Specimen Validity Testing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.49 Billion |

| Market Size (2031) | USD 3.41 Billion |

| Growth Rate (2026 - 2031) | 6.47% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Specimen Validity Testing Market Analysis by Mordor Intelligence

The specimen validity testing market size is expected to grow from USD 2.34 billion in 2025 to USD 2.49 billion in 2026 and is forecast to reach USD 3.41 billion by 2031 at 6.47% CAGR over 2026-2031. The trajectory reflects tightening workplace-safety mandates, accelerated adoption of point-of-care (POC) testing platforms, and technology upgrades that detect sophisticated adulteration attempts. Employers in transportation, energy, and healthcare continue to widen testing coverage, while government updates—such as the January 2025 federal panel expansion that now includes fentanyl and norfentanyl—raise the integrity bar for all laboratories. Rising telehealth use has also opened a new remote-collection channel, prompting demand for tamper-evident devices and AI-driven analytics that verify specimen integrity in real time. Although non-urine matrices are gaining favor, the specimen validity testing market remains buoyed by high-volume urine programs that still dominate regulated settings.

Key Report Takeaways

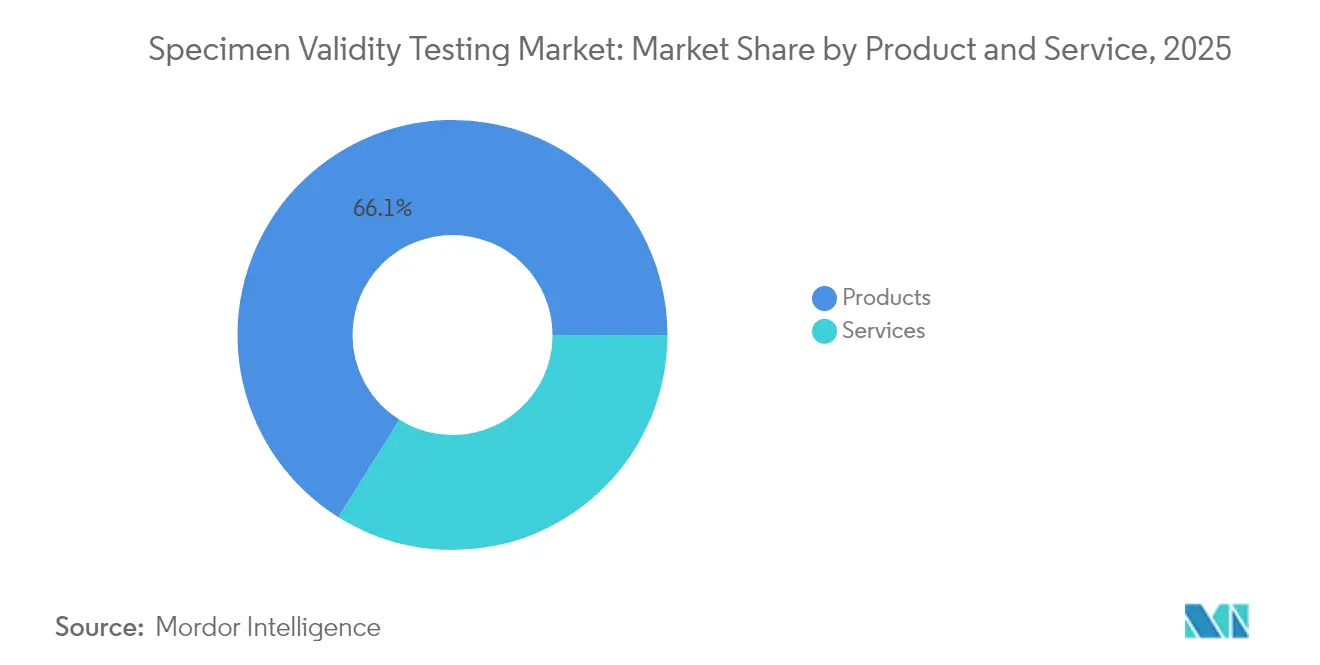

- By product & service, consumable products maintained 66.10% revenue share in 2025, whereas services are forecast to post the fastest 7.12% CAGR through 2031.

- By type, laboratory testing held 59.10% of the specimen validity testing market share in 2025, while POC platforms are slated to expand at a 7.18% CAGR to 2031.

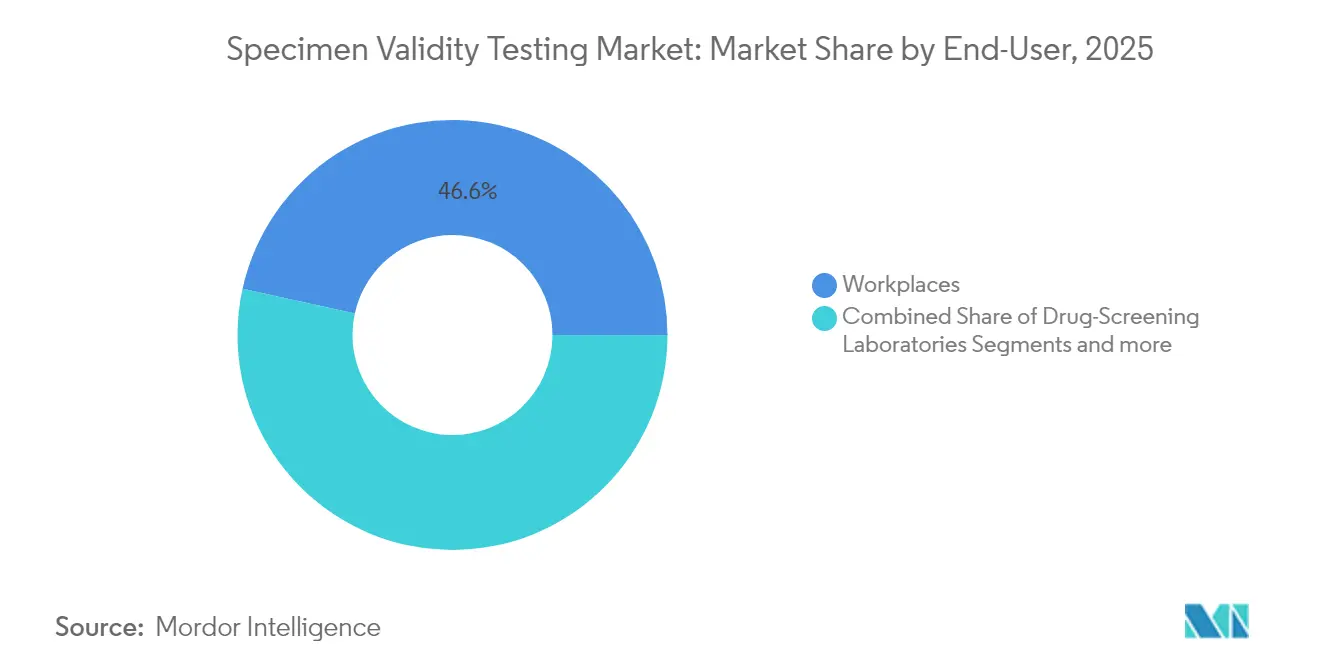

- By end-user, workplace programs led with 46.55% revenue share in 2025; drug-screening laboratories record the highest projected 7.22% CAGR through 2031.

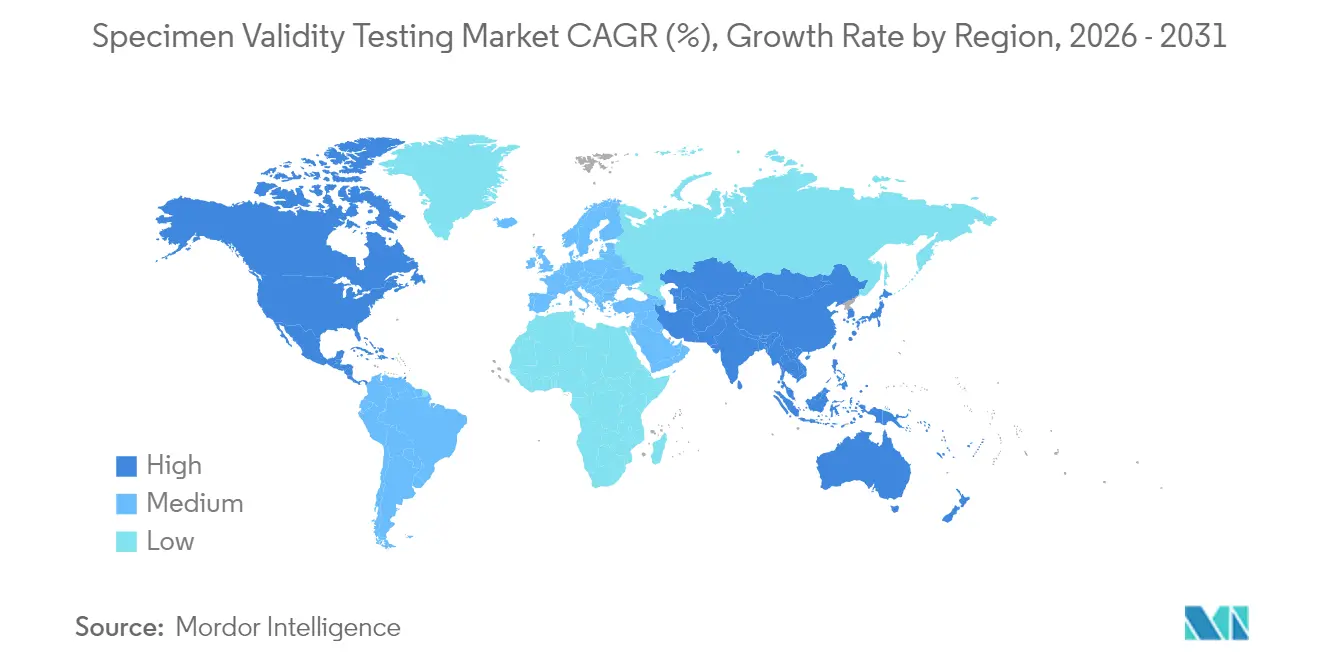

- By geography, North America commanded 41.00% share of the specimen validity testing market size in 2025; Asia-Pacific is set to grow at a 7.30% CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Specimen Validity Testing Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing workplace drug-testing mandates | +1.2% | Global, concentrated in North America & EU | Medium term (2-4 years) |

| Rapid adoption of POC SVT devices | +0.9% | North America & Asia-Pacific | Short term (≤ 2 years) |

| Telehealth expansion spurring at-home kits | +0.7% | North America & EU | Medium term (2-4 years) |

| Machine-learning algorithms for live adulteration detection | +0.6% | Global, led by North America | Long term (≥ 4 years) |

| Cannabis legalization driving differentiated panels | +0.5% | North America, spreading to EU | Short term (≤ 2 years) |

| Supply-chain security boosting sterile controls | +0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Workplace Drug-Testing Mandates

Regulators on six continents are strengthening corporate safety rules, pushing employers to verify not only drug presence but the authenticity of each sample. OSHA-aligned directives in the United States, Canada’s Transportation of Dangerous Goods Regulations, and the Oman Ministry of Manpower’s compulsory oil-and-gas testing order underscore a collective move toward stricter specimen validity checks. Large conglomerates increasingly embed chain-of-custody software and Medical Review Officer (MRO) oversight into standard operating procedures, mitigating litigation risk after accidents. The resulting demand multiplier lifts recurring sales of temperature strips, oxidant assays, and digital custody systems [1]General Civil Aviation Authority, "ACCEPTABLE MEANS OF COMPLIANCE," gcaa.gov.ae.

Rapid Adoption of POC SVT Devices

Newly cleared handheld analyzers now complete adulterant screens in under six minutes, meeting the “immediacy” standard required in post-incident investigations. U.S. Food and Drug Administration (FDA) clearance for on-site fentanyl assays has set a precedent for integrating validity checks into single-step POC cups. Employers value reduced downtime, while laboratories see fewer rejected samples, shortening billing cycles. Vendors respond with modular readers that print compliance-ready reports, reinforcing recurring consumable revenues.

Telehealth Expansion Spurring At-Home SVT Kits

Remote management of opioid-dependence and pain-management patients demands self-collection kits that guard against substitution. Academic trials show over 80% completion rates for remote urine submissions when validity parameters—temperature, pH, creatinine—are built into collection devices. Health insurers now require documentary proof of validity before reimbursing high-complexity codes, driving clinics to adopt tamper-evident transport tubes and Bluetooth temperature sensors.

Machine-Learning Algorithms for Live Adulteration Detection

Research laboratories deploy deep-learning models that compare time-series spectra, flagging anomalies impossible to see through single-parameter assays. Early validation studies achieve 95%+ accuracy in identifying synthetic urine or oxidant spikes. Commercial rollout is poised to cut false-negative rates and ease the interpretation burden on MROs, giving suppliers of compatible mass-spectrometry reagents a competitive edge [2]Yi-Ching Lin, "PS2MS: A Deep Learning-Based Prediction System for Identifying New Psychoactive Substances Using Mass Spectrometry," ACS Publications, pubs.acs.org.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited awareness among small & mid-size clinics | -0.8% | Global, more acute in Asia-Pacific & MEA | Short term (≤ 2 years) |

| Shift toward non-urine matrices | -0.6% | North America & EU | Medium term (2-4 years) |

| Data-privacy constraints on biometric platforms | -0.4% | EU & North America | Long term (≥ 4 years) |

| Sporadic reagent shortages & raw-material spikes | -0.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Limited Awareness Among Small & Mid-Size Clinics

Smaller healthcare providers often underestimate liability tied to invalid samples. Surveys highlight that 59% of point-of-care implementation barriers relate to training and quality assurance, leaving many clinics without temperature verification or specific-gravity checks. Reimbursement policies now deny claims lacking validity documentation, but knowledge gaps persist, slowing uptake [3]Blue Cross Blue Shield of Michigan, "Drug Testing in Pain Management and Substance Use Disorder Treatment," bcbsm.com.

Shift Toward Non-Urine Matrices Reducing SVT Demand

Federal authorization of oral-fluid testing for government employees has prompted private firms to adopt saliva as a primary matrix, which lowers adulteration risk and thus the need for multi-parameter urine validity panels. Forecasts suggest 30% of federally regulated tests could migrate to oral fluid within four years, trimming growth potential for urine-focused consumables.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product & Service: Products Retain Scale, Services Accelerate

Products anchored 66.10% of 2025 revenue, sustained by the consumable nature of assay kits, oxidant reagents, creatinine standards, and single-use collection cups. Temperature-indicator strips alone generated a high-velocity replacement cycle, especially in large logistics and energy enterprises. Services, however, post a 7.12% CAGR through 2031 as employers outsource result interpretation and compliance audits to MRO consultants and specialty laboratories. Medical-legal environments favor bundled offerings that merge chain-of-custody management with machine-learning analytics. The specimen validity testing market size for services is forecast to reach USD 1.2 billion by 2031, maintaining momentum despite the dominance of consumables.

The services wave also rides on remote-collection medicine. Telehealth platforms contract third-party labs to verify sample temperature and oxidant levels on arrival, paying premium fees for same-day adjudication. Demand spikes for virtual MRO reviews in cross-border employment programs, broadening addressable revenue and solidifying the specimen validity testing market as a holistic solution rather than a product vertical alone.

By Type: Laboratory Testing Dominant, POC Gains Speed

Laboratory workflows held 59.10% share in 2025. Centralised labs wield liquid-chromatography tandem mass-spectrometry (LC-MS/MS) systems that analyse temperature, specific gravity, creatinine, pH, and oxidants with regulatory precision. That infrastructure underpins the specimen validity testing market share leadership of large reference laboratories. Yet POC formats advance 7.18% CAGR, propelled by portable photometers and immunochromatographic cups that cross-check three or more validity parameters in minutes. The specimen validity testing market size tied to POC platforms is expected to climb to USD 1.45 billion by 2031 as device accuracy approaches lab standards.

High-risk sectors such as construction now deploy ruggedised POC analyzers at job sites for post-incident testing, curbing downtime. Meanwhile, hybrid models see specimens first screened by POC devices and only positives—together with any flagged validity anomalies—sent to labs, optimising workload distribution.

By End-User: Workplaces Lead, Laboratories Accelerate

Corporate programs accounted for 46.55% of 2025 revenue, cementing their role as the primary consumer of validity consumables. Transportation, oil and gas, and public sector employers maintain mandatory pre-employment and random testing, ensuring steady volume. Drug-screening laboratories rise fastest at 7.22% CAGR, mirroring consolidation that pulls smaller clinic volumes into high-throughput hubs.

Pain-management clinics, under payer scrutiny, increasingly outsource to specialised facilities capable of furnishing comprehensive validity metrics. Criminal-justice agencies, another critical niche, demand chain-of-custody traceability and have begun requesting machine-readable temperature logs, deepening the role of advanced validity platforms.

Geography Analysis

North America retained 41.00% revenue in 2025 and remains regulatory pacesetter for the specimen validity testing market. The Department of Health and Human Services requires each regulated urine specimen to document temperature (32-38 °C), pH (4.5-8.0), specific gravity (≥1.003), and creatinine (≥20 mg/dL) immediately after collection SAMHSA. The January 2025 panel revision, which added fentanyl and norfentanyl, further heightened laboratories’ need for precise validity confirmation to avoid false negatives under new analyte cutoffs Federal Register. Parallel Department of Transportation mandates apply to roughly 10 million safety-sensitive workers, guaranteeing high test volumes. Canada’s privacy-oriented framework reduces random testing but emphasises oral-fluid programs that still rely on temperature and chain-of-custody documentation for defensibility.

Asia-Pacific posts the fastest 7.30% CAGR through 2031, propelled by multinational factories in China and India that embed U.S. Occupational Safety and Health Administration (OSHA) best practices into local operations. Global diagnostic giants have opened regional hubs to supply assay kits and provide MRO services in native languages. Cross-border trade compliance drives companies to adopt U.S.-style chain-of-custody systems, giving the specimen validity testing market fresh scale. Regional governments are studying mandatory drug-testing statutes, particularly in transportation and mining, which would further embed specimen integrity checks.

Europe offers fragmented regulation. German rail operators apply stringent specimen-validity rules modelled on U.S. federal guidelines, whereas France limits testing to safety-sensitive roles and imposes stricter privacy filters. The EU’s In Vitro Diagnostic Regulation (IVDR) imposes performance and post-market surveillance obligations on validity devices entering the bloc, raising entry barriers yet standardising quality. Pan-European employers thus lean toward CE-marked collection systems that integrate barcoded integrity seals and cloud custody logs.

The Middle East and Africa follow international oil-and-gas contracting standards. GCC aviation regulators require MRO-overseen validity checks, with chain-of-custody protocols mirroring U.S. SAMHSA guidelines. South Africa’s mining houses partner with global laboratories to meet buyer expectations for high-integrity testing metrics. South America is led by Brazil, where Law 13.103/15 compels professional drivers to undergo periodic toxicological assessments that include specimen validity documentation; hair testing’s popularity nonetheless demands cross-validation protocols to confirm authenticity. Argentina’s expanding automotive sector imports U.S. DOT guidelines to satisfy supply-chain partners.

Competitive Landscape

The specimen validity testing market features moderate fragmentation. Abbott, Thermo Fisher Scientific, Laboratory Corporation of America, Quest Diagnostics, and Siemens Healthineers collectively account for a decent portion of the global revenue. Scale advantages stem from integrated assay-to-analytics portfolios and extensive logistics networks. Abbott’s iCUP platform now embeds real-time temperature monitoring and oxidant strips, bundling validity with rapid drug screens Abbott. Quest Diagnostics has expanded its international footprint to 80+ nations, offering cloud-based chain-of-custody dashboards that streamline multinational compliance Quest Diagnostics.

Technology differentiation drives current competition. Partnerships between reference labs and AI vendors deliver machine-learning adulteration classifiers, raising service stickiness. Siemens Healthineers pilots cloud-linked mass-spectrometry workflows that flag atypical creatinine-to-specific-gravity ratios in near-real-time, cutting report burdens on MROs. Meanwhile, specialty suppliers such as Labcon emphasise medical-grade, IATA-compliant collection cups, addressing supply-chain sterility concerns Labcon.

Start-ups focus on saliva and microsampling innovations—areas poised to erode urine volumes yet still require proof of donor identity and sample integrity. Incumbents hedge by acquiring or licensing these technologies, maintaining revenue irrespective of matrix shifts. Regional providers in Asia-Pacific court multinational contracts by offering bilingual MRO support and turnkey cloud tracking, challenging North American dominance.

Specimen Validity Testing Industry Leaders

-

Abbott

-

Thermo Fisher Scientific

-

LabCorp

-

Healgen Scientific LLC

-

Premier Biotech, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: The U.S. Department of Health and Human Services updated Mandatory Guidelines, adding fentanyl and norfentanyl while removing MDMA and MDA, compelling laboratories to adjust validity workflows Federal Register.

- December 2024: BD and Babson Diagnostics introduced capillary-blood microsampling technology, expanding validity-testing concepts into small-volume blood collection BD.

- August 2024: FDA cleared the first POC fentanyl urine screen on the RYAN analyzer, catalysing on-site validity verification FDA.

- February 2024: SAMHSA released a revised Urine Specimen Collection Handbook detailing updated validity thresholds and adulteration-detection steps SAMHSA.

Global Specimen Validity Testing Market Report Scope

As per the scope of the report, specimen validity testing (SVT) is the screening test for urine samples to detect any adulteration, dilution, or substitution. SVT provides critical information regarding the reliability and accuracy of drug test results to clinicians, and it also validates that the urine sample tested is a valid human urine specimen. The specimen validity testing market is segmented by drug type (antibacterial drugs, anti-fungal drugs, antiviral drugs, and other drugs), indication (bloodstream infections, urinary tract infections, surgical site infections, pneumonia, and other indications), and geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| Products | Assay Kits |

| Reagents & Calibrators | |

| Disposables | |

| Services |

| Laboratory Testing |

| Rapid and POC Testing |

| Workplaces |

| Law-Enforcement and Criminal-Justice Systems |

| Drug-Screening Laboratories |

| Pain-Management Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product and Service | Products | Assay Kits |

| Reagents & Calibrators | ||

| Disposables | ||

| Services | ||

| By Type | Laboratory Testing | |

| Rapid and POC Testing | ||

| By End-User | Workplaces | |

| Law-Enforcement and Criminal-Justice Systems | ||

| Drug-Screening Laboratories | ||

| Pain-Management Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the specimen validity testing market?

The specimen validity testing market size stands at USD 2.49 billion in 2026 and is projected to reach USD 3.41 billion by 2031.

Which region dominates the specimen validity testing market?

North America leads with 41.00% revenue share in 2025 due to stringent federal workplace requirements.

Why are services growing faster than products?

Rising protocol complexity, remote testing, and the need for expert Medical Review Officer interpretation are driving a 7.12% CAGR for services.

How is AI influencing specimen validity testing?

Machine-learning models now detect sophisticated adulteration patterns with 95%+ accuracy, enhancing laboratory reliability and competitive differentiation.

What impact do non-urine matrices have on market growth?

The shift toward oral fluid and hair testing reduces demand for traditional urine validity consumables but opens opportunities for new integrity verification tools tailored to alternative matrices.

Which end-user segment is expanding most rapidly?

Drug-screening laboratories, buoyed by consolidation and outsourcing trends, are set to grow at a 7.22% CAGR through 2031.

Page last updated on: