although philanthropic funding targets sub-USD 10 price points, achieving this target without sacrificing analytical performance remains unresolved, which slows volume growth in the highest-need geographies.

Lack Of Single Definitive Biomarker → Diagnostic Uncertainty

Physicians confront overlapping panels with varying thresholds, leading to indecision, especially in moderate-risk pregnancies. The IMPROvED consortium halted a protein-panel project when cross-reactivity reduced accuracy, underscoring technical complexity. This ambiguity encourages clinics to delay full deployment until harmonized guidelines emerge, shaving 0.3 percentage points from the expected CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Blood Assays Anchor Adoption Yet Multiplex Panels Accelerate

Blood assays retain a 47.44% share because clinicians trust their familiar draw-and-analyze workflow, and FDA-approved sFlt-1/PlGF kits deliver reproducible results that fit quality-control norms. This dominance ensures that the preeclampsia diagnostics market size linked to blood tests remains large, even as new entrants emerge. Multiplex genetic platforms demonstrate a 5.89% CAGR, offering earlier detection at the booking visit and integrating AI analysis into tele-prenatal apps.

In parallel, urine-based assays demonstrate a fourfold higher sensitivity in proof-of-concept studies, hinting at a potential for displacement in the future if analytical precision matches that of their blood counterparts. Imaging remains confirmatory rather than screening-focused, sustaining a niche presence. Overall, the preeclampsia diagnostics market responds to risk-stratification innovations but maintains blood tests as the cornerstone of standard care.

By Product: Consumables Creativity Versus Instrument Expansion

Kits and reagents account for 49.28% of the preeclampsia diagnostics market share, as each test cycle requires fresh cartridges and antibody pairs. Vendors derive stable recurring revenue once hospitals lock in brand-specific calibrators. Instruments grow at a rate of 4.44% because point-of-care analyzers shorten turnaround times and are well-suited for outpatient clinics. The preeclampsia diagnostics market size allocated to instruments is expected to increase as decentralized care gains traction, as illustrated by IIT Madras’s 30-minute PlGF biosensor, which circumvents central lab queues.

Software and analytics suites emerge as premium add-ons, bundling cloud dashboards that rank pregnancy risk scores and push decision alerts to obstetricians via secure messaging. Companies calibrate go-to-market strategies by matching consumables pricing with local purchasing power, while retaining higher margins on data subscriptions purchased by tertiary centers.

By End User: Hospitals Retain Control While Tele-Prenatal Adoption Surges

Hospitals account for 46.57% revenue because acute intervention capability remains pivotal when severe preeclampsia escalates. The preeclampsia diagnostics market size is tied to hospital budgets and therefore underpins baseline demand. Home-based collection and tele-prenatal services are projected to post the highest 6.32% CAGR, as patients prioritize convenience and pandemic-era digital habits persist.

Diagnostic centers offer overflow capacity, particularly in countries where central labs lack sufficient bandwidth, while maternal-fetal clinics are among the first to adopt novel biomarkers to differentiate care. Academic laboratories continue to seed innovation pipelines by maintaining pregnancy biobanks that enable the refinement of algorithms.

By Technology: Immunoassays Dominate, AI Analytics Redefine Prediction

Immunoassays hold a 38.31% share, bolstered by decades of validation and standardized quality control metrics. This segment anchors the preeclampsia diagnostics market; however, AI-driven analytics expand at the fastest rate of 5.98%, delivering personalized risk scoring that integrates genomic, proteomic, and hemodynamic inputs.

Molecular diagnostics identify growth opportunities through RNA signature models, while point-of-care systems expand access in clinics lacking advanced analyzers. Imaging complements, but does not displace, biochemical testing. However, AI interpretation of ultrasound flows could soon merge imaging findings with biomarker data in a unified dashboard.

By Mode of Testing: Laboratory Supremacy Meets Point-of-Care Momentum

Laboratory-based testing captures 66.37% share due to entrenched central-lab ecosystems in hospitals and reference networks. This dominance significantly contributes to the size of the preeclampsia diagnostics market. Point-of-care testing, which is growing at a 5.61% annual rate, gains credibility as handheld devices achieve laboratory-grade precision. WHO-supported pilots in Kenya and India reinforce clinical confidence by proving real-time triage is feasible in frontline clinics.

Companies such as MOMM Diagnostics prototype cartridge-based readers designed for emergency rooms. At the same time, MirZyme’s UKCA-approved blood-test genie requires no new hardware, lowering capital hurdles for community obstetric practices.

Geography Analysis

North America’s 36.57% share is driven by FDA approvals, payer coverage, and integrated care networks that rapidly embed validated tests. Labcorp’s first-trimester panel launch in May 2024 accelerated nationwide availability, while the Foundation for the National Institutes of Health orchestrates multicenter biomarker validation that harmonizes clinical guidelines.

Asia-Pacific leads growth with a 4.24% CAGR to 2030. Rising maternal age in China and Japan, combined with government investments in perinatal health, expands the addressable population. IIT Madras’s PlGF biosensor and MirZyme’s partnership with Archerfish illustrate regional innovation that could cut import dependence. Trials in Singapore, Malaysia, and Thailand demonstrate early demand for tele-prenatal risk scoring.

Europe maintains steady momentum through the NHS adoption of the Oxford blood test and EU funding for the IMPROvED consortium. Harmonized procurement in public health systems creates predictable reagent volumes. Roche’s 2024 expansion into 18 Latin American public hospitals reveals a template for growth in South America, where urban maternity wards modernize diagnostic protocols. The Middle East and Africa anticipate future uptake once low-cost point-of-care units clear WHO prequalification and donor programs subsidize rollout.

Competitive Landscape

Market concentration is moderate. Multinationals Abbott, Roche, and Thermo Fisher possess regulatory prowess, extensive distribution networks, and the capital necessary for large-scale clinical trials. Roche’s 2025 clearance intensifies U.S. competition, prompting price benchmarking across hospital groups. Start-ups mirror the preeclampsia diagnostics industry trend toward precision medicine, with Mirvie’s RNA platform and Trinity Biotech’s PrePsia acquisition illustrating how disruptive tech migrates into corporate portfolios.

Strategic moves include Trinity Biotech taking over Metabolomics Diagnostics for USD 1.3 million to accelerate commercialization, and Gravidas Diagnostics securing ARPA-H funding to develop home-based kits. Vendors differentiate themselves based on prediction lead time, ease of sample collection, and analytics integration, rather than antibody chemistry alone. Supply chain resilience for monoclonal antibodies becomes a brand credential after pandemic disruptions spotlighted vulnerabilities.

Preeclampsia Diagnostics Industry Leaders

F. Hoffmann-La Roche

Thermo Fisher Scientific Inc.

Siemens Healthineers

Abbott

Revvity Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: IIT Madras researchers unveiled the P-FAB biosensor, which offers femtomolar PlGF sensitivity and a 30-minute workflow, targeting resource-constrained clinics.

- February 2025: University of Queensland published data on nanoflower sensor accuracy exceeding 90% at 11-13 weeks of gestation, furthering ultra-early risk assessment.

Global Preeclampsia Diagnostics Market Report Scope

| Blood Tests |

| Urine Tests |

| Imaging Tests |

| Genetic / Multiplex / Other Emerging Tests |

| Kits & Reagents |

| Instruments |

| Consumables |

| Software / AI Platforms |

| Hospitals |

| Diagnostic Centers |

| Specialty Maternal-Fetal Clinics |

| Home Healthcare & Tele-Prenatal |

| Research & Academic Laboratories |

| Immunoassays |

| Molecular Diagnostics |

| Point-of-Care Testing |

| Imaging Technologies |

| AI-Driven Analytics |

| Laboratory-based Testing |

| Point-of-Care Testing |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | Blood Tests | |

| Urine Tests | ||

| Imaging Tests | ||

| Genetic / Multiplex / Other Emerging Tests | ||

| By Product | Kits & Reagents | |

| Instruments | ||

| Consumables | ||

| Software / AI Platforms | ||

| By End User | Hospitals | |

| Diagnostic Centers | ||

| Specialty Maternal-Fetal Clinics | ||

| Home Healthcare & Tele-Prenatal | ||

| Research & Academic Laboratories | ||

| By Technology | Immunoassays | |

| Molecular Diagnostics | ||

| Point-of-Care Testing | ||

| Imaging Technologies | ||

| AI-Driven Analytics | ||

| By Mode of Testing | Laboratory-based Testing | |

| Point-of-Care Testing | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the preeclampsia diagnostics market?

The preeclampsia diagnostics market size is USD 1.14 billion in 2025.

How fast is the sector expected to grow?

The market is projected to expand at a 2.39% CAGR, reaching USD 1.28 billion by 2030.

Which region leads adoption of biomarker tests?

North America holds 36.57% market share due to early FDA clearances and reimbursement coverage.

Which test type is gaining share most rapidly?

Genetic and multiplex assays show the fastest 5.89% CAGR because they enable first-trimester prediction.

Why do kits and reagents dominate product revenue?

Hospitals reorder consumables for every patient, giving kits and reagents a 49.28% share of global sales.

What restrains uptake in low-income countries?

High per-test costs and cold-chain logistics limit access despite significant disease burden.

Page last updated on: