United States Freestanding Emergency Department Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

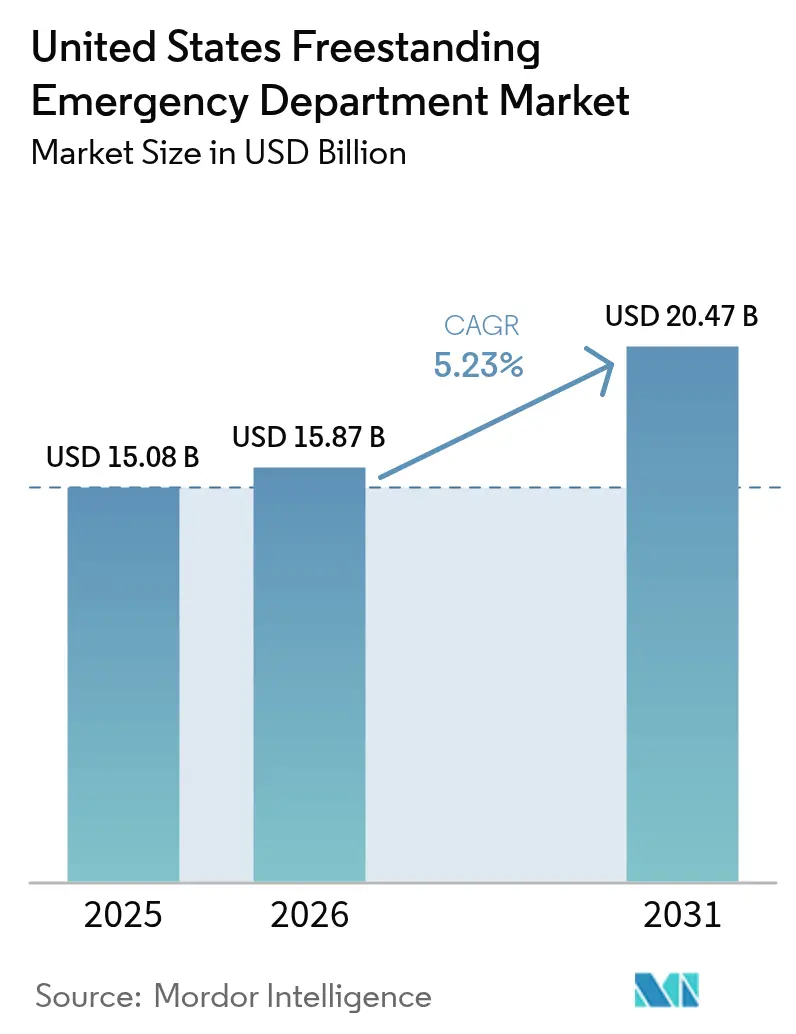

| Base Year Market Size (2025) | USD 15.08 Billion |

| Market Size (2026) | USD 15.87 Billion |

| Market Size (2031) | USD 20.47 Billion |

| Growth Rate (2026 - 2031) | 5.23% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Freestanding Emergency Department Market Analysis by Mordor Intelligence

The United States Freestanding Emergency Department Market size was valued at USD 15.08 billion in 2025 and is estimated to grow from USD 15.87 billion in 2026 to reach USD 20.47 billion by 2031, at a CAGR of 5.23% during the forecast period (2026-2031).

This steady expansion reflects a structural shift in how emergency care is delivered, driven by migration into high-growth suburbs, state-level deregulation, and hospital strategies that favor capital-light outpatient footprints. Hospital systems deploy AI-enabled triage tools that shorten door-to-provider times, while independent operators move quickly into rural pockets where critical-access hospitals have closed. Population aging, the spread of high-deductible health plans, and federal New Access Points grants together deepen demand for proximate, lower-wait-time emergency services. Competitive positioning increasingly hinges on the ability to combine diagnostic imaging and laboratory services with emergency medicine staffing in facilities located near busy retail corridors.

Key Report Takeaways

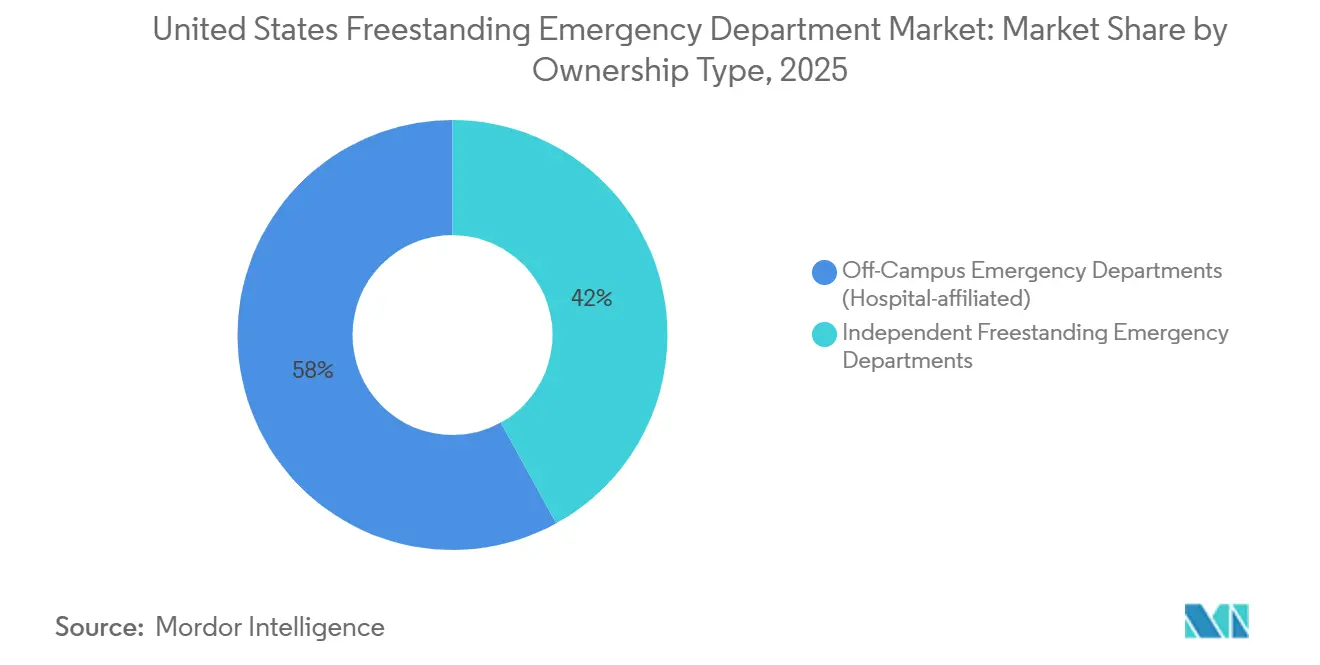

- By ownership type, hospital-affiliated off-campus emergency departments led with 58.02% revenue share in 2025, while independent freestanding emergency departments are projected to expand at a 5.87% CAGR through 2031.

- By service, emergency care and other services accounted for 58.37% of revenue in 2025, and imaging services are forecast to grow at a 6.39% CAGR through 2031.

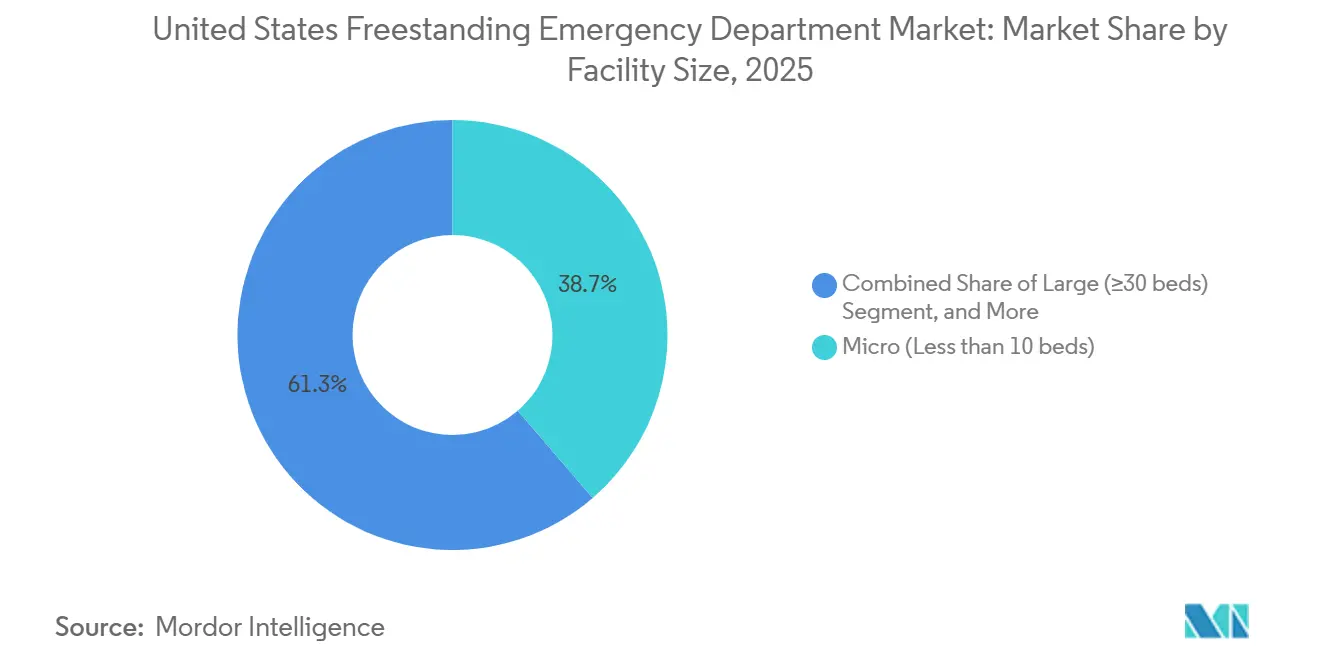

- By facility size, micro facilities with fewer than 10 beds held a 38.70% share in 2025, while medium-sized facilities with 20 to 29 beds are advancing at a 6.80% CAGR through 2031.

- By U.S. census region, the South accounted for 45.62% of the value in 2025, and the West is projected to grow at a 6.15% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Freestanding Emergency Department Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Consumer-driven health plans and federal grant programmes | + 0.9% | National, with concentrated gains in rural and underserved areas receiving federal Rural Health Transformation funding | Medium term (2-4 years) |

| Rising demand for convenience-care access | + 1.2% | Suburban corridors across South and West census regions, particularly Texas, Arizona, Colorado metro areas | Short term (≤ 2 years) |

| Expansion of hospital outpatient strategies | + 1.0% | National, led by large health systems deploying off-campus sites | Medium term (2-4 years) |

| Rapid uptake of AI-enabled triage and ambient documentation | + 0.7% | Early adoption in large urban systems, spillover to independent operators in competitive markets | Long term (≥ 4 years) |

| Hybrid ED/urgent-care co-licensing models | + 0.5% | States with flexible licensing frameworks such as Delaware, Tennessee, Colorado | Long term (≥ 4 years) |

| State-level regulatory easing (CON exemptions) | + 0.8% | Tennessee, Colorado, Arizona, and states considering certificate-of-need reform | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer-Driven Health Plans and Federal Grant Programmes

Federal grant programs lower capital barriers and address workforce shortages by tying loan repayments to medically underserved areas. The FY 2025 budget doubles community health center financing, positioning freestanding emergency departments as referral anchors that can absorb emergency demand for 37 million Americans.[1]Source: Health Resources and Services Administration, “FY 2025 Budget Tackles Gaps in Access to Primary Care,” HRSA.GOV In 2026, federal support plays a pivotal role, highlighted by a USD 204 million grant allocated to New Hampshire under the Rural Health Transformation Program. This funding is part of a broader USD 50 billion national initiative spanning 2026 to 2030 aimed at enhancing access to emergency and urgent care in underserved counties. Additional funding is directed toward telehealth infrastructure and advanced practice provider training, ensuring 24/7 coverage in areas with limited on-site emergency physicians. Utilization trends indicate a divide by income: higher earners prioritize time savings despite higher facility fees, while lower-income individuals often delay visits until conditions worsen. Independent operators are strategically expanding into suburban areas, offering services that align with these utilization patterns.

Rising Demand for Convenience-Care Access

Patient surveys show that door-to-provider times under 15 minutes strongly influence facility choice; freestanding emergency departments routinely meet this threshold, whereas hospital EDs average 45 minutes or more.[2]Source: The Journal of Healthcare Contracting, “Health Systems Gobble Up Urgent Care Locations,” JHCONLINE.COM Health-system acquisitions of urgent-care chains illustrate strategic alignment around convenience: HCA Healthcare acquired 41 Texas centers in 2025 to create feeder networks for nearby freestanding EDs. Facilities situated along commuter routes capture after-work traffic and divert non-life-threatening cases from congested hospital campuses. Hybrid facilities that combine urgent-care and emergency licensure allow on-site physicians to direct nearly 70% of visits to lower-acuity billing, improving patient affordability while preserving emergency capabilities.

Expansion of Hospital Outpatient Strategies

Major systems now allocate more than half of their capital budgets to outpatient projects. HCA Healthcare’s USD 6 billion pipeline will add up to 20 outpatient locations per hospital by 2030, with freestanding emergency departments serving as anchors that cross-sell imaging, surgery, and specialty consults. Site-of-care migration could unlock USD 50 billion in value as payers incentivize treatment outside inpatient settings. AI-powered ambient documentation tools embedded in emergency bays reduce clinician charting time by 80%, supporting higher patient throughput. CommonSpirit Health, with a national network spanning 140 hospitals and more than 2,200 care sites across 24 states, continues to emphasize community-based emergency access that reduces main-campus crowding and improves experience metrics linked to reimbursement incentives.

Rapid Uptake of AI-Enabled Triage and Ambient Documentation

AI-enabled triage and ambient documentation tools are shortening throughput times while reducing dependence on in-demand emergency physicians, although rollout is uneven because of malpractice concerns and the need to align with legacy EHR workflows. A 2024 Kaiser Permanente study reported that large language models reached 72% accuracy in emergency department triage, with performance falling in cases involving multiple comorbidities or atypical symptoms, which signals hybrids of clinician oversight and AI augmentation as the practical path in the near term. Ambient documentation solutions that transcribe visits in real time and complete charts are cutting paperwork by 30% to 40%, which frees physician time for additional encounters and improves job satisfaction. Independent operators often adopt these tools faster because they face fewer IT governance layers and can contract directly with vendors, whereas large health systems must align procurement and risk review across many stakeholders.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High total cost per visit vs urgent-care alternatives | - 0.8% | National, with acute sensitivity in Midwest and Northeast regions where urgent care density is highest | Short term (≤ 2 years) |

| CMS reimbursement and billing-policy volatility | - 1.1% | National, particularly impacting non-excepted off-campus emergency departments subject to site-neutral payment reductions | Medium term (2-4 years) |

| Price-transparency pressure on facility fees | - 0.6% | National, with enforcement concentrated in states with additional transparency mandates such as Colorado and California | Medium term (2-4 years) |

| Staffing shortages and wage inflation | - 0.9% | National, with severe constraints in rural markets and in states with restrictive scope-of-practice laws for advanced practice providers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Total Cost Per Visit Vs Urgent-Care Alternatives

Freestanding emergency departments typically charge facility fees of USD 1,500 to USD 3,000 per visit across acuity levels, compared to USD 100 to USD 200 in urgent care for many low-complexity conditions, raising consumer cost concerns and reputational risk. Commercial payers are responding with prior authorization, network design, and differential cost-sharing to steer avoidable visits to lower-cost sites, thereby narrowing the pool of commercially insured patients willing to absorb higher out-of-pocket costs. High-deductible plan designs amplify this friction because members pay the full facility fee until they reach deductibles, which drives negative reviews when patients later learn their visit was processed as out-of-network. Urgent care chains are countering convenience by expanding late hours, adding on-site diagnostics, and publishing clear prices to compete head-to-head for minor illnesses and injuries.

CMS Reimbursement and Billing-Policy Volatility

The 2025 Hospital Outpatient Prospective Payment System final rule reshapes quality-reporting requirements and prior-authorization thresholds, adding administrative cost layers for independent facilities. Out-of-network status with large commercial plans exposes patients to surprise bills, erodes satisfaction, and triggers reputational risk. Compliance with the No Surprises Act obliges facilities to invest in expanded revenue-cycle teams, tempering EBITDA margins. Independent freestanding emergency departments face a different constraint because they cannot bill facility fees under OPPS unless they convert to hospital outpatient status, which would then bring EMTALA obligations, charity care policies, and, in some states, certificate-of-need oversight. Medicare Advantage carriers are using plan networks and cost-sharing levers to steer enrollees toward urgent care or primary care for lower-acuity conditions, citing higher total costs of care when those cases present to freestanding emergency departments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Ownership Type: Hospital Networks Defend Share as Independents Exploit Regulatory Gaps

Off-campus emergency departments held a 58.02% share of the United States freestanding emergency department market in 2025, leveraging integrated electronic health records, favorable Medicare Part B billing, and hospital referral streams. Independent centers, though smaller in aggregate footprint, are projected to outpace at a 5.87% CAGR through 2031 as entrepreneurial groups exploit regulatory gaps in counties underserved by hospitals.

Hospital systems continue to treat off-campus units as strategic beachheads that deter competitors. HCA Florida’s USD 70 million plan to open three new sites across Pasco, Hernando, and Citrus Counties exemplifies an asset-light expansion play that places branded emergency access within 10 miles of growing subdivisions. Independent operators counter by specializing in pediatric trauma or geriatric-friendly environments, differentiating on shorter triage queues and concierge-style amenities.

By Service: Imaging Revenue Surges as AI Interpretation Compresses Diagnosis Timelines

Emergency care and other services represented 58.37% of the United States freestanding emergency department market size in 2025, underscoring the core use case that drove early adoption. Imaging, however, is forecast to be the fastest-growing line at 6.39% CAGR, buoyed by high-resolution CT and point-of-care ultrasound installations that generate premium reimbursements.

High-throughput diagnostic suites allow physicians to rule out stroke, pulmonary embolism, or appendicitis within 30 minutes, aligning with value-based contracts that penalize avoidable inpatient admissions. Laboratory panels are increasingly automated, cutting stat chemistry turnaround to under 15 minutes and supporting tighter door-to-decision cycles.

By Facility Size: Medium Configurations Gain as Operators Balance Throughput and Capital Efficiency

In 2025, micro facilities with fewer than 10 beds accounted for 38.70% of the U.S. freestanding emergency department market. Their popularity stems from compact real estate requirements, a lean staffing model of 2 to 3 nurses per shift, and streamlined permitting processes, making them well-suited for retail plazas and strip-mall conversions. Medium-sized facilities with 20 to 29 beds represent the fastest-growing segment, projected to grow at a 6.80% CAGR through 2031. This configuration is increasingly preferred as it effectively balances imaging utilization, laboratory throughput, and the capacity to stabilize higher-acuity patients before transfer. Small facilities, with 10 to 19 beds, remain a practical option in markets with moderate demand and uncertain growth trajectories. In contrast, extensive facilities with 30 or more beds are less common due to their cost structure and regulatory challenges, which resemble those of full-service hospitals without the benefit of a comparable case mix or trauma designation.

Geography Analysis

In 2025, the South census region is projected to hold a significant 45.62% share of the U.S. freestanding emergency department market. This growth is primarily driven by Texas's regulatory framework, which enables the expansion of both hospital-affiliated and independent freestanding emergency departments without requiring certificate-of-need approval. Consequently, cities such as Dallas-Fort Worth, Houston, Austin, and San Antonio are experiencing a high density of these facilities. In 2024, Texas saw a population increase of 473,000 residents, with growth concentrated in suburban counties that prioritize convenient access along major corridors. Florida is also expanding its market presence through strategic hospital system deployments, supported by networks like AdventHealth, which has a strong footprint in Orlando and Tampa. In Tennessee, a 2025 law is accelerating the establishment of satellite emergency departments. These facilities, exempt from certificate-of-need review if located within 10 miles of a parent hospital, are being developed in areas such as Nashville, Memphis, and Knoxville, where several major systems operate.

The West is the fastest-growing region, with a projected CAGR of 6.15% through 2031. This growth is fueled by population inflows into cities like Phoenix, Denver, Las Vegas, and Colorado Springs, while urban hospital emergency departments remain concentrated in downtown areas. Colorado's absence of certificate-of-need requirements for freestanding sites facilitates faster market entry, with timelines ranging from 12 to 18 months from site selection to operational launch under current licensure processes. While Las Vegas, Nevada, is experiencing strong metro growth, the state has been slower to develop freestanding sites than neighboring Western states, leaving opportunities for independent entrants in certain areas. In contrast, Midwestern and Northeastern states face challenges due to higher urgent care density and stricter certificate-of-need regulations. These factors extend development timelines and limit the supply of new facilities relative to demand growth. Additionally, several Northeastern metropolitan areas encounter high real estate costs, which reduce the profitability of freestanding emergency facilities compared to outpatient alternatives.

Competitive Landscape

In the fragmented U.S. freestanding emergency department market, no single operator commands more than a 15% national share. This is largely due to varying state licensing regimes and certificate-of-need exemptions, which create local entry conditions that favor regional growth over national consolidation. HCA Healthcare, with its extensive network of 186 hospitals and over 2,300 care sites, operates numerous freestanding emergency departments in Florida, Texas, and Tennessee. The company leverages its scale to secure advantageous payer contracts and invests in AI-driven workflows to optimize operational efficiency. Tenet Healthcare, managing 60 hospitals and 570 outpatient centers, focuses on suburban areas where off-campus emergency departments can attract commercially insured patients before they turn to independent competitors.

Western states, particularly Nevada, Idaho, and Utah, offer significant growth opportunities as suburban expansion has outpaced hospital-led freestanding deployments. Additionally, rural markets are benefiting from federal grants and state partnerships aimed at stabilizing 24/7 coverage. Technology adoption is becoming a critical differentiator, with operators integrating AI-assisted radiology interpretations and ambient documentation to reduce labor pressures and enhance patient experiences. However, challenges such as integration complexities with legacy EHRs and inconsistencies in malpractice policies are slowing the uniform implementation of these technologies across larger systems.

United States Freestanding Emergency Department Industry Leaders

CHRISTUS Health

Ascension

Emerus Hospital Partners, LLC.

Universal Health Services, Inc.

HCA Healthcare

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Ascension Saint Thomas, in partnership with Murfreesboro Medical Clinic (MMC), announced plans to expand emergency care services in Rutherford County. Subject to regulatory approval, a new freestanding emergency department will be constructed on MMC’s Lascassas Pike property, providing 24/7 emergency care to the community.

- September 2025: The Health Care Authority of the City of Anniston (RMC), Jacksonville State University (Jax State), the City of Jacksonville, and Developer Solutions and Facilities Development Company (DSF) collaborated to enhance emergency healthcare access by moving forward with plans to establish a freestanding emergency department (FED) in Jacksonville.

- March 2025: California Senate Bill 588 proposed a statewide study on deploying freestanding emergency departments to mitigate healthcare deserts.

- July 2025: CMS introduced post-PHE guidance enabling licensed freestanding emergency departments to directly participate in Medicare and Medicaid programs, enhancing surge capacity capabilities.

- March 2025: California proposed Senate Bill 588 to conduct a statewide study on deploying freestanding emergency departments to address healthcare access gaps in underserved areas.

- January 2025: HCA Healthcare announced its intention to open 15 additional freestanding emergency departments across Florida, Texas, and Tennessee by 2026. This initiative, representing a USD 150 million capital investment, aims to address suburban demand while strategically positioning facilities within 10 to 15 miles of existing hospital campuses. The expansion leverages Tennessee's certificate-of-need exemption for satellite emergency departments and Florida's favorable licensing environment.

United States Freestanding Emergency Department Market Report Scope

As per the scope of the report, freestanding emergency departments (FSEDs) are healthcare facilities that provide emergency services but are not located on hospital campuses. These FSEDs can be owned by hospitals or act independently.

The US Freestanding Emergency Department Market is segmented by ownership type, consisting of hospital-affiliated and independent subsegments, and by service, consisting of laboratory service, imaging service, emergency care, and other services. By facility size, the market is segmented into micro (<10 beds), small (10-19 beds), medium (20-29 beds), and large (30+ beds). By U.S. Census region, the market is segmented into the Northeast, Midwest, South, and West. The report offers market size and forecasts in value (USD) for the above segments.

| Off-Campus Emergency Departments (Hospital-affiliated) |

| Independent Freestanding Emergency Departments |

| Emergency Care & Other Services |

| Imaging Services |

| Laboratory Services |

| Micro (<10 beds) |

| Small (10-19 beds) |

| Medium (20-29 beds) |

| Large (>30 beds) |

| Northeast |

| Midwest |

| South |

| West |

| By Ownership Type | Off-Campus Emergency Departments (Hospital-affiliated) |

| Independent Freestanding Emergency Departments | |

| By Service | Emergency Care & Other Services |

| Imaging Services | |

| Laboratory Services | |

| By Facility Size (Bed Count) | Micro (<10 beds) |

| Small (10-19 beds) | |

| Medium (20-29 beds) | |

| Large (>30 beds) | |

| By U.S. Census Region | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

What is the current size and 2031 outlook for the United States freestanding emergency department market?

The market is USD 15.87 billion in 2026 and is projected to reach USD 20.47 billion by 2031 at a 5.23% CAGR.

Which service line is growing fastest in the United States freestanding emergency department space?

Imaging services are the fastest-growing, advancing at a 6.39% CAGR through 2031 as AI interpretation and point-of-care ultrasound compress diagnosis times.

How are regulations shaping independent growth in the United States freestanding emergency department ecosystem?

States such as Texas and Colorado permit freestanding sites without certificate-of-need approvals, while CMS site-neutral rules and No Surprises Act constraints shape billing and margins.

Which regions are leading and accelerating within the United States freestanding emergency department landscape?

The South holds 45.62% share led by Texas, and the West is the fastest-growing at a 6.15% CAGR driven by suburban migration into metros such as Phoenix and Denver.

How is AI changing throughput and documentation in United States freestanding emergency departments?

Large language models have shown 72% triage accuracy in one 2024 study, and ambient documentation tools are reducing charting time by 30% to 40%, which increases clinician capacity.

What are the primary margin risks for United States freestanding emergency department operators?

Site-neutral payment cuts for non-excepted off-campus sites, price-transparency enforcement on facility fees, and payer steerage toward urgent care increase revenue pressure, especially where urgent care density is high.

Page last updated on: