Non-Invasive Prenatal Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

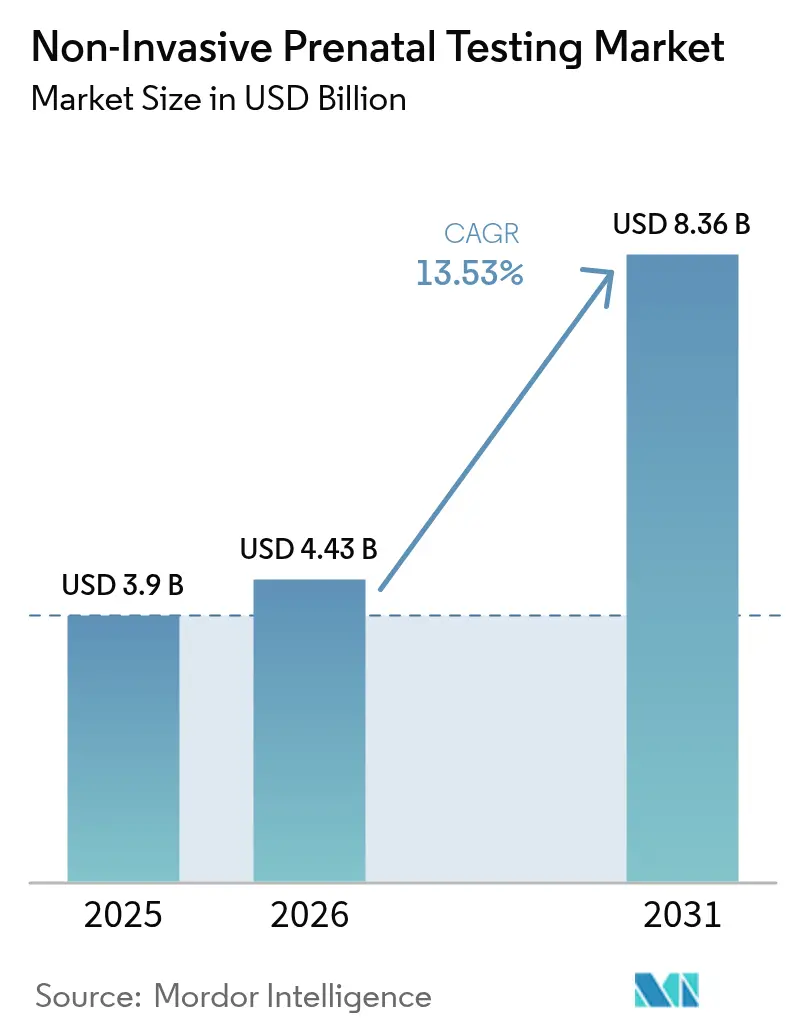

| Market Size (2026) | USD 4.43 Billion |

| Market Size (2031) | USD 8.36 Billion |

| Growth Rate (2026 - 2031) | 13.53% CAGR |

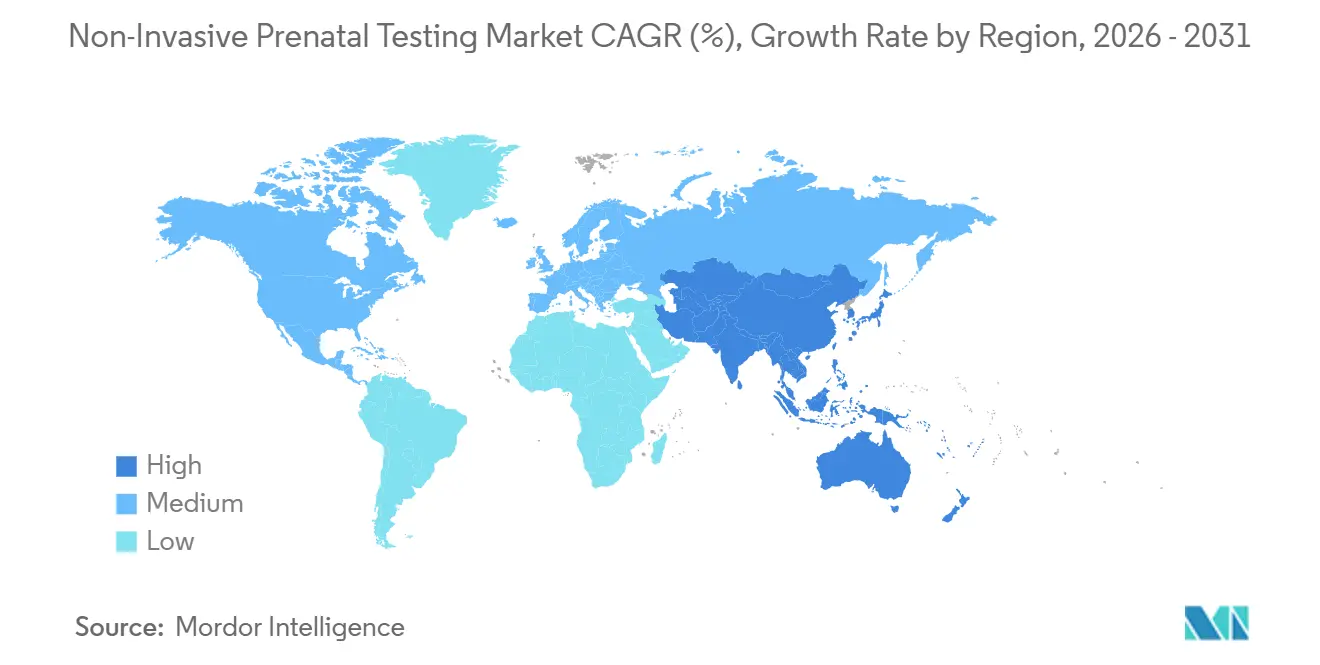

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Non-Invasive Prenatal Testing Market Analysis by Mordor Intelligence

The non-invasive prenatal testing market size is projected to expand from USD 3.9 billion in 2025 and USD 4.43 billion in 2026 to USD 8.36 billion by 2031, registering a 13.53% CAGR over 2026-2031. Sequencing costs falling below USD 200 per sample, universal guideline support, and payer policies that now cover average-risk pregnancies are converting NIPT from a specialist screen into a first-line test in obstetric care. Rising maternal age—births to women aged 35-44 climbed 3.2% in 2024—elevates aneuploidy risk and broadens the eligible population. Technology is also shifting: isothermal rolling-circle amplification (RCA) workflows that avoid thermal cyclers are growing rapidly, lowering capital barriers for smaller laboratories. Competitive dynamics are intensifying as BGI Genomics undercuts Western pricing in Asia-Pacific while Labcorp’s 2024 acquisition of Invitae consolidates U.S. capacity.

Key Report Takeaways

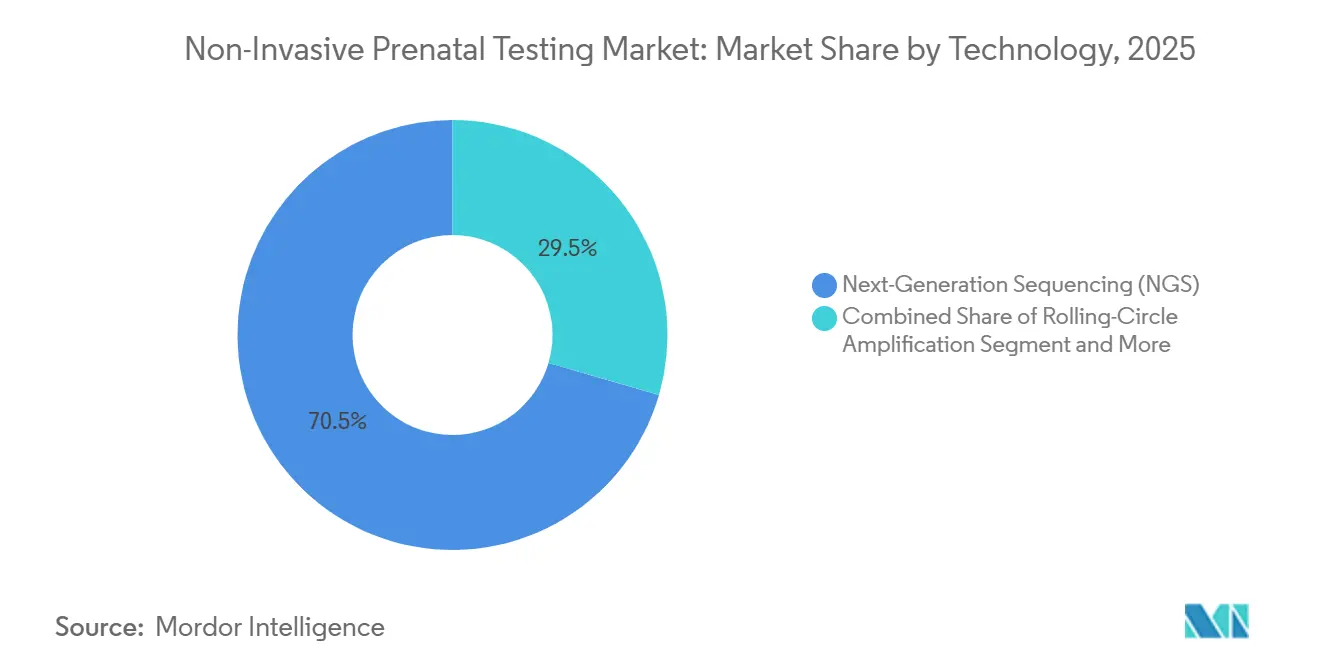

- By technology, next-generation sequencing led with 70.55% of the non-invasive prenatal testing market share in 2025; RCA is projected to expand at an 18.25% CAGR to 2031.

- By test type, aneuploidy screening accounted for 85.53% of the non-invasive prenatal testing market size in 2025, while whole-genome cfDNA screening is advancing at a 19.75% CAGR through 2031.

- By gestation window, the 13-24-week segment captured 50.15% share in 2025; testing at 10-12 weeks is growing at 14.82% CAGR on algorithmic fetal-fraction gains.

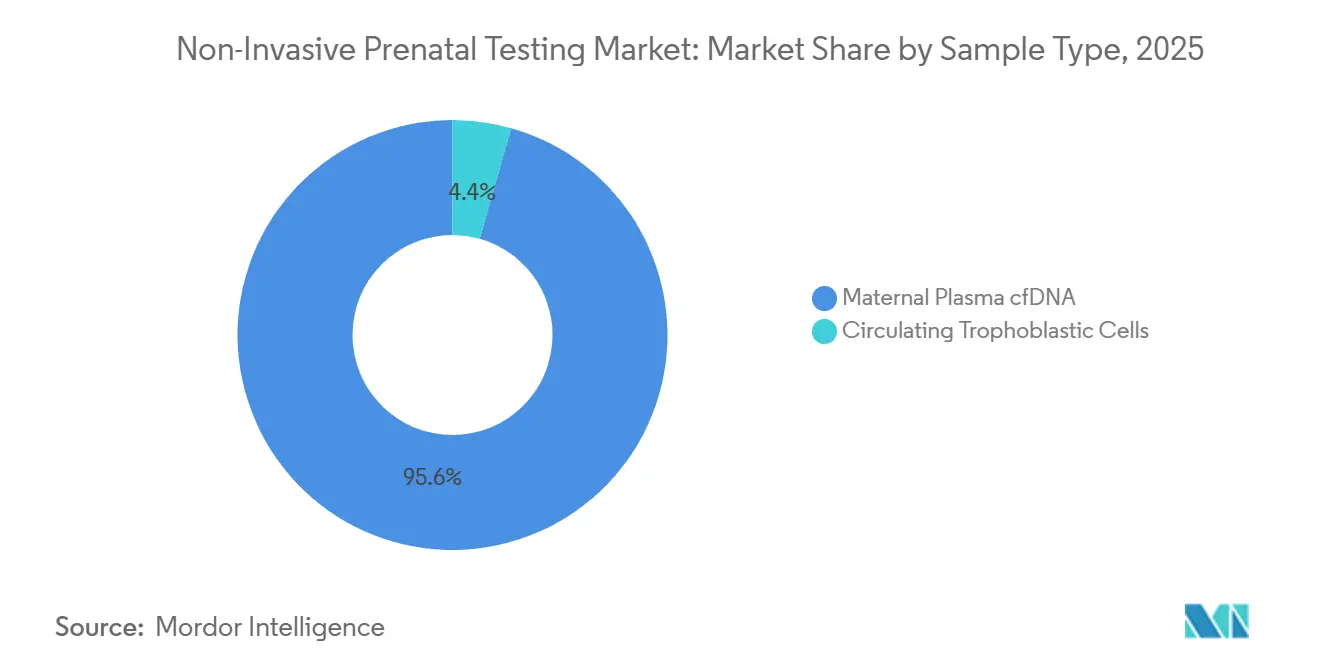

- By sample type, maternal plasma cfDNA dominated with 95.65% share in 2025; circulating trophoblastic cells are forecast to increase at 20.32% CAGR as microfluidics mature.

- By component, services held 62.23% revenue share in 2025, whereas kits & reagents are rising at 16.21% CAGR as hospitals decentralize testing.

- By end user, diagnostic laboratories controlled 58.5% in 2025; IVF & fertility clinics show the fastest 17.42% CAGR due to bundled PGT-A workflows.

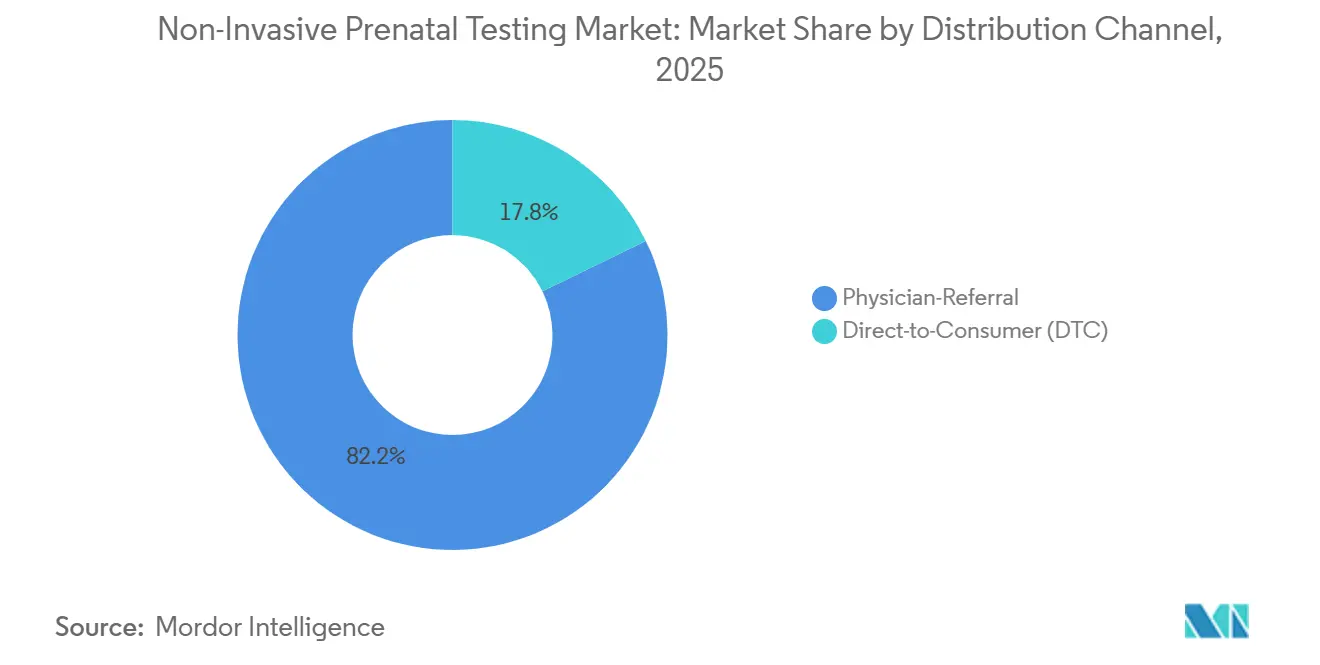

- By distribution channel, physician-referral paths held 82.23% in 2025, yet direct-to-consumer services are expanding at 21.02% CAGR despite stricter FDA oversight.

- By application, Down syndrome detection represented 72.52% revenue in 2025, while Turner syndrome screening is increasing at 15.12% CAGR on improved sex-chromosome calling.

- By geography, North America led with 45.23% share in 2025; Asia-Pacific is the fastest region, growing at 16.42% CAGR on domestic platform approvals and payer adoption.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Non-Invasive Prenatal Testing Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global maternal age elevating aneuploidy risk | +2.8% | Global, with acute concentration in North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Shift from invasive karyotyping to cfDNA screening | +3.1% | Global, led by North America & EU, accelerating in APAC urban centers | Medium term (2-4 years) |

| Sequencing cost curve less than USD 200/sample enabling mass adoption | +2.5% | Global, most pronounced in price-sensitive APAC and Latin America markets | Short term (≤ 2 years) |

| Payer coverage expansion to average-risk pregnancies | +2.2% | North America & EU core, selective adoption in GCC and urban China | Medium term (2-4 years) |

| AI-assisted fetal fraction calling improving first-trimester accuracy | +1.6% | Global, early gains in North America, EU, Australia, South Korea | Medium term (2-4 years) |

| Bundled reproductive-genetic panels (carrier + NIPT) gaining traction | +1.3% | North America, EU, Israel, Singapore; emerging in India, Brazil | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Global Maternal Age Elevating Aneuploidy Risk

Women are delaying childbirth for economic and career reasons, pushing the median maternal age higher in every OECD country. In the United States, the mean age at first birth reached 27.8 years in 2024. Age-linked trisomy incidence drives obstetricians to recommend cfDNA screening universally, especially where public programs subsidize testing for women ≥ 35 years. National registries in Denmark, Japan, and South Korea record parallel shifts, converting high-risk screening into population-level demand. As older mothers often pursue prenatal care earlier and more frequently, laboratories can capture samples sooner, lifting overall test volumes. This demographic trend feeds long-term growth for the non-invasive prenatal testing market by expanding both the eligible base and the clinical urgency for accurate, low-risk diagnostics.

Shift from Invasive Karyotyping to cfDNA Screening

Professional societies now endorse cfDNA as first-line screening, eliminating legacy risk-stratification hurdles. ACOG’s 2024 bulletin recommends cfDNA for all pregnancies, while ACMG’s 2025 statement highlights > 99% detection for trisomy 21 versus 85% for biochemical methods. Payers have followed suit; UnitedHealthcare, Centene, and Medica stopped requiring high-risk justification in 2024-2025, transforming care pathways. Amniocentesis, though still definitive, carries a 0.1-0.3% loss risk that many patients now avoid, further propelling cfDNA volumes. As laboratories retire serum screening platforms, sequencing capacity is redeployed to support expanded panels, reinforcing the migration away from invasive diagnostics and boosting the non-invasive prenatal testing market.

Sequencing Cost Curve Less Than USD 200/Sample Enabling Mass Adoption

High-throughput instruments such as Illumina’s NovaSeq X deliver whole-genome reads at USD 200, down 40% from 2022 levels[1]Illumina Inc., “NovaSeq X Platform Economics,” Illumina, ILLUMINA.COM. Complete Genomics’ DNBSEQ-T7 claims sub-USD 150 costs in 2025, pressuring incumbents on price. Public programs respond: California’s Prenatal Screening Program reimburses NIPT at USD 344, reflecting falling lab expense. Lower input costs let providers offer tests nearer biochemical-screening prices, unlocking adoption in middle-income brackets across China, India, and Brazil. As volume scales, reagent suppliers shift to subscription models, making per-test economics even more favorable and sustaining growth for the non-invasive prenatal testing market.

Payer Coverage Expansion to Average-Risk Pregnancies

Coverage has widened dramatically. UnitedHealthcare’s 2024 policy opened benefits to 2.8 million additional pregnancies each year. Centene mirrored this in 2025, while Medicare’s draft NCD proposes funding for women ≥ 35 years or abnormal ultrasound findings. These decisions erase cost barriers and integrate NIPT into routine prenatal panels. Even where microdeletion panels remain excluded, core aneuploidy screening volumes spike. Commercial labs that once relied on cash-pay patients now secure predictable reimbursement, improving margin stability and reinforcing the expansion trajectory of the non-invasive prenatal testing market.

Restraints Impact Analysis of Non-Invasive Prenatal Testing Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persisting ethical debate on secondary findings & sex selection | -1.2% | Global, most acute in India, China, Middle East; regulatory friction in EU | Long term (≥ 4 years) |

| Bioinformatics talent shortage in emerging markets | -0.9% | APAC (ex-Japan, Australia), Latin America, Middle East & Africa | Medium term (2-4 years) |

| Discordant results in multifetal / IVF pregnancies dampen clinician confidence | -0.7% | Global, concentrated in markets with high IVF utilization (Israel, Spain, Denmark, Japan) | Medium term (2-4 years) |

| Reimbursement push-back on microdeletion add-ons | -1.1% | North America & EU core, selective coverage in private-pay Asia markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persisting Ethical Debate on Secondary Findings & Sex Selection

Incidental maternal findings—such as malignancy signals in cfDNA—raise disclosure dilemmas that require extra counseling time and consent forms. In India, audits uncovered clinics reporting fetal sex in violation of the PCPNDT Act, prompting license suspensions[2]Ministry of Health and Family Welfare India, “PCPNDT Audit 2024,” MOHFW.GOV.IN. China similarly bans non-medical sex reporting. The European Society of Human Genetics now urges explicit pre-test consent for secondary findings. Added administrative overhead can deter providers and delay testing, moderating growth in the non-invasive prenatal testing market.

Bioinformatics Talent Shortage in Emerging Markets

ISCB tallied fewer than 800 clinical-genomics bioinformaticians across India, Brazil, and Southeast Asia in 2024. Limited local expertise forces outsourcing of data analysis, adding up to five days of turnaround and eroding cost advantages. South Africa’s pilot NIPT service experienced 12-week backlogs over software staffing gaps. Although BGI’s training academy graduated 240 analysts in 2024, demand still outstrips supply, capping throughput expansion in several high-growth regions of the non-invasive prenatal testing market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Non-Invasive Prenatal Testing Market Segment Analysis

By Technology:

Isothermal Methods Challenge Sequencing DominanceThe non-invasive prenatal testing market size for technology reached USD 3.9 billion in 2025, with next-generation sequencing accounting for 70.55%. RCA platforms, however, are accelerating at an 18.25% CAGR on simpler, benchtop hardware that slashes capital costs. Clinical Chemistry reported 98.7% concordance between RCA and NGS for trisomy 21 detection, cutting library prep time to 90 minutes. NGS remains entrenched thanks to FDA grandfathering and CE-IVD validation pathways, but small hospitals favor RCA kits that match daily throughput needs.

NGS players continue to enhance throughput; Illumina’s NextSeq 2000 multiple-flow-cell architecture allows labs to batch low-volume runs flexibly, while Thermo Fisher’s Genexus integrates sample-to-report automation. Even so, isothermal vendors appeal to decentralized networks in Latin America and Southeast Asia where power stability and HVAC constraints limit traditional sequencers. Patent disputes between Illumina and Natera over SNP methodologies inject uncertainty, prompting some providers to trial open-filed RCA alternatives. Overall, technology diversification broadens supplier competition and underpins sustained growth for the non-invasive prenatal testing market.

By Test Type:

Genome-Wide Panels Gain GroundIn 2025, aneuploidy panels held 85.53% of the non-invasive prenatal testing market share. Whole-genome cfDNA screening, meanwhile, is growing at 19.75% CAGR as clinicians seek copy-number variant (CNV) insights beyond common trisomies. The Lancet study of 90,000 pregnancies identified clinically significant CNVs in 1.7% of cases missed by standard panels. Despite payer hesitancy, private patients opt for broader coverage, especially in China where domestic kits bundle genome-wide analysis at sub-USD 450 price points.

Microdeletion screening faces reimbursement roadblocks in the United States but gains traction in Germany and Israel for high-risk cohorts. Rh-D genotyping remains a niche, stabilizing revenues in Rhesus-negative populations. Monogenic disorder cfDNA panels are emerging; Natera’s 21-gene Fetal Focus launch in 2026 illustrates a pivot toward single-gene detection without extra blood draws. As validation datasets expand, broader panels could shift payer perspectives, accelerating revenue diversification inside the non-invasive prenatal testing market.

By Gestation Window:

Earlier Testing Reshapes WorkflowsThe non-invasive prenatal testing market size tied to the 13-24-week capturing 50.15%. Algorithms that refine fetal-fraction estimates now support reliable calls as early as 10 weeks, propelling the 10-12-week cohort at a 14.82% CAGR. Obstetrics & Gynecology data show patients tested before 13 weeks are 40% likelier to act on abnormal results within legal termination timelines.

Earlier draws appeal to telehealth prenatal programs, permitting same-day phlebotomy at primary-care clinics. However, strict ultrasound dating requirements in Japan and parts of Europe slow first-trimester uptake. Laboratories mitigate redraw risk through predictive models that flag low expected fetal fraction, scheduling later collections when necessary. Wider first-trimester adoption accelerates turnover and elevates total addressable volume across the non-invasive prenatal testing market.

By Sample Type:

Fetal Cell Isolation EmergesMaternal cfDNA retained 95.65% share in 2025. Yet rare fetal cells, captured via microfluidics, are forecast to rise at 20.32% CAGR. Science Translational Medicine demonstrated 96% karyotype concordance to amniocentesis using DEPArray-isolated cells. Single-cell analysis may solve confined placental mosaicism false positives but currently costs USD 200-300 above cfDNA workflows and lacks FDA clearance.

Vendors target high-risk patients refusing invasive tests; Menarini won CE-IVD in 2024, and Rarecells plans a 2027 launch. Automation and economies of scale are critical to mainstream adoption. If per-test costs fall below USD 400, fetal-cell NIPT could cannibalize cfDNA share, introducing fresh competition inside the non-invasive prenatal testing market.

By Component:

Kits & Reagents Capture Decentralization MomentumServices dominated revenue at 62.23% in 2025, reflecting centralized labs processing > 10,000 monthly samples. Kits & reagents, however, are growing at 16.21% CAGR as hospital-based genomics labs bring testing in-house to cut 3-5-day courier delays. Illumina’s VeriSeq v2 kit lists at USD 350 per sample with embedded DRAGEN analytics, letting mid-volume centers break even at 400 tests per year.

Instrument makers downsize footprints; Thermo Fisher’s Genexus occupies < 2 m², ideal for suburban hospitals. Europe’s IVDR accelerates kit demand by mandating CE-IVD products, disadvantaging home-brew assays. As kit penetration rises, reagent suppliers diversify distribution, bolstering recurring revenue streams for stakeholders in the non-invasive prenatal testing market.

By End User:

IVF Clinics Integrate Genetics Across the Care ContinuumDiagnostic laboratories controlled 58.5% share in 2025, serving obstetric offices through established courier loops. IVF & fertility clinics will outpace at 17.42% CAGR, pairing PGT-A embryo screens with pregnancy NIPT follow-up. A Fertility & Sterility survey showed 62% of IVF patients choose NIPT compared with 34% in natural conceptions. Clinics appreciate integrated results spanning carrier status, embryo genetics, and pregnancy health, reinforcing their role as premium genetic services hubs.

Hospitals retain relevance in markets with bundled maternity packages, yet facility fees make them costlier than freestanding labs. Research institutes focus on expanding test scope to preeclampsia risk and single-gene disorders. The IVF channel’s growth increases sample complexity—multiple gestations, mosaicism—spurring algorithm refinements that benefit the wider non-invasive prenatal testing market.

By Distribution Channel:

Direct-to-Consumer Models Test Regulatory BoundariesPhysician-referral pathways generated 82.23% of 2025 revenue, underlining clinician gatekeeping in most jurisdictions. Direct-to-consumer platforms are set to grow at a 21.02% CAGR. FDA draft guidance requires 510(k) review for at-home kits, pushing players like Everly Health to pause offerings, yet providers that embed telehealth consults continue operating.

Transparent USD 299 price points attract younger pregnant individuals lacking established obstetric care. NSGC’s 2025 poll found 18% of orders initiated without onsite physician visits. Europe bans pure DTC marketing in key countries, while Australia permits it with mandatory counseling. Regulatory clarity will decide whether DTC models remain a niche convenience or evolve into a mainstream conduit for the non-invasive prenatal testing market.

By Application:

Sex-Chromosome Panels Narrow False PositivesDown syndrome commands 72.52% of 2025 revenue thanks to prevalence and strong clinical consensus. Turner syndrome, however, is the fastest-rising application at 15.12% CAGR after algorithmic threshold adjustments halved false positives. UnitedHealthcare now reimburses sex-chromosome aneuploidy panels, broadening payer acceptance beyond trisomies.

Clinicians value comprehensive risk insights but caution that variable phenotypes complicate counseling. Combining cfDNA with first-trimester ultrasound boosts positive predictive value to 78% for monosomy X. As machine-learning-derived risk scores mature, sex-chromosome panels should gather incremental share, diversifying application revenues within the non-invasive prenatal testing market.

Geography Analysis

North America Non-Invasive Prenatal Testing Market

North America led the non-invasive prenatal testing market in 2025 with a 45.23% share, supported by guideline-driven universal screening and payers that removed risk prerequisites. Average negotiated test prices remain high at USD 800-1,200, sustaining healthy margins for U.S. labs. Canada’s funding varies provincially; Ontario covers women ≥ 40 years, while British Columbia relies on private pay, capping national penetration at 35%. Mexico’s private hospitals offer USD 600-800 tests, but public institutions still default to biochemical screening.

APAC Non-Invasive Prenatal Testing Market

Asia-Pacific is the fastest-growing region at 16.42% CAGR. China’s NMPA approvals for BGI and Berry Genomics platforms lifted national test volumes 40% year-over-year. Domestic sequencing economics enable USD 150-300 pricing, expanding access beyond top-tier cities. Japan’s certified facility network increased to 142 in 2025, though cautious counseling slows mass adoption. India’s urban middle class drives volumes at INR 18,000 (USD 215) per test, yet rural cold-chain gaps limit nationwide reach.

Europe, Middle East and LATAM Non-Invasive Prenatal Testing Market

Europe shows mid-single-digit growth influenced by IVDR compliance costs. Germany funds only high-risk cases but covers microdeletions for select patients. The U.K.’s NHS restricts NIPT to women flagged high-risk by first-trimester screens, a targeted policy that still cut amniocentesis 60%. Middle East adoption is led by the UAE, where expatriate populations demand premium prenatal care; Dubai labs report 25% annual growth. Latin America is nascent beyond Brazil, where Dasa launched USD 500 NIPT in 2024.

Regulatory Landscape

In the United States, the FDA classifies NIPT/NIPS as medical devices under the Federal Food, Drug, and Cosmetic Act, and began the first stage of its laboratory-developed test (LDT) phaseout policy in May 2025. This increases pressure on laboratories to align claims, quality systems, and evidence generation with FDA expectations.

In Europe, Regulation (EU) 2017/746 (IVDR) places genetic testing, including NIPT, within a prescriptive conformity-assessment framework involving independent notified bodies and performance evaluation expectations for genetic diagnostics. Several national programs also add operational controls: Norway reported 36 private enterprises approved to offer NIPT for trisomy 13, 18, and 21 across 54 locations as of March 2025, the Netherlands adjusted licensing requirements within its national prenatal screening framework in mid-2025, and Japan continues to manage access via its Prenatal Testing Certification System Operation Committee, with accredited medical and analytical institutions listed as of March 2026.

Competitive Landscape

Market concentration is moderate: the top five suppliers hold a significant share of global revenue, leaving room for regional challengers. Labcorp’s 2024 Invitae acquisition merged 1.2 million annual tests into a 2,000-site network, consolidating U.S. capacity. BGI Genomics enjoys 40% gross margins by controlling sequencers, reagents, and software, undercutting Western pricing across APAC[3]BGI Genomics, “Annual Report 2024,” BGI.COM. Natera differentiates through SNP-based analytics claiming 99.9% trisomy 21 sensitivity, though patent litigation with Illumina continues to shape technology choice.

Emerging entrants pursue fetal-cell isolation to solve placental mosaicism false positives; Menarini’s DEPArray earned CE-IVD in 2024. Oxford Nanopore pilots same-day NIPT on portable sequencers, courting point-of-care scenarios. Strategic moves include Cooper Surgical’s EMR integration with Illumina, streamlining ordering in IVF clinics. As payer scrutiny intensifies, labs emphasize reporting quality and genetic-counselor access to defend premium pricing in the non-invasive prenatal testing market.

Non-Invasive Prenatal Testing Industry Leaders

Centogene NV

F. Hoffmann-La Roche Ltd.

Eurofins Scientific SE

Revvity, Inc.

BGI Genomics Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Non-Invasive Prenatal Testing Market Companies Covered in this Report

- Agilent Technologies

- Berry Genomics

- BGI Genomics Co. Ltd

- Centogene

- Eurofins

- F. Hoffmann-La Roche Ltd (Ariosa)

- Fulgent Genetics Inc.

- Genetron Health

- Illumina

- Invitae

- Laboratory Corp of America Holdings (Labcorp)

- MedGenome Labs

- Myriad Women's Health Inc.

- Natera

- QIAGEN

- Ravgen Inc.

- Revvity, Inc.

- Thermo Fisher Scientific

Market Opportunities and Future Outlook

Clinical and commercial whitespace is widening beyond common aneuploidy screening into diagnostic-adjacent pathways and hard-to-call populations. Single-gene and low-fetal-fraction performance are central focus areas: Natera launched its 21-gene Fetal Focus single-gene NIPT in January 2026, and in May 2026 announced an enhanced Panorama NIPT powered by SNP-informed deep sequencing that reported a 0.5% no-call rate in low fetal-fraction samples. The company also advanced the EXPAND prospective, blinded study beyond 2,000 enrolled patients. These launches support broader first-trimester use where redraws and no-calls have been operational barriers, and they create room for differentiated pricing and contracting tied to fewer repeat draws and clearer workflows for IVF and higher-BMI cohorts.

A second opportunity track is non-invasive confirmation of high-risk screens, designed to reduce reliance on invasive procedures while maintaining confidence in positive calls. In May 2026, BillionToOne launched Unity Confirm, positioned as a fetal cell-based confirmation test for high-risk NIPT results, with validation prepared for presentation at ACOG 2026, targeting the gap between screening and amniocentesis follow-up. At the same time, intellectual property disputes are shaping partnering and build-versus-buy decisions, including Illumina initiating patent litigation against BillionToOne in May 2026. The dispute underscores the premium placed on defensible workflows, including SNP-informed methods, fetal-cell approaches, and emerging multiomic or single-cell directions described in recent scientific literature, and it tends to favor suppliers with strong validation packages and scalable bioinformatics.

Recent Industry Developments in Non-Invasive Prenatal Testing Market

- July 2026: Illumina filed patent litigation against BillionToOne in the United States and Europe, signaling a intensification of competitive dynamics around SNP-informed and cell-based NIPT workflows. The action foregrounds defensible testing architectures and could influence partnerships, licensing, and go-to-market strategies across high-risk NIPT segments.

- May 2026: BillionToOne launched Unity Confirm, a fetal cell-based confirmation test for high-risk NIPT results, with validation prepared for presentation at ACOG 2026. This expansion tightens follow-up testing options and emphasizes non-invasive confirmation in complex screening pathways.

- May 2026: Natera announced an enhanced Panorama NIPT powered by SNP-informed deep sequencing, reporting a 0.5% no-call rate in low fetal-fraction samples and progress from the EXPAND study with over 2,000 enrolled patients. The upgrade sharpens early-gestation testing and reduces redraw requirements, influencing payer discussions and lab throughput.

Non-Invasive Prenatal Testing Market Report Scope and Research Methodology

Market Definition and Coverage

This market is counted as revenues generated from non-invasive prenatal testing during pregnancy, using maternal blood (cell-free DNA and related workflows) to screen for fetal chromosomal and select genetic conditions across laboratory and clinical settings.

Scope exclusions: invasive diagnostic procedures (such as amniocentesis and CVS) and routine pregnancy imaging or biochemical tests that are not part of NIPT are excluded.

Segments Covered in This Report

- By Technology

- Next-Generation Sequencing (NGS)

- Rolling-Circle Amplification

- Microarray

- Real-Time PCR

- Other Technologies

- By Test Type

- Aneuploidy Screening

- Microdeletion / Microduplication Screening

- Whole-Genome cfDNA Screening

- Rh-D Genotyping

- Monogenic Disease Testing

- By Gestation Window

- 10 - 12 Weeks

- 13 - 24 Weeks

- > 24 Weeks

- By Sample Type

- Maternal Plasma cfDNA

- Circulating Trophoblastic Cells

- By Component

- Instruments

- Kits & Reagents

- Services

- By End User

- Hospitals & Birthing Centers

- Diagnostic Laboratories

- IVF & Fertility Clinics

- Research Institutes

- By Distribution Channel

- Physician-Referral

- Direct-to-Consumer (DTC)

- By Application

- Down Syndrome (Trisomy 21)

- Edwards Syndrome (Trisomy 18)

- Patau Syndrome (Trisomy 13)

- Turner Syndrome

- Other Chromosomal Abnormalities

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to frame the demand pool and practical pricing bands before the model was built. We referenced public health and statistics sources such as US CDC natality and maternal age data, OECD health statistics, WHO maternal and newborn health indicators, and national health ministry publications where birth volumes and screening recommendations are summarized.

To link clinical adoption with commercial activity, we also reviewed sources including peer-reviewed obstetrics and genetics journals, guidelines published by professional medical societies, and customs or trade statistics where relevant for diagnostics equipment and reagents. Company filings, investor presentations, and reputable press were used to cross check test menu expansion, lab capacity, and reimbursement changes. Where needed, paid subscriptions were used to confirm product timing and technology focus from company financials and patent databases. The desk sources mentioned here are illustrative, and additional public documents were used for collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on speaking with people who see ordering behavior and testing volumes directly, such as diagnostic lab leaders, hospital and clinic decision makers, and maternal fetal medicine professionals, along with a few distribution and reimbursement-informed roles. Since this is a global market, inputs were balanced across mature and emerging geographies so assumptions on uptake, pricing, and test mix could be checked and then adjusted where needed.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 29% | CXOs: 13% | APAC: 43% |

| Mid tier: 57% | Functional/Unit leaders: 43% | EMEA: 36% |

| Smaller Players: 14% | Managers: 44% | Americas: 21% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where live births and the maternal age mix are translated into an addressable pregnancy cohort, then filtered by NIPT penetration by region and risk category before volumes are priced. To keep the totals realistic, results are corroborated with selective bottom-up checks, including sampled test volume by channel, lab throughput discussions, and a simple ASP times volume sense check for high adopting countries.

Key inputs used in the model include annual birth counts, the share of pregnancies in advanced maternal age brackets, guideline-driven screening eligibility, payer coverage trends, the test menu mix (aneuploidy screening versus microdeletions and other add-ons), and average selling prices by channel (physician referral versus direct-to-consumer). When a country level data point was missing, gaps were filled using peer-country proxies based on births, income level, and known reimbursement strictness, then validated through interviews.

Forecasting uses scenario analysis supported by exponential smoothing on historical adoption signals, with adjustments for sequencing cost trends and expected policy changes that experts flagged. The final growth path is constrained by what labs can operationally deliver, which is why capacity and turnaround time expectations are used as guardrails.

Data Validation & Update Cycle

Validation is done through multiple passes where modeled revenues are compared against independent signals, including total testing volumes implied by penetration rates, pricing bands seen in the market, and expected utilization by the trimester window. When large variances show up, assumptions are revisited and, where needed, experts are re-contacted to confirm whether the change reflects timing, currency, or reporting mix.

Before sign-off, the work is reviewed by another analyst to check calculations, definitions, and whether any part of the model double counts services, kits, or instrument revenues. Reports are refreshed annually, and interim updates are made when material events occur, such as major reimbursement moves, guideline updates, or technology shifts. Right before delivery, a final pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Non Invasive Prenatal Testing Market Size Compared With Other Published Estimates

Published values for non-invasive prenatal testing often vary because not everyone counts the same revenue streams or uses the same starting year, and growth rates are anchored to different clinical adoption assumptions. Differences also come from how pricing is handled, especially when test menus expand and when currency conversion is done at different time points.

The biggest spread usually shows up when one estimate bundles broader genetic testing revenues, or when instruments and services are added on top of test kits without checking for overlap, then a high penetration rate is applied across all pregnancies. Another frequent driver is the base case choice, where some figures lean aggressive on direct-to-consumer uptake or assume faster reimbursement expansion, while the approach here ties volumes to births, trimester timing, and guideline-backed ordering patterns, which is why the 2025 value is kept at USD 3.90 B (2025) for Mordor Intelligence.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 3.90 B (2025) | |

| Global Consultancy A | USD 4.59 B (2024) | Uses a different base year and mixes forecast windows, and its scope commonly includes a wider methodology and product basket, which can pull adjacent prenatal and genetic testing revenues into the total. |

| Industry Publisher B | USD 7.18 B (2025) | Leans on a broader component roll-up where services and instruments can be counted alongside test revenues with limited de-duplication, and assumes faster ASP and penetration progression across regions. |

The table shows that most of the gap can be traced to scope bundling and how pricing and penetration are stepped forward year to year. By keeping the demand pool tied to births, applying region-specific uptake checks, and separating components to avoid double counting, the estimate stays more repeatable when assumptions are updated and re-validated.

Key Questions Answered in the Report

How quickly is the non-invasive prenatal testing market expected to grow through 2031?

Revenue is forecast to rise from USD 4.43 billion in 2026 to USD 8.36 billion by 2031, advancing at a 13.53% CAGR.

Which technology is gaining momentum against next-generation sequencing?

Rolling-circle amplification is the fastest-growing method, expanding at an 18.25% CAGR due to its isothermal workflow and lower capital costs.

Why is Asia-Pacific the fastest regional market?

Domestic platform approvals, sub-USD 300 pricing, and rising maternal age push Asia-Pacific volumes at a 16.42% CAGR.

What is driving early-gestation testing demand?

AI-enhanced fetal-fraction algorithms reduce first-trimester no-call rates, enabling accurate results from 10 weeks gestation.

How are IVF clinics influencing test adoption?

Bundled embryo screening and pregnancy NIPT packages boost uptake, making IVF centers the fastest-growing end-user category at 17.42% CAGR.

Page last updated on: