Pregnancy Products Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.67 Billion |

| Market Size (2031) | USD 3.49 Billion |

| Growth Rate (2026 - 2031) | 5.52% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pregnancy Products Market Analysis by Mordor Intelligence

The pregnancy products market size is expected to grow from USD 2.53 billion in 2025 to USD 2.67 billion in 2026 and is forecast to reach USD 3.49 billion by 2031 at 5.52% CAGR over 2026-2031. The pregnancy products market benefits from widening employer-funded family-building benefits, rapid uptake of artificial-intelligence fetal-monitoring wearables, and a booming e-pharmacy channel that removes distance barriers for rural consumers. Consumer migration toward flavorful prenatal gummies, rising venture-capital inflows into maternal-health start-ups, and corporate ESG commitments to clean-label stretch-mark topicals further extend the pregnancy products market runway. FDA clearances for wireless fetal monitors and mainstream adoption of digital pregnancy-test kits shorten traditional care pathways, reinforcing adoption among digitally engaged mothers. Competitive intensity remains moderate, with multinational healthcare conglomerates leveraging omnichannel footprints while direct-to-consumer newcomers use transparency and subscription models to win loyalty in the pregnancy products market.

Key Report Takeaways

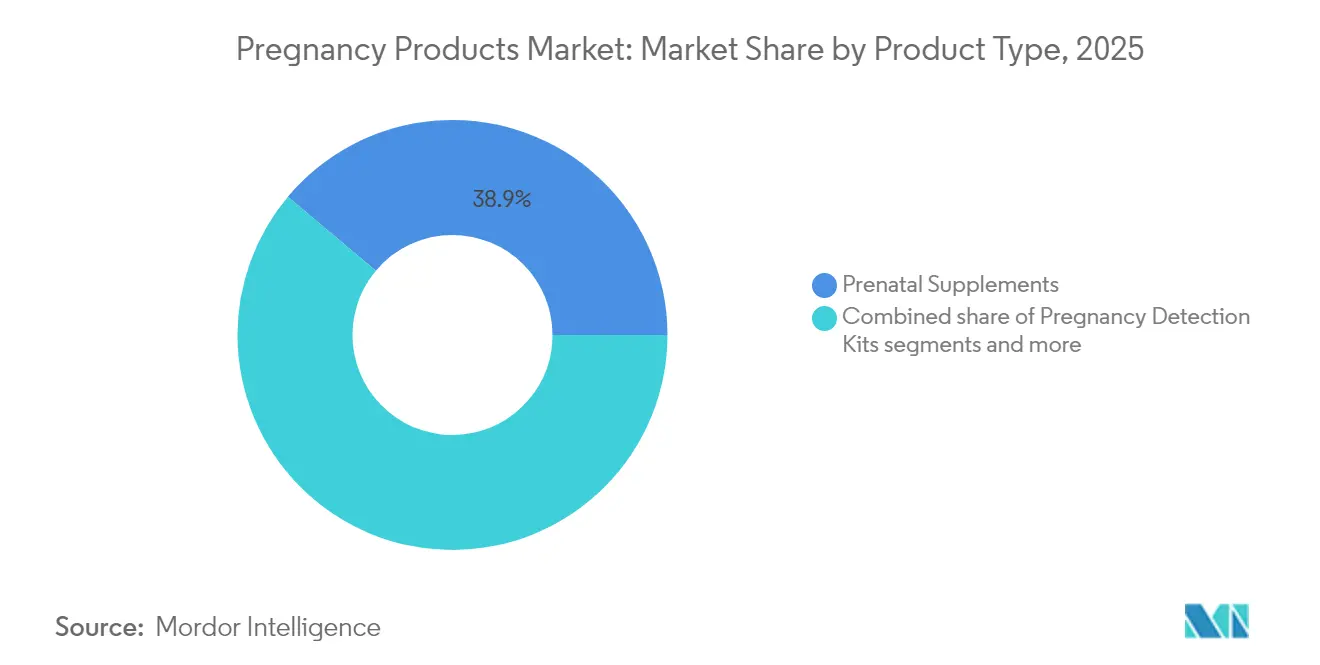

- By product type, prenatal supplements held 38.88% of pregnancy products market share in 2025, whereas prenatal monitoring devices are projected to expand at a 6.51% CAGR through 2031.

- By stage, the pregnancy phase commanded 53.33% of the pregnancy products market size in 2025, while the pre-conception segment is poised for a 5.61% CAGR to 2031.

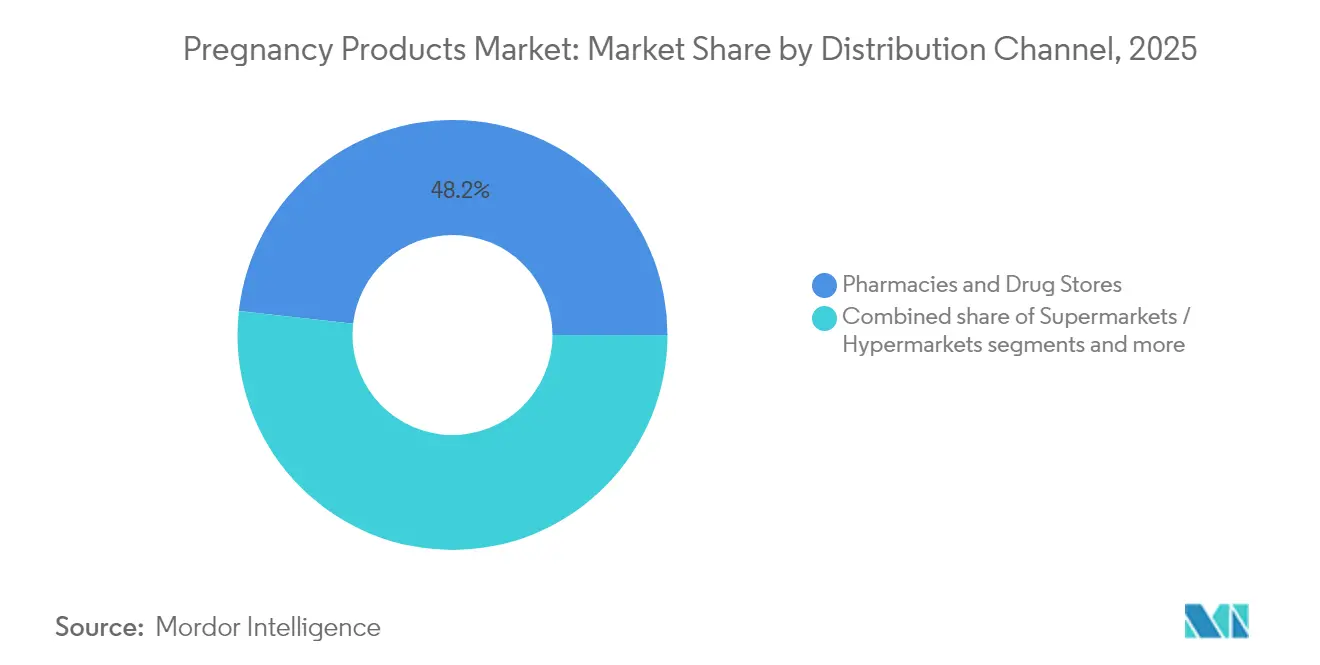

- By distribution channel, pharmacies and drug stores captured 48.22% of the pregnancy products market size in 2025; online retail is forecast to grow at a 5.76% CAGR over 2026-2031.

- By geography, North America led with a 34.98% revenue share in 2025, yet Asia-Pacific is set to post the fastest 5.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pregnancy Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising penetration of over-the-counter digital pregnancy-test kits | +0.8% | Asia-Pacific, Sub-Saharan Africa | Medium term (2-4 years) |

| Mainstream shift toward prenatal gummy formats | +0.6% | North America & Europe | Short term (≤ 2 years) |

| E-pharmacy boom lowering access barriers for rural expectant mothers | +1.2% | Global with Asia-Pacific focus | Long term (≥ 4 years) |

| Growth in employer-funded maternal-wellness benefits packages | +0.9% | North America expanding to Europe | Medium term (2-4 years) |

| AI-enabled fetal-monitoring wearables gaining clinical validation | +0.7% | Global led by North America | Long term (≥ 4 years) |

| Corporate ESG pressure favoring clean-label stretch-mark topicals | +0.4% | North America & Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Penetration of Over-the-Counter Digital Pregnancy-Test Kits in Emerging Economies

Community home-testing programs in rural Kenya report 84% acceptance, linking positive results to antenatal care services. A Nigerian initiative that coupled mobile phones with service upgrades raised primary-facility utilization among pregnant women. Yet kit shortages, privacy worries, and counterfeit imports on e-commerce platforms require continued investment in supply-chain integrity and patient education.

Mainstream Shift Toward Prenatal Gummy Formats in North America & Europe

Nutritionists now highlight bioavailable choline at 450 mg per day for fetal brain development, prompting brands to upgrade formulations. Retailers are dedicating shelf end-caps to gummies, while subscription models sustain recurring revenue in the pregnancy products market. Although saturation risks loom, sugar-reduced and plant-based variants keep innovation pipelines robust, supporting steady demand.

E-pharmacy Boom Lowering Access Barriers for Rural Expectant Mothers

Mobile apps now aggregate ordering, tele-consults, and doorstep delivery, shrinking travel costs and wait times for pregnant women in underserved regions. In Southwest Nigeria, video-based staff training plus digitized records improved clinic attendance and staff motivation. Pilot projects combining mobile ordering with community-health-worker guidance also cut rural preterm births, although statistical significance varied. Integration of artificial intelligence for predictive analytics promises personalized risk alerts tied directly to online pharmacies, cementing long-term growth for the pregnancy products market.

AI-Enabled Fetal-Monitoring Wearables Gaining Clinical Validation

FDA clearance for GE Healthcare’s Novii+ and Bloomlife’s MFM-Pro validated remote uterine and heart-rate tracking outside hospitals. Correlation coefficients of 0.92 for fetal heart rate and 0.97 for maternal heart rate versus cardiotocography underscore clinical robustness. A cardiac-derived algorithm reached 89.8% sensitivity in contraction detection, outperforming conventional sensors in obese patients. These devices mitigate clinician shortages and enable at-home monitoring that became essential during COVID-19, expanding premium slices of the pregnancy products market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing reports of mislabeled prenatal supplements | -1.1% | Global, concentrated in North America | Short term (≤ 2 years) |

| Price inflation across maternity wear supply chains | -0.6% | Global | Medium term (2-4 years) |

| Fake/grey-market pregnancy-test kits on e-commerce platforms | -0.4% | Global, particularly Asia-Pacific | Short term (≤ 2 years) |

| Low prenatal-vitamin adherence in low-literacy populations | -0.8% | Sub-Saharan Africa, South Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Reports of Mislabeled Prenatal Supplements

A 2023 Government Accountability Office audit found 11 of 12 top-selling prenatal supplements carried nutrient amounts outside acceptable label deviations[1]Source: U.S. Government Accountability Office, “Prenatal Supplements: Amounts of Some Key Nutrients Differed from Product Labels,” gao.gov . FDA warning letters to manufacturers such as Quality Supplement Manufacturing highlighted poor identity testing and adulteration risks. Label discrepancies erode consumer trust and raise overdose or deficiency threats, restraining near-term sales in the pregnancy products market. Retailers have begun mandating third-party assays and QR-code traceability to restore credibility. Brands aligning with pharmacopeial standards stand to gain shelf priority as regulations tighten.

Price Inflation Across Maternity-Wear Supply Chains

Volatile cotton and freight prices inflate input costs, prompting mid-tier apparel brands to pass expenses on to consumers. While premium athleisure remains resilient due to higher discretionary budgets among urban mothers, value segments experience demand elasticity. Manufacturers are experimenting with recycled fibers and local production hubs to offset logistics shocks, yet margin compression persists. Persistent inflation could divert household spending to essential prenatal health items over fashion, nudging the pregnancy products market toward non-discretionary segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Supplements Lead, Monitoring Devices Accelerate

Prenatal supplements captured 38.88% pregnancy products market share in 2025, underscoring clinical consensus on folic-acid, iron, and choline intake. Pharmacies leverage pharmacist counseling and employer benefit cards to drive steady unit turnover. AI-powered apps that remind mothers of dosing windows further bolster compliance, extending lifetime value across refill cycles. In contrast, FDA-cleared wireless monitors position prenatal monitoring devices for a 6.51% CAGR, with hospitals integrating at-home data feeds into electronic records to reduce clinic visits. Early adopters tout improved high-risk pregnancy surveillance, propelling hospital procurement budgets and direct-to-consumer purchases. Pregnancy detection kits maintain baseline demand, especially in emerging economies where clinic access is limited. Clean-label stretch-mark creams ride ESG tailwinds, while maternity wear navigates cost pressure by bundling with merchandise return schemes. High-density memory-foam pregnancy pillows and luxury postpartum recovery kits fill discretionary niches, complementing core health categories and rounding out the pregnancy products market.

By Stage: Pregnancy Dominates, Pre-conception Gains Momentum

The pregnancy stage accounted for 53.33% of pregnancy products market size in 2025, reflecting nine months of continuous demand across supplements, monitors, and apparel. Hospital discharge packs often bundle sample vitamins and creams, deepening brand exposure. Tele-obstetrics platforms integrate fetal monitor rentals and digital nutrition plans, further anchoring consumption. Pre-conception is forecast to expand at a 5.61% CAGR, powered by fertility-benefit coverage that reimburses ovulation predictors, genetic testing, and nutrient preload kits. Employers that subsidize egg freezing widen the customer funnel well before conception, lengthening product journeys in the pregnancy products market. Post-partum remains under-served, but interest in lactation aids, pelvic-floor trainers, and overnight care packages is rising, illustrated by luxury retreats in New York and San Francisco offering bundled recovery services. Payors like UnitedHealthcare will reimburse doula support from 2026, signaling formal recognition of holistic care needs.

By Distribution Channel: Pharmacies Prevail, Online Retail Surges

Pharmacies and drug stores retained 48.22% share of the pregnancy products market size in 2025, aided by pharmacist credibility and rapid access to time-sensitive items such as nausea relief and iron supplements. Chain pharmacies add point-of-care labs and vaccination booths, drawing sustained footfall. Online retail, however, is set for a 5.76% CAGR as direct-to-consumer brands exploit quizzes, tele-chat, and subscription refills to bypass physical shelf limits. Ritual’s transparency-centric model crossed USD 250 million annual revenue, proving online scalability. Counterfeit risks persist on open marketplaces, pushing shoppers toward brand-owned sites with batch verification. Supermarkets serve budget-conscious households by bundling prenatal staples within weekly grocery runs, while specialty boutiques cater to premium shoppers seeking curated assortments and expert fittings.

Geography Analysis

North America commands 34.98% of 2025 revenue thanks to broad insurance coverage, employer fertility perks, and cultural acceptance of proactive maternal care. Digital-health partnerships like Maven Clinic reduced NICU admissions by 40% and emergency visits by 33% for enterprise clients, demonstrating tangible ROI. E-pharmacy fulfillment centers support same-day prenatal deliveries, embedding convenience within the pregnancy products market. Regulatory alertness, however, stays high as GAO tests reveal label inaccuracies and the FDA increases inspections.

Asia-Pacific is projected to deliver the highest 5.86% CAGR through 2031, buoyed by urbanization, rising disposable income, and government investments in maternal health. Local brands tailor herbal prenatal formulas to cultural diets, while multinationals localize SKUs and partner with e-pharmacy giants to reach tier-2 cities.

Europe maintains steady growth fueled by sustainability-led innovation. L’Oréal’s eco-designed stretch-mark creams and traceable sourcing frameworks set category standards, while GDPR dictates stringent data-handling rules for digital monitors. Birth-rate declines encourage companies to widen lifetime value by upselling postpartum and menopause solutions, merging women’s health lines under unified brand roofs. South America and Middle East & Africa remain nascent yet promising, given youthful demographics and improving digital infrastructure; however, supply-chain fragmentation and price sensitivity necessitate tiered-pricing strategies to unlock full potential of the pregnancy products market.

Regulatory Landscape

Regulation in the pregnancy products market splits between consumer health products, such as prenatal supplements and stretch-mark topicals, and medical devices or software, such as fetal monitoring wearables and AI-enabled ultrasound or decision-support tools. In the United States, FDA activity in 2026 reinforced device-submission and software oversight. The agency finalized guidance on the Content of Human Factors Information in Medical Device Marketing Submissions for CDRH-regulated devices (May 2026) and issued clinical decision support (CDS) software guidance (January 2026), covering software analyzing signals from fetal heart rate monitors and intrauterine pressure catheters when intended to drive clinical intervention.

In Europe, pregnancy-related devices follow the Medical Device Regulation (MDR, Regulation (EU) 2017/745) and associated designation codes, while conformity routes are shaped by updates to harmonised standards published in the Official Journal of the European Union. In June 2026, the European Commission published Decisions (EU) 2026/1231 and (EU) 2026/1313, updating MDR/IVDR harmonised standards, including updated EN ISO 15223-1 and EN 60601-1, which affects labeling and electrical safety expectations for device makers pursuing presumption of conformity. Parallel policy work continued through the European Commission evaluation of MDR/IVDR (finalized in 2025) and related proposals aimed at reducing burden and addressing device availability constraints, which in turn influences compliance cost and timing for new prenatal monitoring technologies.

Value Chain Analysis

The value chain spans ingredient and component sourcing (vitamin and mineral premixes, gummies excipients, packaging, and for devices, sensors, electronics, and biocompatible polymers), formulation and manufacturing (GMP-driven supplement production and precision and sterile device manufacturing), quality and testing, and regulatory documentation. For medical devices, post-market surveillance obligations and lifecycle quality controls are built into operations, reinforced in Europe through MDR requirements and related guidance such as MDCG 2025-10 on post-market surveillance expectations.

Distribution and activation move through wholesalers, pharmacies and drug stores, online retail and e-pharmacies, and provider channels (OB-GYN clinics and hospitals) that can bundle products into care pathways. Technology partnerships increasingly sit between manufacturing and clinical deployment, linking OEM platforms and AI services in ultrasound and monitoring. GE HealthCare collaborations to add AI ultrasound solutions (Voluson ecosystem) show how software layers, cloud delivery, and clinical workflow integration operate alongside physical device supply. In emerging markets, published supply-chain assessments for maternal health supplies point to bottlenecks including import dependence, limited local manufacturing capacity, and last-mile delivery constraints, which can increase stockout risk for time-sensitive commodities and reduce availability of higher-complexity monitoring solutions outside major urban centers.

Competitive Landscape

The pregnancy products market is moderately fragmented. Prenatal supplements feature low entry barriers, enabling influencer-led start-ups to coexist with healthcare conglomerates. Johnson & Johnson leverages global logistics to keep price points competitive, while newcomers anchor differentiation in clean sourcing and clinically backed claims. FDA scrutiny of label accuracy raises compliance costs, potentially accelerating consolidation as smaller brands struggle to fund testing.

In prenatal monitoring devices, regulatory hurdles concentrate share among technology specialists. GE Healthcare and Bloomlife enjoy first-mover advantages following FDA approvals, whereas smaller entrants seek hospital partnerships to pilot AI algorithms. Venture-capital funds quadrupled maternal-health investments between 2022-2024, aiming to integrate devices, tele-obstetrics, and analytics into cohesive ecosystems.

Quality accreditation and ESG credentials now decide shelf prominence. Brands that publish contaminant assays and measure carbon footprints receive retailer preference and corporate-benefit inclusion. As integrated care bundles that span fertility to postpartum gain traction, market players capable of orchestrating multi-product portfolios stand to outpace single-category specialists, even as new compliance rules tighten the pregnancy products industry.

Pregnancy Products Industry Leaders

Abbott

Clarins Group

Expansxience Laboratories Inc.

Nine Naturals LLC

Noodle & Boo

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Wireless, continuous maternal-fetal monitoring and AI-enabled obstetric decision support create whitespace where clinical staffing constraints and reduced in-person visit models shift care into home and hybrid settings. Evidence in 2026 includes FDA 510(k) clearance for Sibel Healths ANNE maternal wireless monitoring platform (February 2026) and FDA classification activity that formalized prognostic tests for preeclampsia as Class II with special controls (effective June 26, 2026). Together, these steps strengthen commercialization pathways for remote monitoring, complication-risk stratification, and software-enabled interpretation that can be integrated into hospital systems and virtual maternity care.

Payment and program infrastructure also broaden the addressable funnel for pregnancy products beyond retail shelves. Materna Medical obtaining a new ICD-10-PCS procedure code for the Ellora Obstetrical System (effective April 1, 2026) provides a reimbursement anchor for labor-and-delivery technologies, while expansion of employer-funded maternal benefits, including doula support in the United States, supports channels for curated product bundles. These bundles can include supplements, monitoring device rentals, and postpartum recovery kits. Outside the United States, targeted public funding such as the NSW Governments AUD 7.4 million investment (May 2026) in Baymatobs AI-powered maternal-foetal early warning platform highlights active support for scalable digital tools that detect high-impact complications, creating partnership opportunities for device makers, tele-obstetrics platforms, and e-pharmacy distributors seeking clinically validated offerings.

Recent Industry Developments

- June 2026: Pulsenmore announced a strategic partnership with Ouma Health to integrate its FDA-authorized home ultrasound platform into virtual maternity care models in the United States. The partnership links at-home imaging capture with clinical follow-up and care navigation, strengthening the remote prenatal monitoring pathway that supports demand for connected pregnancy devices and services.

- June 2025: Nestle announced womens health as a new growth platform and launched Materna DHA in Asia-Pacific, with expansion into India aligned to local regulations. The rollout expands the prenatal supplementation portfolio across fast-growing markets and reinforces localization and compliant labeling across cross-border products.

- August 2024: Abbott expanded the Pure Bliss by Similac infant formula line with European-made and USDA-certified organic products, including an organic liquid formula positioned for U.S. retail. The update reinforces premiumization and clean-label positioning around maternal and early-life nutrition, influencing adjacent pregnancy-stage purchasing baskets through pharmacy and mass retail channels.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers consumer pregnancy-related products purchased for pre-conception, pregnancy, and post-partum needs, measured in value terms across major regions. The scope reflects products typically sold through pharmacies, supermarkets, specialty stores, and online channels.

Scope exclusions: We exclude clinical service revenues and procedure fees, and we also do not include broader baby care items that are not specifically positioned for pregnancy or post-partum use.

Segmentation Overview

- By Product Type (Value)

- Prenatal Supplements

- Pregnancy Detection Kits

- Stretch-Mark Care Products

- Maternity Wear

- Pregnancy Pillows

- Prenatal Monitoring Devices

- Post-partum Care Products

- By Stage (Value)

- Pre-conception

- Pregnancy

- Post-partum

- By Distribution Channel (Value)

- Supermarkets / Hypermarkets

- Pharmacies & Drug Stores

- Online Retail

- Specialty Stores

- By Geography (Value)

- North America

- United States

- Canada

- Mexico

- Europe

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to lock the market boundary, confirm demand signals, and set realistic assumptions for pricing and channel mix before interviews start. We use public health and demographic statistics, including CDC natality data, WHO and UNICEF maternal health publications, and OECD health indicators, to understand the size and direction of the pregnancy cohort.

On the supply and compliance side, we cross-check relevant labeling and safety guidance from regulators such as the US FDA for supplements and other health products, and we review public customs and trade statistics where applicable. Public company filings and investor presentations help us understand category exposure and channel strategy without relying on private sales logs. We also review patent databases and trusted press coverage to capture product innovation and claims trends that can shift average selling prices and mix. The sources listed above are illustrative, and many other public references were also used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary interviews and surveys were run with product manufacturers, distributors, retail channel specialists, and subject matter experts who track maternal health consumption patterns. Respondent input was used to confirm category splits such as prenatal supplements, pregnancy detection kits, stretch-mark care, maternity wear, and pregnancy pillows, typical price bands, and how online versus offline purchasing is shifting by region. We then rechecked the assumptions across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 15% | APAC: 45% |

| Mid tier: 49% | Functional/Unit leaders: 27% | EMEA: 37% |

| Smaller Players: 19% | Managers: 58% | Americas: 18% |

Market-Sizing & Forecasting

Our core model starts with a top-down demand pool build using pregnancy cohort indicators and category penetration assumptions, which we then map to channel availability by region. Once the addressable pool is set, value is constructed by applying blended pricing logic to each major product bucket, and the totals are aggregated into the global market.

To keep the model practical, we use a short list of repeatable inputs, such as live births and fertility trends, prenatal supplement and test-kit usage rates, the online share shift for pregnancy-related purchases, typical replenishment cycles for supplements, and observed price inflation for personal care and apparel. Where public data gaps exist for smaller countries or niche categories, we apply ratios from similar markets and then adjust them based on expert feedback. The totals are corroborated with selective bottom-up approximations, such as sampled price ranges multiplied by plausible unit volumes and channel checks, so no single assumption dominates the outcome.

For forecasting, we use scenario analysis, supported by consensus views collected in interviews on drivers such as maternal health awareness, premiumization in stretch-mark care, and the pace of e-commerce adoption. These driver paths are applied year by year so the forecast stays explainable and can be updated when a major variable changes.

Data Validation & Update Cycle

Outputs are validated through triangulation across independent signals. We then check variance by region, by product group, and by implied per-pregnancy spend. If a country result is unusually high or low, we revisit driver inputs, recheck pricing and penetration assumptions, and re-contact sources when the variance cannot be explained by demographics or channel structure.

Before sign-off, the model and assumptions go through multiple analyst review steps so calculation errors and scope leakage are caught early. Reports are refreshed annually, and interim updates are triggered when there are material events such as regulatory changes affecting supplements, major channel disruptions, or sharp inflation shifts that move category pricing. Right before delivery, we do a final pass on key inputs so clients receive the most current view possible.

Mordor Intelligence's Pregnancy Products Market Sizing Compared With Other Published Estimates

Published market sizes for pregnancy products can vary widely, even when the topic label sounds the same. Most differences come from how each publisher defines what counts as a pregnancy product, which year is treated as the starting point, and how prices and channel mixes are converted into a single value number.

Key gap drivers are often scope expansion into adjacent baby care, or the opposite choice of counting only topical care and leaving out supplements, detection kits, and maternity wear. Some estimates also treat the market as a broad maternal umbrella and then apply a high-level growth rate, which can inflate the value if per-pregnancy usage rates and channel price mixes are not validated consistently. Currency timing, inflation assumptions, and refresh cadence also matter, since small pricing changes compound quickly in consumer categories.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.67 B (2026) | |

| Global Research Publisher A | USD 34.45 B (2024) | The scope centers on pregnancy care skincare and topical items with a broad end-user framing, and it appears to capture a wider personal care spend pool beyond pregnancy-specific product baskets across stages and channels. |

| Industry Research Publisher B | USD 32.95 B (2024) | The estimate groups pregnancy tests, vitamins, maternity products, and postnatal products under a wide consumer umbrella and uses long-horizon growth assumptions, which can overstate totals when category usage rates and blended pricing by channel are not tightly validated. |

Live-birth and fertility cohort checks, plus category-level usage and price-band validation from interviews, are the evidence that keeps Mordor Intelligence tied to a pregnancy-specific basket instead of a broader maternal spend total. After the included product families are kept consistent and the same demand pool is applied across regions, the remaining spread is mainly explained by how widely other publications group postnatal and general personal care items into the category.

Key Questions Answered in the Report

What is the current value of the pregnancy products market?

The pregnancy products market size stands at USD 2.67 billion in 2026 and is forecast to reach USD 3.49 billion by 2031.

Which product category holds the largest share?

Prenatal supplements lead with 38.88% market share in 2025, reflecting sustained clinical emphasis on nutrient supplementation.

Which region is growing fastest?

Asia-Pacific is projected to post the highest 5.86% CAGR through 2031, driven by expanding healthcare access and rising disposable incomes.

How are digital technologies influencing product demand?

FDA-cleared wireless fetal monitors and AI-enabled wearables allow remote pregnancy management, accelerating premium demand among high-risk pregnancies.

What major restraint could dampen market growth?

Increasing reports of mislabeled prenatal supplements, highlighted by GAO investigations and FDA enforcement, may erode consumer trust and slow adoption.

Why are employers investing in maternal-wellness benefits?

Data from digital health platforms show programs can cut NICU admissions by 40% and lower emergency visits by 33%, translating to significant cost savings for employers.

Page last updated on: