Preterm Birth And PROM Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

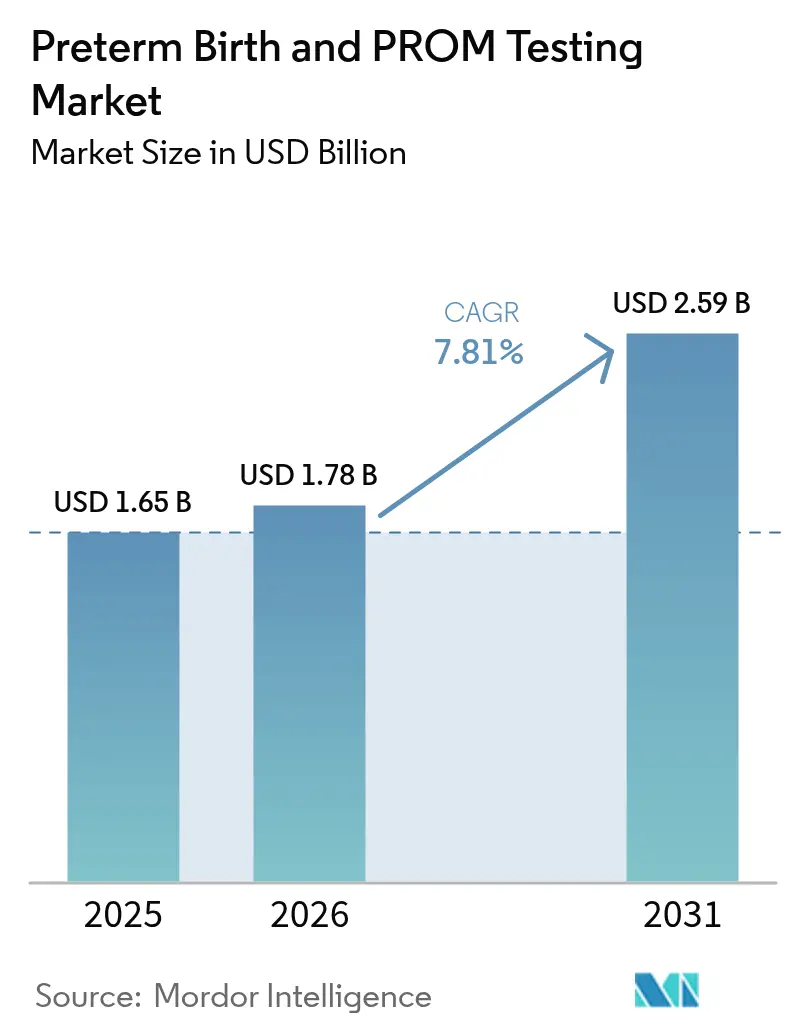

| Market Size (2026) | USD 1.78 Billion |

| Market Size (2031) | USD 2.59 Billion |

| Growth Rate (2026 - 2031) | 7.81% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Preterm Birth And PROM Testing Market Analysis by Mordor Intelligence

The preterm birth and PROM testing market size is expected to grow from USD 1.65 billion in 2025 to USD 1.78 billion in 2026 and is forecast to reach USD 2.59 billion by 2031 at 7.81% CAGR over 2026-2031. Rising global preterm birth rates, significant neonatal mortality, and mounting economic burdens on health systems keep demand for accurate, early-stage diagnostics strong. Rapid progress in biomarker validation, especially cell-free RNA signatures that predict risk up to four months before delivery, accelerates the shift from reactive to predictive maternal care[1]European Society of Human Genetics, “Cell-Free RNA Predicts Preterm Birth,” eshg.org. Point-of-care platforms still dominate clinical workflows, yet centralized laboratories are gaining traction through broader test menus and higher analytical sensitivity. Regionally, North America leads on the back of robust reimbursement, while Asia-Pacific contributes the fastest revenue growth as prenatal screening programs scale. Regulatory tightening around laboratory-developed tests pressures smaller firms but simultaneously opens consolidation avenues for large diagnostics groups.

Key Report Takeaways

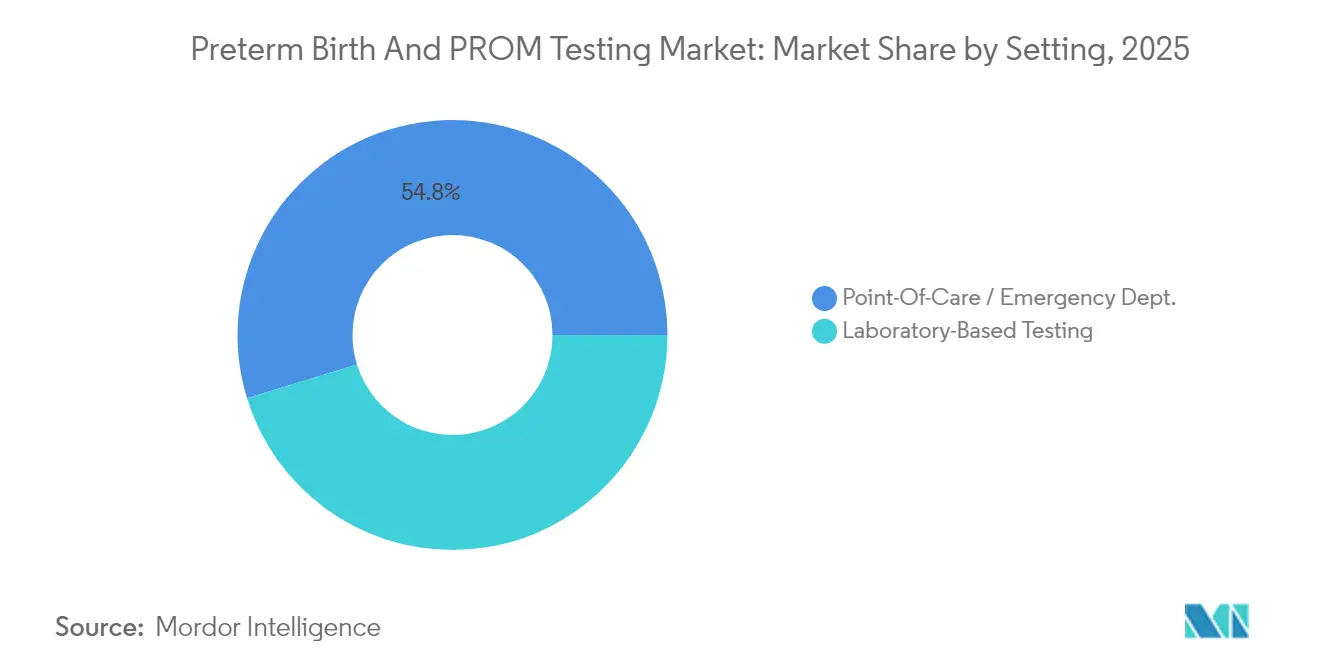

- By test setting, point-of-care diagnostics captured 54.76% of the preterm birth and PROM testing market share in 2025; laboratory-based testing is projected to expand at an 10.98% CAGR through 2031.

- By biomarker category, fetal fibronectin held 41.88% of the preterm birth and PROM testing market share in 2025, while placental alpha-microglobulin-1 is rising at a 10.07% CAGR through 2031.

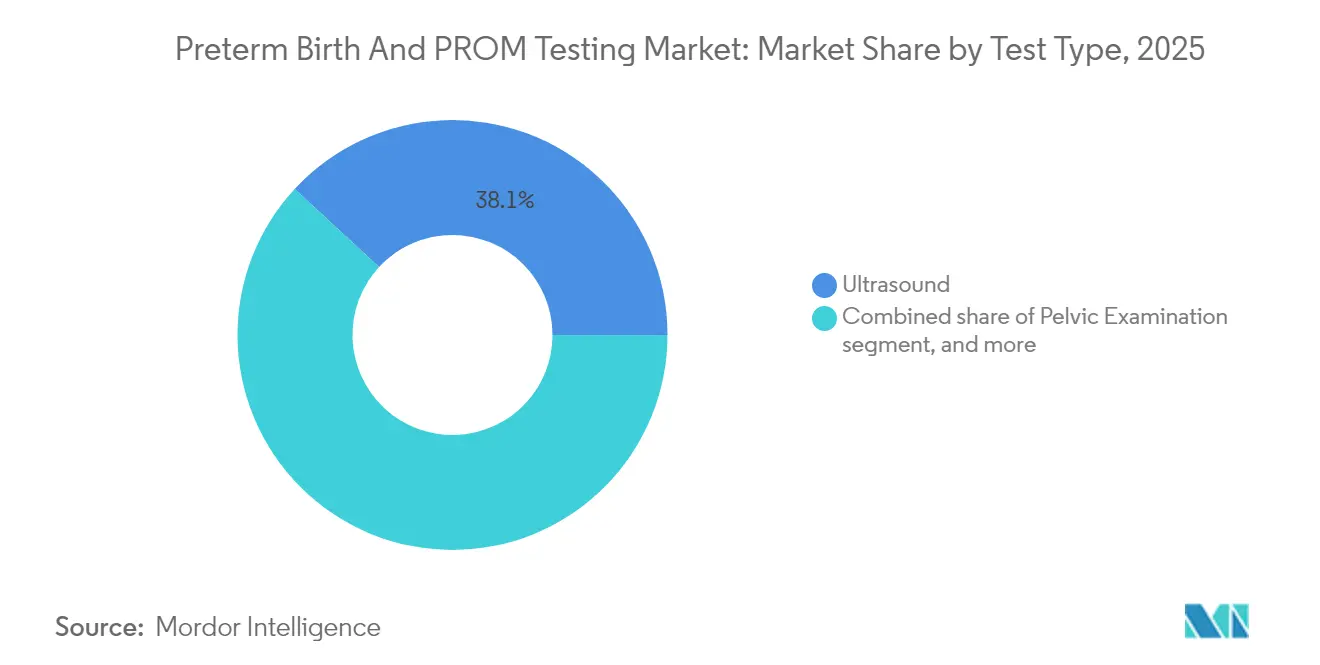

- By test type, ultrasound accounted for 38.12% of the preterm birth and PROM testing market size in 2025; biochemical markers are growing at 9.96% CAGR between 2026-2031.

- By end user, hospitals and maternity centers controlled 60.55% revenue in 2025; home-based care and remote monitoring show the highest projected CAGR at 10.92% through 2031.

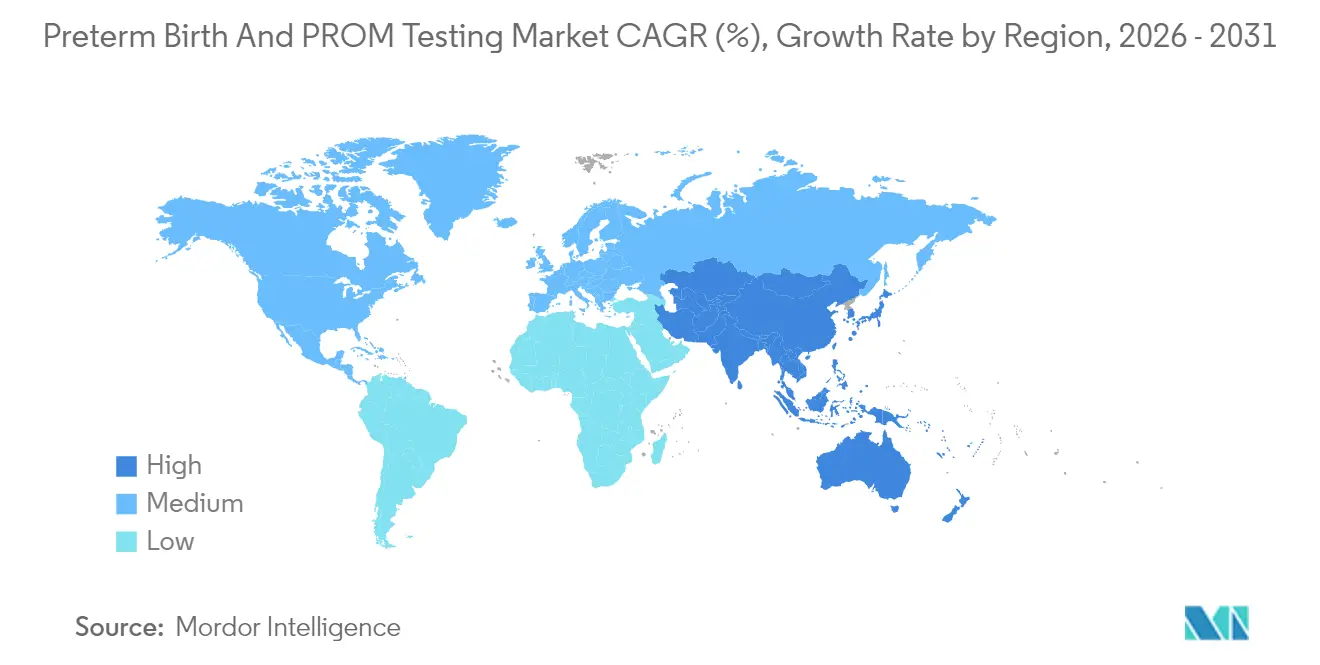

- By geography, North America led with 42.76% revenue share in 2025, whereas Asia-Pacific is forecast to advance at a 9.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Preterm Birth And PROM Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global preterm birth incidence | +2.1% | Sub-Saharan Africa, South Asia, global spillover | Long term (≥ 4 years) |

| Technological advancements in point-of-care diagnostics | +1.8% | North America, Europe, expanding to Asia-Pacific | Medium term (2-4 years) |

| Expansion of prenatal screening programs | +1.5% | Asia-Pacific core, Latin America spillover | Medium term (2-4 years) |

| Increasing healthcare expenditure on maternal care | +1.2% | Global, led by developed markets | Long term (≥ 4 years) |

| Favorable reimbursement and regulatory support | +0.9% | North America, European Union | Short term (≤ 2 years) |

| Growing adoption of telehealth and home testing | +0.8% | Global, pronounced in rural areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Global Preterm Birth Incidence

Annual preterm births already exceed 15 million and continue climbing despite medical advances. Asia accounts for more than half of those births, intensifying diagnostic demand in high-population regions[2]Constance Agius, “Preterm Birth in Asia,” Frontiers in Pediatrics, frontiersin.org. Preterm complications cost the United States health system over USD 25 billion each year, spurring payer investment in early detection technologies that reduce neonatal intensive care stays[3]National Conference of State Legislatures, “Preterm Birth Costs,” ncsl.org. Reduction of neonatal mortality has become a central performance metric in national maternal-child health plans, ensuring that budget allocations favor evidence-based diagnostic tools. Advanced maternal age, increasingly common in developed economies, raises baseline risk and keeps demand elevated over the long term.

Technological Advancements in Point-of-Care Diagnostics

Hand-held and bedside analyzers now deliver results within minutes, eliminating laboratory delays during acute obstetric evaluations. Quantitative ultrasound that maps cervical microstructure predicts preterm risk as early as week 23, a notable improvement over history-based assessments. Wearable sensors capturing heart-rate variability supply real-time data feeds that machine-learning models convert into 82% accurate risk scores. Combining artificial intelligence with established biomarkers increases diagnostic specificity while minimizing false positives. Such converged platforms strengthen the role of point-of-care testing within the preterm birth and PROM testing market.

Expansion of Prenatal Screening Programs

Government-funded screening drives steady test adoption in India, Indonesia, and Brazil, where maternal mortality targets align with WHO guidance for comprehensive antenatal care. Cost-efficient assays such as salivary progesterone kits widen rural access. Telehealth portals further extend reach, improving appointment adherence and sample-return rates across dispersed geographies. Standardized national protocols lower per-test costs and stabilize procurement pipelines, benefiting diagnostics vendors with scalable production.

Increasing Healthcare Expenditure on Maternal Care

Hospitalization costs for preterm infants have tripled in economies like South Korea, pushing health systems to prioritize prevention. Clinical studies report an 18% decline in severe neonatal morbidity after integrating maternal biomarker testing into care pathways. Payers favor combined cervical-length measurement and fetal fibronectin testing because the protocol reduces perinatal death by up to 15% while cutting overall costs by 31%. Value-based reimbursement models therefore reinforce spending on early diagnostics within the preterm birth and PROM testing market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited accessibility in low-resource settings | −1.4% | Sub-Saharan Africa, rural Asia, Latin America | Long term (≥ 4 years) |

| High cost of advanced diagnostic tests | −1.1% | Global, strongest in emerging markets | Medium term (2-4 years) |

| Stringent regulatory approval processes | −0.8% | Global, heightened in North America and Europe | Medium term (2-4 years) |

| Competition from alternative monitoring modalities | −0.6% | Global, greater in technologically advanced markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Accessibility in Low-Resource Settings

Diagnostics uptake lags in regions with fragile health infrastructure where preterm birth rates are highest. Shortages of trained personnel and laboratory equipment restrict biomarker testing coverage[4]Journal of Global Health, “Diagnostics Access in Low-Resource Settings,” jogh.org. The cessation of fetal fibronectin supply in remote Australian clinics forced costly patient transfers and highlighted supply chain fragility. Persistent digital divides hamper telehealth solutions, and cold-chain requirements add logistical hurdles. These systemic barriers slow penetration of the preterm birth and PROM testing market in underserved regions.

High Cost of Advanced Diagnostic Tests

Premium assays priced at several hundred USD remain out of reach for many patients because private insurers often exclude preventive maternity testing. Direct-to-consumer models widen access but primarily serve affluent groups. Heightened FDA oversight of laboratory-developed tests raises compliance costs, which manufacturers pass on through higher list prices. Capital outlays for point-of-care devices further deter adoption by smaller clinics in cost-sensitive markets. Unless price and reimbursement hurdles ease, test volumes in the preterm birth and PROM testing market will remain uneven.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Test Type: Ultrasound Dominance Drives Current Practice

Ultrasound retained a 38.12% revenue share in 2025, securing its place as the primary modality for cervical-length assessment and fetal surveillance. Quantitative ultrasound now detects microstructural cervical changes that forecast preterm birth risk several weeks earlier than legacy imaging approaches. Biochemical markers, accounting for a smaller 2025 base, exhibit the fastest 9.96% CAGR as clinicians seek objective molecular readouts that complement imaging. Pelvic examination and uterine monitoring continue to serve supportive roles but lack the predictive power of combined biomarker panels. Emerging digital biomarkers and AI-powered analytics promise integrated solutions, signaling longer-term evolution of the preterm birth and PROM testing market.

The widening preference for multimodal assessment underscores a shift toward comprehensive risk profiling. Ultrafast imaging plus biomarker quantification delivers actionable probabilities that drive early interventions such as antenatal steroids. Remote ultrasound systems linked to specialist review extend capability to community settings, while disposable biochemical cartridges simplify bedside workflows. These converging trends strengthen future demand within the preterm birth and PROM testing market size for hybrid platforms that merge imaging with molecular diagnostics.

By Biomarker Category: PAMG-1 Challenges fFN Supremacy

Fetal fibronectin (fFN) commands 41.88% share and remains clinically entrenched due to robust guideline support. Negative fFN results give clinicians 96% confidence that delivery will not occur within two weeks, allowing safe discharge and cost avoidance. Placental alpha-microglobulin-1 (PAMG-1) is growing at a 10.07% CAGR and demonstrates superior predictive performance for delivery within seven days. IGFBP-1 gains traction in low-resource environments because it delivers 91% sensitivity and 82.6% specificity using minimally invasive collection. Cytokines and cell-free RNA represent frontier categories undergoing clinical validation.

Competitive dynamics within the biomarker space are intensifying as novel targets enter multi-analyte panels. Assay developers emphasize high positive predictive value to minimize unnecessary interventions. Laboratories leverage digital PCR for quantitative reads that refine cutoffs and stratify risk tiers, thereby expanding the preterm birth and PROM testing market size for advanced biomarker panels.

By Setting: Laboratory Precision Gains on Point-of-Care Convenience

Point-of-care and emergency settings held 54.76% share in 2025, reflecting the urgency of decision-making when preterm labor is suspected. Ten-minute fFN assays guide steroid administration and maternal transfer within critical windows. Laboratory testing, projected at 10.98% CAGR, benefits from multiplex panels, digital PCR, and next-generation sequencing that outperform single-marker bedside kits. Centralized laboratories can run multi-omics panels that point-of-care systems cannot yet support.

Regulatory focus on laboratory-developed tests reshapes competitive positions. Large reference laboratories absorb compliance overhead and gain volume, whereas smaller point-of-care vendors face higher relative costs. Over time, hybrid care pathways are likely to prevail, with rapid triage tests at the bedside followed by confirmatory lab panels, expanding utilization across both settings in the preterm birth and PROM testing market.

By End User: Home Care Disrupts Hospital-Centric Models

Hospitals and maternity centers accounted for 60.55% revenue in 2025, underscoring their role in complex risk management and emergent care. Maternal-fetal medicine units routinely adopt multi-marker panels alongside imaging. However, home-based care shows 10.92% CAGR as telehealth reimbursement accelerates remote monitoring. Consumer-initiated tests such as Sera Prognostics’ PreTRM enable women to obtain blood draws locally and receive personalized risk scores online. Wearable sensors integrated with cloud analytics add continuous surveillance without clinic visits.

Diagnostic companies adapt by packaging kits suitable for nurse-home visits, by forging alliances with mail-in laboratories, and by embedding apps that couple results with virtual consultations. Ambulatory birth centers bridge hospital and home settings, purchasing mid-cost analyzers that complement basic imaging. These distributed models enlarge patient reach, reinforcing momentum within the preterm birth and PROM testing market.

Geography Analysis

North America held 42.76% of 2025 revenue due to near-universal insurance coverage for key biomarker assays, including new CPT payment for at-home fetal monitoring that removed a traditional access barrier. The United States leads global direct-to-consumer uptake, reflecting strong digital health maturity and patient engagement. Canada’s single-payer system funds national screening programs, ensuring consistent demand. Mexico’s public-private partnerships extend testing to rural areas, though logistic bottlenecks remain. While urban centers showcase high penetration, Indigenous and remote communities still report lower utilization, indicating pockets of unmet need within the preterm birth and PROM testing market.

Asia-Pacific is the fastest-growing region at 9.28% CAGR through 2031. China channels substantial public funds into maternal-child health and conducts cohort studies across 60 neonatal intensive care units that help validate diagnostics. India’s private providers integrate cost-efficient assays into large antenatal camps, while policy reforms aim to lower out-of-pocket costs. Japan and South Korea drive premium-segment demand for high-sensitivity biomarker panels, supported by advanced hospital networks. Australia’s supply disruptions underscore ongoing infrastructure challenges that vendors must address to capture rural opportunities. Diverse income profiles in the region create segmented pricing strategies across the preterm birth and PROM testing market.

Europe maintains steady expansion on the strength of harmonized clinical guidelines and stable reimbursement. NICE recommendations standardize biomarker use across the United Kingdom, which speeds hospital adoption. Germany and France allocate public budgets for preventive screening, integrating tests into bundled antenatal packages. Italy and Spain deploy point-of-care kits in midwife-led clinics to reduce referral delays. Regulatory clarity encourages innovation, though value assessments remain stringent. Meanwhile, Middle East & Africa and South America register rising attention from multilateral aid programs. Limited infrastructure slows immediate growth, yet unmet clinical need remains pronounced, signaling longer-term upside for the preterm birth and PROM testing market.

Competitive Landscape

Competitive intensity is moderate. Hologic retains a stronghold with its fFN assay, leveraging decades of data and wide regulatory clearance. Abbott and Qiagen offer broad prenatal menus, integrating preterm birth risk with infectious disease and genetic screening to deepen accounts. Reference laboratories such as Labcorp and Quest Diagnostics bundle biomarker panels with non-invasive prenatal testing, capturing share across provider networks.

Regulatory tightening by the FDA favors well-capitalized firms that can manage new compliance layers. Emerging players like Sera Prognostics disrupt through direct-to-consumer channels that bypass traditional referral chains, stimulating price transparency and patient empowerment. Technology convergence expands the field: Mirvie’s RNA platform predicts preterm birth months ahead and has attracted venture funding for commercialization. Device innovators such as Novocuff raise capital for mechanical prevention solutions that complement biomarker diagnostics.

Strategic collaborations intensify. Roche partners with hospital networks to deploy multi-analyte maternal health panels, while Nuvo aligns with Sheba Medical Center to integrate AI-based remote monitoring. Acquisition pipelines remain active as larger groups seek proprietary markers and digital health assets to reinforce ecosystem offerings within the preterm birth and PROM testing market. The overall landscape favors companies that can present robust real-world evidence of outcome improvement and budget impact to payers.

Preterm Birth And PROM Testing Industry Leaders

Hologic, Inc.

Abbott

QIAGEN

Sera Prognostics

CooperSurgical

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Roche received FDA 510(k) clearance for the Elecsys sFlt-1/PlGF ratio test for preeclampsia risk assessment.

- February 2025: Sheba Medical Center partnered with Nuvo to deploy AI maternity monitoring that enhances preterm birth prediction.

- June 2021: Nuvo Group received the United States Food and Drug Administration approval for the expanded utility of its INVU, a prescription-initiated remote pregnancy monitoring platform to add a new uterine activity module that enables remote monitoring of uterine activity.

- October 2024: Sera Prognostics expanded direct-to-consumer access for the PreTRM blood test.

- September 2024: Qiagen unveiled more than 100 new assays for its QIAcuity digital PCR platform, including maternal health applications.

- July 2024: Novocuff secured USD 26 million to develop a preterm birth prevention device.

Global Preterm Birth And PROM Testing Market Report Scope

As per the scope of the report, preterm birth is the birth of the baby before completion of the 37 weeks. Preterm babies are prone to various medical complications and have weakened immunity. PROM testing is a type of test that detects the premature rupturing of the fetal membranes. The Global Preterm Birth and PROM Testing Market is segmented by test type (Pelvic exam, Ultrasound, Biochemical Markers, Uterine Monitoring, and Others) and geography (North America, Europe, Asia-Pacific, Middle East, and Africa, South America). The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD million) for the above segments.

| Pelvic Examination |

| Ultrasound |

| Biochemical Markers |

| Uterine Monitoring |

| Other Test Types |

| Fetal Fibronectin (fFN) |

| Placental Alpha-Microglobulin-1 (PAMG-1) |

| Insulin-Like Growth Factor-Binding Protein-1 (IGFBP-1) |

| Interleukins & Other Cytokines |

| Laboratory-Based Testing |

| Point-Of-Care / Emergency Dept. |

| Hospitals & Maternity Centers |

| Diagnostic Laboratories |

| Ambulatory & Freestanding Birth Centers |

| Home-Care & Remote Monitoring |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Test Type | Pelvic Examination | |

| Ultrasound | ||

| Biochemical Markers | ||

| Uterine Monitoring | ||

| Other Test Types | ||

| By Biomarker Category | Fetal Fibronectin (fFN) | |

| Placental Alpha-Microglobulin-1 (PAMG-1) | ||

| Insulin-Like Growth Factor-Binding Protein-1 (IGFBP-1) | ||

| Interleukins & Other Cytokines | ||

| By Setting | Laboratory-Based Testing | |

| Point-Of-Care / Emergency Dept. | ||

| By End User | Hospitals & Maternity Centers | |

| Diagnostic Laboratories | ||

| Ambulatory & Freestanding Birth Centers | ||

| Home-Care & Remote Monitoring | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the preterm birth and PROM testing market?

The market stands at USD 1.78 billion in 2026.

How fast is the market expected to grow?

The market is forecast to increase at an 7.81% CAGR, reaching USD 2.59 billion by 2031.

Which test setting holds the largest revenue share?

Point-of-care diagnostics captured 54.76% of market revenue in 2025.

Which biomarker is growing the fastest?

Placental alpha-microglobulin-1 leads growth with a 10.07% CAGR through 2031.

Which region shows the highest growth rate?

Asia-Pacific posts the fastest regional CAGR at 9.28% between 2026-2031.

What factor contributes most to market expansion?

Rising global preterm birth incidence adds an estimated +2.1% to the overall CAGR forecast.

Page last updated on: