Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

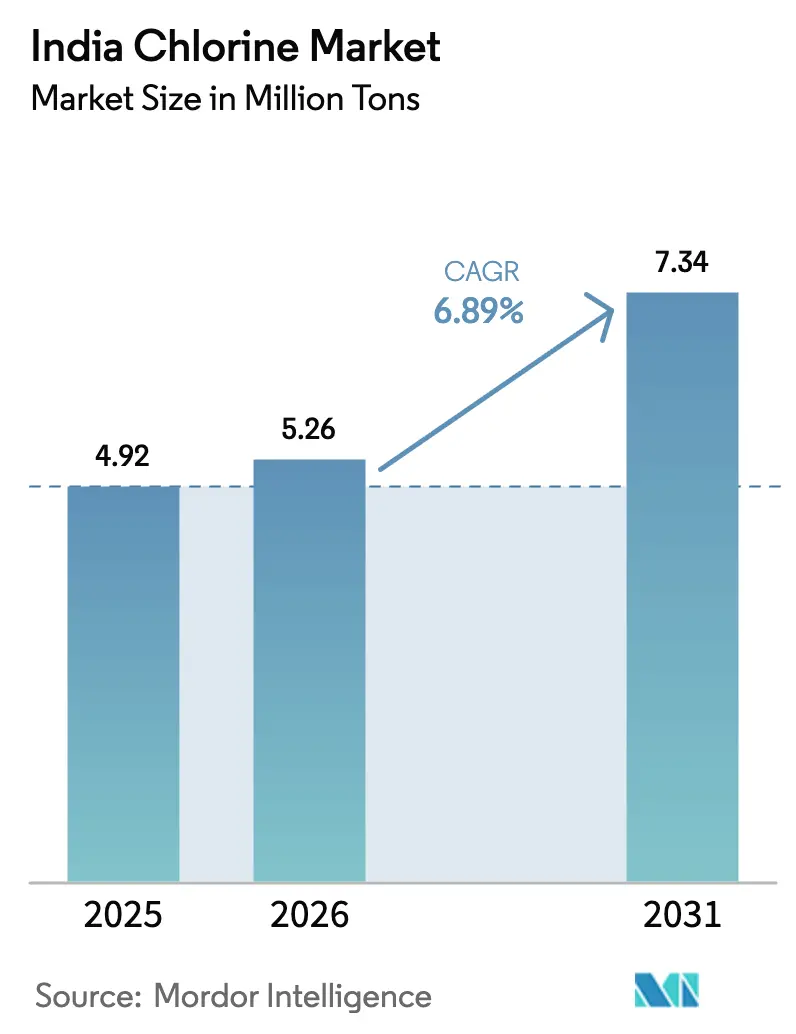

| Base Year Market Size (2025) | 4.92 Million tons |

| Market Volume (2026) | 5.26 Million tons |

| Market Volume (2031) | 7.34 Million tons |

| Growth Rate (2026 - 2031) | 6.89% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Chlorine Market Analysis by Mordor Intelligence

The India Chlorine Market size was valued at 4.92 Million tons in 2025 and estimated to grow from 5.26 Million tons in 2026 to reach 7.34 Million tons by 2031, at a CAGR of 6.89% during the forecast period (2026-2031). Steady capacity additions in polyvinyl chloride (PVC), rapid municipal water-treatment rollouts, and expanding pharmaceutical production give the India chlorine market a broad, multi-sector growth base. Producers continue to favor captive consumption strategies that shelter earnings from negative spot‐pricing swings while ensuring reliable feedstock for downstream vinyls, water-treatment chemicals, and specialty intermediates. The switch from mercury to membrane electrolysis improves cost positions by cutting electricity use and supporting compliance with stricter pollution norms. Integrated players with energy-efficient plants and downstream extensions are therefore consolidating their lead, even as regional demand spreads toward the eastern states.

Key Report Takeaways

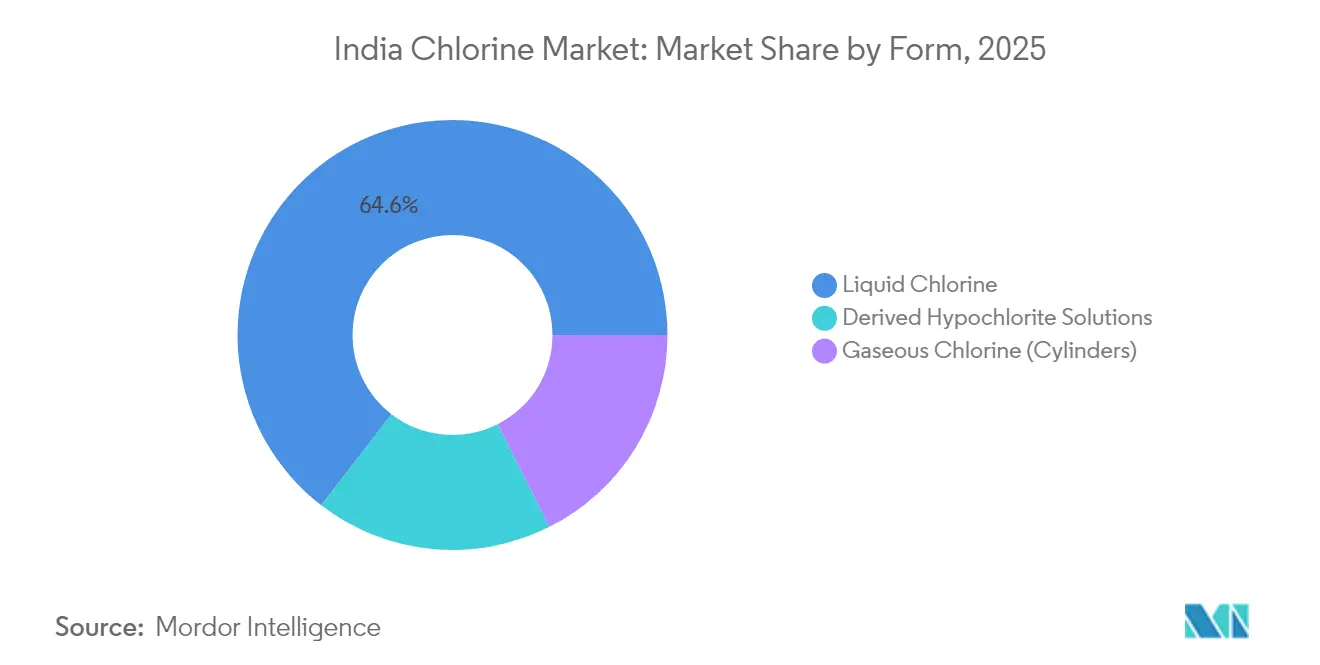

- By form, liquid chlorine held 64.55% of the India chlorine market share in 2025, whereas derived hypochlorite solutions are expanding at a 7.03% CAGR through 2031.

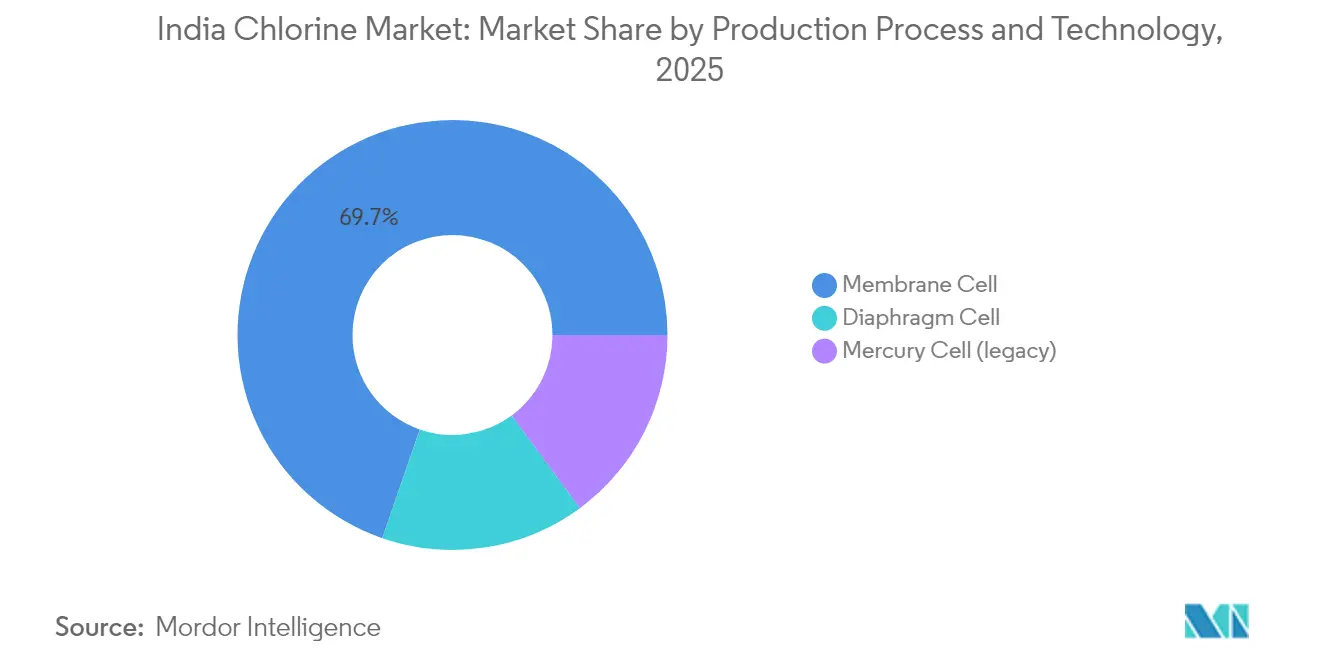

- By production technology, membrane cell accounted for 69.70% of the India chlorine market size in 2025 and is advancing at a 6.94% CAGR over the forecast horizon.

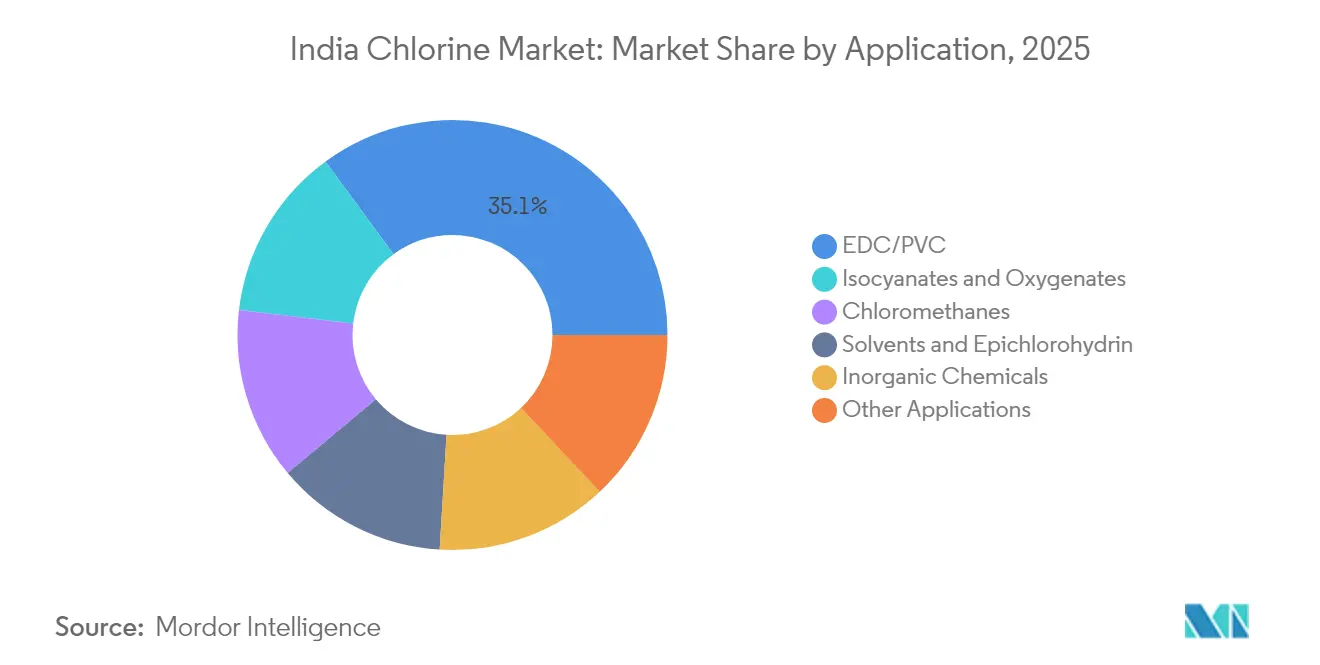

- By application, EDC/PVC led with 35.05% usage in 2025; isocyanates and oxygenates are projected to grow fastest at a 7.21% CAGR to 2031.

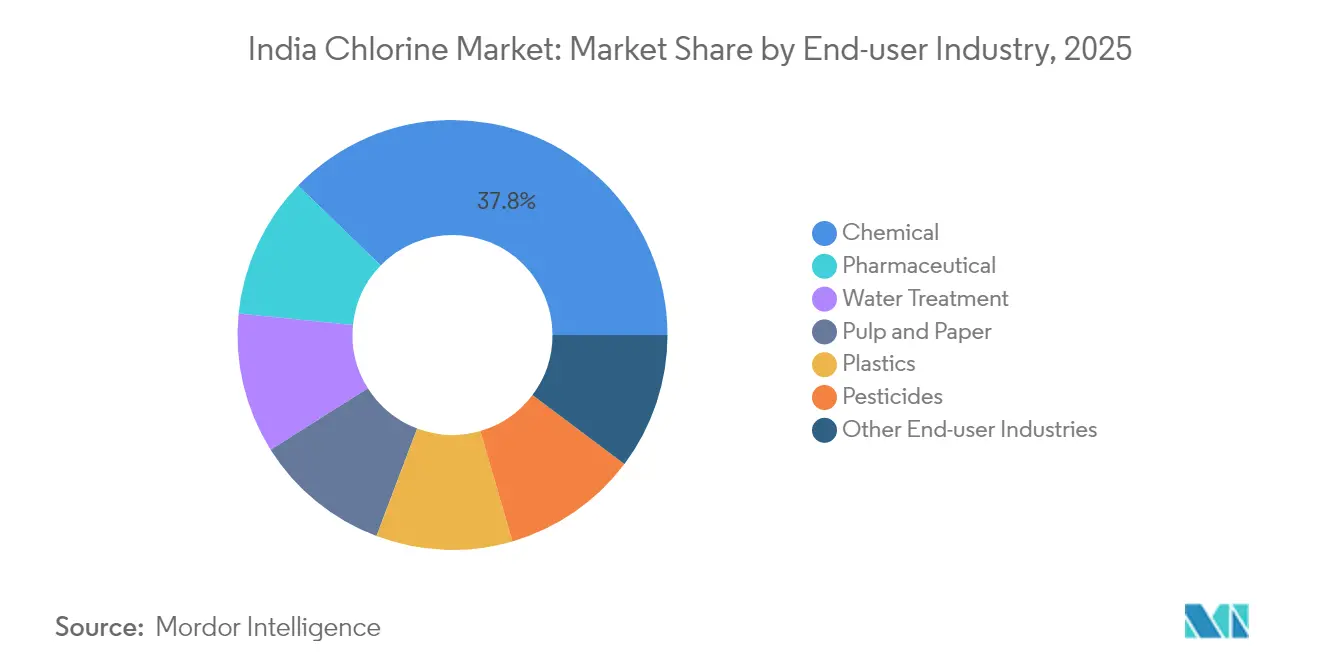

- By end-user industry, chemical accounted for 37.75% of overall consumption in 2025, while pharmaceutical is set to post a 7.38% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Chlorine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of PVC and CPVC Capacity Pipeline | +2.1% | West India, South India | Medium term (2-4 years) |

| Rapid Growth in Municipal Water-Treatment Infrastructure | +1.8% | National, with early gains in rural areas | Long term (≥ 4 years) |

| Strong Pharmaceuticals and Agro-Chemicals Output Linkage | +1.5% | West India, South India | Medium term (2-4 years) |

| Captive Consumption Strategy Amid Negative Chlorine Pricing | +1.0% | West India, South India | Short term (≤ 2 years) |

| Accelerated Switch to Membrane-Cell Technology Lowering Energy Cost | +1.2% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expansion of PVC and CPVC Capacity Pipeline

New PVC and CPVC plants are central to the next growth wave in the India chlorine market. Domestic PVC demand climbed 9% in 2024, encouraging firms such as Adani and Reliance to schedule multi-stage vinyl expansions that will lift captive chlorine offtake[1]Reliance Industries Ltd., “FY 2024 Annual Report,” ril.com . CPVC resin capacity at Epigral nearly tripled to 75,000 TPA in 2024, widening domestic supply for high-temperature piping and lowering import dependence. The capacity pipeline shifts the supply–demand balance by absorbing merchant chlorine and stabilizing realizations for integrated producers. Margin exposure to global vinyl price cycles remains, yet energy-efficient plants and port-adjacent logistics give western clusters a structural edge. Policymakers view vinyl import substitution as strategic for infrastructure, reinforcing offtake security for chlorine producers.

Rapid Growth in Municipal Water-Treatment Infrastructure

The Jal Jeevan Mission lifted rural piped-water coverage to 79.74% of households by March 2025, creating a non-cyclical demand channel for chlorine disinfectants. Municipal operators favor hypochlorite because it simplifies storage and dosing in decentralized schemes. Rising urban wastewater volumes also require chlorine dosing at sewage plants to meet pathogen limits prescribed by the Bureau of Indian Standards. As water coverage expands into underserved eastern districts, chlorine usage disperses geographically and lowers the historic concentration in Gujarat-centered industrial corridors. Long-term budget allocations further insulate water-treatment demand from macro swings that affect commodity chemicals.

Strong Pharmaceuticals and Agro-Chemicals Output Linkage

Chlorine-based intermediates remain indispensable for India’s agrochemical exports, which reached USD 5.5 billion in 2024. Production Linked Incentive (PLI) schemes for APIs and bulk drugs spur new domestic facilities that intensify chlorine procurement. Registration approvals for 118 active molecules in 2024 included several chlorinated compounds, underpinning steady intermediate demand. Export-oriented formulators lean on backward integration to secure chlorine derivatives, reducing exposure to import logistics. Rising environmental norms in key importing regions also favor compliant Indian manufacturers, sustaining chlorine pull from the specialty chemical value chain.

Captive Consumption Strategy Amid Negative Chlorine Pricing

When caustic-soda prices climb but chlorine prices fall, integrated operators redirect chlorine internally rather than release it into a weak merchant market. Grasim reached a 62% chlorine integration rate in FY 2024, limiting its exposure to spot volatility. Such strategies smooth revenue, justify continuous plant operation, and support downstream projects in EDC, epichlorohydrin, and chloromethanes. Captive models gain further relevance as western clusters grapple with high storage costs and transport restrictions on gaseous chlorine. The approach reinforces the position of diversified conglomerates in the India chlorine market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Environmental and Worker-Safety Regulations | -1.2% | National, with stricter enforcement in West India | Short term (≤ 2 years) |

| Excess Caustic-Soda Capacity Creating Chlorine Oversupply | -0.8% | West India, South India | Medium term (2-4 years) |

| Limited Downstream Integration (Disposal Logistics Cost) | -0.6% | East India, North India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Environmental and Worker-Safety Regulations

The Central Pollution Control Board includes chlor-alkali in its red category, requiring comprehensive impact assessments for any expansion. Zero-liquid-discharge norms add costly evaporators and crystallizers, pushing up unit capital cost. Plants using legacy mercury cells face stranded assets and must invest heavily in brine-filtration, membranes, and gas handling equipment to comply. Worker-safety norms mandate specialized personal protective gear, leak-detection systems, and on-site emergency response teams. Smaller standalone producers often struggle with the capital load, tilting the India chlorine industry toward larger, better-funded operators.

Excess Caustic-Soda Capacity Creating Chlorine Oversupply

Total caustic-soda capacity hit 320,430 TPA by March 2025, outpacing domestic demand growth and forcing plants to run at lower operating rates. Because chlorine production is chemically linked to caustic output, oversupply drags chlorine realizations down. Export options relieve caustic imbalance yet cannot absorb the concurrent chlorine surplus. Smaller plants lacking downstream chlorine integration sell into a weak merchant market and face high freight costs for liquid shipments. Integrated majors shield themselves by channeling chlorine into EDC, PVC, and chlorinated solvents, keeping utilization steady during pricing troughs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Liquid Chlorine Dominance Drives Infrastructure Efficiency

Liquid chlorine accounted for 64.55% of the India chlorine market share in 2025, anchored by well-developed rail and tanker infrastructure between Gujarat’s production hubs and downstream consumers. The India chlorine market size for hypochlorite solutions is, however, set to expand briskly as municipal schemes prefer safer, diluted products with simpler logistics. Gaseous cylinders remain a niche choice for small-scale users who value precise dosing over bulk-handling economics.

Liquid chlorine continues to dominate large EDC plants that require uninterrupted, high-purity feedstock. Western ports simplify raw salt supply, and pipelines in Dahej and Bharuch enable direct transfers to vinyl units. Meanwhile, hypochlorite gains ground in health-care facilities and public utilities seeking low-risk chlorine handling. State water boards issue tenders that explicitly favor local hypochlorite supply, redirecting some volume away from pressurized gas formats. Overall, diversifying form preferences enrich the value proposition for integrated producers.

By Production Process and Technology: Membrane Cell Technology Captures Market Leadership

Membrane technology captured 69.70% of overall output in 2025 and is projected to grow at 6.94% through 2031, reflecting its critical role in the India chlorine market. Diaphragm cells hang on in a few plants where brine purity is easier to manage, while mercury cells are fast approaching retirement.

The India chlorine market size gains efficiency as membrane units roll out advanced rectifiers that raise current density without overheating. Operators invest in nanofiltration to strip sulfates and calcium, cutting brine purge volumes by up to 90%. Hydrogen co-produced from membrane plants feeds new hydrogen-peroxide lines and onsite boilers, securing incremental revenue streams. Equipment suppliers betting on diaphragm retrofits are pivoting toward turnkey membrane packages that promise quick payback under high power tariffs.

By Application: EDC/PVC Leadership Faces Specialty Chemical Competition

EDC/PVC applications absorbed 35.05% of chlorine in 2025, driven by import-substitution policies that encourage local vinyl production. At the same time, isocyanates and oxygenates are recording a 7.21% CAGR as polyurethane demand grows in refrigeration, automotive, and insulation markets.

The India chlorine market size tied to EDC/PVC remains large, yet specialty chemicals are chipping away by offering higher margins and lower cyclicality. Epigral’s new chlorotoluenes line exemplifies how producers migrate to value-added derivatives. Epichlorohydrin volumes that feed epoxy resins also respond to the electronics and electric-vehicle sectors. Demand diversity broadens chlorine usage and cushions the impact of PVC margin swings linked to global capacity additions.

By End-user Industry: Chemical Industry Dominance Amid Pharmaceutical Acceleration

Chemical industry consumed 37.75% of total volume in 2025, underscoring the centrality of integrated complexes in Gujarat and Tamil Nadu. Pharmaceutical industry, however, is rising at a 7.38% CAGR to 2031, supported by government PLI incentives for APIs.

Within chemicals, captive chlorine moves into chloromethanes, solvents, and fluoropolymers. Water-treatment demand scales with new sewage and effluent plants in urban belts. The India chlorine market size associated with pharmaceuticals grows as companies add multi-purpose plants that leverage chlorine chemistry for high-value intermediates. Chemplast Sanmar’s USD 121 million expansion confirms this pivot toward custom manufacturing for regulated markets.

Geography Analysis

West India generated 36.20% of 2025 volume, reflecting the dominance of Gujarat’s salt resources, port access, and co-located downstream clusters. Integrated complexes in Dahej channel chlorine straight into vinyls, epichlorohydrin, and chlorinated solvents. State environmental rules favor large units able to finance membrane upgrades. The India chlorine market share in the west therefore remains stable, even as older mercury cells retire.

East and North-East India is the fastest-expanding region at a 7.05% CAGR. Government incentives lower project costs, and new industrial corridors create fresh offtake for chlorine derivatives. Jal Jeevan Mission contracts in Bihar and Assam pull hypochlorite demand eastward, easing regional supply imbalances. Producers consider barge and rail solutions to connect eastern plants with raw salt and caustic-soda markets in the west.

South India maintains consistent growth on the back of specialty chemicals and pharma clusters in Tamil Nadu, Andhra Pradesh, and Telangana. Chlorine moves into CPVC, APIs, and pesticides produced in these states. North India shows steady, though moderate, gains as water-treatment and plastic-pipe plants roll out, depending on chlorine shipments from western plants until local capacity materializes. Collectively, regional diversification dilutes historical concentration and supports a resilient India chlorine market.

Competitive Landscape

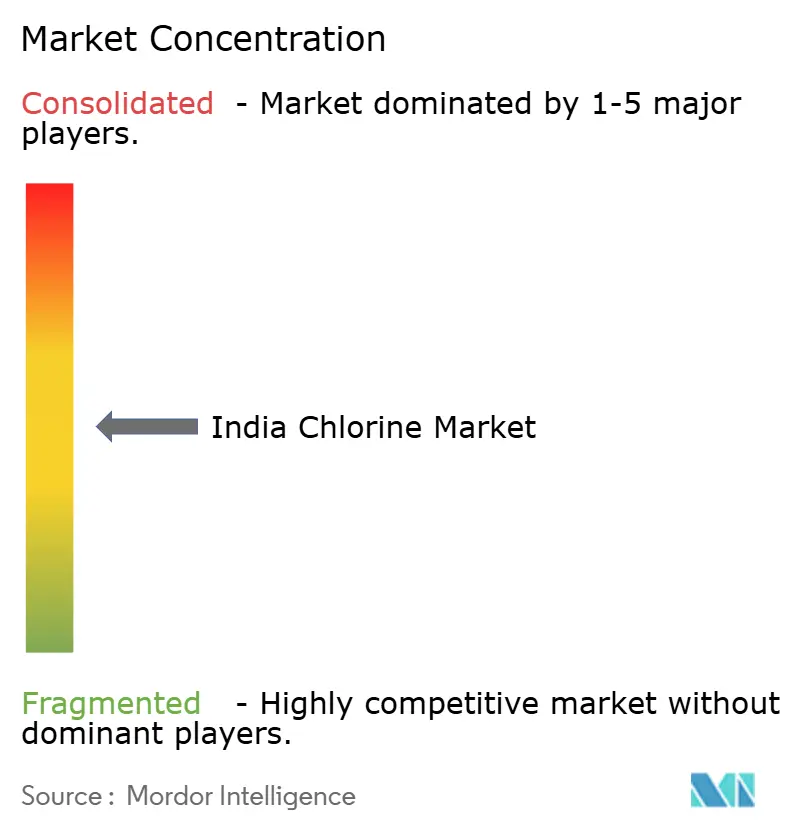

The India chlorine market features a moderately concentrated field where Reliance Industries, Tata Chemicals, and Grasim Industries anchor capacity. Reliance integrates chlorine into one of the world’s largest vinyl chains, insulating its electrolysis units from merchant swings. Grasim leverages a 62% integration rate that channels chlorine into epoxy, chloromethane, and textile-grade caustic[2]Grasim Industries Ltd., “Investor Presentation FY 2024,” grasim.com . Tata Chemicals balances export caustic sales with domestic chlorine derivative projects.

Second-tier players such as DCM Shriram, Epigral, and Chemplast Sanmar advance through specialty derivatives. Epigral’s chlorotoluenes facility inaugurates a differentiated aromatic chlorination platform. Chemplast Sanmar funnels chlorine into custom pharmaceuticals and paste PVC, broadening its earnings mix. As mercury-cell phase-outs accelerate, capital intensity rises, prompting alliances with technology providers and engineering contractors.

Emerging entrants eye membrane revamps bundled with captive power and hydrogen valorization. Central Pollution Control Board norms accelerate consolidation because smaller standalone plants face disproportionate compliance costs. Integrated majors acquire distressed assets to secure regional footholds, maintaining the moderate concentration that characterizes the India chlorine industry.

India Chlorine Industry Leaders

Grasim Industries Limited (Aditya Birla)

Gujarat Alkalies and Chemicals Limited

DCM Shriram

Chemplast Sanmar Limited

NIRMA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: DCM Shriram and Aarti Industries Ltd. formed a long-term partnership, making DCM Shriram the exclusive chlorine supplier to Aarti Industries' new Jhagadia facility in Gujarat. The agreement includes a new underground chlorine pipeline, which will increase Aarti's daily chlorine consumption by 200 tonnes, thereby improving operational efficiency.

- March 2025: Gujarat Alkalies and Chemicals Limited (GACL) inaugurated its 30,000-tonne-per-annum chlorotoluenes plant in Dahej, which utilizes chlorine for production. The facility produces chlorine-based value-added chemicals, including benzyl chloride, benzyl alcohol, and benzaldehyde, with the aim of boosting exports and creating employment.

India Chlorine Market Report Scope

Chlorine is the most abundant element in the periodic table's halogen family. It is a critical component of the chemical and pharmaceutical industries. Chlorine contributes to advancements in fields as diverse as disinfecting, medicine, and public safety. The Indian chlorine market is segmented by application and end-user industry. By application, the market is segmented into EDC/PVC, isocyanates and oxygenates, chloromethanes, solvent and epichlorohydrin, inorganic chemicals, and other applications. By end-user industry, the market is segmented into water treatment, pharmaceuticals, chemicals, pulp and paper, plastics, pesticides, and other end-user industries. For each segment, market sizing and forecasts have been done on the basis of volume (kilotons).

By Form

| Liquid Chlorine |

| Gaseous Chlorine (Cylinders) |

| Derived Hypochlorite Solutions |

By Production Process and Technology

| Membrane Cell |

| Diaphragm Cell |

| Mercury Cell (legacy) |

By Application

| EDC/PVC |

| Isocyanates and Oxygenates |

| Chloromethanes |

| Solvents and Epichlorohydrin |

| Inorganic Chemicals |

| Other Applications |

By End-user Industry

| Chemical |

| Water Treatment |

| Pharmaceutical |

| Pulp and Paper |

| Plastics |

| Pesticides |

| Other End-user Industries |

| By Form | Liquid Chlorine |

| Gaseous Chlorine (Cylinders) | |

| Derived Hypochlorite Solutions | |

| By Production Process and Technology | Membrane Cell |

| Diaphragm Cell | |

| Mercury Cell (legacy) | |

| By Application | EDC/PVC |

| Isocyanates and Oxygenates | |

| Chloromethanes | |

| Solvents and Epichlorohydrin | |

| Inorganic Chemicals | |

| Other Applications | |

| By End-user Industry | Chemical |

| Water Treatment | |

| Pharmaceutical | |

| Pulp and Paper | |

| Plastics | |

| Pesticides | |

| Other End-user Industries |

Key Questions Answered in the Report

How large is the India chlorine market in 2026?

The India chlorine market size is 5.26 million tons in 2026.

What CAGR is projected for chlorine demand in India through 2031?

Demand is forecast to rise at a 6.89% CAGR between 2026 and 2031.

Which production technology holds the largest share?

Membrane cell technology accounts for 69.70% of current capacity.

Why is West India dominant in chlorine production?

Gujarat’s salt resources, port access, and integrated petrochemical clusters give West India a 36.20% market share.

Page last updated on: