Calcium Ammonium Nitrate Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Market Size (2025) | USD 5.5 Billion |

| Market Size (2030) | USD 6.90 Billion |

| Growth Rate (2025 - 2030) | 4.60% CAGR |

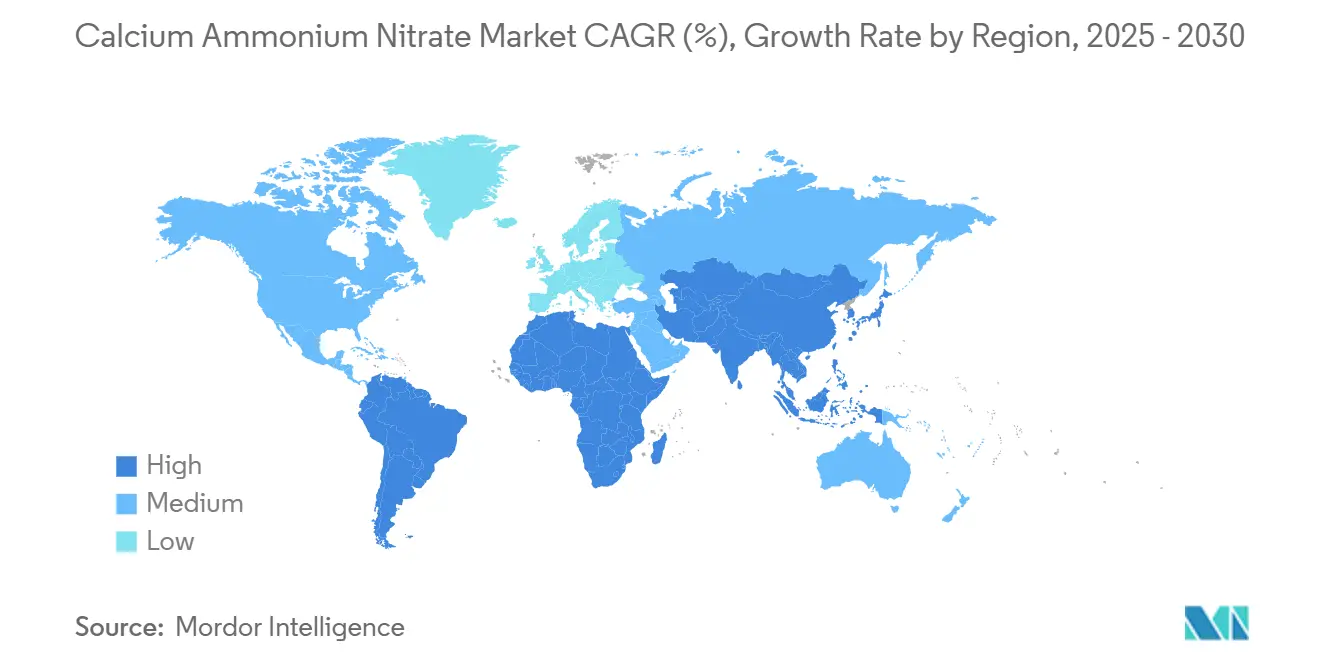

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

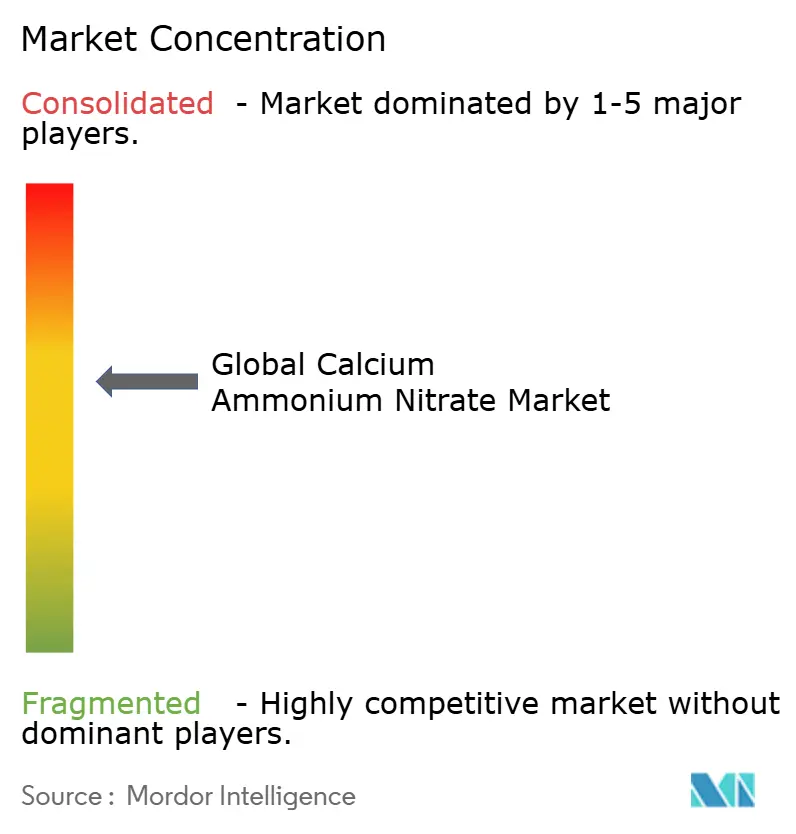

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Calcium Ammonium Nitrate Market Analysis by Mordor Intelligence

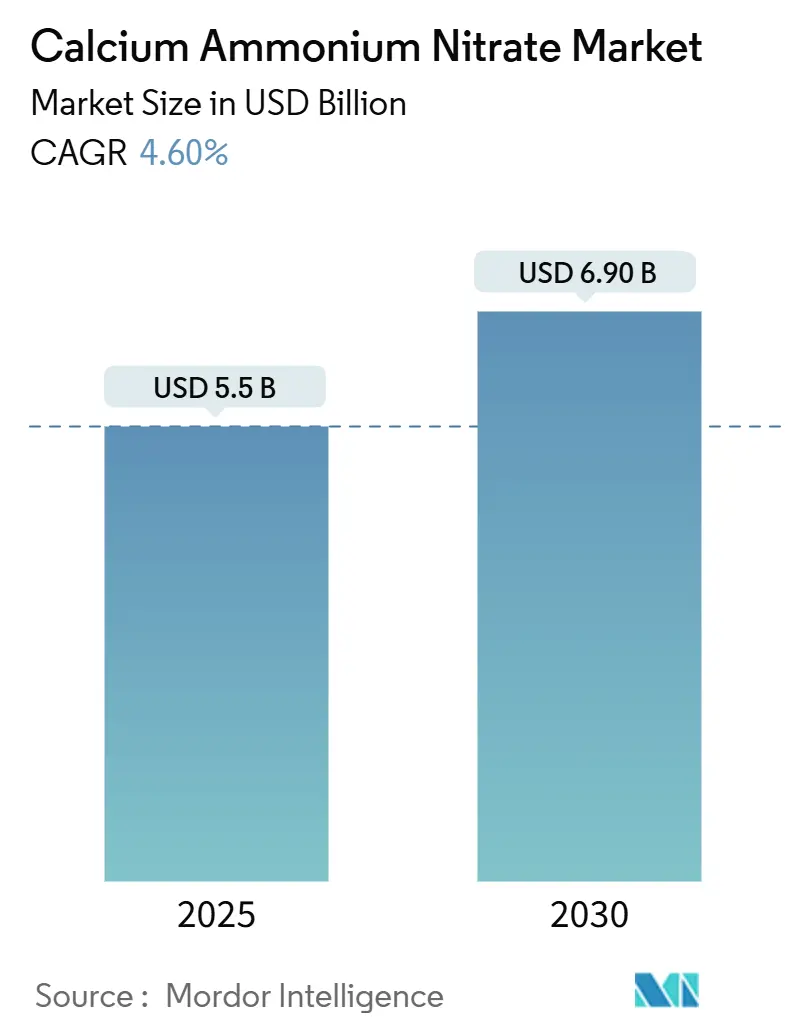

The calcium ammonium nitrate market size is currently valued at USD 5.5 billion and is projected to reach USD 6.9 billion by 2030, reflecting a 4.6% CAGR. Market size growth stems from European decarbonization mandates, Asia-Pacific greenhouse expansion, and precision-driven fertilizer use that tilts demand toward lower-carbon nitrate products [1]Source: European Commission, “Fertilizers Regulation (EU) 2019/1009,” ec.europa.eu. Heightened natural gas prices in Europe are pushing producers to invest in low-carbon ammonia pathways, while the forthcoming Carbon Border Adjustment Mechanism will add cost pressure to high-carbon imports, increasing domestic competitiveness [2]Source: Carbon Trust, “The Carbon Border Adjustment Mechanism Explained,” carbontrust.com. The Asia-Pacific region leads regional growth, driven by the rapid adoption of fertigation. Meanwhile, Europe remains the largest regional market, supported by stringent nitrate regulations that favor chloride-free fertilizers. Liquid formulations are experiencing strong growth as growers adopt fertigation and precision delivery systems. At the same time, regenerative farming trends and transportation safety rules temper overall volume growth by encouraging efficient application rates and increasing logistics costs.

Key Report Takeaways

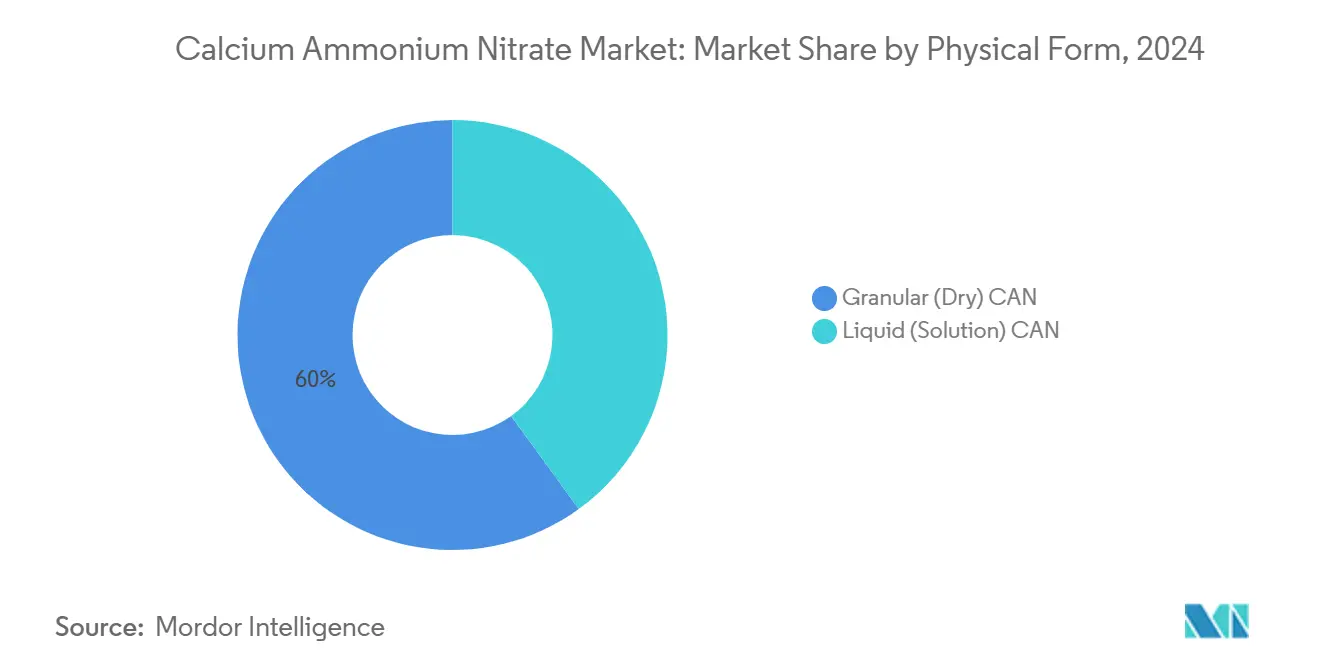

- By physical form, granular products accounted for 60% of the 2024 revenue in the calcium ammonium nitrate market size, while liquid solutions are forecast to post the fastest CAGR of 6.6% through 2030.

- By crop type, cereals and grains led with 46% revenue share in 2024, and fruits and vegetables are projected to advance at a 5.6% CAGR through 2030.

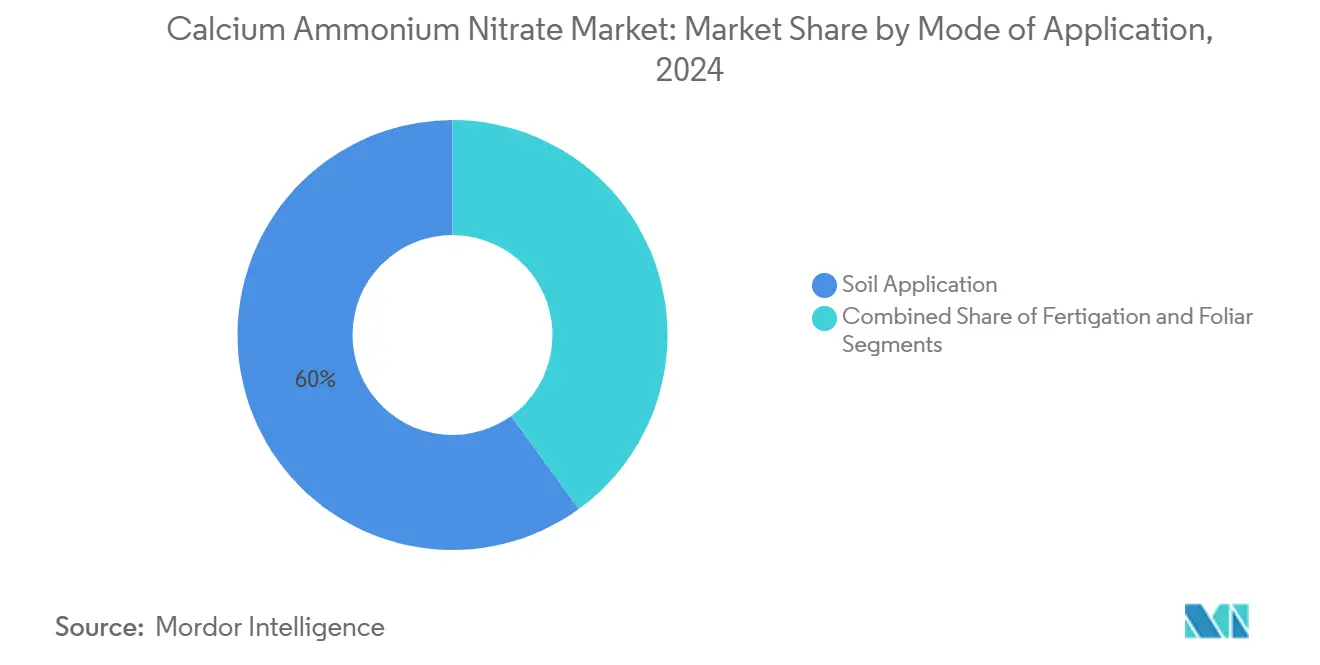

- By mode of application, soil application accounted for 60% of the calcium ammonium nitrate market share in 2024, whereas fertigation is poised to expand at a 7.1% CAGR to 2030.

- By geography, Europe retained the largest 39% market share in 2024, while the Asia-Pacific region is set to grow at a 5.7% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Calcium Ammonium Nitrate Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Evolving European nitrate-use regulations favoring low-carbon fertilizers | +0.7% | Europe primary, and global secondary | Medium term (2-4 years) |

| Shift toward chloride-free nitrogen sources for high-value horticulture | +0.8% | Global, and strongest in Asia-Pacific | Short term (≤ 2 years) |

| Growing fertigation adoption in water-scarce regions | +0.8% | Asia-Pacific, Middle East, and Africa | Medium term (2-4 years) |

| Government incentives for controlled-release formulations | +0.6% | North America, and Europe | Long term (≥ 4 years) |

| Rapid greenhouse expansion in Asia-Pacific | +0.6% | Asia-Pacific primary | Short term (≤ 2 years) |

| Emergence of carbon-credit monetization for low-N₂O fertilizers | +0.5% | Global, and early adoption in Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Evolving European Nitrate-Use Regulations Favoring Low-Carbon Fertilizers

The 2022 entry into force of Regulation (EU) 2019/1009 tightened composition and footprint rules, creating a premium tier for compliant calcium ammonium nitrate while limiting market access for higher-carbon alternatives [3]Source: Eurofins, “EU Fertilizer Regulation Compliance Services,” eurofins.com. Producers are investing in carbon capture to meet the European Union’s goal of storing 50 million metric tons of CO₂ annually by 2030, positioning compliant fertilizers for export advantage as other regions align with European Union (EU) standards.

Shift Toward Chloride-Free Nitrogen Sources for High-Value Horticulture

Premium fruit and vegetable growers favor calcium ammonium nitrate because its chloride-free profile prevents salinity stress in sensitive crops. Controlled-environment agriculture in China, which comprises 60% of global greenhouse area, relies on nitrate-based inputs that preserve soil health and boost yield. Field studies show improved fruit set and reduced drop in pomegranate when calcium nitrate supplements standard nitrogen regimes.

Growing Fertigation Adoption in Water-Scarce Regions

Smart irrigation systems that blend nutrient injection with sensor-guided watering now dominate new installations in the Middle East and North Africa. High solubility makes calcium ammonium nitrate well-suited to these systems, delivering precise nutrient timing and increasing uptake efficiency.

Government Incentives for Controlled-Release Formulations

Tax credits in the United States Inflation Reduction Act reward low-carbon ammonia, spurring investment in coated or slow-release nitrate products that cut runoff and enhance on-farm efficiency. CF Industries, for instance, partnered with POET LLC to pilot the use of low-carbon ammonia in corn production, outlining a path to lower ethanol intensity.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in natural-gas-derived ammonia feedstock prices | -0.9% | Global, and most severe in Europe | Short term (≤ 2 years) |

| Tightening nitrate transport regulations | -0.7% | North America, and Europe | Medium term (2-4 years) |

| Competition from urea and Urea Ammonium Nitrate (UAN) solutions in broad-acre crops | -0.8% | Global, and strongest in North America | Medium term (2-4 years) |

| Rising adoption of regenerative agriculture limiting synthetic inputs | -0.6% | North America, and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Natural-Gas-Derived Ammonia Feedstock Prices

Natural gas price volatility continues to create significant margin pressure for calcium ammonium nitrate producers, with European manufacturers particularly exposed to supply disruptions and price spikes. The United States Energy Information Administration reports that ammonia prices increased sixfold over a two-year period, primarily driven by international natural gas price fluctuations that directly impact production economics. This volatility is compounded by geopolitical tensions affecting gas supplies, with European producers facing sustained high energy costs that undermine their competitive position relative to regions with abundant, low-cost natural gas. The interconnected nature of global ammonia markets means that regional price shocks rapidly transmit across supply chains, creating unpredictable cost structures for downstream calcium ammonium nitrate production. Producers are responding by investing in carbon capture technologies and integrating renewable energy to reduce their dependence on volatile fossil fuel inputs, although these solutions require substantial capital investment and longer implementation timelines.

Tightening Nitrate Transport Regulations

Enhanced safety regulations for ammonium nitrate transport are increasing logistics costs and operational complexity for calcium ammonium nitrate manufacturers and distributors. The United States Department of Transportation has implemented comprehensive updates to hazardous materials regulations, including revised tank car design requirements and enhanced safety protocols for nitrate shipments [4]Source: U.S. Department of Transportation, “Hazardous Materials Regulations Update,” transportation.gov. These regulations mandate specialized handling procedures, certified transport equipment, and enhanced documentation requirements that increase supply chain costs and reduce operational flexibility. The United Kingdom's Health and Safety Executive prohibits the importation of ammonium nitrate with a nitrogen content exceeding 28% without certification of resistance to detonation, creating additional compliance barriers for international trade. These regulatory constraints are particularly challenging for smaller regional producers who lack the scale to absorb increased compliance costs, potentially accelerating market consolidation toward larger, better-capitalized players.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Physical Form: Liquid Solutions Drive Innovation

Granular fertilizers retained 60% of 2024 revenue owing to established soil broadcasting practices across broad-acre crops. OCI reported average calcium ammonium nitrate pricing of USD 294 per metric ton as of 2024, as demand remained steady. The liquid segment now grows at a 6.6% CAGR, propelled by fertigation use among greenhouse growers seeking rapid delivery and uniform nutrient distribution. Producers highlight the compatibility of liquids with automated injection pumps, which reduce labor and improve dosing accuracy. The calcium ammonium nitrate market size for liquid solutions is projected to expand rapidly through 2030 as precision agriculture gains traction on mid-scale farms. Granular products continue serving regions lacking micro-irrigation, supporting balanced growth across both forms.

Liquid adoption marks a broader industry shift toward data-driven farming. Modern sensing tools map real-time nutrient demand, allowing timed liquid injections that prevent leaching. This integration can cut per-hectare application volumes while sustaining yield, aligning with tightening nitrate discharge regulations. Granular materials remain vital in areas that favor bulk handling and season-long release, ensuring the calcium ammonium nitrate market continues to diversify across various delivery technologies.

By Crop Type: Specialty Crops Outpace Commodities

Cereals and grains captured 46% of the 2024 demand due to their extensive acreage, yet growth moderates as growers fine-tune rates through variable-rate application. Fruits and vegetables post the fastest 5.6% CAGR, supported by greenhouse proliferation and chloride sensitivity that rewards nitrate fertilizers. The calcium ammonium nitrate market share of specialty crops will therefore rise through 2030 as growers in China, India, and Spain intensify high-value horticulture. Oilseeds and pulses maintain a stable slice of demand while turf and ornamentals benefit from urban landscaping projects in North America and Gulf economies.

Yield trials demonstrate that the combination of calcium and nitrate reduces physiological disorders, including blossom end rot, enabling specialty growers to obtain quality premiums. Rising disposable incomes in Asia-Pacific further push demand for premium produce, reinforcing specialty crop momentum. Commodity segments still present scale but see incremental demand as precision tools optimize nitrogen efficiency.

By Mode of Application: Fertigation Transforms Delivery Methods

Soil application accounted for 60% of 2024 applications, yet fertigation is now rising at a 7.1% CAGR due to water scarcity responses in the Asia-Pacific, the Middle East, and arid states in the United States. Smart drip systems combine irrigation and nutrient delivery, raising uptake efficiency by double digits compared with surface application. The calcium ammonium nitrate market size for fertigation systems is forecast to expand sharply as governments subsidize micro-irrigation to conserve water. Foliar treatments stay niche for micronutrient correction but gain traction in greenhouse cucurbits and berries, where quick response is critical.

Fertigation’s advance aligns with digital agriculture platforms that automate pH and emulsifiable concentrate (EC) adjustments, ensuring uniform nutrient mixes. Such systems help meet regulatory targets for reducing nitrate runoff. Soil broadcasting persists in extensive cereal regions, offering cost advantages where water is less limiting and labor is scarce. The coexistence of both methods thus stabilizes overall market growth while steering innovation toward precision delivery.

Geography Analysis

Europe maintained a dominant 39% share in 2024, propelled by stringent nitrate and carbon policies that elevate compliant calcium ammonium nitrate demand. Regional growth runs at a moderate 2.7% CAGR to 2030 as market maturity balances regulatory pull. Germany and France, characterized by intensive farming and environmental compliance, are the largest national buyers. Producers prioritize carbon capture and renewable power at ammonia plants to preserve market access under the Carbon Border Adjustment Mechanism, set for full enforcement by 2026.

Asia-Pacific is the fastest-growing region at a 5.7% CAGR, driven by greenhouse expansion in China and India’s subsidy regime that supports nitrate blends. Rapid fertigation adoption in water-stressed northern China and western India amplifies demand for fully soluble nitrate fertilizers. Government schemes encouraging precision agriculture and controlled-environment farming shift focus toward high-purity inputs, anchoring long-term volume gains.

North America exhibits steady growth. Corn and soybean rotations maintain baseline consumption, while sustainability incentives under the Inflation Reduction Act push producers toward low-carbon ammonia projects. Canada’s emphasis on 4R nutrient stewardship and the United States' transport safety updates shape demand toward controlled-release and carbon-verified nitrates. South America, the Middle East, and Africa together account for a rising share as Brazil scales crop area and Gulf nations pursue food security through greenhouse megaprojects.

Competitive Landscape

The calcium ammonium nitrate market shows moderate concentration, with five major players such as Yara International ASA, EuroChem Group AG, CF Industries Holdings Inc., Achema AB, and Uralchem JSC controlling approximately 62% of global revenue in 2024. Yara International ASA produced 429 thousand tons of calcium ammonium nitrate in Q3 2024, optimizing costs through integrated ammonia production and port-based terminals. EuroChem Group AG strengthened its raw material position by acquiring upstream gas assets to minimize feedstock price fluctuations. CF Industries Holdings Inc. advanced its environmental initiatives by launching a 1.4 million metric tons low-carbon ammonia project in 2024, focusing on lifecycle-verified fertilizers.

Natural gas costs account for 60-70% of production expenses for ammonia-based fertilizers, significantly impacting competitive dynamics. Companies are prioritizing the reduction of their carbon footprint and logistics optimization. To secure contracts in European and North American markets, where emissions disclosure is mandatory, manufacturers are investing in green hydrogen pilots and nitric acid capture technologies.

The industry is consolidating its distribution networks. Regional producers are collaborating with technology companies to develop slow-release coatings and digital advisory services, aiming to differentiate through agronomic benefits rather than price. Market leaders are implementing carbon capture technologies and incorporating renewable energy in their operations to comply with environmental regulations and sustainability requirements.

Calcium Ammonium Nitrate Industry Leaders

Yara International ASA

EuroChem Group AG

CF Industries Holdings Inc.

Achema AB

Uralchem JSC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: OCI Global partnered with Raiffeisen Waren‑Zentrale Rhein‑Main AG (RWZ) for the "KlimaPartner Landwirtschaft" carbon‑farming initiative, a collaboration between RWZ and BASF. Under this agreement, OCI will supply low-carbon nitrogen fertilizers, including calcium ammonium nitrate (CAN), Nutramon Novo, and CAN+S Dynamon Novo, manufactured using biogas instead of natural gas.

- July 2024: Yara International ASA and ATOME PLC have signed a non-binding Heads of Terms for the long‑term offtake of all production from ATOME's upcoming 145 MW renewable Calcium Ammonium Nitrate (CAN) facility in Villeta, Paraguay. Under the agreement, Yara will market the fertilizer via its YaraBela line and incorporate it into its “Climate Choice” portfolio, spotlighting low-emission products.

- March 2024: Haifa Group has officially entered the Indian market through a strategic partnership with Deepak Fertilisers' Mahadhan Agritech Limited (MAL). The agreement focuses on promoting advanced water‑soluble specialty fertilizers such as calcium ammonium nitrate and Nutrigation technology to enhance crop yield, nutrient uptake, and reduce environmental impact.

Global Calcium Ammonium Nitrate Market Report Scope

| Granular (Dry) CAN |

| Liquid (Solution) CAN |

| Cereals and Grains |

| Oilseeds and Pulses |

| Fruits and Vegetables |

| Turf and Ornamentals |

| Soil Application |

| Fertigation |

| Foliar |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Physical Form | Granular (Dry) CAN | |

| Liquid (Solution) CAN | ||

| By Crop Type | Cereals and Grains | |

| Oilseeds and Pulses | ||

| Fruits and Vegetables | ||

| Turf and Ornamentals | ||

| By Mode of Application | Soil Application | |

| Fertigation | ||

| Foliar | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the calcium ammonium nitrate market?

The market is valued at USD 5.5 billion in 2025 and is projected to reach USD 6.9 billion by 2030, growing at a 4.6% CAGR.

Which region holds the largest share of the calcium ammonium nitrate market?

Europe leads with a 39% share of the calcium ammonium nitrate market, driven by strict nitrate and carbon regulations that favor compliant products.

Which application method is growing fastest for calcium ammonium nitrate?

Fertigation is the fastest-growing method, projected to register a 7.1% CAGR through 2030 as water-scarce regions adopt precision irrigation.

Why are liquid calcium ammonium nitrate solutions gaining popularity?

Liquids dissolve quickly, integrate seamlessly with fertigation systems, and enable precise nutrient delivery, supporting a 6.6% CAGR.

How do natural gas price swings affect calcium ammonium nitrate producers?

Ammonia derived from natural gas accounts for most production cost, so price spikes compress margins and accelerate investment in renewable hydrogen and carbon capture.

Page last updated on: