Resistor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

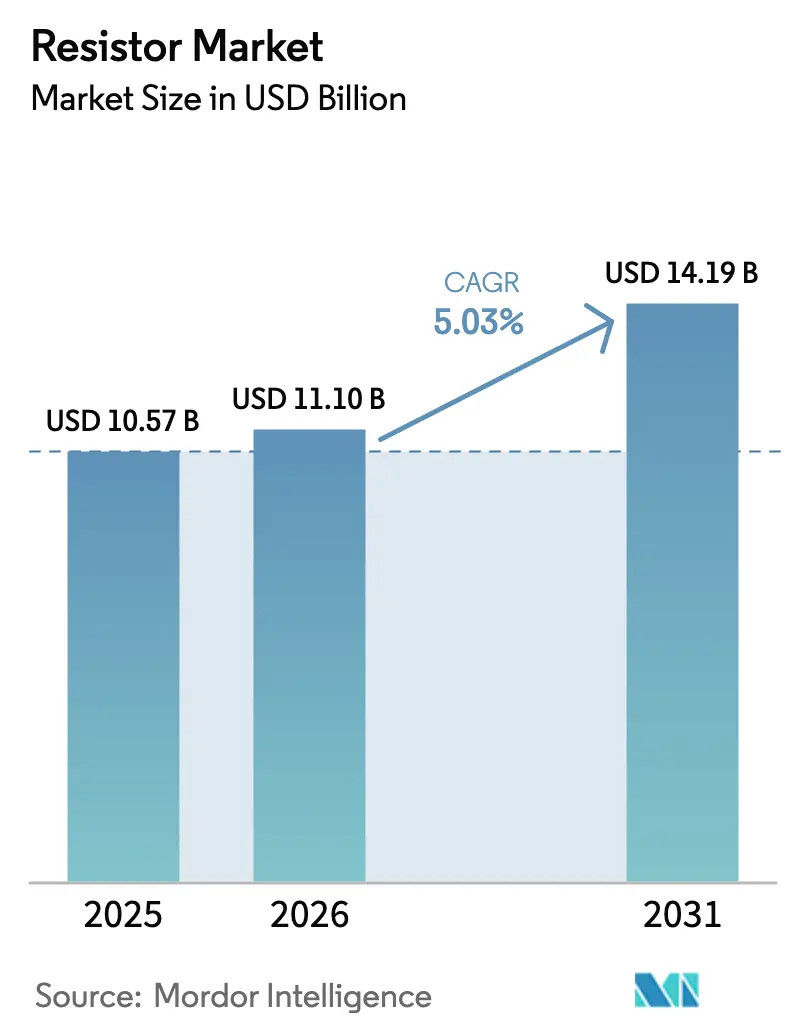

| Market Size (2026) | USD 11.1 Billion |

| Market Size (2031) | USD 14.19 Billion |

| Growth Rate (2026 - 2031) | 5.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Resistor Market Analysis by Mordor Intelligence

The global resistor market size in 2026 is estimated at USD 11.10 billion, growing from 2025 value of USD 10.57 billion with 2031 projections showing USD 14.19 billion, growing at 5.03% CAGR over 2026-2031. This steady expansion reflects growing electronic content across automobiles, next-generation consumer devices, and 5G infrastructure, all of which require higher volumes of precision passive components. Sub-CAGR tailwinds come from the rapid electrification of powertrains that depend on ultra-low-ohmic shunts for battery management, while miniaturization trends push demand for surface-mount chip formats able to fit ever-smaller printed-circuit footprints. The resistor market benefits from a widening array of high-frequency, high-reliability applications that command premium pricing and offset raw-material volatility. Meanwhile, aggressive capacity additions in East Asia underpin cost leadership yet intensify price competition, compelling incumbents to invest in thin-film processes and automotive-grade qualification. Overall, tight tolerance specifications, superior thermal management, and robust supply-chain resilience emerge as pivotal purchase criteria for buyers worldwide

Key Report Takeaways

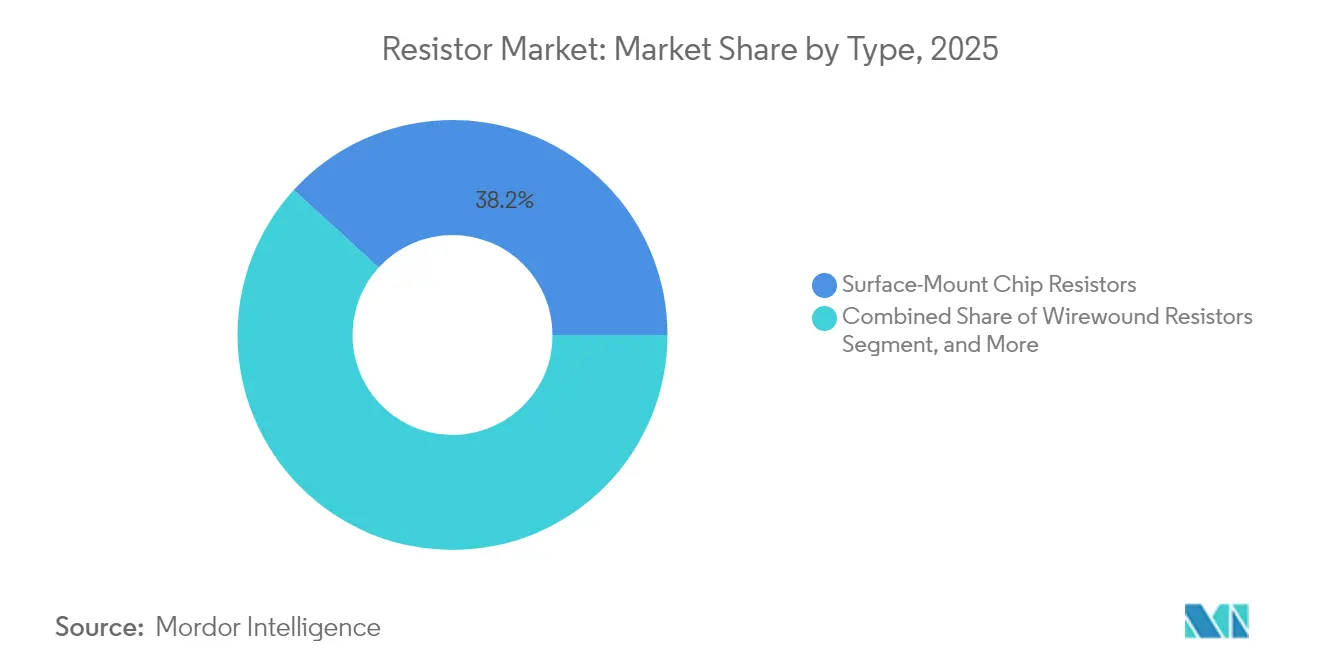

- By type, surface-mount chip resistors led with 38.22% of the resistor market share in 2025, and shunt and current-sense devices are forecast to grow at a 6.49% CAGR to 2031 within the resistor market.

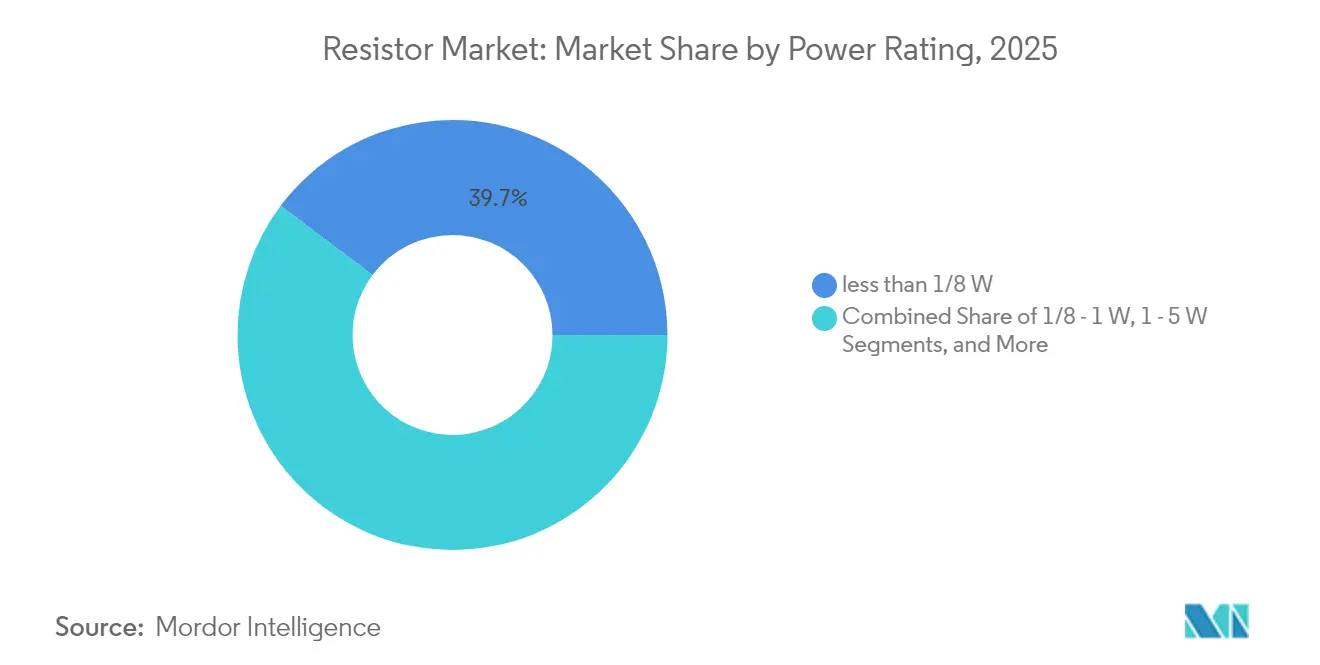

- By power rating, resistors above 5 W are poised to expand at a 6.67% CAGR through 2031 in the resistor market.

- By end-user, automotive applications will post the fastest 6.74% CAGR, outpacing consumer electronics within the resistor market.

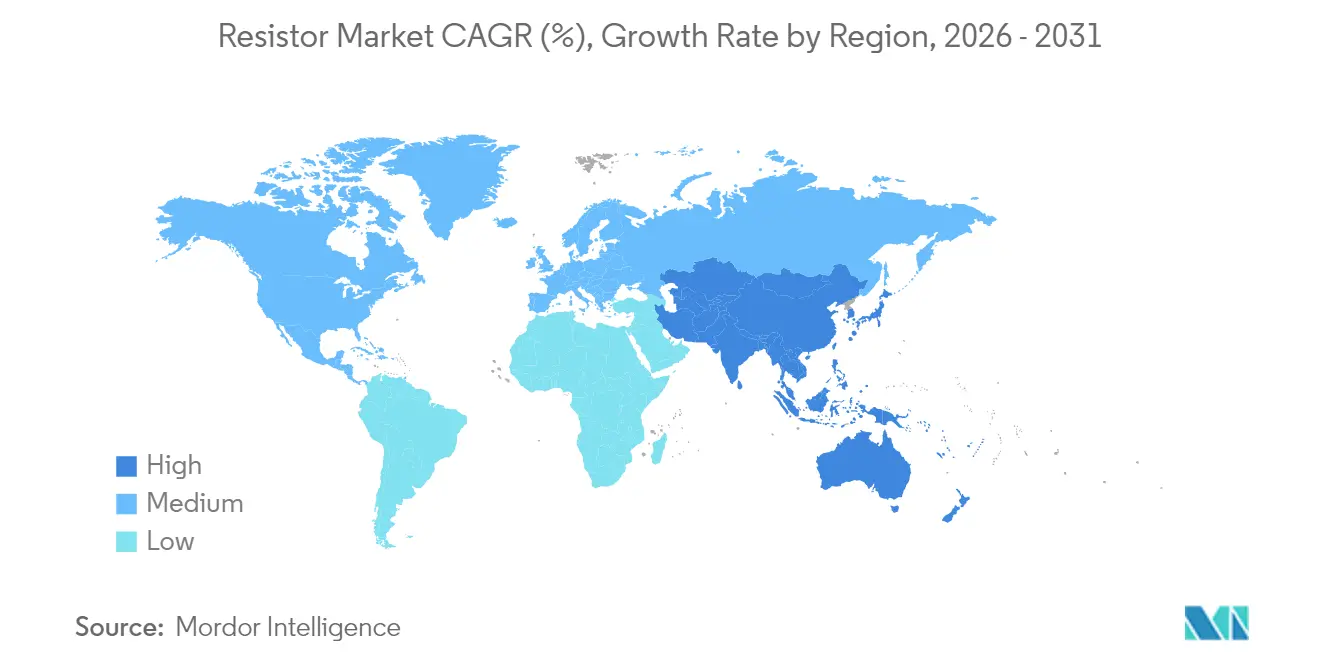

- By geography, Asia-Pacific captured 55.42% revenue share in 2025 and will progress at a 5.62% CAGR through 2031 in the resistor market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Resistor Market Trends and Insights

Driver Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Expanding automotive electronics content per vehicle | +1.2% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Growth in consumer electronics and IoT device volumes | +0.9% | Global, Asia-Pacific manufacturing hubs | Short term (≤ 2 years) |

| Rising adoption of 5G infrastructure and high-frequency applications | +0.7% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Miniaturization trend driving demand for surface-mount chip resistors | +0.6% | Global, Asia-pacific manufacturing | Long term (≥ 4 years) |

| Integration of resistive sensing in EV fast-charging BMS | +0.4% | Global EV markets | Medium term (2-4 years) |

| Precision resistors for quantum-computing hardware | +0.1% | North America and Europe research hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expanding Automotive Electronics Content Per Vehicle

Electric and hybrid vehicles now embed hundreds of discrete shunt components that measure currents up to 2,500 A with micro-ohm precision, pushing demand for AEC-Q200 qualified metal-element devices able to operate up to 170 °C.[1]Source: Isabellenhütte, “EV Shunt Resistors Technical Article,” isabellenhuetteusa.com As OEMs migrate to 48-V architectures and software-defined control systems, the Resistor market gains volume upside from battery-management, ADAS, and traction-inverter boards. Precision drift specifications below ±15 ppm/°C ensure charge-state accuracy throughout the drivetrain’s lifetime, while rugged terminations mitigate vibration stress. Design wins in this space typically last a full model cycle, strengthening visibility for suppliers that meet stringent zero-defect targets. In parallel, charging-station manufacturers specify high-power thick-film units rated up to 150 W to throttle surge energy and prevent thermal runaway.[2]Source: Vishay Intertechnology, “CHA Series Thin-Film Chip Resistors,” vishay.com Collectively, the electrification wave adds resilient, multi-year revenue layers to the resistor market.

Growth in Consumer Electronics and IoT Device Volumes

Smartphones, wearables, and smart-home nodes continue to migrate from 0603 to 0402 and 0201 footprints, compressing real estate by up to 65% without sacrificing performance. Compact packaging raises placement accuracy demands, spurring capex for high-speed pick-and-place machines across contract manufacturers. The Resistor market thus pivots to ultra-miniature formats with ±0.1% tolerance and low TCR to satisfy high-resolution ADC front ends in edge devices. Volume scale for connected sensors drives long production runs, letting vendors amortize tooling and counterbalance wafer-thin margins. Design engineers also prize halogen-free, RoHS-compliant bill-of-materials to align with brand sustainability goals, indirectly boosting differentiated thin-film offerings. Together, these factors lift shipment tonnage even as ASPs fall, sustaining topline momentum for the resistor market.

Rising Adoption of 5G Infrastructure and High-frequency Applications

Millimeter-wave base-station radios require termination networks that maintain impedance stability up to 50 GHz; thin-film chip resistors address this need with alumina substrates and NiCr resistive elements. Migration from 4G to 5G triggers wholesale board redesigns, creating sizable replacement demand for certified passives. Small-cell deployments multiply node counts, expanding the dollar opportunity per square-kilometer served. Power-amplifier linearization further elevates resistor power-handling thresholds, driving innovation in heat-spreader geometries. Telco OEMs award supply contracts only to vendors maintaining multi-site redundancy and ISO/TS 16949 quality, a barrier that narrows field competition and supports price premiums. Consequently, high-frequency rollouts supply a dedicated growth pocket within the broader resistor market.

Miniaturization Trend Driving Demand for Surface-mount Chip Resistors

Next-generation PCB stack-ups adopt high-density interconnect traces below 75 µm, compelling the use of 0201 and emerging 01005 components to maintain signal fidelity. Chip formats reduce parasitic inductance, bolstering high-speed data paths inside smartphones and notebooks. Manufacturers exploit sputtered thin-film processes to secure ≤±0.05% tolerance, supporting precision voltage-divider networks in analog front ends. Shrinkage intensifies metrology challenges, as optical-inspection resolution must keep pace with part size. Consequently, capital expenditure in 2D/3D AOI and X-ray tomography scales in lockstep, embedding additional cost in the value chain. Even so, miniaturization remains an irreversible driver, ensuring long-run elasticity for the resistor market.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Volatility in metal prices (Ni, Pd) is inflating production costs | -0.8% | Global, Asia-Pacific manufacturing | Short term (≤ 2 years) |

| Passive-component supply-chain disruptions | -0.6% | Global, Asia-Pacific hubs | Short term (≤ 2 years) |

| Stricter halogen-free material regulations are raising compliance costs | -0.3% | Europe and North America | Medium term (2-4 years) |

| Integrated passive devices reducing discrete-resistor content | -0.4% | Global, high-volume electronics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Metal Prices Inflating Production Costs

Nickel and palladium feedstock account for up to 25% of variable cost for thin-film chip resistors; spot-price swings exceeding 40% within a quarter compress gross margins for fabricators unless shielded by long-term contracts.[3]Source: Ram Alloys, “Nickel Surcharge Update,” ramalloys.com Hedging strategies partially offset the impact, yet tie up working capital, straining smaller vendors. Price passthrough to OEMs faces resistance amid competitive bidding, prompting substitution toward manganese-based alloys whenever tolerance windows permit. Such volatility weighs on near-term profitability across the resistor market.

Integrated Passive Devices Reducing Discrete-Resistor Content

High-density system-in-package modules now embed resistive, capacitive, and inductive elements on a single glass or silicon substrate, saving board space and simplifying assembly for flagship smartphones. Although discrete solutions remain cost-effective for lower-volume SKUs, IPD penetration in multibillion-unit programs lowers unit demand projections for commodity thick-film resistors. Suppliers therefore pivot toward high-mix, high-margin sectors such as automotive, industrial, and medical where customization needs shield the Resistor market from full displacement.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Surface-Mount Dominance Drives Miniaturization

Surface-mount chip formats generated the largest slice of the resistor market at 38.22% revenue share in 2025, underpinned by automated placement rates surpassing 110,000 components per hour. The segment’s scale economies enable price points below USD 0.0002 per 0603 part, widening use across mass-market devices. At the same time, shunt and current-sense families expand quickest at a 6.49% CAGR, leveraging rising electric-vehicle penetration.

Heightened functional density encourages migration toward 0201 and 01005 footprints, with leading subcontractors upgrading feeders and vision systems to achieve ±15 µm placement accuracy. Yet demand for wirewound and foil technologies persists where power dissipation and ultra-low inductance trump size, notably in industrial inverters and radar systems. Thick-film network arrays secure sockets in routers and base stations, thanks to matched resistor ratios up to 0.05%. Diversified use-cases maintain a balanced growth profile, allowing the Resistor market to hedge against over-reliance on any single form factor.

By Power Rating: High-Power Applications Accelerate Growth

Resistors exceeding 5 W constitute the fastest-rising slice of the Resistor market, slated for a 6.67% CAGR through 2031 as grid-scale storage, fast-charging piles, and renewable-energy converters proliferate. Bulk-metal and thick-film solutions dissipating up to 150 W manage transients during load-dump events, reducing module failure rates. Conversely, sub-1/8-W chips still dominate shipment volume, reflecting continued smartphone and wearable demand; within the resistor market share hierarchy, this low-power bracket held 39.74% in 2025.

Thermal-interface improvements such as direct-bonded-copper substrates and molded epoxy housings enhance derating curves, enabling OEMs to shrink system footprints while elevating performance. Mid-range 1-5 W resistors cater to industrial drives and telecom rectifiers that need moderate power with tight tolerance.

By End-User Industry: Automotive Transformation Drives Growth

Automotive use-cases are expected to post the highest 6.74% CAGR, lifting their contribution within the resistor market. High-voltage battery modules require Kelvin-sensed shunts capable of 0.2% tolerance across temperature swings, while zonal E/E architectures introduce numerous sense-line resistors to monitor subsystem loads. Consumer electronics remains the largest volume consumer, representing 36.80% share, buoyed by sustained smartphone replacement cycles and emerging XR headsets.

Industrial automation and instrumentation demand high-stability foil resistors with ±2 ppm/°C TCR for precision process control. Aerospace and defense segments rely on hermetically sealed wirewounds that comply with MIL-PRF-55342, although order flow depends on program funding cycles. Medical-device OEMs increasingly specify biocompatible, moisture-resistant thin-films for implantable telemetry modules, a specialized niche supporting healthy margins. Together, this diversified user base underpins resilience across the broader resistor market.

Geography Analysis

Asia-Pacific dominates the resistor market, commanding 55.42% revenue in 2025 thanks to vertically integrated electronics manufacturing clusters spanning Shenzhen, Hsinchu, and Kansai. Regional leaders Yageo, Walsin, and TA-I continue to add capacity, leveraging preferential utility rates and mature subcontracting ecosystems. As production scales, local foundries supply sputtered NiCr films and alumina substrates, closing material loopbacks and lowering cycle times. Simultaneously, governments in Japan and South Korea channel research and development grants toward automotive-grade passives to bolster export competitiveness.

North America captured 17.45% of the resistor market size in 2025, anchored by aerospace, defense, and medical device contracts that favor high-reliability foil and wirewound types. The CHIPS and Science Act’s incentives stimulate domestic substrate and thick-film ink production, gradually shortening supply lines. Europe is progressing toward halogen-free mandates; resistor vendors respond with green-polymer encapsulation and lead-free solderable endcaps. Germany and France spearhead investment in EV charging infrastructure, giving a lift to high-power resistor demand.

Emerging economies in Latin America and Africa jointly account for less than 5% of global revenue yet post above-average growth as telecom operators extend 5G footprints and industrial automation gains traction. Middle East participation centers on smart grid rollouts and petrochemical instrumentation, where harsh-environment resistors fetch premium ASPs. These developments illustrate the geographic breadth sustaining long-run expansion of the resistor market.

Competitive Landscape

Moderate concentration characterizes the resistor market, with significant players such as Vishay Intertechnology, Panasonic Industry, and Yageo. Yageo’s USD 740 million acquisition of Pulse Electronics widened its automotive sensor portfolio and shows a sustained appetite for inorganic growth. Vishay committed to multi-site redundancy by commissioning a Ciudad Juárez factory in 2025, boosting North American capacity and diversifying seismic risk. Panasonic continues to commercialize conductive-polymer thick-film pastes that promise 15% better pulse handling, targeting EV brake-chopper circuits.

Smaller Asian contenders such as ROYALOHM and Firstohm differentiate through turnkey ODM services, winning business from consumer-electronics ODMs seeking rapid spin cycles. Western niche specialists, including VPG Foil Resistors, dominate ultrahigh-precision foil segments at TCR values down to 0.05 ppm/°C, catering to metrology and quantum-computing researchers.[5]Source: ES Components, “VPG Foil Resistors,” escomponents.com Cost-centric buyers, however, continue to source commodity chips from large Taiwanese fabs able to deliver billion-unit lots with six-week lead times. Overall, rivalry revolves around technology, quality certification breadth, and continuity of supply, keeping the resistor market dynamic and innovation-oriented.

Resistor Industry Leaders

-

Vishay Intertechnology, Inc.

-

Yageo Corporation

-

Murata Manufacturing Co., Ltd.

-

Panasonic Holdings Corporation (Panasonic Industry)

-

KOA Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Yageo announced a tender offer to acquire Shibaura Electronics, expanding its thermistor and sensor footprint.

- January 2025: onsemi completed the USD 115 million purchase of Qorvo’s SiC JFET business, broadening its power-semiconductor reach.

- September 2024: Vishay closed three resistor factories in restructuring moves intended to save USD 23 million annually.

- August 2024: Delta Electronics bought Alps Alpine’s power-inductor assets for USD 71 million, reinforcing next-generation passive component capabilities.

Global Resistor Market Report Scope

A resistor is a passive electronic component that helps control the flow of electrical current in an electronic circuit. It is commonly utilized in various ways, such as reducing current flow, adjusting signal levels, dividing voltages, biasing active elements, and terminating transmission lines.

The resistor market is segmented by type (surface-mounted chips, network, wirewound, film/oxide/foil, and carbon), by end-user industry (automotive, aerospace and defense, communications, consumer electronics and computing, and other end-user industries), by geography (North America, Europe, Asia-Pacific, Rest of the World). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Surface-Mount Chip Resistors |

| Network / Array Resistors |

| Wirewound Resistors |

| Film / Foil / Oxide Resistors |

| Carbon Composition / Thick-Film Resistors |

| Variable Resistors (Potentiometers, Rheostats) |

| Shunt and Current-Sense Resistors |

| < 1/8 W |

| 1/8 – 1 W |

| 1 – 5 W |

| > 5 W (High-Power) |

| Automotive |

| Aerospace and Defense |

| Telecommunications and Data Infrastructure |

| Consumer Electronics and Computing |

| Industrial Automation and Instrumentation |

| Medical Devices |

| Energy and Power |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Type | Surface-Mount Chip Resistors | ||

| Network / Array Resistors | |||

| Wirewound Resistors | |||

| Film / Foil / Oxide Resistors | |||

| Carbon Composition / Thick-Film Resistors | |||

| Variable Resistors (Potentiometers, Rheostats) | |||

| Shunt and Current-Sense Resistors | |||

| By Power Rating | < 1/8 W | ||

| 1/8 – 1 W | |||

| 1 – 5 W | |||

| > 5 W (High-Power) | |||

| By End-User Industry | Automotive | ||

| Aerospace and Defense | |||

| Telecommunications and Data Infrastructure | |||

| Consumer Electronics and Computing | |||

| Industrial Automation and Instrumentation | |||

| Medical Devices | |||

| Energy and Power | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the global resistor market?

The market is valued at USD 11.10 billion in 2026 and is projected to reach USD 14.19 billion by 2031.

Which geographic region leads resistor production?

Asia-Pacific holds 55.42% of global revenue thanks to its dense electronics manufacturing ecosystem.

Why are high-power resistors growing faster than low-power categories?

Electrification of vehicles and expansion of renewable-energy converters require devices above 5 W, driving a 6.67% CAGR for this segment.

How will integrated passive devices impact discrete resistor demand?

IPDs may reduce chip counts in flagship consumer devices, but automotive, industrial, and medical sectors still rely on discrete resistors for customization and cost efficiency.

Page last updated on: