Preterm Birth Prevention And Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Market Size (2026) | USD 2.08 Billion |

| Market Size (2031) | USD 3.17 Billion |

| Growth Rate (2026 - 2031) | 8.83% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Preterm Birth Prevention And Management Market Analysis by Mordor Intelligence

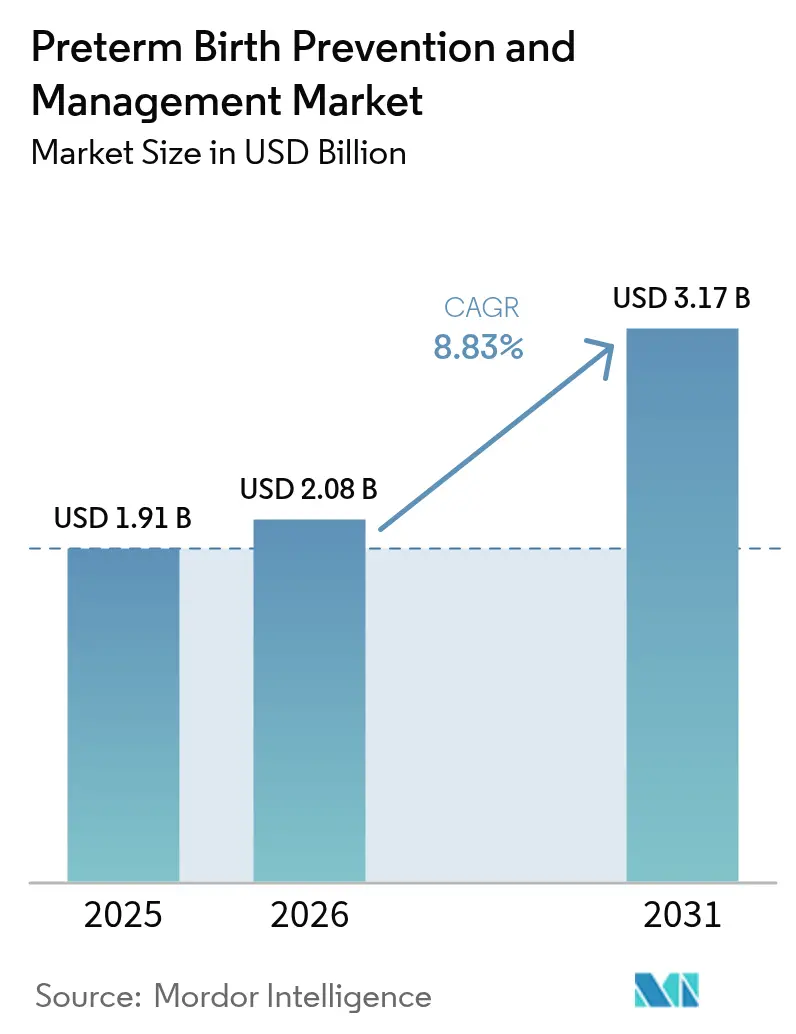

The preterm birth prevention and management market size is expected to grow from USD 1.91 billion in 2025 to USD 2.08 billion in 2026 and is forecast to reach USD 3.17 billion by 2031 at 8.83% CAGR over 2026-2031. Clinical urgency, guideline convergence around progesterone therapy, and rapid adoption of point-of-care biomarker tests anchor current demand. Regulatory withdrawal of ineffective agents has redirected investment toward evidence-based therapeutics and diagnostics, while government funding programs are lowering adoption barriers and catalyzing innovation. Commercial focus is moving from reactive acute-care drugs toward precision risk-stratification platforms that allow earlier, cost-effective intervention. Competitive intensity is rising as pharmaceutical incumbents expand formulation portfolios and diagnostic specialists scale rapid tests with artificial-intelligence (AI) analytics.

Key Report Takeaways

- By intervention, therapeutics led with 60.62% of preterm birth prevention and management market share in 2025; diagnostics are projected to grow at a 9.41% CAGR to 2031

- By route of administration, vaginal formulations commanded 44.02% share of the preterm birth prevention and management market size in 2025, whereas oral delivery is advancing at a 9.62% CAGR between 2026-2031

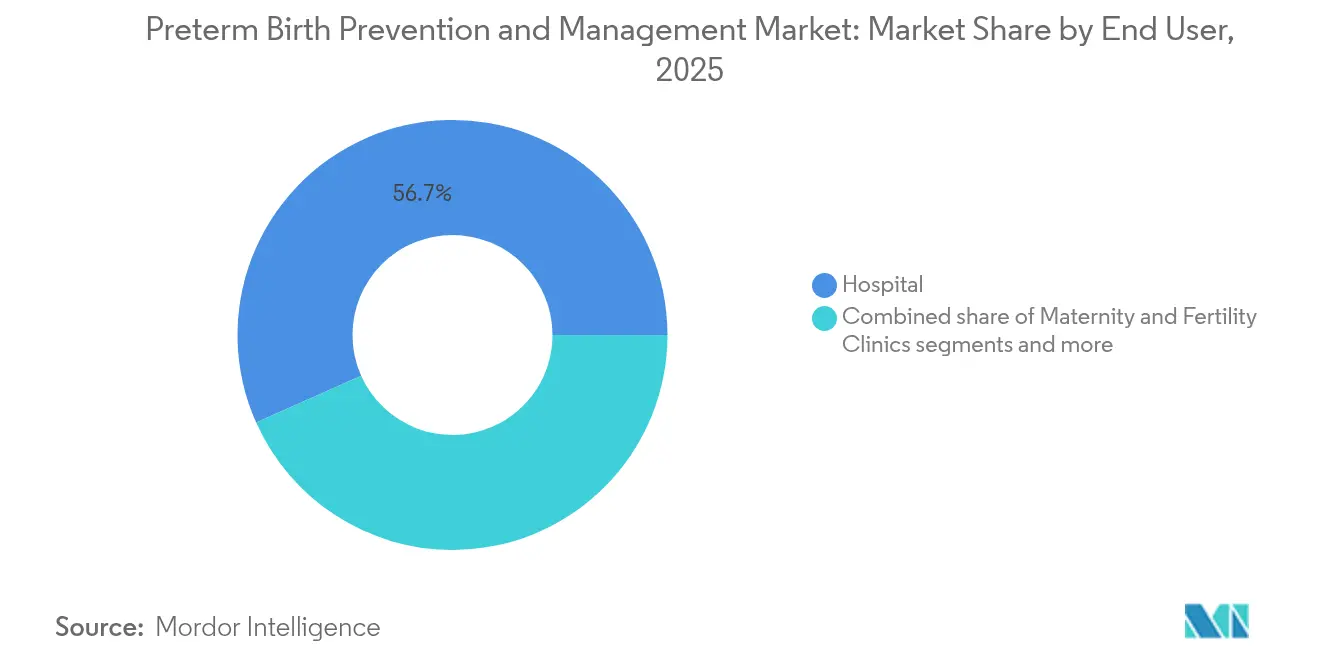

- By end user, hospitals accounted for 56.68% of revenue in 2025 and home healthcare is registering the fastest 10.65% CAGR through 2031

- By gestational-age category, extremely preterm cases (<28 weeks) held 53.21% share and are expanding at 9.88% CAGR, the highest among all categories

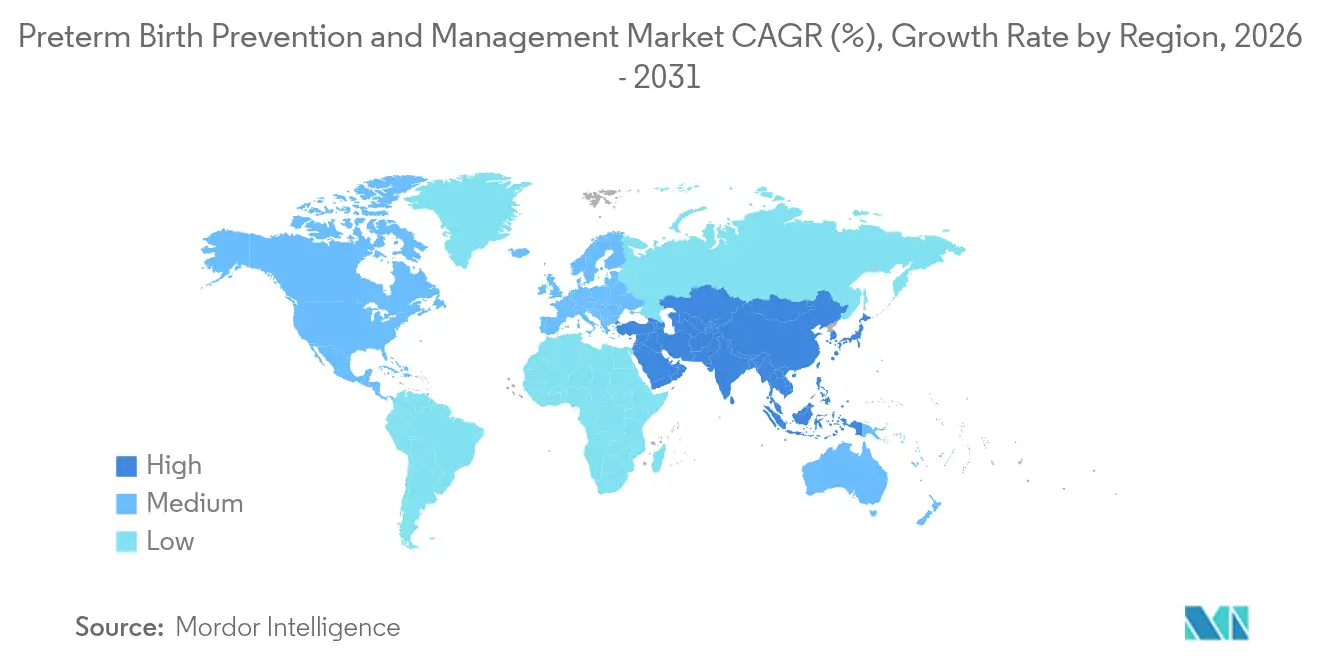

- By geography, North America led with 41.76% share in 2025, while Asia-Pacific is forecast to post the quickest 10.05% CAGR through 2031

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Preterm Birth Prevention And Management Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating global incidence of preterm births | +2.1% | Global, with highest impact in Sub-Saharan Africa and South Asia | Long term (≥ 4 years) |

| Clinical-guideline shift toward progesterone therapy | +1.8% | North America & EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Rapid uptake of point-of-care biomarker tests | +1.5% | Global, led by developed markets | Short term (≤ 2 years) |

| Government maternal-health funding boosts | +1.2% | North America, with spillover to emerging markets | Medium term (2-4 years) |

| AI-driven risk-stratification platforms | +0.9% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Repurposed vasodilators entering late-stage trials | +0.7% | Global clinical trial networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Global Incidence of Preterm Births

Preterm births now affect 13.4 million infants a year, anchoring steady demand across therapeutic and diagnostic segments. Rising maternal age, multiple-birth pregnancies from assisted-reproductive technologies, and persistent care disparities sustain the upward trend. Low- and middle-income countries shoulder the heaviest burden, yet cost pressures are global because life-long care of survivors tops USD 30 billion in annual spending in the United States alone. This epidemiology is driving simultaneous growth in preventive interventions and neonatal intensive-care technologies, reinforcing a dual-growth dynamic that keeps the preterm birth prevention and management market expanding on multiple fronts.

Clinical-Guideline Shift Toward Progesterone Therapy

Professional societies now endorse vaginal progesterone for women with short cervix after the withdrawal of 17-hydroxyprogesterone caproate. The pivotal PREGNANT trial showed a 45% drop in preterm deliveries, eliminating earlier uncertainty and unifying prescribing patterns. Pharmaceutical firms are responding with sustained-release microcrystal formulations that improve adherence, while genetic research is clarifying which patients benefit most. The resulting clarity is channelling capital toward route-of-administration innovation and supports predictable volume growth.

Rapid Uptake of Point-of-Care Biomarker Tests

The shift from subjective assessment to objective biomarker evaluation continues to reshape clinical workflow. The Rapid fFN test delivers results in 10 minutes and registers a 96% negative predictive value, allowing safe discharge of low-risk patients. Parallel advances combine multiple analytes; cell-free RNA signatures can predict preterm birth four months in advance, opening a new prevention window. Growing integration with electronic medical records enables real-time decision support, fuelling the fastest CAGR in the overall preterm birth prevention and management market.

Government Maternal-Health Funding Boosts

Federal spending is expanding. The NIH IMPROVE initiative secured USD 53.4 million for FY2024, and 15 US states received combined grants of USD 19 million for innovative maternal-health projects[1]. Grant dollars focus on hypertension screening, community-based training, and home-based diagnostics, directly enlarging the addressable market and reducing private-sector risk. Similar policy momentum is emerging in Canada, the United Kingdom, and Japan, laying durable demand foundations for the preterm birth prevention and management market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FDA withdrawal of Makena & tighter regulations | -1.4% | North America, with spillover to global regulatory agencies | Short term (≤ 2 years) |

| Limited novel-drug R&D investment | -0.8% | Global pharmaceutical industry | Long term (≥ 4 years) |

| Elective-cesarean trend curbing tocolytic demand | -0.6% | Developed markets, particularly North America and Europe | Medium term (2-4 years) |

| API supply-chain fragility for key hormones | -0.5% | Global, with highest impact in emerging markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

FDA Withdrawal of Makena and Tighter Regulations

Regulators pulled 17-hydroxyprogesterone caproate from the market in 2023 after efficacy and safety doubts surfaced, forcing clinicians to redesign treatment protocols and raising evidentiary hurdles for new agents. The action lengthens development timelines and raises capital requirements for future therapeutics, tempering growth momentum in the near term even as it safeguards patient outcomes.

Limited Novel-Drug R&D Investment

High trial-failure rates and ethical complexities around pregnant populations have curbed venture funding for first-in-class molecules. Developers now prioritize repurposed drugs, such as antibiotics under investigation that showed 40% reduction in preterm births in a recent New England Journal of Medicine trial. This incremental approach constrains breakthrough potential but keeps pipeline risk manageable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Intervention: Diagnostics Mount a Rapid Challenge to Therapeutics

Therapeutics retained leadership with a 60.62% slice of the preterm birth prevention and management market in 2025, anchored by progesterone, calcium channel blockers, and corticosteroids. Vaginal progesterone remains first line, while nifedipine outperforms historic tocolytics in prolonging gestation. Corticosteroids continue to support fetal lung maturation under strict gestational-age windows. Pipeline activity spans oxytocin-receptor antagonists and vasodilator combinations, yet uptake hinges on clearer survival data.

Diagnostics are posting the fastest 9.41% CAGR, fuelled by fibronectin kits, PAMG-1 assays, and cervical-length ultrasound systems that integrate with machine-learning risk-scoring. High negative predictive value shortens hospital stays and guides targeted steroid use, strengthening payer backing. Combined, these trends reinforce the preterm birth prevention and management market as a prevention-first clinical environment.

By Route of Administration: Vaginal Dominance Meets Oral Momentum

Vaginal delivery captured 44.02% share of the preterm birth prevention and management market size in 2025 because local dosing concentrates progesterone where it is needed and minimizes systemic side effects. Self-administration, sustained-release rings, and low storage costs favour further adoption.

Oral formulations are accelerating at 9.62% CAGR, energised by micronization and protective coatings that lift bioavailability to therapeutic thresholds. Patients prefer tablets for convenience, and physicians value simplified prescribing. Parenteral routes retain a corner niche for emergency tocolysis but face user discomfort and higher site-of-care costs.

By End User: Hospitals Remain Anchors as Home Healthcare Expands

Hospitals held 56.68% of revenue in 2025, relying on neonatal intensive-care units and 24 × 7 obstetric teams that manage complex deliveries. Tertiary centres also run most clinical trials, so they keep early access to new technology.

Home healthcare is advancing at 10.65% CAGR thanks to connected devices that transmit uterine-activity and blood-pressure data directly to clinicians. Remote models lower admission rates and improve access in rural settings, thereby enlarging the reach of the preterm birth prevention and management market.

By Gestational-Age Risk Category: Extreme Prematurity Drives Spend

Extremely preterm births accounted for 53.21% of revenue in 2025, and their 9.88% CAGR underscores both clinical need and technological progress. Intensive ventilation, surfactant therapy, and personalised steroid protocols improve survival, justifying resource concentration.

Very preterm (28–32 weeks) and moderate-to-late preterm (32–37 weeks) segments grow steadily as corticosteroid guidelines widen and antenatal care access improves. ACTION-III trial results could broaden corticosteroid use in late-preterm births and increase addressable volumes.

Geography Analysis

North America commanded 41.76% of the preterm birth prevention and management market share in 2025, sustained by reimbursement structures, NIH funding streams, and guideline maturity. Market penetration of rapid biomarker tests and sustained-release progesterone is already high. Regulatory uncertainty after Makena’s withdrawal spurred tighter pharmacovigilance but also nudged clinics toward diagnostically driven care paths.

Asia-Pacific registers the quickest 10.05% CAGR, propelled by broader insurance coverage, government device-approval reforms, and multi-country cohort studies such as CARE-Preterm that standardise neonatal care. China’s expanding NICU network and India’s Single Window regulatory portal are shortening product-rollout timelines, while Japan is integrating vaginal progesterone into routine obstetrics. Collectively, the region is reshaping volume dynamics for the preterm birth prevention and management market.

Europe, the Middle East and Africa, and South America offer incremental upside. EMA’s suspension of 17-hydroxyprogesterone caproate is accelerating adoption of alternative agents. Sub-Saharan Africa remains the highest-incidence region yet faces infrastructure gaps, creating white-space for low-cost diagnostics and telehealth. South American regulators are investing in maternal-health capacity building, helping lift baseline demand.

Competitive Landscape

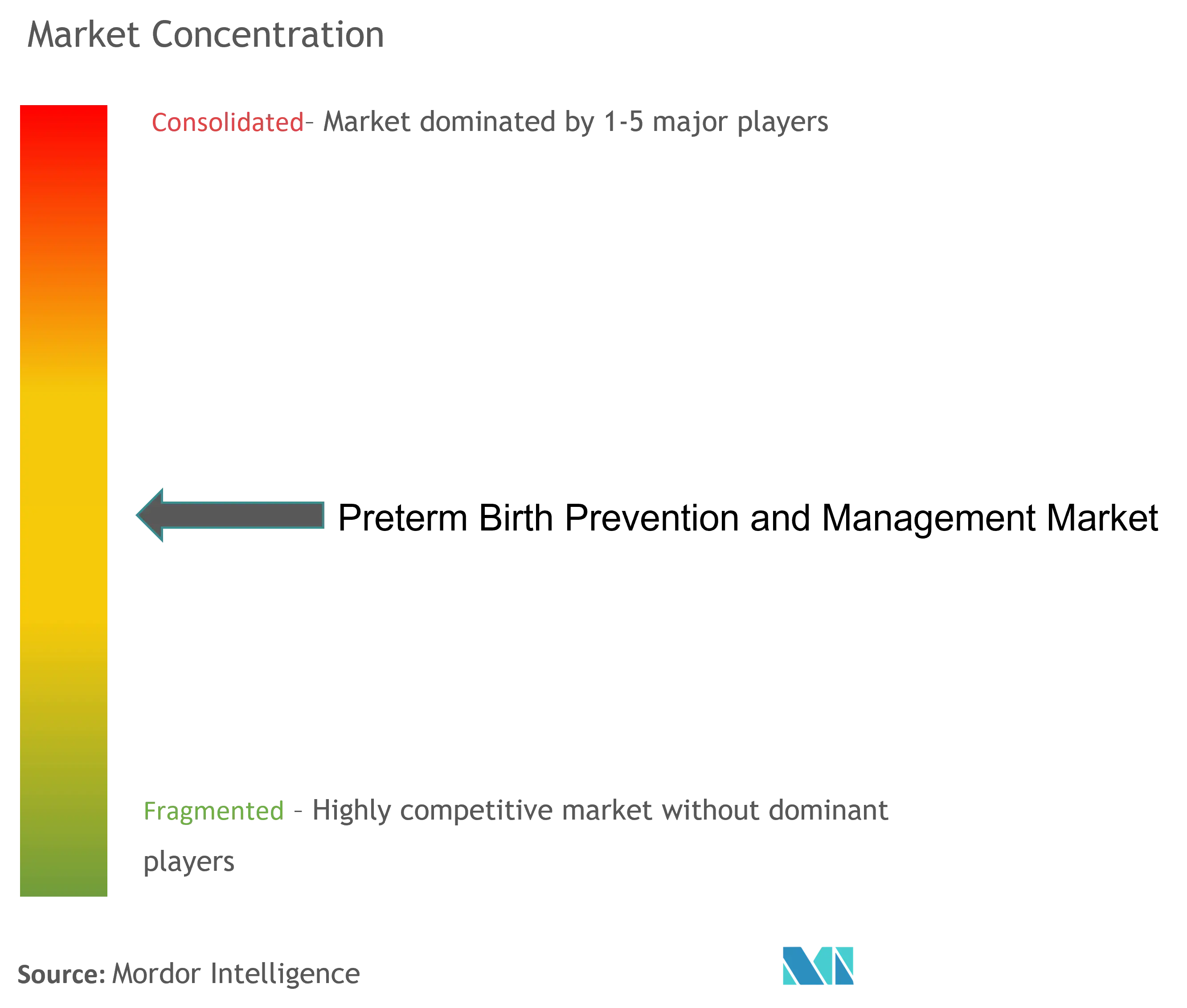

The preterm birth prevention and management market is moderately fragmented because varied g estational-age profiles and mixed care settings demand multiple solutions. Top pharmaceutical suppliers anchor the progesterone and tocolytic space, but diagnostic innovators are scaling faster as point-of-care tests become standard. Market leaders combine risk-prediction algorithms with proprietary biomarker kits, offering bundled solutions that hospitals adopt quickly.

Strategic moves in 2024–2025 confirm the trend. Roche gained FDA clearance for its Elecsys sFlt-1/PlGF ratio test, widening its maternal-health footprint[2]. Large drug makers are upgrading formulation patents to extend revenue streams as generic progesterone looms. Meanwhile, AI start-ups license predictive models to device makers, embedding analytics into existing ultrasound and monitoring equipment.

White-space remains in emerging economies where infrastructure limits diagnostic deployment. Companies are piloting solar-powered analyzers and smartphone-integrated readers to lower cost of ownership. Partnerships with public-health agencies accelerate uptake and distribute financial risk, reinforcing a competitive pivot toward accessibility and scalability in the preterm birth prevention and management market.

Preterm Birth Prevention And Management Industry Leaders

-

Covis Pharma GmbH. (AMAG Pharmaceuticals, Inc.)

-

Ferring B.V.

-

Pfizer Inc.

-

Takeda Pharmaceutical Company Limited.

-

ObsEva

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Roche received FDA 510(k) clearance for its Elecsys sFlt-1/PlGF ratio test to predict severe preeclampsia risk in pregnant women.

- October 2025: The Biden-Harris Administration awarded USD 19 million to 15 states through HRSA to implement innovative maternal health strategies, including early identification and treatment of hypertension to reduce preeclampsia risks.

Global Preterm Birth Prevention And Management Market Report Scope

As per the scope of the report, the preterm birth prevention and management market report covers various therapies which prevent and manage preterm birth. It is defined as babies born alive before 37 weeks of pregnancy are completed. There are sub-categories of preterm birth based on gestational age, i.e., extremely preterm (less than 28 weeks), very preterm (28 to 32 weeks), and moderate to late preterm (32 to 37 weeks). The Preterm Birth Prevention and Management Market is Segmented by Therapy Type (Progesterone Therapy, Corticosteroid Therapy, Tocolytics Therapy, Antibiotics Therapy, Heparin Profylaxis Therapy, and Others), Route of Administration (Oral, Parenteral, and Vaginal), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, and Others), and Geography (North America, Europe, Asia Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Therapeutics | Calcium Channel Blockers |

| Progesterone Therapy | |

| Oxytocin Receptor Antagonists | |

| Corticosteroids | |

| Others | |

| Diagnostics | Biomarker Test Kits (fFN, PAMG-1) |

| Cervical Length Ultrasound Devices | |

| Other Diagnostic Tools |

| Vaginal |

| Oral |

| Parenteral |

| Hospitals |

| Maternity & Fertility Clinics |

| Home Healthcare Settings |

| Research & Academic Institutes |

| Extremely Preterm (<28 w) |

| Very Preterm (28–32 w) |

| Moderate–Late Preterm (32–37 w) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa |

| By Intervention | Therapeutics | Calcium Channel Blockers |

| Progesterone Therapy | ||

| Oxytocin Receptor Antagonists | ||

| Corticosteroids | ||

| Others | ||

| Diagnostics | Biomarker Test Kits (fFN, PAMG-1) | |

| Cervical Length Ultrasound Devices | ||

| Other Diagnostic Tools | ||

| By Route of Administration | Vaginal | |

| Oral | ||

| Parenteral | ||

| By End User | Hospitals | |

| Maternity & Fertility Clinics | ||

| Home Healthcare Settings | ||

| Research & Academic Institutes | ||

| By Gestational-Age Risk Category | Extremely Preterm (<28 w) | |

| Very Preterm (28–32 w) | ||

| Moderate–Late Preterm (32–37 w) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the preterm birth prevention and management market?

The preterm birth prevention and management market is valued at USD 2.08 billion in 2026.

How fast is the market expected to grow over the next five years?

From 2026 to 2031 the market is forecast to expand at an 8.83% CAGR, reaching USD 3.17 billion.

Which intervention segment is expanding the quickest?

Diagnostics—led by rapid fetal-fibronectin and PAMG-1 biomarker tests—posts the fastest 9.41% CAGR through 2031.

Why are vaginal progesterone formulations preferred in clinical practice?

Vaginal progesterone delivers higher local uterine concentrations with fewer systemic side effects and holds 44.02% market share in 2025.

Page last updated on: