Precision Viticulture Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

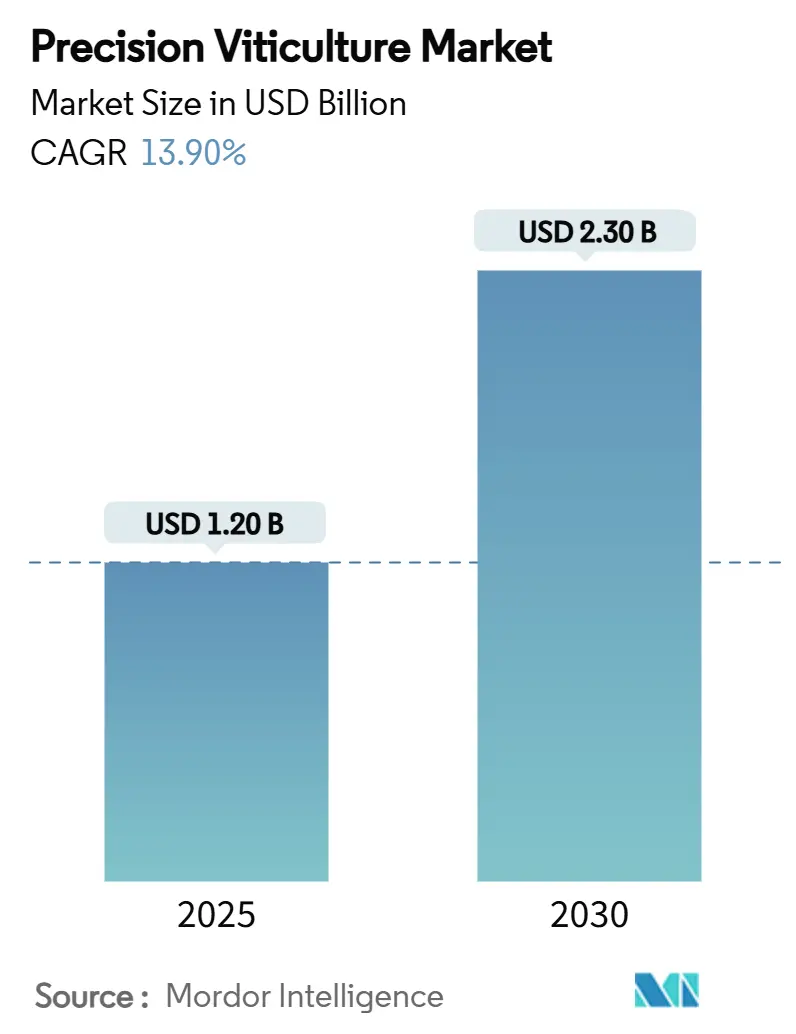

| Market Size (2025) | USD 1.20 Billion |

| Market Size (2030) | USD 2.30 Billion |

| Growth Rate (2025 - 2030) | 13.90% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Precision Viticulture Market Analysis by Mordor Intelligence

The precision viticulture market size is valued at USD 1.20 billion in 2025 and is on course to reach USD 2.30 billion by 2030, advancing at a 13.9% CAGR through the forecast period. Sharply rising labor expenses, the rapid drop in sensor costs, and tougher runoff regulations are steering vineyard owners toward data-driven field operations. Drone-enabled multispectral imaging, once reserved for large estates, now sits below USD 5,000 per unit, opening a broad gateway for medium vineyards to adopt variable-rate spraying and real-time canopy diagnostics. California’s tightening water-quality rules, China’s digital-agriculture subsidies, and Australia’s climate-adaptation incentives together underpin a cross-regional surge in demand for connected equipment. Competitive pressure is also mounting on platform-based ecosystems that combine hardware, AI software, and advisory services are becoming the default procurement model for growers seeking both cost control and verified quality claims.

Key Report Takeaways

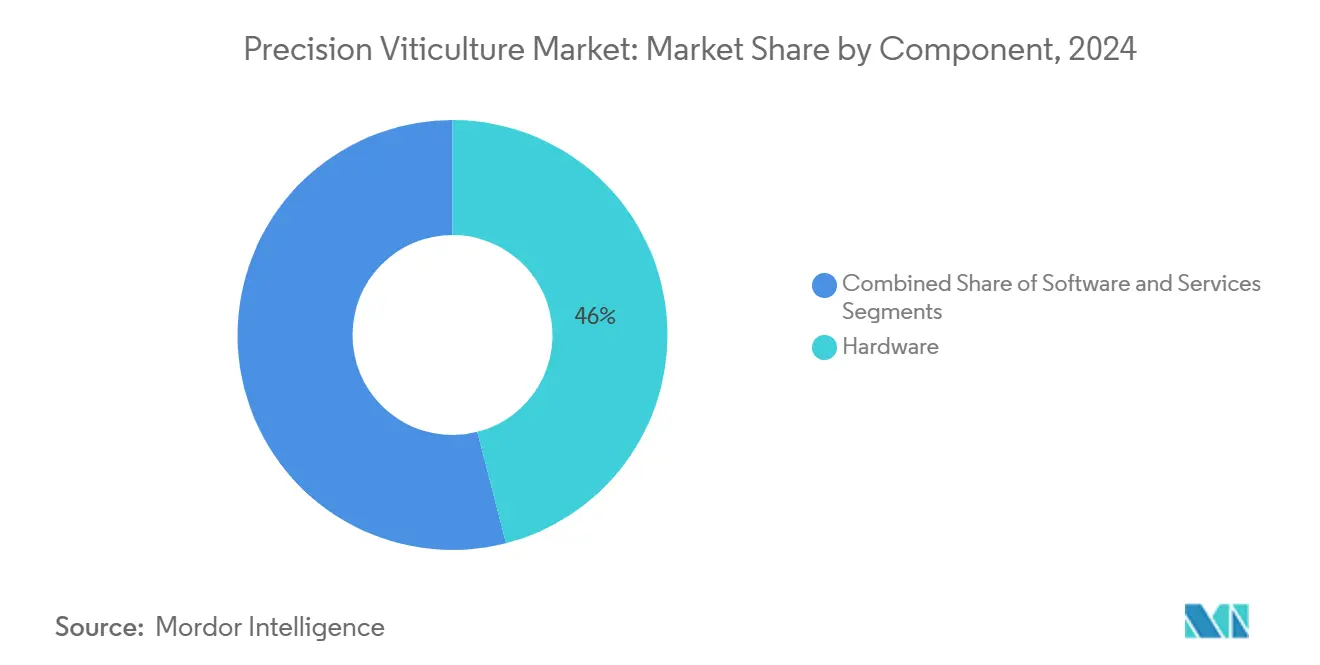

- By component, hardware led with a 46% revenue share in 2024, and software is projected to register the fastest growth at a 17.2% CAGR to 2030.

- By 2024, GPS-guided steering systems accounted for 39% of the precision viticulture market share, while drone-based imaging is forecasted to expand at a 22.5% CAGR through 2030.

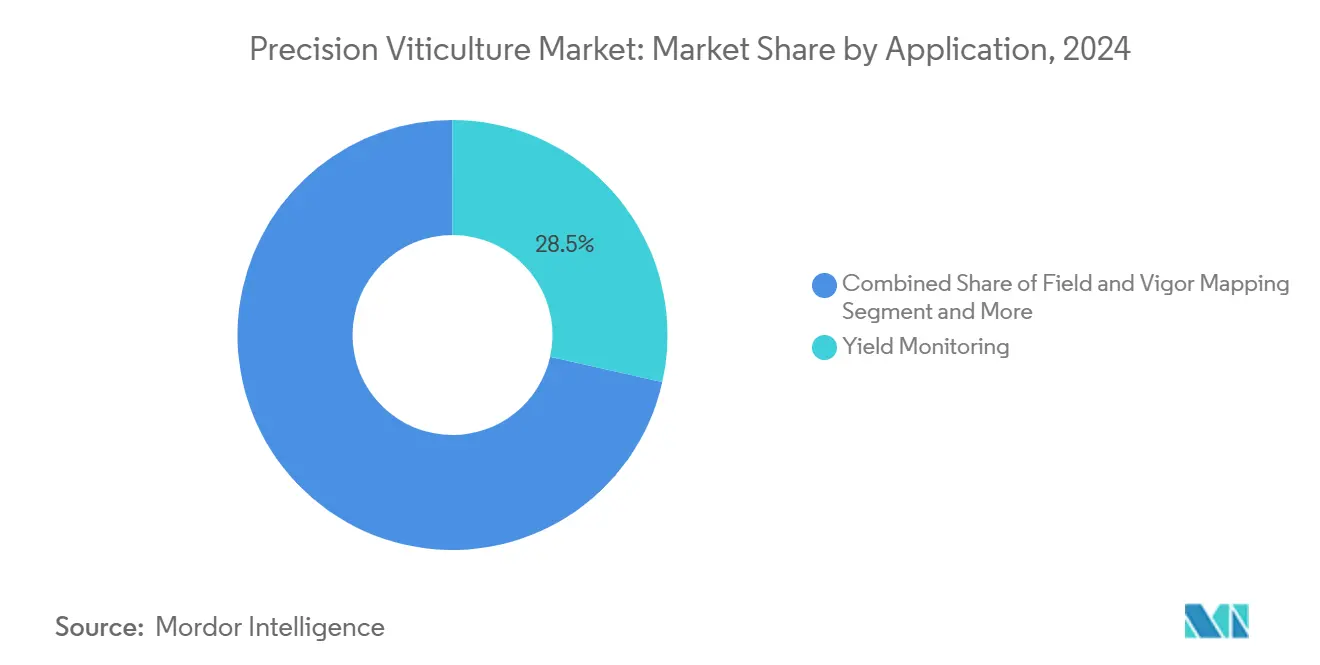

- By application, yield-monitoring tools captured 28.5% of the precision viticulture market size in 2024, and variable-rate systems are poised for 18.4% CAGR growth to 2030.

- By end user, large vineyards held a 44% share of the precision viticulture market size in 2024, and medium vineyards recorded the strongest 19.1% CAGR outlook to 2030.

- By deployment mode, on-premise systems dominated with 61% revenue share in 2024, and cloud-based platforms are projected to grow at a 20.3% CAGR to 2030.

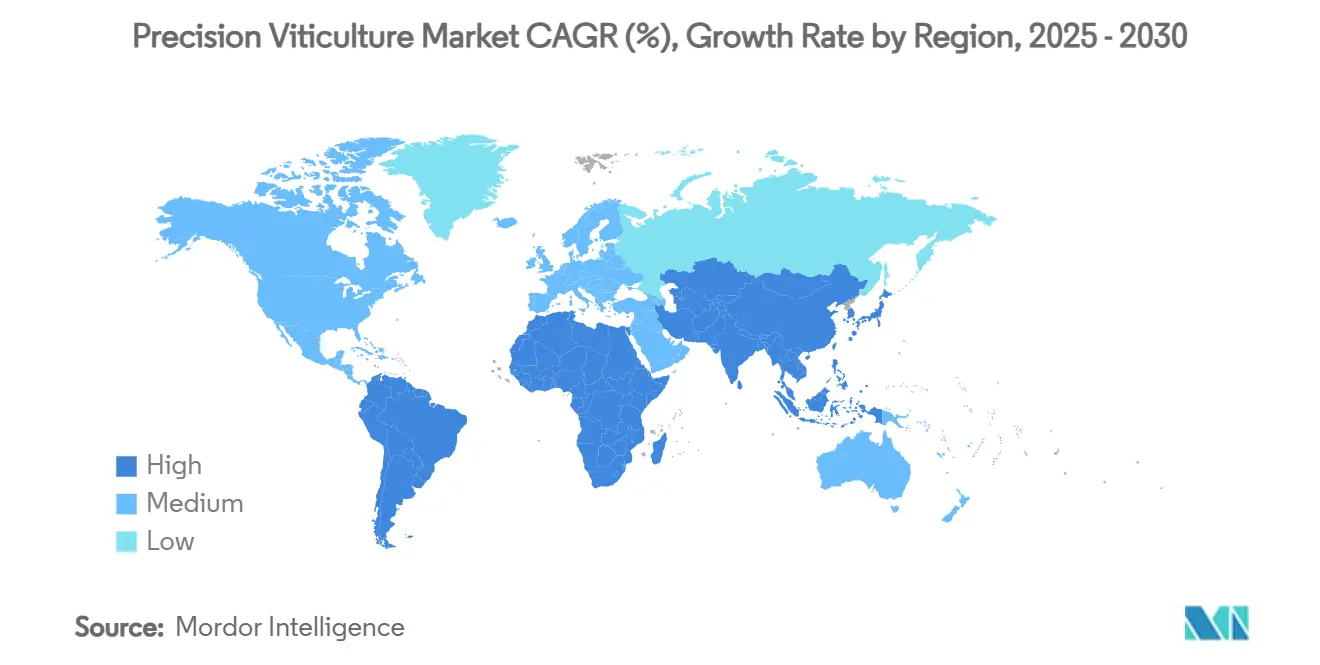

- By geography, North America led with a 36% revenue share in 2024, whereas the Asia-Pacific region is anticipated to clock the fastest 17.8% CAGR through 2030.

Global Precision Viticulture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating Labor Shortages in Vineyards | +3.2% | Global, stronger in North America and Europe | Short term (≤ 2 years) |

| Growing Availability of Affordable Multispectral Drones | +2.8% | Global, early uptake in Asia-Pacific and North America | Medium term (2-4 years) |

| Rising Demand for Premium-Quality, Terroir-Specific Wines | +2.1% | Europe and North America, expanding in South America | Medium term (2-4 years) |

| Carbon-credit Monetization for Low-input Vineyards | +1.4% | Europe and North America, emerging in Asia-Pacific | Long term (≥ 4 years) |

| Regulatory Pressure to Curb Chemical Runoff | +1.8% | North America and Europe, extending to Asia-Pacific | Medium term (2-4 years) |

| Advancement in AI-Powered Yield-Forecasting System | +1.5% | Global, tech hubs in North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Escalating Labor Shortages in Vineyards

Seasonal field crews have thinned by 30% across the major wine belts over the last five years, adding sharp wage inflation and prompting growers to trial autonomous tractors that achieve 92% yield-monitoring accuracy while working around the clock [1]Source: United States Department of Agriculture, “Rural Broadband Progress Report,” usda.gov. California’s new overtime statutes and immigration bottlenecks intensify the cost burden, accelerating the precision viticulture market adoption curve. In Europe, mechanized pruning pilots show 28% labor-hour savings without compromising cane quality, a metric now guiding mid-sized estates in France and Spain toward robotics leasing contracts. Autonomous fleets further reduce harvest bottlenecks by synchronizing machine picking with Brix thresholds detected via in-field sensors, a practice that lifts premium-grade grape intake by up to 7% in Napa trials.

Growing Availability of Affordable Multispectral Drones

Drone system prices are down 60% over the past 5 years, yet deliver centimeter-level mapping and 90% disease-spotting accuracy when paired with edge AI processors [2]Source: MDPI Editors, “Multispectral Drone Imagery for Vineyard Assessment,” mdpi.com . Sub-USD 5,000 quadcopters now transmit stitched NDVI maps to cloud dashboards in under 10 minutes, letting small vineyards dispatch variable-rate sprayers in the same workday. France recently cleared low-risk drone spraying on slopes steeper than 20%, widening use cases for rugged terrains that conventional boom rigs cannot reach. Cross-linking these aerial scans with soil-moisture probes is fast becoming a standard operating procedure that cuts irrigation volumes by 18% season-over-season in Australian pilot blocks.

Rising Demand for Premium-Quality, Terroir-Specific Wines

Consumers consistently pay double for bottles with documented regenerative practices, driving wineries to install dense sensor networks that log canopy microclimate and phenolic profiles in real time [3]Source: Wine Institute, “Premium Wine Market Trends 2025,” wineinstitute.org . Blockchain timestamps of block-by-block data underpin new appellation-grade storytelling and command shelf premiums for boutique labels competing on authenticity rather than production scale. Precision mapping also aligns with sommelier-grade segmentation, enabling selective micro-vinification that captures higher margins without expanding vineyard acreage.

Advancement in AI-Powered Yield-Forecasting Systems

Deep-learning models trained on multispectral and weather datasets now forecast cluster weight within ±6% two weeks before harvest, allowing tighter logistics planning and dynamic pricing commitments [4]Source: Nature Publishing Group, “Deep-Learning Models for Vineyard Yield Prediction,” nature.com . Such predictive accuracy lets cooperatives balance tank allocations ahead of peak crush, improving asset utilization and reducing fermenter downtime. Vendors are layering this forecasting into subscription analytics, a trend that transitions margin potential away from hardware sales toward recurring software revenue for the precision viticulture market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Hardware and Retrofit Costs | -2.4% | Global, highest on small holdings | Short term (≤ 2 years) |

| Fragmented Vineyard Landholding Patterns | -1.8% | Europe and Asia-Pacific, moderate in South America | Medium term (2-4 years) |

| Limited Broadband Coverage in Rural Terroirs | -1.3% | Global rural zones | Medium term (2-4 years) |

| Data Ownership and Privacy Concerns | -0.9% | North America and Europe, rising in Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Hardware and Retrofit Costs

Full-stack precision setups typically cost between USD 15,000 and USD 50,000 per hectare, representing a significant investment for family-operated vineyards, which average 6 hectares in size across Italy and Portugal [5]Source: United States Government Accountability Office, “Precision Agriculture Adoption Challenges,” gao.gov . The USDA (United States Department of Agriculture) offers grants and low-interest credit lines to help mitigate some of these costs. However, adoption slows when vineyards need to reconfigure existing trellis systems to accommodate autonomous equipment. Equipment-as-a-service contracts and regional technology-sharing cooperatives are helping to reduce these barriers. For instance, in Sonoma, a 14-member collective reduced capital expenditure per grower by 64% through the use of shared drone fleets and analytics platforms.

Fragmented Vineyard Landholding Patterns

In Burgundy, France, inheritance traditions result in the division of vineyards into numerous micro-parcels, many of which are smaller than 2 hectares. This fragmentation causes efficiency losses of 15–25% compared to consolidated vineyards [6]Source: Food and Agriculture Organization, “Land Fragmentation and Agricultural Productivity,” fao.org . The fragmented layout complicates data aggregation, as microclimates can vary significantly over short distances, necessitating frequent sensor redeployment and increasing per-acre costs. Portable, clip-on sensing devices aim to address these challenges but often compromise analytical depth, limiting the potential for precision-oriented improvements in fragmented estates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Accelerates while Hardware Commands Near-term Spend

Hardware generated 46% of 2024 revenue as GPS terminals, RTK antennas, and variable-rate sprayers formed the bedrock of precision workflows. The precision viticulture market size for hardware is projected to advance at buoyed by autonomous tractors that reduce labor inputs by up to 40% per hectare. Software, though presently smaller, enjoys the top 17.2% CAGR because AI layers convert raw field data into predictive agronomy insights valued by oenologists. Subscription dashboards now bundle disease alarms, irrigation schedules, and carbon-credit MRV services, a combination that raises switching costs and drives stickier revenue streams. Services occupy 34% share, reflecting the installer network and agronomic consultancy hours needed to operationalize these complex systems.

Smaller estates often choose services-first engagement, outsourcing drone flights and analytics before budgeting for their equipment. This “crawl-walk-run” pathway gradually builds digital muscle, smoothing the adoption curve. Vendors increasingly package hardware leasing, agronomy advice, and platform access in a single contract, a model anticipated to widen the precision viticulture market reach among cost-sensitive European growers.

By Deployment Mode: On-Premise Still Dominant, Cloud Racing Ahead

On-premise architecture retained a 61% share in 2024 as many growers insist on local servers to safeguard terroir IP and mitigate patchy internet. Cloud systems, though, lead in velocity with 20.3% CAGR. When Chilean estate data migrated to the cloud in 2024, nightly AI model refreshes boosted yield-forecast accuracy by 11%, persuading neighboring growers to follow. Hybrid topologies that pair edge gateways with cloud AI inference are emerging, promising secure autonomy with scalable analytics the likely endpoint for digitally mature vineyards inside the precision viticulture market.

Cyber-security audits are becoming a decisive factor in deployment choice, especially for wineries with high-value intellectual property such as proprietary yeast libraries and estate-block phenolic maps. Vendors now offer on-premise “sovereign cloud” appliances that keep raw sensor feeds inside the winery firewall while forwarding only anonymized feature sets for cloud-based AI training. Early pilots in Oregon show these hybrid nodes trimming latency by 40% during harvest while meeting strict data-governance policies, an approach likely to expand as compliance mandates tighten across export markets

By Technology: Guidance Systems in Pole Position, Drones in the Fast Lane

Guidance modules anchored 39% revenue in 2024 and represent the entry point for growers new to site-specific farming. Precision autosteer kits boasting ±2-cm accuracy align boom sprayers exactly atop vineyard rows, cutting overlap and chemical spend by 18% on average across Washington State trials [7]Source: Washington State University Viticulture and Enology, “Autosteer Impacts on Spray Efficiency,” wsu.edu . The precision viticulture market size linked to drone and UAV imagery, although smaller today, is rising at a 22.5% CAGR with permissive spray-drone laws and AI image stitching that delivers 250-acre coverage per flight.

Variable-rate technology operates as the connective tissue between sensing and execution, directing fertilizers and fungicides solely where indices show need. Remote-sensing satellites remain complementary, with scheduled 5-day revisits, which feed mid-season vigor maps that refine intra-row irrigations. Robotics remains a nascent but strategically important field, with commercial prototypes now capable of pruning 240 vines per hour while simultaneously training an onboard model that self-improves across vintages, underscoring an emerging feedback loop within the precision viticulture market.

By Application: Yield Monitoring Still the Anchor, Variable-Rate Gains Pace

Yield sensors fitted to harvesters captured 28.5% market share in 2024, cementing their status as the foundational dataset for field profitability analytics. When those readings merge with sap-flow probes, wineries can allocate premium fermentor space days ahead of picking, shaving logistics friction. Variable-rate application tools, advancing at 18.4% CAGR, resonate with both environmental regulators and CFOs in Chilean coastal vineyards, 19% fertilizer savings translated into USD 140 per acre OPEX drop in 2024 [8]Source: Chilean Ministry of Agriculture, “Site-Specific Nutrient Application Results,” chileag.cl .

Field-and-vigour mapping, integrates NDVI mosaics, electrical conductivity, and leaf-water-potential tracks, giving viticulturists a layered snapshot of spatial heterogeneity. Disease-and-pest modules employ CNN-based leaf classification to detect downy mildew up to seven days earlier than manual scouting, facilitating spot spraying that protects beneficial insects and preserves label residue limits. Harvest quality assessments close the loop by correlating berry phenolics to micro-block soil nuance, supporting pricing models that market terroir authenticity at retail.

By End User: Larger Estates Lead but Medium Vineyards Close the Gap

Operations above 50 hectares accounted for 44% of 2024 revenue as scale economics justify full-suite deployments. Yet, high-growth momentum is found in 10-50 hectare properties, where cooperative financing and declining tech prices drive a 19.1% CAGR. These midsize players often sell through direct-to-consumer channels and therefore prize the data narratives that precision platforms generate, using them to justify price-point differentiation. Small vineyards remain constrained by capital budgets. However, rental drones and pay-per-acre analytics are now lowering the entry barrier, signaling a gradual broadening of the precision viticulture market.

A growing tier of contract service providers now targets small and medium estates with “outcome-based” agreements that bundle hardware leases, agronomic advice, and labor sourcing into a single per-acre fee. These firms guarantee specified pruning accuracy or spray-overlap limits and absorb the technology risk themselves, a model that shortens decision cycles for owners wary of cap-ex exposure. As these subscription services scale, they are expected to shift roughly 6% of total precision viticulture market spending from direct equipment purchases to managed-service contracts by 2030, further flattening the adoption curve for operators under 50 hectares

Geography Analysis

North America held a 36% share in 2024. California's runoff caps and labor shortages drive adoption, while the USDA’s USD 700 million ReConnect Program closes connectivity gaps in rural valleys. Canada’s Okanagan Valley now pilots government-backed carbon-credit schemes tied to precision spray logs, adding a revenue kicker that accelerates platform payback.

Asia-Pacific is charting the swiftest 17.8% CAGR. China’s Digital Villages grants subsidies for GNSS-enabled tractors by up to 30% of the purchase price, igniting an upgrade wave among Ningxia’s emerging wine clusters. Australia couples drought resilience grants with sensor deployments that have already trimmed water demand by 25% in Barossa test beds. New Zealand’s biodiversity offsets likewise hinge on documented spray-volume reductions, aligning perfectly with variable-rate adoption.

Europe shows steady market growth. EU Common Agricultural Policy reforms tie subsidies to soil-health metrics, effectively rewarding aerial imaging and variable-rate seeding. France’s drone-spray clearance and Germany’s tax incentives for autonomous implements provide direct monetary levers. Fragmented holdings continue to slow penetration in Italy and Spain, yet regional cooperatives now pool drone flights to overcome this hurdle, widening the precision viticulture market footprint.

Competitive Landscape

Top-five vendors control the majority of global revenue, signaling moderate concentration yet leaving ample room for niche specialists. Deere & Company leads with a precision equipment portfolio that integrates RTK steering, machine vision, and cloud analytics. Trimble Inc.’s GNSS expertise follows Deere & Company, freshly bolstered by its USD 2 billion joint venture with AGCO Corporation that co-packages hardware and agronomy software into a single procurement channel.

Mid-tier upstarts sharpen focus on targeted pain points. Greeneye Technology’s AI spraying system claims 88% herbicide cuts, a proposition resonating strongly with Europe’s chemical-reduction mandates. Phytech’s plant-stress sensors, meanwhile, anchor new irrigation as-a-service models that guarantee water savings. Consolidation is anticipated to intensify as incumbents scoop specialized IP to complete end-to-end platforms, echoing CNH Industrial NV’s 2025 move to embed Bluewhite autonomy inside New Holland tractors.

Open-interface initiatives are also reshaping rivalry. The AgGateway consortium has released a vineyard-specific adaptation of its ADAPT data-model standard, enabling plug-and-play interoperability between guidance consoles, sensor arrays, and third-party analytics engines. Early adopters report integration times falling from two weeks to three days when onboarding new devices, a time saving that reduces deployment cost by an estimated 9% per project. As more suppliers certify against the standard, competitive emphasis is expected to tilt from proprietary lock-in toward service performance and analytics depth, a shift that benefits growers by lowering switching barriers and stimulating innovation

Precision Viticulture Industry Leaders

Deere & Company

Trimble Inc.

AGCO Corporation

Hexagon Agriculture

Topcon Positioning Systems, Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Deutsche Telekom has implemented a 5G campus network in the Moselle Valley vineyards, facilitating real-time data processing for autonomous robots used in soil cultivation and defoliation. This smart vineyard initiative aims to optimize the use of water, fertilizers, and crop protection while mitigating labor shortages.

- July 2024: VineView launched the PinPoint RTK Handheld GPS Receiver for field data collection, offering accuracy through Real-Time Kinematic (RTK) technology. The device provides 2-5cm (2 inches) accuracy, compared to traditional GPS receivers with 2-4m (7-13ft) accuracy. This precision enables vineyard operators to create detailed maps for decision-making and planning.

- June 2024: CNH Industrial NV and Bluewhite began integrating autonomy into New Holland orchard and vineyard tractors, targeting up to 85% labor-cost relief.

- January 2023: CropX Technologies acquired Tule Technologies, a California-based precision irrigation company. The acquisition expanded CropX's presence in California, specifically in the drip-irrigated specialty crops segment, including grapes and nuts.

Global Precision Viticulture Market Report Scope

| Hardware |

| Software |

| Services |

| Guidance (GPS/GNSS) |

| Variable-Rate Technology |

| Remote Sensing |

| IoT Sensors and Edge Devices |

| Robotics and Drones |

| Yield Monitoring |

| Field and Vigor Mapping |

| Variable-Rate Application |

| Disease and Pest Management |

| Irrigation Management |

| Harvest Quality Assessment |

| Large Vineyards (>50 ha) |

| Medium Vineyards (10-50 ha) |

| Small Vineyards (<10 ha) |

| On-premise |

| Cloud-based |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Italy | |

| Spain | |

| United Kingdom | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Turkey |

| Israel | |

| Saudi Arabia | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Component | Hardware | |

| Software | ||

| Services | ||

| By Technology | Guidance (GPS/GNSS) | |

| Variable-Rate Technology | ||

| Remote Sensing | ||

| IoT Sensors and Edge Devices | ||

| Robotics and Drones | ||

| By Application | Yield Monitoring | |

| Field and Vigor Mapping | ||

| Variable-Rate Application | ||

| Disease and Pest Management | ||

| Irrigation Management | ||

| Harvest Quality Assessment | ||

| By End User | Large Vineyards (>50 ha) | |

| Medium Vineyards (10-50 ha) | ||

| Small Vineyards (<10 ha) | ||

| By Deployment Mode | On-premise | |

| Cloud-based | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Italy | ||

| Spain | ||

| United Kingdom | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Turkey | |

| Israel | ||

| Saudi Arabia | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current precision viticulture market size?

The precision viticulture market size stands at USD 1.20 billion in 2025 and is forecast to reach USD 2.30 billion by 2030.

Which component segment is growing the fastest?

Software shows the quickest momentum, projected at a 17.2% CAGR through 2030 as AI analytics become essential for decision support.

Why are drones vital to precision viticulture?

Affordable multispectral drones enable rapid canopy health mapping, disease detection, and slope-safe spray applications, driving a 22.5% CAGR in the drone technology segment.

Which region leads and which is growing fastest?

North America currently leads with 36% revenue share, while Asia-Pacific posts the fastest 17.8% CAGR as China and Australia ramp up digital farming incentives.

How do precision tools help manage vineyard labor shortages?

Autonomous tractors and AI steering cut manual labor needs by up to 40%, addressing a 30% decline in seasonal worker availability since 2020.

What restrains widespread adoption?

High upfront hardware costs, fragmented landholdings, rural connectivity gaps, and unresolved data-ownership concerns collectively temper adoption speed.

Page last updated on: