Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

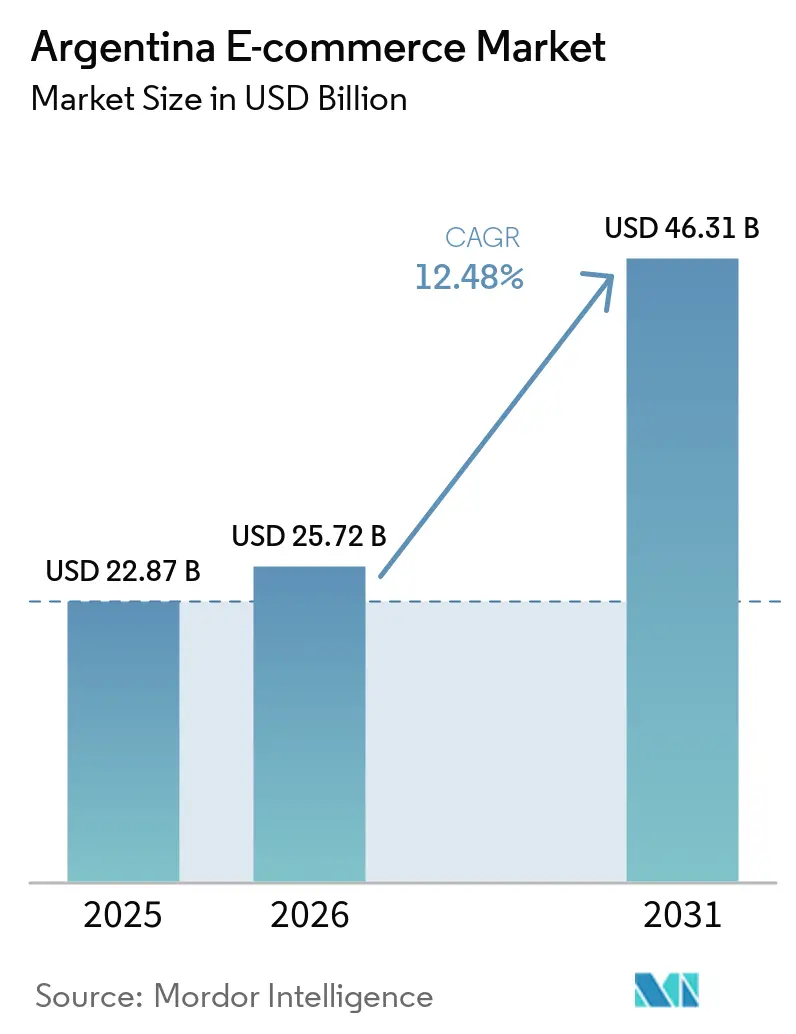

| Base Year Market Size (2025) | USD 22.87 Billion |

| Market Size (2026) | USD 25.72 Billion |

| Market Size (2031) | USD 46.31 Billion |

| Growth Rate (2026 - 2031) | 12.48% CAGR |

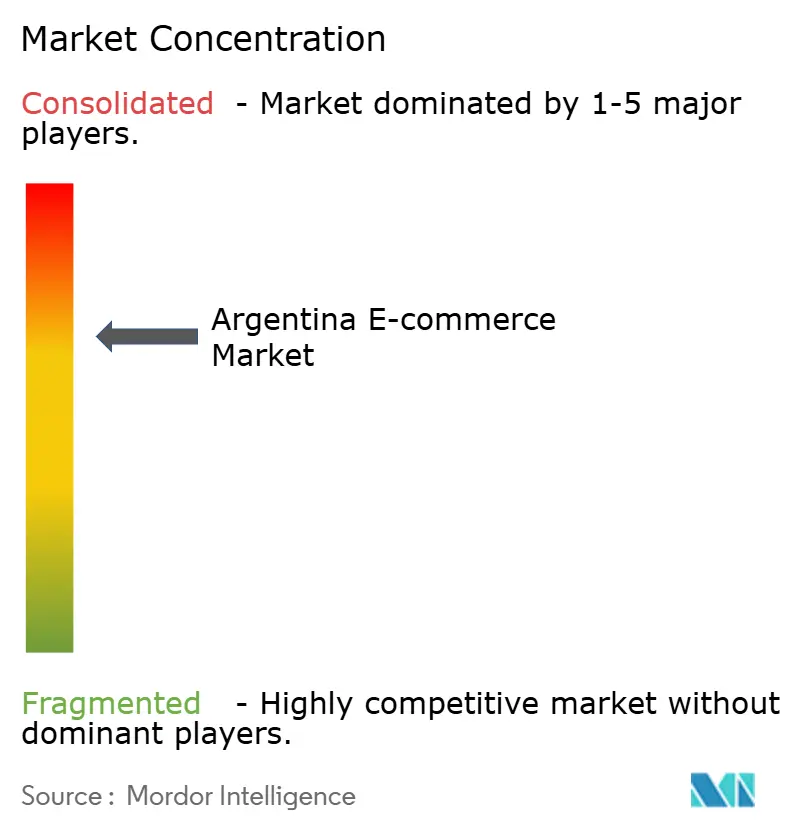

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Argentina E-commerce Market Analysis by Mordor Intelligence

The Argentina e-commerce market size is expected to grow from USD 22.87 billion in 2025 to USD 25.72 billion in 2026 and is forecast to reach USD 46.31 billion by 2031 at 12.48% CAGR over 2026-2031. The Milei administration’s removal of capital controls and higher courier limits is lowering cross-border friction and widening product choice. Mobile shopping already accounts for two-thirds of transactions, and same-day delivery coverage in Buenos Aires and Córdoba now reaches 75% of orders, sharply lifting conversion rates.[1]MercadoLibre Investor Relations, “2025 Global Emerging Markets Presentation,” investor.mercadolibre.com Digital wallets are bringing formerly cash-reliant shoppers online, while “cuotas” installment plans are raising average basket values by more than one-third. Logistics investment is moving beyond the capital to secondary cities, yet poor road quality in the north and northeast still inflates reverse-logistics costs. Competitive intensity is climbing as Amazon, Rappi and TikTok Shop scale local operations, but Mercado Libre’s integrated commerce-payments-logistics flywheel continues to anchor the Argentina e-commerce market.

Key Report Takeaways

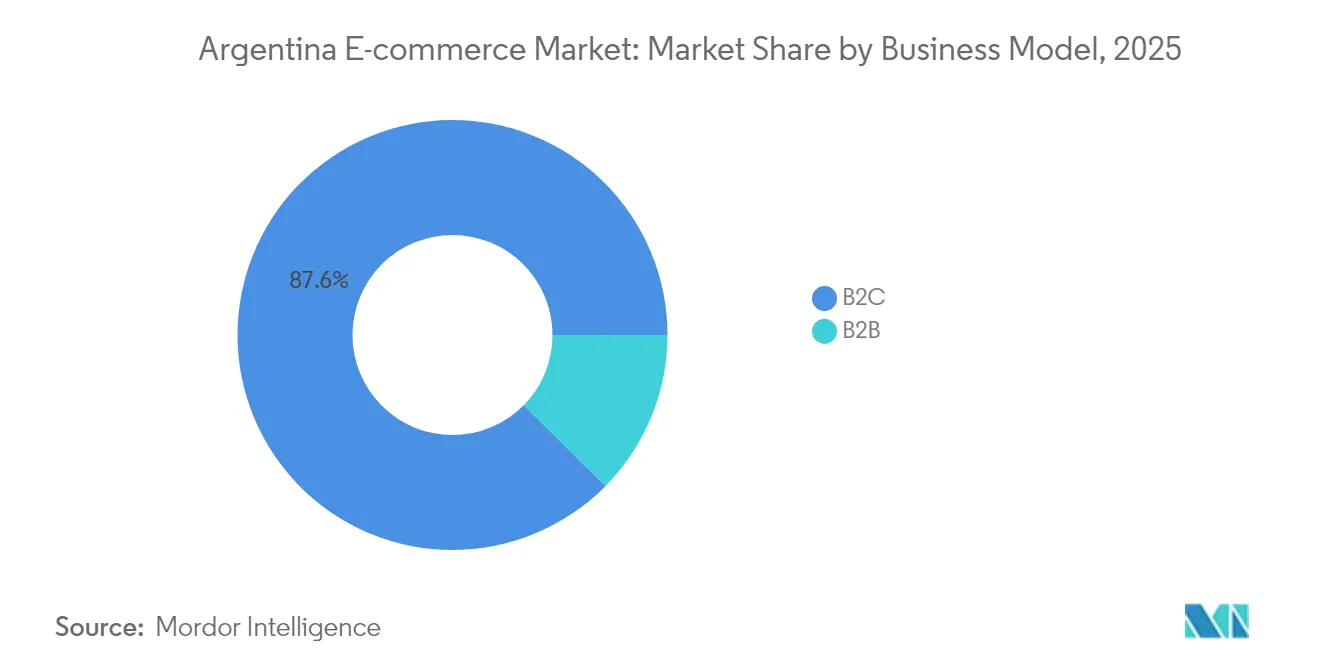

- By business model, the B2C segment led with 87.62% of Argentina e-commerce market share in 2025; B2B is set to grow fastest at a 15.6% CAGR through 2031.

- By device, smartphones captured 67.35% of the Argentina e-commerce market size in 2025, while mobile transactions are expanding at 15.2% CAGR.

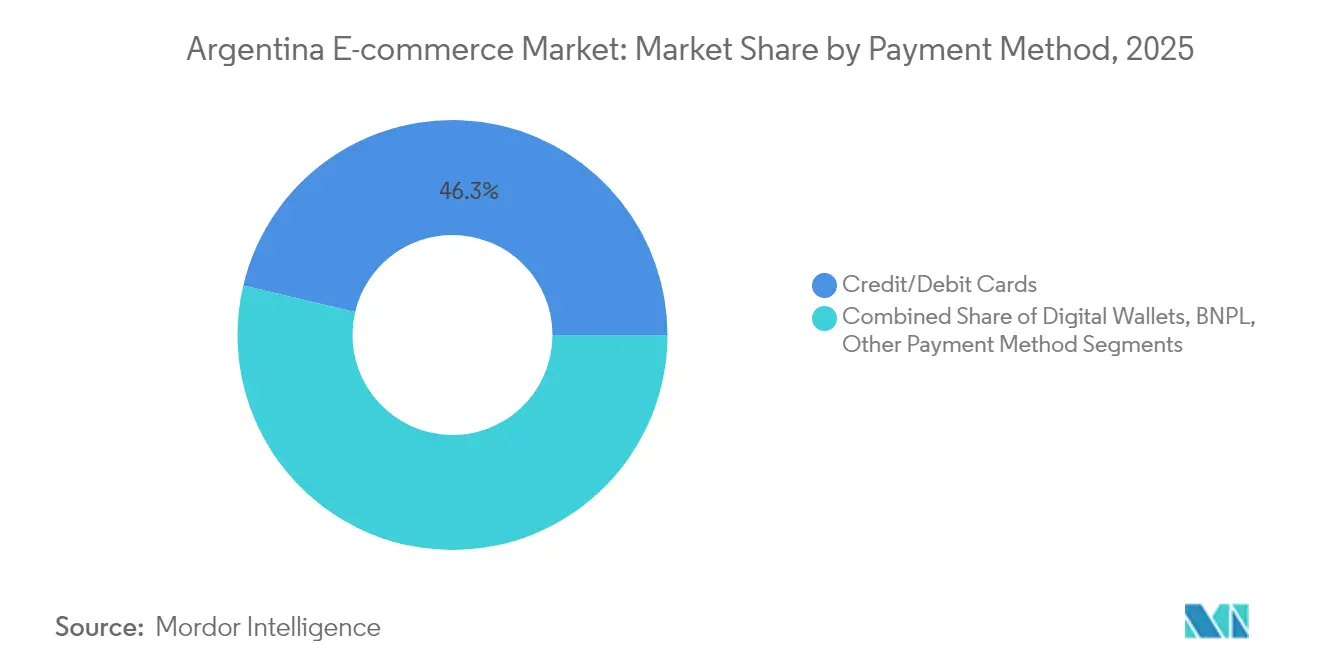

- By payment method, cards retained 46.30% share of the Argentina e-commerce market size in 2025 whereas digital wallets are advancing at 21.6% CAGR to 2031.

- By B2C product category, consumer electronics held 29.62% of Argentina e-commerce market share in 2025; food and beverages is poised for the highest 17.6% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina E-commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Peso Devaluation-Driven Bargain-Hunting From Overseas Consumers | +3.5% | Global, with significant inflows from North America, Europe, and neighboring Latin American countries | Short term (≤ 2 years) |

| Fintech "Cuotas" Installment Plans Expanding Average Basket Values | +2.8% | National, with highest adoption in Buenos Aires, Córdoba, and Rosario | Medium term (2-4 years) |

| Same-Day Delivery Networks in Buenos Aires & Córdoba Enhancing Reliability | +1.9% | Urban centers (Buenos Aires Metropolitan Area, Córdoba, Rosario, Mendoza) | Medium term (2-4 years) |

| Micro-Import Duty Exemptions (< USD 50) Fueling Cross-Border Orders | +1.2% | National, with higher impact in border regions and major cities | Short term (≤ 2 years) |

| Instagram-Led Social Commerce Surge Among 18-34 Urban Shoppers | +0.9% | Urban centers, primarily Buenos Aires, Córdoba, and Mendoza | Medium term (2-4 years) |

| Live-Shopping Streams Offsetting High Brick-and-Mortar Rents | +0.7% | Major urban centers, primarily Buenos Aires | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Peso Devaluation Bargain-Hunting From Overseas Consumers

A 54% peso adjustment in December 2023 positioned Argentine goods as global bargains, triggering a spike in foreign orders for electronics, footwear and digital services. The April 2025 lifting of most capital controls simplified currency settlement and invited a new cohort of international sellers to the Argentina e-commerce market. Narrower gaps between official and parallel exchange rates are reducing FX risk, and cross-border volumes through courier channels doubled in Q1 2025. Although currency effects gradually normalize, the short-term lift contributes the single-largest driver to forecast growth.

Fintech “Cuotas” Installment Plans Expanding Average Basket Values

The national appetite for deferred payments has deep roots, but platform-level integration of 3- to 12-month “cuotas” plans now embeds financing directly at checkout. Merchants report 35-45% higher ticket sizes and materially lower cart abandonment. Mercado Pago, MODO and bank wallets route real-time approval decisions, while BNPL specialists extend credit to thin-file consumers. Rising adoption beyond Buenos Aires is expected to support medium-term growth as economic stabilization eases default risk and speeds regulatory clearance for new credit products.

Same-Day Delivery Networks in Buenos Aires & Córdoba Enhancing Reliability

Investment in urban micro-hubs and AI-driven fleet routing lifted the on-time delivery rate from 30% in 2023 to 75% in 2025. The improvement tackles a long-standing trust gap that once discouraged high-frequency digital grocery orders. Logistics providers now pitch guaranteed 24-hour coverage for 80% of AMBA SKUs, and funding rounds for last-mile start-ups are aimed at scaling similar service levels in Mendoza and Rosario.

Micro-Import Duty Exemptions Fueling Cross-Border Orders

The Puerta a Puerta framework allows 12 tax-free imports annually for parcels up to USD 50 and now waives duties on shipments valued to USD 400. Relaxed weight limits and faster customs release streamline delivery by private couriers and have stimulated a surge in low-value fashion, cosmetics and hobby products entering the country. The regulatory incentive is front-loaded, hence the driver’s short duration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Logistics Bottlenecks Beyond AMBA Elevating Reverse-Logistics Cost | -1.8% | Provincial regions, particularly Northwest and Northeast Argentina | Medium term (2-4 years) |

| Inflation-Indexed Price Volatility Hindering Inventory Hedging | -1.2% | National | Short term (≤ 2 years) |

| Low Int'l Card Approval Rates Triggering Cart Abandonment | -1.0% | National, with higher impact on cross-border transactions | Medium term (2-4 years) |

| Escalating Account-Takeover Fraud Undermining Trust | -0.8% | National, with concentration in major urban centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Logistics Bottlenecks Beyond AMBA Elevating Reverse-Logistics Cost

Forty-six percent of national roads rate as poor, causing delivery windows in Tucumán or Salta to extend well past the 48-hour benchmark reached in the capital. Higher return freight for fashion and footwear erodes margins by up to 20%.[2]Cabify, “Logistics Service for Businesses,” cabify.com Providers like Cabify Logistics are widening depot networks, yet meaningful cost parity with AMBA hinges on multiyear public infrastructure upgrades.

Inflation-Indexed Price Volatility Hindering Inventory Hedging

Although monthly CPI cooled to 2.7% at end-2024, historical memory of triple-digit inflation still shapes supplier contracts and consumer expectations. Retailers routinely adjust online‐list prices several times a month, complicating automated repricing tools and creating mismatches between reservations and settlement. Flash-sale tactics clear exposure, yet limit assortment depth until monetary stability fully restores planning confidence.[3]Administración Federal de Ingresos Públicos, “Puerta a Puerta – Envíos Internacionales,” afip.gob.ar

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Business Model: B2B Digitalization Fuels Next-Wave Growth

The B2C segment controlled 87.62% of the Argentina e-commerce market in 2025, anchored by marketplace leaders and high consumer internet penetration. In contrast, B2B turnover is projected to climb at 15.6% CAGR, pushing its slice of Argentina e-commerce market size from single digits toward a material share by 2031. Mandatory e-invoicing and VAT transparency rules that took effect in 2025 are nudging procurement online, while SMEs adopt digitally integrated sourcing portals that compress lead times and lower administrative overhead.

Platform providers are adding credit terms, bulk pricing and ERP connectors tailored for distributors and manufacturers. Mercado Libre Business and Tiendanube Empresas target Argentina e-commerce industry buyers with catalog management tools and Argentina payments financing that extends up to 90-day payment windows. Government promotion of supply-chain digitization under the MiPyME initiative further underpins adoption across the country’s 1.1 million small firms.

By Device Type: Mobile Commerce Becomes the Default Path-to-Purchase

Mobile accounted for 67.35% of sales in 2025 and is advancing 15.2% CAGR, widening its lead within the Argentina e-commerce market. Young shoppers complete entire journeys—discovery, comparison, payment—on low-bandwidth progressive web apps optimized for prepaid data plans. Biometric log-in elevates perceived security and shaves checkout friction.

Desktop remains relevant in higher-ticket B2B carts where buyers download spec sheets and compare financing options. Yet share migration is clear: super-app ecosystems bundle rides, food delivery and retail into unified interfaces, further embedding shopping into daily mobile routines. This structural tilt supports a rising mobile component of Argentina e-commerce market size across the forecast horizon.

By Payment Method: Digital Wallets Drive Inclusion and Ticket Upsell

Cards still processed 46.30% of online payments in 2025, yet wallet penetration is climbing on a 21.6% CAGR path. Wallets knit together savings, credit and QR functionality, allowing unbanked users to bypass legacy rails. The resulting transaction certainty and instant settlement appeal to merchants who previously hesitated to serve cash customers online.

The Argentina e-commerce market benefits as BNPL micro-loans extend affordability, with average order values jumping where two- and three-installment buttons surface at checkout. Interoperable QR standards mandated by the central bank reduce technical barriers and encourage wider wallet acceptance, accelerating wallet share at the expense of cards and cash-on-delivery.

By B2C Product Category: Electronics Lead, Food Outpaces

Consumer electronics held 29.62% of Argentina e-commerce market share in 2025, reflecting clear specifications and defensible pricing. Electronics merchants leverage “cuotas” financing and free returns to keep handset, laptop and console turnover brisk, buffering volume even during inflation spikes.

Food and beverages post the fastest 17.6% CAGR, driven by quick-commerce models that promise sub-30-minute delivery from dark stores. Cold-chain expansion and real-time stock visibility overcome historical perishability hurdles. Apparel and footwear ride lower import tariffs announced in March 2025, while beauty brands harness influencer tutorials to push sampling kits via social checkout, deepening category diversification within overall Argentina e-commerce market size.

Geography Analysis

Buenos Aires Metropolitan Area anchors the Argentina e-commerce market, enjoying 15-20% higher penetration than the national average. Seventy-five percent of AMBA parcels now arrive within 48 hours, supported by dense micro-fulfillment nodes and bike-courier fleets. Elevated digital literacy and broad wallet adoption further push spend per user above other regions.

Córdoba, Rosario and Mendoza form a second growth corridor as logistics corridors radiate outward. Córdoba’s central location attracts bulk-goods consolidation hubs, shrinking delivery times to adjacent provinces. Local start-ups tailor storefront templates and payment workflows for regional brands, bolstering merchant onboarding. Nonetheless, shipments to Northwest provinces still stretch five to seven days due to under-maintained highways, capping conversion rates despite rising mobile connectivity.

Regional integration within Southern Cone trade lanes intensifies cross-border flows with Chile and Uruguay. Liberalized courier limits plus tariff exemptions on USD 400 orders enhance Argentina’s standing relative to Brazil and Mexico, making the Argentina e-commerce market a preferred landing zone for new Latin American roll-outs. Participation in WTO digital-trade discussions signals alignment with global norms and may unlock smoother data flows for payment authentication and fraud analytics.

Competitive Landscape

Mercado Libre commands roughly 62% of marketplace GMV, sustained by its in-house payments, credit and logistics stack that loops customer data into personalized recommendations. Q1 2025 GMV in Argentina rose 126% year-over-year, highlighting momentum unmatched in its other geographies.

Amazon’s entry with Prime Next-Day pilot services in select AMBA zip codes signals intensifying rivalry. Frávega and Carrefour accelerate omnichannel upgrades, linking in-store inventories with online catalogs to defend share. Vertical specialists like Compragamer (electronics) and Tiendamia (cross-border curated goods) differentiate on depth and sourcing agility. Logistics capability remains the key battleground: firms race to open city-edge sortation centers and adopt AI route optimization to trim last-mile cost per parcel.

Investor interest is broadening. Moova’s USD 5 million Series A will scale sustainable urban delivery to Córdoba and Rosario, while Cabify Logistics extends carbon-neutral fleets to five new cities. Payment enablers add instalment APIs to court merchants chasing higher average order values. As regulatory barriers fall, fresh entrants from Colombia and Peru probe niches such as refurbished devices and luxury resale, adding layers of competition across the Argentina e-commerce market.

Argentina E-commerce Industry Leaders

-

Grupo Carrefour Argentina S.A.

-

Frávega S.A.C.I. e I.

-

Musimundo S.A.

-

Adidas Argentina

-

Easy.com

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Argentina secured a USD 20 billion IMF loan and lifted most currency controls, improving the investment climate for foreign e-commerce entities.

- February 2025: TikTok Shop confirmed Latin American expansion, introducing integrated short-video commerce.

- February 2025: Cabify Logistics expanded e-commerce fleets to Rosario, Mendoza, Mar del Plata and Córdoba.

- January 2025: ARCA rolled out simplified courier rules allowing goods up to 50 kg and USD 3,000, with tariff exemptions for shipments up to USD 400.

Argentina E-commerce Market Report Scope

E-commerce is the purchasing and selling of products and services over the Internet. It is conducted over computers, mobiles, tablets, and other smart devices. There are primarily two types of e-commerce, including Business-to-Consumer (B2C) and Business-to-Business (B2B).

The Argentina E-commerce Market is segmented into B2C E-Commerce (Beauty and Personal Care, Consumer Electronics, Fashion and Apparel, Food and Beverage, Furniture and Home), and B2B E-Commerce.

By Business Model

| B2C |

| B2B |

By Device Type

| Smartphone / Mobile |

| Desktop and Laptop |

| Other Device Types |

By Payment Method

| Credit / Debit Cards |

| Digital Wallets |

| BNPL |

| Other Payment Method |

By B2C Product Category

| Beauty and Personal Care |

| Consumer Electronics |

| Fashion and Apparel |

| Food and Beverages |

| Furniture and Home |

| Toys, DIY and Media |

| Other Product Categories |

| By Business Model | B2C |

| B2B | |

| By Device Type | Smartphone / Mobile |

| Desktop and Laptop | |

| Other Device Types | |

| By Payment Method | Credit / Debit Cards |

| Digital Wallets | |

| BNPL | |

| Other Payment Method | |

| By B2C Product Category | Beauty and Personal Care |

| Consumer Electronics | |

| Fashion and Apparel | |

| Food and Beverages | |

| Furniture and Home | |

| Toys, DIY and Media | |

| Other Product Categories |

Key Questions Answered in the Report

What is the current size of the Argentina e-commerce market?

The market is valued at USD 25.72 billion in 2026 and is forecast to grow to USD 46.31 billion by 2031 at a 12.48% CAGR.

Which business model is growing fastest?

B2B digital commerce is projected to outpace the wider market with a 15.6% CAGR through 2031 as electronic invoicing and VAT rules move procurement online.

How dominant is mobile shopping?

Smartphones generate 67.35% of online transactions today and exhibit the strongest 15.2% CAGR, driven by wallet adoption and super-app ecosystems.

Who leads the competitive landscape?

Mercado Libre holds roughly 62% of marketplace GMV, supported by its integrated payments and logistics network; Amazon, Frávega and Carrefour follow at a distance.

What regulation most recently boosted cross-border sales?

January 2025 courier reforms raised the import cap to USD 3,000 and waived duties on shipments below USD 400, doubling courier volumes in Q1 2025.

Which product category is expanding the quickest?

Food and beverages show the highest 17.6% CAGR due to quick-commerce models and improved cold-chain logistics, even as electronics retain the largest revenue share.

Page last updated on: