Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

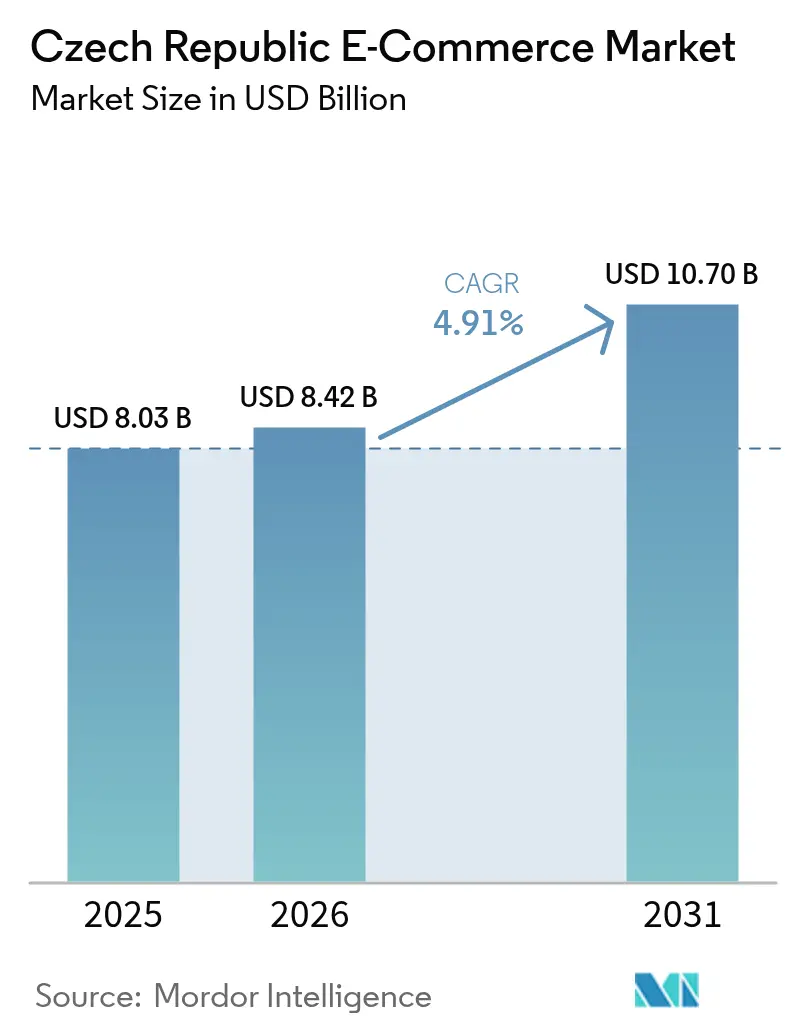

| Base Year Market Size (2025) | USD 8.03 Billion |

| Market Size (2026) | USD 8.42 Billion |

| Market Size (2031) | USD 10.7 Billion |

| Growth Rate (2026 - 2031) | 4.91% CAGR |

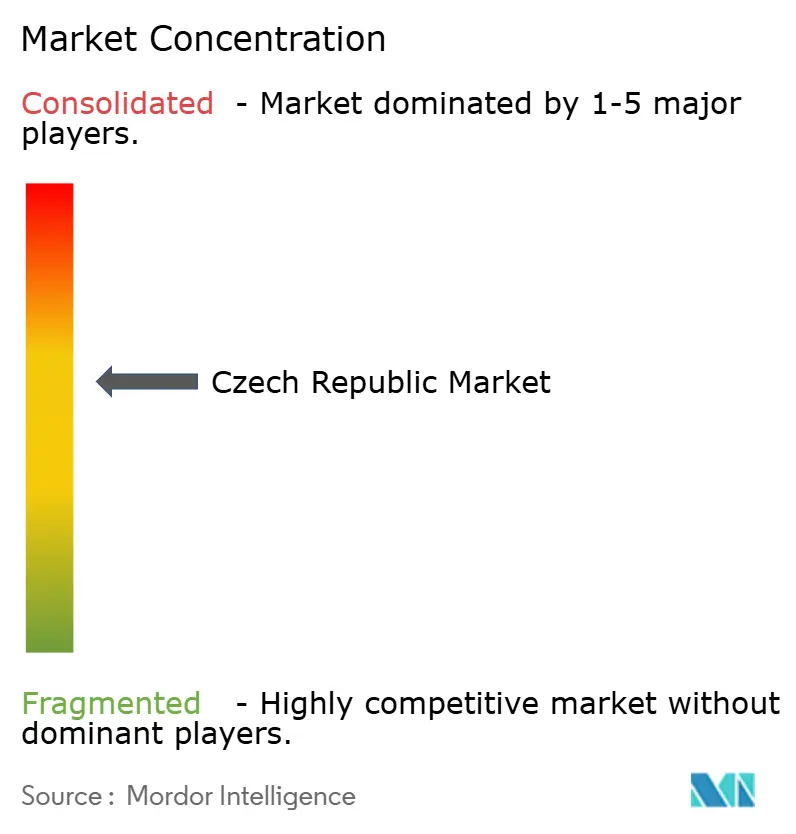

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Czech Republic E-commerce Market Analysis by Mordor Intelligence

The Czech Republic E-commerce Market size is expected to grow from USD 8.03 billion in 2025 to USD 8.42 billion in 2026 and is forecast to reach USD 10.7 billion by 2031 at 4.91% CAGR over 2026-2031. Broader 5G coverage, now available to 94.6% of households, is accelerating mobile-first shopping journeys that already account for 63% of online transactions.[1]5G Observatory, “5G Observatory Report June 2024,” 5gobservatory.eu EU Digital Single Market reforms continue lowering cross-border compliance friction, enabling Czech sellers to scale into Germany, Poland, and Slovakia with streamlined VAT processes.[2]European Commission, “VAT in the Digital Age Final Report,” taxation-customs.ec.europa.eu Same-day grocery services led by Rohlik Group have reset consumer expectations around fulfillment speed, prompting retailers across categories to invest in urban micro-fulfilment and automation. Meanwhile, the rapid take-up of Buy-Now-Pay-Later (BNPL) options is lifting average ticket sizes and broadening the addressable customer base, particularly in fashion and electronics.

Key Report Takeaways

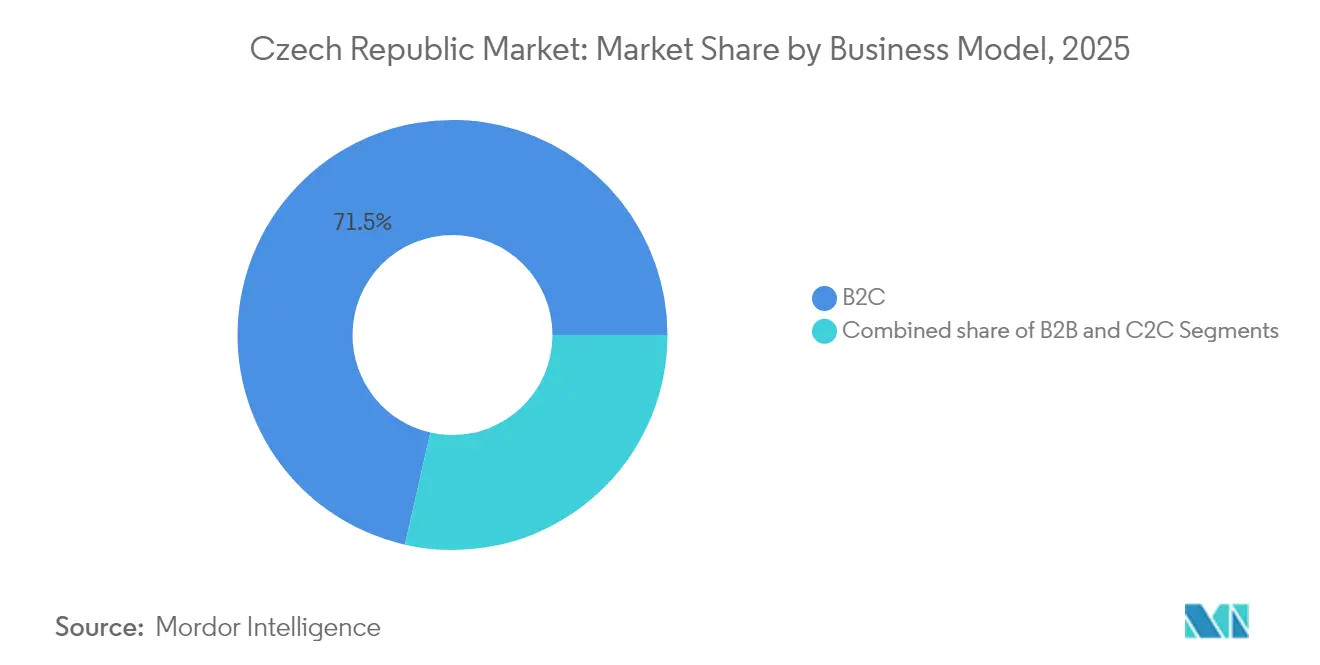

- By business model, B2C held 71.45% of the Czech Republic E-commerce Market share in 2025, while C2C is forecast to expand at a 6.21% CAGR through 2031.

- By device, smartphones commanded 62.35% share of the Czech Republic E-commerce Market size in 2025 and mobile commerce is projected to grow at 6.85% CAGR to 2031.

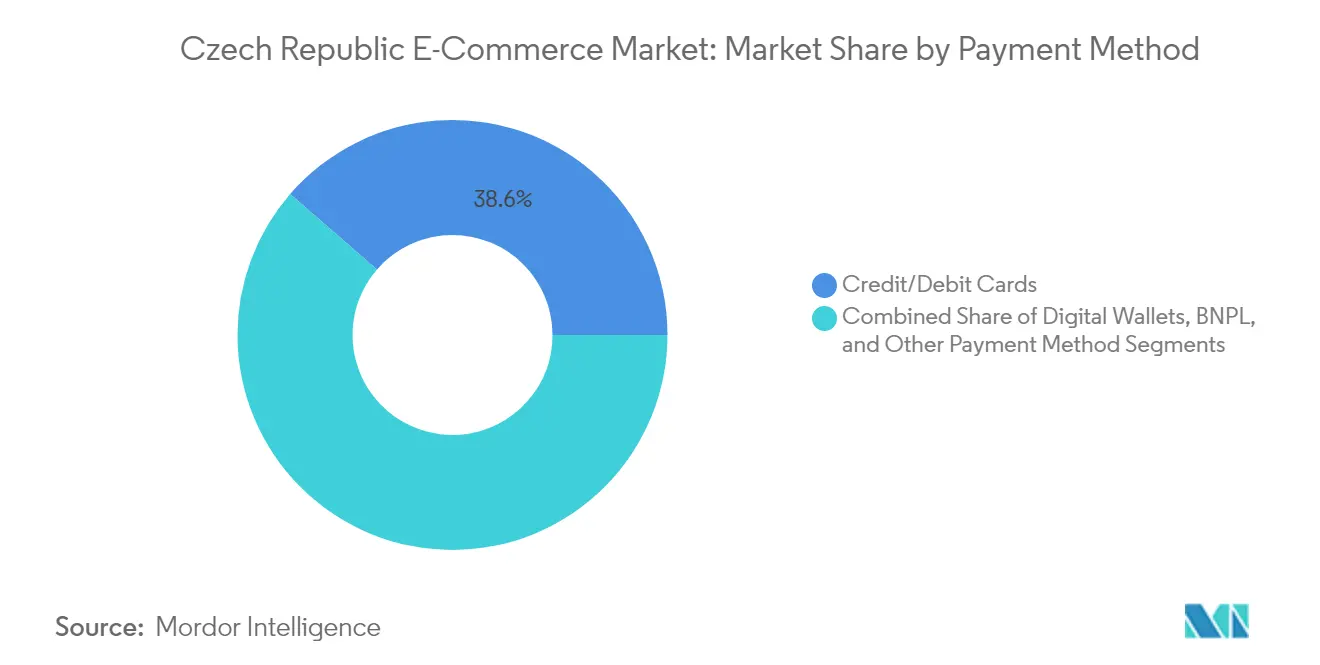

- By payment method, credit and debit cards retained 38.62% share, whereas BNPL transactions are advancing at an 8.1% CAGR to 2031.

- By B2C product category, consumer electronics led with 26.55% revenue share in 2025; food and beverages is forecast to expand at an 8.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Czech Republic E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Mobile Shopping Driven by 5G Roll-out and Smartphone Penetration in Prague-Brno Corridor | +1.2% | Prague-Brno corridor, expanding to secondary cities | Medium term (2-4 years) |

| EU Digital Single Market Reforms Simplifying Cross-Border CZ Logistics | +0.8% | National, with spillover to CEE region | Long term (≥ 4 years) |

| Expansion of Same-Day Grocery Delivery by Rohlik.cz & Hypermarkets | +1.0% | Urban centers, primarily Prague, Brno, Ostrava | Short term (≤ 2 years) |

| Rising Popularity of Sustainable-Goods Marketplaces Among Czech Millennials | +0.6% | National, concentrated in urban demographics | Medium term (2-4 years) |

| Buy-Now-Pay-Later Adoption Boosting Average Order Values | +0.9% | National, strongest in 25-34 age demographic | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Mobile Shopping Driven by 5G Roll-out and Smartphone Penetration in the Prague-Brno Corridor

Comprehensive 5G deployment, including full coverage of the Prague Metro, has enabled seamless high-bandwidth mobile experiences that now convert at higher rates than desktop sessions. Mobile transactions rose 40% year-over-year on Rohlik’s grocery platform during Q1 2025, highlighting the operational leverage generated by real-time inventory visibility and AI-assisted checkouts.[3]Retail Technology Innovation Hub, “Rohlik Group Global Expansion,” retailtechinnovationhub.com Improved latency has also facilitated richer augmented-reality (AR) product demos, driving engagement across fashion and home décor segments. As additional mid-sized cities complete 5G upgrades, retailers are expected to roll out location-aware promotions that enhance impulse purchases. The virtuous cycle of network expansion, app innovation, and consumer adoption is forecast to widen the smartphone share of the Czech Republic E-commerce Market beyond 70% by 2030.

EU Digital Single Market Reforms Simplifying Cross-Border Czech Logistics

The 2021 e-commerce package unified customs procedures and abolished geo-blocking, allowing Czech merchants to serve neighboring markets without establishing separate legal entities. Monthly VAT Control Statements standardize reporting, cutting administrative lead times and enabling near-real-time tax reconciliation. Allegro’s EUR 925 million (USD 998 million) acquisition of Mall Group leverages this harmonization to operate a single marketplace platform across CEE, lowering last-mile costs through shared fulfilment infrastructure. Simplified consumer-protection rules enhance trust in international transactions, further expanding the Czech Republic E-commerce Market addressable base. Over the long term, Czech sellers benefit from improved scale efficiencies while regional shoppers gain access to broader assortments at competitive prices.

Expansion of Same-Day Grocery Delivery by Rohlik.cz and Hypermarkets

Rohlik secured USD 170 million in growth capital from European development banks to roll out Brightpick robots that slash labour costs by 95%, enabling profitable same-day delivery in 13 cities. Fifteen-minute delivery windows have rapidly recalibrated customer expectations, prompting traditional hypermarkets to accelerate micro-fulfilment projects. The grocery model’s proven unit economics provide a template for adjacent categories, such as pharmacy and convenience items, to adopt automated fulfilment. Urban density gives Czech operators a strategic advantage in route optimization, supporting lower per-order delivery costs. As automation scales, grocery platforms are expected to exert deflationary pressure on shipping fees across the broader Czech Republic E-commerce Market.

Rising Popularity of Sustainable-Goods Marketplaces Among Czech Millennials

Millennial consumers exhibit strong environmental values, yet behavioural studies reveal a gap between stated intent and actual purchasing trade-offs. Marketplaces that simplify eco-label discovery and offer circular services, such as resale and refurbishment, are closing this convenience gap. EU proposals banning the destruction of unsold textiles further incentivise platforms to embed lifecycle tracking that reduces waste and improves margin recovery. Retailers are integrating carbon-score filters and sustainably sourced badges directly into search algorithms, nudging shoppers toward greener alternatives without adding decision friction. Niche sellers gain visibility through curated “responsible” storefronts, expanding category diversity. Over the medium term, sustainability credentials are expected to improve conversion rates and basket sizes within the Czech Republic E-commerce Market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Fashion-Vertical Return Rates Elevating Reverse-Logistics Cost | -0.7% | National, concentrated in urban fulfillment centers | Medium term (2-4 years) |

| Urban Fulfilment-Centre Labour Shortages Raising Wage Bills | -0.5% | Prague, Brno, Ostrava metropolitan areas | Short term (≤ 2 years) |

| Post-2021 VAT Harmonisation Increasing SME Compliance Spend | -0.3% | National, disproportionately affecting SMEs | Long term (≥ 4 years) |

| Intensified Price Pressure from Amazon.de & Other EU Platforms | -0.4% | National, strongest in electronics and fashion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Fashion-Vertical Return Rates Elevating Reverse-Logistics Cost

Return ratios of 20% for clothing and up to 37% for footwear compress margins through higher inspection, repackaging, and reshipping expenses. Studies reveal 22-44% of returns never reach secondary consumers, amplifying carbon emissions relative to items that complete resale cycles. Czech platforms invest in virtual try-on tools and AI size recommendations, yet consumer uncertainty persists. Proposed EU rules prohibiting destruction of unsold stock obligate retailers to establish secondary-market channels or donation programmes, adding 15-25% to processing costs. Smaller brands face working-capital strain as inventories linger longer in reverse-logistics loops, retarding growth in the Czech Republic E-commerce Market.

Urban Fulfilment-Centre Labour Shortages Raising Wage Bills

Unemployment at 2.7% and record inflows of foreign workers still leave fulfilment centres understaffed, with average gross monthly wages reaching CZK 45,854 (USD 1,834), up 6.5% year-over-year. Robotics investments offset shortages, yet high capex and scarce automation skills delay deployments for mid-tier merchants. Competition from manufacturing and parcel carriers intensifies wage pressure, especially during seasonal peaks. Rising operating costs are passed through via delivery surcharges, potentially dampening conversion rates. Although marquee players like Rohlik achieve 95% labour savings through Brightpick robots, supply-chain digitisation gaps among smaller operators constrain productivity gains across the Czech Republic E-commerce Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2C Dominance Drives Platform Innovation

B2C transactions generated 71.45% of the Czech Republic E-commerce Market size in 2025, confirming the segment’s structural primacy in consumer engagement and logistics sophistication. Marketplace architecture enables merchants to leverage national fulfilment networks that promise next-day or same-day delivery in major urban clusters. Payment orchestration, loyalty programmes, and AI-driven recommendation engines keep customer lifetime value high, motivating sustained investment in proprietary technology stacks. C2C commerce, growing at 6.21% CAGR, benefits from social-commerce features and integrated payment-escrow protections that mitigate traditional peer-to-peer trust barriers. Family-owned SMEs expanding into B2B digital procurement signal incremental diversification, although integration complexity moderates adoption.

B2C platforms are also incubating niche verticals such as refurbished electronics and circular fashion to capture environmentally conscious shoppers. Allegro’s integration of Mall Group’s CEE assets scales cross-border catalogue breadth and shared warehousing, improving price transparency and search relevance. Meanwhile, the Czech Republic e-commerce industry increasingly tests hybrid direct-to-consumer plus marketplace listings, allowing brands to balance control over brand equity with the traffic scale of large platforms. These blended channel strategies are expected to sustain B2C’s lead through 2031, even as C2C broadens category assortment.

By Device Type: Mobile Commerce Transformation Accelerates

Smartphones captured 62.35% of transactions and are forecast to increase share as 5G ubiquity pushes load times below one second on leading apps. Retailers redesign user interfaces around vertical video, swipe gestures, and biometric authentication, making the checkout journey faster than desktop flows. Social networks that integrate native storefronts fuel discovery commerce, especially among Gen Z cohorts spending three hours daily on mobile. Voice search and AI chat interfaces are emerging within grocer apps, enabling frictionless re-ordering of staples.

Desktop remains the preferred screen for high-consideration purchases such as premium electronics bundles, yet its overall share continues to decline. Smart-TV commerce and in-car infotainment shopping pilots are early-stage but showcase the ambient-commerce direction of the Czech Republic E-commerce Market. Developers balance innovation with accessibility, ensuring progressive web apps work on lower-spec smartphones common outside major cities. As device-agnostic personalisation algorithms mature, seamless hand-off between screens will further entrench mobile’s central role.

By Payment Method: BNPL Disruption Reshapes Transaction Dynamics

Credit and debit cards maintained 38.62% share of the Czech Republic E-commerce Market size in 2025, underpinned by universal POS acceptance and entrenched consumer familiarity. BNPL services, however, outpaced every other payment type, with 8.1% CAGR as flexible instalments resonated with younger shoppers seeking budget management tools. Retailers integrating BNPL at the product page observe uplift in conversion and lower cart abandonment relative to post-checkout financing offers.

Digital wallets benefit from tokenisation and biometric verification that reduce fraud, yet market fragmentation limits scale compared with a unified BNPL narrative. Czech banking incumbents experiment with in-app credit lines to defend share against fintech newcomers. Cross-border merchants view BNPL as a bridge into Central Europe’s under-served credit segments, bolstering sales without credit-card interchange. Regulatory scrutiny around consumer indebtedness is expected to formalise transparency standards, but the underlying demand for frictionless credit remains a secular growth driver across the Czech Republic E-commerce Market.

By B2C Product Category: Electronics Leadership Faces Grocery Disruption

Consumer electronics retained 26.55% of revenue in 2025, supported by stable unit demand for smartphones, gaming consoles, and smart-home devices. Competitive pricing from pan-European distributors and frequent upgrade cycles sustain volume, yet category margins narrow as marketplace competition intensifies. Food and beverages, growing at 8.55% CAGR, threaten to eclipse electronics by 2031 as automated fulfilment compresses delivery lead times to minutes.

Rohlik’s EUR 700 million (USD 756 million) revenue in 2023 underscores the scalability of the grocery model. Electronics sellers respond with premium extended-warranty bundles and trade-in programmes to preserve basket value. Fashion and furniture segments exploit AR visualisation to reduce return risk, but fashion profitability remains constrained by reverse-logistics overheads. The Czech Republic E-commerce Market continues diversifying as niche categories such as pet care and hobby craft record double-digit growth from a smaller base.

Geography Analysis

The Czech Republic punches above its weight in the Central and Eastern European digital economy, capturing a significant portion of the region’s EUR 39 billion (USD 42.1 billion) online sales in 2024, which are set to rise to EUR 60 billion (USD 64.8 billion) by 2029. The Prague-Brno corridor concentrates population density, disposable income, and 5G bandwidth, enabling same-day delivery coverage that outperforms regional peers. E-commerce penetration is projected to reach 15.5% of total retail by 2029, narrowing the gap with Western European benchmarks.

Cross-border commerce already represents 35.6% of Czech online orders, dominated by flows into Germany, Poland, and Slovakia. Harmonised VAT reporting and abolition of geo-blocking reduce friction, while logistics corridors through D5 and D11 motorways shorten transit times. Secondary cities such as Ostrava, Plzeň, and České Budějovice attract investment in satellite fulfilment hubs designed to decentralise inventory and cut last-mile costs. Regional governments offer tax incentives for automation projects that generate skilled employment, reinforcing the Czech Republic E-commerce Market competitiveness.

The nation ranks 30th in the Global Innovation Index, with a top-20 position in knowledge and technology outputs, demonstrating robust R&D capability that supports e-commerce platform innovation. As EU structural funds target digital-skills programmes, labour-market depth should improve outside Prague, alleviating fulfilment staffing bottlenecks. Continued collaboration with German parcel integrators positions Czech hubs as distribution springboards into South-East Europe. Overall, geographic advantages and supportive policy frameworks sustain a growth premium over the broader EU, anchoring the Czech Republic E-commerce Market as a regional bellwether.

Competitive Landscape

Domestic champions such as Alza.cz, Mall.cz, and Rohlik Group leverage home-market intimacy and advanced logistics to protect share against global entrants. Brightpick robotics in Rohlik warehouses deliver a 95% labour reduction, creating a structural cost advantage and facilitating 15-minute delivery promises in Prague and Brno. Allegro’s acquisition of Mall Group responds with scale economics across CEE, pooling seller onboarding, advertising technology, and fulfilment capacity. Amazon’s cross-border proposition, bolstered by the 2024 partnership with Rohlik in Germany, expands assortment reach for Czech shoppers without the fixed cost of local warehousing.

Fintech innovators Twisto and Lemonero differentiate through AI-driven credit decisioning and embedded checkout experiences that raise merchant conversion rates. Competitive intensity accelerates platform investment into edge computing, predictive demand planning, and carbon-footprint dashboards, which serve as new axes of differentiation. Patent filings in warehouse automation and last-mile routing suggest rising barriers to entry for pure-play storefronts lacking operational depth.

Moderate concentration leaves room for vertical specialists, particularly in luxury cosmetics, sports nutrition, and DIY hardware, where curated assortment and community engagement trump scale. However, rising marketing-cost inflation on social networks forces niche players to consider partnerships with larger marketplaces for traffic acquisition. Strategic alliances around white-label fulfilment and shared dark-store networks are likely as suppliers seek omnichannel resilience. Overall, the Czech Republic E-commerce Market exhibits disciplined rivalry that spurs technology adoption without tipping into destructive price wars.

Czech Republic E-commerce Industry Leaders

Alza.cz

Mall.cz

Aukro SRO

Notino s.r.o.

Rohlik Group a.s.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Rohlik Group announced EUR 700 million (USD 756 million) in 2023 sales and targeted EUR 1 billion (USD 1.08 billion) for 2024, signalling confidence in its automated fulfilment model. Management’s strategy aligns scale economics with a path to cash-positive operations by 2025, reinforcing investor faith in grocer-led disruption.

- November 2024: Rohlik Group formalised a partnership with Amazon.de to integrate Czech automated grocery fulfilment into Amazon Prime Germany, using alliance synergies to broaden SKU reach and monetise excess capacity during off-peak slots.

- June 2024: Rohlik Group secured USD 170 million from the EBRD and EIB to fund robotic expansion into 10+ new cities, underscoring institutional support for automation as a lever to penetrate untapped urban centres.

- June 2024: O2 Czechia completed 618 5G base-station upgrades in North Moravia and delivered full 5G coverage across Prague Metro, a first in Europe, enabling seamless underground mobile commerce and strengthening telco differentiation.

Czech Republic E-commerce Market Report Scope

An e-commerce marketplace is a place or website where customers can look at goods from many different sellers, shops, or even individuals.The third-party providers are in charge of manufacturing and delivery, and the marketplace owner is in charge of customer acquisition and payment processing. B2B and B2C e-commerce are separate segments of the Czech Republic's e-commerce market. The market under study is further broken down into consumer electronics, fashion and clothing, food and beverage, and furniture and home by B2C e-commerce.

The Czech Republic E-commerce Market is segmented by B2C eCommerce (Beauty and Personal Care, Consumer Electronics, Fashion and Apparel, Food and Beverage, Furniture and Home), and B2B eCommerce.

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Business Model

| B2C |

| B2B |

| C2C |

By Device Type

| Smartphone / Mobile |

| Desktop and Laptop |

| Other Device Types |

By Payment Method

| Credit / Debit Cards |

| Digital Wallets |

| BNPL |

| Other Payment Method |

By B2C Product Category

| Beauty and Personal Care |

| Consumer Electronics |

| Fashion and Apparel |

| Food and Beverages |

| Furniture and Home |

| Toys, DIY and Media |

| Other Product Categories |

| By Business Model | B2C |

| B2B | |

| C2C | |

| By Device Type | Smartphone / Mobile |

| Desktop and Laptop | |

| Other Device Types | |

| By Payment Method | Credit / Debit Cards |

| Digital Wallets | |

| BNPL | |

| Other Payment Method | |

| By B2C Product Category | Beauty and Personal Care |

| Consumer Electronics | |

| Fashion and Apparel | |

| Food and Beverages | |

| Furniture and Home | |

| Toys, DIY and Media | |

| Other Product Categories |

Key Questions Answered in the Report

What is the current size of the Czech Republic E-commerce Market?

The Czech Republic E-commerce Market reached USD 8.42 billion in 2026 and is projected to grow to USD 10.7 billion by 2031 at a 4.91% CAGR.

Which segment holds the largest share in the Czech Republic E-commerce Market?

B2C platforms hold the largest share, accounting for 71.45% of transactions in 2025, driven by extensive product assortments and fast fulfilment.

How fast is mobile commerce growing in the Czech Republic?

Mobile commerce represents 62.35% of transactions and is forecast to grow at a 6.85% CAGR through 2031 as 5G coverage reaches national scale.

What role does BNPL play in Czech online shopping?

BNPL already captures 5% of online sales and is expanding at 8.1% CAGR, increasing average basket sizes by up to 35% for fashion and electronics.

Which product category is expanding the fastest?

Food and beverages lead growth with an 8.55% CAGR, propelled by automated grocery fulfilment and 15-minute delivery windows in major cities.

How concentrated is the Czech Republic E-commerce Market?

The market is moderately concentrated with a score of 6, indicating that the top five players hold around 60% share, leaving room for niche and regional specialists to scale.

Page last updated on: