Precision Resistor Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

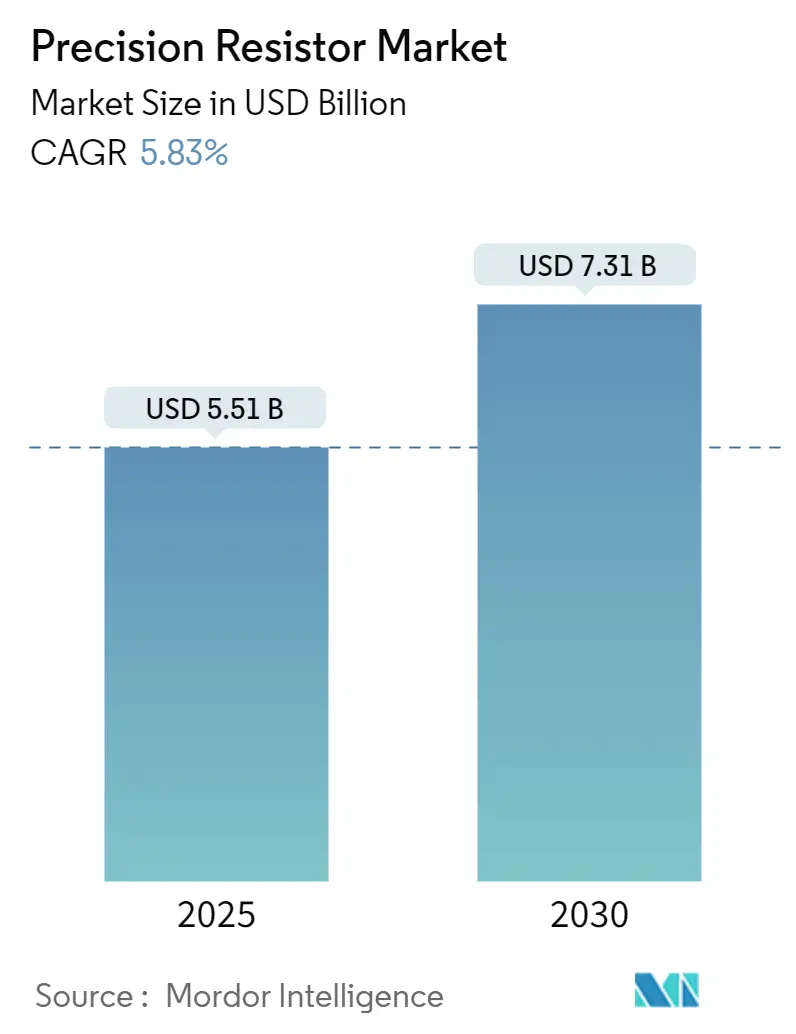

| Market Size (2025) | USD 5.51 Billion |

| Market Size (2030) | USD 7.31 Billion |

| Growth Rate (2025 - 2030) | 5.83% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Precision Resistor Market Analysis by Mordor Intelligence

The precision resistor market size stands at USD 5.51 billion in 2025 and is projected to reach USD 7.31 billion by 2030, growing at a 5.83% CAGR. Robust demand for ultra-low-TCR components in 5G base-station calibration, electric-vehicle battery-management, quantum-computing cryogenic hardware and high-resolution medical imaging is accelerating design-in cycles for ever-smaller form factors and tighter tolerance bands. Manufacturers that master metal-foil, thin-film and bulk-metal foil processes are finding new revenue streams in current-sense shunts for bidirectional converters, while regulatory upgrades under IEC 60115-4 are pushing industrial automation users toward premium-grade, long-life parts. Supply-side attention on ruthenium and nickel-chromium feedstock security and on miniaturisation beyond 0402M packages is reshaping capital-spending priorities, especially across Asia-Pacific fabs.

Key Report Takeaways

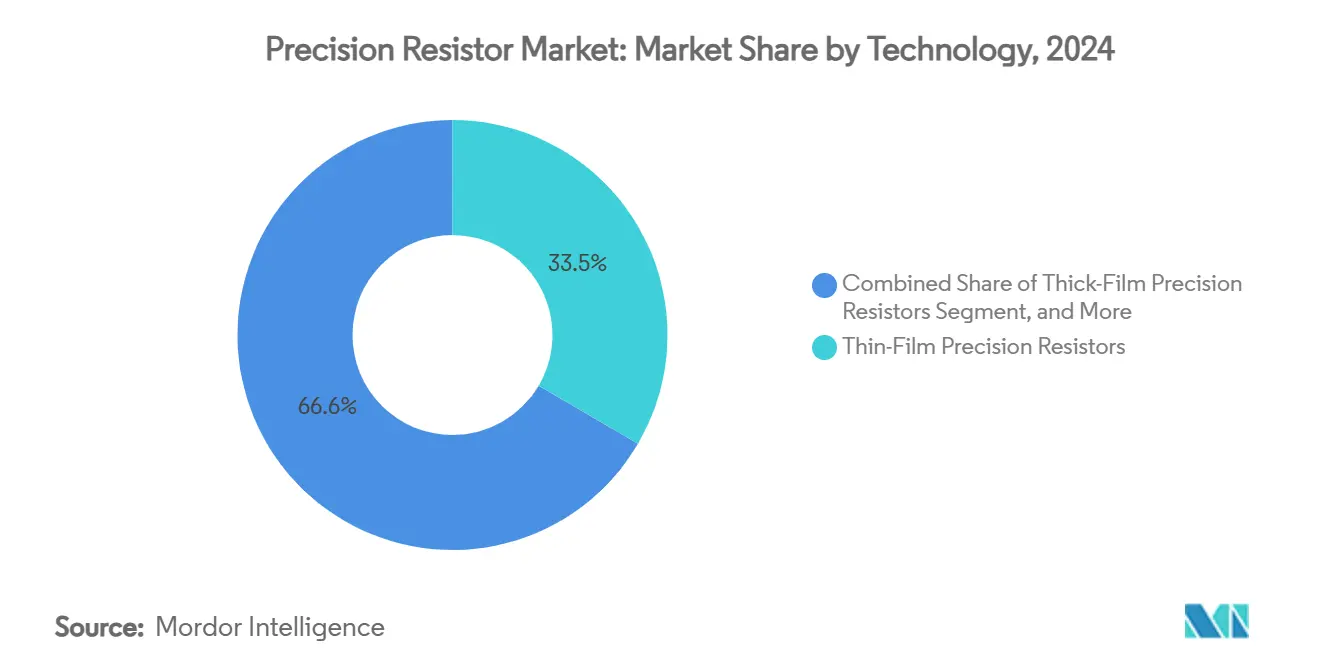

- By technology, thin-film captured 33.45% of the precision resistor market share in 2024 while metal-foil is forecast to expand at 6.45% CAGR to 2030.

- By mounting configuration, surface-mount chip packages commanded 45.21% of the precision resistor market size in 2024 and are on track for a 7.02% CAGR through 2030.

- By resistance range, the 1 Ω–100 Ω band accounted for 37.50% of the precision resistor market size in 2024 and is expected to post a 6.34% CAGR to 2030.

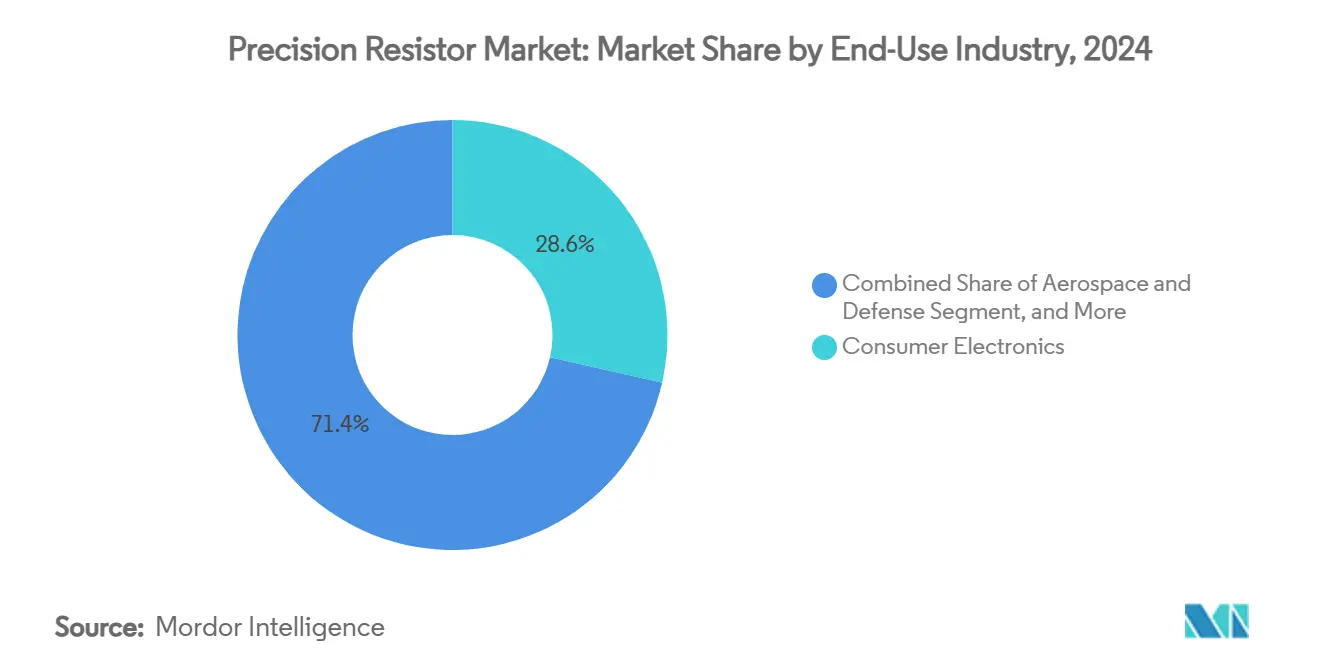

- By end-use industry, consumer electronics led with 28.56% of the precision resistor market share in 2024 while automotive electronics and xEV segments record the fastest 6.30% CAGR through 2030.

- By application, current-sensing represented 33.90% of the precision resistor market size in 2024 and is projected at a 6.54% CAGR to 2030.

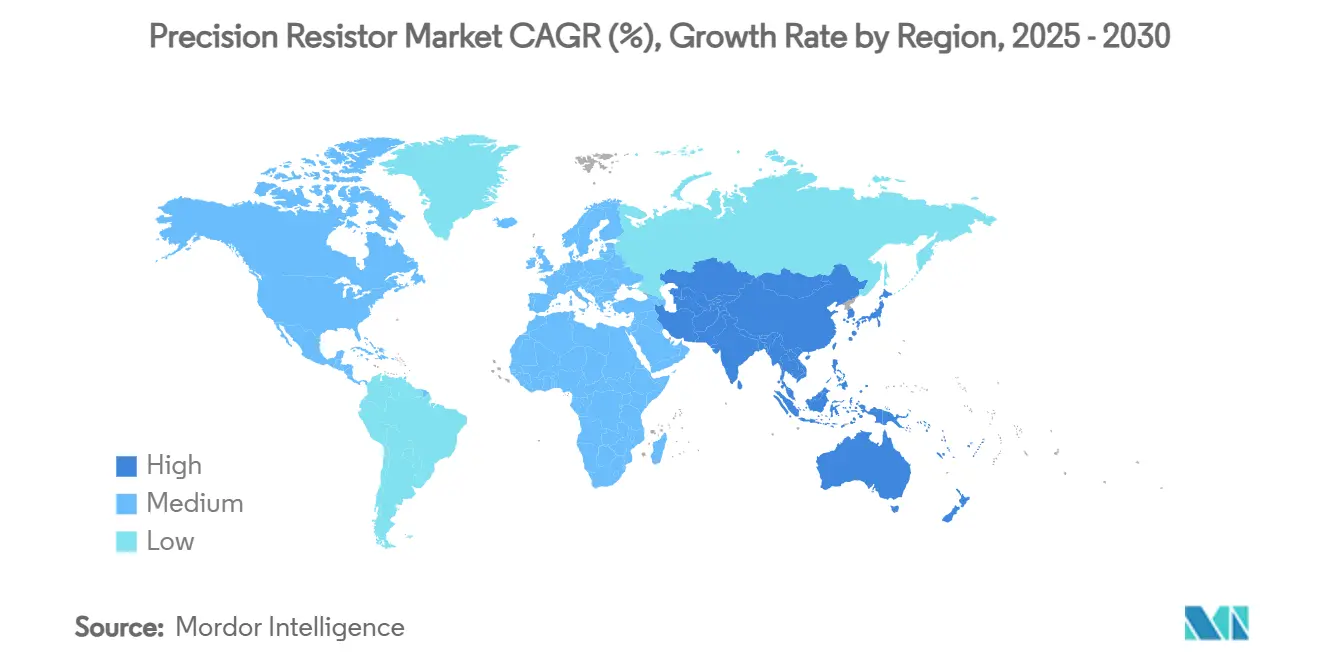

- By geography, Asia-Pacific controlled 47.00% of the precision resistor market size in 2024 and is expanding at a 6.98% CAGR toward 2030

Global Precision Resistor Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Advanced T&M equipment in 5G and semiconductor fabs | +1.2% | APAC, North America | Medium term (2–4 years) |

| EV battery-management demand for ultra-low-TCR shunts | +0.9% | China, Europe, North America | Medium term (2–4 years) |

| Growth in medical imaging and diagnostics electronics | +0.7% | North America, Europe | Long term (≥ 4 years) |

| Surge in current-sense designs for high-efficiency power conversion | +0.8% | Global | Short term (≤ 2 years) |

| Quantum-computing cryogenic hardware | +0.3% | North America, Europe | Long term (≥ 4 years) |

| Stricter IEC 60115-4 reliability upgrades | +0.4% | Global | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Proliferation of advanced T&M equipment in 5G and semiconductor fabs

Massive 5G rollout plans require calibration benches that hold sub-ppm drift across wide temperature swings, amplifying demand for bulk-metal foil parts that deliver 0.14 ppm/°C stability.[1]Alpha Electronics, “Bulk Metal Foil Resistor Technology,” alpha-elec.co.jpWafer-level cryogenic probes running at 4.4 K in superconducting device lines push the same precision requirements into semiconductor fabs, linking orders for sub-Ω reference resistors directly to planned capacity adds. Glass-based passives under semi-additive patterning for mmWave modules add another pull by enforcing low insertion-loss targets. As telcos accelerate millimetre-wave coverage, procurement teams bind resistor life-cycle commitments to infrastructure schedules, locking in multi-year supply contracts. Consequently, the precision resistor market is deeply aligned with the cadence of 5G macro-cell deployments.

Rising EV battery-management demand for ultra-low-TCR shunt resistors

Active cell-balancing topologies in 400 V and 800 V packs need 0.1% accuracy shunts that remain within tolerance from –40 °C to +85 °C, elevating thin-film and metal-strip designs. Online electrochemical impedance spectroscopy requires micro-ohm stability to protect signal-to-noise ratios, increasing design wins for ±5 ppm/°C products. Patent filings for next-generation BMS architectures peaked in 2020 and stayed buoyant through 2024, signalling sustained OEM investment. Commercial-vehicle migration to higher voltages raises insulation-monitoring accuracy thresholds, widening the addressable market for precision shunts. As global EV output climbs, the precision resistor market integrates tightly with battery pack volume forecasts.

Growth in medical imaging and diagnostics electronics

Sub-millivolt fidelity in MRI receiver chains relies on resistors that toggle between superconducting and dissipative states within 12 µs without excess noise spikes.[2]I. Saniour et al., “Cryogen-Free Cryostat for RF Coils,” epjti.epj.org RTD-based temperature-measurement boards targeting 0.1 °C accuracy lean on matched resistor networks with 0.05% tracking tolerance. Cryogenic broadband power sensors that certify microwave-power delivery down to 0.1 dB uncertainty further reinforce demand for low-drift precision references. Portable imaging and point-of-care devices need tight thermal monitoring across 285–310 K to guarantee patient safety. These evolving specifications sustain a high-value niche inside the precision resistor market.

Surge in current-sense designs for high-efficiency power conversion

Four-terminal Kelvin shunts with less than or equals to 100 mV drops are now standard in high-density buck regulators and DC energy meters. IEC 62053-41 drafts for DC metering accuracy accelerate design refresh cycles in EV chargers and microgrids. Buck topologies that replace linear regulators lower thermal budgets, amplifying interest in sub-mΩ resistors that combine low power loss with tight tolerance. Smart-grid rollouts call for decade-long drift stability, shifting procurement policies towards premium resistor classes. These shifts translate into multi-segment pull for the precision resistor market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Commodity-level price pressure on thin/thick-film devices | -0.8% | APAC | Short term (≤ 2 years) |

| Supply-chain volatility for Ru and NiCr thin-film feedstocks | -0.6% | APAC | Medium term (2–4 years) |

| EMI and excess-noise limits curbing metal-film use in RF designs | -0.4% | Global | Medium term (2–4 years) |

| On-chip resistor integration inside ASICs | -0.5% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Commodity-level price pressure on thin/thick-film devices

Smartphone slowdown in 2024–2025 left a glut of standard 0603 and 0402 chips, forcing ASP erosion for mainstream thin-film lines. Distributors in Asia pivoted to direct-to-factory models, compressing margins across the mid-tier. RoHS-driven material substitutions raised process costs and introduced performance variability, squeezing profit pools further. Automotive and PC segments cushioned the blow, yet handset-centric volumes still dictate price floors. As a result, oversupply risk tempers near-term revenue forecasts in the precision resistor market.

Supply-chain volatility for Ru and NiCr thin-film feedstocks

Ruthenium and nickel-chromium sputtering targets source heavily from politically sensitive regions, exposing fabs to freight and export-control shocks. Taiwan-centric manufacturing further concentrates risk along the South China Sea corridor. U.S. policy reviews of critical materials spotlight platinum-group metals, hinting at future strategic stockpile moves that could distort pricing. Ru interconnect adoption at advanced semiconductor nodes intensifies competition for the same element, pitting resistor makers against foundries for supply. These uncertainties restrain gross-margin outlooks within the precision resistor market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Thin-Film Dominance Drives Innovation

Thin-film devices held 33.45% of the precision resistor market share in 2024 thanks to ±10 ppm/°C stability and small-geometry scalability, translating into USD 1.87 billion of the precision resistor market size that year. Metal-foil variants, though representing a smaller base, are set for the fastest 6.45% CAGR through 2030 because aerospace, quantum and metrology users specify drift below 2 ppm per year. Thick-film continues to satisfy smartphone and IoT cost targets, but margin headroom narrows as substrate and paste costs fluctuate. Wire-wound remains indispensable in ≥ 5 W power stages that must absorb surge energy without hot-spotting. Over the forecast, hybrid substrates that embed thin-film arrays next to bulk-metal shunts illustrate the co-existence of technologies rather than outright displacement.

Acceleration in zero-ohm jumpers and micro-ohm shunts further diversifies the technology stack. Vendors now offer 0.2 mΩ parts rated for 100 A pulses, embedding four-terminal layouts inside strip packages. Simultaneously, IC-processed RC arrays unlock sub-0.05% matching in compact footprints, aiding high-speed ADC front-ends. Collectively, these advances sharpen the competitive contours of the precision resistor market.

By Mounting Configuration: Surface-Mount Miniaturisation Accelerates

Surface-mount dominated with 45.21% of the precision resistor market size in 2024, equal to USD 2.53 billion, and is projected to deliver a 7.02% CAGR through 2030. Transition beyond 0402M toward 03015M packages yields a 44% footprint reduction and 58% mass savings, spurring investments in high-resolution pick-and-place optics. Tape-and-reel tolerance, solder-fillet geometry, and overmoulding parameters all enter tighter control windows as component height plunges below 0.15 mm.

Through-hole axial and radial parts persist in railway, defence, and heavy-machinery retrofits where vibration isolation and thermal inertia trump board density. Precision resistor networks in SOIC or QSOP casings serve op-amp gain-setting tasks that need ratiometric accuracy across temperature sweeps. Kelvin-sense shunts tailored for BMS boards couple low inductance with four-terminal pads, expanding value-added opportunities for suppliers willing to machine copper-manganin sandwich constructions. This blend of shrinking chips and specialised legacy formats underscores the versatility of the precision resistor market.

By Resistance Range: Mid-Range Values Lead Applications

The 1 Ω–100 Ω band generated 37.50% of the precision resistor market size in 2024, mirroring the current-sense sweet spot for DC-link monitoring in motor drives and EV packs. Below 0.1 Ω, metal-strip shunts with copper-manganin terminations manage thermal gradients while offering 1 W–15 W ratings that prevent hot-spot failures in 800 V architectures. The 0.1 Ω–1 Ω slice supports power-conversion feedback loops where voltage drop must remain under 100 mV.

Higher-value networks between 100 Ω and 10 kΩ populate voltage-divider ladders and sensor bias circuits, while ultra-high-resistance devices beyond 10 MΩ now headline quantum-grade metrology thanks to Peta-Ohm SiC structures. Alloy choice shifts across this spectrum, moving from Cu-Ni blends for low ohms to NiCrAl for mid-range and SiCrN for ≥ 1 MΩ films. These material permutations illustrate how resistance value segmentation maps directly onto the diversified demand profile in the precision resistor market.

By End-Use Industry: Consumer Electronics Leads Amid Automotive Upswing

Consumer electronics retained 28.56% of the precision resistor market share in 2024 as smartphones, wearables and tablets adopted tighter quiescent-current budgets. Yet the automotive and xEV category is advancing at a 6.30% CAGR through 2030, buoyed by global mandates on electrification and by the proliferation of advanced driver-assistance systems that crave accurate current diagnostics. Test-and-measurement boxes for 5G frequencies create premium pull for sub-ppm devices, reinforcing revenue diversification.

Industrial automation customers rush to upgrade legacy PLC cards to comply with IEC 60115-4, which elevates fault-tolerance thresholds. Medical imaging OEMs pursue ±0.01% tolerance sets to refine SNR in superconducting coils, whereas aerospace and defence segments adopt MIL-PRF-55342-class parts with failure rates below 0.01 %/1,000 h. Telecommunications infrastructure and grid-edge devices round out the matrix, showing that the precision resistor market spans mass-consumer to mission-critical verticals without dependency on a single sector.

By Application: Current-Sensing Dominates Precision Requirements

Current-sensing captured 33.90% of the precision resistor market size in 2024, energised by BMS designs, DC-link monitors, and smart-meter installations. Integrated shunt-plus-amplifier ICs such as INA260 reduce board area and measurement error, but still hinge on ultra-stable resistive elements. Calibration equipment and metrology labs represent a high-margin subset, relying on calculable resistance standards with negligible AC-DC differences up to 2 MHz.

Voltage-division permanently underpins sensor excitation in industrial control, while temperature-compensation networks require precision packs to offset drift in gain-critical locales. Feedback loops inside servo drives and RF power amplifiers depend on low-TC matched arrays that preserve phase margin over time. Altogether, these sockets ensure recurring design cycles and establish a resilient floor for the precision resistor market.

Geography Analysis

Asia-Pacific controlled 47.00% of the precision resistor market size in 2024, boosted by Taiwan’s manufacturing cluster, where YAGEO alone generates 30% of global resistor output.[3]YAGEO Group, “Corporate Presentation Q2 2023,” yageo.com The region pairs proximity to smartphone and EV assembly hubs with mature substrate supply chains, creating structural cost advantages. Yet rising geopolitical tension along crucial sea lanes injects freight-delay risk and encourages OEMs to dual-source thin-film feedstocks outside the immediate zone.

North America maintains leadership in quantum computing, defence, and medical imaging niches that justify premium unit pricing. Vishay Intertechnology posted USD 715.2 million revenue in Q1 2025 and signalled improving order momentum via a 1.08 book-to-bill ratio despite restructuring moves.[4]Vishay Intertechnology, “Q1 2025 Results,” stocktitan.net Federal incentives for domestic semiconductor expansion also lift demand for sub-ppm calibration standards in wafer fabs and metrology labs.

Europe’s automotive supply chain centres on Germany and France, where stringent functional-safety norms spur adoption of AEC-Q200-graded resistors. Industrial automation revamps under IEC 60115-4 deepen replacement cycles for through-hole wire-wound parts. Regional emphasis on renewable-energy integration extends opportunities in smart-grid monitoring, adding another tailwind to the precision resistor market across the continent.

Competitive Landscape

The precision resistor market hosts a moderately concentrated field. Vishay Intertechnology, YAGEO Group, and KOA Corporation apply decades of thin-film deposition know-how, multi-continent fabs, and expansive patent portfolios to secure key sockets. Vishay’s 2024 restructuring closed three sites to streamline the Vishay 3.0 strategy while preserving investment capacity for high-value foil lines. YAGEO’s tender for Shibaura positions the firm to blend NTC thermistor capability with its existing chip-resistor breadth, improving cross-selling leverage across automotive and industrial channels.

KOA Corporation courts EV and industrial players via metal-plate shunts and high-temperature thick-film parts, focusing on long-term drift specs under AEC-Q200. Specialists such as EBG Elektronische Bauelemente break through with ±5 ppm ultra-high-precision resistors targeting smart-grid inverters. Arrow Electronics’ alliance with Ohmite redistributes power-resistor channels worldwide, signalling fresh distributor-manufacturer dynamics.

White-space growth emerges in cryogenic quantum hardware, edge-AI inference boards, and zero-ohm jumpers for high-power rail interconnects. Vendors that co-design with silicon-carbide MOSFET module makers, or align with supply-chain de-risking programs, will likely secure next-generation volume. Continuous material science progress, notably in Ru alternatives, remains the chief differentiator that can reorder the hierarchy within the precision resistor market.

Precision Resistor Industry Leaders

Vishay Intertechnology

YAGEO Group

KOA Corporation

Viking Tech Corp.

Panasonic Industry Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: YAGEO Corporation increased its tender offer for Shibaura Electronics to 6,200 JPY per share to strengthen its NTC thermistor portfolio.

- May 2025: Vishay Intertechnology reported Q1 2025 revenues of USD 715.2 million and a 1.08 book-to-bill ratio.

- April 2025: Arrow Electronics formed a worldwide distribution pact with Ohmite Manufacturing to broaden power-resistor reach.

- March 2025: IEC published the IEC 60115-4:2022 fixed power resistor update.

Global Precision Resistor Market Report Scope

| Thin-Film Precision Resistors |

| Thick-Film Precision Resistors |

| Metal-Foil / Bulk-Metal Foil Resistors |

| Wire-Wound Precision Resistors |

| Metal-Film Precision Resistors |

| Current-Sense Shunts |

| Surface-Mount Chip (0201-2512) |

| Through-Hole Axial and Radial |

| Precision Resistor Networks / Arrays |

| Kelvin-sense Four-Terminal Packages |

| less than or equals to 0.1 Ω |

| 0.1 Ω – 1 Ω |

| 1 Ω – 100 Ω |

| 100 Ω – 10 kΩ |

| above 10 kΩ |

| Test and Measurement Instruments |

| Industrial Automation and Controls |

| Automotive Electronics and xEV |

| Medical Devices and Life-Science Equipment |

| Aerospace and Defense |

| Telecommunications Infrastructure |

| Consumer Electronics |

| Energy and Power Management |

| Other End-user Industries |

| Current-Sensing / Shunt |

| Precision Measurement and Calibration |

| Voltage Division and Reference |

| Temperature Compensation Networks |

| Feedback and Control Loops |

| Other Applications |

| North America |

| South America |

| Europe |

| Asia-Pacific |

| Middle East and Africa |

| By Technology | Thin-Film Precision Resistors |

| Thick-Film Precision Resistors | |

| Metal-Foil / Bulk-Metal Foil Resistors | |

| Wire-Wound Precision Resistors | |

| Metal-Film Precision Resistors | |

| Current-Sense Shunts | |

| By Mounting Configuration | Surface-Mount Chip (0201-2512) |

| Through-Hole Axial and Radial | |

| Precision Resistor Networks / Arrays | |

| Kelvin-sense Four-Terminal Packages | |

| By Resistance Range | less than or equals to 0.1 Ω |

| 0.1 Ω – 1 Ω | |

| 1 Ω – 100 Ω | |

| 100 Ω – 10 kΩ | |

| above 10 kΩ | |

| By End-Use Industry | Test and Measurement Instruments |

| Industrial Automation and Controls | |

| Automotive Electronics and xEV | |

| Medical Devices and Life-Science Equipment | |

| Aerospace and Defense | |

| Telecommunications Infrastructure | |

| Consumer Electronics | |

| Energy and Power Management | |

| Other End-user Industries | |

| By Application | Current-Sensing / Shunt |

| Precision Measurement and Calibration | |

| Voltage Division and Reference | |

| Temperature Compensation Networks | |

| Feedback and Control Loops | |

| Other Applications | |

| By Geography | North America |

| South America | |

| Europe | |

| Asia-Pacific | |

| Middle East and Africa |

Key Questions Answered in the Report

Which technology segment is expanding fastest?

Metal-foil precision resistors are forecast to post the highest 6.45% CAGR through 2030, driven by sub-ppm stability needs in metrology, aerospace and quantum-computing.

Why is Asia-Pacific so dominant in supply and demand?

The region hosts large-scale fabs, dense electronics assembly clusters and strategic sourcing of substrate materials, giving it 47% market share and the highest 6.98% regional growth rate.

What role do precision resistors play in electric vehicles?

They enable 0.1%-accuracy current sensing for cell balancing and insulation monitoring in 400 V and 800 V battery packs, ensuring safety and extending battery life.

How are new IEC standards affecting purchasing decisions?

The IEC 60115-4:2022 update tightens stability and flammability tests, prompting industrial users to upgrade to higher-reliability resistor classes, thereby lifting premium-grade demand.

Are supply-chain risks significant for resistor makers?

Yes, reliance on ruthenium and nickel-chromium thin-film feedstocks sourced from geopolitically sensitive regions introduces cost volatility and potential shortages.

Page last updated on: