Potassium Chlorate Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

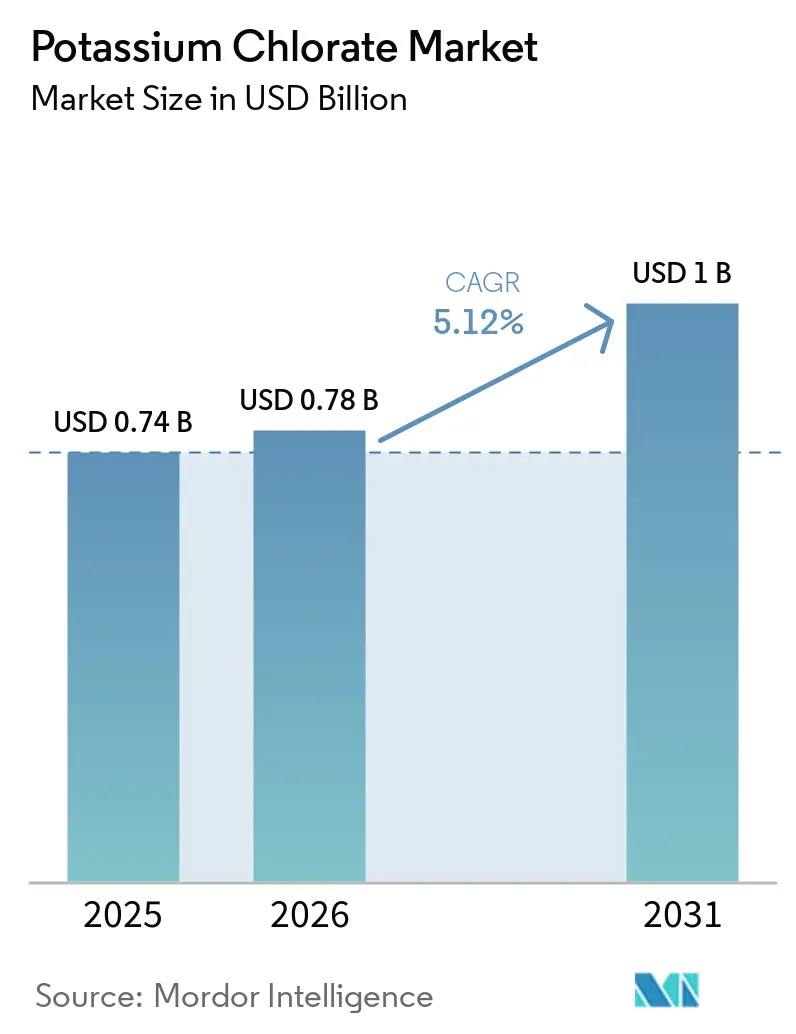

| Market Size (2026) | USD 0.78 Billion |

| Market Size (2031) | USD 1 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Potassium Chlorate Market Analysis by Mordor Intelligence

The potassium chlorate market size is expected to increase from USD 0.74 billion in 2025 to USD 0.78 billion in 2026 and reach USD 1 billion by 2031, growing at a CAGR of 5.12% over 2026-2031. Demand is pivoting from legacy herbicide use toward high-margin niches such as chemical oxygen generation, renewable-powered electrolysis, and specialty oxidizers for fireworks, textile bleaching, and mini-rocket fuels. Defense contractors are qualifying chlorate relatives, yet cost-advantaged chlorate retains appeal in one-time oxygen cartridges and match heads. India is capitalizing on export openings created by U.S. and EU curbs, while Brazil and Sweden illustrate how renewable electricity reshapes chlorate cost curves. Producers positioned at integrated pulp or hydrogen-peroxide complexes enjoy power savings and Scope 3 emission reductions that strengthen margins even as European utilities raise tariffs.

Key Report Takeaways

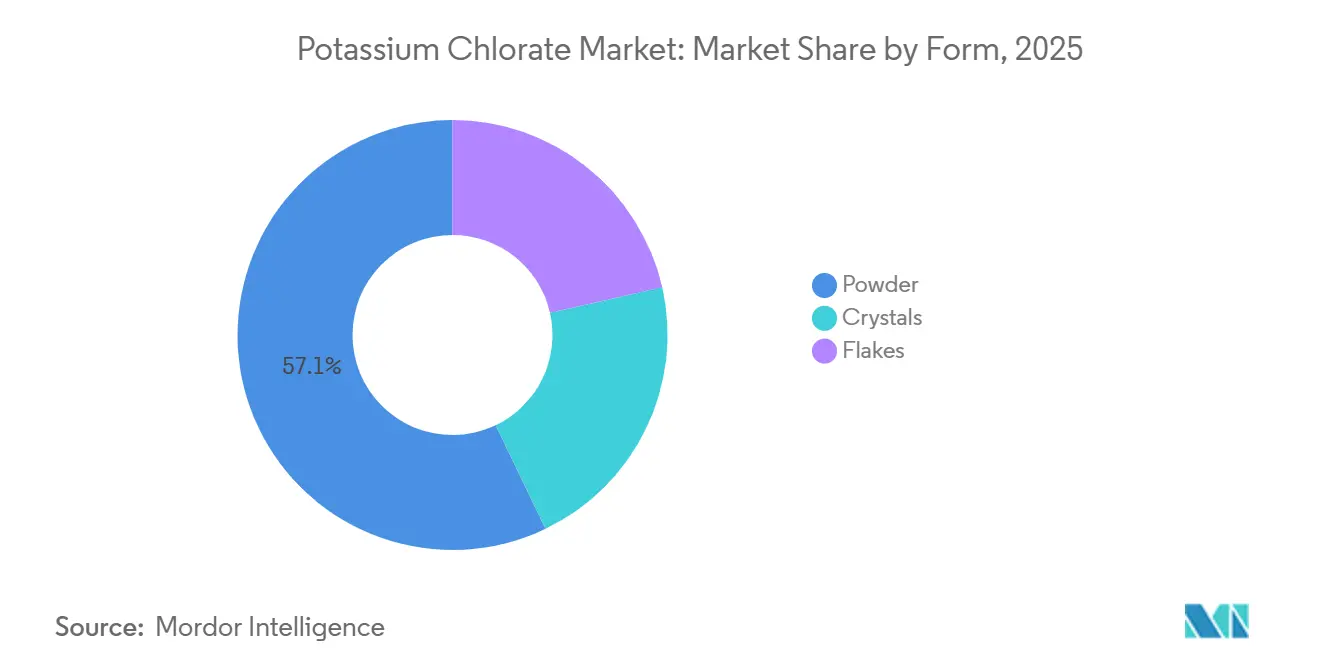

- By form, powder led with 57.12% revenue share in 2025; flakes are projected to advance at a 5.51% CAGR to 2031.

- By purity grade, technical grade commanded 73.25 % of the potassium chlorate market share in 2025, while laboratory grade recorded the highest projected CAGR at 5.78% through 2031.

- By application, agrochemicals accounted for 32.78% of the potassium chlorate market size in 2025, and laboratory reagents and oxygen generators are projected at 5.89% through 2031.

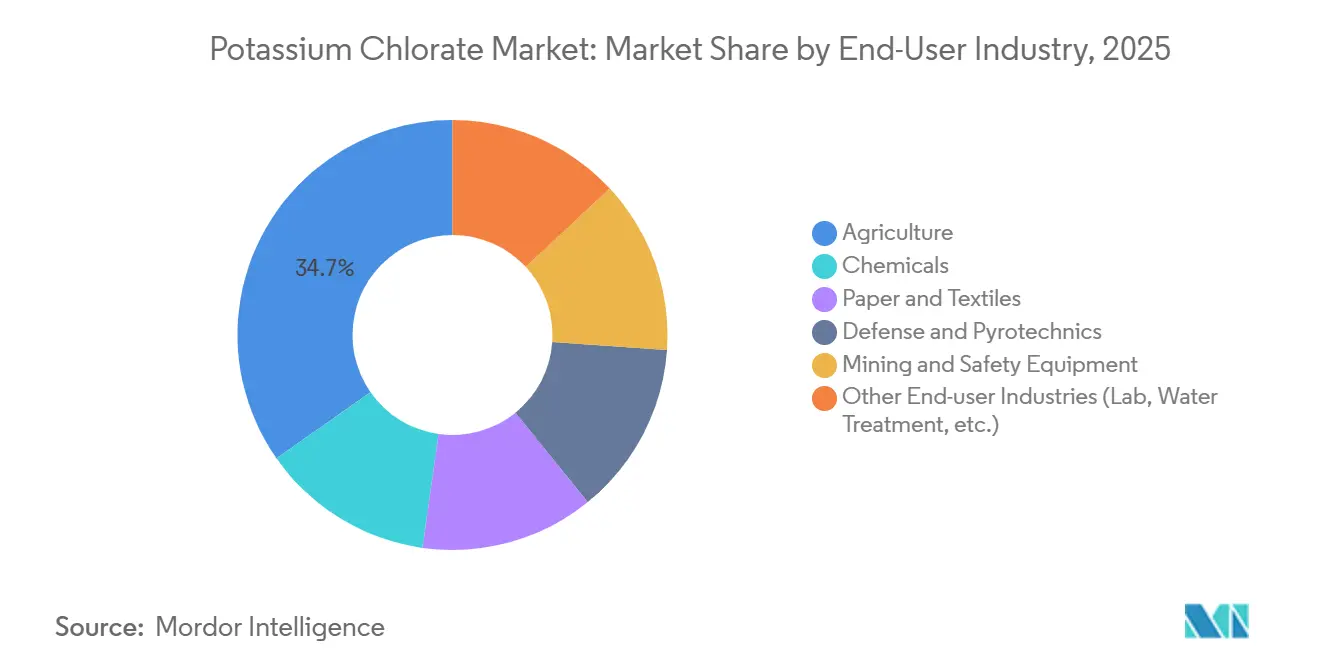

- By end-use industry, agriculture led with 34.71% revenue share in 2025, whereas other diversified end-user industries are forecast to grow at 6.11% CAGR to 2031.

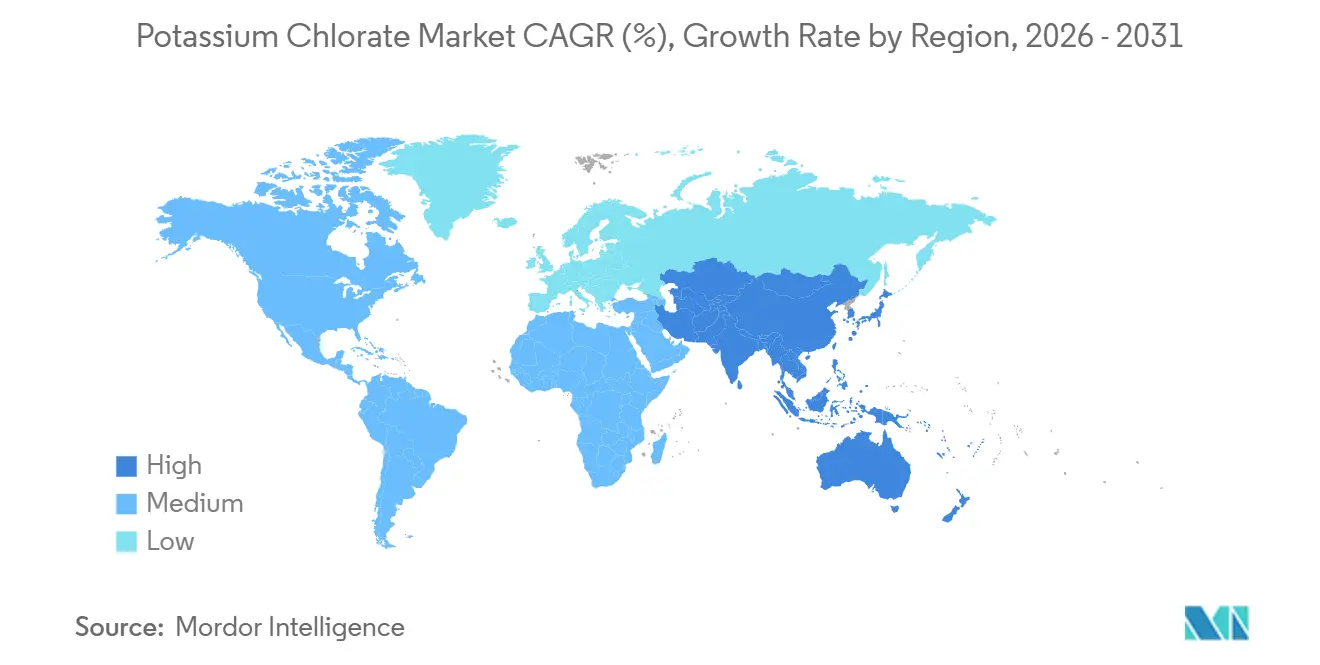

- By geography, Asia-Pacific dominated with 47.12% share in 2025 and is expected to register the quickest regional CAGR at 5.98% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Potassium Chlorate Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of agro-chemical defoliant formulations | +0.8% | Asia-Pacific (India, ASEAN), South America (Brazil) | Medium term (2-4 years) |

| Shift toward chlorine-free oxidative bleaching in recycled textiles | +0.6% | Asia-Pacific (China, India, Bangladesh), Europe | Long term (≥4 years) |

| Growing use in low-temperature chemical oxygen generators | +1.2% | Global, with concentration in North America, Europe, the Middle-East | Short term (≤2 years) |

| Cost-advantaged renewable-powered electrolysis capacity additions | +1.4% | South America (Brazil), Nordic Europe (Sweden), select Asia-Pacific sites | Medium term (2-4 years) |

| Micro-particle engineered oxidizers for mini-rocket & drone propulsion | +0.5% | North America, Europe, select Asia-Pacific (Japan, South Korea) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Expansion of Agro-Chemical Defoliant Formulations

Cotton mechanization is expanding in Brazil's Cerrado region and India's Gujarat belt, increasing demand for fast-acting desiccants that do not leave sodium residues. Formulators are incorporating potassium chlorate into adjuvant packages to promote faster leaf drop under humid harvest conditions. In 2023-24, India exported 27,726 tons of chlorate, indicating surplus production capacity that can cater to growing cotton acreage in markets such as Kenya and Thailand[1]Government of India, “Chemical and Petrochemical Statistics at a Glance – 2024,” chemicals.gov.in. In the United States, EPA regulations prohibit the use of pre-harvest chlorate, leading to the redirection of surplus Asian production to less-regulated markets. While mechanization rates in South Asia remain below 15%, pilot programs in Punjab and Sindh have demonstrated cost savings, encouraging potential future adoption. Overall, chlorate's agronomic role is declining in Western markets but stabilizing in emerging cotton-producing regions.

Shift Toward Chlorine-Free Oxidative Bleaching in Recycled Textiles

Global apparel brands are requesting low-chlorine discharge scores, leading Asian textile mills to adopt electrochemical oxidants that maintain fiber strength. Potassium chlorate enables the in-situ generation of hypochlorite or hydrogen peroxide at room temperature, reducing bleaching cycle durations and energy consumption. Nouryon’s Eka HP Puroxide product line integrates chlorate electrolysis with green hydrogen, achieving up to a 90% reduction in Scope 3 emissions[2]Nouryon, “Oxidizing ability with potassium chlorate,” nouryon.com. Textile mills in Bangladesh and Vietnam, which process over 8 million tons of textiles annually, are early adopters to meet EU REACH compliance requirements. On-site systems eliminate the need for transporting unstable oxidants and provide a return on investment within three production cycles. Consequently, suppliers of bleaching chemicals are identifying a new growth opportunity in the demand for high-purity chlorate.

Growing Use in Low-Temperature Chemical Oxygen Generators

Mining refuge chambers, aircraft galleys, and naval vessels are moving from heavy pressurized cylinders to solid-state oxygen candles. A single MineSpec unit produces 2,600 tons of breathable oxygen over 90 minutes without requiring external power. Potassium chlorate is selected over sodium-based alternatives in damp underground mining environments due to its lower hygroscopicity and longer shelf life. U.S. Navy supplier OC Lugo provides oxygen candles that generate 3,341 tons per unit, classified as UN 3356 oxidizers, reflecting demand in the defense sector. As regulations on lithium-battery transport become stricter, chemical oxygen generators are increasingly utilized for emergency breathing systems in cargo aircraft. These trends are driving the adoption of laboratory-grade chlorate in aerospace and mining supply chains.

Cost-Advantaged Renewable-Powered Electrolysis Capacity Additions

Electricity accounts for over 60% of the variable costs in chlorate production, making co-location with biomass or hydroelectric power a cost-efficient strategy. Nouryon’s USD 4.6 billion Mato Grosso do Sul project is set to increase South American chlorate production by 20%, utilizing biomass steam from pulp mills to power electrodes. The company’s earlier Ribas do Rio Pardo facility integrates green hydrogen with chlorate production, enabling expansion into peroxide applications. A 2026 study published in Nature Communications highlights the use of membrane cells that leverage salinity-gradient energy to produce chlorine with minimal external power, indicating potential for off-grid chlorate production modules in the future. Transitioning to renewable energy sources allows producers to mitigate risks from European power price fluctuations, which reduced Ercros’ chlor-derivative EBITDA by 63.2% in 2024. Renewable energy provides a competitive cost advantage and enhances resilience against long-term carbon fees.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory bans on chlorate-based herbicides | -0.9% | North America, Europe | Short term (≤2 years) |

| Substitution by potassium perchlorate & sodium chlorate | -1.1% | Global, with concentration in North America, Europe, and Asia-Pacific defense sectors | Medium term (2-4 years) |

| EU micro-particle discharge limits tightening match formulations | -0.4% | Europe, with spillover to export-oriented producers in Japan, India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Regulatory Bans and Micro-Particle Limits on Herbicide and Match Uses

The EPA's 2026 tolerance exemption is limited to post-harvest fumigation, excluding chlorate from U.S. pre-harvest cotton programs. In the European Union, Prior Informed Consent regulations mandate exporters to obtain buyer approval, while new micro-particle discharge limits being drafted in Brussels are expected to increase compliance costs for match production facilities. In Japan, which produces 80% of its domestic match supply in Himeji, authorities are considering similar dust standards that may reduce chlorate consumption. These regulatory developments collectively reduce chlorate tons in OECD markets, even as emerging economies adjust restrictions.

Substitution by Potassium Perchlorate and Sodium Chlorate in Defense and Bleaching

Potassium perchlorate is recognized for its higher thermal stability and lower sensitivity, leading NewMarket to plan a more than 50% increase in AMPAC's capacity by 2026 to support solid rocket motor production. Sodium chlorate is widely used in chlorine dioxide pulp bleaching, with Nouryon’s Brazil facility incorporating this integration to reduce dependence on potassium salts. Defense contractors select perchlorate due to its compliance with insensitive munitions standards, while sanctions on Chinese chlorate exporters are driving Western efforts to re-qualify alternative sources. These factors collectively contribute to a gradual transition in oxidative applications from potassium chlorate to substitutes that are chemically or politically more suitable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-use Industry: Agriculture at the Helm, Diversification Underway

Powder accounted for 57.12% of the potassium chlorate market share in 2025, driven by its use in match heads, agricultural blends, and laboratory reagents. Nouryon’s ISO-certified Alby mill customizes grind curves to meet the requirements of European match manufacturers. Crystal grades are used in pharmaceutical synthesis but face competition from Chinese commodities. Flake volumes are expected to grow at a CAGR of 5.51%, as aerial-shell manufacturers prefer dense particles that reduce void space and enhance burn consistency. Japanese fireworks manufacturers are increasingly specifying flake morphology to optimize multi-stage color bursts. As a result, the market size for potassium chlorate flakes is projected to grow faster than the overall market through 2031.

By Purity Grade: Technical Grade Anchors Volume, Laboratory Grade Surges

Technical-grade potassium chlorate (less than or equal to 99%) accounted for 73.25% of the projected 2025 market size, primarily serving cost-sensitive agrochemical and match industries. Assay tolerances permit bromate levels below 100 ppm and chloride levels below 2,000 ppm, which are sufficient for most oxidizer applications. Laboratory-grade potassium chlorate (greater than or equal to 99%) is expected to grow at a CAGR of 5.78%, driven by demand in pharmaceutical intermediates and specialty analytics requiring stricter heavy-metal controls. According to EU REACH dossiers, the compound has a water solubility of 69.9 g/L at 20°C, a critical parameter for laboratories designing crystallization processes.

Growth in the technical-grade segment is limited by herbicide bans in Western markets; however, emerging cotton-growing regions and the use of potassium chlorate in mining oxygen candles maintain baseline demand. Laboratory-grade potassium chlorate benefits from India's expanding contract manufacturing sector and China's advancements in specialty dye synthesis. As dual-use export regulations become increasingly stringent, suppliers providing audited chain-of-custody documentation are able to command premium pricing, enhancing value capture in the high-purity segment of the potassium chlorate market.

By Application: Agrochemicals Lead, Oxygen Generators Post Fastest Gains

Agrochemicals accounted for 32.78% of the projected 2025 revenue but are seeing a reduction in market share as regulators increasingly support alternatives like thidiazuron and diuron. In contrast, laboratory reagents and oxygen generators are expected to grow at a compound annual growth rate (CAGR) of 5.89% through 2031, driven by mandates for mining safety and upgrades in aerospace emergency breathing systems. Fireworks maintain cultural significance, particularly in Japan and during India’s Diwali season, while the demand for safety matches is decreasing due to the growing use of lighters.

In the textile industry, chlorate is primarily used as a feedstock for on-site oxidant generation, a practice gaining popularity under the European Union's wastewater standards. Disinfectant and specialty oxidation applications represent a smaller segment but yield high margins due to the demand for small-batch packaging. Overall, the application landscape is shifting toward regulated, high-value oxygen and laboratory-related uses, helping to stabilize revenue as agrochemical volumes level off.

By End-User Industry: Agriculture Shrinks, Laboratories and Mining Grow

Agriculture accounted for 34.71% of 2025 end-user revenue; however, bans in the United States and stricter EU residue regulations are expected to limit future tons. The mining, defense, and laboratory sectors are projected to grow at a compound annual growth rate (CAGR) of 6.11%, driven by demand for safety oxygen candles, rocket oxidizers, and pharmaceutical reagents. The paper and textiles industries are anticipated to achieve mid-single-digit growth as mills implement on-site oxidant cells to comply with ISO 14001 audit requirements.

In the defense sector, demand trends vary: perchlorate is gaining market share in propellants, while chlorate retains cost advantages in single-use oxygen cartridges and specific illuminating flares. In mining, regulatory changes in countries such as Chile, South Africa, and Canada are requiring longer-duration refuge systems, increasing sales of candles that utilize high-purity potassium chlorate. This shift in end-user demand supports the long-term stability of the potassium chlorate market.

Geography Analysis

Asia-Pacific is projected to account for 47.12% of the revenue in 2025, with a compound annual growth rate (CAGR) of 5.98%, supported by India's export growth and China's feedstock control policies. In 2024, China's domestic potassium chloride (KCl) production decreased by 0.56% to 3.05 million tons, while consumption increased by 15.51%, raising import dependency to over 50%. Increased scrutiny on exports, following U.S. sanctions on China Chlorate Tech Co., has led to regional stockpiling efforts.

In North America, agricultural usage is declining, but demand from the defense and oxygen-device sectors remains steady. The NewMarket-AMPAC expansion is expected to meet the requirements of NASA and Department of Defense (DoD) programs by late 2026. In Europe, the only dedicated chlorate plant, located in Alby, benefits from Swedish hydropower for cost efficiency.

South America is emerging as a key player, with Nouryon's Mato Grosso do Sul project increasing regional output by 20% and utilizing biomass steam to reduce power costs. In the Middle East and Africa, growth is concentrated in Kenya and South Africa, primarily supported by Indian exports for cotton and mining applications. Overall, regions with renewable energy resources are attracting new chlorate investments, while areas reliant on fossil fuel grids face reduced margins.

Competitive Landscape

The Potassium Chlorate market is moderately fragmented. Nouryon highlights its global leadership in the supply of pyrotechnics-grade products from its Alby plant, providing customized particle curves under ISO 9001 and ISO 14001 certifications. NewMarket is investing USD 100 million to increase AMPAC's perchlorate production capacity by 50% for use in rocket motors, directly competing with chlorates in propulsion applications but not in oxygen candle production. Indian companies, including Vaighai Agro and Pandian Chemicals, utilize lower-cost power and labor to supply technical-grade powder to African and ASEAN cotton-growing regions.

Chinese manufacturers primarily cater to domestic demand for matches and fireworks but face potential sanctions related to dual-use exports. Emerging technologies, such as membrane salinity-gradient chlorine cells, have the potential to decentralize chlorate production at desalination plants, challenging the scale advantages of established producers. Additionally, traceability and compliance with REACH documentation are becoming critical differentiators for suppliers, as buyers in aerospace, pharmaceuticals, and mining increasingly require auditable supply chains.

Potassium Chlorate Industry Leaders

Vaighai Agro.

Chongqing Changshou Salt Chemical Co.,Ltd.

Occidental Chemical Corporation

Sichuan Chemical Works

Nouryon

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The EPA finalized a tolerance exemption for chlorate residues, specifically linked to potassium chlorate, resulting exclusively from post-harvest chlorine dioxide fumigation. This exemption took effect on January 30, 2026, and did not apply to pre-harvest defoliation uses.

- September 2024: Nouryon has started operations at an integrated facility for hydrogen peroxide, potassium chlorate, sodium chlorate, and chlorine dioxide in Ribas do Rio Pardo, Brazil. This facility adds renewable-powered capacity to the South American supply base, supporting the production of potassium chlorate used in various industrial applications.

Global Potassium Chlorate Market Report Scope

Potassium chlorate is a strong inorganic oxidizing agent that appears as a white crystalline powder. Its primary applications include use in explosives, fireworks, safety matches, and as a laboratory oxygen source. Due to its high reactivity, it is considered hazardous, with fire and explosion risks when combined with combustible materials.

The microporous insulation market is segmented by form, purity grade, application, end-user industry, and geography. By form, the market is segmented into powder, crystals, and flakes. By purity grade, the market is segmented into technical (less than or equal to 99 %) and laboratory (greater than or equal to 99%). By application, the market is segmented into safety matches, fireworks and explosives, agrochemicals (herbicides/defoliants), textile bleaching and printing, laboratory reagents and oxygen generators, and other applications (disinfectants, etc.). By end-user industry, the market is segmented into chemicals, agriculture, paper and textiles, defense and pyrotechnics, mining and safety equipment, and other end-user industries (lab, water treatment, etc.). The report also covers the market size and forecasts for microporous insulation in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Powder |

| Crystals |

| Flakes |

| Technical (Less than equal to 99 %) |

| Laboratory (Greater than equal to 99 %) |

| Safety Matches |

| Fireworks and Explosives |

| Agrochemicals (Herbicides/Defoliants) |

| Textile Bleaching and Printing |

| Laboratory Reagents and Oxygen Generators |

| Other Applications (Disinfectants, etc.) |

| Chemicals |

| Agriculture |

| Paper and Textiles |

| Defense and Pyrotechnics |

| Mining and Safety Equipment |

| Other End-user Industries (Lab, Water Treatment, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Form | Powder | |

| Crystals | ||

| Flakes | ||

| By Purity Grade | Technical (Less than equal to 99 %) | |

| Laboratory (Greater than equal to 99 %) | ||

| By Application | Safety Matches | |

| Fireworks and Explosives | ||

| Agrochemicals (Herbicides/Defoliants) | ||

| Textile Bleaching and Printing | ||

| Laboratory Reagents and Oxygen Generators | ||

| Other Applications (Disinfectants, etc.) | ||

| By End-User Industry | Chemicals | |

| Agriculture | ||

| Paper and Textiles | ||

| Defense and Pyrotechnics | ||

| Mining and Safety Equipment | ||

| Other End-user Industries (Lab, Water Treatment, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current market size of Potassium Chlorate Market?

The potassium chlorate market size is expected to increase from USD 0.74 billion in 2025 to USD 0.78 billion in 2026 and reach USD 1 billion by 2031, growing at a CAGR of 5.12% over 2026-203.

Why are flakes gaining share over powders?

Flakes offer higher density and tighter particle-size tolerances sought by pyrotechnics producers, propelling a 5.51% CAGR that outpaces the overall market.

How do renewable power sources influence production costs?

Facilities integrated with biomass or hydropower cut electricity costs, which account for over 60% of variable expense, allowing Brazilian and Swedish plants to out-compete fossil-grid peers.

What is driving substitution by perchlorate in defense?

Potassium perchlorate’s superior thermal stability and lower sensitivity meet stringent insensitive-munition standards, leading defense suppliers such as NewMarket’s AMPAC to expand perchlorate output by 50%.

Page last updated on: