Resistive RAM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

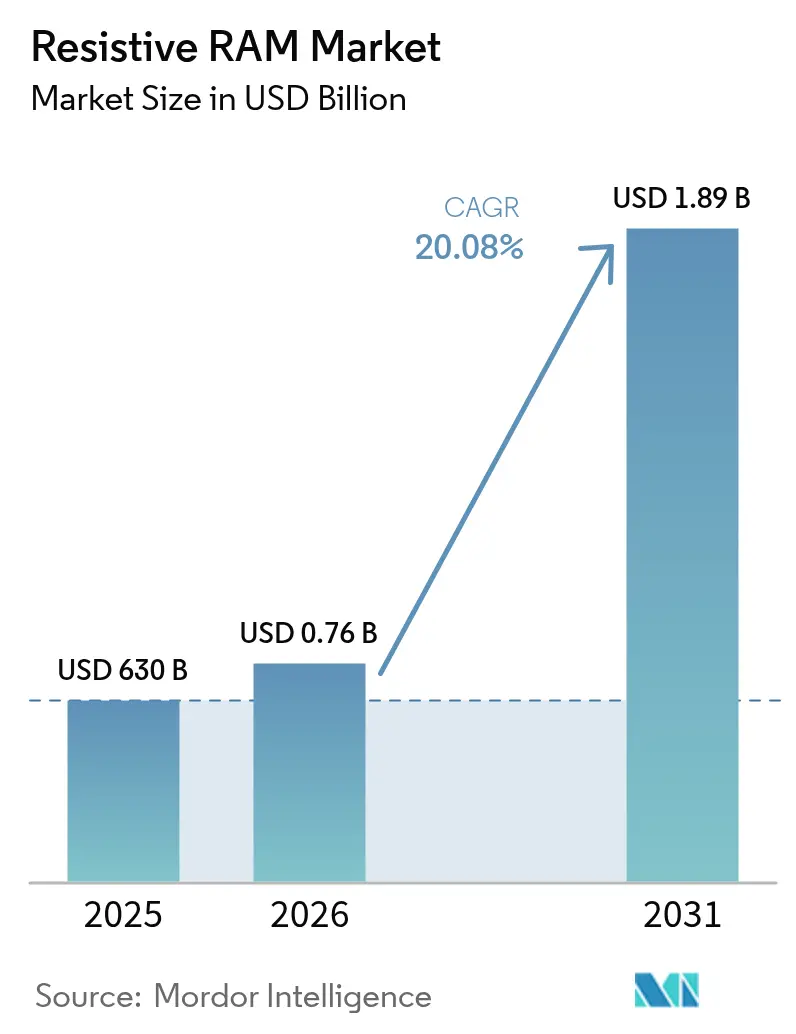

| Market Size (2026) | USD 0.76 Billion |

| Market Size (2031) | USD 1.89 Billion |

| Growth Rate (2026 - 2031) | 20.08% CAGR |

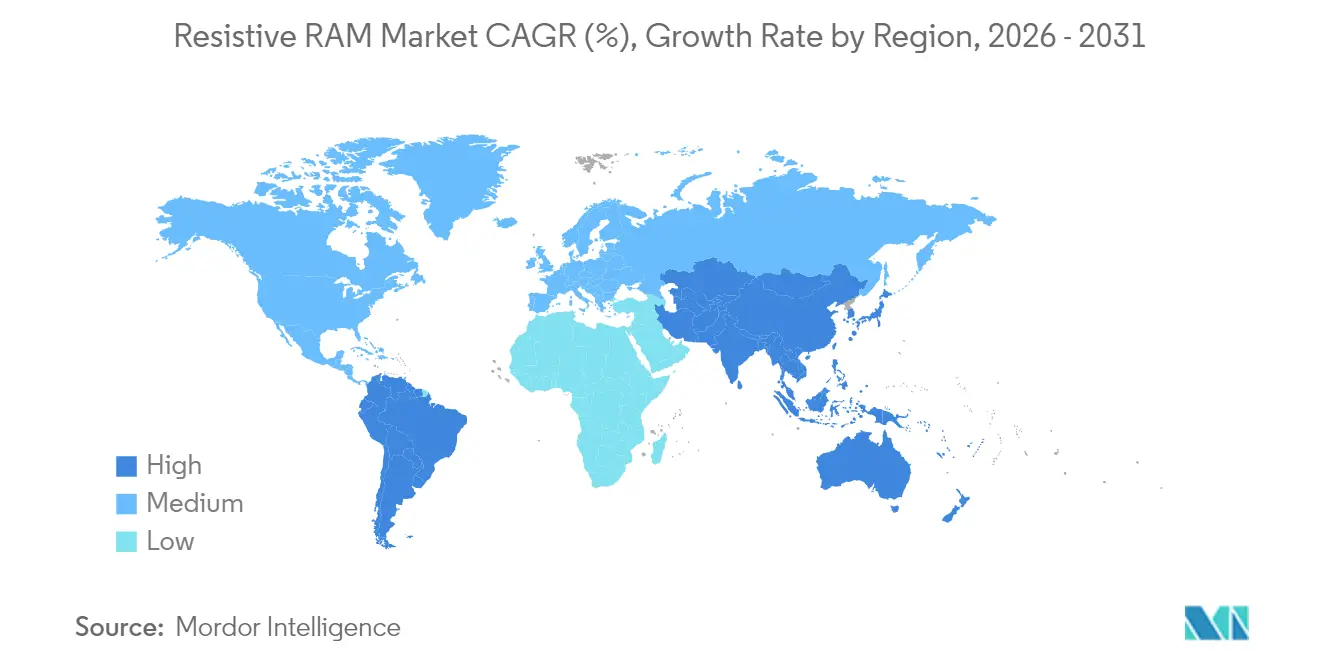

| Fastest Growing Market | South America |

| Largest Market | Asia Pacific |

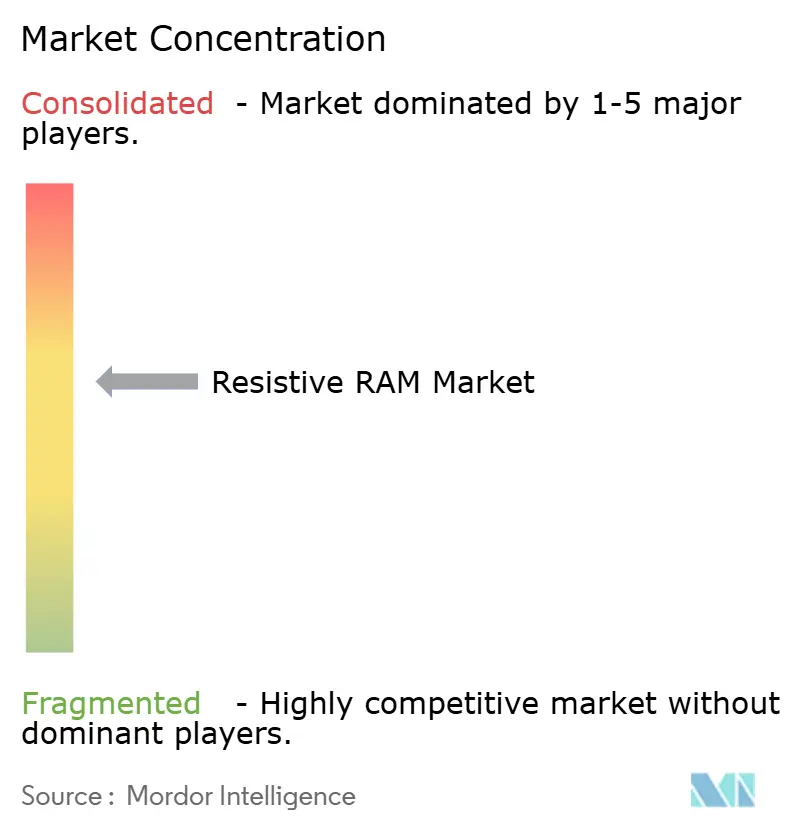

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Resistive RAM Market Analysis by Mordor Intelligence

Resistive random access memory market size in 2026 is estimated at USD 756.5 million, growing from 2025 value of USD 630 million with 2031 projections showing USD 1.89 billion, growing at 20.08% CAGR over 2026-2031. Multiple factors drove this steep climb. Production-grade endurance above 10¹² cycles unlocked mission-critical and high-write-frequency workloads, while sub-1V switching created headroom for battery-powered edge devices. Asia-Pacific’s deep foundry base accelerated embedded ReRAM tape-outs below 28 nm, and automotive ADAS programs raised demand for high-temperature non-volatile options that conventional flash could not meet. Venture capital funding for neuromorphic compute start-ups also added momentum. Together, these trends signaled that ReRAM was moving from laboratory proof-of-concept to mainstream volume adoption.

Key Report Takeaways

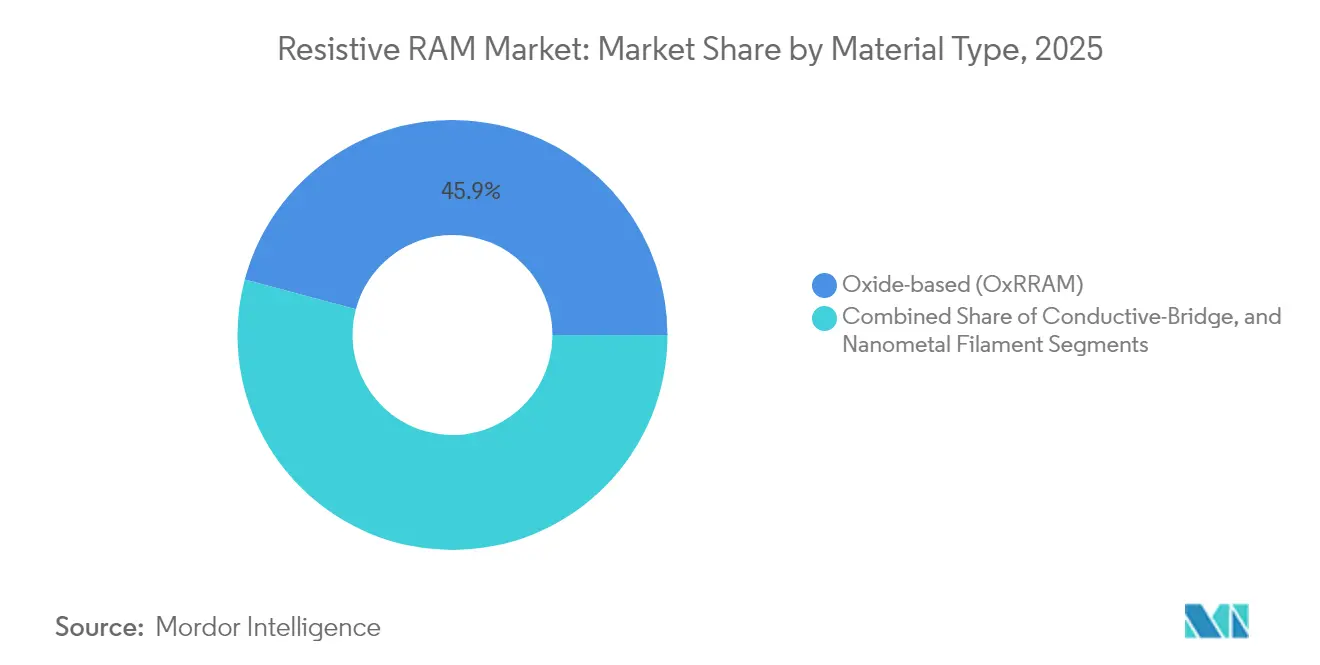

- By material type, oxide-based solutions held 45.85 of % resistive random access memory market share in 2025, while conductive-bridge variants are forecast to grow at a 25.45% CAGR through 2031.

- By form factor, embedded devices led with 54.85% of the resistive random access memory market in 2025; stand-alone devices are poised for a 24.6% CAGR to 2031.

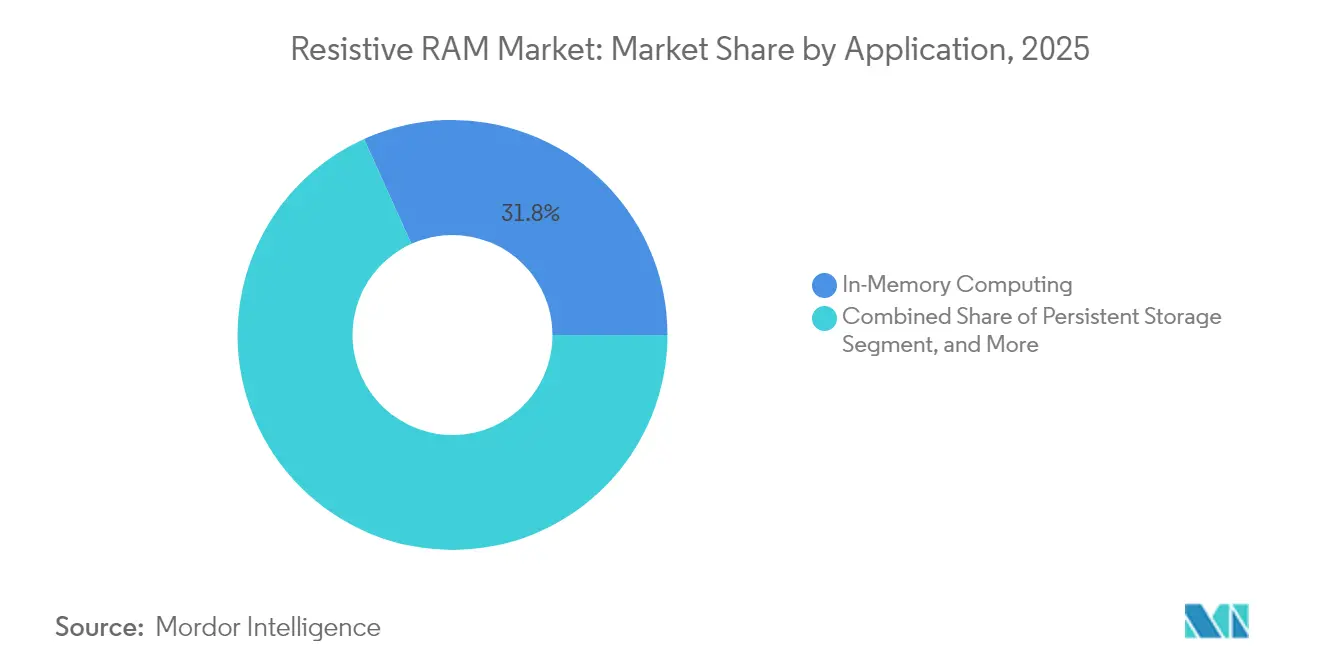

- By application, in-memory computing captured 31.75% share of the resistive random access memory market size in 2025; persistent storage is expected to post the quickest 28.32% CAGR to 2031.

- By end user, industrial and IoT devices accounted for 37.75% of the 2025 resistive random access memory market size, whereas data centers and enterprise SSDs should rise at 25.68% CAGR.

- By geography, Asia-Pacific commanded 40.85% of 2025 revenue; South America is projected to expand at 21.65% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Resistive RAM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Breakthrough endurance improvements beyond 10^12 cycles | +4.2% | Global, with APAC leading adoption | Medium term (2-4 years) |

| Sub-1V switching enabling ultra-low-power edge devices | +3.8% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Foundry support for embedded ReRAM at 28nm and below | +5.1% | APAC core, spill-over to North America | Medium term (2-4 years) |

| Automotive ADAS demand for high-temperature NVM | +2.9% | Global, with early gains in Germany, Japan, US | Long term (≥ 4 years) |

| VC funding surge in neuromorphic compute start-ups | +2.3% | North America and EU primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Breakthrough endurance beyond 10¹² cycles

Endurance exceeding 10¹² cycles positioned ReRAM as a realistic flash replacement for write-intensive enterprise workloads. Academic teams reported aluminum-scandium nitride ferroelectric stacks persisting through 10¹⁰ cycles while retaining polarization.[1]arXiv, “Write Cycling Endurance Exceeding 10¹⁰ in Sub-50 nm Ferroelectric AlScN,” arxiv.org Weebit Nano later validated 100,000 program cycles at 150 °C during automotive tests. This durability lets storage vendors contemplate using ReRAM for hot-tier caching that had previously defaulted to DRAM.

Sub-1 V switching for ultra-low-power edge devices

Research from the University of Virginia showed a 0.6 V conductive-bridge ReRAM macro consuming 8 pJ per write, eliminating charge-pump overhead. Intel echoed the feasibility of sub-1V operation when it demonstrated FinFET-based embedded ReRAM on 22FFL nodes. Battery life gains mattered across wearables, sensor nodes, and smart meters.

Foundry support for embedded ReRAM at 28 nm and below

Commercial qualification by Samsung on 28 nm FD-SOI and Intel on 22 nm FinFET processes meant system-on-chip designers could access ReRAM without bespoke fabs. Density improved as Weebit Nano taped out an 8 Mbit macro on 22 nm FDSOI. Mainstream foundry backing shortened time-to-market for MCU vendors chasing cost and board-area savings.

Automotive ADAS demand for high-temperature NVM

Micron estimated that vehicles required 90 GB of memory in 2025 and would exceed 278 GB by 2026. Phase-change and ReRAM options capable of 150 °C operation fit those profiles. STMicroelectronics’ Stellar xMemory microcontrollers underlined industry migration toward flash alternatives. Functional-safety rules in Europe, Japan, and the US amplified this pull.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Filament variability causing write-noise and bit-error | -3.1% | Global, particularly affecting high-volume manufacturing | Medium term (2-4 years) |

| Limited IP/know-how outside a handful of licensors | -2.4% | Global, with a stronger impact in emerging markets | Long term (≥ 4 years) |

| Challenging integration with 3D NAND BEOL stacks | -1.8% | APAC and North America primarily | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Filament variability causing write-noise and bit-error

Variability in conductive paths hampered yield during high-reliability production. Studies on Ta₂O₅ devices linked voltage-dependent noise to degraded weight resolution in neural arrays.[2]arXiv, “Benchmarking Stochasticity Behind Reproducibility: Denoising Strategies in Ta₂O₅ Memristors,” arxiv.org Crossbar-scale thermal interactions added uncertainty. Wake-up cycling in Al₂O₃ stacks offered mitigation but lengthened process flows.

Limited IP and know-how outside a few licensors

Patents around switching mechanisms sat with Crossbar, Weebit Nano, and select IDM players, forcing smaller entrants into complex negotiations or long R&D detours. Knowledge barriers extended to heterogeneous BEOL integration that only a handful of research fabs had mastered. This concentration slowed price erosion and ecosystem expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Oxide-based leadership meets conductive-bridge acceleration

Oxide-based devices retained 45.85% share of the resistive random access memory market in 2025. HfO₂ and Al₂O₃ stacks were already part of mainstream CMOS flows, which lowered adoption risk. Conductive-bridge variants, often copper-based, registered a 25.45% CAGR outlook because their sub-1V write capability aligned with wearables and micro-power nodes. The resistive random access memory market size for conductive-bridge devices is projected to reach USD 0.60 billion by 2031, reflecting designers’ preference for energy headroom in edge architectures. Nanometal filament approaches captured niche demand where extreme miniaturization or high radiation tolerance mattered. Hybrid carbon filaments demonstrated forming-free operation at 37 nm with >10⁷ cycles.

Oxide-based suppliers responded by enhancing endurance through vacancy-engineered layers that reduced cycle-to-cycle variability. Foundry libraries now bundle oxide-based ReRAM macros alongside logic IP, simplifying MCU tape-outs. Conversely, conductive-bridge proponents leveraged lower programming currents to market battery-life gains. Both camps invested in neural-network analog weight storage demonstrations to tap AI accelerators.

By Form Factor: Embedded integration underpins mainstream demand

Embedded solutions held 54.85% of revenue in 2025 because system-on-chip designers valued die-space savings and simplified bills of materials. MCU vendors embedded 1-4 Mbit macros for secure code storage, firmware updates, and instant-on features. The resistive random access memory market share of embedded devices is expected to remain above 50% through 2031, even as stand-alone density rises.

Stand-alone ReRAM recorded a 24.6% CAGR projection as AI and HPC customers sought bespoke memory modules. Designers could tune array geometry and selector stacks without logic constraints, enabling larger word lines for parallel analog multiply-accumulate. A 4 Mbit compute-in-memory macro with 8-bit precision demonstrated inference at micro-joule energy levels. Cloud vendors evaluated these stand-alone chips as DRAM cache complements for training workloads that benefit from in-situ weight updates.

By Application: In-memory computing leads while persistent storage scales fastest

In-memory computing accounted for 31.75% of 2025 sales. Analog multiply-accumulate within cross-bar arrays reduced data movement between memory and compute, a bottleneck in AI inference. Academic prototypes mapped convolution layers onto 256×256 ReRAM tiles and showed double-digit energy savings versus SRAM accelerators. Persistent storage, however, will outpace at 28.32% CAGR. As NAND endurance limits surfaced under AI logging loads, data-center architects pursued storage-class memory tiers that combined DRAM-like access speed with non-volatility. The resistive random access memory market size allocated to persistent storage is projected to rise to USD 0.52 billion by 2031.

Fast boot/code storage stayed essential for industrial controllers where cold-start times impact safety. Automotive ECUs adopted small ReRAM partitions to hold calibration data that changes with over-the-air updates. Overall, application demand diversified, cushioning suppliers from single-segment cyclicality.

By End User: Industrial IoT stayed largest, datacenters surged

Industrial and IoT devices consumed 37.75% of 2025 shipments thanks to sensors deployed in factories, grids, and agriculture. They valued ReRAM’s radiation tolerance and ability to store logs during brownouts. Datacenters will deliver the steepest 25.68% CAGR as AI workloads mushroom. Hyperscalers piloted tier-zero caches that used ReRAM DIMMs ahead of NAND SSDs to trim write amplification.

Automotive controllers required zero-error logging and high-temperature retention. Wearables and consumer electronics added smaller but strategic volumes where battery life optics drive premium SKU pricing. The resistive random access memory industry, therefore, served a cross-section of mass-market and specialist customers, lowering business risk.

Geography Analysis

Asia-Pacific commanded 40.85% revenue in 2025. Massive foundry investments by Samsung, SK Hynix, and Kioxia expanded embedded ReRAM design kits below 28 nm. South Korea allocated USD 75 billion for advanced memory capacity through 2028, funneling funds into high-bandwidth and next-generation NVM lines. Japan pursued a USD 67 billion semiconductor renaissance plan with ReRAM earmarked for AI edge devices.

South America emerged as the fastest-growing cluster, posting 21.65% CAGR. Brazil funded a R$650 million (USD 130 million) expansion in Atibaia and Manaus to localize encapsulation and test, targeting both ReRAM and DRAM packaging. Regional governments also facilitated the rare-earth mineral supply for oxide films. The resistive random access memory market in South America, therefore, benefited from vertical integration incentives. North America retained design leadership, leveraging automotive and aerospace use cases that demand radiation hardening. The resistive random access memory market size for the US and Canada is forecast to climb alongside ADAS memory mix shifts. Europe focused on industrial control vendors integrating compute-in-memory macros for real-time analytics. The Middle East and Africa saw early traction in smart-city sensor grids where low-power persistent memory reduced maintenance cycles.

Competitive Landscape

The market displayed moderate concentration. Samsung, Intel, and Micron combined chip-scale manufacturing mastery with deep patent estates to supply embedded ReRAM IP libraries to ASIC and MCU customers. Specialized firms such as Crossbar, Weebit Nano, 4DS Memory, and Ferroelectric Memory GmbH competed via licensing and fab-less partnerships. Weebit Nano’s demo with DB HiTek at PCIM 2025 showed the leverage of foundry alliances.

Strategic moves in 2024-2025 included SK Hynix’s USD 75 billion capacity build, Everspin’s USD 9.25 million radiation-hardened eMRAM contract with Frontgrade, and SoftBank-Intel collaboration on stacked DRAM-ReRAM hybrids aiming for 50% power cuts in AI servers. RAAAM Memory Technologies drew EUR 5.25 million (USD 6.14 million) in EU funding to commercialize on-chip variants, signalling that disruptive entrants continued to receive institutional backing.

Some vendors differentiated on automotive-grade qualification, others on neuromorphic precision. Patent filings around voltage-supply circuits and selector stacks hinted at continued device-physics innovation.[4]Justia Patents, “Voltage Supply Circuit, Memory Cell Arrangement,” justia.com As cost curves improve, the competitive frontier is likely to shift toward software ecosystems able to exploit compute-in-memory primitives.

Resistive RAM Industry Leaders

Panasonic Corporation

Adesto Technologies

Fujitsu Ltd

Crossbar Inc.

Rambus Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: SoftBank and Intel partnered on AI memory chips using stacked DRAM-ReRAM wiring, targeting 50% power reduction for Japan’s data-center fleets.

- May 2025: Weebit Nano and DB HiTek demonstrated integrated ReRAM chips at PCIM 2025.

- January 2025: Everspin won a USD 9.25 million Frontgrade contract for radiation-hardened eMRAM macro development to serve aerospace programs.

- January 2025: Numem announced MRAM chiplet sampling by end-2025, delivering 4 TB/s bandwidth per stack.

Global Resistive RAM Market Report Scope

Resistive random access memory(ReRAM or RRAM) is a non-volatile random access computer memory that operates on the principle of changing the resistance over a dielectric solid-state material. Resistive random access memory is based on applying the memory function by changing the material's resistance between a high and low state.

The Resistive RAM Market is segmented by Application (Embedded, Standalone), End-user (Industrial/IoT/Wearables/Automotive, SSD/Datacenters/Workstations), and Geography (Americas, Europe, China, Japan, Asia-Pacific ((excl China and Japan)). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Oxide-based (OxRRAM) |

| Conductive-Bridge (CBRAM) |

| Nanometal Filament |

| Embedded ReRAM |

| Stand-alone ReRAM |

| In-Memory Computing |

| Persistent Storage |

| Fast Boot / Code Storage |

| Industrial and IoT Devices |

| Automotive and Mobility |

| Datacentres and Enterprise SSD |

| Wearables and Consumer Electronics |

| North America | United States | |

| Canada | ||

| South America | Brazil | |

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Material Type | Oxide-based (OxRRAM) | ||

| Conductive-Bridge (CBRAM) | |||

| Nanometal Filament | |||

| By Form Factor | Embedded ReRAM | ||

| Stand-alone ReRAM | |||

| By Application | In-Memory Computing | ||

| Persistent Storage | |||

| Fast Boot / Code Storage | |||

| By End-user | Industrial and IoT Devices | ||

| Automotive and Mobility | |||

| Datacentres and Enterprise SSD | |||

| Wearables and Consumer Electronics | |||

| By Geography | North America | United States | |

| Canada | |||

| South America | Brazil | ||

| Rest of South America | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| South Korea | |||

| Taiwan | |||

| India | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What was the global value of the resistive random access memory market in 2026?

It stood at USD 756.5 million and is projected to climb to USD 1.89 billion by 2031.

Which material type led the resistive random access memory market in 2025?

Oxide-based devices dominated with 45.85% market share, mainly due to mature CMOS compatibility.

Why is South America the fastest-growing region?

Government incentives and new packaging investments in Brazil positioned the region for a 21.65% CAGR between 2026-2031.

How does ReRAM benefit edge and IoT devices?

Sub-1V switching enables ultra-low-power writes, which extend battery life while maintaining data persistence during power loss.

What technical hurdle most limits ReRAM adoption today?

Filament variability, which introduces write-noise and bit errors, remains the key challenge for high-volume manufacturing.

Which end-user segment is forecast to grow quickest through 2031?

Datacenters and enterprise SSDs are expected to expand at a 25.68% CAGR as AI workloads demand high-endurance, low-latency non-volatile memory.

Page last updated on: