Power Management Integrated Circuit (PMIC) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 44.72 Billion |

| Market Size (2031) | USD 63.69 Billion |

| Growth Rate (2026 - 2031) | 7.33% CAGR |

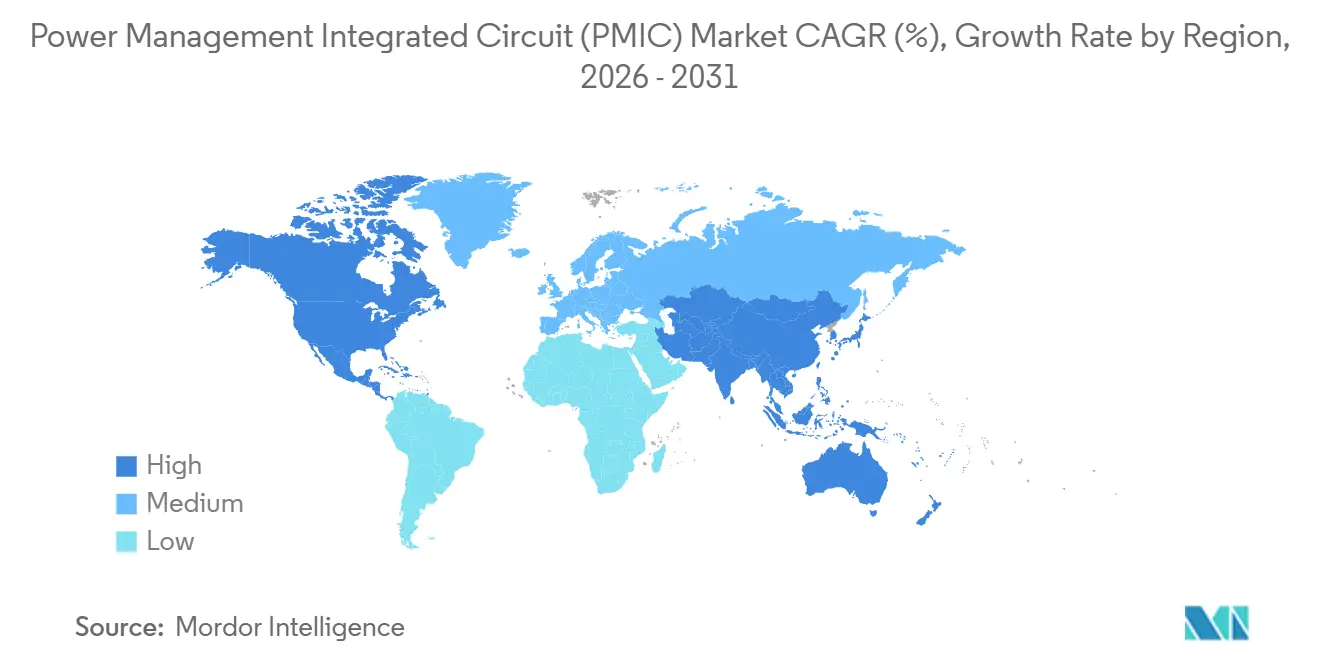

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Power Management Integrated Circuit (PMIC) Market Analysis by Mordor Intelligence

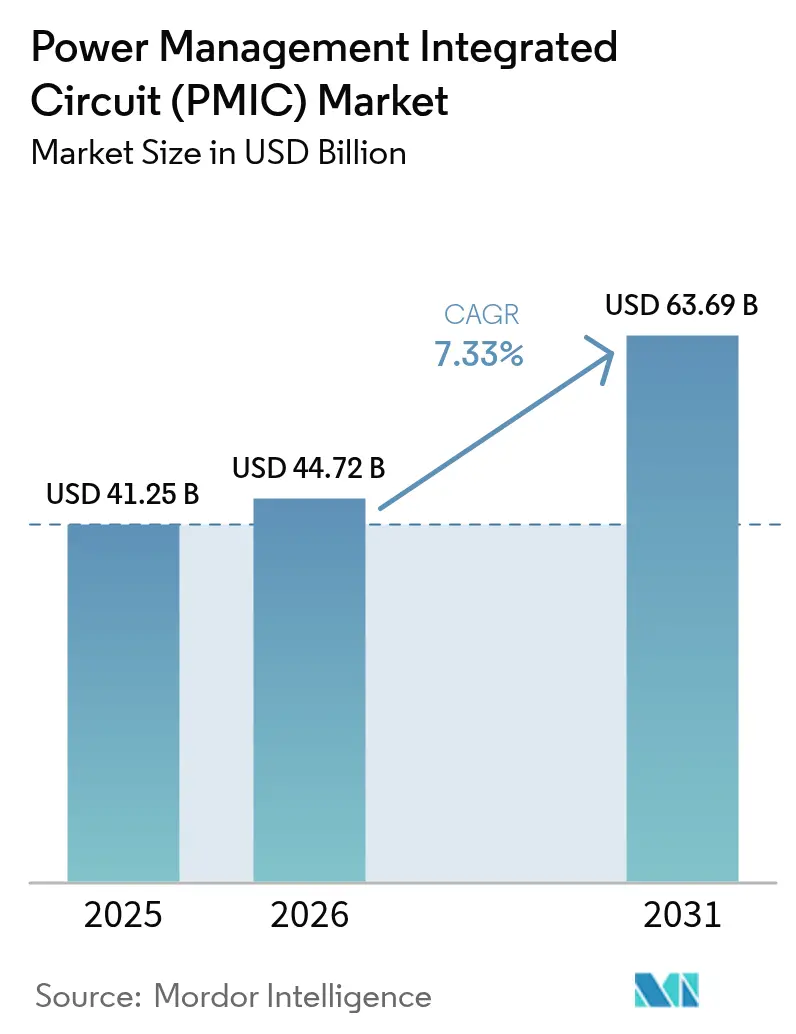

The Power management integrated circuit (PMIC) market size is projected to expand from USD 41.25 billion in 2025 and USD 44.72 billion in 2026 to USD 63.69 billion by 2031, registering a CAGR of 7.33% between 2026 to 2031. Growth is gaining momentum as electrification mandates, edge-computing roll-outs, and migration below 20-nanometer nodes reshape power-delivery architectures across automotive, consumer, and industrial platforms. Demand for programmable PMIC firmware, which allows over-the-air power optimization, is fragmenting the value chain and shortening design cycles. Analog incumbents are investing in 300-millimeter capacity to defend gross margins, while fabless specialists leverage outsourced foundry access to deliver application-specific devices in six to nine months. Sub-20-nanometer integration supports on-die voltage regulation for graphics processors that already exceed 600-watt thermal-design power, and silicon-carbide adoption in 800-volt electric vehicles is lifting current-handling requirements above 300 amperes per module. Supply-chain cyclicality remains a headline risk but foundry lead times moderated from 26 weeks in early 2025 to 18 weeks by year-end, easing the near-term constraint on the Power management integrated circuit (PMIC) market.

Key Report Takeaways

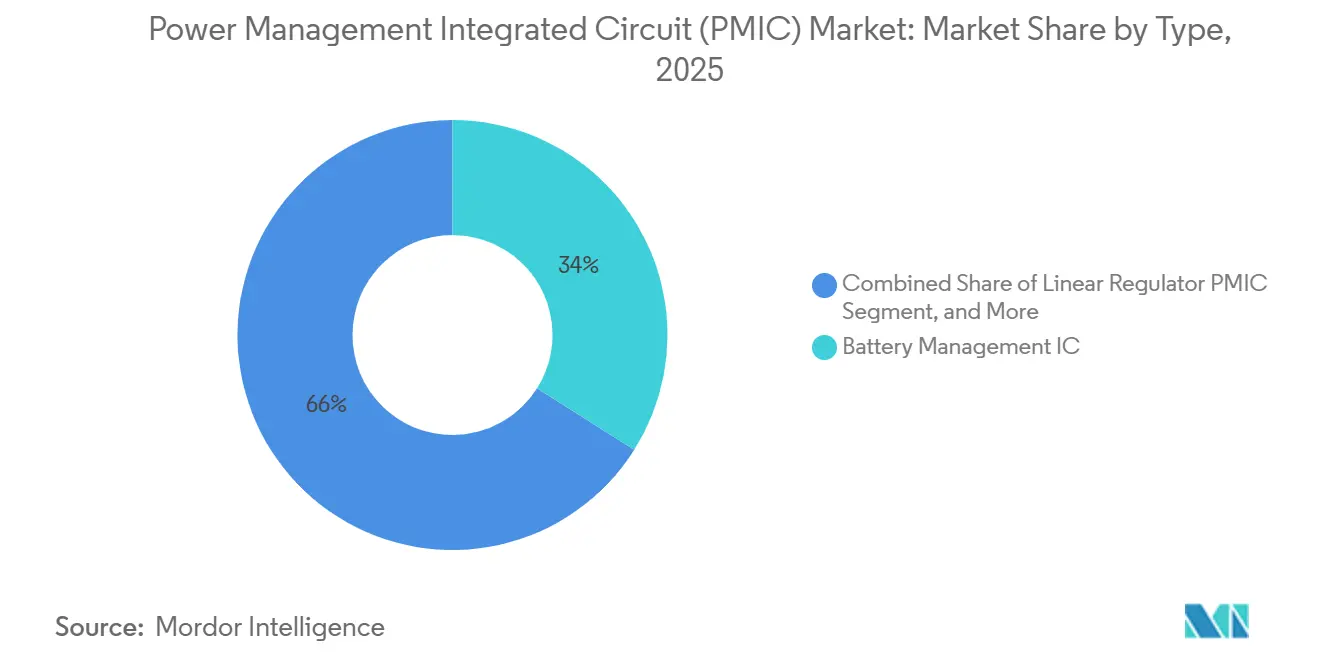

- By IC type, Battery Management ICs led with 33.96% of Power management integrated circuit market share in 2025, while the same segment is also forecast to grow fastest at a 9.83% CAGR through 2031.

- By application, Consumer Electronics held 41.23% revenue share in 2025 and Automotive plus e-Mobility is advancing at the highest 9.37% CAGR through 2031.

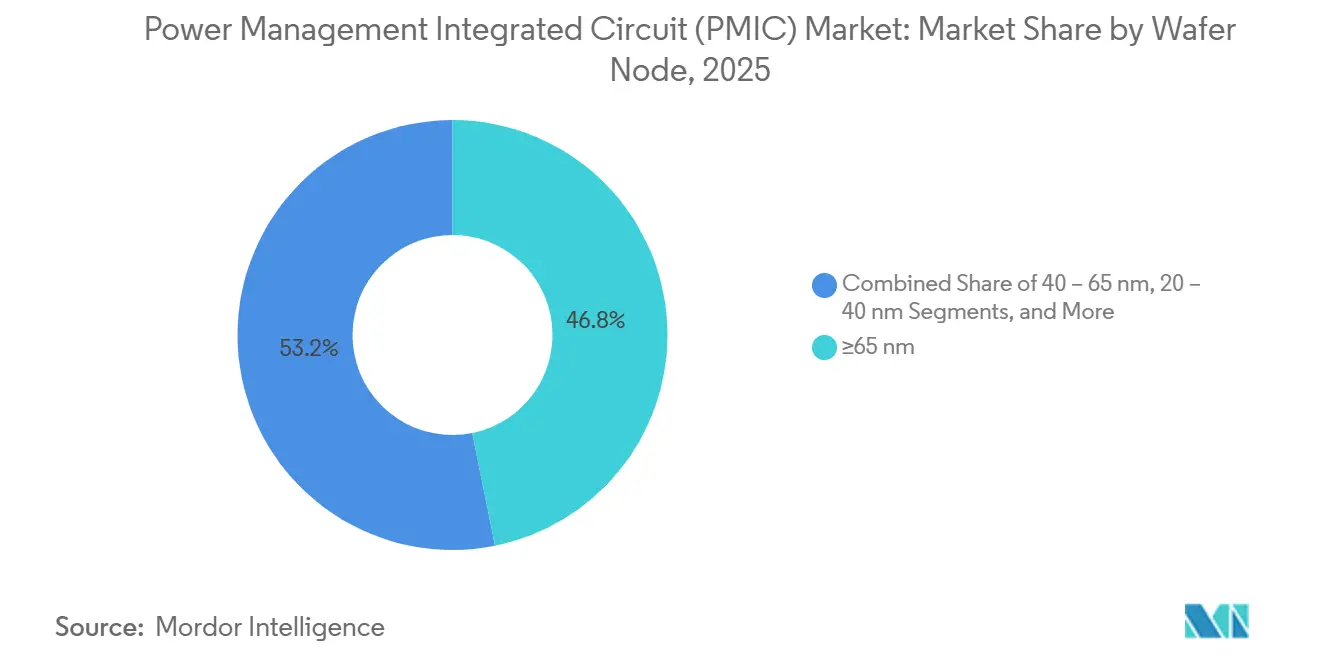

- By wafer node, processes at or above 65 nanometers accounted for 46.84% share of the Power management integrated circuit market size in 2025, whereas sub-20-nanometer nodes are set to expand at an 8.48% CAGR to 2031.

- By power range, Low-power devices captured 49.94% of 2025 revenue and High-power PMICs are projected to climb at an 8.39% CAGR over the forecast horizon.

- By geography, Asia-Pacific commanded 44.23% of 2025 revenue and the Middle East is the fastest-growing region at an 8.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Power Management Integrated Circuit (PMIC) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid EV and xEV penetration elevating demand for high-current, high-efficiency PMICs | +2.1% | Global, with concentration in China, Europe, North America | Medium term (2-4 years) |

| Shrinking process nodes (<20 nm) enabling higher on-chip power density | +1.8% | Asia-Pacific core, spill-over to North America and Europe | Long term (≥4 years) |

| Government energy-efficiency mandates for consumer and industrial electronics | +1.3% | Europe and North America, expanding to Asia-Pacific | Short term (≤2 years) |

| Edge-AI and IoT proliferation requiring ultra-low-quiescent-current PMICs | +1.0% | Global, early gains in North America and Asia-Pacific | Medium term (2-4 years) |

| Integration of programmable PMIC firmware enabling OTA power-optimization updates | +0.7% | North America and Europe, gradual adoption in Asia-Pacific | Medium term (2-4 years) |

| Growth of AI accelerators in data centers driving multi-phase PMIC adoption | +0.9% | North America and Asia-Pacific, selective uptake in Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rapid EV And xEV Penetration Elevating Demand For High-Current, High-Efficiency PMICs

Electric-vehicle sales surpassed 14 million units in 2025, with China accounting for 60% of volume and Europe contributing 25%, lifting battery-management silicon content per car from USD 450 in 2024 to USD 620 in 2025.[1]Björn Rosqvist, “EV Outlook 2025,” International Energy Agency, iea.org The migration from 400-volt to 800-volt platforms in models such as the Kia EV6 reduces charging time below 18 minutes and cuts harness weight by 30%, but it also necessitates silicon-carbide DC-DC converters switching above 100 kHz at junction temperatures exceeding 175 °C. European Union rules mandating 48-volt mild hybrids in vehicles above 1,800 kg add bidirectional buck-boost PMIC demand, while on-board chargers now integrate 96%-efficient power-factor-correction stages to meet CISPR 25 limits. Battery second-life applications create a USD 1.2 billion aftermarket for PMICs that recalibrate state-of-health algorithms across –40 °C to +85 °C temperature ranges. Collectively, these forces accelerate revenue in the Power management integrated circuit (PMIC) market.

Shrinking Process Nodes Enabling Higher On-Chip Power Density

TSMC began 2-nanometer production with backside power-delivery networks that double current density versus 5-nanometer, letting on-die regulators source 50 A/mm² for artificial-intelligence accelerators. Intel’s 18A node merges PowerVia interconnect with RibbonFET, allowing mixed linear and switched-mode blocks on a 4 mm² die and shrinking board area 40%. Samsung’s 3-nanometer gate-all-around process isolates voltage islands to improve power-supply rejection above 80 dB, and advanced fan-out packaging stacks PMIC dice beside wide-bandgap power stages for density of 1,200 W/in³. EUV adoption cut mask layers for analog blocks from 28 to 22, trimming non-recurring costs 15% and reducing design cycles to 14 months. These advances underpin long-term expansion of the Power management integrated circuit (PMIC) market.

Government Energy-Efficiency Mandates For Consumer And Industrial Electronics

The EU Regulation 2025/2052 requires 0.1-watt no-load and 88% active-mode efficiency for chargers starting January 2026, pushing the adoption of quasi-resonant controllers and synchronous rectification. The U.S. Department of Energy raised external supply efficiency to 89% and capped standby at 0.075 watts in December 2025, driving burst-mode operation that cuts switching loss 20%. China’s GB 43844-2025 mandates standby draw below 0.5 watts and live power displays, accelerating the adoption of buck converters in set-top boxes and routers. California expanded Title 20 to battery-powered lawn equipment, and India’s Bureau of Energy Efficiency launched a star-label program for LED drivers with 85-lm/W minimum efficacy. Regulatory pull through cements demand in the Power management integrated circuit (PMIC) market.

Edge-AI And IoT Proliferation Requiring Ultra-Low-Quiescent-Current PMICs

Edge-AI processor shipments topped 500 million units in 2025, each needing PMICs with sub-1-µA sleep current for decade-long coin-cell life. Bluetooth LE 5.4 and Matter-over-Thread traffic spikes every 2 ms, so buck-boost converters must wake within 10 µs and settle in 5 µs to avoid radio droop. Energy-harvesting IoT nodes integrate maximum-power-point tracking that extracts microwatt-level power and stores it in supercapacitors until 3.3 V is reached. On-die regulators in Apple’s A18 Bionic scale rails from 0.6 V to 1.2 V to cut inference power from 800 mW to 200 mW. These innovations lift volumes across the Power management integrated circuit (PMIC) market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain cyclicality of foundry capacity for analog and mixed-signal nodes | -1.2% | Global, acute in Asia-Pacific and North America | Short term (≤2 years) |

| Rising design complexity driving NRE costs beyond reach of smaller OEMs | -0.9% | Global, disproportionate impact on emerging markets | Medium term (2-4 years) |

| Thermal-management limits in ultra-thin consumer devices | -0.6% | Global, concentrated in consumer electronics segment | Short term (≤2 years) |

| Increasing counterfeit PMIC influx affecting reliability perceptions | -0.5% | Asia-Pacific and Middle East, spill-over to South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Cyclicality Of Foundry Capacity For Analog And Mixed-Signal Nodes

Utilization at 180-nm and 130-nm lines dipped from 92% in Q1 2025 to 78% in Q3 before rebounding, stretching lead times to 22 weeks at GlobalFoundries and raising wafer premiums 10% at TSMC. Concentration in Taiwan and Singapore exposes the chain to natural-disaster and geopolitical risk, prompting the U.S. CHIPS Act to earmark USD 2 billion for domestic analog fabs, though first production is unlikely before 2028. Smaller OEMs that cannot lock capacity have shifted to catalog PMICs, trading 15% board-area efficiency for supply assurance and avoiding USD 3 million to USD 5 million in NRE. These dynamics cap near-term upside for the Power management integrated circuit (PMIC) market.

Rising Design Complexity Driving NRE Costs Beyond Reach Of Smaller OEMs

NRE for 28-nm PMICs exceeded USD 5 million in 2025, up 40% from 2023, due to stricter electromagnetic-compatibility testing and ISO 26262 ASIL-D coverage that extends validation to 18 months. Analog design talent scarcity inflated consulting rates to USD 300 per hour and stretched recruiting cycles to nine months, forcing startups to outsource to India and Eastern Europe with 30% savings but heightened IP risk. Chiplet approaches add 25% extra cost for 3D electromagnetic and thermal analysis tools. Rising barriers temper participation in the Power management integrated circuit (PMIC) market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By IC Type: Battery-Management Leadership Sustains Momentum

Battery Management ICs held 33.96% of 2025 revenue and anchor expansion as electric-vehicle production and stationary storage scale rapidly. The segment’s Power management integrated circuit market size advantage derives from sub-10 mV cell-balancing accuracy and <2% state-of-charge error that extend lithium-ion pack life.[2]NXP Semiconductors, “Battery-Management Portfolio Guide,” nxp.com

DC-DC converter PMICs benefit from distributed power architectures in servers and telecom equipment that cut copper loss 15%, while linear regulators remain indispensable for noise-sensitive RF chains despite thermal limits. Voltage-reference supervisors safeguard medical electronics with 5 ppm/°C drift, and motor-driver PMICs now manage 20 kHz field-oriented control in collaborative robots. Wireless-charging PMICs reached 15 W transfer in 2025 and are on a roadmap to 50 W for laptops, though 85% peak efficiency is the current ceiling. Together, these categories underpin balanced growth across the Power management integrated circuit (PMIC) market.

By Application: Automotive Electrification Outpaces Consumer Demand

Consumer electronics retained a 41.23% share in 2025 as 2.1 billion smartphones, tablets, and wearables shipped, each embedding multiple regulators for displays, cameras, and audio paths. In contrast, automotive and e-Mobility posted a 9.37% CAGR, adding high-voltage battery management, on-board charging, and inverter gate drivers that raise silicon content to USD 850 by 2031.

Industrial automation and robotics require –40 °C to +105 °C ratings and 1-million-hour MTBF, while telecom infrastructure employs 200-A multi-phase buck converters running at >92% efficiency. Medical devices demand 4 kV isolation and <10 µA leakage for patient safety, and IoT sensors tailor ultra-low-quiescent PMICs that extend coin-cell life to 12 years. These varied requirements reinforce diversification within the Power management integrated circuit (PMIC) market.

By Wafer Node: Legacy Lines Coexist With Advanced Processes

Legacy processes ≥65 nm retained 46.84% share of the Power management integrated circuit market size in 2025, thanks to 98% yields on fully depreciated 200-mm tools that keep unit prices at USD 0.15–0.80.

Mixing 40-nm logic with embedded flash enables programmable sequencing in servers, while 20-nm to 40-nm options integrate multi-megahertz converters within 16 mm² packages for smartphones. Sub-20-nm nodes, growing at 8.48% CAGR, now co-locate digital loops and analog stages for 1-MHz closed-loop bandwidth in GPUs. Although mask costs surge, hyperscale clients justify adoption, ensuring a tiered technology stack across the Power management integrated circuit (PMIC) market.

By Power Range: High-Power Devices Gain Share

Low-power PMICs below 5 W captured 49.94% revenue in 2025, yet high-power devices above 100 W are advancing at 8.39% CAGR on the back of 11 kW and 22 kW electric-vehicle chargers and industrial inverters. High-power silicon-carbide MOSFETs halve switching loss and tolerate 200 °C junctions, reducing heatsink volume 40%.[3]Wolfspeed, “Silicon-Carbide Power Devices Technical Brief,” wolfspeed.com

Automotive traction inverters rely on gate-driver PMICs with 1 µs fault response, and data-center PDUs deploy PMBus-enabled regulators delivering 600 A with adaptive phase shedding. Wireless roadway charging targeting 50 kW requires resonant PMICs that sustain 90% efficiency despite 150 mm coil gaps. These advances broaden the high-end opportunity in the Power management integrated circuit (PMIC) market.

Geography Analysis

Asia-Pacific accounted for 44.23% of global 2025 revenue, buoyed by China’s USD 150 billion self-sufficiency push, Japan’s zero-ppm automotive qualification, and Taiwan’s foundry leadership from 180 nm to 2 nm. China’s nine-million-unit EV output lifted local PMIC suppliers such as BYD Semiconductor to 35% domestic share by offering 20% lower cost solutions. Japan’s Renesas and Rohm leverage decades of Toyota collaboration to maintain AEC-Q100 supremacy, while South Korea’s capacitor-in-package innovations shrink smartphone boards 25%. The region remains the fulcrum of the Power management integrated circuit (PMIC) market.

The Middle East is the fastest-growing region at an 8.12% CAGR, catalyzed by a USD 6.4 billion Saudi fab and an Abu Dhabi partnership with GlobalFoundries that targets automotive and industrial PMICs from 2027. North America benefits from the CHIPS Act, with Texas Instruments’ four new 300-mm lines adding 40,000 wafers per month of analog capacity by 2028. European electrification mandates are driving demand for battery management and 48-V mild-hybrid devices, with Infineon and STMicroelectronics adding capacity in Germany and Italy.

South America’s Manaus and Tierra del Fuego clusters localize catalog PMICs for white goods despite tariffs up to 35%, while Africa’s USD 200 million market centers on off-grid solar chargers that require ultra-low-power PMICs. Collectively, these dynamics shape regional trajectories in the Power management integrated circuit (PMIC) market.

Competitive Landscape

The top five vendors, Texas Instruments, Analog Devices, Infineon Technologies, NXP Semiconductors, and STMicroelectronics, controlled roughly 55% of 2025 revenue, demonstrating moderate concentration within the Power management integrated circuit (PMIC) market. These vertically integrated leaders maintain gross margins above 60% and reinvest 15%–18% of revenue into research and development for advanced nodes and IP blocks. Ongoing consolidation, highlighted by Analog Devices’ USD 21 billion Maxim deal and Renesas’ USD 5.9 billion Dialog purchase, secures long-term foundry access and broadens portfolios.

Disruptive fabless firms such as Monolithic Power Systems and Silergy capture share in consumer and computing niches by bringing application-specific PMICs to market within nine months. Software-defined power management with over-the-air updates reduces stock-keeping units by 40%, and wide-bandgap co-development partnerships integrate silicon-carbide or gallium-nitride stages for triple power density gains.

Patent activity topped 1,200 grants in 2025 for adaptive phase-shedding converters that lift light-load efficiency from 70% to 85%. Functional-safety compliance at ISO 26262 ASIL-D creates entry barriers by adding USD 2 million and 24 months to qualification, preserving incumbent advantage while still allowing space for agile newcomers within the Power management integrated circuit (PMIC) market.

Power Management Integrated Circuit (PMIC) Industry Leaders

-

Texas Instruments Inc.

-

Analog Devices, Inc.

-

Infineon Technologies AG

-

NXP Semiconductors N.V.

-

STMicroelectronics N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Texas Instruments began production at its USD 11 billion Sherman, Texas 300-mm fab, adding 13,000 wafers per month of analog capacity.

- January 2026: Infineon Technologies launched the AURIX TC4x microcontroller with integrated multi-phase PMIC for 800-V battery systems.

- December 2025: Analog Devices rolled out the MAX17634 6-A synchronous buck converter at 95% efficiency for 48-V mild hybrids.

- November 2025: Renesas invested USD 900 million to expand 300-mm capacity for automotive PMICs in Takasaki, Japan.

Global Power Management Integrated Circuit (PMIC) Market Report Scope

A power management integrated circuit (PMIC) is an integrated circuit that has wide applications because of its role in battery management, voltage regulation, and charging functions. These ICs are mostly used in battery-operated devices and consumer electronics, such as smartphones, Bluetooth headsets, and portable industrial and medical equipment. A PMIC is used to manage power on electronic devices or in modules on devices that may have a range of voltages. The PMIC manages battery power charging and sleep modes, DC-to-DC conversion, and scaling of voltages down or up, among others.

The Power Management Integrated Circuit (PMIC) Market Report is Segmented by IC Type (Linear Regulator, DC-DC Converter, Battery Management, Voltage Reference, Motor-Control, and Wireless-Charging), Application (Consumer, Automotive, Industrial, Telecom, Healthcare, and IoT), Wafer Node (≥65 nm, 40-65 nm, 20-40 nm, and <20 nm), Power Range (Low, Medium, and High), and Geography. The Market Forecasts are in Value (USD).

| Linear Regulator PMIC |

| DC-DC Converter PMIC |

| Battery Management IC |

| Voltage Reference and Supervisor IC |

| Motor-Control and Driver PMIC |

| Wireless-Charging PMIC |

| Consumer Electronics |

| Automotive and e-Mobility |

| Industrial and Robotics |

| Telecommunications and Networking |

| Healthcare and Medical Devices |

| IoT and Edge Devices |

| ?65 nm |

| 40 – 65 nm |

| 20 – 40 nm |

| <20 nm |

| Low Power PMICs |

| Medium Power PMICs |

| High Power PMICs |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Egypt | |

| Rest of Africa |

| By IC Type | Linear Regulator PMIC | |

| DC-DC Converter PMIC | ||

| Battery Management IC | ||

| Voltage Reference and Supervisor IC | ||

| Motor-Control and Driver PMIC | ||

| Wireless-Charging PMIC | ||

| By Application | Consumer Electronics | |

| Automotive and e-Mobility | ||

| Industrial and Robotics | ||

| Telecommunications and Networking | ||

| Healthcare and Medical Devices | ||

| IoT and Edge Devices | ||

| By Wafer Node | ?65 nm | |

| 40 – 65 nm | ||

| 20 – 40 nm | ||

| <20 nm | ||

| By Power Range | Low Power PMICs | |

| Medium Power PMICs | ||

| High Power PMICs | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large will the Power management integrated circuit (PMIC) market be by 2031?

How large will the Power management integrated circuit (PMIC) market be by 2031?

Which PMIC segment grows fastest through 2031?

Battery-management ICs post the highest 9.83% CAGR as EV platforms shift to 800-volt and second-life storage emerges.

Why is sub-20-nanometer adoption important for PMICs?

Advanced nodes double current density and enable on-die voltage regulation that meets the 600-watt demands of AI accelerators.

What regions lead and grow quickest in PMIC revenue?

Asia-Pacific led with 44.23% share in 2025, while the Middle East expands fastest at an 8.12% CAGR thanks to new fab investments.

How are programmable PMICs changing product strategy?

Firmware-upgradable devices cut SKUs 40%, allow post-deployment voltage tweaks, and shorten time-to-market for system integrators.

What is the main risk to PMIC supply security?

Analog foundry capacity swings: lead times peaked at 26 weeks in 2025, exposing OEMs without long-term allocations to shortages.

Page last updated on: